egypt outlook - october2015

TRANSCRIPT

For the use of Rasmala Egypt Asset Management, not for circulation[Type the company name]

Egypt’s Outlook - Crossroads

October 2015

Rasmala Egypt Asset Management Smart Village F 16, P.O Box 133 Km 28 Cairo Alex Desert Road, Egypt Tel: +202 353 70575 Fax: +202 353 53686

www.rasmala.com

For the use of Rasmala Egypt Asset Management, not for circulation

Egypt’s Outlook - Crossroads 2015

1 For the use of Rasmala Egypt Asset Management, not for circulation

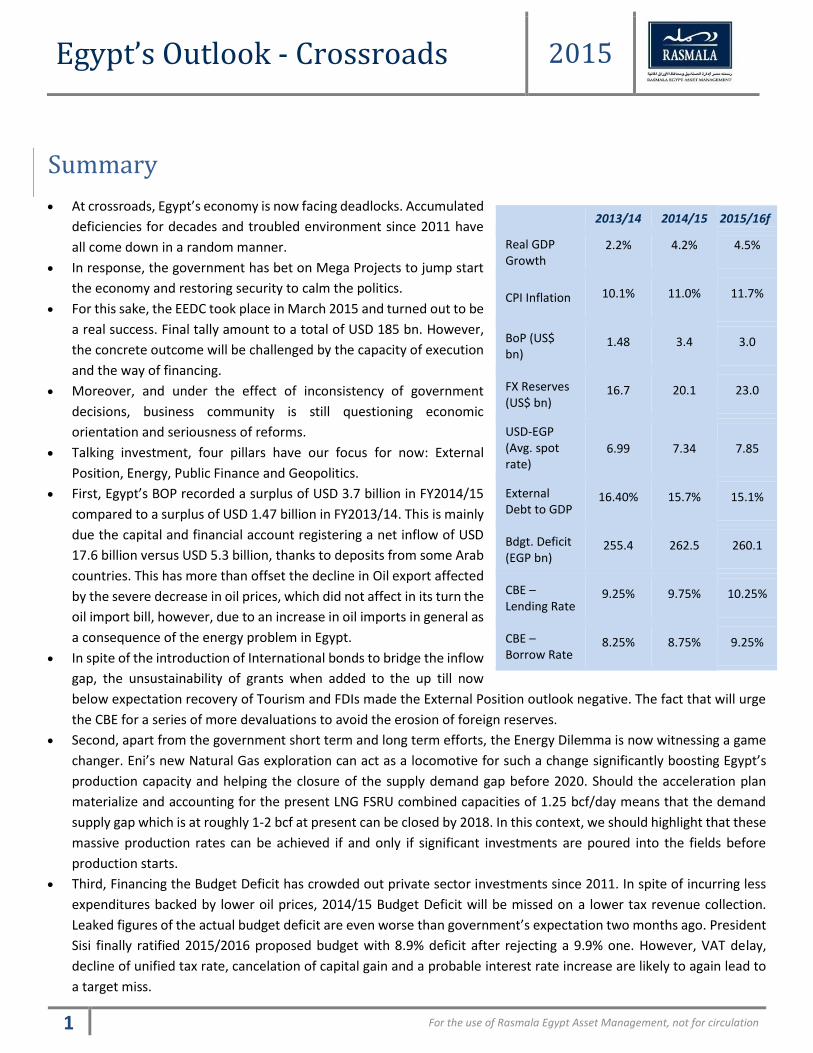

Summary

At crossroads, Egypt’s economy is now facing deadlocks. Accumulated

deficiencies for decades and troubled environment since 2011 have

all come down in a random manner.

In response, the government has bet on Mega Projects to jump start

the economy and restoring security to calm the politics.

For this sake, the EEDC took place in March 2015 and turned out to be

a real success. Final tally amount to a total of USD 185 bn. However,

the concrete outcome will be challenged by the capacity of execution

and the way of financing.

Moreover, and under the effect of inconsistency of government

decisions, business community is still questioning economic

orientation and seriousness of reforms.

Talking investment, four pillars have our focus for now: External

Position, Energy, Public Finance and Geopolitics.

First, Egypt’s BOP recorded a surplus of USD 3.7 billion in FY2014/15

compared to a surplus of USD 1.47 billion in FY2013/14. This is mainly

due the capital and financial account registering a net inflow of USD

17.6 billion versus USD 5.3 billion, thanks to deposits from some Arab

countries. This has more than offset the decline in Oil export affected

by the severe decrease in oil prices, which did not affect in its turn the

oil import bill, however, due to an increase in oil imports in general as

a consequence of the energy problem in Egypt.

In spite of the introduction of International bonds to bridge the inflow

gap, the unsustainability of grants when added to the up till now

below expectation recovery of Tourism and FDIs made the External Position outlook negative. The fact that will urge

the CBE for a series of more devaluations to avoid the erosion of foreign reserves.

Second, apart from the government short term and long term efforts, the Energy Dilemma is now witnessing a game

changer. Eni’s new Natural Gas exploration can act as a locomotive for such a change significantly boosting Egypt’s

production capacity and helping the closure of the supply demand gap before 2020. Should the acceleration plan

materialize and accounting for the present LNG FSRU combined capacities of 1.25 bcf/day means that the demand

supply gap which is at roughly 1-2 bcf at present can be closed by 2018. In this context, we should highlight that these

massive production rates can be achieved if and only if significant investments are poured into the fields before

production starts.

Third, Financing the Budget Deficit has crowded out private sector investments since 2011. In spite of incurring less

expenditures backed by lower oil prices, 2014/15 Budget Deficit will be missed on a lower tax revenue collection.

Leaked figures of the actual budget deficit are even worse than government’s expectation two months ago. President

Sisi finally ratified 2015/2016 proposed budget with 8.9% deficit after rejecting a 9.9% one. However, VAT delay,

decline of unified tax rate, cancelation of capital gain and a probable interest rate increase are likely to again lead to

a target miss.

2013/14 2014/15 2015/16f

Real GDP Growth

2.2% 4.2% 4.5%

CPI Inflation 10.1% 11.0% 11.7%

BoP (US$ bn)

1.48 3.4 3.0

FX Reserves (US$ bn)

16.7 20.1 23.0

USD-EGP (Avg. spot rate)

6.99 7.34 7.85

External Debt to GDP

16.40% 15.7% 15.1%

Bdgt. Deficit (EGP bn)

255.4 262.5 260.1

CBE – Lending Rate

9.25% 9.75% 10.25%

CBE – Borrow Rate

8.25% 8.75% 9.25%

Egypt’s Outlook - Crossroads 2015

2 For the use of Rasmala Egypt Asset Management, not for circulation

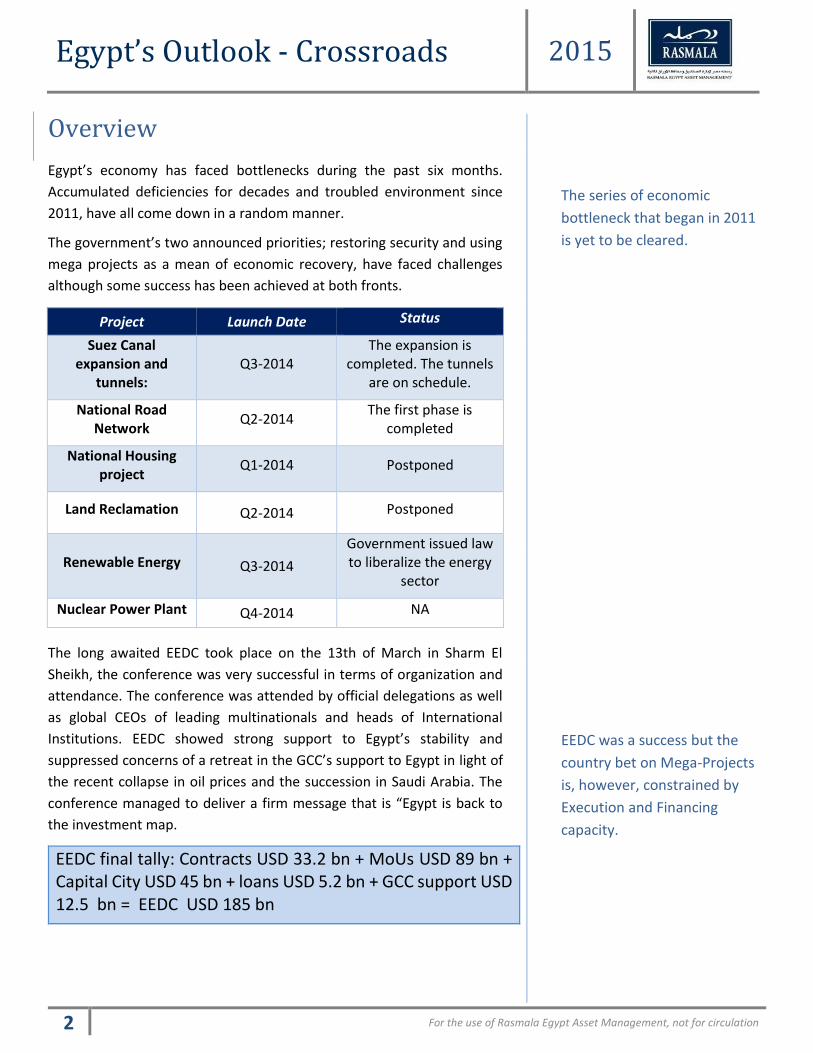

Overview

Egypt’s economy has faced bottlenecks during the past six months.

Accumulated deficiencies for decades and troubled environment since

2011, have all come down in a random manner.

The government’s two announced priorities; restoring security and using

mega projects as a mean of economic recovery, have faced challenges

although some success has been achieved at both fronts.

The long awaited EEDC took place on the 13th of March in Sharm El

Sheikh, the conference was very successful in terms of organization and

attendance. The conference was attended by official delegations as well

as global CEOs of leading multinationals and heads of International

Institutions. EEDC showed strong support to Egypt’s stability and

suppressed concerns of a retreat in the GCC’s support to Egypt in light of

the recent collapse in oil prices and the succession in Saudi Arabia. The

conference managed to deliver a firm message that is “Egypt is back to

the investment map.

Project Launch Date Status

Suez Canal expansion and

tunnels: Q3-2014

The expansion is completed. The tunnels

are on schedule.

National Road Network

Q2-2014 The first phase is

completed

National Housing project

Q1-2014 Postponed

Land Reclamation Q2-2014 Postponed

Renewable Energy Q3-2014

Government issued law to liberalize the energy

sector

Nuclear Power Plant Q4-2014 NA

EEDC final tally: Contracts USD 33.2 bn + MoUs USD 89 bn + Capital City USD 45 bn + loans USD 5.2 bn + GCC support USD 12.5 bn = EEDC USD 185 bn

The series of economic

bottleneck that began in 2011

is yet to be cleared.

EEDC was a success but the

country bet on Mega-Projects

is, however, constrained by

Execution and Financing

capacity.

Egypt’s Outlook - Crossroads 2015

3 For the use of Rasmala Egypt Asset Management, not for circulation

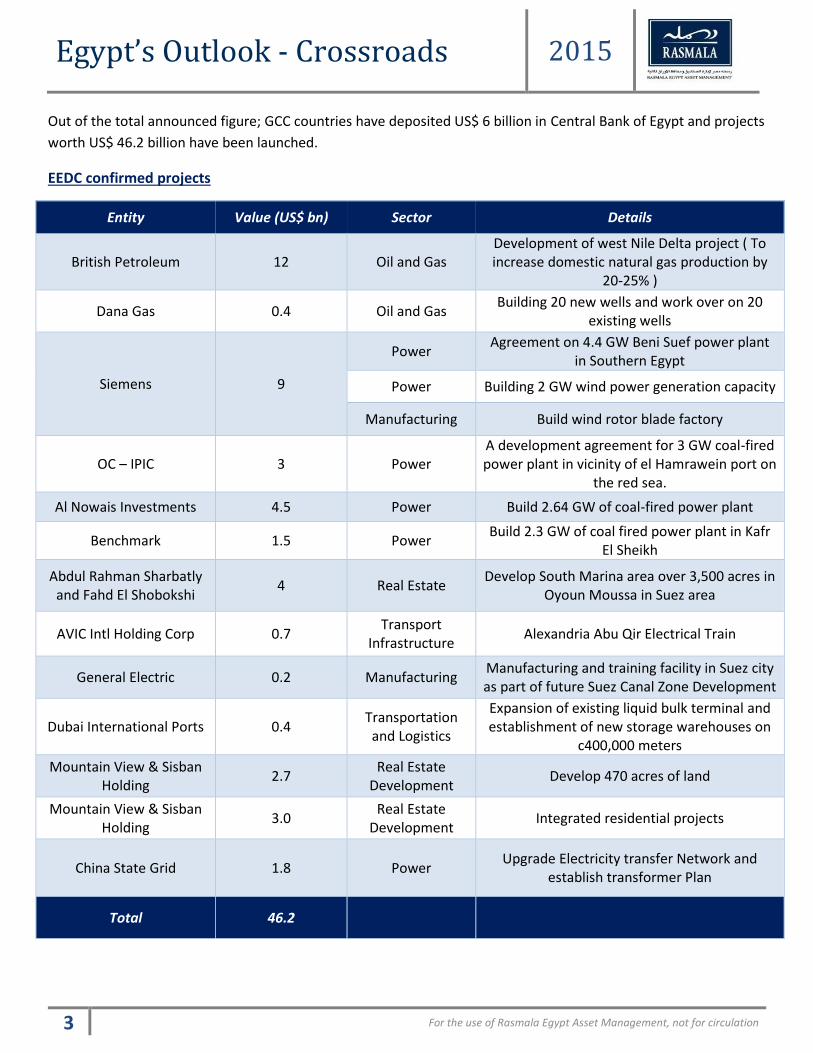

Out of the total announced figure; GCC countries have deposited US$ 6 billion in Central Bank of Egypt and projects

worth US$ 46.2 billion have been launched.

EEDC confirmed projects

Entity Value (US$ bn) Sector Details

British Petroleum 12 Oil and Gas Development of west Nile Delta project ( To increase domestic natural gas production by

20-25% )

Dana Gas 0.4 Oil and Gas Building 20 new wells and work over on 20

existing wells

Siemens 9

Power Agreement on 4.4 GW Beni Suef power plant

in Southern Egypt

Power Building 2 GW wind power generation capacity

Manufacturing Build wind rotor blade factory

OC – IPIC 3 Power A development agreement for 3 GW coal-fired power plant in vicinity of el Hamrawein port on

the red sea.

Al Nowais Investments 4.5 Power Build 2.64 GW of coal-fired power plant

Benchmark 1.5 Power Build 2.3 GW of coal fired power plant in Kafr

El Sheikh

Abdul Rahman Sharbatly and Fahd El Shobokshi

4 Real Estate Develop South Marina area over 3,500 acres in

Oyoun Moussa in Suez area

AVIC Intl Holding Corp 0.7 Transport

Infrastructure Alexandria Abu Qir Electrical Train

General Electric 0.2 Manufacturing Manufacturing and training facility in Suez city as part of future Suez Canal Zone Development

Dubai International Ports 0.4 Transportation and Logistics

Expansion of existing liquid bulk terminal and establishment of new storage warehouses on

c400,000 meters

Mountain View & Sisban Holding

2.7 Real Estate

Development Develop 470 acres of land

Mountain View & Sisban Holding

3.0 Real Estate

Development Integrated residential projects

China State Grid 1.8 Power Upgrade Electricity transfer Network and

establish transformer Plan

Total 46.2

Egypt’s Outlook - Crossroads 2015

4 For the use of Rasmala Egypt Asset Management, not for circulation

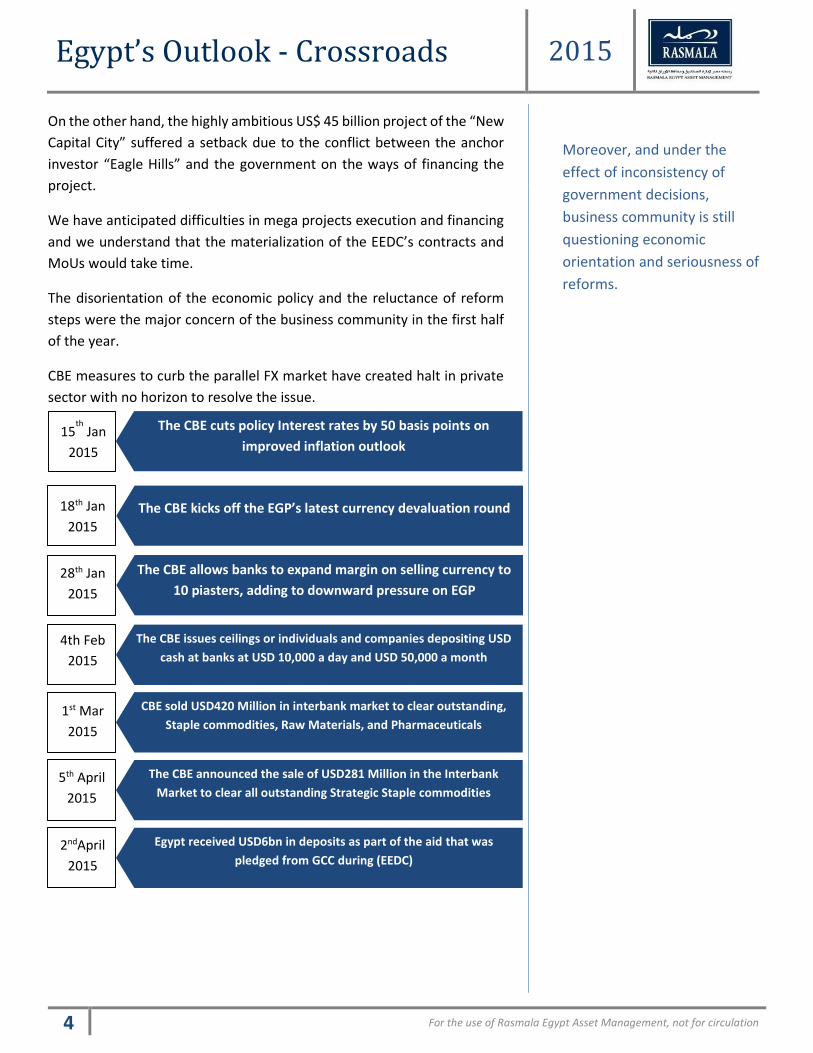

On the other hand, the highly ambitious US$ 45 billion project of the “New

Capital City” suffered a setback due to the conflict between the anchor

investor “Eagle Hills” and the government on the ways of financing the

project.

We have anticipated difficulties in mega projects execution and financing

and we understand that the materialization of the EEDC’s contracts and

MoUs would take time.

The disorientation of the economic policy and the reluctance of reform

steps were the major concern of the business community in the first half

of the year.

CBE measures to curb the parallel FX market have created halt in private

sector with no horizon to resolve the issue.

Moreover, and under the

effect of inconsistency of

government decisions,

business community is still

questioning economic

orientation and seriousness of

reforms.

The CBE cuts policy Interest rates by 50 basis points on

improved inflation outlook 15

th Jan

2015

The CBE kicks off the EGP’s latest currency devaluation round 18th Jan

2015

The CBE allows banks to expand margin on selling currency to

10 piasters, adding to downward pressure on EGP 28th Jan

2015

The CBE issues ceilings or individuals and companies depositing USD

cash at banks at USD 10,000 a day and USD 50,000 a month

4th Feb

2015

CBE sold USD420 Million in interbank market to clear outstanding,

Staple commodities, Raw Materials, and Pharmaceuticals 1st Mar

2015

The CBE announced the sale of USD281 Million in the Interbank

Market to clear all outstanding Strategic Staple commodities 5th April

2015

Egypt received USD6bn in deposits as part of the aid that was

pledged from GCC during (EEDC) 2ndApril

2015

Egypt’s Outlook - Crossroads 2015

5 For the use of Rasmala Egypt Asset Management, not for circulation

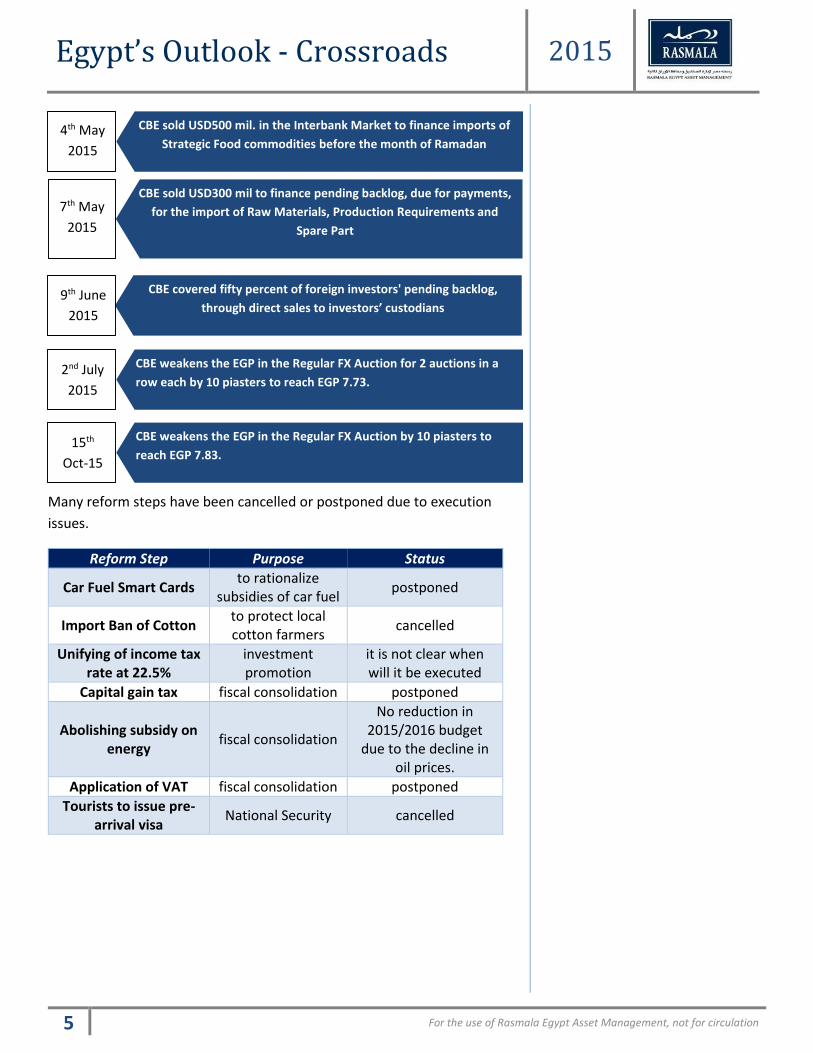

Many reform steps have been cancelled or postponed due to execution

issues.

Reform Step Purpose Status

Car Fuel Smart Cards to rationalize

subsidies of car fuel postponed

Import Ban of Cotton to protect local cotton farmers

cancelled

Unifying of income tax rate at 22.5%

investment promotion

it is not clear when will it be executed

Capital gain tax fiscal consolidation postponed

Abolishing subsidy on energy

fiscal consolidation

No reduction in 2015/2016 budget

due to the decline in oil prices.

Application of VAT fiscal consolidation postponed

Tourists to issue pre-arrival visa

National Security cancelled

CBE sold USD500 mil. in the Interbank Market to finance imports of

Strategic Food commodities before the month of Ramadan 4th May

2015

CBE sold USD300 mil to finance pending backlog, due for payments,

for the import of Raw Materials, Production Requirements and

Spare Part

7th May

2015

CBE covered fifty percent of foreign investors' pending backlog,

through direct sales to investors’ custodians 9th June

2015

CBE weakens the EGP in the Regular FX Auction for 2 auctions in a

row each by 10 piasters to reach EGP 7.73.

2nd July

2015

CBE weakens the EGP in the Regular FX Auction by 10 piasters to

reach EGP 7.83.

15th

Oct-15

Egypt’s Outlook - Crossroads 2015

6 For the use of Rasmala Egypt Asset Management, not for circulation

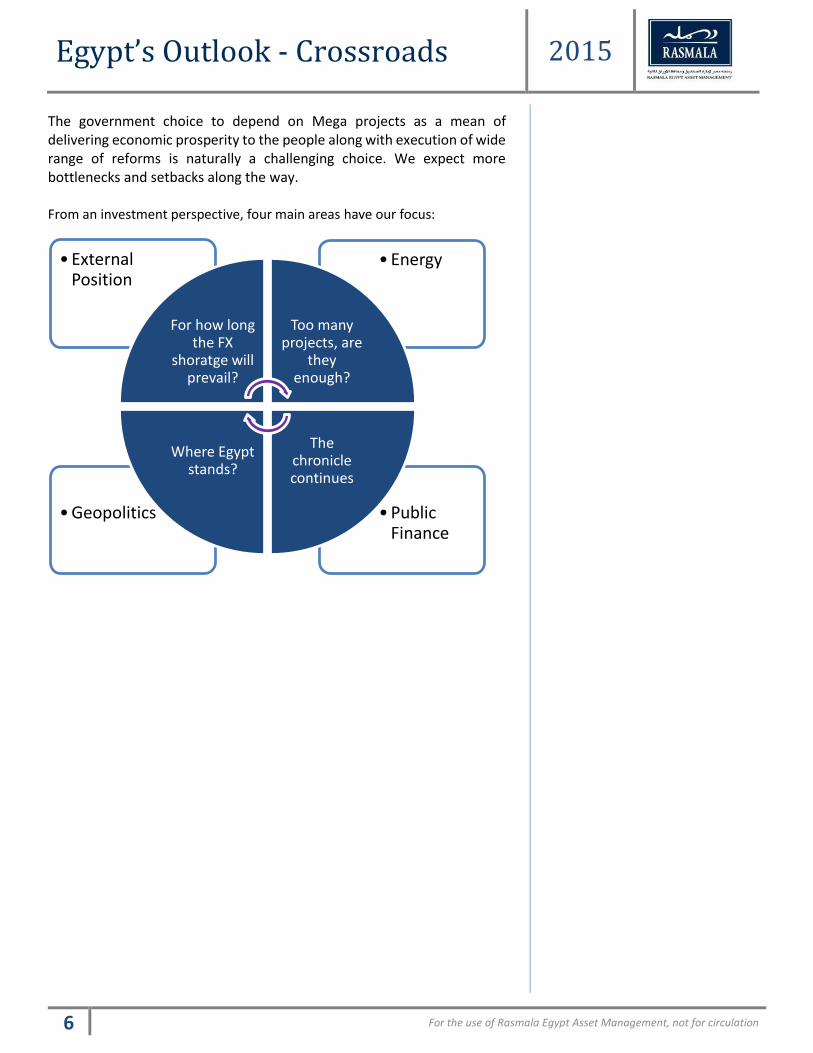

The government choice to depend on Mega projects as a mean of delivering economic prosperity to the people along with execution of wide range of reforms is naturally a challenging choice. We expect more bottlenecks and setbacks along the way. From an investment perspective, four main areas have our focus:

• Public Finance

• Geopolitics

• Energy• External Position

For how long the FX

shoratge will prevail?

Too many projects, are

they enough?

The chronicle continues

Where Egypt stands?

Egypt’s Outlook - Crossroads 2015

7 For the use of Rasmala Egypt Asset Management, not for circulation

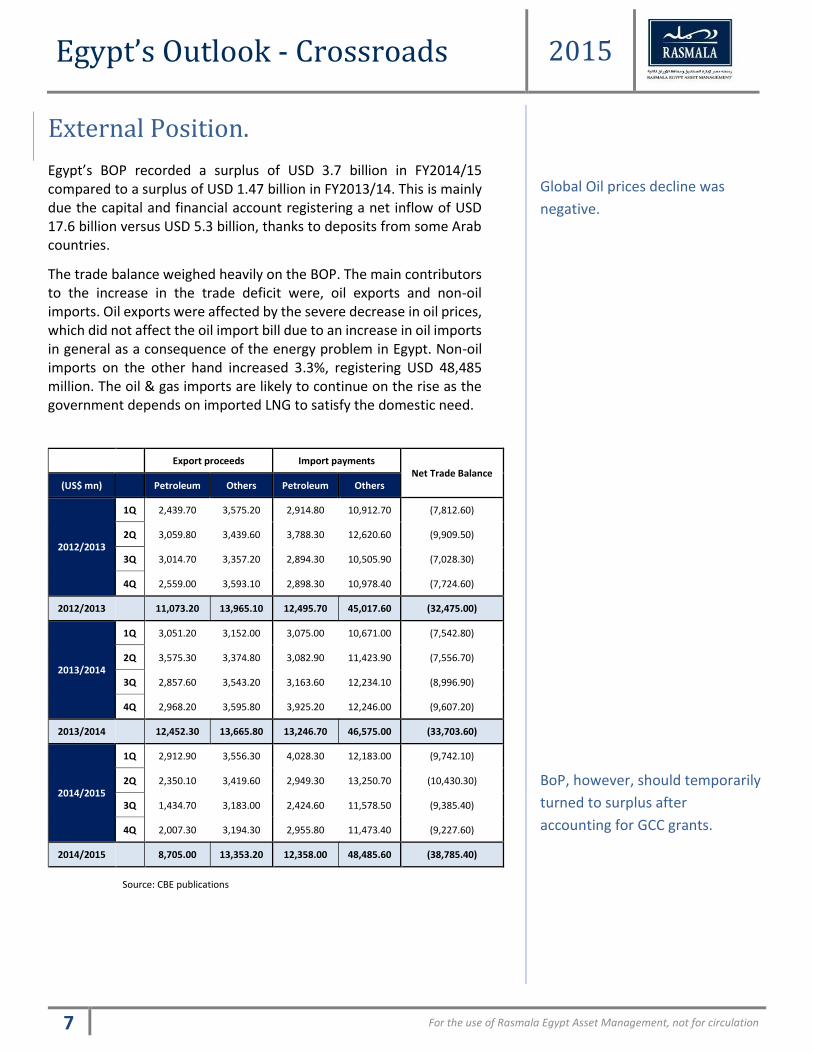

External Position.

Egypt’s BOP recorded a surplus of USD 3.7 billion in FY2014/15 compared to a surplus of USD 1.47 billion in FY2013/14. This is mainly due the capital and financial account registering a net inflow of USD 17.6 billion versus USD 5.3 billion, thanks to deposits from some Arab countries.

The trade balance weighed heavily on the BOP. The main contributors to the increase in the trade deficit were, oil exports and non-oil imports. Oil exports were affected by the severe decrease in oil prices, which did not affect the oil import bill due to an increase in oil imports in general as a consequence of the energy problem in Egypt. Non-oil imports on the other hand increased 3.3%, registering USD 48,485 million. The oil & gas imports are likely to continue on the rise as the government depends on imported LNG to satisfy the domestic need.

Export proceeds Import payments Net Trade Balance

(US$ mn) Petroleum Others Petroleum Others

2012/2013

1Q 2,439.70 3,575.20 2,914.80 10,912.70 (7,812.60)

2Q 3,059.80 3,439.60 3,788.30 12,620.60 (9,909.50)

3Q 3,014.70 3,357.20 2,894.30 10,505.90 (7,028.30)

4Q 2,559.00 3,593.10 2,898.30 10,978.40 (7,724.60)

2012/2013 11,073.20 13,965.10 12,495.70 45,017.60 (32,475.00)

2013/2014

1Q 3,051.20 3,152.00 3,075.00 10,671.00 (7,542.80)

2Q 3,575.30 3,374.80 3,082.90 11,423.90 (7,556.70)

3Q 2,857.60 3,543.20 3,163.60 12,234.10 (8,996.90)

4Q 2,968.20 3,595.80 3,925.20 12,246.00 (9,607.20)

2013/2014 12,452.30 13,665.80 13,246.70 46,575.00 (33,703.60)

2014/2015

1Q 2,912.90 3,556.30 4,028.30 12,183.00 (9,742.10)

2Q 2,350.10 3,419.60 2,949.30 13,250.70 (10,430.30)

3Q 1,434.70 3,183.00 2,424.60 11,578.50 (9,385.40)

4Q 2,007.30 3,194.30 2,955.80 11,473.40 (9,227.60)

2014/2015 8,705.00 13,353.20 12,358.00 48,485.60 (38,785.40)

Source: CBE publications

Global Oil prices decline was

negative.

BoP, however, should temporarily

turned to surplus after

accounting for GCC grants.

Egypt’s Outlook - Crossroads 2015

8 For the use of Rasmala Egypt Asset Management, not for circulation

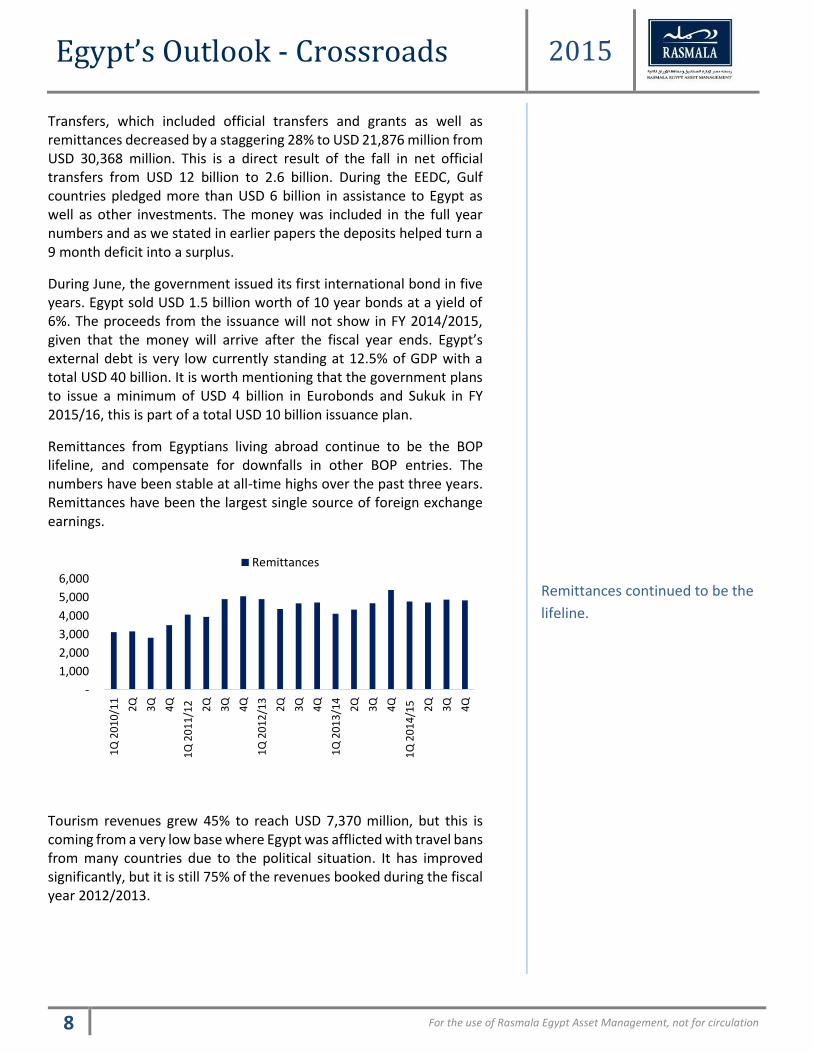

Transfers, which included official transfers and grants as well as remittances decreased by a staggering 28% to USD 21,876 million from USD 30,368 million. This is a direct result of the fall in net official transfers from USD 12 billion to 2.6 billion. During the EEDC, Gulf countries pledged more than USD 6 billion in assistance to Egypt as well as other investments. The money was included in the full year numbers and as we stated in earlier papers the deposits helped turn a 9 month deficit into a surplus.

During June, the government issued its first international bond in five years. Egypt sold USD 1.5 billion worth of 10 year bonds at a yield of 6%. The proceeds from the issuance will not show in FY 2014/2015, given that the money will arrive after the fiscal year ends. Egypt’s external debt is very low currently standing at 12.5% of GDP with a total USD 40 billion. It is worth mentioning that the government plans to issue a minimum of USD 4 billion in Eurobonds and Sukuk in FY 2015/16, this is part of a total USD 10 billion issuance plan.

Remittances from Egyptians living abroad continue to be the BOP lifeline, and compensate for downfalls in other BOP entries. The numbers have been stable at all-time highs over the past three years. Remittances have been the largest single source of foreign exchange earnings.

Tourism revenues grew 45% to reach USD 7,370 million, but this is coming from a very low base where Egypt was afflicted with travel bans from many countries due to the political situation. It has improved significantly, but it is still 75% of the revenues booked during the fiscal year 2012/2013.

-

1,000

2,000

3,000

4,000

5,000

6,000

1Q

20

10

/11

2Q

3Q

4Q

1Q

20

11

/12 2Q

3Q

4Q

1Q

20

12

/13

2Q

3Q

4Q

1Q

20

13

/14

2Q

3Q

4Q

1Q

20

14

/15 2Q

3Q

4Q

Remittances

Remittances continued to be the

lifeline.

Egypt’s Outlook - Crossroads 2015

9 For the use of Rasmala Egypt Asset Management, not for circulation

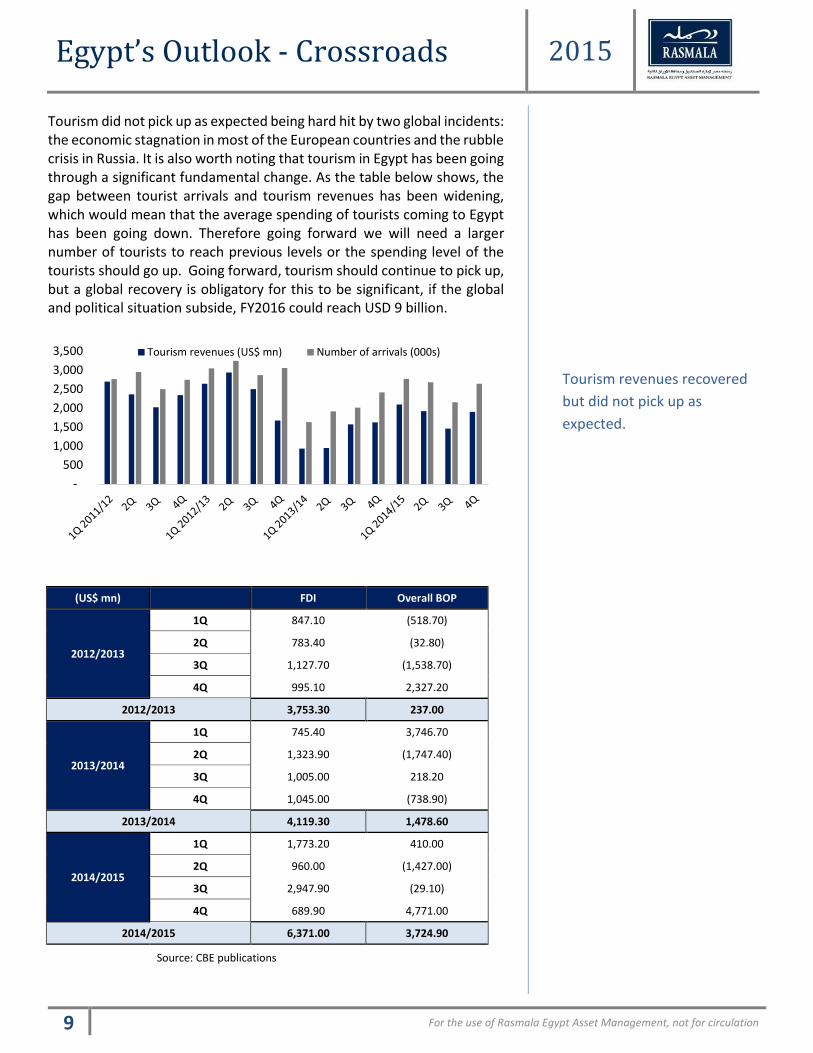

Tourism did not pick up as expected being hard hit by two global incidents: the economic stagnation in most of the European countries and the rubble crisis in Russia. It is also worth noting that tourism in Egypt has been going through a significant fundamental change. As the table below shows, the gap between tourist arrivals and tourism revenues has been widening, which would mean that the average spending of tourists coming to Egypt has been going down. Therefore going forward we will need a larger number of tourists to reach previous levels or the spending level of the tourists should go up. Going forward, tourism should continue to pick up, but a global recovery is obligatory for this to be significant, if the global and political situation subside, FY2016 could reach USD 9 billion.

(US$ mn) FDI Overall BOP

2012/2013

1Q 847.10 (518.70)

2Q 783.40 (32.80)

3Q 1,127.70 (1,538.70)

4Q 995.10 2,327.20

2012/2013 3,753.30 237.00

2013/2014

1Q 745.40 3,746.70

2Q 1,323.90 (1,747.40)

3Q 1,005.00 218.20

4Q 1,045.00 (738.90)

2013/2014 4,119.30 1,478.60

2014/2015

1Q 1,773.20 410.00

2Q 960.00 (1,427.00)

3Q 2,947.90 (29.10)

4Q 689.90 4,771.00

2014/2015 6,371.00 3,724.90

Source: CBE publications

-

500

1,000

1,500

2,000

2,500

3,000

3,500 Tourism revenues (US$ mn) Number of arrivals (000s)

Tourism revenues recovered

but did not pick up as

expected.

Egypt’s Outlook - Crossroads 2015

10 For the use of Rasmala Egypt Asset Management, not for circulation

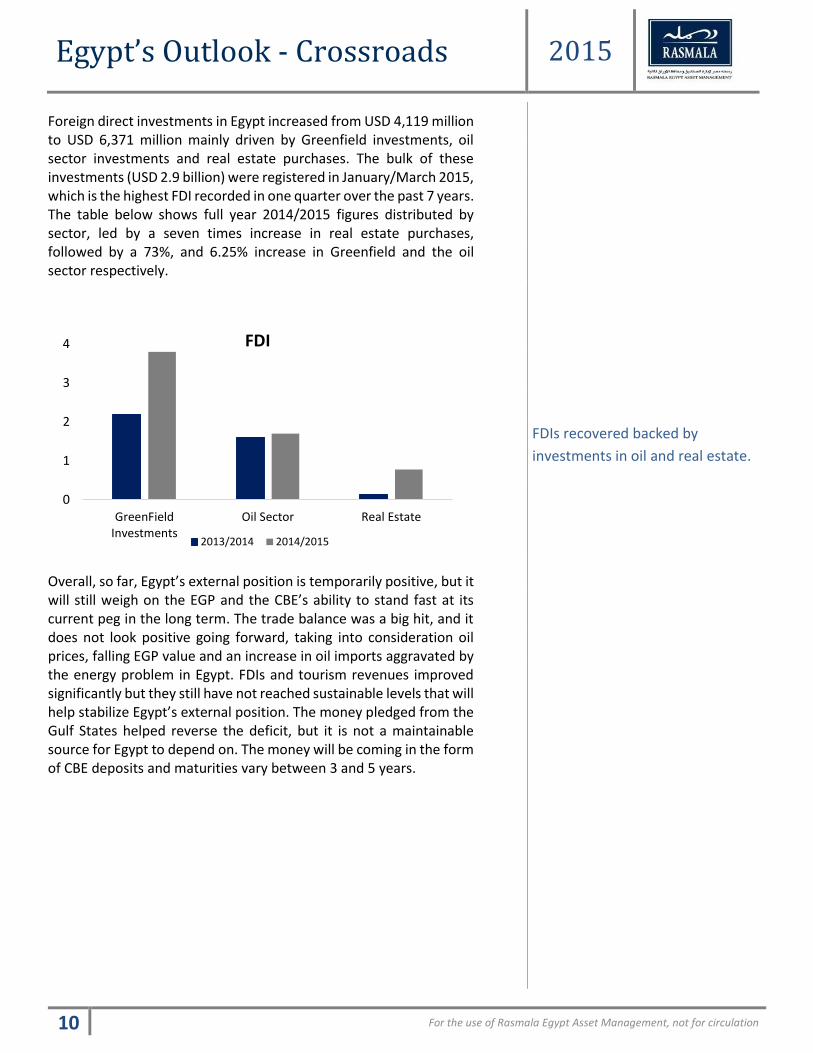

Foreign direct investments in Egypt increased from USD 4,119 million to USD 6,371 million mainly driven by Greenfield investments, oil sector investments and real estate purchases. The bulk of these investments (USD 2.9 billion) were registered in January/March 2015, which is the highest FDI recorded in one quarter over the past 7 years. The table below shows full year 2014/2015 figures distributed by sector, led by a seven times increase in real estate purchases, followed by a 73%, and 6.25% increase in Greenfield and the oil sector respectively.

Overall, so far, Egypt’s external position is temporarily positive, but it will still weigh on the EGP and the CBE’s ability to stand fast at its current peg in the long term. The trade balance was a big hit, and it does not look positive going forward, taking into consideration oil prices, falling EGP value and an increase in oil imports aggravated by the energy problem in Egypt. FDIs and tourism revenues improved significantly but they still have not reached sustainable levels that will help stabilize Egypt’s external position. The money pledged from the Gulf States helped reverse the deficit, but it is not a maintainable source for Egypt to depend on. The money will be coming in the form of CBE deposits and maturities vary between 3 and 5 years.

0

1

2

3

4

GreenFieldInvestments

Oil Sector Real Estate

FDI

2013/2014 2014/2015

FDIs recovered backed by

investments in oil and real estate.

Egypt’s Outlook - Crossroads 2015

11 For the use of Rasmala Egypt Asset Management, not for circulation

Even though the BOP was positive and the change in FX reserves are

positive it is a consequence of the deposits from the Gulf States.

Therefore, it is safe to assume that the CBE will not be able to hold

the peg for long unless either Gulf aid continues or situation improves

at a faster pace. The CBE will probably have to dig into its FX reserves

to keep the EGP at current levels, given the negative effects on the

economy of the CBEs tough FX restrictions. At the critical level of NIR

of US$ 16.3 billion, the most likely scenario is a series of managed

devaluations that will increase the attractiveness of the EGP, and help

increase inflows. We expect USD to reach EGP8 by year-end.

Scenario Analysis

Action Outcome

CBE maintains the FX rate at current level and ask for more help from GCC

The existing restrictions will continue

CBE executes managed devaluation in

anticipation of sharp recovery in FDI and

tourism

The shortage will continue at a lower magnitude

CBE let the currency float in order to attract

portfolio inflow

The restrictions will diminish and more liquidity appears in the interbank

market.

International bonds issuance

are trendy but

unsustainability of grants

made the outlook negative

urging the CBE for a series of

more devaluations.

Egypt’s Outlook - Crossroads 2015

12 For the use of Rasmala Egypt Asset Management, not for circulation

Energy

A. Roots & Fallouts

Since the political uprising of 2011, issues related to the contractual agreements governing Egypt’s gas and oil sectors have come to the fore. A more challenging scenario has evolved with regard to IOCs (International Oil Companies) as Egypt’s fiscal position has deteriorated over the past two years, stemming from the generous subsidization of gas and refined products by the government.

While the government, through the MOP and its agencies, purchase gas at capped rates, it makes gas available in the domestic market at much lower rates – a discrepancy that caused EGPC to run up high levels of debt and fall behind on payments to IOCs in 2012.

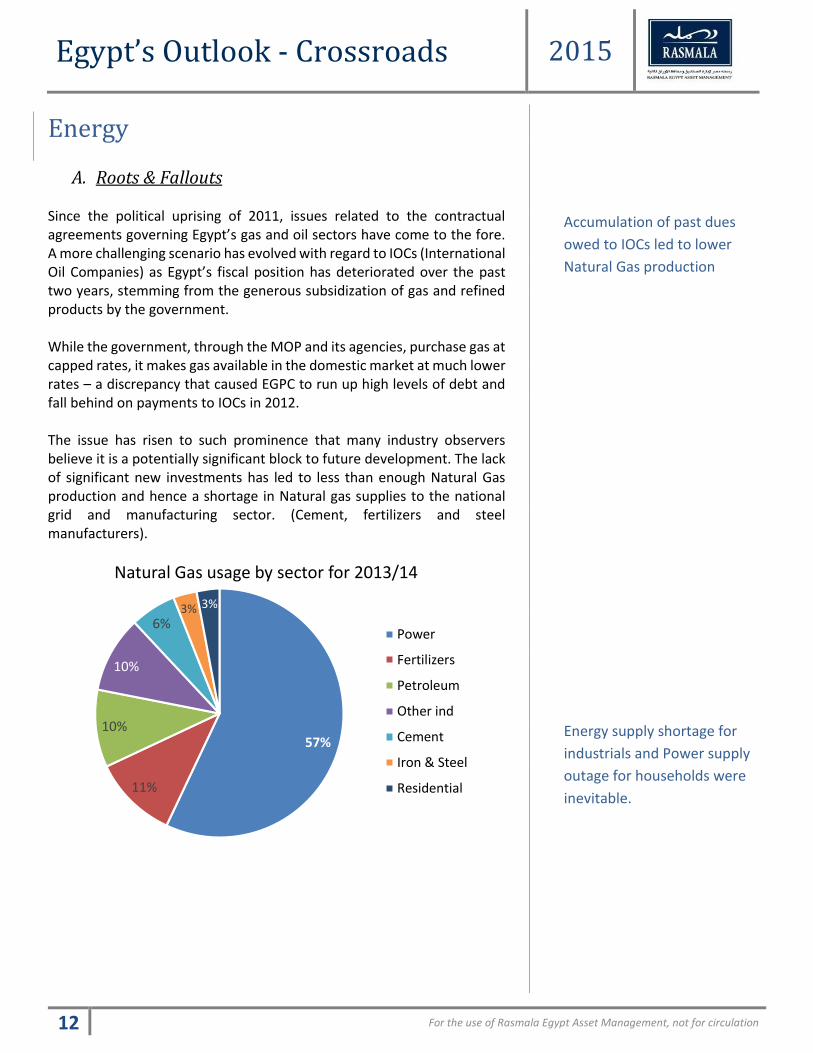

The issue has risen to such prominence that many industry observers believe it is a potentially significant block to future development. The lack of significant new investments has led to less than enough Natural Gas production and hence a shortage in Natural gas supplies to the national grid and manufacturing sector. (Cement, fertilizers and steel manufacturers).

57%

11%

10%

10%

6%3% 3%

Natural Gas usage by sector for 2013/14

Power

Fertilizers

Petroleum

Other ind

Cement

Iron & Steel

Residential

Accumulation of past dues

owed to IOCs led to lower

Natural Gas production

Energy supply shortage for

industrials and Power supply

outage for households were

inevitable.

Egypt’s Outlook - Crossroads 2015

13 For the use of Rasmala Egypt Asset Management, not for circulation

As per a petroleum ministry report, average natural gas production declined (as of June 2015) to 4.395 bcf/day down from 4.75 bcf/day in FY 2014 making the natural gas deficit stands little above 1 bcf/day (20% short of domestic demand of 5.5 bcf/day) compared to 700 mcf/day in March and a targeted 350 mcf/day.

B. Initiatives to resolve

The government launched a series of measures to address the dilemma:

IOC Past Dues:

The overall entitlements and past dues for the 9M 2014/2015 period amounted USD 12.7Bn. The government successfully paid USD 9.4Bn with the remaining USD 3.2Bn to be settled by 1H2016. The figure increased by USD 300Mn in August but the relative stability is ensuring the success of the government plan in paying the new commitments.

Oil & Gas:

The Hoegh Gallant floating storage and regasification unit (FSRU) from Norway's Hoegh LNG arrived off Ain Sukhna on the Gulf of Suez in April 2015 with an import capacity of 500 mcf/day equating to 9% of Egypt’s estimated 2015 gas production. Egypt has exported LNG in the past, but the Hoegh Gallant allowed the country to begin imports. Hoegh signed a five-year contract with Egypt in November 2014 to provide the import terminal and the country has since agreed to a number of LNG import deals. The government also announced on 3 August that it had commissioned a second Floating and Storage Regasification Unit (FSRU), the contract was awarded to BW Gas, with a contractual period of five years. The new terminal has the capacity of receiving 750 mcf/day, more than doubling the country’s gas import capacity to 1.25 bcf/day. The terminal arrived at Ain al Sokhna port in October and is to start pumping gas into the national grid by end of the same month. The second unit will be devoted mostly to the industrial sector to cover shortfalls, mostly in the fertilizer, steel and cement sectors.

The EGAS board has agreed to import 35 LNG cargoes from Russia's Gazprom over five years. This year and next it has agreed to take 33 cargoes from Trafigura, 9 from Vitol, 7 from Noble and 6 from Algeria's Sonatrach. In the 11th of June, Egypt received the first LNG cargo from Australia making the total shipments received by then to three. It’s important to highlight

The government launched a

series of initiatives to resolve

on both the Energy and Power

fronts.

Egypt’s Outlook - Crossroads 2015

14 For the use of Rasmala Egypt Asset Management, not for circulation

that the cost of the LNG that will be imported during FY2015/2016 will be around USD3.55 billion with Imports are likely to cost around USD 8.5/MMBTU on average.

At the occasion of the Economic Summit, the Ministry of Petroleum signed contracts worth USD 28.6Bn in addition to USD 50.4Bn MOUs & HOAs in the Energy sector to reduce the gap between exports and imports in this sector by year 2020. In total the additional capacity amounts to 24.5 million tons per annum of natural gas equivalent to 60% of estimated production in 2015. The major big contract was with the British petroleum Company worth USD12Bn to increase domestic natural gas production by 20-25%.

The government is planning to adjust the buying price of Natural Gas from the IOCs. In March, Egypt agreed with the German RWE DEA to raise the Natural Gas price to USD 3.5/MMBTU up from USD 2.5/MMBTU. Moreover, the negotiations to do the same with the Italians ENI & Edison yielded an upgrade in price to USD 5.88/MMBTU.

The Ministry of Petroleum plans for deregulating the natural gas market aiming to reduce the government’s role in the natural gas sector.

Egypt is to start distributing oil products via smart cards somewhere in 2H2016.

EGAS recently offered to supply 100% of fertilizer and steel companies’ natural gas needs by end of October through LNG imports at a new pricing formula, which will allow 50% of the new price to be set at USD9.00/mmbtu with the rest being set at prevailing industry prices.

ENI new Gas discovery:

ENI announced in August that it has made a supergiant gas discovery in the deep waters of Egypt. The discovery could hold a potential 30 tcf of gas (equivalent to 5.5 billion barrel of oil covering an area of 100 sqkm) representing 45% of Egypt’s current reserves (65.2 tcf currently). Moreover, ENI CEO said that the field could potentially hold 40 tcf, providing a further 11% boost to reserves.

Potential profits could amount to USD 74Mn after accounting for the recovery cost distributed as 65% for Egypt and 35% for ENI.

ENI announced a supergiant

discovery in the deep waters

of Egypt.

Egypt’s Outlook - Crossroads 2015

15 For the use of Rasmala Egypt Asset Management, not for circulation

Later in August, EGAS officials agreed with ENI to accelerate production of Natural Gas from Zohr to begin production of 700 mcf per day starting January 2017, with the production rate expected to reach 2.4 bcf per day by January 2018. Production should double to 5.1 bcf per day by January 2019 noting that the total investment cost in the field is estimated to range between USD 8Bn and USD 10Bn.

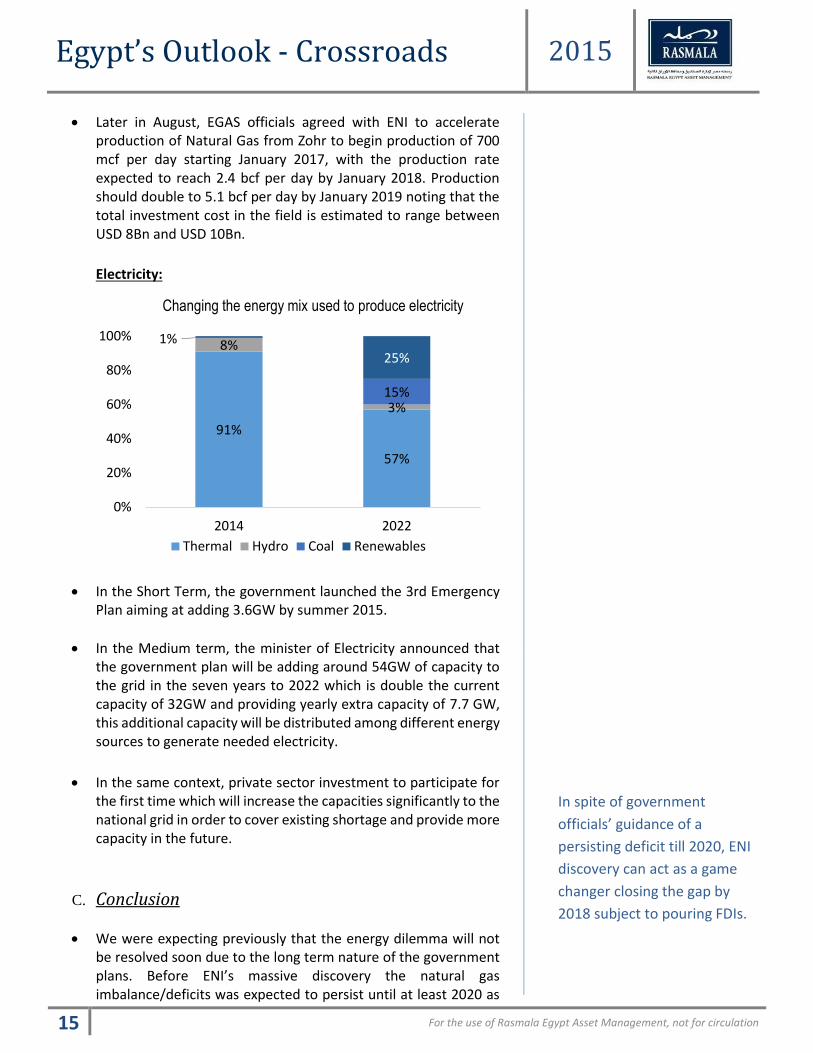

Electricity:

In the Short Term, the government launched the 3rd Emergency Plan aiming at adding 3.6GW by summer 2015.

In the Medium term, the minister of Electricity announced that the government plan will be adding around 54GW of capacity to the grid in the seven years to 2022 which is double the current capacity of 32GW and providing yearly extra capacity of 7.7 GW, this additional capacity will be distributed among different energy sources to generate needed electricity.

In the same context, private sector investment to participate for the first time which will increase the capacities significantly to the national grid in order to cover existing shortage and provide more capacity in the future.

C. Conclusion

We were expecting previously that the energy dilemma will not be resolved soon due to the long term nature of the government plans. Before ENI’s massive discovery the natural gas imbalance/deficits was expected to persist until at least 2020 as

91%

57%

8%

3%15%

1%

25%

0%

20%

40%

60%

80%

100%

2014 2022

Changing the energy mix used to produce electricity

Thermal Hydro Coal Renewables

In spite of government

officials’ guidance of a

persisting deficit till 2020, ENI

discovery can act as a game

changer closing the gap by

2018 subject to pouring FDIs.

Egypt’s Outlook - Crossroads 2015

16 For the use of Rasmala Egypt Asset Management, not for circulation

per government officials since the majority of the upstream gas projects were not due to come on stream until 2017 when BP’s major West Nile Delta project enter the production phase (700 mcf/day).

However, the new Natural Gas exploration can act as a game changer that might significantly boost Egypt’s production capacity and help close the supply demand gap before 2020. Should the acceleration plan materialize and accounting for the present LNG FSRU combined capacities of 1.25 bcf/day means that the demand supply gap which is at roughly 1-2 bcf at present can be closed by 2018. In this context, we should highlight that these massive production rates can be achieved if and only if significant investments are poured into the fields before production starts.

Gas shortages look likely to peak in 2016 according to experts estimates (24% deficit).The short term outlook will be strongly affected by the tradeoff between supplying natural gas to the electricity grid and supplying it to industrials. The issue is typically intensified in the summer season. Electricity outages this season , however, were evidently reduced and this can be attributed to:

Supplying the Electricity Grid with more Natural Gas at the

expense of the industrials. Industrials that were affected

the most are Steel and Fertilizers. Cement on the other

hand benefited from the government decision to provide

them with HFO instead of Natural Gas availing of the lower

international oil prices. Moreover, the industry will be

released from its conventional energy ties as the

conversion to coal is on its way.

Connection Startup of the 3rd Emergency Plan power

plants to the national grid. As mentioned earlier, the

Electricity ministry successfully added 3,600 MW to the

national grid.

In short, energy-intensive sectors are likely to continue

suffering from shortage in Natural Gas until 2017 with

few exceptions in cement sector due to the dependency

on coal.

Egypt’s Outlook - Crossroads 2015

17 For the use of Rasmala Egypt Asset Management, not for circulation

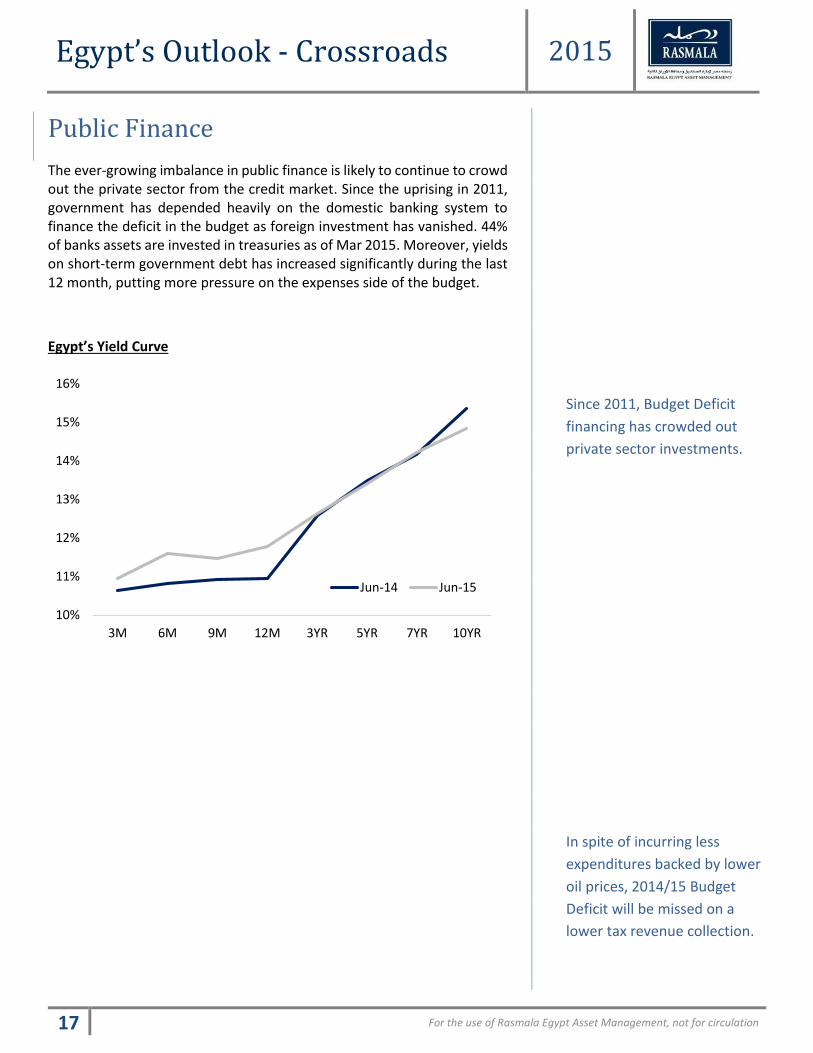

Public Finance

The ever-growing imbalance in public finance is likely to continue to crowd out the private sector from the credit market. Since the uprising in 2011, government has depended heavily on the domestic banking system to finance the deficit in the budget as foreign investment has vanished. 44% of banks assets are invested in treasuries as of Mar 2015. Moreover, yields on short-term government debt has increased significantly during the last 12 month, putting more pressure on the expenses side of the budget.

Egypt’s Yield Curve

10%

11%

12%

13%

14%

15%

16%

3M 6M 9M 12M 3YR 5YR 7YR 10YR

Jun-14 Jun-15

Since 2011, Budget Deficit

financing has crowded out

private sector investments.

In spite of incurring less

expenditures backed by lower

oil prices, 2014/15 Budget

Deficit will be missed on a

lower tax revenue collection.

Egypt’s Outlook - Crossroads 2015

18 For the use of Rasmala Egypt Asset Management, not for circulation

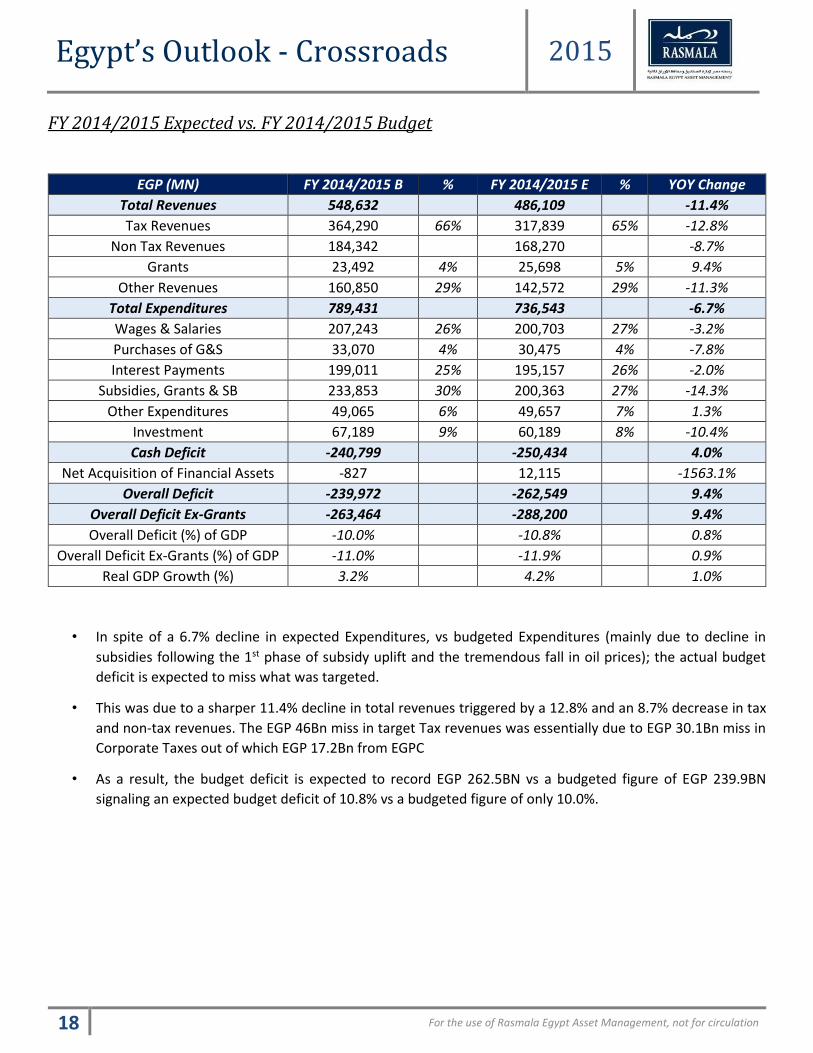

FY 2014/2015 Expected vs. FY 2014/2015 Budget

• In spite of a 6.7% decline in expected Expenditures, vs budgeted Expenditures (mainly due to decline in

subsidies following the 1st phase of subsidy uplift and the tremendous fall in oil prices); the actual budget

deficit is expected to miss what was targeted.

• This was due to a sharper 11.4% decline in total revenues triggered by a 12.8% and an 8.7% decrease in tax

and non-tax revenues. The EGP 46Bn miss in target Tax revenues was essentially due to EGP 30.1Bn miss in

Corporate Taxes out of which EGP 17.2Bn from EGPC

• As a result, the budget deficit is expected to record EGP 262.5BN vs a budgeted figure of EGP 239.9BN

signaling an expected budget deficit of 10.8% vs a budgeted figure of only 10.0%.

EGP (MN) FY 2014/2015 B % FY 2014/2015 E % YOY Change

Total Revenues 548,632 486,109 -11.4%

Tax Revenues 364,290 66% 317,839 65% -12.8%

Non Tax Revenues 184,342 168,270 -8.7%

Grants 23,492 4% 25,698 5% 9.4%

Other Revenues 160,850 29% 142,572 29% -11.3%

Total Expenditures 789,431 736,543 -6.7%

Wages & Salaries 207,243 26% 200,703 27% -3.2%

Purchases of G&S 33,070 4% 30,475 4% -7.8%

Interest Payments 199,011 25% 195,157 26% -2.0%

Subsidies, Grants & SB 233,853 30% 200,363 27% -14.3%

Other Expenditures 49,065 6% 49,657 7% 1.3%

Investment 67,189 9% 60,189 8% -10.4%

Cash Deficit -240,799 -250,434 4.0%

Net Acquisition of Financial Assets -827 12,115 -1563.1%

Overall Deficit -239,972 -262,549 9.4%

Overall Deficit Ex-Grants -263,464 -288,200 9.4%

Overall Deficit (%) of GDP -10.0% -10.8% 0.8%

Overall Deficit Ex-Grants (%) of GDP -11.0% -11.9% 0.9%

Real GDP Growth (%) 3.2% 4.2% 1.0%

Egypt’s Outlook - Crossroads 2015

19 For the use of Rasmala Egypt Asset Management, not for circulation

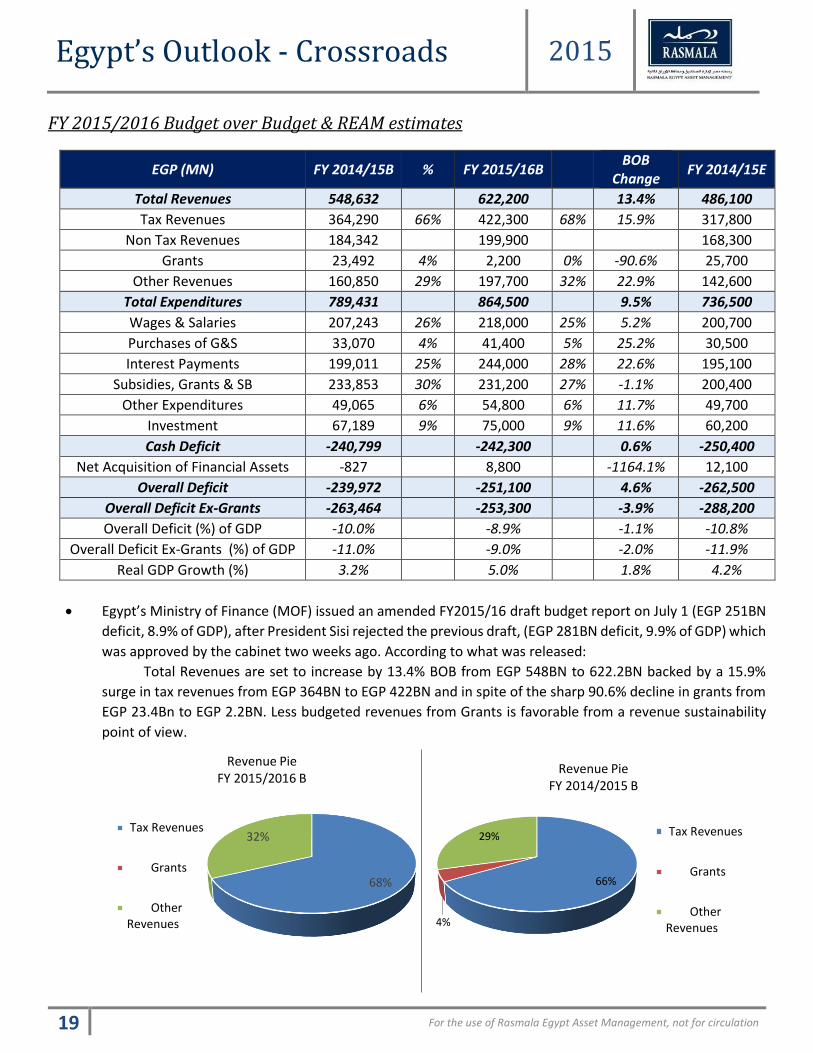

FY 2015/2016 Budget over Budget & REAM estimates

EGP (MN) FY 2014/15B % FY 2015/16B BOB

Change FY 2014/15E

Total Revenues 548,632 622,200 13.4% 486,100

Tax Revenues 364,290 66% 422,300 68% 15.9% 317,800

Non Tax Revenues 184,342 199,900 168,300

Grants 23,492 4% 2,200 0% -90.6% 25,700

Other Revenues 160,850 29% 197,700 32% 22.9% 142,600

Total Expenditures 789,431 864,500 9.5% 736,500

Wages & Salaries 207,243 26% 218,000 25% 5.2% 200,700

Purchases of G&S 33,070 4% 41,400 5% 25.2% 30,500

Interest Payments 199,011 25% 244,000 28% 22.6% 195,100

Subsidies, Grants & SB 233,853 30% 231,200 27% -1.1% 200,400

Other Expenditures 49,065 6% 54,800 6% 11.7% 49,700

Investment 67,189 9% 75,000 9% 11.6% 60,200

Cash Deficit -240,799 -242,300 0.6% -250,400

Net Acquisition of Financial Assets -827 8,800 -1164.1% 12,100

Overall Deficit -239,972 -251,100 4.6% -262,500

Overall Deficit Ex-Grants -263,464 -253,300 -3.9% -288,200

Overall Deficit (%) of GDP -10.0% -8.9% -1.1% -10.8%

Overall Deficit Ex-Grants (%) of GDP -11.0% -9.0% -2.0% -11.9%

Real GDP Growth (%) 3.2% 5.0% 1.8% 4.2%

Egypt’s Ministry of Finance (MOF) issued an amended FY2015/16 draft budget report on July 1 (EGP 251BN

deficit, 8.9% of GDP), after President Sisi rejected the previous draft, (EGP 281BN deficit, 9.9% of GDP) which

was approved by the cabinet two weeks ago. According to what was released:

Total Revenues are set to increase by 13.4% BOB from EGP 548BN to 622.2BN backed by a 15.9%

surge in tax revenues from EGP 364BN to EGP 422BN and in spite of the sharp 90.6% decline in grants from

EGP 23.4Bn to EGP 2.2BN. Less budgeted revenues from Grants is favorable from a revenue sustainability

point of view.

68%

32%

Revenue PieFY 2015/2016 B

Tax Revenues

Grants

OtherRevenues

66%

4%

29%

Revenue PieFY 2014/2015 B

Tax Revenues

Grants

OtherRevenues

Egypt’s Outlook - Crossroads 2015

20 For the use of Rasmala Egypt Asset Management, not for circulation

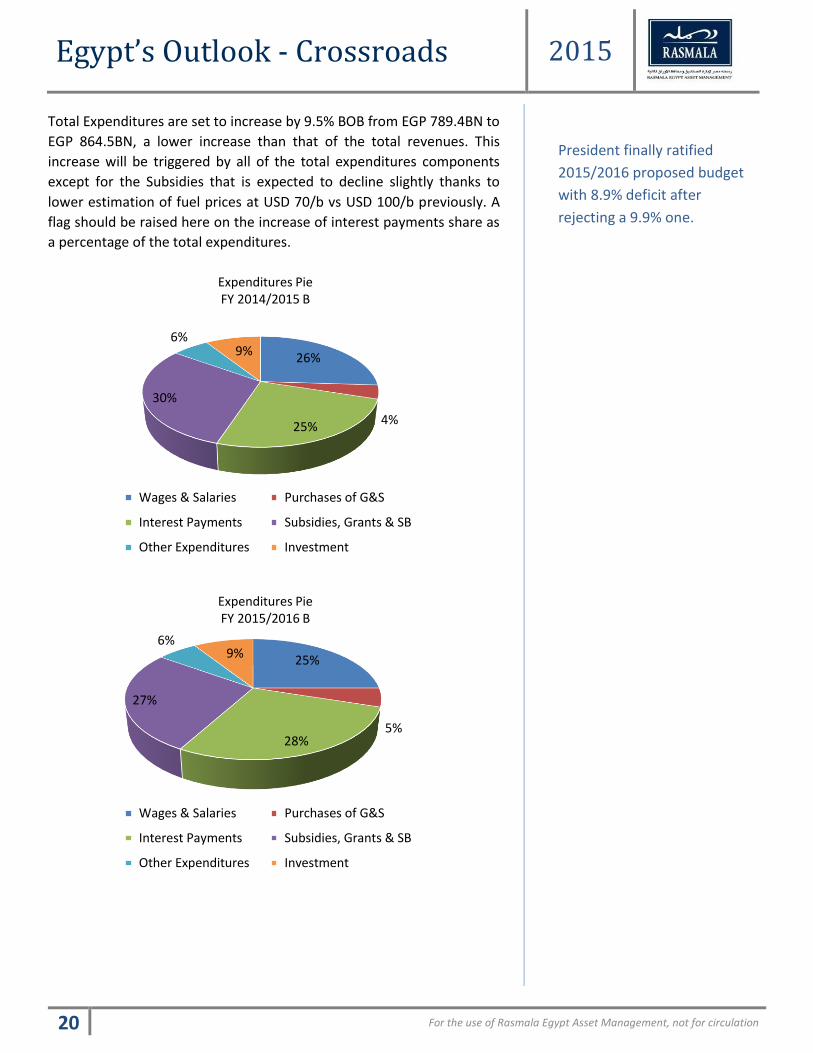

Total Expenditures are set to increase by 9.5% BOB from EGP 789.4BN to

EGP 864.5BN, a lower increase than that of the total revenues. This

increase will be triggered by all of the total expenditures components

except for the Subsidies that is expected to decline slightly thanks to

lower estimation of fuel prices at USD 70/b vs USD 100/b previously. A

flag should be raised here on the increase of interest payments share as

a percentage of the total expenditures.

26%

4%25%

30%

6%9%

Expenditures PieFY 2014/2015 B

Wages & Salaries Purchases of G&S

Interest Payments Subsidies, Grants & SB

Other Expenditures Investment

25%

5%28%

27%

6%9%

Expenditures Pie FY 2015/2016 B

Wages & Salaries Purchases of G&S

Interest Payments Subsidies, Grants & SB

Other Expenditures Investment

President finally ratified

2015/2016 proposed budget

with 8.9% deficit after

rejecting a 9.9% one.

Egypt’s Outlook - Crossroads 2015

21 For the use of Rasmala Egypt Asset Management, not for circulation

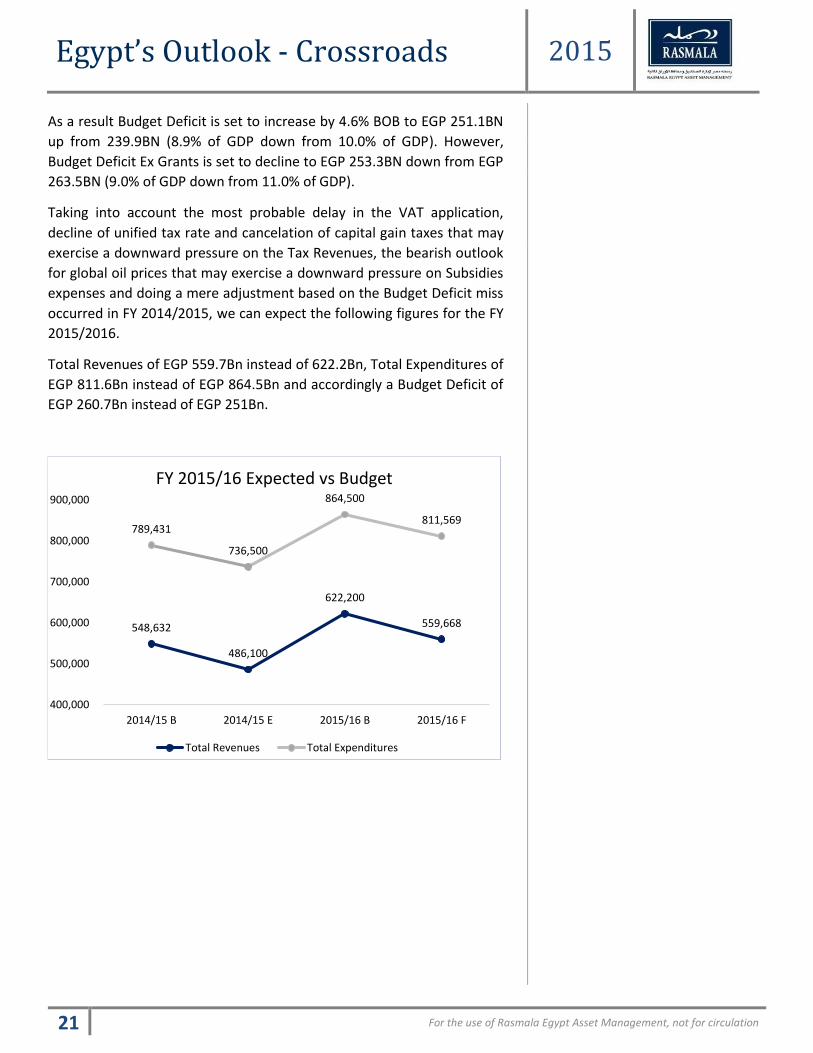

As a result Budget Deficit is set to increase by 4.6% BOB to EGP 251.1BN

up from 239.9BN (8.9% of GDP down from 10.0% of GDP). However,

Budget Deficit Ex Grants is set to decline to EGP 253.3BN down from EGP

263.5BN (9.0% of GDP down from 11.0% of GDP).

Taking into account the most probable delay in the VAT application,

decline of unified tax rate and cancelation of capital gain taxes that may

exercise a downward pressure on the Tax Revenues, the bearish outlook

for global oil prices that may exercise a downward pressure on Subsidies

expenses and doing a mere adjustment based on the Budget Deficit miss

occurred in FY 2014/2015, we can expect the following figures for the FY

2015/2016.

Total Revenues of EGP 559.7Bn instead of 622.2Bn, Total Expenditures of

EGP 811.6Bn instead of EGP 864.5Bn and accordingly a Budget Deficit of

EGP 260.7Bn instead of EGP 251Bn.

548,632

486,100

622,200

559,668

789,431

736,500

864,500

811,569

400,000

500,000

600,000

700,000

800,000

900,000

2014/15 B 2014/15 E 2015/16 B 2015/16 F

FY 2015/16 Expected vs Budget

Total Revenues Total Expenditures

Egypt’s Outlook - Crossroads 2015

22 For the use of Rasmala Egypt Asset Management, not for circulation

Miscellaneous thoughts about 2015/2016 Budget

Revenues

• Tax revenues should grow by EGP 104.5Bn compared to what is

expected in FY 2014/2015 backed by:

o A unified corporate tax law of 22.5%: The tax law

specifying the new 22.5% rate has not, however, been

issued by the president bearing in mind that the ministry

also said that the government would unify the tax rate on

special economic zones to 22.5% up from 10% at present.

o VAT Application: MOF said in its release that it would

apply VAT in FY 2015/2016 without giving a timeline nor

an estimated net increase in revenues due to its

application. As per a latter announcement by the head of

taxing authority VAT is expected to generate EGP 30BN by

next year.

o Complete Application of Real Estate Tax: Real Estate Tax

should record EGP 3.5Bn in 2015/2016 up from 0.9Bn

expected in FY 2014/2015.

o New Custom Law: increasing collections through more

monitoring.

o Economic Improvement: Implying higher corporate profit

and taxes.

• Non Tax revenues should grow by EGP 31.6Bn compared to what

is expected in FY 2014/2015 backed by:

o Full application of the Mining Law: With EGP, 10BN

expected proceeds.

o Channeling more profits from CBE, EGPC and Gvt Public

Sector entities: amounting to EGP 102BN in FY 2015/2016.

o Other Proceeds: from industrial licenses issuances and

land disputes settlement.

Egypt’s Outlook - Crossroads 2015

23 For the use of Rasmala Egypt Asset Management, not for circulation

Expenditures

• In spite of increasing EGP 17.3Bn in absolute terms, Wages and

Salaries are declining slightly as a percentage of total expenditures

(25% in FY 2015/2016 vs. 27% in FY 2014/2015) and as a

percentage of GDP (7.7% in FY 2015/2016 vs. 8.3% in FY

2014/2015).

• There was no mention of any energy subsidy cuts as the decrease

in spending will be purely a function of a full year impact of low

international oil prices.

• Fuel subsidies are estimated at EGP 62BN in FY 2015/2016 down

from an expected figure of EGP 70BN in FY 2014/2015 and EGP

100BN budgeted in the same year.

• The significant 22.6% increase in interest payments was a result of

the increasing Public Debt Level to finance budget deficit of higher

than 10% of GDP since FY 2010/2011.

It is important here to highlight that the interest payments are not

only a function of Debt Level as they also depend on the Interest

Rate Level.

Inflationary pressures are likely to increase over the coming few

months given the EGP devaluation round and the planned

implementation of the VAT. This will leave the CBE with no option

but to hike interest rates to control inflation. The fact that may

threaten the realization of the target deficit set by the

government.

• Contribution to Pension Funds will witness a tremendous 57%

increase to EGP 52.5Bn in FY 2015/2016 vs. EGP 33.2Bn in FY

2013/2014.

• Health, Education and scientific research will enjoy a 12.8% BOB

increase to EGP 159.9BN but still lower at 5.7% of GDP than the

10-12% target that should be reached by FY 2016/2017. The figure

can reach 6.8% of GDP if we added the indirect spending on health

and education.

• Public spending will continue on track enjoying an 11.6% BOB

increase to EGP 75BN (2.7% of GDP) out of which EGP 55BN

financed by revenues while the remaining financed by grants, debt

and self-finance. However, the figure as a percentage of GDP is still

lower than those budgeted in Mubarak era.

Egypt’s Outlook - Crossroads 2015

24 For the use of Rasmala Egypt Asset Management, not for circulation

Other

• The MOF release insisted that in spite of the improvement of FY

2015/2016 Budget Deficit in absolute and relative terms than what

is expected in FY 2014/2015, this would not come at the expense

of the poor.

• Real GDP growth is likely to grow by 5% in FY 2015/2016 compared

to 4.2% estimated in FY 2014/2015 and 3.2% budgeted in the same

year.

• Public Debt is likely to decline to EGP 2.6TN (90% of GDP) in FY

2015/2016 down from EGP 92.2% of GDP in FY 2014/2015 and

should decline to 80-85% by 2018/2019.

• Total Financing Needs are expected to record EGP 1.34TN (EGP

1,095Bn debt settlement + EGP 251Bn deficit) in FY 2015/2016

that are likely to be financed by Treasury securities.

Our View:

• FY 2015/2016 Budget figures are likely to be missed on many

fronts, first: a most probable delay in VAT application, second:

decrease of the unified tax rate, third: the cancelation of capital

gain taxes, fourth: a more bearish outlook over oil prices, fifth: the

targeted budget deficit has been already missed in FY2014/2015

hitting the credibility of the government figures and finally, the

very short time interval between the 1st draft refused by the

president and the 2nd approved one raising questions on the

validity of these almost overnight amendments. Moreover, the

figures may be distorted again should the CBE intervene to raise

interest rates again to contain inflation waves that may blow

subsequent to EGP devaluation and VAT application.

• A Newspaper revealed according to unidentified sources that the

actual budget deficit for the fiscal year 2014/2015 recorded EGP

299Bn vs a budgeted figure of EGP 240Bn. This was attributed by

the same sources to a sharp decline in Revenues by EGP 124Bn to

EGP 425Bn more than offsetting a better cost management on the

Expenditures side. The below estimate figure stemmed 50% from

a lower tax revenues and 50% from a lower non tax revenues.

Meanwhile, Expenditures recorded EGP 713Bn cutting thus an EGP

76Bn from the budgeted figure mainly due to the lower global oil

prices leading to a decline in cost of subsidies. If we took into

consideration these unofficial figures, our estimation for FY

2015/2016 budget deficit can be amended to EGP 304Bn instead

of the budgeted EGP 251Bn representing 10.8% of GDP instead of

the targeted 8.9%.

However, VAT delay, decline of

unified tax rate, cancelation of

capital gain and a probable

interest rate increase are likely

to again lead to a target miss.

Egypt’s Outlook - Crossroads 2015

25 For the use of Rasmala Egypt Asset Management, not for circulation

Geopolitics

Egypt has launched limited air strikes on ISIS - related sect in Libya in a

response to murdering Egyptian citizens in February 2015. In Yemen, Egypt

has explicitly participated in a Saudi-led coalition against rebels. In March,

Egypt re-initiated the Joint Arab Military Force pact as a vehicle for future

participation in any potential military threat. Moreover, we understand

that Egypt will be active party defending Arab’s interest in face of Iran’s

potential threats. On the other hand, the conflict between Egypt and Saudi

Arabia over the Syria’s tragedy is not a speculation anymore.

Apart from the Libyan front, Egypt has no land borders with the current

regional confrontations. On the Eastern side, the relations with Israel is

not a concern as both countries have honored the peace accord since

1979. Moreover, we believe the situation in Libya will not require another

military action.

Accordingly, Egypt is in a relatively safer position than many

neighborhoods, which makes it a potential destination for regional

investment that are looking for more politically stable markets.

Investment Application

We still hold our medium term positive outlook for Egyptian equities

though the near term negative obstacles that are facing the private

investment activities. In fact, the decline in stock prices in the first 9

months of 2015 is a catalyst for our stance as valuation became more

attractive.

While we have a potential ease of energy dilemma in 2017 but the

shortage in the FX liquidity is more pressing from foreign investment

perspective. The scenario of managed devaluation of EGP is not likely to

trigger portfolio inflows unless coupled with a sharp recovery in FDI of

more than US$ 10 billion in the next 12 month.

We believe portfolio inflows will be critical to ease the FX shortage and to

reduce the cost of government debt, hence lowering the budget deficit.

Meanwhile, pockets of value still hold. Infrastructure-related companies

such as Sewedy and Orascom Construction are attractive. Cement sector

players that fully converted to coal are offering attractive entry to a

lucrative industry. Real Estate developers and banks will maintain their

ranks at our top picks list.