eólica del guadiana, s.l. - saeta yield · eÓlica del guadiana, s.l. notes to financial...

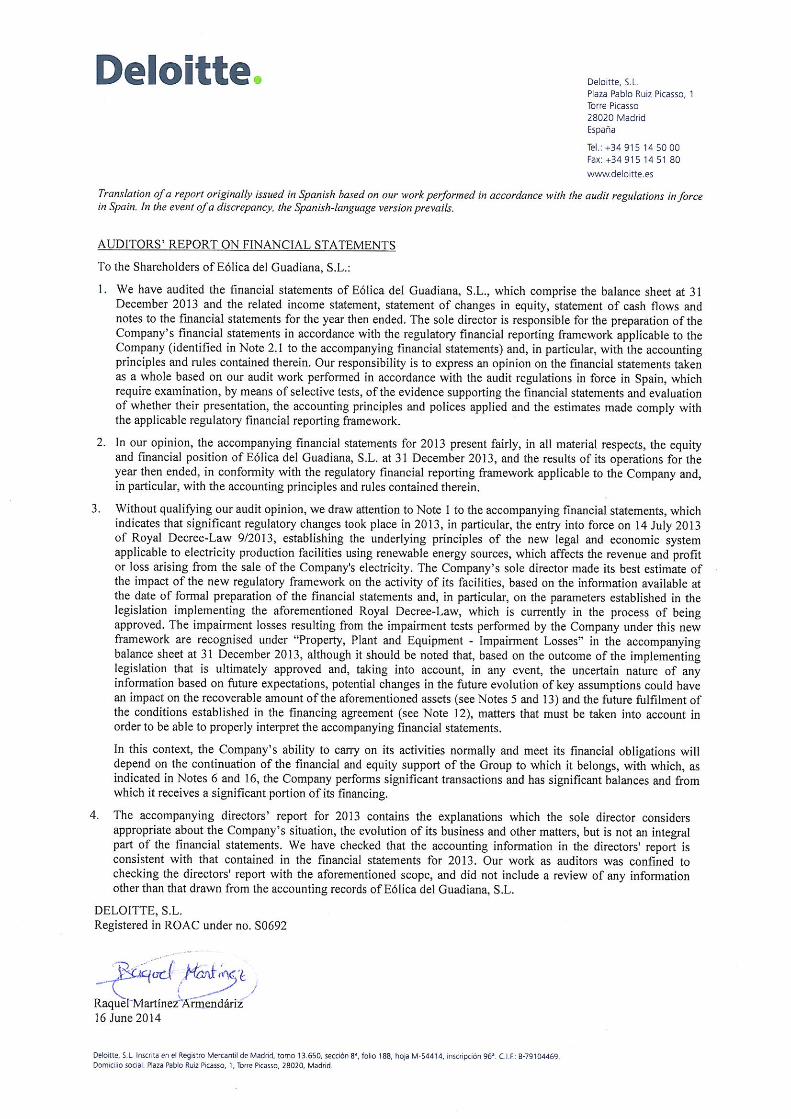

TRANSCRIPT

Eólica del Guadiana, S.L. Financial Statements and Directors’ Report for the year ended 31 December 2013

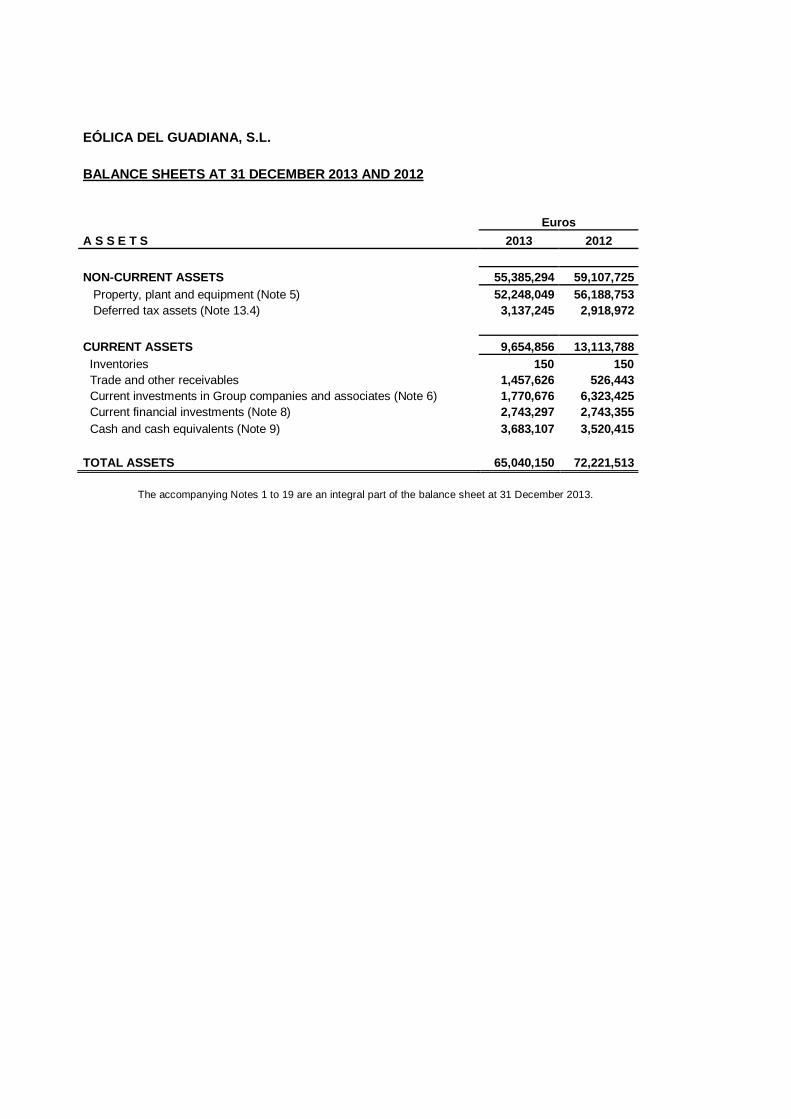

EÓLICA DEL GUADIANA, S.L.

BALANCE SHEETS AT 31 DECEMBER 2013 AND 2012

Euros

A S S E T S 2013 2012

NON-CURRENT ASSETS 55,385,294 59,107,725 Property, plant and equipment (Note 5) 52,248,049 56,188,753 Deferred tax assets (Note 13.4) 3,137,245 2,918,972

CURRENT ASSETS 9,654,856 13,113,788 Inventories 150 150 Trade and other receivables 1,457,626 526,443 Current investments in Group companies and associates (Note 6) 1,770,676 6,323,425 Current financial investments (Note 8) 2,743,297 2,743,355 Cash and cash equivalents (Note 9) 3,683,107 3,520,415

TOTAL ASSETS 65,040,150 72,221,513

The accompanying Notes 1 to 19 are an integral part of the balance sheet at 31 December 2013.

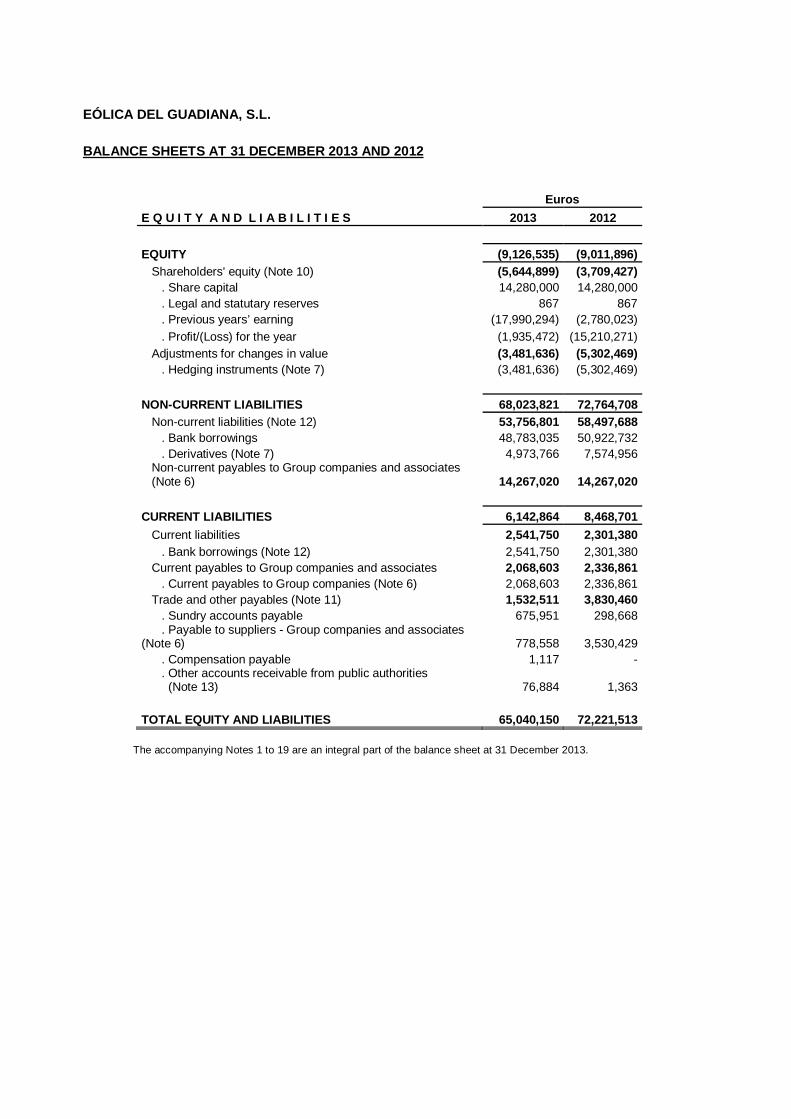

EÓLICA DEL GUADIANA, S.L.

BALANCE SHEETS AT 31 DECEMBER 2013 AND 2012

Euros

E Q U I T Y A N D L I A B I L I T I E S 2013 2012

EQUITY (9,126,535) (9,011,896) Shareholders' equity (Note 10) (5,644,899) (3,709,427) . Share capital 14,280,000 14,280,000 . Legal and statutary reserves 867 867 . Previous years’ earning (17,990,294) (2,780,023) . Profit/(Loss) for the year (1,935,472) (15,210,271) Adjustments for changes in value (3,481,636) (5,302,469) . Hedging instruments (Note 7) (3,481,636) (5,302,469)

NON-CURRENT LIABILITIES 68,023,821 72,764,708 Non-current liabilities (Note 12) 53,756,801 58,497,688 . Bank borrowings 48,783,035 50,922,732 . Derivatives (Note 7) 4,973,766 7,574,956 Non-current payables to Group companies and associates (Note 6) 14,267,020 14,267,020

CURRENT LIABILITIES 6,142,864 8,468,701

Current liabilities 2,541,750 2,301,380 . Bank borrowings (Note 12) 2,541,750 2,301,380 Current payables to Group companies and associates 2,068,603 2,336,861 . Current payables to Group companies (Note 6) 2,068,603 2,336,861 Trade and other payables (Note 11) 1,532,511 3,830,460 . Sundry accounts payable 675,951 298,668 . Payable to suppliers - Group companies and associates (Note 6) 778,558 3,530,429 . Compensation payable 1,117 - . Other accounts receivable from public authorities (Note 13) 76,884 1,363

TOTAL EQUITY AND LIABILITIES 65,040,150 72,221,513

The accompanying Notes 1 to 19 are an integral part of the balance sheet at 31 December 2013.

EÓLICA DEL GUADIANA, S.L.

INCOME STATEMENTS FOR THE YEARS ENDED 31 DECEMBER 2 013 AND 2012

Euros

2013 2012

CONTINUING OPERATIONS Revenue (Note 15.1) 7,491,261 6,995,546 Capitalised expenses of in-house work on assets (Note 5) 49,864 767,861 Procurements (27,261) - Other operating income - 26 Staff costs (Note 15.3) (30,081) (28,736) Other operating expenses (Note 15.2) (2,282,271) (2,507,404) Depreciation and amortisation charge (Notes 5) (4,519,506) (4,514,207) Impairment of and gains or losses on disposal of property, plant and equipment (Note 5) 528,938 (18,100,000)

OPERATING INCOME 1,210,944 (17,386,914)

Finance Income (Note 15.4) - 1,933 Finance costs (Note 15.4) (3,975,905) (4,343,977)

FINANCIAL RESULTS (3,975,905) (4,342,044)

PROFIT/(LOSS) BEFORE TAX (2,764,961) (21,728,958)

Income tax (Note 13.3) 829,489 6,518,687

PROFIT/(LOSS) FOR THE PERIOD FROM CONTINUING (1,935,472) (15,210,271) OPERATIONS

PROFIT/(LOSS) FOR THE PERIOD (1,935,472) (15,210,271)

The accompanying Notes 1 to 19 are an integral part of the income statement for 2013.

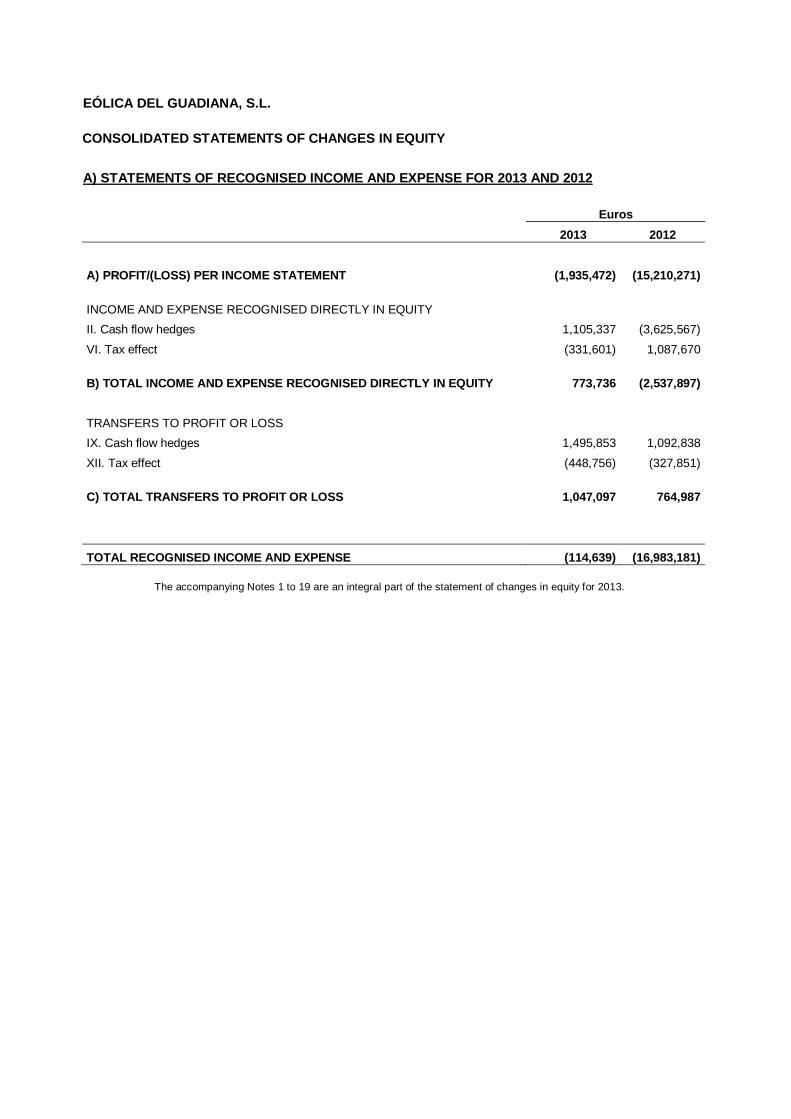

EÓLICA DEL GUADIANA, S.L.

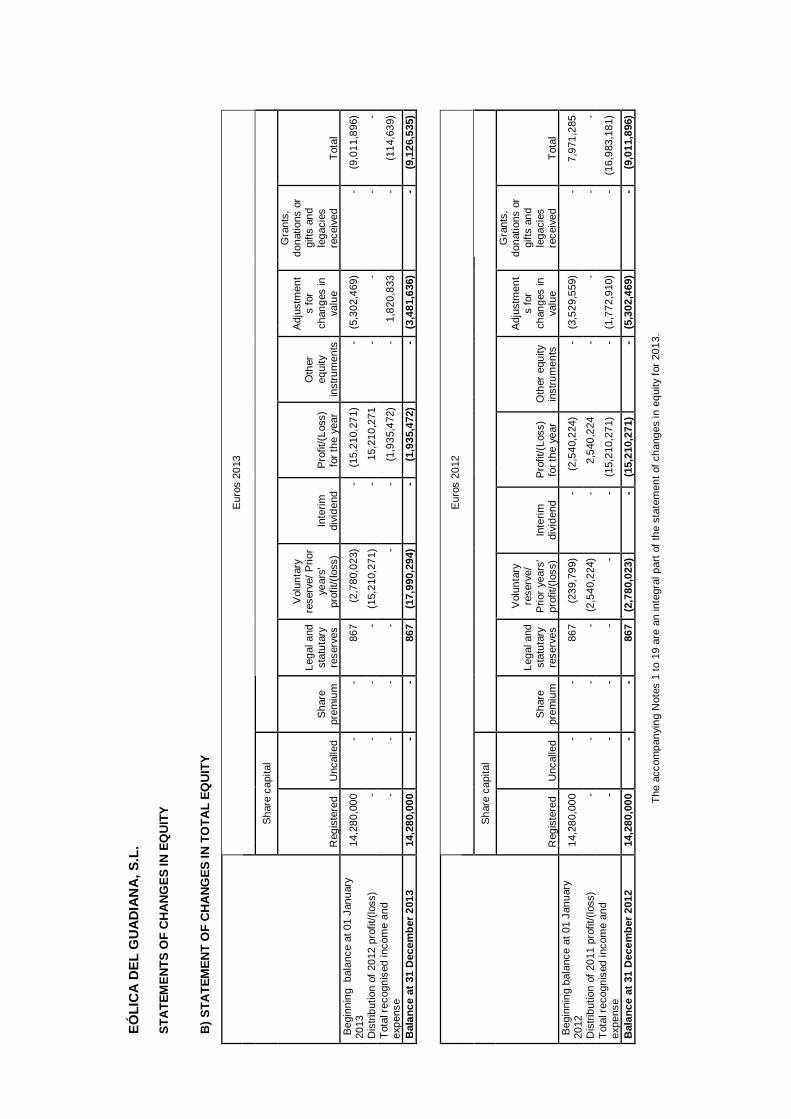

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY A) STATEMENTS OF RECOGNISED INCOME AND EXPENSE FOR 2013 AND 2012

Euros

2013 2012

A) PROFIT/(LOSS) PER INCOME STATEMENT (1,935,472) (15,210,271)

INCOME AND EXPENSE RECOGNISED DIRECTLY IN EQUITY

II. Cash flow hedges 1,105,337 (3,625,567)

VI. Tax effect (331,601) 1,087,670

B) TOTAL INCOME AND EXPENSE RECOGNISED DIRECTLY IN EQUITY 773,736 (2,537,897)

TRANSFERS TO PROFIT OR LOSS

IX. Cash flow hedges 1,495,853 1,092,838

XII. Tax effect (448,756) (327,851)

C) TOTAL TRANSFERS TO PROFIT OR LOSS 1,047,097 764,987

TOTAL RECOGNISED INCOME AND EXPENSE (114,639) (16,983,181)

The accompanying Notes 1 to 19 are an integral part of the statement of changes in equity for 2013.

E

ÓLI

CA

DE

L G

UA

DIA

NA

, S.L

. S

TA

TE

ME

NT

S O

F C

HA

NG

ES

IN E

QU

ITY

B

) S

TA

TE

ME

NT

OF

CH

AN

GE

S IN

TO

TA

L E

QU

ITY

Eur

os 2

013

S

hare

cap

ital

Reg

iste

red

Unc

alle

d S

hare

pr

emiu

m

Lega

l and

st

atut

ary

rese

rves

Vol

unta

ry

rese

rve/

Prio

r ye

ars'

pr

ofit/

(los

s)

Inte

rim

divi

dend

P

rofit

/(Lo

ss)

for

the

year

Oth

er

equi

ty

inst

rum

ents

Adj

ustm

ent

s fo

r ch

ange

s in

va

lue

Gra

nts,

do

natio

ns o

r gi

fts a

nd

lega

cies

re

ceiv

ed

Tot

al

Beg

inni

ng b

alan

ce a

t 01

Janu

ary

2013

14

,280

,000

-

- 86

7 (2

,780

,023

) -

(15,

210,

271)

-

(5,3

02,4

69)

- (9

,011

,896

)

Dis

trib

utio

n of

201

2 pr

ofit/

(loss

) -

- -

- (1

5,21

0,27

1)

- 15

,210

,271

-

- -

- T

otal

rec

ogni

sed

inco

me

and

expe

nse

- -

- -

- -

(1,9

35,4

72)

- 1,

820,

833

- (1

14,6

39)

Bal

ance

at 3

1 D

ecem

ber

2013

14

,280

,000

-

- 86

7 (1

7,99

0,29

4)

- (1

,935

,472

) -

(3,4

81,6

36)

- (9

,126

,535

)

Eur

os 2

012

S

hare

cap

ital

Reg

iste

red

Unc

alle

d S

hare

pr

emiu

m

Lega

l and

st

atut

ary

rese

rves

Vol

unta

ry

rese

rve/

P

rior

year

s'

prof

it/(l

oss)

In

terim

di

vide

nd

Pro

fit/(

Loss

) fo

r th

e ye

ar

Oth

er e

quity

in

stru

men

ts

Adj

ustm

ent

s fo

r ch

ange

s in

va

lue

Gra

nts,

do

natio

ns o

r gi

fts a

nd

lega

cies

re

ceiv

ed

Tot

al

Beg

inni

ng b

alan

ce a

t 01

Janu

ary

2012

14

,280

,000

-

- 86

7 (2

39,7

99)

- (2

,540

,224

) -

(3,5

29,5

59)

- 7,

971,

285

Dis

trib

utio

n of

201

1 pr

ofit/

(loss

) -

- -

- (2

,540

,224

) -

2,54

0,22

4 -

- -

- T

otal

rec

ogni

sed

inco

me

and

expe

nse

- -

- -

- -

(15,

210,

271)

-

(1,7

72,9

10)

- (1

6,98

3,18

1)

Bal

ance

at 3

1 D

ecem

ber

2012

14

,280

,000

-

- 86

7 (2

,780

,023

) -

(15,

210,

271)

-

(5,3

02,4

69)

- (9

,011

,896

)

The

acc

ompa

nyin

g N

otes

1 to

19

are

an in

tegr

al p

art o

f th

e st

atem

ent o

f cha

nges

in e

quity

for

201

3.

1

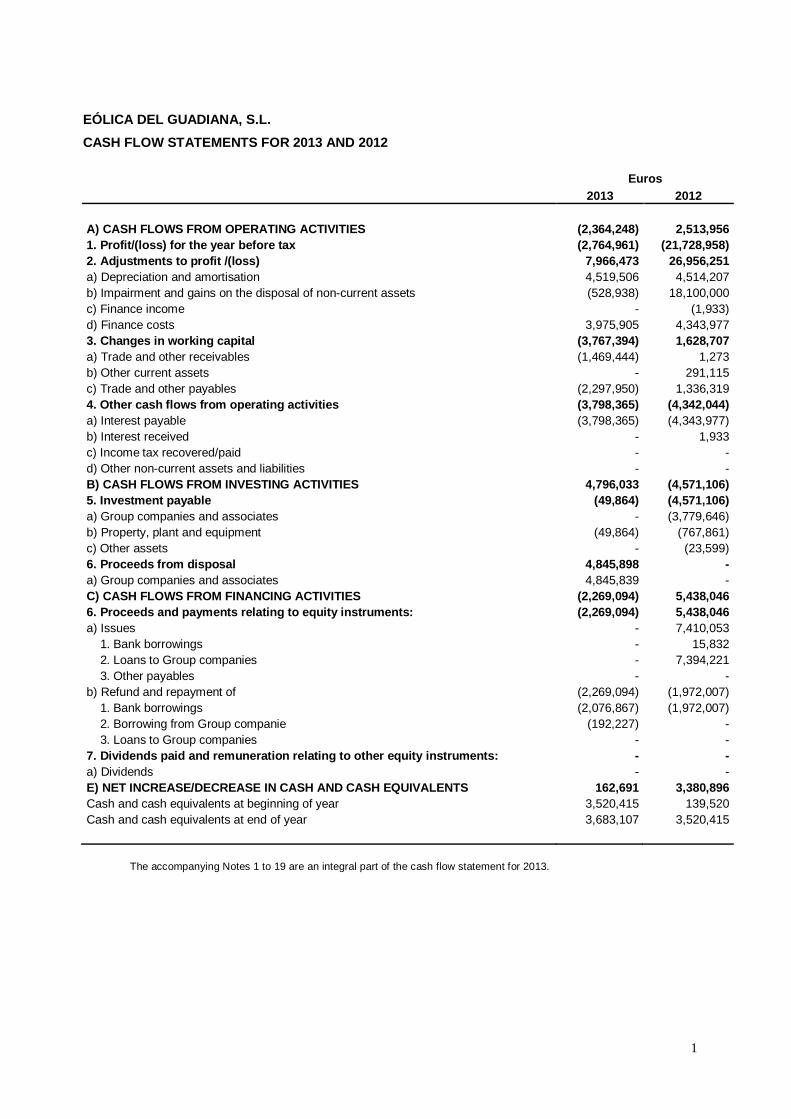

EÓLICA DEL GUADIANA, S.L.

CASH FLOW STATEMENTS FOR 2013 AND 2012

Euros 2013 2012

A) CASH FLOWS FROM OPERATING ACTIVITIES (2,364,248) 2,513,956 1. Profit/(loss) for the year before tax (2,764,961) (21,728,958) 2. Adjustments to profit /(loss) 7,966,473 26,956,251 a) Depreciation and amortisation 4,519,506 4,514,207 b) Impairment and gains on the disposal of non-current assets (528,938) 18,100,000 c) Finance income - (1,933) d) Finance costs 3,975,905 4,343,977 3. Changes in working capital (3,767,394) 1,628,707 a) Trade and other receivables (1,469,444) 1,273 b) Other current assets - 291,115 c) Trade and other payables (2,297,950) 1,336,319 4. Other cash flows from operating activities (3,798,365) (4,342,044) a) Interest payable (3,798,365) (4,343,977) b) Interest received - 1,933 c) Income tax recovered/paid - - d) Other non-current assets and liabilities - - B) CASH FLOWS FROM INVESTING ACTIVITIES 4,796,033 (4,571,106) 5. Investment payable (49,864) (4,571,106) a) Group companies and associates - (3,779,646) b) Property, plant and equipment (49,864) (767,861) c) Other assets - (23,599) 6. Proceeds from disposal 4,845,898 - a) Group companies and associates 4,845,839 - C) CASH FLOWS FROM FINANCING ACTIVITIES (2,269,094) 5,438,046 6. Proceeds and payments relating to equity instrum ents: (2,269,094) 5,438,046 a) Issues - 7,410,053 1. Bank borrowings - 15,832 2. Loans to Group companies - 7,394,221 3. Other payables - - b) Refund and repayment of (2,269,094) (1,972,007) 1. Bank borrowings (2,076,867) (1,972,007) 2. Borrowing from Group companie (192,227) - 3. Loans to Group companies - - 7. Dividends paid and remuneration relating to othe r equity instruments: - - a) Dividends - - E) NET INCREASE/DECREASE IN CASH AND CASH EQUIVALEN TS 162,691 3,380,896 Cash and cash equivalents at beginning of year 3,520,415 139,520 Cash and cash equivalents at end of year 3,683,107 3,520,415

The accompanying Notes 1 to 19 are an integral part of the cash flow statement for 2013.

2

EÓLICA DEL GUADIANA, S.L.

Notes to Financial Statements for the year ended 31 December 2013 1. Company activities

EÓLICA DEL GUADIANA, S.L. was incorporated as a limited company on 16 December 2002 and has not changed its name since its incorporation. Its registered office is currently in Huelva at calle Manuel Siurot, 27. The Company's object is: A) The positioning, construction and operation of wind farms, as well as the construction, expansion or adaptation of hydroelectric projects and, in general, research, study, construction and exploitation of facilities the purpose of which is to generate electricity with renewable resources (wind, solar, etc.) and the sale or distribution of the electricity produced to third parties. B) The preparation of any kind of engineering calculation project. C) The construction of any kind of civil engineering works, both public and private. D) The acquisition, administration, sale, general trade, exploitation of any kind, construction, promotion and development of any type of property and, in general, the performance of all types of transactions specific to real estate companies. E) The production, manufacture, sale and marketing, import and export of all types of agricultural products and electronic, electric and mechanic material and computer programs. F) Any other legal activity, related or not to the above, that the shareholders at the General Meeting resolve to undertake. These activities which compose the Company object may be wholly or partially carried on by the Company indirectly through the ownership of shares or equity interests in companies with an identical or similar company object. The wind farm through which Eólica del Guadiana operates is called Parque Eólico Montegordo. The Company does not have sufficient staff of their own or staff of this type and, therefore, it signed an agreement for the operation and maintenance of the farm with Urbaenergía, S.L. a company belonging to the Cobra/ACS Group to which it belongs. The provisional entry into service of the wind farm took place on 16 December 2010. The plant was definitively registered in the administrative registry of special regime production facilities established by Royal Decree 661/2007 on 6 April 2011. The Company belongs to a group of companies (ACS Group) which is managed in accordance with the Group's criteria. Energía y Recursos Ambientales, S.A. is the primary shareholder of the Company which is in turn 99.99% owned by the ACS Group company Cobra Gestión de Infraestructuras, S.A.

3

Regulatory Framework The special regime electricity production business in Spain is regulated by Spanish Electricity Industry Law 54/1997, of 27 November, and by the subsequent implementing regulations which are as follows:

- Royal Decree 436/2004, in force from 1 April 2004 to 1 June 2007.

- Royal Decree 661/2007, in force from 1 June 2007. The remuneration framework supporting renewable energies under the special regime for facilities which were registered in the pre-assignment register at 28 January 2012 was regulated up until this year by this royal decree. This Royal Decree stipulates two tariff regimes for wind-powered facilities; the market price option through a representative where upper limits ("ceilings") and lower limits ("floors") are established at the aggregate price (market price plus the premium) applicable to the sale of energy on the market; and the tariff option in which the regulated tariff is received. The facilities may choose the sale option for periods of no less than one year.

- Likewise, Royal Decree 661/2007 recognises in its transitional provision one that wind farms, among

others, which started up prior to 1 January 2008 have the right to maintain the premiums and incentives established under the previous regime (RD 436/2004, of 12 March) until 31 December 2012 in the market price sale option.

- In addition, Royal Decree 6/2009, of 30 April, introduces the pre-assignment system such that it

limits the pre-assigned facilities to the amounts and premiums set forth in RD 661/2007, as well as for those established going forward once the objectives of the 2020 Renewable Energies Plan are reached.

- The objective of Royal Decree 1614/2010, of 7 December, is to modify and regulate matters related

to electricity production from solar thermal and wind technologies, in a deficit control scenario. The main developments are the establishment of a limit on the equivalent operating hours entitled to a premium for solar thermal and wind power technologies, the obligation of the solar thermal energy industry to sell at a regulated tariff for the 12 months following the entry into force of the RD, or the start-up of the plant, if it were subsequent thereto and a 35% reduction of the premiums for wind power technology qualifying under RD 661/2007 and for the period between the approval of the RD and 31 December 2012.

- On 28 January 2012, Royal Decree-Law 1/2012 (RDL 1/2012) was published in the Official State

Gazette (Boletín Oficial del Estado, BOE), taking effect on the same day, which eliminated the pre-assignment remuneration process and the economic incentives for new facilities which produce electricity from cogeneration, renewable energy sources and waste.

- On 28 December 2012, Law 15/2012, of 27 December, on tax measures for energy sustainability

was published in the BOE which affects all facilities which produce electricity in Spain from 2013. Noteworthy among these measures is the creation of a 7% tax on activities related to the production and incorporation of electricity measured at power station busbars in the electric system (mainland, island and non-mainland). Likewise, this law also amends the current economic framework of certain renewable energy facilities excluding from the premium economic regime energy attributable to the use of fuel produced in facilities which use non-consumable renewable energy as a primary source, unless they are hybrid facilities which use non-consumable and consumable renewable energy sources (in which case the energy attributable to the use of the consumable renewable source could have the right to the premium economic regime), and the Ministry of Industry, Energy and Tourism is responsible for establishing the methodology for calculating the aforementioned energy.

4

- Royal Decree Law 2/2013 on urgent measures for the electricity system and the financial sector establishing certain adjustment to certain electricity industry costs was approved on 1 February 2013. From 01 January 2013 premium of the technologies are set at zero, eliminating the floor and ceiling of the market sale option, and maintaining the tariff sale option. It also modifies the ratio for updating the aforementioned tariffs which is now tied to the underlying inflation rather than the CPI. This royal legislative decree establishes that the owners of the facilities must choose between the sale of energy under the regulated tariff option or the option to sell freely on the market without receiving their premium. Once the option is chosen it is irrevocable. For practical purposes, this RDL lead the Company to choose the fixed tariff option from 2013.

- On 12 July 2013, Royal Decree-Law 9/2013 was published on urgent measures to guarantee the

financial stability and sustainability of the electricity system which affect the remuneration regime for facilities which produce electricity from cogeneration, renewable energy sources and waste. This royal decree-law, which entered into force on 14 July 2013, repealed, among others, RDL 661/2007, of 25 May, and RDL 6/2009, of 30 April, under which the Company's facilities which produce electricity qualified, in accordance with that described in the previous paragraphs, for the remuneration framework supporting renewable energies.

This royal decree-law introduces substantial changes to the applicable legal and economic framework, which will be based on the following principles:

o The remuneration of facilities which produce electricity under the special regime will be determined by: i) the sale of energy generated valued at market price and ii) a specific remuneration consisting of a period per unit of installed power which covers, where appropriate, if necessary, the investment costs of a standard facility which cannot be recovered in the market through the sale of energy, as well as a period for the operation which covers, where applicable, the difference between the operating costs and the revenue from the aforementioned standard facility's participation in the market.

o In order to calculate the specific remuneration for a standard facility over the course of its regulatory

useful life, and based on the activity of an efficient and well-managed company, the following will be taken into account: i) the revenue from the sale of energy valued at market production price, ii) the average operating costs necessary to carry out the activity and iii) the initial value of the investment of a standard facility.

o The remuneration regime established for each standard facility will not exceed the minimum level

necessary to cover the costs which allow these facilities to compete on an equal basis in the electricity market and to be able to obtain "reasonable profitability" with regard to each standard facility. This reasonable profitability will, before tax, be based on the average performance in the secondary market of government bonds for the ten years prior to the entry into force of the royal decree-law, plus a margin of 300 basis points which may be revised every six years.

o In order to calculate the specific remuneration for a standard facility, under no circumstances will the costs

or investments determined by law or administrative acts which are not applicable throughout Spain be taken into account. Furthermore, only the costs and investments which respond exclusively to electricity production will be taken into account.

o Royal Decree-Law 9/2013 will enable the revision of the parameters for this remuneration regime every

six years. o Lastly, the following specialities are established for the facilities developed in the island and non-mainland

electricity systems: i) exceptionally specific standard facilities may be defined and ii) the remuneration regime for these facilities may include, exceptionally, an incentive for the investment and execution during a certain period, when its installation entails a significant reduction in costs for the aforementioned systems.

5

- The bases for this new remuneration framework are included primarily in article 14 of Spanish Electricity Industry Law 24/2013, of 26 December, which also specifies the criteria for and the manner in which the remuneration parameters are to be revised for facilities which produce electricity from renewable energy sources, high-efficiency cogeneration and waste with a specific remuneration regime. Thus, the remuneration parameters shall be set for regulatory periods which will be effective for six years. The remuneration parameters may be revised prior commencement of the regulatory period. If this revision is not performed the parameters will be understood as extended for the entirety of the following regulatory period. Law 24/2013, of 26 December, also establishes that the reasonable profitability value for the remainder of the regulatory life will be established by law prior to the start of each regulatory period and that under no circumstances may the regulatory useful life or the standard value of the initial investment of a facility be revised once recognised. In addition, this law stipulates that the estimates for revenue from the sale of the energy generated for the remainder of the regulatory period will be revised every three years, valued at the market production price, based on the evolution of market prices and the forecast for operating hours. Lastly, it establishes that the values of the remuneration for the operation and extended operation for technologies whose operating costs depend essential on the price of fuel will be updated at least annually. In this connection, in February 2014, a draft Ministerial Order which sets all of the above-mentioned parameters necessary to determine the remuneration applicable to renewable energies, cogeneration and waste was provided to the interested parties in the context of the hearing process commenced by the Spanish National Securities Market and Competition Commission. In practice, the Company's facilities are subject to the new remuneration model established by the Spanish Electricity Industry Law and by RDL 9/2013, since the latter's entry into force. Thus, the revenue received from the energy sales made since 14 July 2013 have been settled by means of a payment on account of the remuneration which ultimately applies.

The regulatory modifications described above were included in the Company's business plan. The sole director evaluated the recoverability of the carrying amount of the property, plant and equipment and adjusted the impairment loss to the impairment test performed, the effect of which is recognised under "Property, plant and equipment" in the balance sheet at 31 December 2013 (Note 5). During the first half of 2013, the wind farm invoiced under the regulated tariff option. The facilities owned by the Company which operate in the Spanish market have elected the remuneration option established in article 24.1.a) through GNERA which acts merely as an intermediary between the producer and the electricity market (OMEL and REE).

2. Basis of presentation of the financial statements

2.1) Regulatory financial reporting framework applicable to the Company

These financial statements were prepared by the sole director in accordance with the regulatory financial reporting framework applicable to the Company, which consists of:

- The Spanish Commercial Code and all other Spanish corporate law. - The Spanish National Chart of Accounts approved by Royal Decree 1514/2007. - The mandatory rules approved by the Spanish Accounting and Audit Institute in order to implement the

Spanish National Chart of Accounts and its supplementary rules. - All other applicable Spanish accounting legislation.

2.2) Fair presentation

The financial statements, which were obtained from the accounting records of EÓLICA DEL GUADIANA S.L., are presented in accordance with Royal Decree 1514/2007 approving the Spanish National Chart of Accounts and, accordingly, present fairly the Company's equity, financial position and results of operations and cash flows.

6

These financial statements at 31 December 2013, which were formally prepared by the Company's sole director, will be submitted for approval by the shareholders at the General Meeting, and it is considered that they will be approved without any changes. The abridged financial statements for 2012 were approved by the shareholders at the General Meeting held on 25 July 2013. 2.3) Going concern principle of accounting The Company's sole director prepared the financial statements in accordance with the going concern principle of accounting taking into account the expected cash flows, credit facilities available, as well as the on-going financial support of the Group to which it belongs in order to meet the obligations it has undertaken so that it may realise its assets and settle its liabilities for the amounts and with the classification reflected in the financial statements. As indicated in Note 10.3, no grounds for dissolution apply to the Company. 2.4) Accounting principles applied The financial statements were prepared in accordance with the generally accepted accounting principles and measurement bases described in Note 4. All obligatory accounting principles with a significant effect on the financial statements were applied in their preparation.

2.5) Key issues in relation to the measurement and estimation of uncertainty In preparing the accompanying financial statements estimates were made by the Company's sole director in order to quantify certain of the assets, liabilities, income, expenses and obligations reported herein. These estimates relate basically to the following: - The useful life of the property, plant and equipment (Note 4.1). - The assessment of possible impairment losses on certain assets (Note 4.1). - The fair value of certain financial instruments (see Note 4.3). - The recovery of deferred tax assets (Note 4.4). - Credit risk management (Note 18.2). Although these estimates were made on the basis of the best information available at the date of preparation of these financial statements on the events analysed, events that take place in the future might make it necessary to change these estimates in coming years. Changes in accounting estimates would be applied prospectively, recognising the effects of the change in estimates in the financial statements. 2.6) Comparative information

The information relating to 2012 included in these notes to the financial statements is presented for comparison purposes with that relating to 2013. 2.7) Grouping of items Certain items in the balance sheet, income statement, statement of changes in equity and cash flow statement are grouped together to facilitate their understanding; however, whenever the amounts involved are material, the information is broken down in the related notes to the financial statements. 2.8) Changes in accounting policies

In 2013 there were no significant changes in accounting policies with respect to the policies applied in 2012.

7

2.9) Correction of errors In preparing the accompanying financial statements no significant errors were detected that would have made it necessary to restate the amounts included in the financial statements for 2012.

3. Allocation of profit/(losses)

The proposed distribution of profit/(loss) for 2013 that the Company's sole director will submit for approval by the shareholders at the General Meeting is as follows:

Euros

Profit/(Loss) for 2013 (1,935,472)

Allocation of profit/(loss):

. Previous years’ earning

(1,935,472)

As stated in Note 12, in accordance with the financing agreement entered into with various financial institutions, there are restrictions on the distribution of dividends to the shareholder, unless the conditions established in provision 14, point 3 of the agreement is met. The aforementioned restrictions are:

• Any other significant debt owed by the borrower which has matured has been settled in full, including that arising from this credit facility.

• No early maturity event has arisen and the distribution to shareholders does not give rise to any of the aforementioned events;

• The first amortisation payment has been made on this credit facility;

• The debt service reserve fund is fully funded;

• The debt service coverage ratio for the previous year exceeds 1.10.

• The amounts to be distributed to the shareholders do not in any case exceed the balance of the

restricted drawdown account; and

• There was a net profit in the previous year.

• No other means of capital remuneration will be allowed other than those included in the definition of shareholder distributions, unless prior authorisation has been obtained from the lenders.

4. Accounting Policies

The principal measurement bases used by EÓLICA DEL GUADIANA, S.L. in preparing its abridged financial statements for 2013, in accordance with the Spanish National Chart of Accounts, were as follows: 4.1) Property, plant and equipment Property, plant and equipment are initially recognised at acquisition cost and are subsequently reduced by the related accumulated depreciation and by any impairment losses recognised.

8

Property, plant and equipment upkeep and maintenance expenses are recognised in the income statement for the year in which they are incurred. However, the costs of improvements leading to increased capacity or efficiency or to a lengthening of the useful lives of the assets are capitalised. For non-current assets that necessarily take a period of more than twelve months to get ready for their intended use, the capitalised costs include such borrowing costs as might have been incurred before the assets are ready for their intended use and which have been charged by the supplier or relate to loans or other borrowings directly attributable to the acquisition or production of the assets. In-house work on non-current assets is measured at accumulated cost (external costs plus in-house costs, determined on the basis of in-house materials consumption, labour and general manufacturing costs calculated using absorption rates similar to those used for the measurement of inventories). The Company depreciates the cost of its property, plant and equipment using the straight-line method over the years of estimated useful life of the assets, the detail being as follows: Property, plant and equipment financed with project finance The investments made by the Company in the wind farms it operates were financed through a project finance structure (financing applied to projects). These financing structures are applied to projects capable in their own right of providing sufficient guarantees to the participating banks with regard to the repayment of the funds borrowed to finance them. The project's assets are financed, on the one hand, through a contribution of funds by the developers, which is limited to a given amount, and on the other, generally of a larger amount, through borrowed funds in the form of long-term debt. The debt servicing of these credit facilities or loans is supported mainly by the cash flows to be generated by the project in the future and by security interests in the project's assets. These assets are valued at the costs directly allocable to construction until they come into service (studies and designs, compulsory purchases, project execution, project management and administration expenses, installations and similar items) and the portion relating to other indirectly allocable costs, to the extent that they relate to the construction period. Also included under this heading are the borrowing costs incurred prior to the entry into operation of the assets arising from the external financing thereof. Capitalised borrowing costs arise from specific borrowings expressly used for the acquisition of an asset. Impairment of property, plant and equipment At the end of each reporting period, the Company reviews the carrying amounts of its property, plant and equipment to determine whether there is any indication that those assets might have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where the asset does not generate itself cash flows that are independent from other assets, the Company estimates the recoverable amount of the smallest identifiable cash-generating unit to which the asset belongs.

Years of Estimated Useful Life

Construction and installation work

18

9

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognised as an expense immediately. Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (cash-generating unit) in prior years. A reversal of an impairment loss is recognised as income immediately. The recoverable amount is the higher of fair value less costs to sell and value in use. In order to calculate the value in use of this type of asset, a projection is made of the expected cash flows until the end of the asset's useful life. The projections include both known data (based on the project agreements) as well as basic assumptions supported by specific studies carried out by experts or other historical data (demand, production, etc.). Likewise, macroeconomic data projections are made: inflation, interest rate, etc. using the data provided by independent specialized sources. The discount rates used to discount these cash flows take into account the cost of equity and in each case includes the business risk. As a result of the analysis performed, the directors consider it necessary to recognise impairment losses on the Company's facilities (Note 5). 4.2) Leases Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards incidental to ownership of the leased asset to the lessee. All other leases are classified as operating leases. The Company as lessee Assets acquired under finance leases are classified based on the nature of the leased asset. A liability is recognised for the same amount, which is the lower of the fair value of the leased asset and the present value at the start of the lease of the agreed upon minimum lease payments. Lease payments are distributed between finance costs and the reduction of the liability. The same depreciation, impairment and derecognition criteria are applied to the leased assets as to assets of the same nature. Payments under operating leases are recognised as expenses in the income statement when incurred. 4.3) Financial instruments 4.3.1) Financial assets The financial assets held by the Company are classified in the following categories:

a) Loans and receivables: financial assets arising from the sale of goods or the rendering of services in the ordinary course of the Company's business, or financial assets which, not having commercial substance, are not equity instruments or derivatives, have fixed or determinable payments and are not traded in an active market. Interest income is calculated in the year in which it accrues on a time proportion basis.

10

b) Held-to-maturity (fixed-income securities): debt securities with fixed maturity and determinable payments that are traded in an active market and which the Company has the positive intention and ability to hold to the date of maturity.

Financial assets are initially recognised at the fair value of the consideration given, plus any directly attributable transaction costs. Subsequently, loans and receivables are measured at amortised cost. The Company derecognises a financial asset when it expires or when the rights to the cash flows from the financial asset have been transferred and substantially all the risks and rewards incidental to ownership of the financial asset have been transferred, such as in the case of the outright sale of assets, factoring of trade receivables in which the Company does not retain any credit or interest rate risk, sale of financial assets under an agreement to repurchase them at their fair value or the securitisation of financial assets in which the transferor does not retain any subordinated debt, provide any type of guarantee or assume any other type of risk. However, the Company does not derecognise financial assets, and recognises a financial liability for an amount equal to the consideration received, in transfers of financial assets in which substantially all the risks and rewards of ownership are retained, such as in the case of bill discounting, with-recourse factoring, sales of financial assets under an agreement to repurchase them at a fixed price or at the selling price plus interest and the securitisation of financial assets in which the transferor retains a subordinated interest or any other kind of guarantee that absorbs substantially all the expected losses. 4.3.2) Financial liabilities Financial liabilities include accounts payable by the Company that have arisen from the purchase of goods or services in the normal course of the Company’s business and those which, not having commercial substance, cannot be classed as derivative financial instruments. Accounts payable are initially recognised at the fair value of the consideration received, adjusted by the directly attributable transaction costs. These liabilities are subsequently measured at amortised cost. Liability derivative financial instruments are measured at fair value, following the same criteria as for financial assets held for trading described in the previous section. The Company derecognises financial liabilities when the obligations giving rise to them cease to exist. 4.3.3) Hedging financial instruments The Company uses derivative financial instruments to hedge the risks to which its business activities, operations and future cash flows are exposed. Basically, these risks relate to changes in interest rates. The Company arranges hedging financial instruments in this connection, mainly IRS (Interest Rate Swap). In order for these financial instruments to qualify for hedge accounting, they are initially designated as such and the hedging relationship is documented. Also, the Company verifies, both at inception and periodically over the term of the hedge (at least at the end of each reporting period), that the hedging relationship is effective, i.e. that it is prospectively foreseeable that the changes in the fair value or cash flows of the hedged item (attributable to the hedged risk) will be almost fully offset by those of the hedging instrument and that, retrospectively, the gain or loss on the hedge was within a range of 80-125% of the gain or loss on the hedged item.

11

In 2013 and 2012, the Company used only cash flow hedges. In hedges of this nature, the portion of the gain or loss on the hedging instrument that has been determined to be an effective hedge is recognised temporarily in equity and is recognised in the income statement in the same period during which the hedged item affects profit or loss, unless the hedge relates to a forecast transaction that results in the recognition of a non-financial asset or a non-financial liability, in which case the amounts recognised in equity are included in the initial cost of the asset or liability when it is acquired or assumed. Hedge accounting is discontinued when the hedging instrument expires or is sold, terminated or exercised, or no longer qualifies for hedge accounting. At that time, any cumulative gain or loss on the hedging instrument recognised in equity is retained in equity until the forecast transaction occurs. If a hedged transaction is no longer expected to occur, the net cumulative gain or loss recognised in equity is transferred to net profit or loss for the year. The fair value of the hedging financial instruments used by the Company (interest rate swaps) is calculated by discounting future settlements between fixed and floating interest rates to their present value, in line with implicit market rates, obtained from long-term interest rate swap curves. Implicit volatility is used to calculate the fair values of caps and floors using option valuation models. The derivatives arranged by the Company at 31 December 2013 met all the requirements indicated above to qualify as hedges and, therefore, the changes in the fair value of these derivative financial instruments for the year ended 31 December 2013 were recognised under “Valuation adjustments” in equity. 4.4) Income tax Tax expense (tax income) comprises current tax expense (current tax income) and deferred tax expense (deferred tax income). The current income tax expense is the amount payable by the Company as a result of income tax settlements for a given year. Tax credits and other tax benefits, excluding tax withholdings and pre-payments, and tax loss carryforwards from prior years effectively offset in the current year reduce the current income tax expense. The deferred tax expense or income relates to the recognition and derecognition of deferred tax assets and liabilities. These include temporary differences measured at the amount expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities and their tax bases, and tax loss and tax credit carryforwards. These amounts are measured at the tax rates that are expected to apply in the period when the asset is realised or the liability is settled. Deferred tax liabilities are recognised for all taxable temporary differences, except for those arising from the initial recognition of goodwill or of other assets and liabilities in a transaction that is not a business combination and affects neither accounting profit (loss) nor taxable base amount. Deferred tax assets are recognised to the extent that it is considered probable that the Company will have taxable profits in the future against which the deferred tax assets can be utilised. Deferred tax assets and liabilities arising from transactions charged or credited directly to equity are also recognised in equity.

12

The deferred tax assets recognised are reassessed at the end of each reporting period and the appropriate adjustments are made to the extent that there are doubts as to their future recoverability. Also, unrecognised deferred tax assets are reassessed at the end of each reporting period and are recognised to the extent that it has become probable that they will be recovered through future taxable profits. The Company is included in consolidated tax group no. 30/99 headed by ACS Actividades de Construcción y Servicios, S.A., as well as VAT group no. 0194/08 headed by ACS Actividades de Construcción y Servicios, S.A. since 2010. 4.5) Income and expense Revenue and expenses are recognised in profit or loss for the year on an accrual basis, i.e. when the actual flow of the related goods and services occurs, regardless of when the resulting monetary or financial flow arises. Revenue is measured at the fair value of the consideration received, net of discounts and taxes. Revenue from sales is recognised when the significant risks and rewards of ownership of the goods sold have been transferred to the buyer, and the Company retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold. Revenue from the rendering of services is recognised by reference to the stage of completion of the transaction at the end of the reporting period, provided the outcome of the transaction can be estimated reliably. Interest income from financial assets is recognised using the effective interest method and dividend income is recognised when the shareholder's right to receive payment has been established. Interest and dividends from financial assets accrued after the date of acquisition are recognised as income. 4.6) Related-party transactions The Company performs all its transactions with related parties on an arm's length basis. Also, the transfer prices are adequately supported and, therefore, the Company’s sole director considers that there are no material risks in this connection that might give rise to significant liabilities in the future. 4.7) Provisions and contingencies When preparing the financial statements, the Company’s sole director made a distinction between: a) Provisions: credit balances covering present obligations arising from past events, the settlement of which is

likely to cause an outflow of resources, but which are uncertain as to their amount and/or timing. b) Contingent liabilities: possible obligations that arise from past events and whose existence will be

confirmed only by the occurrence or non-occurrence of one or more future events not wholly within the Company's control.

The financial statements include all the provisions with respect to which it is considered that it is more likely than not that the obligation will have to be settled. Contingent liabilities are not recognised in the abridged financial statements but rather are disclosed in the notes to the abridged financial statements, unless the possibility of an outflow in settlement is considered to be remote. Provisions are measured at the present value of the best possible estimate of the amount required to settle or transfer the obligation, taking into account the information available on the event and its consequences, recording the adjustments which arise as a result of the update of these provisions as a finance cost as it accrues.

13

4.8) Environmental assets and liabilities

Environmental assets are deemed to be assets used on a lasting basis in the Company's operations whose main purpose is to minimise environmental impact and protect and improve the environment, including the reduction or elimination of future pollution. 4.9) Current/non-current classification Balances are classified as current and non-current in the accompanying balance sheet. Current balances include balances which the Company expects to sell, consume, pay or realise during its normal operations. The remaining balances are classified as non-current.

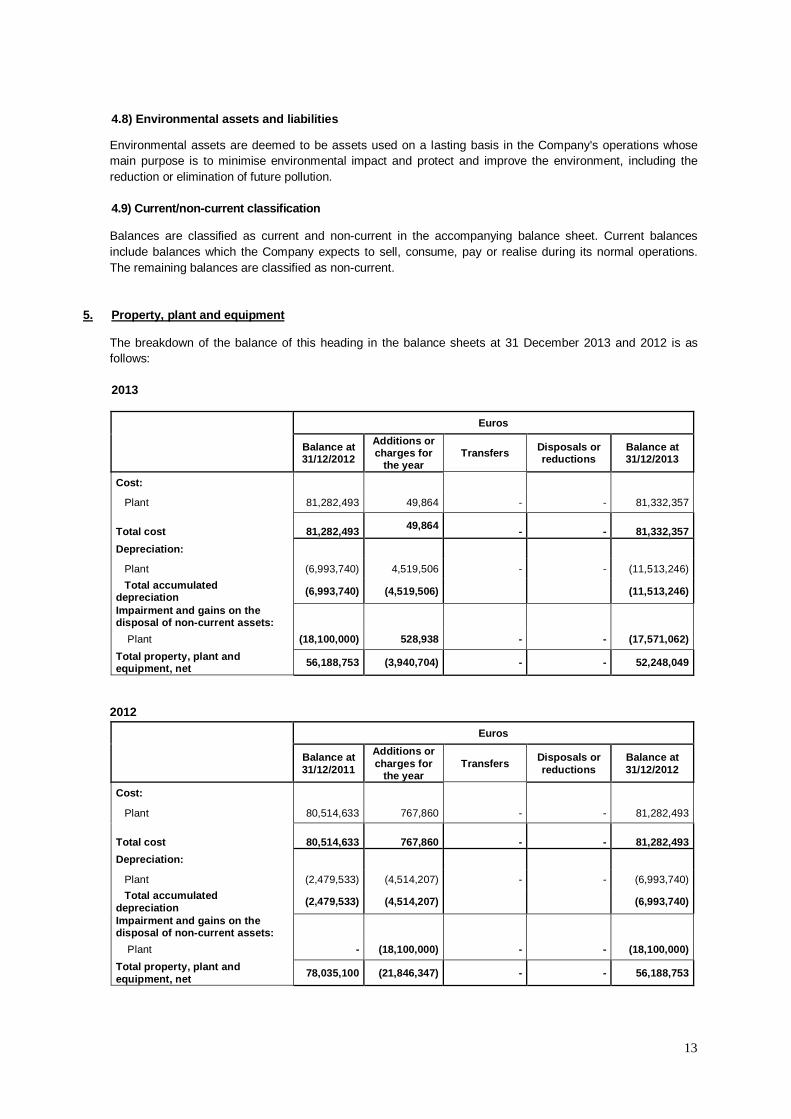

5. Property, plant and equipment The breakdown of the balance of this heading in the balance sheets at 31 December 2013 and 2012 is as follows: 2013

2012

Euros

Balance at 31/12/2012

Additions or charges for

the year Transfers Disposals or

reductions Balance at 31/12/2013

Cost:

Plant 81,282,493 49,864 - - 81,332,357

Total cost

81,282,493 49,864

-

-

81,332,357

Depreciation:

Plant (6,993,740) 4,519,506 - - (11,513,246)

Total accumulated depreciation (6,993,740) (4,519,506) (11,513,246)

Impairment and gains on the disposal of non-current assets:

Plant (18,100,000) 528,938 - - (17,571,062)

Total property, plant and equipment, net 56,188,753 (3,940,704) - - 52,248,049

Euros

Balance at 31/12/2011

Additions or charges for

the year Transfers

Disposals or reductions

Balance at 31/12/2012

Cost:

Plant 80,514,633 767,860 - - 81,282,493

Total cost

80,514,633

767,860

-

-

81,282,493

Depreciation:

Plant (2,479,533) (4,514,207) - - (6,993,740)

Total accumulated depreciation

(2,479,533) (4,514,207) (6,993,740)

Impairment and gains on the disposal of non-current assets:

Plant - (18,100,000) - - (18,100,000)

Total property, plant and equipment, net 78,035,100 (21,846,347) - - 56,188,753

14

Property, plant and equipment is comprised of equipment and facilities necessary to exploit the wind farm operated by the Company (Note 1). The additions recognised in 2013 correspond in full to the capitalisation of the expenses related to the construction work in progress corresponding to the tax on building, installations and other works (Impuesto sobre Construcciones, Instalaciones y Obras, ICIO) for the years in which the construction work on the wind farm was performed. The Company takes out insurance policies to cover the possible risks to which its property, plant and equipment are subject. At 2013 and 2012 year end these risks were adequately covered. To secure compliance with the obligations arising from the financing agreement described in Note 12, the Company definitively assigned to the lenders all of the collection and other rights and the guarantees arising from the plant construction, operation, maintenance and refurbishment agreements, management and administration services, as well as land use and energy sale and purchase agreements and indemnities for the insurance policies taken out by the Company. At 31 December 2013, the Company did not have any fully depreciated items of property, plant and equipment. In addition, at 31 December 2013 and 2012, there were no firm property, plant and equipment purchase commitments.

Since new and significant regulatory changes occurred in the Spanish electricity system in 2013 (see Note 1), the Company's sole director tested the property, plant and equipment for impairment at 31 December 2013.

In order to carry out the aforementioned impairment test, in compliance with the corresponding current legislation, the recoverable amount of all of the assets was established as the higher of value in use and the net sale price that would be obtained from the assets.

The directors deemed the recoverable amount the value in use of the assets.

In order to calculate the value in use of this type of asset, a projection is made of the expected cash flows until the end of the asset's useful life (20 years from its entry into service, plus 5 additional years as a procedure for calculating the residual value), including the best estimate of the income which they expect to receive pursuant to Royal Decree-Law 9/2013 and its definitive implementing provisions in the process of approval. The projections include both known data (based on the project agreements) as well as basic assumptions supported by specific studies carried out by experts or other historical data (demand, production, etc.). Likewise, macroeconomic data projections are made: inflation, interest rate, etc. using the data provided by independent specialized sources.

The project's operating cash flows are discounted at an average floating WACC rate based on the evolution of the gearing envisaged for the project in the remainder of its useful life. The discount rate used by the Company in its impairment test ranges from 8% to 9%. Taking into account the analysis carried out by the Company with respect to the evolution of the regulatory environment described in Note 1, the Company reversed a portion of the impairment of its non-current assets recognised in 2012 amounting to EUR 529 thousand which was recognised under "Impairment and gains or losses on disposals of non-current assets" in the income statement. The estimated income in accordance with the new regulations was obtained based on the parameters of the draft ministerial order described in Note 1 which, at the reporting date, is pending approval and constitutes the best estimate at said date. The accumulated impairment losses recognised in accordance with the regulatory framework described in Note 1 amounted to EUR 17,571,062.

Operating leases

With respect to the land on which the wind farm described in the previous note is located, various leases were entered into which expire on 18 August 2041.

15

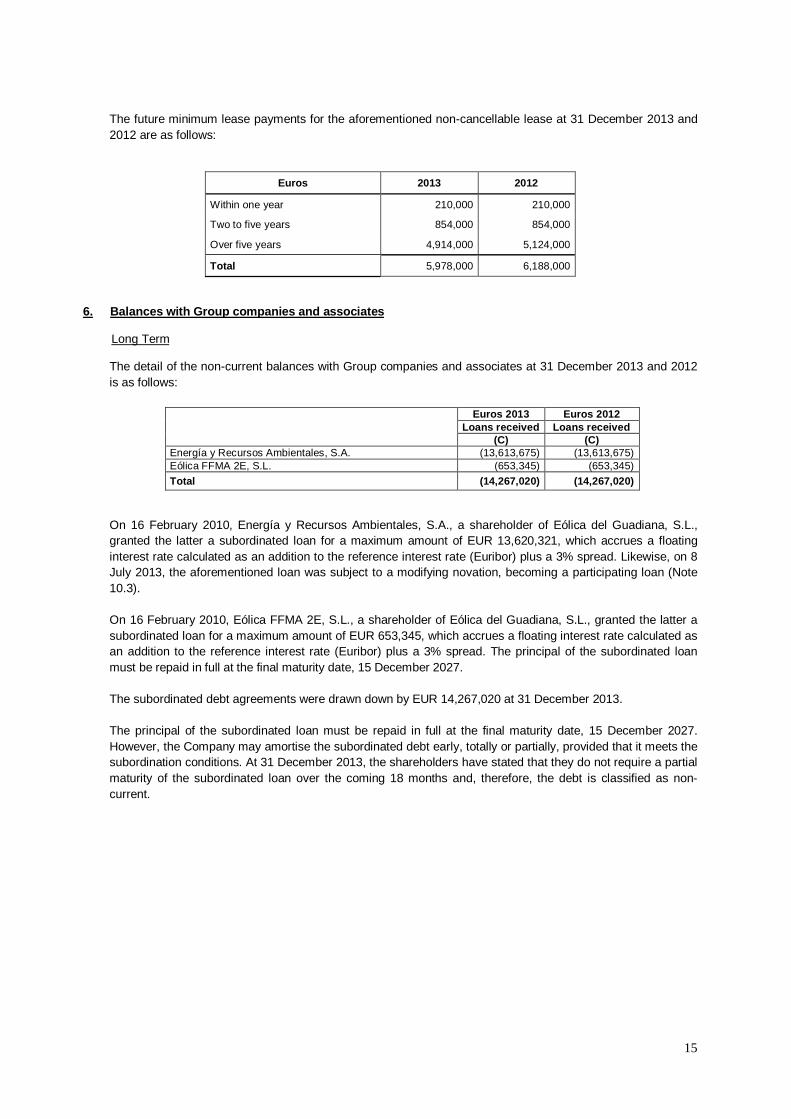

The future minimum lease payments for the aforementioned non-cancellable lease at 31 December 2013 and 2012 are as follows:

Euros 2013 2012

Within one year 210,000 210,000

Two to five years 854,000 854,000

Over five years 4,914,000 5,124,000

Total 5,978,000 6,188,000

6. Balances with Group companies and associates

Long Term The detail of the non-current balances with Group companies and associates at 31 December 2013 and 2012 is as follows:

Euros 2013 Euros 2012 Loans received Loans received

(C) (C) Energía y Recursos Ambientales, S.A. (13,613,675) (13,613,675) Eólica FFMA 2E, S.L. (653,345) (653,345)

Total (14,267,020) (14,267,020)

On 16 February 2010, Energía y Recursos Ambientales, S.A., a shareholder of Eólica del Guadiana, S.L., granted the latter a subordinated loan for a maximum amount of EUR 13,620,321, which accrues a floating interest rate calculated as an addition to the reference interest rate (Euribor) plus a 3% spread. Likewise, on 8 July 2013, the aforementioned loan was subject to a modifying novation, becoming a participating loan (Note 10.3). On 16 February 2010, Eólica FFMA 2E, S.L., a shareholder of Eólica del Guadiana, S.L., granted the latter a subordinated loan for a maximum amount of EUR 653,345, which accrues a floating interest rate calculated as an addition to the reference interest rate (Euribor) plus a 3% spread. The principal of the subordinated loan must be repaid in full at the final maturity date, 15 December 2027. The subordinated debt agreements were drawn down by EUR 14,267,020 at 31 December 2013. The principal of the subordinated loan must be repaid in full at the final maturity date, 15 December 2027. However, the Company may amortise the subordinated debt early, totally or partially, provided that it meets the subordination conditions. At 31 December 2013, the shareholders have stated that they do not require a partial maturity of the subordinated loan over the coming 18 months and, therefore, the debt is classified as non-current.

16

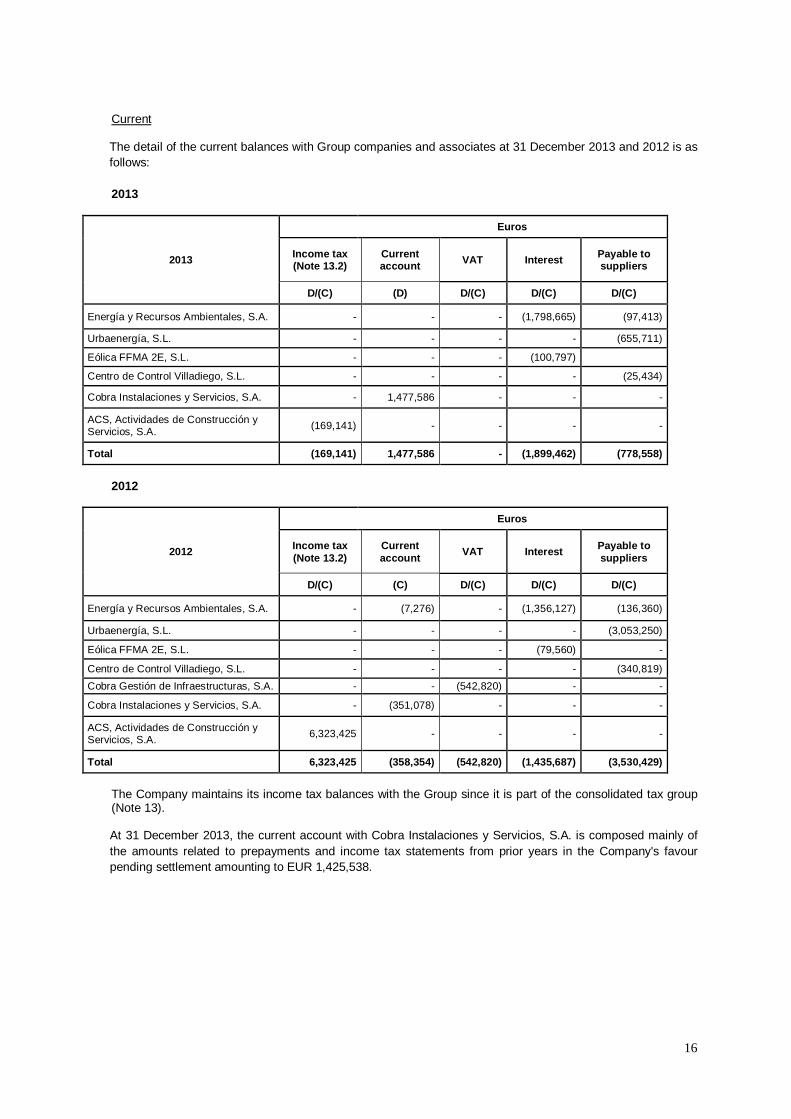

Current The detail of the current balances with Group companies and associates at 31 December 2013 and 2012 is as follows: 2013

2013

Euros

Income tax (Note 13.2)

Current account VAT Interest Payable to

suppliers

D/(C) (D) D/(C) D/(C) D/(C)

Energía y Recursos Ambientales, S.A. - - - (1,798,665) (97,413)

Urbaenergía, S.L. - - - - (655,711)

Eólica FFMA 2E, S.L. - - - (100,797)

Centro de Control Villadiego, S.L. - - - - (25,434)

Cobra Instalaciones y Servicios, S.A. - 1,477,586 - - -

ACS, Actividades de Construcción y Servicios, S.A. (169,141) - - - -

Total (169,141) 1,477,586 - (1,899,462) (778,558)

2012

2012

Euros

Income tax (Note 13.2)

Current account

VAT Interest Payable to suppliers

D/(C) (C) D/(C) D/(C) D/(C)

Energía y Recursos Ambientales, S.A. - (7,276) - (1,356,127) (136,360)

Urbaenergía, S.L. - - - - (3,053,250)

Eólica FFMA 2E, S.L. - - - (79,560) -

Centro de Control Villadiego, S.L. - - - - (340,819)

Cobra Gestión de Infraestructuras, S.A. - - (542,820) - -

Cobra Instalaciones y Servicios, S.A. - (351,078) - - -

ACS, Actividades de Construcción y Servicios, S.A. 6,323,425 - - - -

Total 6,323,425 (358,354) (542,820) (1,435,687) (3,530,429)

The Company maintains its income tax balances with the Group since it is part of the consolidated tax group (Note 13). At 31 December 2013, the current account with Cobra Instalaciones y Servicios, S.A. is composed mainly of the amounts related to prepayments and income tax statements from prior years in the Company's favour pending settlement amounting to EUR 1,425,538.

17

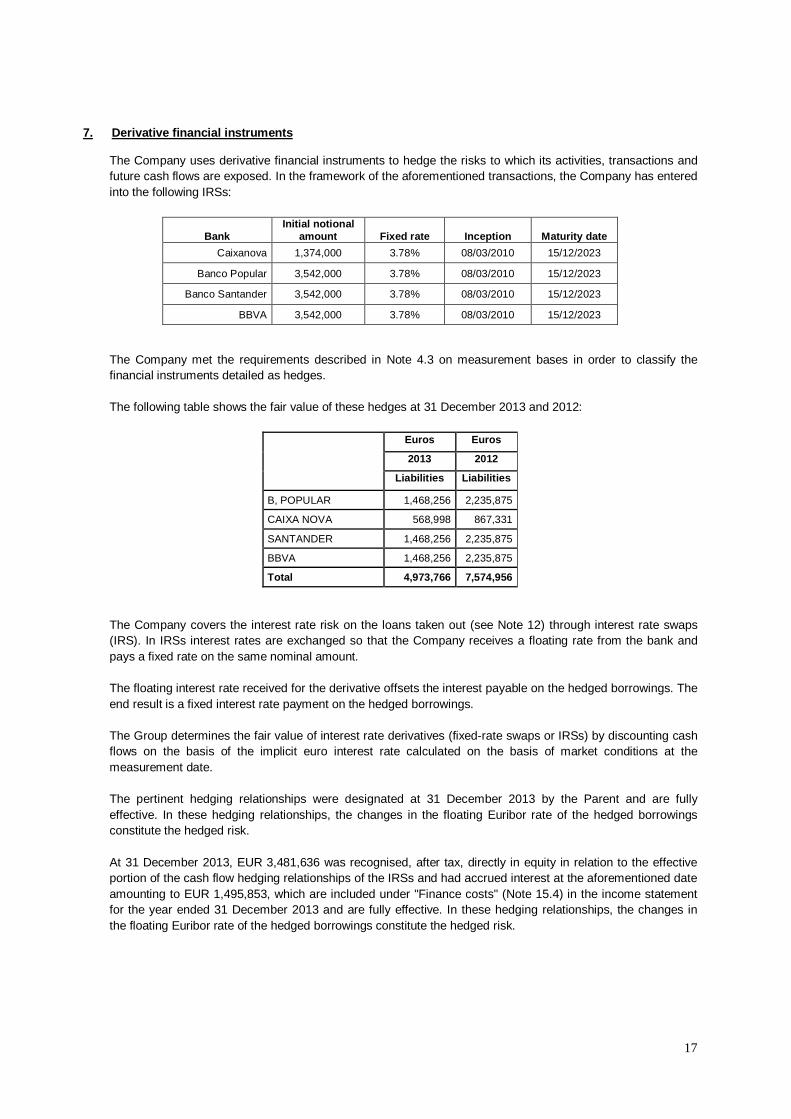

7. Derivative financial instruments

The Company uses derivative financial instruments to hedge the risks to which its activities, transactions and future cash flows are exposed. In the framework of the aforementioned transactions, the Company has entered into the following IRSs:

Bank Initial notional

amount Fixed rate Inception Maturity date

Caixanova 1,374,000 3.78% 08/03/2010 15/12/2023

Banco Popular 3,542,000 3.78% 08/03/2010 15/12/2023

Banco Santander 3,542,000 3.78% 08/03/2010 15/12/2023

BBVA 3,542,000 3.78% 08/03/2010 15/12/2023

The Company met the requirements described in Note 4.3 on measurement bases in order to classify the financial instruments detailed as hedges. The following table shows the fair value of these hedges at 31 December 2013 and 2012:

Euros Euros

2013 2012

Liabilities Liabilities

B, POPULAR 1,468,256 2,235,875

CAIXA NOVA 568,998 867,331

SANTANDER 1,468,256 2,235,875

BBVA 1,468,256 2,235,875

Total 4,973,766 7,574,956

The Company covers the interest rate risk on the loans taken out (see Note 12) through interest rate swaps (IRS). In IRSs interest rates are exchanged so that the Company receives a floating rate from the bank and pays a fixed rate on the same nominal amount. The floating interest rate received for the derivative offsets the interest payable on the hedged borrowings. The end result is a fixed interest rate payment on the hedged borrowings. The Group determines the fair value of interest rate derivatives (fixed-rate swaps or IRSs) by discounting cash flows on the basis of the implicit euro interest rate calculated on the basis of market conditions at the measurement date. The pertinent hedging relationships were designated at 31 December 2013 by the Parent and are fully effective. In these hedging relationships, the changes in the floating Euribor rate of the hedged borrowings constitute the hedged risk. At 31 December 2013, EUR 3,481,636 was recognised, after tax, directly in equity in relation to the effective portion of the cash flow hedging relationships of the IRSs and had accrued interest at the aforementioned date amounting to EUR 1,495,853, which are included under "Finance costs" (Note 15.4) in the income statement for the year ended 31 December 2013 and are fully effective. In these hedging relationships, the changes in the floating Euribor rate of the hedged borrowings constitute the hedged risk.

18

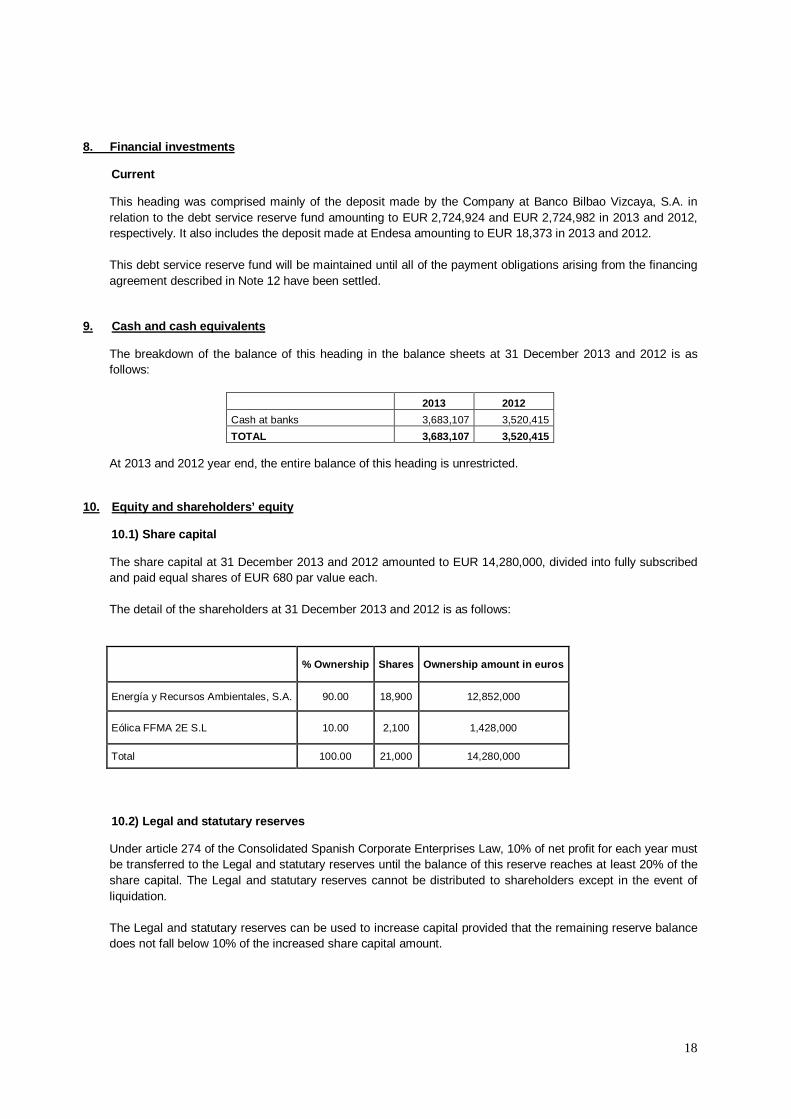

8. Financial investments

Current

This heading was comprised mainly of the deposit made by the Company at Banco Bilbao Vizcaya, S.A. in relation to the debt service reserve fund amounting to EUR 2,724,924 and EUR 2,724,982 in 2013 and 2012, respectively. It also includes the deposit made at Endesa amounting to EUR 18,373 in 2013 and 2012. This debt service reserve fund will be maintained until all of the payment obligations arising from the financing agreement described in Note 12 have been settled.

9. Cash and cash equivalents

The breakdown of the balance of this heading in the balance sheets at 31 December 2013 and 2012 is as follows:

2013 2012

Cash at banks 3,683,107 3,520,415

TOTAL 3,683,107 3,520,415 At 2013 and 2012 year end, the entire balance of this heading is unrestricted.

10. Equity and shareholders’ equity

10.1) Share capital

The share capital at 31 December 2013 and 2012 amounted to EUR 14,280,000, divided into fully subscribed and paid equal shares of EUR 680 par value each. The detail of the shareholders at 31 December 2013 and 2012 is as follows:

% Ownership Shares Ownership amount in euros

Energía y Recursos Ambientales, S.A. 90.00 18,900 12,852,000

Eólica FFMA 2E S.L 10.00 2,100 1,428,000

Total 100.00 21,000 14,280,000

10.2) Legal and statutary reserves

Under article 274 of the Consolidated Spanish Corporate Enterprises Law, 10% of net profit for each year must be transferred to the Legal and statutary reserves until the balance of this reserve reaches at least 20% of the share capital. The Legal and statutary reserves cannot be distributed to shareholders except in the event of liquidation. The Legal and statutary reserves can be used to increase capital provided that the remaining reserve balance does not fall below 10% of the increased share capital amount.

19

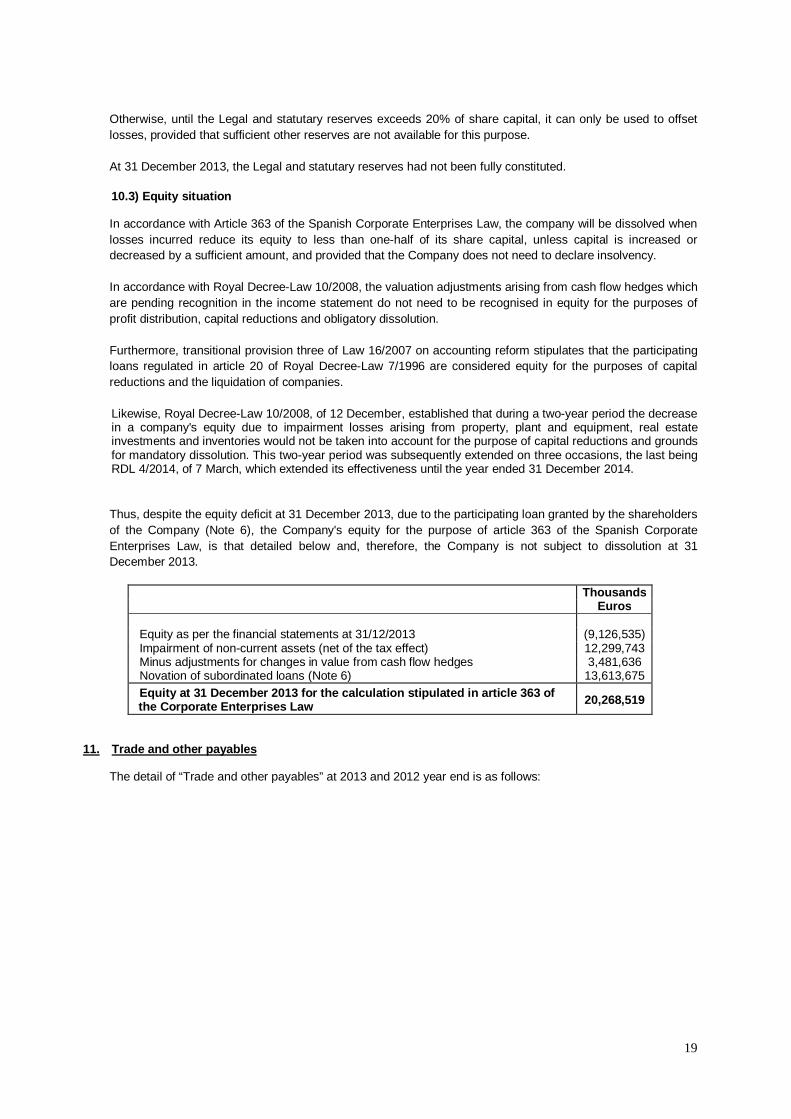

Otherwise, until the Legal and statutary reserves exceeds 20% of share capital, it can only be used to offset losses, provided that sufficient other reserves are not available for this purpose. At 31 December 2013, the Legal and statutary reserves had not been fully constituted.

10.3) Equity situation

In accordance with Article 363 of the Spanish Corporate Enterprises Law, the company will be dissolved when losses incurred reduce its equity to less than one-half of its share capital, unless capital is increased or decreased by a sufficient amount, and provided that the Company does not need to declare insolvency. In accordance with Royal Decree-Law 10/2008, the valuation adjustments arising from cash flow hedges which are pending recognition in the income statement do not need to be recognised in equity for the purposes of profit distribution, capital reductions and obligatory dissolution. Furthermore, transitional provision three of Law 16/2007 on accounting reform stipulates that the participating loans regulated in article 20 of Royal Decree-Law 7/1996 are considered equity for the purposes of capital reductions and the liquidation of companies. Likewise, Royal Decree-Law 10/2008, of 12 December, established that during a two-year period the decrease in a company's equity due to impairment losses arising from property, plant and equipment, real estate investments and inventories would not be taken into account for the purpose of capital reductions and grounds for mandatory dissolution. This two-year period was subsequently extended on three occasions, the last being RDL 4/2014, of 7 March, which extended its effectiveness until the year ended 31 December 2014.

Thus, despite the equity deficit at 31 December 2013, due to the participating loan granted by the shareholders of the Company (Note 6), the Company's equity for the purpose of article 363 of the Spanish Corporate Enterprises Law, is that detailed below and, therefore, the Company is not subject to dissolution at 31 December 2013.

Thousands Euros

Equity as per the financial statements at 31/12/2013 (9,126,535) Impairment of non-current assets (net of the tax effect) 12,299,743 Minus adjustments for changes in value from cash flow hedges 3,481,636 Novation of subordinated loans (Note 6) 13,613,675 Equity at 31 December 2013 for the calculation stip ulated in article 363 of the Corporate Enterprises Law 20,268,519

11. Trade and other payables

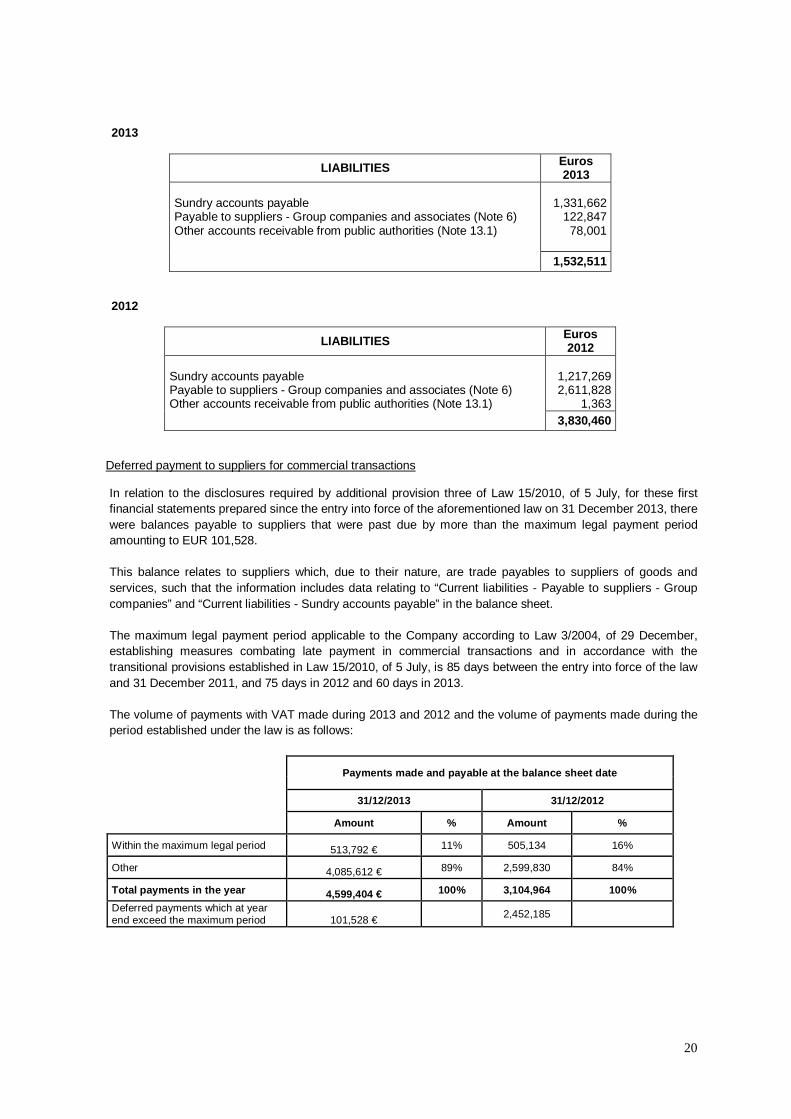

The detail of “Trade and other payables” at 2013 and 2012 year end is as follows:

20

2013

LIABILITIES Euros 2013

Sundry accounts payable Payable to suppliers - Group companies and associates (Note 6) Other accounts receivable from public authorities (Note 13.1)

1,331,662

122,847 78,001

1,532,511

2012

LIABILITIES Euros 2012

Sundry accounts payable Payable to suppliers - Group companies and associates (Note 6) Other accounts receivable from public authorities (Note 13.1)

1,217,269 2,611,828

1,363 3,830,460

Deferred payment to suppliers for commercial transactions

In relation to the disclosures required by additional provision three of Law 15/2010, of 5 July, for these first financial statements prepared since the entry into force of the aforementioned law on 31 December 2013, there were balances payable to suppliers that were past due by more than the maximum legal payment period amounting to EUR 101,528. This balance relates to suppliers which, due to their nature, are trade payables to suppliers of goods and services, such that the information includes data relating to “Current liabilities - Payable to suppliers - Group companies” and “Current liabilities - Sundry accounts payable” in the balance sheet. The maximum legal payment period applicable to the Company according to Law 3/2004, of 29 December, establishing measures combating late payment in commercial transactions and in accordance with the transitional provisions established in Law 15/2010, of 5 July, is 85 days between the entry into force of the law and 31 December 2011, and 75 days in 2012 and 60 days in 2013. The volume of payments with VAT made during 2013 and 2012 and the volume of payments made during the period established under the law is as follows:

Payments made and payable at the balance sheet date

31/12/2013 31/12/2012

Amount % Amount %

Within the maximum legal period 513,792 € 11% 505,134 16%

Other 4,085,612 € 89% 2,599,830 84%

Total payments in the year 4,599,404 € 100% 3,104,964 100%

Deferred payments which at year end exceed the maximum period 101,528 € 2,452,185

21

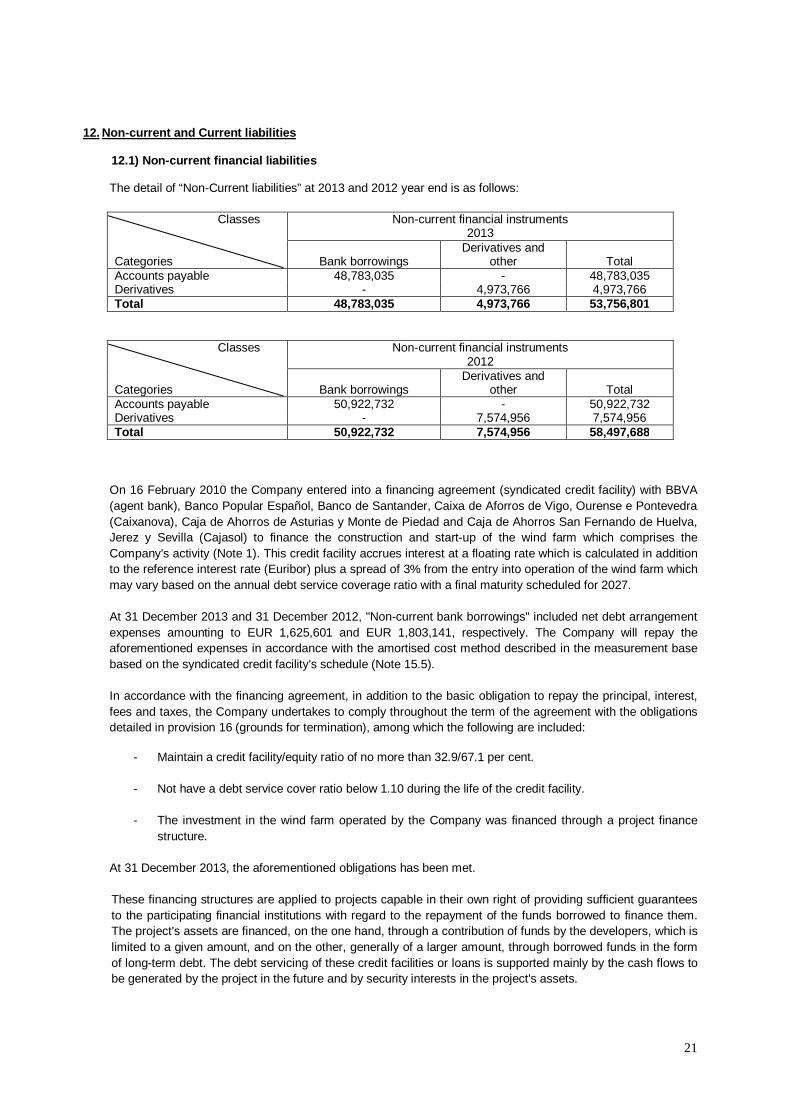

12. Non-current and Current liabilities

12.1) Non-current financial liabilities

The detail of “Non-Current liabilities” at 2013 and 2012 year end is as follows:

On 16 February 2010 the Company entered into a financing agreement (syndicated credit facility) with BBVA (agent bank), Banco Popular Español, Banco de Santander, Caixa de Aforros de Vigo, Ourense e Pontevedra (Caixanova), Caja de Ahorros de Asturias y Monte de Piedad and Caja de Ahorros San Fernando de Huelva, Jerez y Sevilla (Cajasol) to finance the construction and start-up of the wind farm which comprises the Company's activity (Note 1). This credit facility accrues interest at a floating rate which is calculated in addition to the reference interest rate (Euribor) plus a spread of 3% from the entry into operation of the wind farm which may vary based on the annual debt service coverage ratio with a final maturity scheduled for 2027. At 31 December 2013 and 31 December 2012, "Non-current bank borrowings" included net debt arrangement expenses amounting to EUR 1,625,601 and EUR 1,803,141, respectively. The Company will repay the aforementioned expenses in accordance with the amortised cost method described in the measurement base based on the syndicated credit facility's schedule (Note 15.5). In accordance with the financing agreement, in addition to the basic obligation to repay the principal, interest, fees and taxes, the Company undertakes to comply throughout the term of the agreement with the obligations detailed in provision 16 (grounds for termination), among which the following are included:

- Maintain a credit facility/equity ratio of no more than 32.9/67.1 per cent.

- Not have a debt service cover ratio below 1.10 during the life of the credit facility.

- The investment in the wind farm operated by the Company was financed through a project finance structure.

At 31 December 2013, the aforementioned obligations has been met. These financing structures are applied to projects capable in their own right of providing sufficient guarantees to the participating financial institutions with regard to the repayment of the funds borrowed to finance them. The project's assets are financed, on the one hand, through a contribution of funds by the developers, which is limited to a given amount, and on the other, generally of a larger amount, through borrowed funds in the form of long-term debt. The debt servicing of these credit facilities or loans is supported mainly by the cash flows to be generated by the project in the future and by security interests in the project's assets.

Classes Non-current financial instruments 2013

Categories Bank borrowings

Derivatives and other Total

Accounts payable 48,783,035 - 48,783,035 Derivatives - 4,973,766 4,973,766 Total 48,783,035 4,973,766 53,756,801

Classes Non-current financial instruments 2012

Categories Bank borrowings

Derivatives and other Total

Accounts payable 50,922,732 - 50,922,732 Derivatives - 7,574,956 7,574,956 Total 50,922,732 7,574,956 58,497,688

22

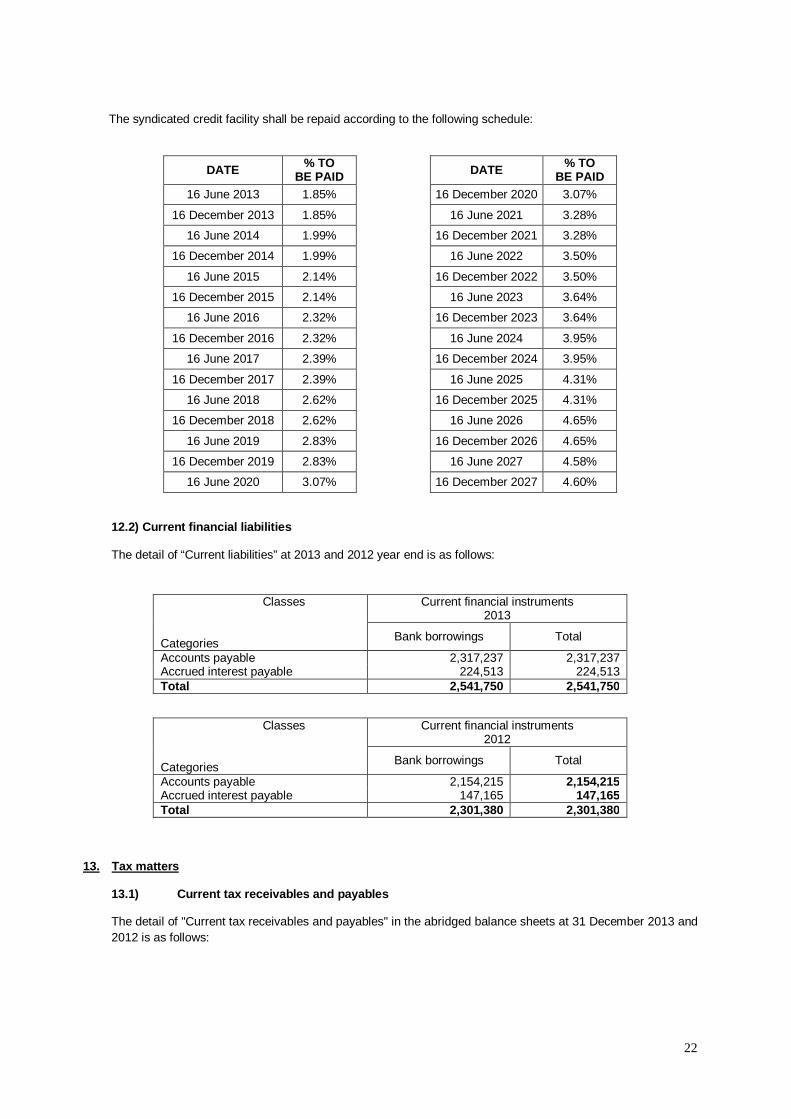

The syndicated credit facility shall be repaid according to the following schedule:

DATE % TO BE PAID

DATE % TO BE PAID

16 June 2013 1.85% 16 December 2020 3.07%

16 December 2013 1.85% 16 June 2021 3.28%

16 June 2014 1.99% 16 December 2021 3.28%

16 December 2014 1.99% 16 June 2022 3.50%

16 June 2015 2.14% 16 December 2022 3.50%

16 December 2015 2.14% 16 June 2023 3.64%

16 June 2016 2.32% 16 December 2023 3.64%

16 December 2016 2.32% 16 June 2024 3.95%

16 June 2017 2.39% 16 December 2024 3.95%

16 December 2017 2.39% 16 June 2025 4.31%

16 June 2018 2.62% 16 December 2025 4.31%

16 December 2018 2.62% 16 June 2026 4.65%

16 June 2019 2.83% 16 December 2026 4.65%

16 December 2019 2.83% 16 June 2027 4.58%

16 June 2020 3.07% 16 December 2027 4.60%

12.2) Current financial liabilities The detail of “Current liabilities” at 2013 and 2012 year end is as follows:

13. Tax matters

13.1) Current tax receivables and payables

The detail of "Current tax receivables and payables" in the abridged balance sheets at 31 December 2013 and 2012 is as follows:

Classes Current financial instruments 2013

Categories

Bank borrowings Total

Accounts payable 2,317,237 2,317,237 Accrued interest payable 224,513 224,513 Total 2,541,750 2,541,750

Classes Current financial instruments 2012

Categories

Bank borrowings Total

Accounts payable 2,154,215 2,154,215 Accrued interest payable 147,165 147,165 Total 2,301,380 2,301,380

23

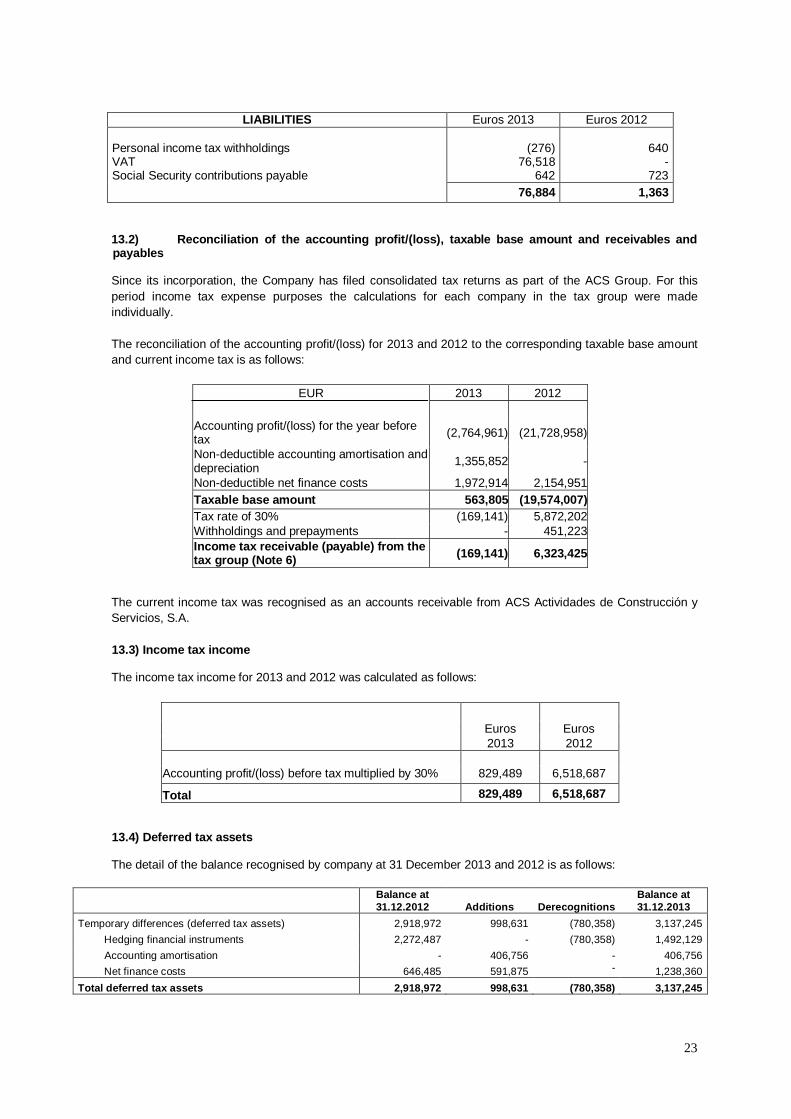

LIABILITIES Euros 2013 Euros 2012 Personal income tax withholdings VAT Social Security contributions payable

(276)

76,518 642

640

- 723

76,884 1,363 13.2) Reconciliation of the accounting profit/(loss), taxable base amount and receivables and payables

Since its incorporation, the Company has filed consolidated tax returns as part of the ACS Group. For this period income tax expense purposes the calculations for each company in the tax group were made individually. The reconciliation of the accounting profit/(loss) for 2013 and 2012 to the corresponding taxable base amount and current income tax is as follows:

EUR 2013 2012

Accounting profit/(loss) for the year before tax (2,764,961) (21,728,958)

Non-deductible accounting amortisation and depreciation

1,355,852 -

Non-deductible net finance costs 1,972,914 2,154,951Taxable base amount 563,805 (19,574,007)Tax rate of 30% (169,141) 5,872,202Withholdings and prepayments - 451,223Income tax receivable (payable) from the tax group (Note 6) (169,141) 6,323,425

The current income tax was recognised as an accounts receivable from ACS Actividades de Construcción y Servicios, S.A.

13.3) Income tax income

The income tax income for 2013 and 2012 was calculated as follows:

Euros Euros 2013 2012

Accounting profit/(loss) before tax multiplied by 30% 829,489 6,518,687

Total 829,489 6,518,687 13.4) Deferred tax assets The detail of the balance recognised by company at 31 December 2013 and 2012 is as follows:

Balance at 31.12.2012 Additions

Derecognitions

Balance at 31.12.2013

Temporary differences (deferred tax assets) 2,918,972 998,631 (780,358) 3,137,245

Hedging financial instruments 2,272,487 - (780,358) 1,492,129

Accounting amortisation - 406,756 - 406,756

Net finance costs 646,485 591,875 - 1,238,360

Total deferred tax assets 2,918,972 998,631 (780,358) 3,137,245

24

The amount of the temporary differences relates to the tax effect of following items: - The value of the derivative hedging instrument at 2013 and 2012 year end (Note 4.3.3).

- The net non-deductible finance costs for the year based on Royal Decree-Law 12/2012, of 30 March, limiting the deduction of "net finance costs", in general, to a maximum of 30% of the "operating profit for the year". For these purposes, the law determines "net finance costs" as the excess finance costs with respect to the income arising from the transfer to third parties of equity incurred in the tax period. In any case, up to EUR 1 million in net finance costs for the period, without any limit, are deductible. The net finance costs which have not been deducted may be deducted in the tax periods which conclude in the immediate and consecutive 18 years, together with those of the corresponding tax period.

- Non-deductible amortisation and depreciation expenses for the year: in accordance with the change implemented by Law 16/2012 effective for tax periods beginning in 2013 and 2014, the accounting amortisation and depreciation of property, plant and equipment, intangible assets and real estate investments may only be deducted up to 70% of the amount which would have been deductible for tax purposes in accordance with sections 1 and 4 of article 11 of the Consolidated Text of the Spanish Income Tax Law. The accounting amortisation and depreciation which is not deductible for tax purposes due to the application of this restriction, will not be considered impairment and will be deducted beginning from the first tax period of 2015 on a straight-line basis over a period of 10 years or over the course of the asset's useful life, at the Company's choice.

The deferred tax assets indicated above were recognised in the balance sheet because the Company’s sole director considered that, based on his best estimate of the project and the estimates of the tax group to which it belongs, in accordance with the Company's economic and financial model and the expected cash flows, it is likely that these assets will be recovered. Royal Decree-Law 9/2011, of 19 August, on measure to improve the quality and cohesion of the national health system, consolidated tax filing and assessment of the maximum amount of State guarantees for 2011, introduces amendments to the Consolidated Spanish Income Tax Law approved by Royal Legislative Decree 4/2004, of 5 March. Of these amendments, it is worth noting that for the tax periods beginning on or after 1 January 2012, duly reported tax losses can be offset against the taxable profits of the tax periods ending in the 18 successive years immediately following that in which they arose. 13.5) Years open for review by the tax authorities and tax audits

Under current legislation, taxes cannot be deemed to have been definitely settled until the tax returns have been reviewed by the tax authorities or until the statute-of-limitation period has expired. At 31 December 2013, the Company has the last four years open for review for all the taxes applicable to it, as well as income tax since 2009 and VAT since 2010 because it belongs to the tax group. At present, specifically, VAT from 2008 to 2010 of the Group to which the Company belongs is being reviewed. The Company's sole director considers that the tax returns for the various taxes have been filed correctly and, therefore, even in the event of discrepancies in the interpretation of current tax legislation in relation to the tax treatment afforded to certain transactions, such liabilities as might arise would not have a material effect on the accompanying financial statements for the year ended 31 December 2013 and, thus, no provision was recorded in this connection. The system for determining transfer prices is adequately designed with a view to complying with tax legislation. Therefore, transfer prices are adequately supported and there are no material risks in this connection.

25

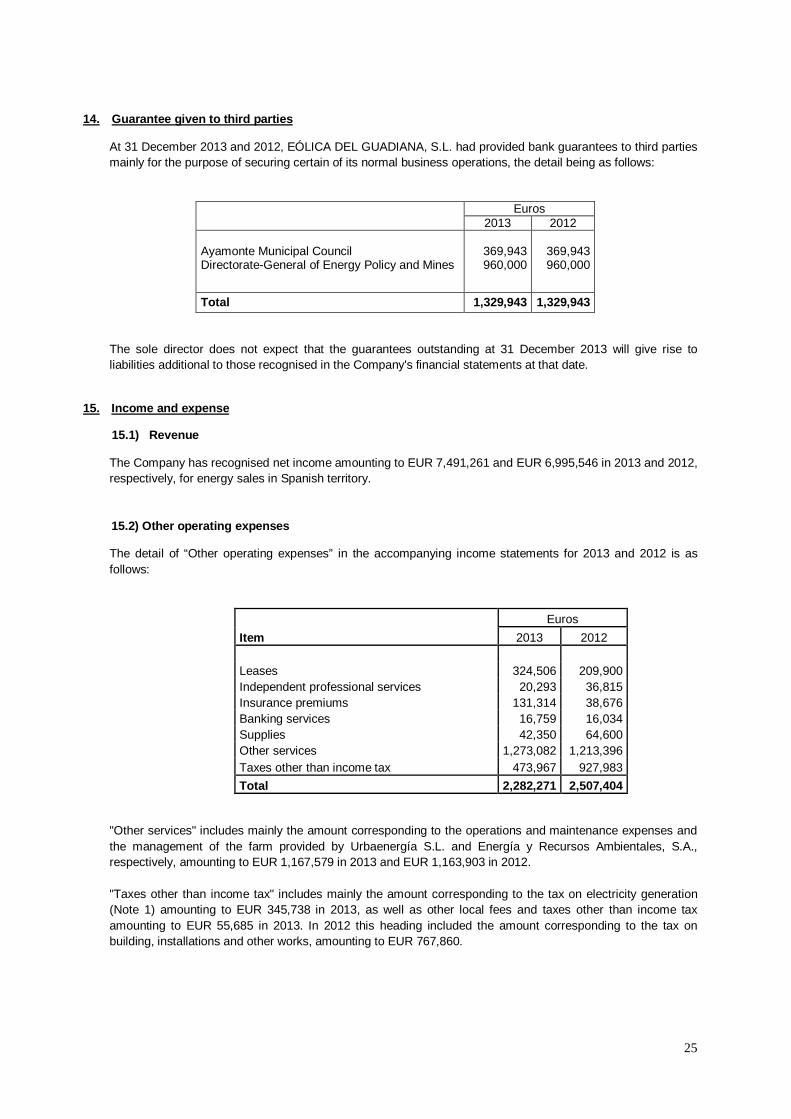

14. Guarantee given to third parties

At 31 December 2013 and 2012, EÓLICA DEL GUADIANA, S.L. had provided bank guarantees to third parties mainly for the purpose of securing certain of its normal business operations, the detail being as follows:

Euros 2013 2012 Ayamonte Municipal Council Directorate-General of Energy Policy and Mines

369,943 960,000

369,943 960,000

Total 1,329,943 1,329,943

The sole director does not expect that the guarantees outstanding at 31 December 2013 will give rise to liabilities additional to those recognised in the Company's financial statements at that date.

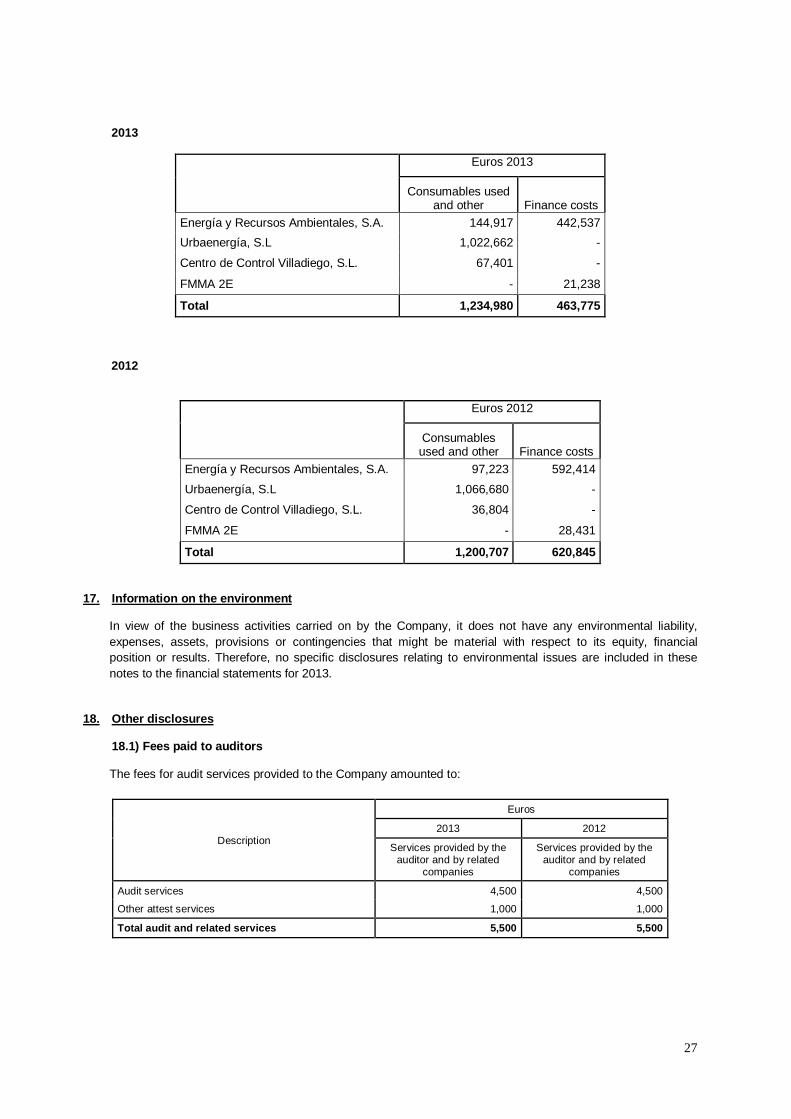

15. Income and expense

15.1) Revenue The Company has recognised net income amounting to EUR 7,491,261 and EUR 6,995,546 in 2013 and 2012, respectively, for energy sales in Spanish territory. 15.2) Other operating expenses The detail of “Other operating expenses” in the accompanying income statements for 2013 and 2012 is as follows:

Euros

Item 2013 2012 Leases 324,506 209,900 Independent professional services 20,293 36,815 Insurance premiums 131,314 38,676 Banking services 16,759 16,034 Supplies 42,350 64,600 Other services 1,273,082 1,213,396 Taxes other than income tax 473,967 927,983

Total 2,282,271 2,507,404 "Other services" includes mainly the amount corresponding to the operations and maintenance expenses and the management of the farm provided by Urbaenergía S.L. and Energía y Recursos Ambientales, S.A., respectively, amounting to EUR 1,167,579 in 2013 and EUR 1,163,903 in 2012. "Taxes other than income tax" includes mainly the amount corresponding to the tax on electricity generation (Note 1) amounting to EUR 345,738 in 2013, as well as other local fees and taxes other than income tax amounting to EUR 55,685 in 2013. In 2012 this heading included the amount corresponding to the tax on building, installations and other works, amounting to EUR 767,860.

26

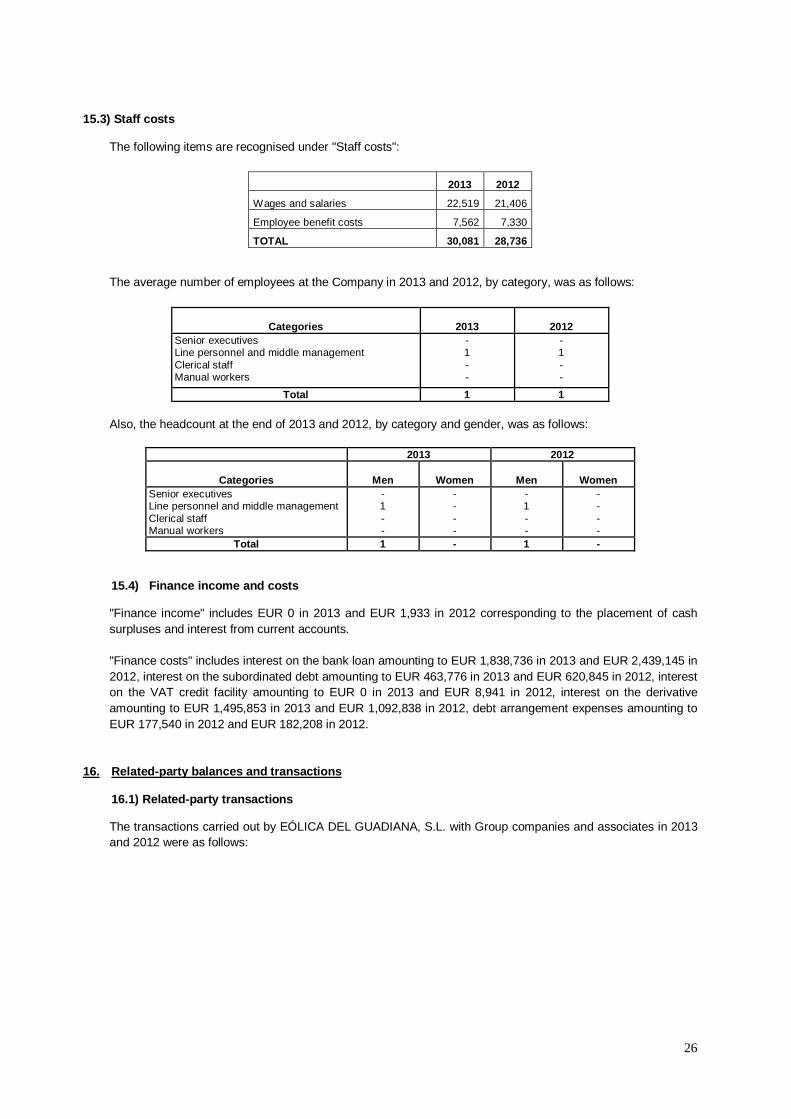

15.3) Staff costs The following items are recognised under "Staff costs":

2013 2012

Wages and salaries 22,519 21,406

Employee benefit costs 7,562 7,330

TOTAL 30,081 28,736

The average number of employees at the Company in 2013 and 2012, by category, was as follows:

Categories

2013

2012

Senior executives Line personnel and middle management Clerical staff Manual workers

- 1 - -

- 1 - -

Total 1 1

Also, the headcount at the end of 2013 and 2012, by category and gender, was as follows:

2013 2012

Categories

Men

Women

Men

Women Senior executives Line personnel and middle management Clerical staff Manual workers

- 1 - -

- - - -

- 1 - -

- - - -