electricity technology in a carbon-constrained future · electricity technology in a...

TRANSCRIPT

Electricity Technology in a Carbon-Constrained Future

Utah Climate Change SymposiumMay 8, 2007

Bryan Hannegan, Ph.D. Vice President - Environment

2© 2007 Electric Power Research Institute, Inc. All rights reserved.

Presentation Objective

Provide a factual framework for discussing:

I. Generation technologies and investment decisions in a world with carbon constraints

II. R&D needs to achieve a low-cost, low-carbon portfolio of electricity technologies

III. Technical feasibility of using this portfolio of technologies to reduce U.S. electric sector CO2 emissions

IV. Economic implications of achieving significant CO2 reductions with/without low-cost, low-carbon technologies

3© 2007 Electric Power Research Institute, Inc. All rights reserved.

Pulverized Coal

30

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2 , $/metric ton

Levelized Cost of Electricity, $/MWh

2010 - 2015

PC

Rev. 1Q2007

Determine LCOE (capital cost, O&M, fuel)

Adjust for CO2 costs: 0.8 Tons CO2 /MWh X $50/Ton = +$40/MWh

4© 2007 Electric Power Research Institute, Inc. All rights reserved.

Natural Gas Combined Cycle

30

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2 , $/metric ton

Levelized Cost of Electricity, $/MWh

NGCC@$8

NGCC@$4

2010 - 2015

NGCC@$6

Rev. 1Q2007

0.4 Tons CO2 /MWh X $50/Ton = +$20/MWh

5© 2007 Electric Power Research Institute, Inc. All rights reserved.

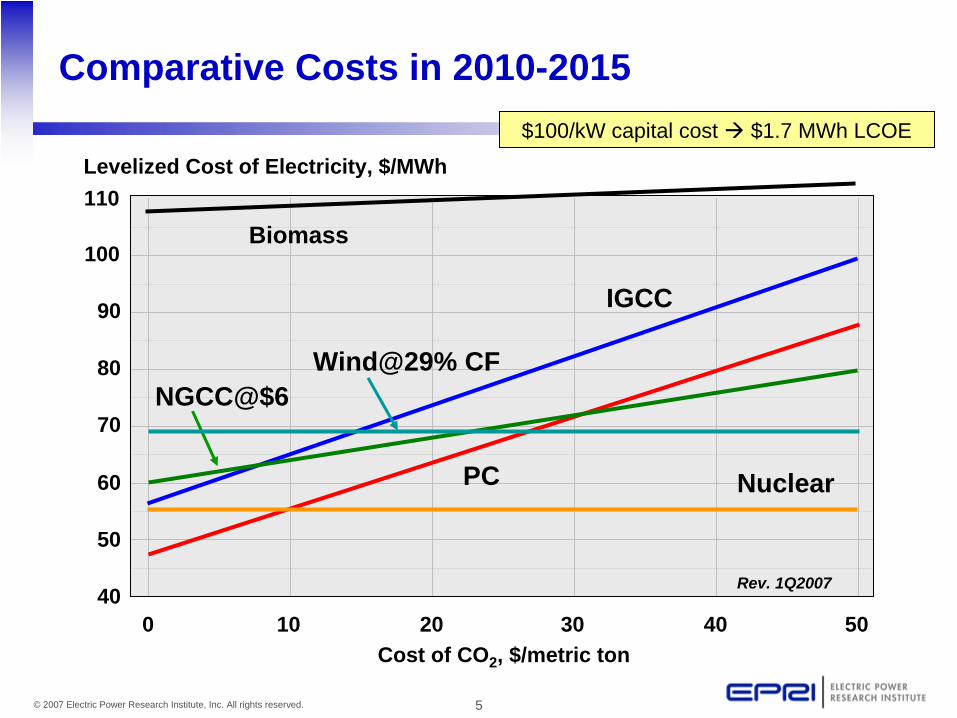

Comparative Costs in 2010-2015

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2 , $/metric ton

Levelized Cost of Electricity, $/MWh

Wind@29% CF

PC

IGCC

Biomass

Rev. 1Q2007

110

Nuclear

NGCC@$6

$100/kW capital cost $1.7 MWh LCOE

6© 2007 Electric Power Research Institute, Inc. All rights reserved.

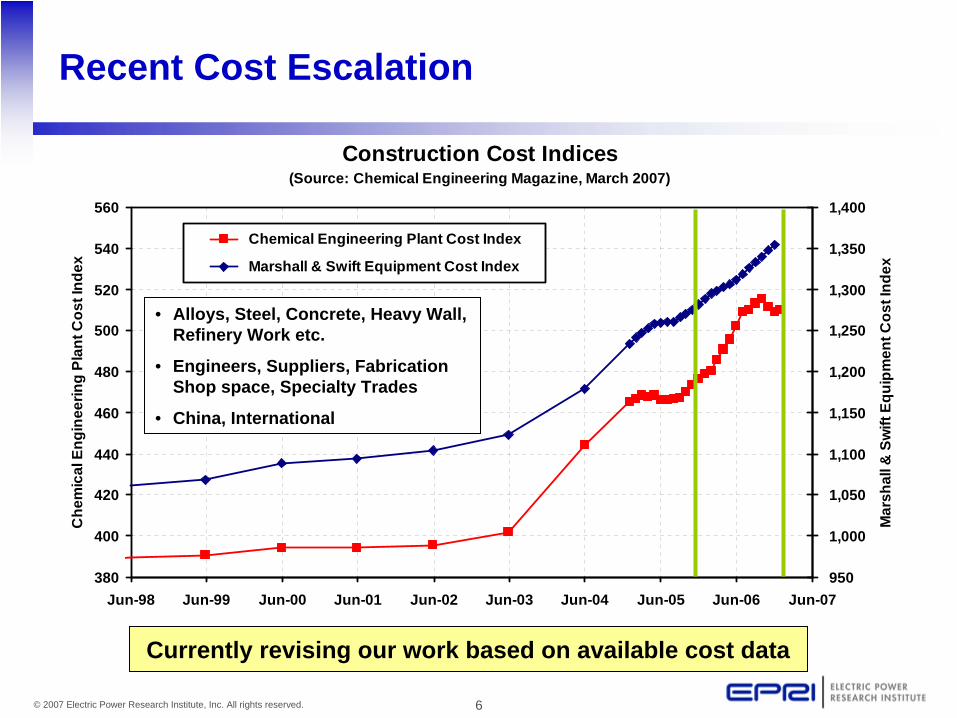

Recent Cost Escalation

Construction Cost Indices(Source: Chemical Engineering Magazine, March 2007)

380

400

420

440

460

480

500

520

540

560

Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07

Che

mic

al E

ngin

eerin

g Pl

ant C

ost I

ndex

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

Mar

shal

l & S

wift

Equ

ipm

ent C

ost I

ndex

Chemical Engineering Plant Cost Index

Marshall & Swift Equipment Cost Index

• Alloys, Steel, Concrete, Heavy Wall, Refinery Work etc.

• Engineers, Suppliers, Fabrication Shop space, Specialty Trades

• China, International

Currently revising our work based on available cost data

7© 2007 Electric Power Research Institute, Inc. All rights reserved.

Near-Term Implications

• New advanced light water reactors have cost advantage, but unlikely to enter operation until after 2015

• Renewables unlikely to extend beyond mandated requirement due to poor comparative economics– Exception is good wind with tax incentives (but limited in scale)

• As a result, most new base-load generation will utilize fossil technologies without CO2 capture and storage– PC vs. IGCC economics a function of coal type, other factors – Gas vs. coal choice depends on future gas prices, capital costs

Very limited opportunity for significant economic CO2 reduction!!!

8© 2007 Electric Power Research Institute, Inc. All rights reserved.

Presentation Objective

Provide a factual framework for discussing:

I. Generation technologies and investment decisions in a world with carbon constraints

II. R&D needs to achieve a low-cost, low-carbon portfolio of electricity technologies

III. Technical feasibility of using this portfolio of technologies to reduce U.S. electric sector CO2 emissions

IV. Economic implications of achieving significant CO2 reductions with/without low-cost, low-carbon technologies

9© 2007 Electric Power Research Institute, Inc. All rights reserved.

Key Technology Challenges

1. Smart grids and communications infrastructures to enable end-use efficiency and demand response, distributed generation, and PHEVs.

2. A grid infrastructure with the capacity and reliability to operate with 20-30% intermittent renewables in specific regions.

3. Significant expansion of nuclear energy enabled by continued safe and economic operation of existing nuclear fleet; and a viable strategy for managing spent fuel.

4. Commercial-scale coal-based generation units operating with 90+% CO2 capture and storage in a variety of geologies.

Significant cost-effective CO2 reductions from the U.S. electric sector will require ALL of the following technology advances:

10© 2007 Electric Power Research Institute, Inc. All rights reserved.

Average Annual Funding R&D Gap

2007- 2011

2012- 2016

2017- 2021

2022- 2026

2027- 2031 Avg

ENABLE ENERGY EFFICIENCY & DER Smart grids and communications infrastructures to enable end-use efficiency and demand response, DER (i.e. Solar PV) and PHEVs. Improve equipment efficiency.

$310 $290 $240 $140 $120 $220

GRID INTEGRATION WITH RENEWABLESA grid infrastructure with the capacity and reliability to operate with 20-30% intermittent renewable generation in specific regions.

$400 $370 $330 $300 $300 $340

NUCLEAR Significant expansion of nuclear energy enabled by continued operation of the existing nuclear fleet and a viable strategy for managing spent fuel. Includes new RD&D for ALWR deployment support.

$170 $170 $170 $100 $100 $140

ADVANCED COAL, CO2 CAPTURE and STORAGE Commercial-scale coal-based generation units operating with ~90% CO2 capture and storage in a variety of geologies.

$480 $800 $800 $620 $400 $620

Total $1360 $1630 $1540 $1160 $920 $1320V3 ;4-19-07 HC

million $/yr

11© 2007 Electric Power Research Institute, Inc. All rights reserved.

Example: Dynamic Energy Management

12© 2007 Electric Power Research Institute, Inc. All rights reserved.

2007 2012 2017 20272022

Complete 5MW Chilled Ammonia Pilot (PC + CO2

capture)

Multiple full-scale demonstrations (Adv. PC + CO2

capture, Adv. IGCC)

Commercial availability of CO2

storage; all new coal plants capture/store

90% of CO2Advanced PC, IGCC efficiencies*

reach 33-35% Advanced PC, IGCC efficiencies*

reach 43-45%

Completion - DOE Regional Partnerships deployment phase

Completion of DOE Regional Partnerships validation phase

Completion - DOE Regional Partnerships site characterization

*These are target efficiencies for plants including CO2 capture

Timeline: Advanced Coal with CCS

13© 2007 Electric Power Research Institute, Inc. All rights reserved.

Comparative Costs in 2020-2025

30

40

50

60

70

80

90

100

0 10 20 30 40 50Cost of CO2 , $/metric ton

Levelized Cost of Electricity, $/MWh

NuclearWind@40%

Biomass

NGCC@$6

A Low-Cost, Low-Carbon Electricity Generation Portfolio

IGCC w/capture

PC w/capture

Rev. 1Q2007

14© 2007 Electric Power Research Institute, Inc. All rights reserved.

Presentation Objective

Provide a factual framework for discussing:

I. Generation technologies and investment decisions in a world with carbon constraints

II. R&D needs to achieve a low-cost, low-carbon portfolio of electricity technologies

III. Technical feasibility of using this portfolio of technologies to reduce U.S. electric sector CO2 emissions

IV. Economic implications of achieving significant CO2 reductions with/without low-cost, low-carbon technologies

15© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

U.S. Electricity Sector CO2 Emissions

• Base case from EIA “Annual Energy Outlook 2007”– includes some efficiency, new renewables, new nuclear– assumes no CO2 capture or storage due to high costs

Using EPRI deployment assumptions, calculate change in CO2 relative to EIA base case

16© 2007 Electric Power Research Institute, Inc. All rights reserved.

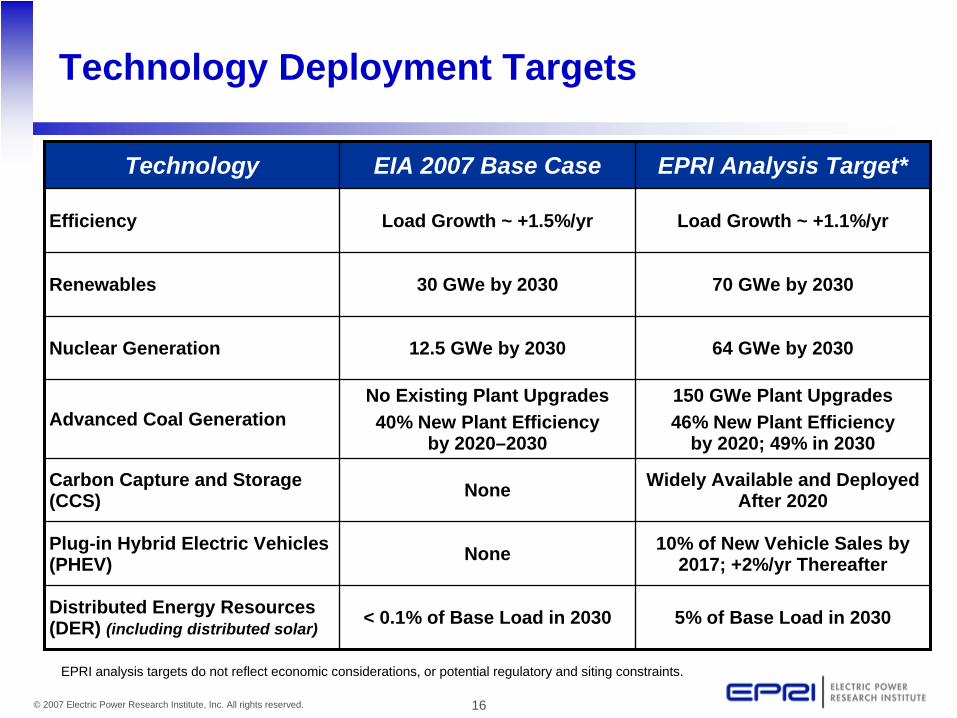

Technology Deployment Targets

Technology EIA 2007 Base Case EPRI Analysis Target*

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

Carbon Capture and Storage (CCS) None Widely Available and Deployed

After 2020

Plug-in Hybrid Electric Vehicles (PHEV) None 10% of New Vehicle Sales by

2017; +2%/yr Thereafter

Distributed Energy Resources (DER) (including distributed solar) < 0.1% of Base Load in 2030 5% of Base Load in 2030

EPRI analysis targets do not reflect economic considerations, or potential regulatory and siting constraints.

17© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

9% reduction in base load by 2030

Benefit of Achieving Efficiency Target

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

18© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns) EIA Base Case 2007

Benefit of Achieving Renewables Target

50 GWe new renewables by 2020; +2 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

19© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

Benefit of Achieving Nuclear Generation Target

24 GWe new nuclear by 2020; +4 GWe/yr thereafter

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

20© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

Benefit of Achieving Advanced Coal Target

46% efficiency by 2020, 49% efficiency by 2030

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

21© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

Benefit of Achieving CCS Target

After 2020, all new coal plants capture and store 90% of their CO2 emissions

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

22© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

Benefit of Achieving PHEV and DER Targets

5% shift to DER from base load in 2030PHEV sales = 10% by 2017; 30% by 2027

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

23© 2007 Electric Power Research Institute, Inc. All rights reserved.

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctric

Sec

tor

CO

2 Em

issi

ons

(mill

ion

met

ric to

ns)

EIA Base Case 2007

CO2 Reductions … Technical Potential*

Technology EIA 2007 Reference Target

Efficiency Load Growth ~ +1.5%/yr Load Growth ~ +1.1%/yr

Renewables 30 GWe by 2030 70 GWe by 2030

Nuclear Generation 12.5 GWe by 2030 64 GWe by 2030

Advanced Coal GenerationNo Existing Plant Upgrades40% New Plant Efficiency

by 2020–2030

150 GWe Plant Upgrades46% New Plant Efficiency

by 2020; 49% in 2030

CCS None Widely Deployed After 2020

PHEV None 10% of New Vehicle Sales by 2017; +2%/yr Thereafter

DER < 0.1% of Base Load in 2030 5% of Base Load in 2030

* Achieving all targets is very aggressive, but potentially feasible.

24© 2007 Electric Power Research Institute, Inc. All rights reserved.

U.S. Electricity Generation: 2030

Other Fossil1.7%

Natural Gas13.5%

Coal w/o CCS59.6%

Non-Hydro Renewables

3.0%Conventional Hydropower

5.6%

Nuclear Power16.6%

5406 TWh

Nuclear Power25.5%

Coal with CCS14.6%

Coal w/o CCS39.0%

Other Fossil0.6%

Natural Gas8.7%

Conventional Hydropower

4.9%

Non-Hydro Renewables

6.7%

5401 TWh

EIA Base Case* Advanced Technology Targets

* Base case from EIA “Annual Energy Outlook 2007”

25© 2007 Electric Power Research Institute, Inc. All rights reserved.

Presentation Objective

Provide a factual framework for discussing:

I. Generation technologies and investment decisions in a world with carbon constraints

II. R&D needs to achieve a low-cost, low-carbon portfolio of electricity technologies

III. Technical feasibility of using this portfolio of technologies to reduce U.S. electric sector CO2 emissions

IV. Economic implications of achieving significant CO2 reductions with/without low-cost, low-carbon technologies

26© 2007 Electric Power Research Institute, Inc. All rights reserved.

Preliminary Economic Results in Brief

Absent advanced electricity technologies, CO2 constraints result in • Price-induced conservation and “demand destruction”

• Fuel switching to natural gas

• Higher electricity prices

• High cost to U.S. economy

With advanced electricity technologies, CO2 constraints result in • Growth in electrification

• Continued use of coal (w/CCS) and nuclear

• Lower, more stable electricity prices

• 50-66% lower cost to U.S. economy

Results insensitive to CO2 constraints and capital cost assumptions