edition of april 15, 2013 financial tips for weathering the furlough: your lifeboat drill a...

TRANSCRIPT

Edition of April 15, 2013

Financial Tips for Weathering the Furlough:Your Lifeboat Drill

a presentation from Army Community Service (ACS) of

USAG Rock Island Arsenal

“Uncle Jon” Cook• Survivor Outreach Services – Financial Counselor

• Financial Readiness Program

• Personal Financial Management (PFM) Specialist

• Accredited Financial Counselor (AFC)

• Army Emergency Relief (AER)

• Notary Public

• Employment Readiness Program

• Military Spouse Employment Program (MSEP)

• (Former) Professional in Human Resources (PHR) & (Former) Certified Workforce Development Professional (CWDP)

(309) 782 - 0815 1 – 877 – 882 – 0523

jon.c.cook.civ @ mail. mil

www. riamwr. com / acs /

Personal Financial Management

a Call to ActionCan your current savings carry you through the furlough and reduced

pay?

Can you cut enough expenses to stay within the budget?

Through end of September? (through ____?)• Actions you, your family and your co-workers may take now to prepare.• Commit to short and long term goals.• Resources available to meet your goals.

www. military saves. org

Ready Army is the Army’s proactive campaign to increase the resilience of the Army community and enhance the readiness of the force …

http://readyarmy.ria.army.mil

Sequence of the Presentation

• Lifeboat Drill Concept• Working the Numbers• Follow-up Actions• Personal Financial Management (PFM) Web Sites, plus References and Resources• Financial Tips for “Weathering the Furlough”• A Call to Action

Please do ask questions as we go through the session.

This presentation is designed to give you quite a few “Scooby Doo” moments!

Mother and Daughter Team:

Elizabeth Warren(now Senator Warren)

Amelia Warren Tyagi

Lifeboat Drill:

• In an emergency …

• Supplies (savings and assets)

• What fits “in the boat”?

Stupid Question – but play along:

How many sides does a circle have?

TWO!Inside & Outside

Your Income Circle:What is Spendable?

What is your Take-home Pay?

All of your expenses have to

fitinside the circle!

Why plan for savings now? Savings is way off in my future!

“It’s not the money you make; it’s the money you get to keep!” Ric Edelmann

The Three Types of Money:$ Past = debt $ Present = daily living expenses

$ Future = non-routine expenses & emergencies

Personal Financial Management Web $ites

www.riamwr.com/acs/financial-readiness

4b. Excel Spreadsheet in weekly bands for

persons paid bi-weekly

7. Excel Spreadsheet for figuring out

“how far your money will go?”

Lifeboat Drill: what expenses will fit within your take-home pay?

Spreadsheet from www.riamwr.com/acs/financial-readiness/

Do you need to add savings to

cover all of your expenses?

Other MS Excel Spreadsheets and Worksheets

Furlough Pay EstimatorMoney Allocation Plan ($ MAP)

[budget] in Weekly Bands

“Savings to Spend”Annual Spending

Estimation

www.riamwr.com/acs/financial-readiness/

UNCLASSIFIED 12

Disqualifying & Mitigation Criteria for Delinquent Financial Accounts

– Inability or unwillingness to satisfy debts. – Indebtedness caused by frivolous/irresponsible

spending with no intent/effort to repay the debt.

– Recurring history of bad debts, garnishments, liens, repossessions write offs, etc.

– Bankruptcy caused by financial irresponsibility. – Indebtedness caused by gambling, alcohol,

drug abuse, or other factors indicating poor judgment.

– A pattern of living beyond one’s means or ability to pay.

– Indifference to paying lawful financial obligations.

– The writing of checks with insufficient funds. – Engaging in deceitful/illegal actions: tax evasion,

embezzlement, fraud or attempts to evade lawful creditors.

• The indebtedness was so infrequent or occurred under circumstances that it is not likely to recur and does not cast doubts on the individual’s good judgment.

• Financial problems were largely beyond the person’s control (loss of employment, economic downturn, divorce, separation, medical expenses, etc.) and the individual acted responsibly under the circumstances.

• Person is receiving professional help, and there are clear indications the financial problem is being resolved or is under control.

• Individual made a good-faith effort to repay the debt.

• There is documentation and a reasonable basis to dispute the past due debt and evidence of actions to resolve the issue.

• A scheduled program of systematic debt repay is established (debt-consolidation program, court supervised payment program, etc.,).

Examples of Disqualifying Factors: Examples of Mitigation Factors:

KEY: Take Responsibility! Adjust Spending! Act to resolve!

May be able to pay less than the full balance.This slide courtesy of Security Office of

Tank and Automotive Command (TACOM)

UNCLASSIFIED 13

Factors that Could Affect an Individual’s Continued Eligibility to Classified Information and FOUO Level

DOD Computer Access• AR 380-67, para 9-103 states,

“Individuals having access to classified information must report promptly to their security office… any information of the type referred to in appendix I (Adjudicative Guidelines).”

• A challenge facing Civilian Employees before the Furlough has been financial issues, and the furlough is expected to increase the challenges some individuals are facing.

G2, TACOM LCMC has compiled the following informal list of financial challenges that could affect an individual’s access:

• Recurring history of failing to pay one’s debts when due.

• 90 - 120+ days over due for a minimum payment.

• Charge-offs, repossessions, suspension of credit cards or accounts.

• Failure to pay court directed settlements/judgments.

• Short sale/Foreclosure.• CH 11, 13, or 7 Bankruptcy.• Failure to file/pay taxes or tax lien.• Total overdue debt is more than $10K.

If you are experiencing any of the financial challenges listed on this chart, you need to self-report to your supporting Security Office for assistance.

This slide courtesy of Security Office of Tank and Automotive Command (TACOM)

www. annual credit report.com

All 3 at once; and / or start a 4-month rotation

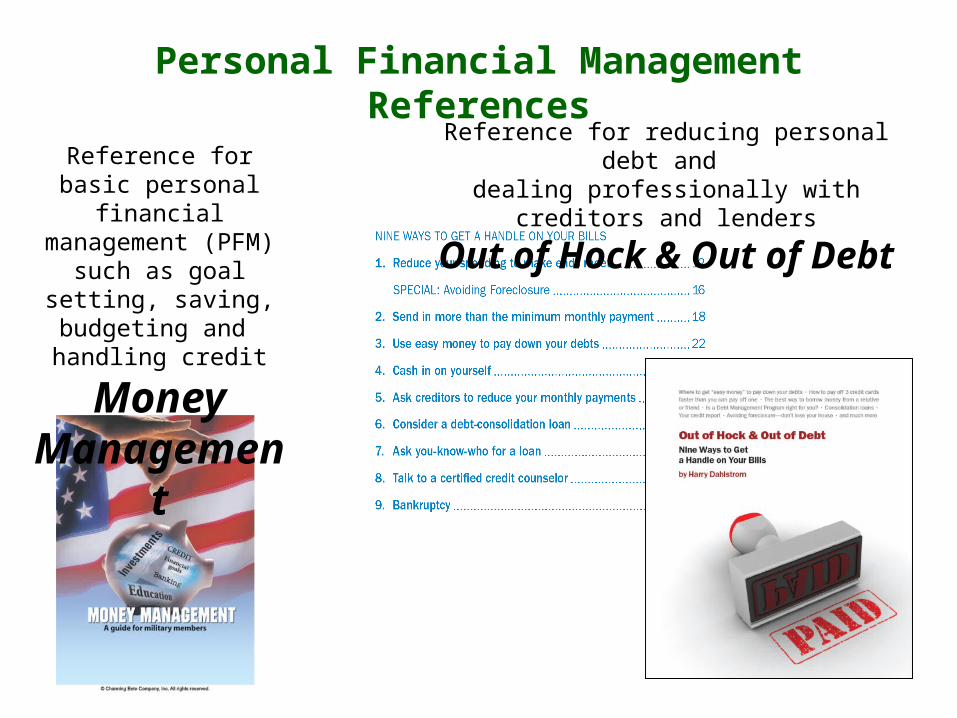

Personal Financial Management References

Reference for reducing personal debt and dealing professionally with creditors and lenders

Out of Hock & Out of DebtReference for basic personal financial

management (PFM) such as goal setting, saving,

budgeting and handling credit

Money Management

Collaborating with your Creditorssome thoughts

Secured Creditor: a creditor that has a security interest and can by contract either take back an item or turn off a service.Examples:• Mortgage lender – repossesses the home• Car loan lender – repossesses the car• Utility – turns off the service• Doctor – denies future services• Federally subsidized student loan – Dept of Ed garnishes IRS refunds

Unsecured Creditor: makes a loan without a security interestExamples: credit cards or personal loansNote: an unsecured creditor will go “ugly early” because they are unsecured and know that they need a court judgment in order to recover their money.

Both types of creditors can make notations on your credit report! As you decide “who makes it into the lifeboat,” consider your secured creditors first (there can be exceptions)

Collaborating with your Creditorssome thoughts (continued)

What’s in it for the creditor to cooperate? Their bottom line is money It is cheaper for them to retain a customer than to find a new customer The primary lender of credit may be flexible (debt collectors may not be as flexible) You have been a loyal customer and hope to continue to do business with them in the future. The accommodation will be a short term fix only through the furlough. “You are a patriotic Federal employee and you need their help also to assist our government through this fiscal crisis” “You cannot pay money your employer isn’t paying you”

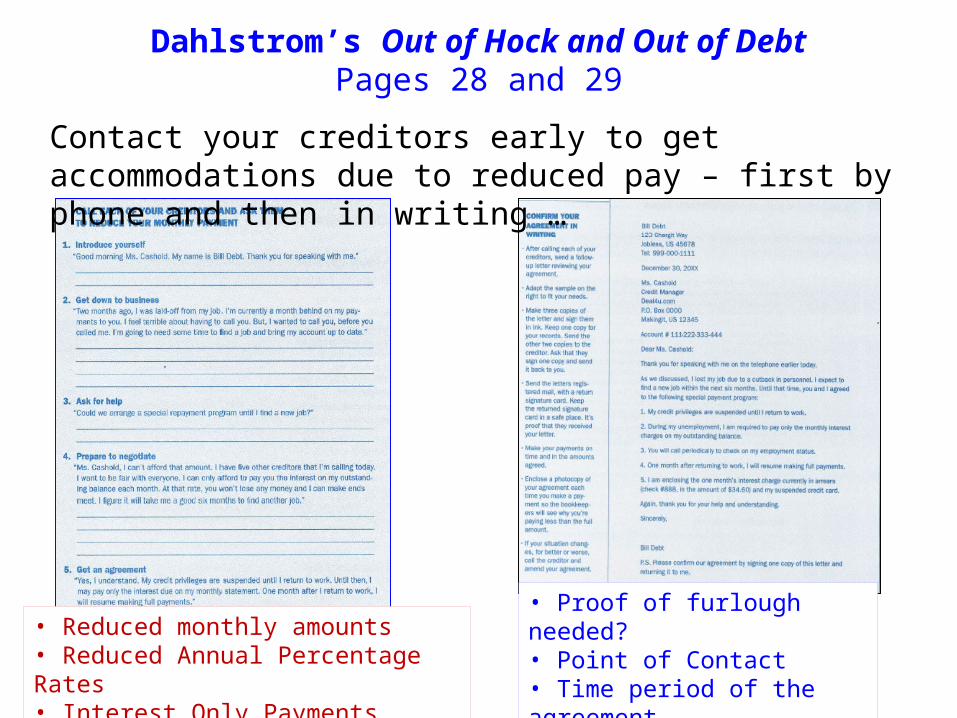

Dahlstrom’s Out of Hock and Out of DebtPages 28 and 29

Contact your creditors early to get accommodations due to reduced pay – first by phone and then in writing …

• Reduced monthly amounts• Reduced Annual Percentage Rates• Interest Only Payments

• Proof of furlough needed?• Point of Contact• Time period of the agreement• Impact on Credit Report, if any

www.riafcu.com(563) 355-3800

• Consult with a personal representative • Learning about Saving Strategies• Learn about low interest products• Consult with financial coaches on impacts of dealing with creditors

Consult with your financial institution(s) and

creditor(s) early if you foresee a problem!

Your on-post Financial Institution

My Army One Source at www.myarmyonesource.com> (1) Family Programs and Services (on the upper left) > (2) Family programs > (3) Financial Readiness

Personal Financial Management Web $ites

1

2

3

Personal Financial Management Web $ites

http://www.powerpay.org

PowerPay from Utah State Extension Service & Utah State University

Personal Financial Management Web $ites

www.feedthepig.org

Ways to Save!

www.consumer.ftc.gov/articles/0163-66-ways-save-money

66 Ways to Save Money!

Personal Financial Management Web $ites

http://www.feea.org

Scholarships for Federal Employees

and Family Members

Application for Assistance

Personal Financial ManagementInstallation Resources

1. First Line Supervisor, your Supervisory Chain, and your personnel office

2. Civilian Personnel Advisory Center (CPAC RIA)

Furlough Hotline – (309) 782-1742; https://ncweb.ria.army.mil/riacpac/

3. Security Office to alert them of credit report & security clearance issues –

(309) 782-6611

4. “Ask the Garrison Manager” via Garrison Public Affairs Officer (PAO):

Eric Cramer, (309) 782-7746, [email protected]

5. Army Community Service (ACS) – (309) 782-0829 / -0815

6. Employee Assistance Program (EAP) – (309) 782-4357 (2-HELP)

7. Chaplain’s Office (Army Sustainment Command) – (309) 782-0910

8. On-post Financial Institution = RIA Federal Credit Union www.riafcu.com

General Number: (563) 355-3800; RIA Branch Manager: ext 1000

Personal Financial Management Community Resources

United Way of the Quad CitiesInformation and Referral Service “2 – 1 – 1”

http://unitedwayqc.org/our-work/2-1-1

Financial Tips for“Weathering the Furlough”

• When battling the budget, you have three options: • (1) decrease expenses; • (2) increase income; or • (3) do both.

• Encourage your team and family to contribute to solutions.• The Personal Financial Management (PFM) goal does not change:

spend less than you make!• Consider what you’ll save• Trim the fat from your budget • Wipe out unnecessary expenses • Cut back on food costs • Contact your financial institution and creditors to ask for an accommodation• Dip into savings cautiously • Apply for loans if necessary• Make extra money • Military Saves and Ready Army Informational Campaigns• Theodore Roosevelt had this advice: “Do what you can, with what you have, where you are.”

* Adjust W-4 Withholding

http://www.irs.gov/Individuals/IRS-Withholding-Calculator

Desire more take home pay?Desire an instant pay raise?Get too much money in your tax refunds?Are you starving for 51 weeks and then get money dumped on you, and then go back to starving?Adjust your W-4 Withholdings for Federal and State taxes!

Why give the revenue services an interest free loan?Put the money in your bi-weekly paycheck $$!

Personal Financial Management

a Call to ActionCan your current savings carry you through the furlough and reduced

pay?

Can you cut enough expenses to stay within the budget?

Through end of September? (through ____?)• Actions you, your family and your co-workers may take now to prepare.• Commit to short and long term goals.• Resources available to meet your goals.