"energía eólica marina en el reino unido". ore catapult

TRANSCRIPT

Offshore Wind in the UK

Ignacio Marti

Innovation and Research Director, ORE Catapult

Intergune October 2016

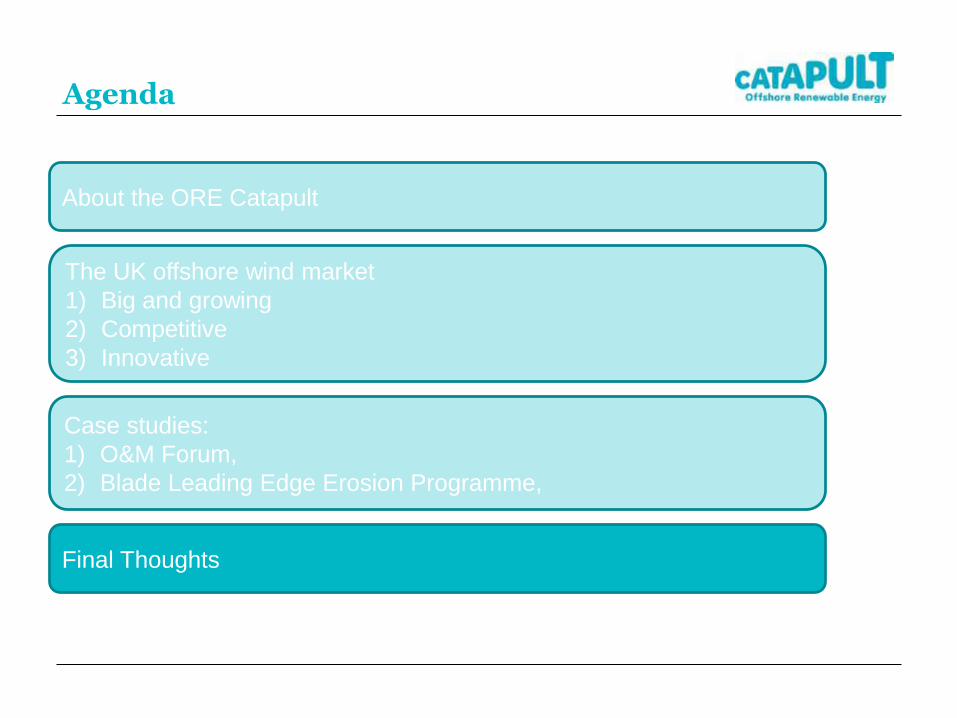

Agenda

About the ORE Catapult

The UK offshore wind market

1) Big and growing

2) Competitive

3) Innovative

Case studies:

1) O&M Forum,

2) Blade Leading Edge Erosion Programme,

Final Thoughts

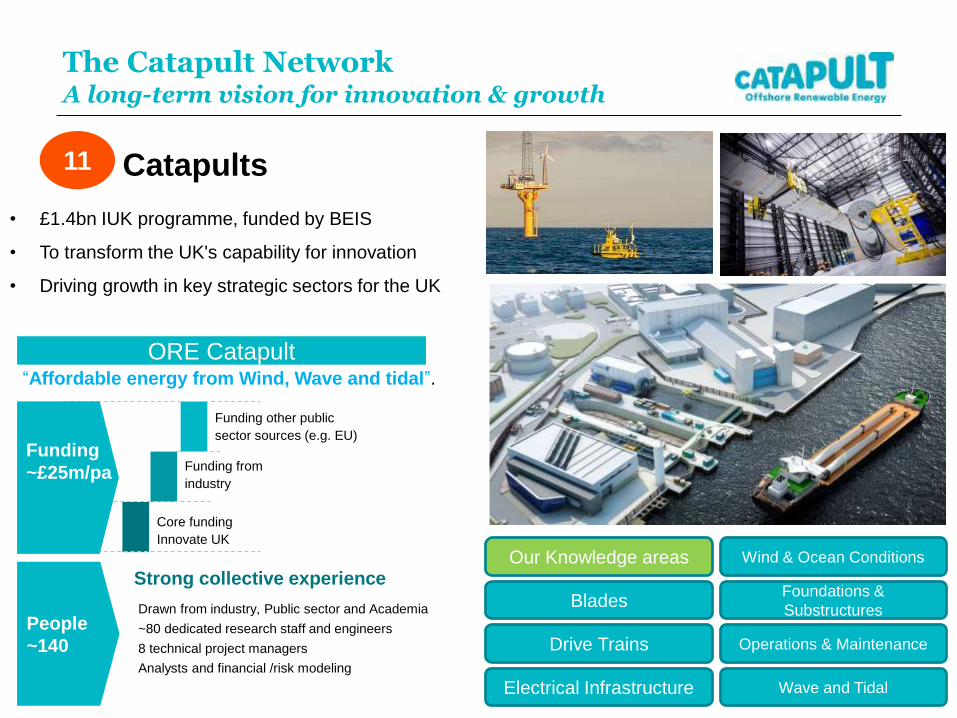

The Catapult NetworkA long-term vision for innovation & growth

• £1.4bn IUK programme, funded by BEIS

• To transform the UK's capability for innovation

• Driving growth in key strategic sectors for the UK

11 Catapults

Core funding

Innovate UK

Funding from

industry

Funding other public

sector sources (e.g. EU)

People

~140

Strong collective experience

Drawn from industry, Public sector and Academia

~80 dedicated research staff and engineers

8 technical project managers

Analysts and financial /risk modeling

ORE Catapult

Funding

~£25m/pa

“Affordable energy from Wind, Wave and tidal”.

Blades

Drive Trains

Electrical Infrastructure

Wind & Ocean Conditions

Foundations &

Substructures

Operations & Maintenance

Wave and Tidal

Our Knowledge areas

The ORE Catapult

Agenda

About the ORE Catapult

The UK offshore wind market

1) Big and growing

2) Competitive

3) Innovative

Case studies:

1) O&M Forum,

2) Blade Leading Edge Erosion Programme,

Final Thoughts

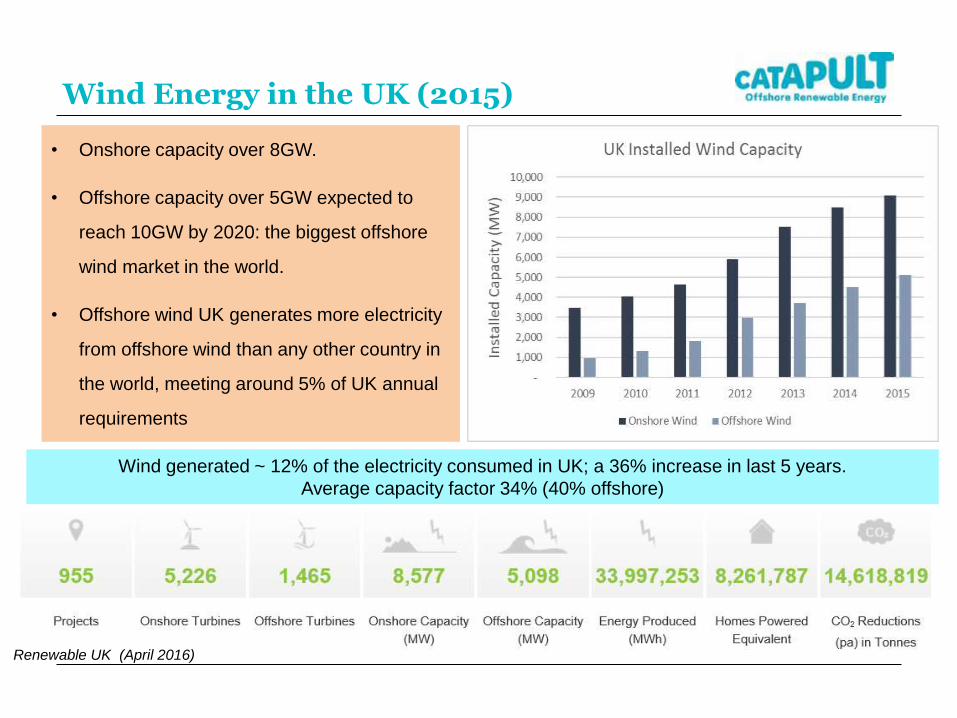

Wind Energy in the UK (2015)

• Onshore capacity over 8GW.

• Offshore capacity over 5GW expected to

reach 10GW by 2020: the biggest offshore

wind market in the world.

• Offshore wind UK generates more electricity

from offshore wind than any other country in

the world, meeting around 5% of UK annual

requirements

Renewable UK (April 2016)

Wind generated ~ 12% of the electricity consumed in UK; a 36% increase in last 5 years.

Average capacity factor 34% (40% offshore)

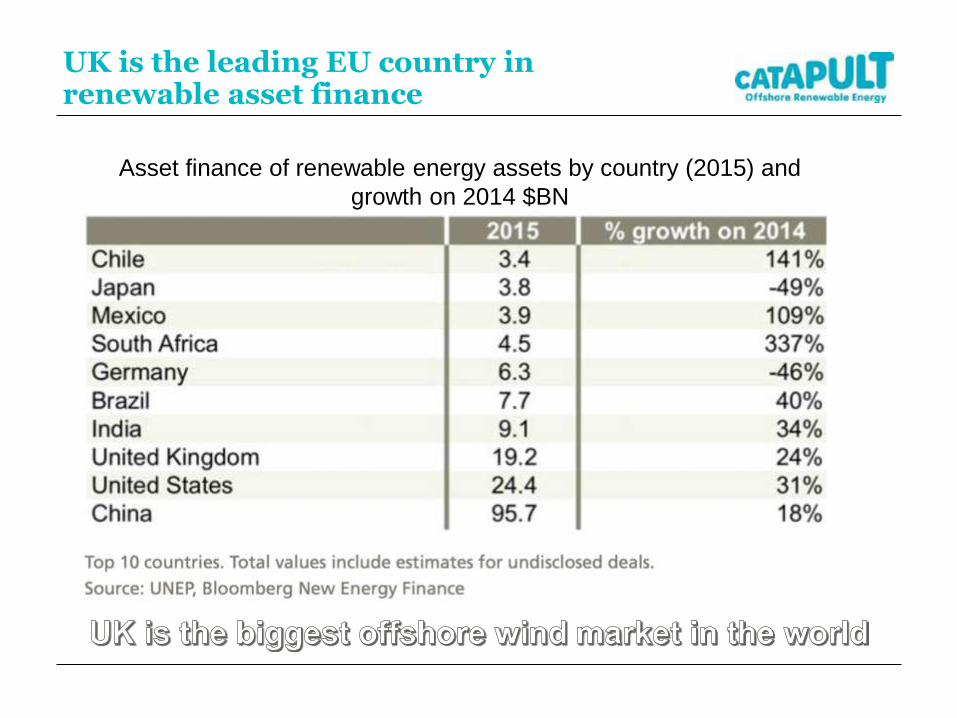

UK is the leading EU country in renewable asset finance

Asset finance of renewable energy assets by country (2015) and

growth on 2014 $BN

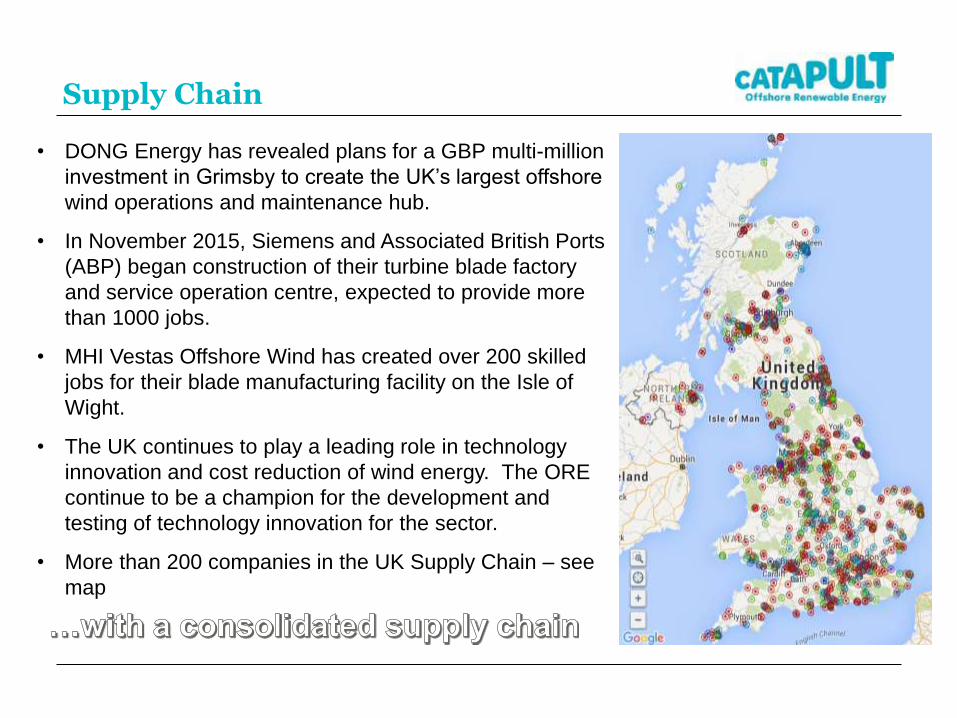

Supply Chain

• DONG Energy has revealed plans for a GBP multi-million

investment in Grimsby to create the UK’s largest offshore

wind operations and maintenance hub.

• In November 2015, Siemens and Associated British Ports

(ABP) began construction of their turbine blade factory

and service operation centre, expected to provide more

than 1000 jobs.

• MHI Vestas Offshore Wind has created over 200 skilled

jobs for their blade manufacturing facility on the Isle of

Wight.

• The UK continues to play a leading role in technology

innovation and cost reduction of wind energy. The ORE

continue to be a champion for the development and

testing of technology innovation for the sector.

• More than 200 companies in the UK Supply Chain – see

map

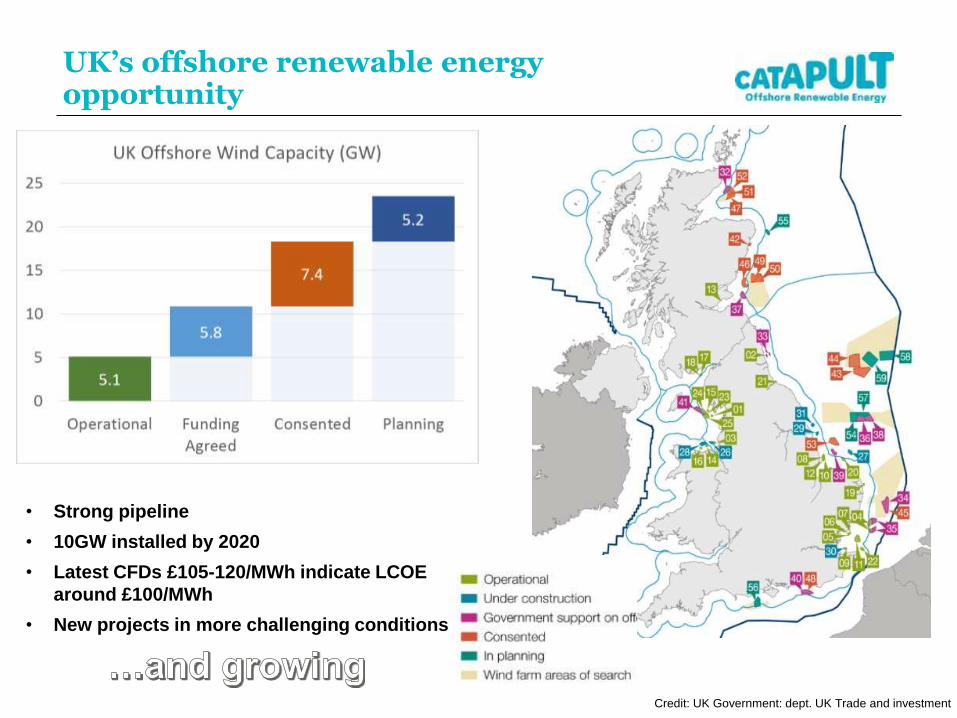

UK’s offshore renewable energy opportunity

• Strong pipeline

• 10GW installed by 2020

• Latest CFDs £105-120/MWh indicate LCOE

around £100/MWh

• New projects in more challenging conditions

Credit: UK Government: dept. UK Trade and investment

Cost Reduction Monitoring Framework

https://ore.catapult.org.uk/crmf

Our Cost Reduction Monitoring Framework:Creating confidence & informing priorities

Wind & ocean conditions

C 2% reduction

Electrical

infrastructure

C 2% reduction

Installation &

decommissioning

C 4% reduction

O&M

C 5-8% reduction Increase in Turbine Power Rating

C 11% reduction

Foundations & sub-structure C 4% reduction

Blades C 6% reduction

Drive trains C 2.4% reduction

Graphic courtesy of Babcock International

FID

2020

UK Supply chain and growth

• Each year ORE Catapult tracks cost

reduction on behalf of the industry

though financial “audit” and interviews

with the supply chain.

• The resultant “CRMF” is the dash

board which is used to inform where

we focus efforts

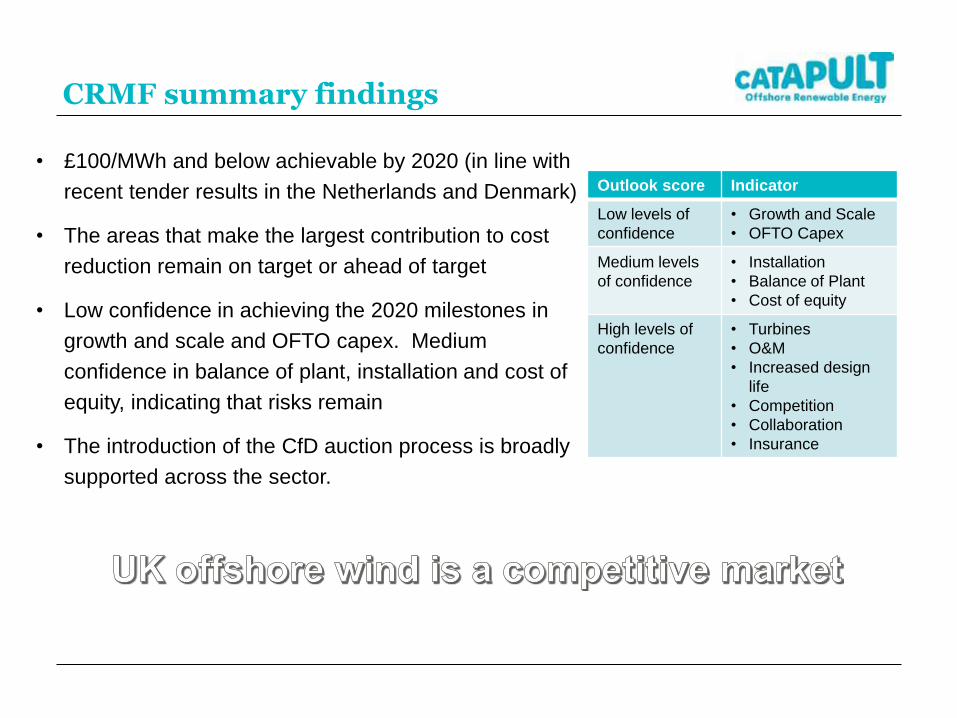

CRMF summary findings

• £100/MWh and below achievable by 2020 (in line with

recent tender results in the Netherlands and Denmark)

• The areas that make the largest contribution to cost

reduction remain on target or ahead of target

• Low confidence in achieving the 2020 milestones in

growth and scale and OFTO capex. Medium

confidence in balance of plant, installation and cost of

equity, indicating that risks remain

• The introduction of the CfD auction process is broadly

supported across the sector.

Outlook score Indicator

Low levels of

confidence

• Growth and Scale

• OFTO Capex

Medium levels

of confidence

• Installation

• Balance of Plant

• Cost of equity

High levels of

confidence

• Turbines

• O&M

• Increased design

life

• Competition

• Collaboration

• Insurance

Future cost of offshore wind

http://www.kic-innoenergy.com/reports/

LCOE reductions are driven by innovation

Source KIC Innoenergy & BVG

Agenda

About the ORE Catapult

The UK offshore wind market

1) Big and growing

2) Competitive

3) Innovative

Case studies:

1) O&M Forum,

2) Blade Leading Edge Erosion Programme,

Final Thoughts

Case study 1: O&M Forum

• Discussion forum with UK offshore wind

farm owner/operators

• Attended by offshore wind farm asset

managers and other key staff

• Valuable insight to help promote best

practice and shape ORE Catapult

activities

• Joint Industry Project on scheduled

maintenance excellence being developed

with forum members

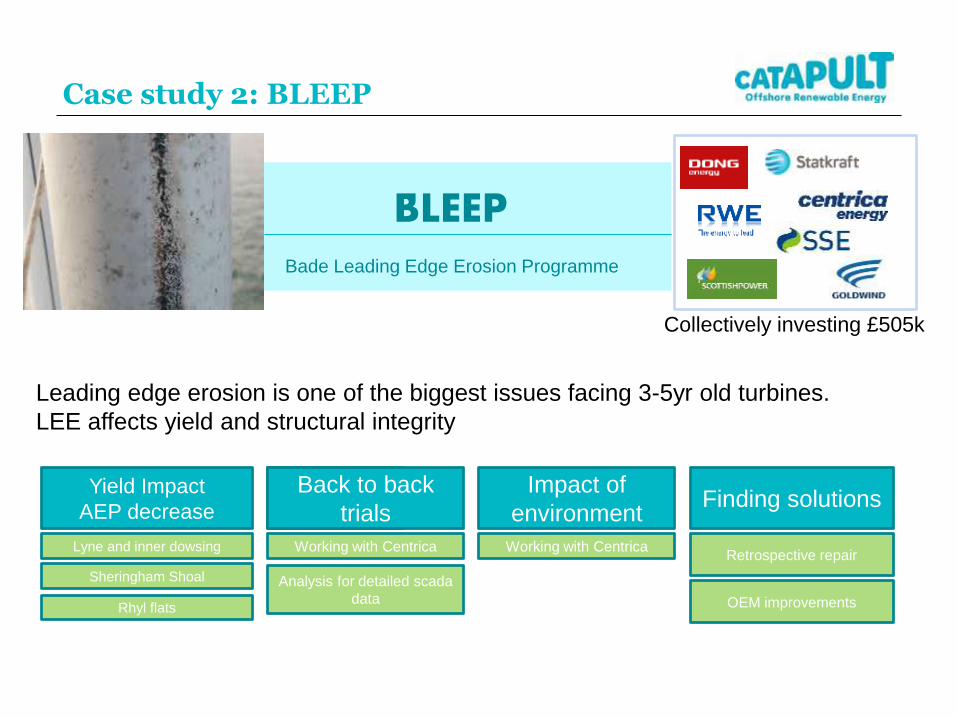

Case study 2: BLEEP

Collectively investing £505k

Yield Impact

AEP decrease

Lyne and inner dowsing

Sheringham Shoal

Rhyl flats

Back to

back trials

Analysis for detailed scada

data

Impact of

environment

Working with Centrica

Back to back

trials

Working with Centrica

Finding solutions

Retrospective repair

OEM improvements

Leading edge erosion is one of the biggest issues facing 3-5yr old turbines.

LEE affects yield and structural integrity

BLEEPBade Leading Edge Erosion Programme

Agenda

About the ORE Catapult

The UK offshore wind market

1) Big and growing

2) Competitive

3) Innovative

Case studies:

1) O&M Forum,

2) Blade Leading Edge Erosion Programme,

Final Thoughts

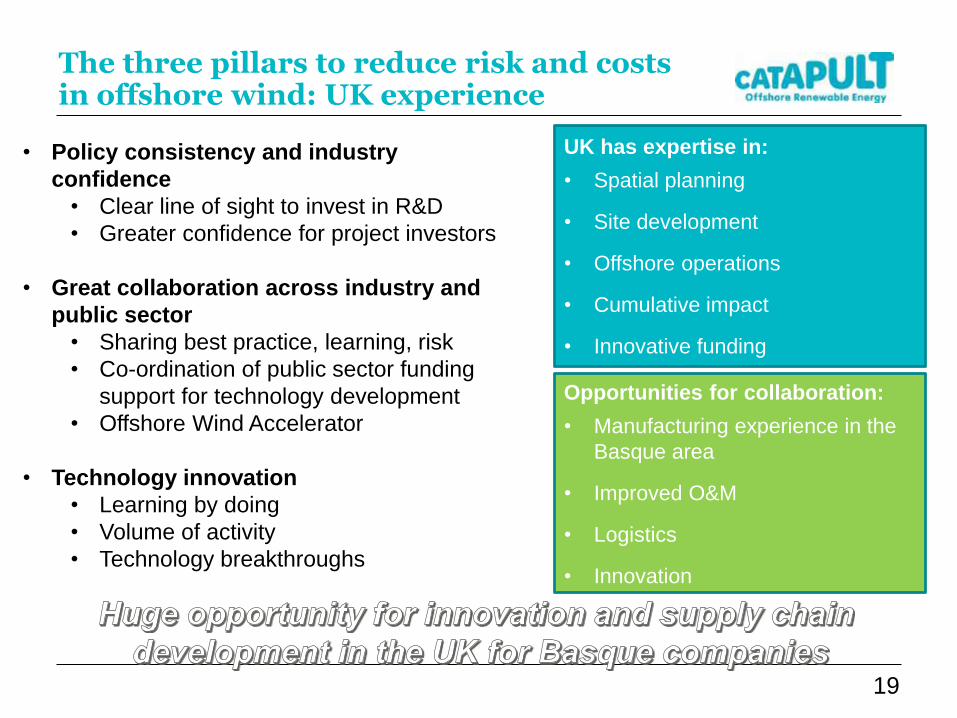

The three pillars to reduce risk and costs in offshore wind: UK experience

19

• Policy consistency and industry

confidence

• Clear line of sight to invest in R&D

• Greater confidence for project investors

• Great collaboration across industry and

public sector

• Sharing best practice, learning, risk

• Co-ordination of public sector funding

support for technology development

• Offshore Wind Accelerator

• Technology innovation

• Learning by doing

• Volume of activity

• Technology breakthroughs

UK has expertise in:

• Spatial planning

• Site development

• Offshore operations

• Cumulative impact

• Innovative funding

Opportunities for collaboration:

• Manufacturing experience in the

Basque area

• Improved O&M

• Logistics

• Innovation