energy and co2 emissions outlook world energy outlook - 2006 … · © oecd/iea - 2007...

TRANSCRIPT

© OECD/IEA - 2007

INTERNATIONAL ENERGY AGENCY

Energy and COEnergy and CO22 Emissions OutlookEmissions OutlookWorld Energy Outlook World Energy Outlook -- 20062006

Laura CozziEconomic Analysis Division

© OECD/IEA - 2007

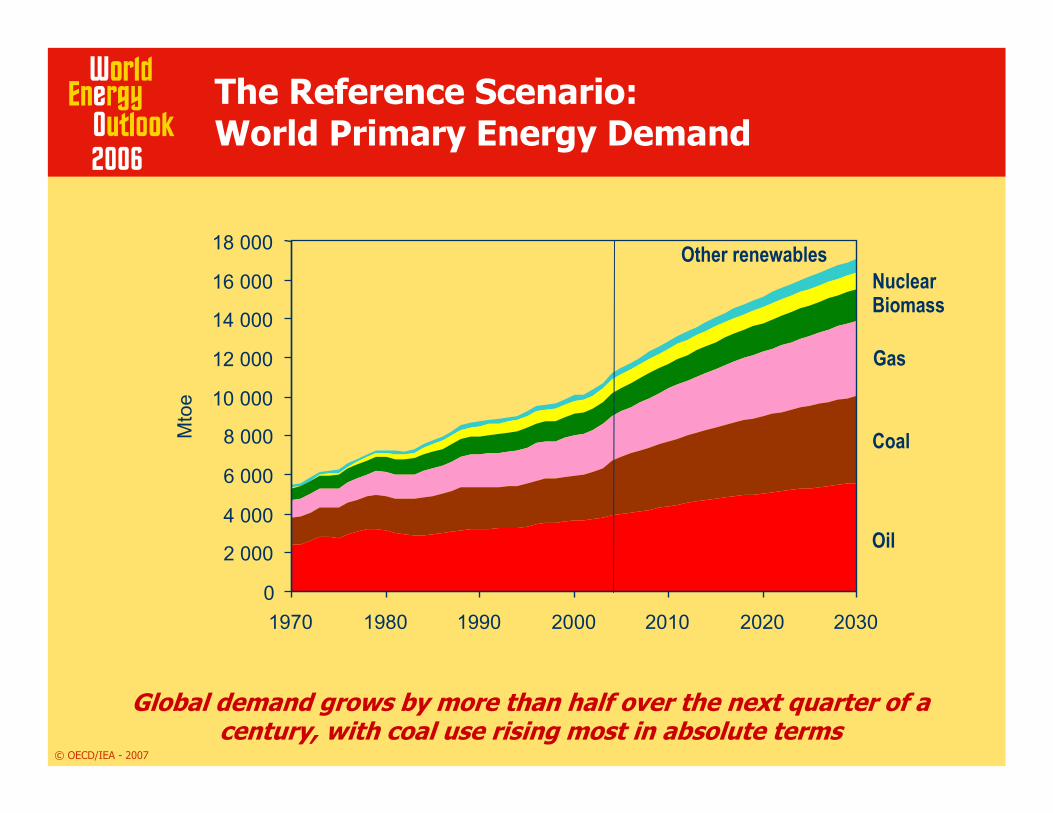

The Reference Scenario: World Primary Energy Demand

Global demand grows by more than half over the next quarter of acentury, with coal use rising most in absolute terms

Oil

Coal

Gas

BiomassNuclear

Other renewables

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

1970 1980 1990 2000 2010 2020 2030

Mto

e

© OECD/IEA - 2007

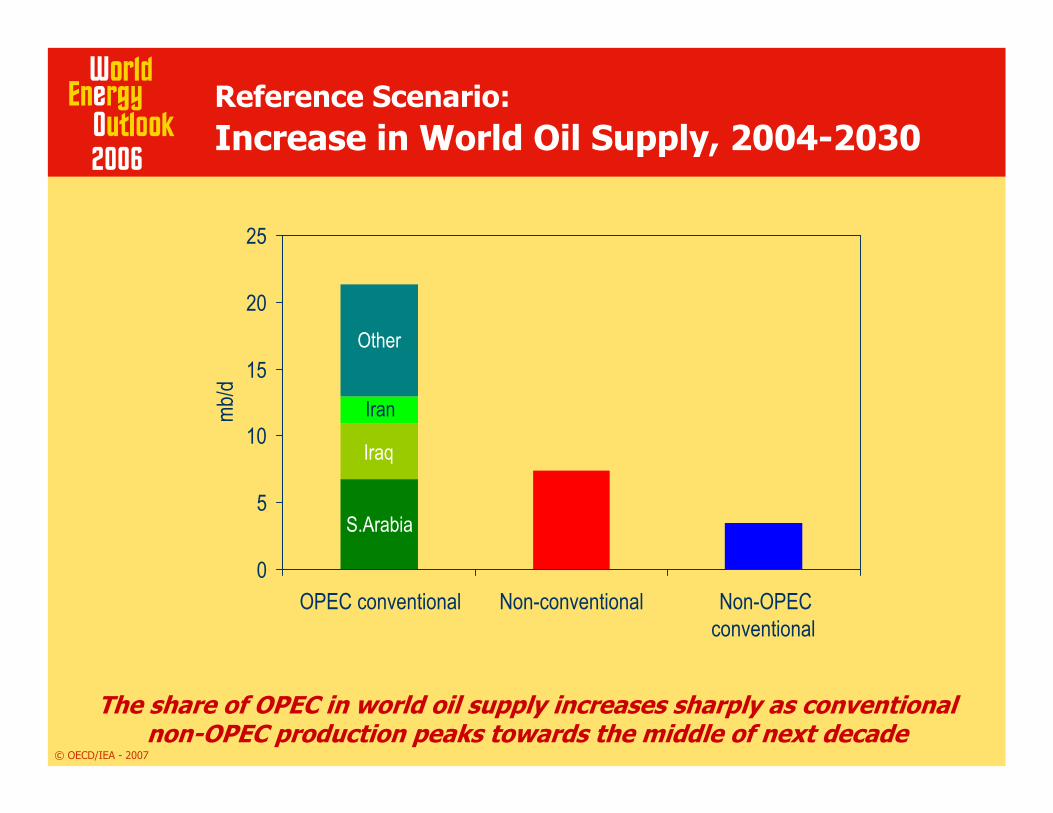

Reference Scenario:Increase in World Oil Supply, 2004-2030

The share of OPEC in world oil supply increases sharply as conventional non-OPEC production peaks towards the middle of next decade

S.Arabia

Iraq

Iran

Other

0

5

10

15

20

25

OPEC conventional Non-conventional Non-OPECconventional

mb/d

© OECD/IEA - 2007

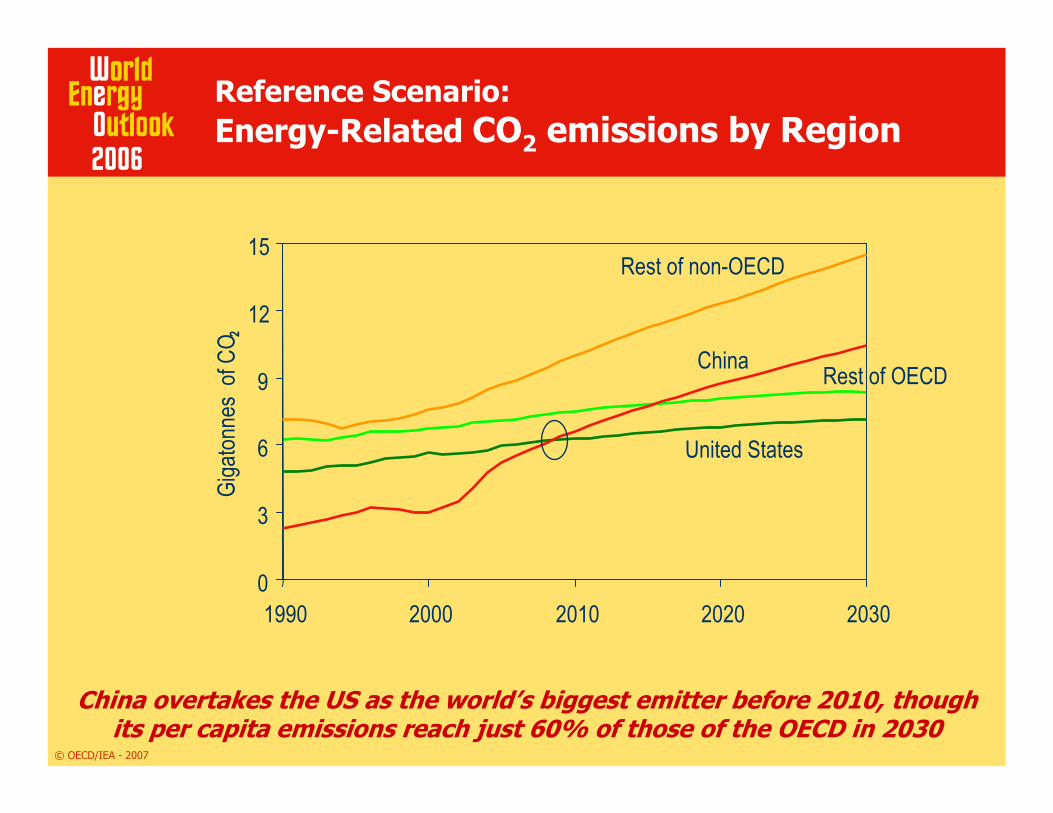

Reference Scenario:Energy-Related CO2 emissions by Region

China overtakes the US as the world’s biggest emitter before 2010, though its per capita emissions reach just 60% of those of the OECD in 2030

0

3

6

9

12

15

1990 2000 2010 2020 2030

Giga

tonne

sof

CO2

United States

China

Rest of non-OECD

Rest of OECD

© OECD/IEA - 2007

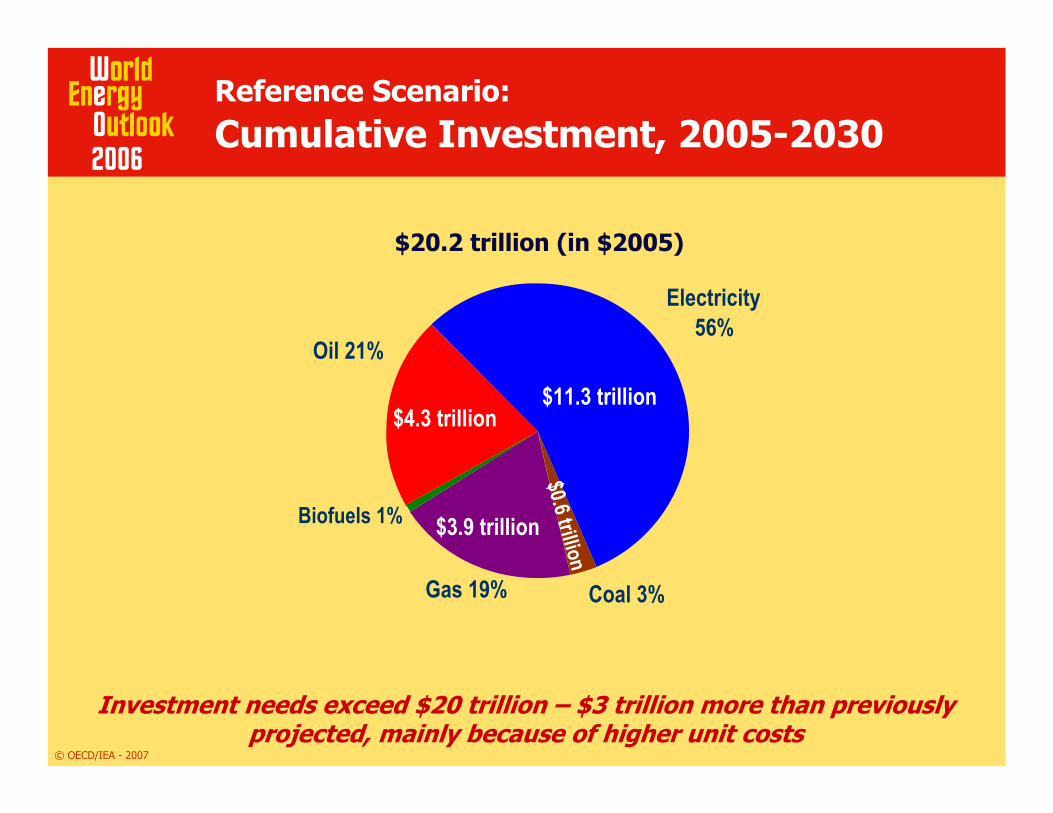

Oil 21%

Electricity56%

Coal 3%Gas 19%

Reference Scenario:Cumulative Investment, 2005-2030

Investment needs exceed $20 trillion – $3 trillion more than previously projected, mainly because of higher unit costs

$20.2 trillion (in $2005)

$4.3 trillion$11.3 trillion

$3.9 trillion$0.6 trillion

Biofuels 1%

© OECD/IEA - 2007

The Next Ten Years Will Determine Our Energy Future

Investment over the next decade will lock in technology for up to 60 years

China and India - growing at breakneck speed fueled by energy

OECD power plants – significant portion reaching to retirement

Security of supply is under threat because the balance of power is shifting

Oil production in non-OPEC countries is set to peak,

Gas production to peak in OECD

© OECD/IEA - 2007

INTERNATIONAL ENERGY AGENCY

Alternative Policy Scenario Alternative Policy Scenario

© OECD/IEA - 2007

Alternative Policy Scenario: Mapping a Better Energy Future

Analyses impact of government policies under consideration to enhance security & curb emissionsDemonstrates that we can significantly reduce growth in energy demand & emissions and stimulate alternative energy production

Oil demand is reduced by 13 mb/d in 2030 - equivalent to current output of Saudi Arabia & IranOil savings in 2015 savings reach 5 mb/d CO2 emissions are 6.3 Gt (16%) lower in 2030 –equivalent to the current emissions of US and Canada

Delaying action by 10 years would reduce the impact on emissions in 2030 by three-quarters

© OECD/IEA - 2007

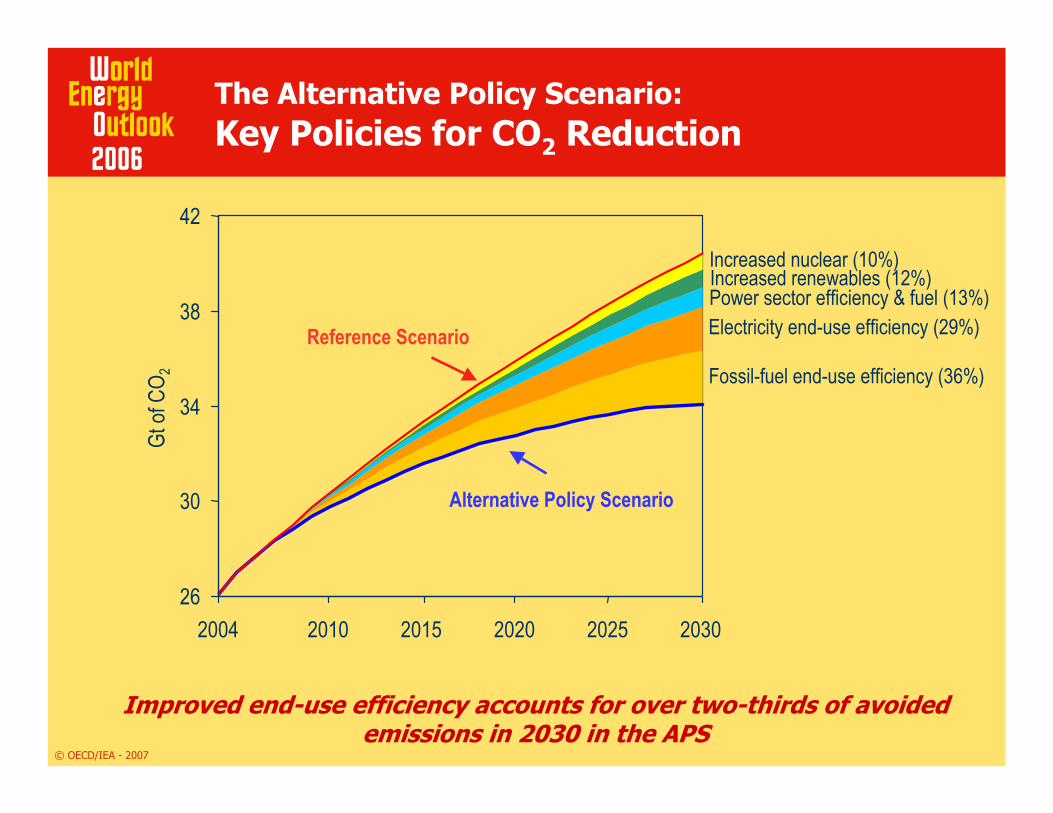

Improved end-use efficiency accounts for over two-thirds of avoided emissions in 2030 in the APS

Alternative Policy Scenario

Reference Scenario

Increased nuclear (10%)Increased renewables (12%)Power sector efficiency & fuel (13%) Electricity end-use efficiency (29%)

Fossil-fuel end-use efficiency (36%)

26

30

34

38

42

2004 2010 2015 2020 2025 2030

Gtof

CO2

The Alternative Policy Scenario:Key Policies for CO2 Reduction

© OECD/IEA - 2007

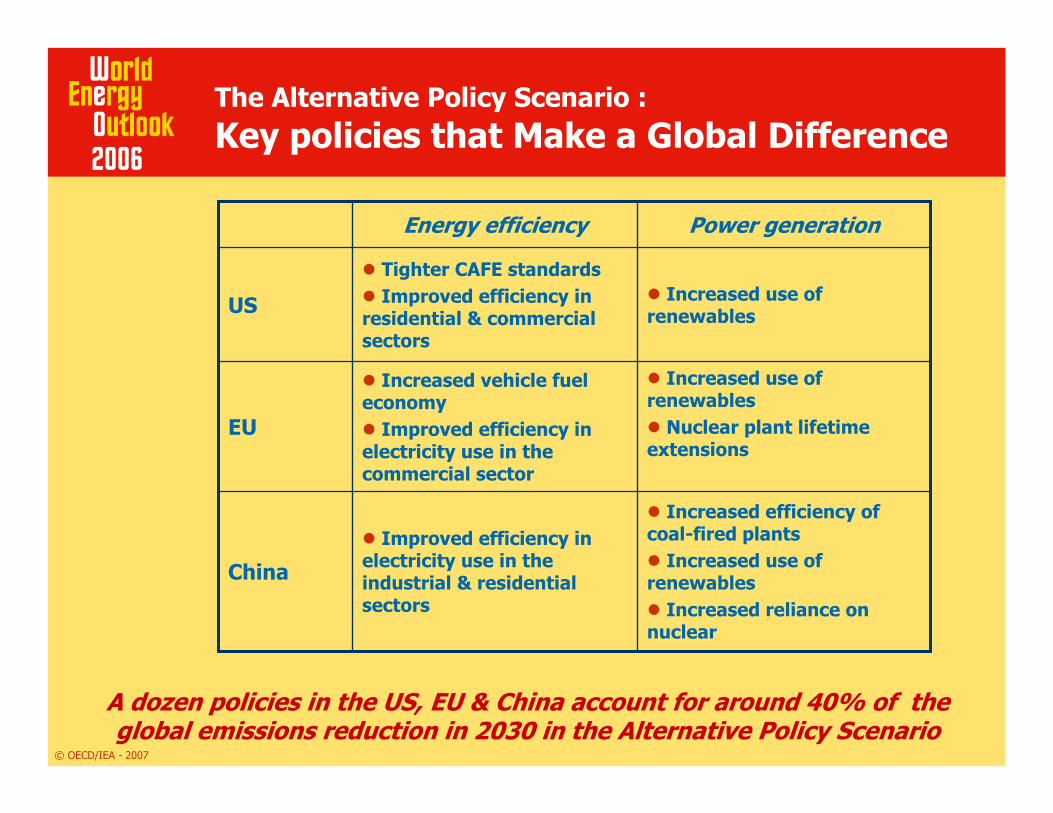

The Alternative Policy Scenario :Key policies that Make a Global Difference

A dozen policies in the US, EU & China account for around 40% of the global emissions reduction in 2030 in the Alternative Policy Scenario

Increased efficiency of coal-fired plants

Increased use of renewables

Increased reliance on nuclear

Improved efficiency in electricity use in the industrial & residential sectors

China

Increased use of renewables

Nuclear plant lifetime extensions

Increased vehicle fuel economy

Improved efficiency in electricity use in the commercial sector

EU

Increased use of renewables

Tighter CAFE standardsImproved efficiency in

residential & commercial sectors

US

Power generationEnergy efficiency

© OECD/IEA - 2007

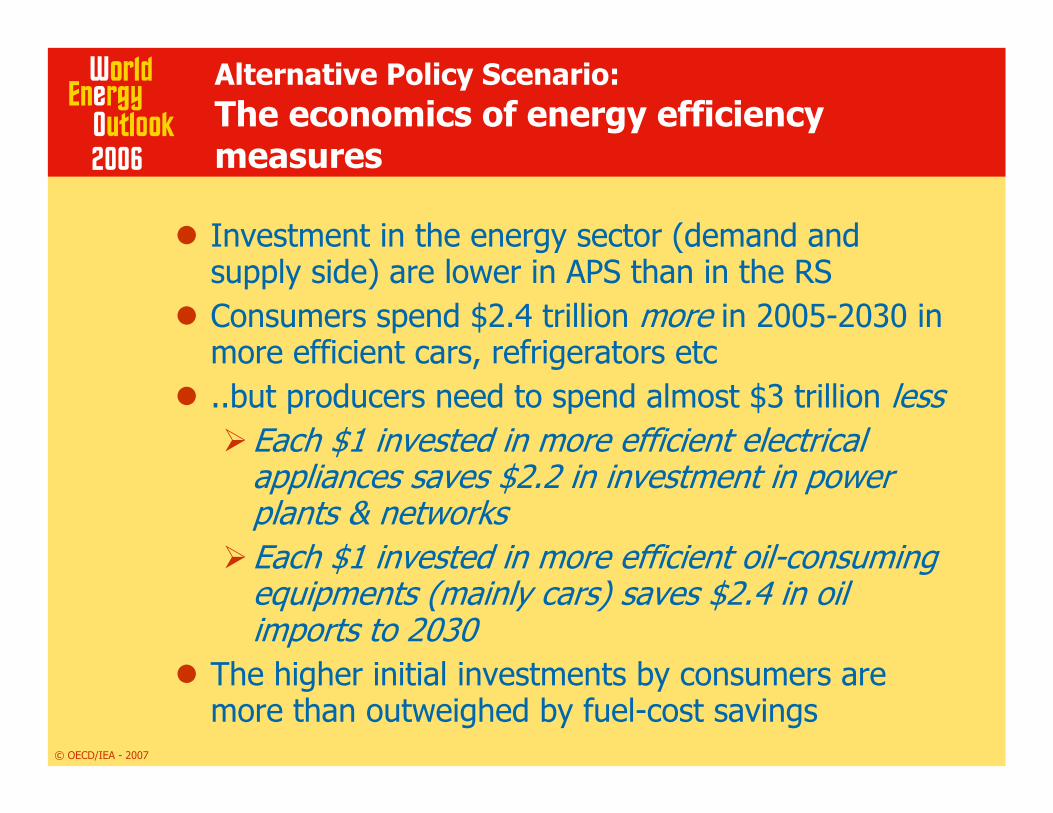

Alternative Policy Scenario:The economics of energy efficiency measures

Investment in the energy sector (demand and supply side) are lower in APS than in the RSConsumers spend $2.4 trillion more in 2005-2030 in more efficient cars, refrigerators etc..but producers need to spend almost $3 trillion less

Each $1 invested in more efficient electrical appliances saves $2.2 in investment in power plants & networksEach $1 invested in more efficient oil-consuming equipments (mainly cars) saves $2.4 in oil imports to 2030

The higher initial investments by consumers are more than outweighed by fuel-cost savings

© OECD/IEA - 2007

Reference Scenario

26

30

34

38

42

2004 2030

Gtof

CO2

Alternative Policy Scenario

Efficiency of electricity use CCS and efficiency in industry Biofuels and hybrids

Efficiency of power plants Nuclear power-plants Renewables-based generation

CCS in power generation 2015

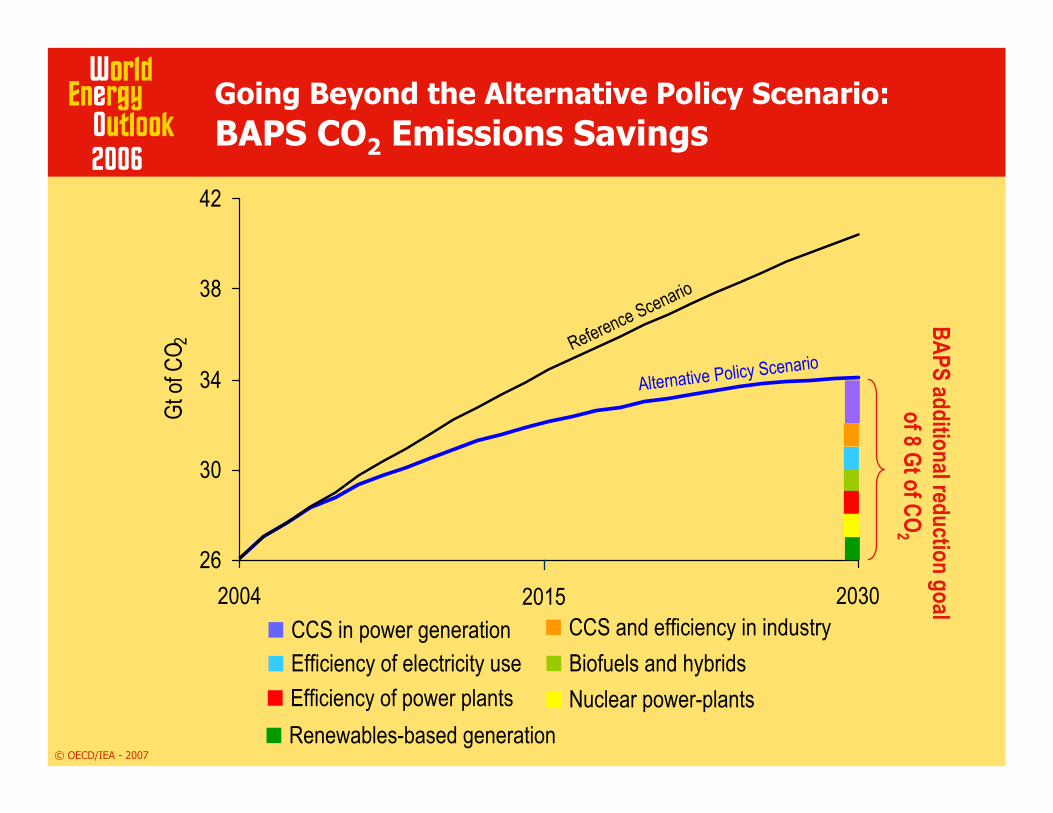

Going Beyond the Alternative Policy Scenario:BAPS CO2 Emissions Savings

BAPS additional reduction goalof 8 Gtof CO

2

© OECD/IEA - 2007

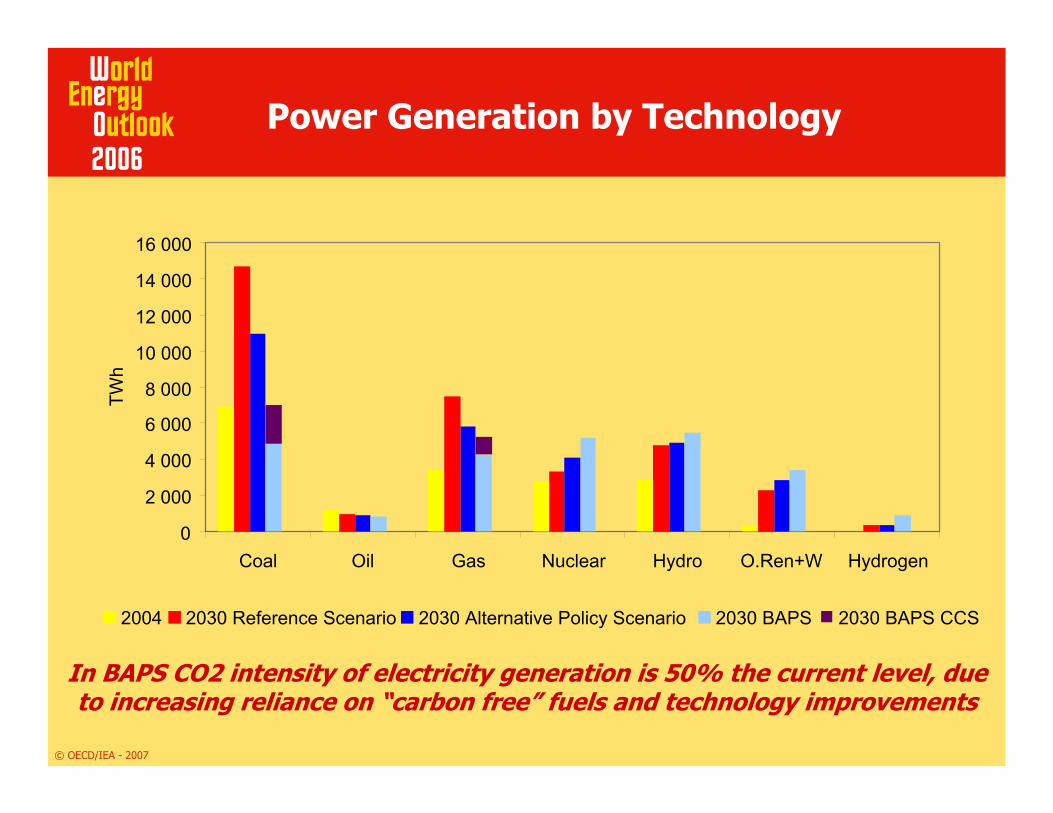

Power Generation by Technology

In BAPS CO2 intensity of electricity generation is 50% the current level, due to increasing reliance on “carbon free” fuels and technology improvements

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

Coal Oil Gas Nuclear Hydro O.Ren+W Hydrogen

TWh

2004 2030 Reference Scenario 2030 Alternative Policy Scenario 2030 BAPS 2030 BAPS CCS

© OECD/IEA - 2007

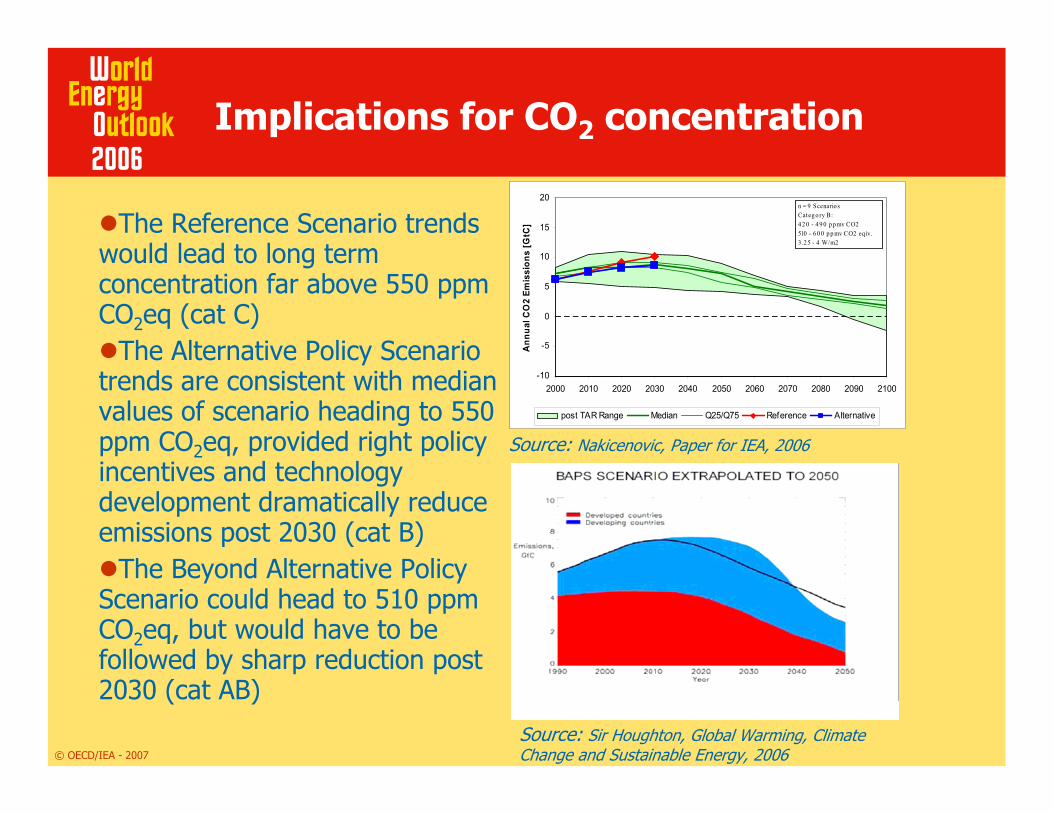

Implications for CO2 concentration

The Reference Scenario trends would lead to long term concentration far above 550 ppmCO2eq (cat C)

The Alternative Policy Scenario trends are consistent with median values of scenario heading to 550 ppm CO2eq, provided right policy incentives and technologydevelopment dramatically reduce emissions post 2030 (cat B)

The Beyond Alternative Policy Scenario could head to 510 ppmCO2eq, but would have to be followed by sharp reduction post 2030 (cat AB)

-10

-5

0

5

10

15

20

2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

Ann

ual C

O2

Emis

sion

s [G

tC]

post TAR Range Median Q25/Q75 Reference Alternative

n = 9 ScenariosCategory B:42 0 - 49 0 ppmv CO2510 - 6 00 pp mv CO2 eq iv.3 .25 - 4 W/m2

Source: Nakicenovic, Paper for IEA, 2006

Source: Sir Houghton, Global Warming, Climate Change and Sustainable Energy, 2006

© OECD/IEA - 2007

Summing Up

The Reference Scenario projects a vulnerable, dirty and expensive global energy systemThe Alternative Policy Scenario maps out a cleaner, cleverer and more competitive energy future based on new policies –mainly on energy efficiency, renewables and nuclear Strong political will and urgent government action is needed to change existing investment patterns and move Beyond the Alternative Policy Scenario

© OECD/IEA - 2007

Next steps – WEO 2007 & WEO 2008

WEO-2007 China and India insights In addition to RS and APS, high growth scenario is also exploredImplications for energy markets and global emissionsCo-operation with TERI, ERI and indian/chineseauthoritiesRelease: 7 November 2007

WEO-2008in-depth analysis of climate change scenarios –understanding energy implications of different post kyotointernational architecturesin-depth field by field analysis of top 200 oil producing fields