environmental & economic analysis into the impact of rhi

TRANSCRIPT

Environmental & Economic Analysis into the Impact of RHI Options

Renewable Heat Association Northern Ireland

April 2021

Contents

Key Observations............................................................................................................................... 1

1. Introduction & Background ..................................................................................................... 4

2. How has Renewable Heat usage in NI evolved? ................................................................ 9

3. What are the rural economy/socio-economic benefits of RHI? ................................... 14

4. What are the Environmental and Social Impacts of Biomass?.................................... 20

5. How has DfE developed the consultation process? ....................................................... 28

6. Do the assumptions behind DfE’s options hold? ........................................................... 36

7. What option represents the best balance of fairness and public spending? .......... 49

0

Key Observations

1

Key Observations

This report reflects Grant Thornton’s independent assessment of the various assumptions and

calculations applied to determine the financial implications of the non-domestic Renewable Heat

Incentive (RHI) Options presented by the Department for the Economy (DfE) as part of their 2021

‘Northern Ireland Non-Domestic Renewable Heat Incentive Scheme – Future of the Scheme’

consultation1. Based on our assessment, which notes what we regard as a series of omissions and

missteps in calculating tariffs and compensation rates, the report concludes with a proposal on the most

appropriate way forward for the RHI scheme. The analysis undertaken to produce this report leads to

the following key observations.

There is a clear societal and political imperative to controlling climate change. Not all of the options put forward in the 2021 Consultation paper are conducive to that position – indeed, whilst two would have an immediate opposite effect, the uncertainty that this process has created, will, in our opinion, have a damaging effect upon confidence in government and the acceptability of renewable energy alternatives.

That the Department knew, or might reasonably have been expected to know the accurate cost of heat generation from biomass, from LPG and from oil and might reasonably have been expected to use those costs in the calculation of the tariff payable .

That the positive effect of the cultivation and use of bioenergy crops is acknowledged by the UK Committee for Climate Change. Cultivation of sustainable forestry and bioenergy crops is widely accepted as positive for the environment. The options proposed in the consultation, if enacted, could have a significantly damaging economic impact on these enterprises – to a point that, without demand, there is no point in investment in them.

Considerable progress has been made in establishing a green economy for Northern Ireland. It is our opinion that this progress is at risk of being reversed if the Scheme is terminated. We estimate that if all participants in the non-domestic RHI scheme reverted to kerosene, this will generate 120,557 tonnes of CO2 in comparison to 16,629 tonnes for wood pellets per annum. The longer term dis-benefits will continue beyond the 15 years remaining of the Scheme

The Department had estimated that 480 boilers would, on the post 2019 tariffs fail to receive 12% RoR and thus, could be party to the voluntary buy-out arrangements. It is difficult to reconcile this statement with the assertion that a 12% RoR is available and impossible to reconcile this position with the Buglass assessment that case studies which he had analysed had a negative rate of return.

That the Department for the Economy, knew or, might reasonably have been expected to consistently identify the appropriate counter factual fuel, fuel volume and fuel price when instructing external consultants to make recommendations as to rebate tariffs.

For fairness, consistent, objective valuation of CAPEX and OPEX costs need to be the baseline for any calculation. We have concerns that, in this instance, they were not.

We have concerns that CAPEX cost analysis omits relevant and appropriate costs. These omissions make decision-making on the basis of such analysis, unsound.

We express concern regarding the accuracy of the cost-capture methodology. Without an accurate and sound baseline, calculation of an appropriate rate of return is not feasible.

1 https://www.economy-ni.gov.uk/consultations/northern-ireland-non-domestic-renewable-heat-incentive-scheme-future-scheme

2

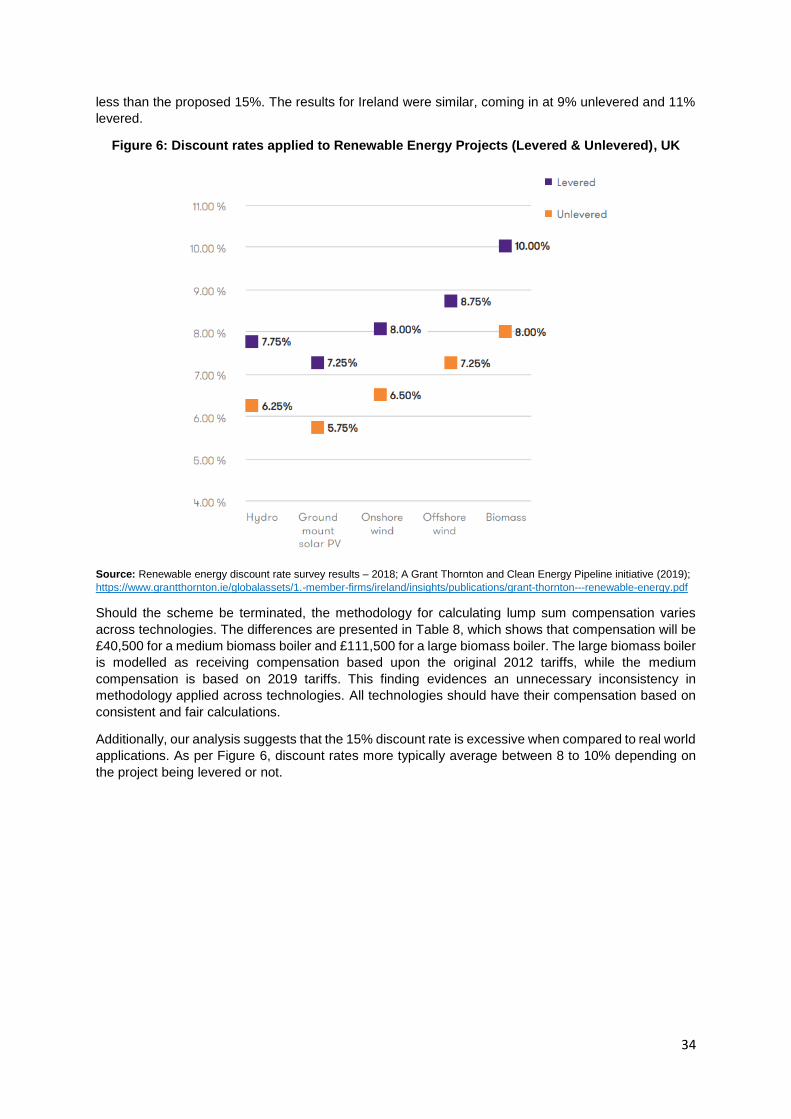

As with appropriate and accurate CAPEX & OPEX cost capture, the use of discount factors for the purpose of deployment in legislation, must be on a sound and reasoned basis. We note that the approach proposed is inconsistent with previous calculations.

The counterfactual fuel and price of that fuel is a key element in the calculation of an appropriate rebate tariff and will have a significant impact in determining behavioural change (from fossil fuels to renewable energy) is encouraged. If calculated incorrectly, it could have long-term implications.

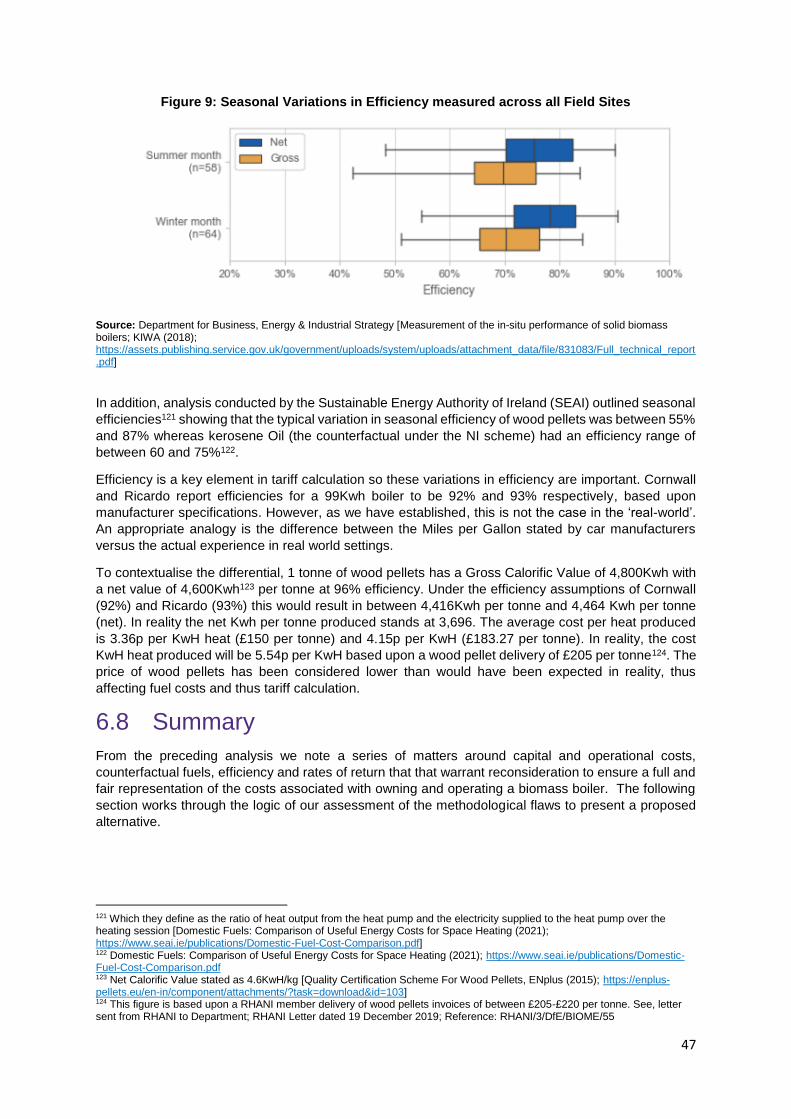

We judge fuel pricing to be a significant element in driving tariff mis-calculation. As may be seen from the graph below, selection of a (known) atypical price reference point exacerbates and compounds this matter.

System efficiency is a critical factor in the calculation of the cost of generation of heat. A mis-step in this calculation will compound other mis-steps in counterfactual fuel type/volume and therefore price calculation. The compounding effect may result in the theoretical (and incorrect) rebate calculated differing from the real-world experience of participants.

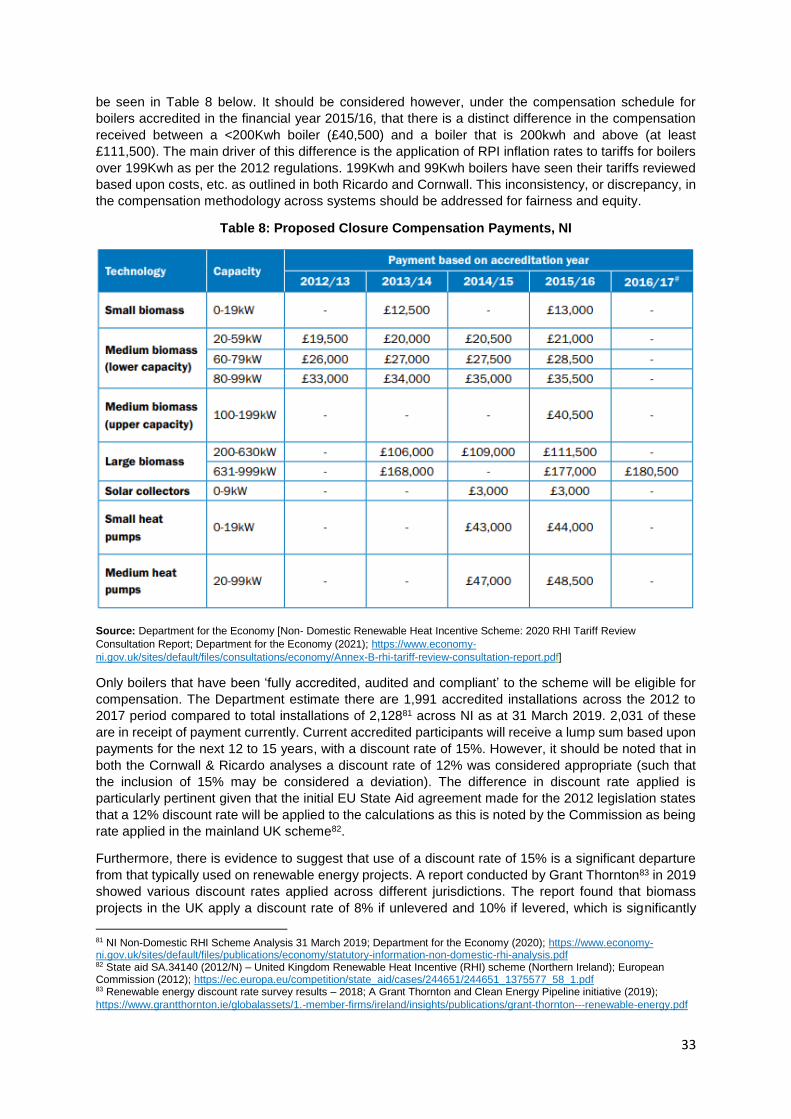

By using real-world data and applying a consistent discount rate, we have determined that the required compensation to terminate the DfE/participant relationship for systems accredited in 2015 is as follows, effective April 2020:

o 99 kWh boiler - £122,927

o 199 kWh boiler - £146,702

A key aim of the RHI scheme was carbon reduction. This is best achieved by keeping the

scheme open. Should the scheme continue a tariff calculation suggests an appropriate Tier 1

tariff of 9.06p/Kwh and a Tier 2 tariff of 2.95p/Kwh for a 99kw boiler and 6.43p/Kwh for a Tier 1

199 Kwh boiler.

3

1. Introduction & Background

4

1. Introduction &

Background

1.1 Introduction

Grant Thornton were commissioned by the Renewable Heat Association for Northern Ireland (RHANI)2

to carry out an economic review and analysis into the non-domestic Renewable Heat Incentive (RHI)

Options presented by the Department for the Economy (DfE) as part of their 2021 ‘Northern Ireland

Non-Domestic Renewable Heat Incentive Scheme – Future of the Scheme’ consultation3.

This report reflects Grant Thornton’s independent assessment of the various assumptions and

calculations applied to determine the financial implications of the RHI scheme options. Based on our

assessment, which notes what we regard as a series of omissions and missteps in calculating tariffs

and compensation rates, the report concludes with a proposal on the most appropriate way forward for

the RHI scheme.

Interestingly, during the course of writing this report, the GB non-domestic RHI scheme closed (on 31st

March 2021). ‘Closed’ in the GB context relates to new entrants rather than termination of the whole

scheme. This is a noteworthy and different context to the various NI options that have been proposed.

1.2 Background

The RHI scheme has been subject to two acts of primary legislation and a series of significant other

events. Table 1 summarises these key events.

Table 1: Non-Domestic RHI Chronology and key events Event Significance

2010: Strategic Energy Framework The Strategic Energy Framework, aimed to achieve a more secure and sustainable energy system where:

energy is as competitively priced as possible alongside robust security of supply

much more of our energy from renewable sources and the resulting economic opportunities are fully exploited

energy efficiency is maximised. 2012: The Renewable Heat Incentive Scheme Regulations (Northern Ireland) 2012

https://www.legislation.gov.uk/nisr/2012/396/contents/made

Regulations provided for the payment of a set tariff for a fixed period of 20 years to participants. As at 31 March 2019, there were 2,128 installations.

NI Audit Office4 notes that 564 of these applications were made between November 2012 and March 2015. Applications begin to

2 We are grateful to Balcas Timber Limited who also provided a financial contribution to the research. 3 https://www.economy-ni.gov.uk/consultations/northern-ireland-non-domestic-renewable-heat-incentive-scheme-future-scheme 4 https://www.niauditoffice.gov.uk/sites/niao/files/media-files/Final%20CAG%20Report%2028%20June%202016%20%28after%20typo%20correction%29.pdf

5

Event Significance

spike in 2015 (see below). Of greater importance are the 788 boilers admitted between April and October 2015 when the DFP authority to operate the scheme had lapsed, leading to the Comptroller and Auditor General to qualify the Department’s accounts5.

2015 –The Renewable Heat Incentive Schemes (Amendment) Regulations (Northern Ireland) 2015 (legislation.gov.uk)

https://www.legislation.gov.uk/nisr/2015/371/contents/made

The key point arising from these Regulations was that they introduced a tiering system and a cap on the heat eligible for tariff payments to all installations accredited after that date, in line with the GB scheme.

Between April 2015 and March 2016, 1,564 RHI applications were made, bringing the total to 2,128.

2016: Scheme Suspension

https://www.ofgem.gov.uk/publications-and-updates/suspension-northern-ireland-rhi#

The Renewable Heat Incentive (RHI) scheme was suspended to new applicants on 29 February 2016.

2016 Public Accounts Committee, Northern Ireland Assembly commence an inquiry into the actions of the Department for the Economy

The long-term environmental and economic impacts of curtailing the DfE RHI Scheme were fully understood in 2016 with evidence noting ‘that the consequence of what happened is very detrimental to growth.’6

2017 The Renewable Heat Incentive Scheme (Amendment) Regulations (Northern Ireland) 2017

https://www.legislation.gov.uk/nisr/2017/32/regulation/5/made

'Tiered' tariff system introduced for a reclassified (sub-100 kWh) band. The regime introduced an “initial,” 1st tier of 15% load, 1,314 hours of operation, followed by a lower valued tier to a maximum total number of operating hours for which payment would be made.

The 2017 Regulations were to have effect for 12 months; on expiry, the legislative construct was such that there was no authority to make payment to this cohort beyond 31 Mar 18. This gave rise to the need for the 2018 legislation passed by Westminster in the absence of a sitting Executive and Assembly.

2017: Public Inquiry A Public inquiry into the RHI scheme, chaired by Sir Patrick Coghlin, begins hearing evidence.

2018: Northern Ireland (Regional Rates and Energy) Act 2018

https://www.legislation.gov.uk/ukpga/2018/6/section/2/enacted

A 12-month continuation of the 2017 tariff for the small/medium cohort of approximately 1,900 systems (all sub 100 kWh).

2018: The future of the Non-Domestic Renewable Heat Incentive Scheme | Department for the Economy

Consultation sets out the Department's proposals for the future of the Non-Domestic Renewable Heat Incentive. 8 Options were proposed in the consultation, with the preferred option being to establish a new set of tariffs for all small and medium sized biomass boilers accredited to the scheme. The intention was to bring forward legislation to effect these changes. The Department’s proposed options are informed by Ricardo Energy and Environment (‘Ricardo’). The Ricardo Report identified “the extent to which the current NIRHI biomass tariffs are set at too high a level and suggested three main alternative tariff scenarios. Ricardo also estimated the projected cost to DfE and the rate of return to participants for each of the tariff scenarios compared with the current and previous tariff structures on the NI and GB RHI Schemes. Ricardo indicated that a subsidy was not required in respect of the CHP plants which applied to the NIRHI Scheme and suggested that it would now be appropriate to switch from the use of the Retail Prices Index (RPI) to the Consumer Prices Index (CPI) when calculating the annual inflationary uplift of tariff levels.” (DfE)

5 https://www.economy-ni.gov.uk/sites/default/files/publications/economy/DETI-Annual-Report-2015-16.pdf 6 https://www.youtube.com/watch?v=VF5PqC97rOU

6

Event Significance

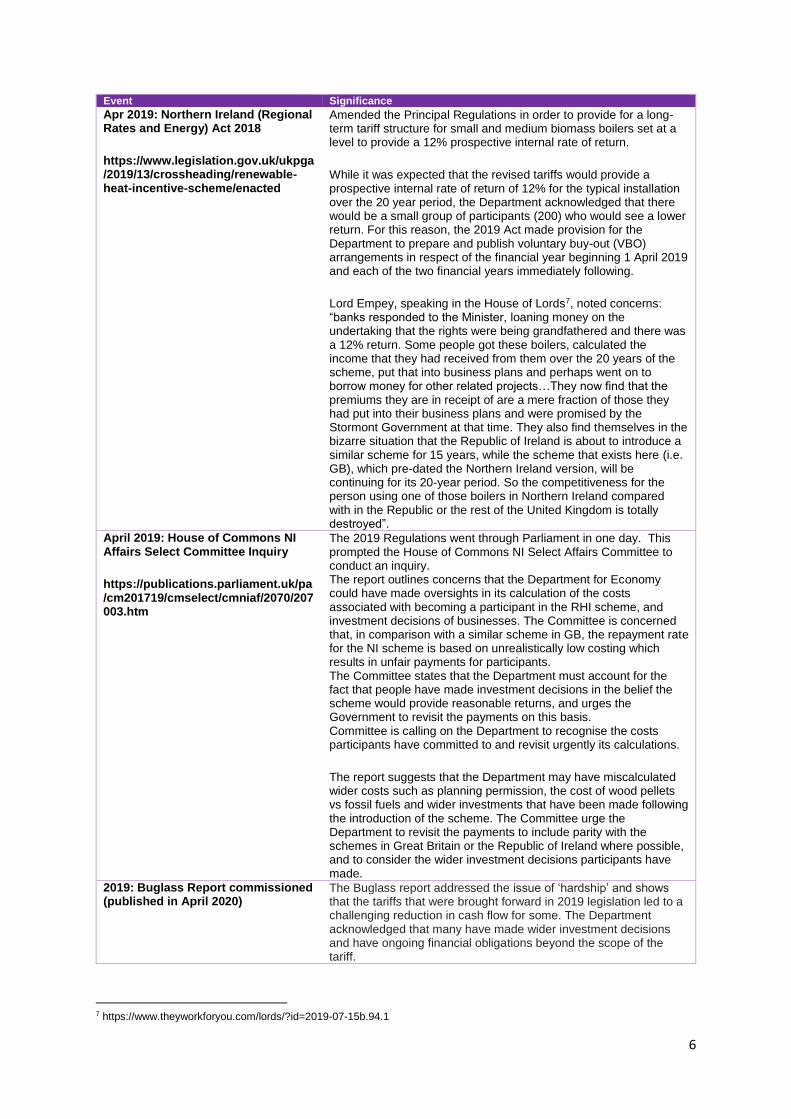

Apr 2019: Northern Ireland (Regional Rates and Energy) Act 2018

https://www.legislation.gov.uk/ukpga/2019/13/crossheading/renewable-heat-incentive-scheme/enacted

Amended the Principal Regulations in order to provide for a long-term tariff structure for small and medium biomass boilers set at a level to provide a 12% prospective internal rate of return.

While it was expected that the revised tariffs would provide a prospective internal rate of return of 12% for the typical installation over the 20 year period, the Department acknowledged that there would be a small group of participants (200) who would see a lower return. For this reason, the 2019 Act made provision for the Department to prepare and publish voluntary buy-out (VBO) arrangements in respect of the financial year beginning 1 April 2019 and each of the two financial years immediately following.

Lord Empey, speaking in the House of Lords7, noted concerns: “banks responded to the Minister, loaning money on the undertaking that the rights were being grandfathered and there was a 12% return. Some people got these boilers, calculated the income that they had received from them over the 20 years of the scheme, put that into business plans and perhaps went on to borrow money for other related projects…They now find that the premiums they are in receipt of are a mere fraction of those they had put into their business plans and were promised by the Stormont Government at that time. They also find themselves in the bizarre situation that the Republic of Ireland is about to introduce a similar scheme for 15 years, while the scheme that exists here (i.e. GB), which pre-dated the Northern Ireland version, will be continuing for its 20-year period. So the competitiveness for the person using one of those boilers in Northern Ireland compared with in the Republic or the rest of the United Kingdom is totally destroyed”.

April 2019: House of Commons NI Affairs Select Committee Inquiry

https://publications.parliament.uk/pa/cm201719/cmselect/cmniaf/2070/207003.htm

The 2019 Regulations went through Parliament in one day. This prompted the House of Commons NI Select Affairs Committee to conduct an inquiry. The report outlines concerns that the Department for Economy could have made oversights in its calculation of the costs associated with becoming a participant in the RHI scheme, and investment decisions of businesses. The Committee is concerned that, in comparison with a similar scheme in GB, the repayment rate for the NI scheme is based on unrealistically low costing which results in unfair payments for participants. The Committee states that the Department must account for the fact that people have made investment decisions in the belief the scheme would provide reasonable returns, and urges the Government to revisit the payments on this basis. Committee is calling on the Department to recognise the costs participants have committed to and revisit urgently its calculations.

The report suggests that the Department may have miscalculated wider costs such as planning permission, the cost of wood pellets vs fossil fuels and wider investments that have been made following the introduction of the scheme. The Committee urge the Department to revisit the payments to include parity with the schemes in Great Britain or the Republic of Ireland where possible, and to consider the wider investment decisions participants have made.

2019: Buglass Report commissioned (published in April 2020)

The Buglass report addressed the issue of ‘hardship’ and shows that the tariffs that were brought forward in 2019 legislation led to a challenging reduction in cash flow for some. The Department acknowledged that many have made wider investment decisions and have ongoing financial obligations beyond the scope of the tariff.

7 https://www.theyworkforyou.com/lords/?id=2019-07-15b.94.1

7

Event Significance

2020: RHI Inquiry Findings Published

https://wayback.archive-it.org/11112/20200911092828/https:/www.rhiinquiry.org/report-independent-public-inquiry-non-domestic-renewable-heat-incentive-rhi-scheme

RHI inquiry report published 13 March 2020

Northern Ireland Renewable Heat Incentive Scheme – 2020 Tariff Review

https://www.economy-ni.gov.uk/consultations/northern-ireland-renewable-heat-incentive-scheme-2020-tariff-review

Following a review by energy consultants Cornwall Insight of the variables which underpin the tariff structure for medium biomass boilers (20 – 199kW) on the Northern Ireland non-domestic RHI Scheme, the Department proposes to increase tariffs in line with the consultants’ recommendations. The approach by Cornwall Insight forms a significant element of our assessment.

2020: New Decade, New Approach The New Decade, New Approach8 document leads to the restoration of the NI Executive and indicates that “RHI will be closed down and replaced by a scheme that effectively cuts carbon emissions”. Unlike the New Decade, New Approach document (which is an agreement rather than legislative commitment), the draft outcomes framework Programme for Government consultation makes no reference to RHI9.

2021: Northern Ireland Non-Domestic Renewable Heat Incentive Scheme – Future of the Scheme consultation

In January 2020 the New Decade, New Approach (NDNA) document, published by the UK and Irish Governments, provided the basis for restoration of devolution in Northern Ireland. NDNA included a commitment for reform to take account of the findings of the Independent Public Inquiry into the Non-Domestic Renewable Heat Incentive (RHI) Scheme and, in relation to the Executive’s potential Programme for Government strategic priority of addressing climate change, a specific commitment to closure of RHI itself and replacement with a scheme which effectively cuts carbon emissions. This consultation seeks views on options for the future of the Non-Domestic RHI Scheme.

1.3 Project Scope

The following sections present Grant Thornton’s opinion on the four options proposed in the current

consultation document. In forming this opinion, we have focussed on the Environmental Impact, Rate

of Return, Employment/Economic Impact as well as the appropriateness of the cost assumptions that

underpin the tariff calculations for each of the options considered.

The report answers the following questions:

- Chapter 2: How has Renewable Heat usage in NI evolved?

- Chapter 3: What are the rural economy/socio-economic benefits of RHI?

- Chapter 4: What are the Environmental and Social Impacts of Biomass?

- Chapter 5: How has DfE developed the consultation process?

- Chapter 6: Do the assumptions behind DfE’s options hold?

- Chapter 7: What option represents the best balance of fairness and public spending?

8 https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/856998/2020-01-08_a_new_decade__a_new_approach.pdf 9 https://www.northernireland.gov.uk/sites/default/files/consultations/newnigov/pfg-draft-outcomes-framework-consultation.pdf

8

2. How has Renewable Heat usage in NI evolved?

9

2. How has Renewable

Heat usage in NI

evolved?

2.1 Climate Change prompts greater action

Action to combat climate change and to reduce carbon emissions has shifted up the agenda for national

governments and public bodies, with agreement that carbon emissions have increased global

temperatures. Observations suggest that the global average temperature has now increased by more

than 1 degree Celsius since the pre-industrial era, resulting in rising sea levels and reductions in both

the snow and ice caps across both the Arctic and Antarctic.

In response to this pressing issue, 196 National Governments agreed to reduce their overall carbon

emissions, signing up to the Paris Agreement which commits signatories to a legally binding

commitment to limit global warming to 1.5 degrees Celsius compared to pre-industrial levels.10. The UK

Government has set the aim of reducing carbon emissions by 68% compared to 1990 levels while also

setting a target of complete carbon-neutrality by 205011. Similarly, the Northern Ireland Strategic

Framework for Energy committed the direction and future of Northern Ireland to the development and

commitment of renewable energies i.e. “to create relevant conditions for an increase to 40% electricity

consumption from renewable sources by 202012”.

The devolved countries of the UK have developed, or are developing, similar targets on climate change.

Carbon neutrality and zero-carbon aims feature predominantly in the NI Executive’s Programme for

Government (PfG) consultation.13. Unlike the New Decade, New Approach document, the draft

outcomes framework PfG consultation makes no reference to RHI.

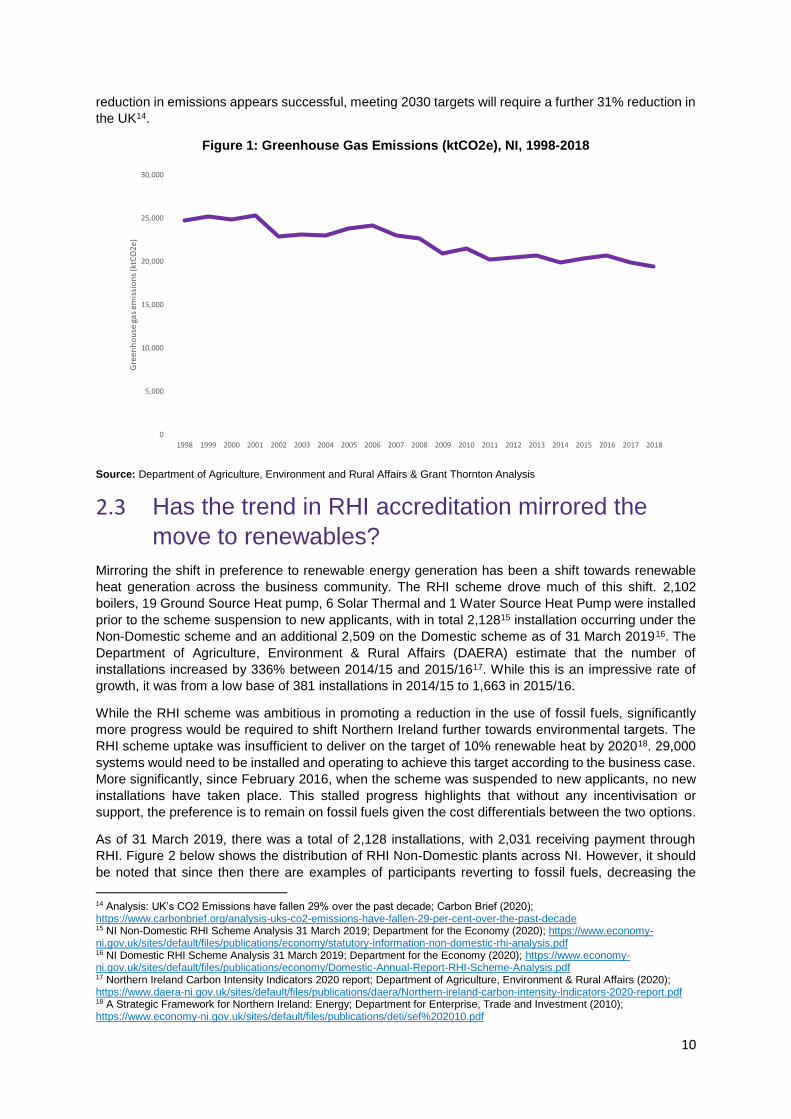

2.2 What has the trend in Carbon Emissions in NI

been?

Across the UK, the overall level of greenhouse gas emissions in 2019 were significantly lower, by

45.2%, than they were in 1990. In a similar vein, NI greenhouse gas emissions have declined by 21.3%

since 1998. This decline is against the backdrop of growth of 111% in the NI economy over the same

period. Figure 1 below shows the trend in greenhouse gas emissions across NI since 1998. While the

10 The Paris Agreement; United Nations Climate Change; https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement 11 UK sets ambitious new climate target ahead of UN Summit; GOV.uk (2020); https://www.gov.uk/government/news/uk-sets-ambitious-new-climate-target-ahead-of-un- 12 Energy: A Strategic Framework for Northern Ireland; Department for Enterprise, Tarde and Investment (2010); https://www.economy-ni.gov.uk/sites/default/files/publications/deti/sef%202010.pdf 13 Programme for Government Draft Outcomes Framework: Consultation Document; Northern Ireland Executive (2021); https://www.northernireland.gov.uk/sites/default/files/consultations/newnigov/pfg-draft-outcomes-framework-consultation.pdf

10

reduction in emissions appears successful, meeting 2030 targets will require a further 31% reduction in

the UK14.

Figure 1: Greenhouse Gas Emissions (ktCO2e), NI, 1998-2018

Source: Department of Agriculture, Environment and Rural Affairs & Grant Thornton Analysis

2.3 Has the trend in RHI accreditation mirrored the

move to renewables?

Mirroring the shift in preference to renewable energy generation has been a shift towards renewable

heat generation across the business community. The RHI scheme drove much of this shift. 2,102

boilers, 19 Ground Source Heat pump, 6 Solar Thermal and 1 Water Source Heat Pump were installed

prior to the scheme suspension to new applicants, with in total 2,12815 installation occurring under the

Non-Domestic scheme and an additional 2,509 on the Domestic scheme as of 31 March 201916. The

Department of Agriculture, Environment & Rural Affairs (DAERA) estimate that the number of

installations increased by 336% between 2014/15 and 2015/1617. While this is an impressive rate of

growth, it was from a low base of 381 installations in 2014/15 to 1,663 in 2015/16.

While the RHI scheme was ambitious in promoting a reduction in the use of fossil fuels, significantly

more progress would be required to shift Northern Ireland further towards environmental targets. The

RHI scheme uptake was insufficient to deliver on the target of 10% renewable heat by 202018. 29,000

systems would need to be installed and operating to achieve this target according to the business case.

More significantly, since February 2016, when the scheme was suspended to new applicants, no new

installations have taken place. This stalled progress highlights that without any incentivisation or

support, the preference is to remain on fossil fuels given the cost differentials between the two options.

As of 31 March 2019, there was a total of 2,128 installations, with 2,031 receiving payment through

RHI. Figure 2 below shows the distribution of RHI Non-Domestic plants across NI. However, it should

be noted that since then there are examples of participants reverting to fossil fuels, decreasing the

14 Analysis: UK’s CO2 Emissions have fallen 29% over the past decade; Carbon Brief (2020); https://www.carbonbrief.org/analysis-uks-co2-emissions-have-fallen-29-per-cent-over-the-past-decade 15 NI Non-Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/statutory-information-non-domestic-rhi-analysis.pdf 16 NI Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/Domestic-Annual-Report-RHI-Scheme-Analysis.pdf 17 Northern Ireland Carbon Intensity Indicators 2020 report; Department of Agriculture, Environment & Rural Affairs (2020); https://www.daera-ni.gov.uk/sites/default/files/publications/daera/Northern-ireland-carbon-intensity-indicators-2020-report.pdf 18 A Strategic Framework for Northern Ireland: Energy; Department for Enterprise, Trade and Investment (2010); https://www.economy-ni.gov.uk/sites/default/files/publications/deti/sef%202010.pdf

0

5,000

10,000

15,000

20,000

25,000

30,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Gre

enh

ou

se g

as e

mis

sio

ns

(ktC

O2e

)

11

above installation figure of 2,128. This was highlighted as part of Buglass’s research, which showed

that many had reversed to fossil fuels due to the viability of biomass boilers following the tariff cuts, or

were thinking of doing so. The majority of installations are in rural areas and the majority of installations

(53%19) occur in the Agriculture sectors. A further 8.4% of installations are in the forestry and wood

processing sector20. The Department’s Rural Needs Impact Assessment21 acknowledges a greater

impact of changes on rural areas but that change proposals are ‘not likely to impact on people in rural

areas differently from people in urban areas, i.e., the effect on participants will be the same regardless

of the area they live in.’ To be clear, the hardship and business risk issues are the same in urban and

rural areas but the uptake in predominantly rural areas weights the impact to those areas.

Figure 2: Distribution of Non-Domestic RHI Accreditations, NI, 2019

Source: Department of Agriculture, Environment and Rural Affairs & Grant Thornton Analysis

Under the Domestic Scheme, around 2,509 accredited RHI technology were installed, with 1,106 of

these being biomass boilers22. Analysis23 conducted by the Department for Environment Agriculture

and Rural Affairs on 2015/16 domestic installations found that oil was the main source of fuel displaced.

The main fuel displaced in the Non-Domestic Scheme was LPG (having been used by poultry farmers

to heat poultry houses24). This observation was noted by the Department in a footnote to the European

Commission as part of a State Aid document, which stated “the Northern Ireland authorities have

explained that liquid petroleum gas was the appropriate counterfactual fuel for most biomass

installations because it was the original fuel being used by the majority of RHI scheme participants25”.

19 1,124 NI Non-Domestic RHI boiler installations occurred in the Agriculture sector [NI Non-Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/statutory-information-non-domestic-rhi-analysis.pdf] 20 NI Non-Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/statutory-information-non-domestic-rhi-analysis.pdf 21 https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/Draft-rural-needs-impact-assessment-future-non-domestic-rhi-scheme.pdf 22 NI Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/Domestic-Annual-Report-RHI-Scheme-Analysis.pdf 23 Northern Ireland Carbon Intensity Indicators 2020 report; Department of Agriculture, Environment & Rural Affairs (2020); https://www.daera-ni.gov.uk/sites/default/files/publications/daera/Northern-ireland-carbon-intensity-indicators-2020-report.pdf 24 State Aid SA. 47501 (2017/NN) – United Kingdom Northern Ireland Renewable Heat Incentive Scheme 2017-18 (Footnote 6); European Commission (2017) 25 State Aid SA. 47501 (2017/NN) – United Kingdom Northern Ireland Renewable Heat Incentive Scheme 2017-18 (Footnote 6); European Commission (2017)

12

This is in conflict to both Ricardo, Cornwall and Department, with Cornwall stating that “there is little

overall transparency of the number of consumers using LPG and coal in Northern Ireland26”.

As part of the accreditation and audit process, participants need to provide fuel records historically on

both current wood pellets and the displaced fossil fuels.

Additionally, correspondence between the Department’s Permanent Secretary and a then MLA

referenced “A figure of 30p per litre for LPG has been provided to DfE by some NIRHI participants as

the discounted LPG price afforded to poultry farmers through a supply arrangement”. This figure of 30p

per litre remains valid at the time of preparing this report.

The Department does/has access to knowledge about the costs and availability/usage of LPG and

should apply this information in its calculations.

The effectiveness of the RHI scheme in driving change to more environmentally favourable fuels is

clear, although since the scheme was suspended to new applicants in 2016 the pace of change ceased.

As noted within the ‘New Decade New Approach27’ document, it is the stated aim of the NI Executive

to close the scheme permanently and replace it with another suitable scheme which ‘effectively’ cuts

carbon emissions. However, the GB RHI scheme also closed permanently on midnight of the 31 March

2021 but will continue for current participants28. Current participants will receive the tariff guaranteed to

them on their accreditation date, with these tariffs being index linked.

It is worth noting that installations peaked at 2,128 at 31 March 2019. No additional installations have

taken place since 2016 and due to tariff revision, etc. this number has in fact slowly decreased as boiler

owners revert to fossil fuel. The closure or termination of the scheme will see all support being removed

and likely prompt a dramatic reversion to fossil fuels due to the unviability of biomass boilers without

support.

The options proposed by the department for the future of the Non-Domestic RHI Scheme are the subject

of the assessment which follows.

26 Review of Tariff for NI Non-Domestic RHI Scheme; Cornwall Insight (2020); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/Cornwall-Insight-NIRHI-tariff-review.pdf 27 New Decade New Approach; UK & Irish Governments (2020); https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/856998/2020-01-08_a_new_decade__a_new_approach.pdf 28 NDRHI Closure; Ofgem (2021); https://www.ofgem.gov.uk/environmental-programmes/non-domestic-rhi/about-non-domestic-rhi/ndrhi-closure

13

3. What are the rural economy/socio-economic benefits of RHI?

14

3. What are the rural

economy/socio-

economic benefits of

RHI?

3.1 The Economic Benefits of RHI to NI’s Rural

Economy

As part of the consultation on the future of the Non-Domestic RHI scheme, the DfE outlined two of the

proposed four options that involve the closure of the scheme with/without compensation. The economic

impact of the scheme closure in rural areas of NI was of particular concern (recalling that 53% of

installations relate to agriculture). These impacts were highlighted as part of the 2019 Consultation

responses, in which the opinion was offered that there had been a negative economic impact through

job losses and cash flow issues due to amendments to the RHI scheme, and that less than 30% of

installers were still operating.29 Many applicants had to sell off assets, lay off staff, postpone investments

or divert funds from other elements of the business having factored in contractually expected returns

into business plans for other business activities. Strikingly, many of the participants stated “they would

not have installed a biomass heating system under the tiered tariffs30”, as the tiered tariffs had made

their businesses ‘uncompetitive’ in comparison to counterparts in the rest of the UK. In addition, the

2017 tariff changes also had wider impacts on installers with many installers stating there “has been a

major loss of jobs in their companies”, while also seeing “many of their former competitors are no longer

operating31”. As such, it can be seen that through first-hand consultation responses that the change in

scheme under the 2017 tariffs have had a negative economic impact on both installers and participants,

with both having seen business fall and job losses occur. Whereas those that entered the scheme post-

November 2015 noted that while the 2017 and 2018 legislation didn’t have immediate impacts, they did

note that if the scheme were to close this would have ‘severe’ financial impacts upon their businesses32.

29 The Future of the Northern Ireland Non-Domestic Renewable Heat Incentive Scheme: Consultation Report; Department for the Economy (2019); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/rhi-non-domestic-consultation-report.pdf 30 The Future of the Northern Ireland Non-Domestic Renewable Heat Incentive Scheme: Consultation Report; Department for the Economy (2019); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/rhi-non-domestic-consultation-report.pdf 31 The Future of the Northern Ireland Non-Domestic Renewable Heat Incentive Scheme: Consultation Report; Department for the Economy (2019); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/rhi-non-domestic-consultation-report.pdf 32 The Future of the Northern Ireland Non-Domestic Renewable Heat Incentive Scheme: Consultation Report; Department for the Economy (2019); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/rhi-non-domestic-consultation-report.pdf

15

The Agriculture sector in NI is significant in the context of the overall regional economy. The sector

supports 3.6% of total workforce jobs in NI33. In comparison, Agriculture in the UK as a whole only

supports 1.2% of total workforce jobs34. Overall, out of all Non-Domestic RHI installations 53% of these

occurred in the Agriculture sector, with many of these installations being a single or double boiler

installation.

The closure of the RHI scheme will not only impact directly on users and installers of RHI boilers, but

also impact indirectly on the wider rural economy. For boiler owners, the Buglass Energy Advisory35

report notes that participants are experiencing negative cash flow impacts due to reduced tariffs whilst

carrying debt obligations which were entered in to based on 2012 tariffs. The Buglass report also noted

that these impacts around cash flow stress and debt repayment will ultimately lead to “impairment of

competitive position” as well as ”reduction in business scale – closure of business lines, staff closures

or premature closures”. In addition, the Buglass report also noted that has been significant opportunity

costs incurred, with businesses having to forego investment opportunities in order to service their debt

on the loan taken out as well as meet the businesses “overall cash flow obligations”. The Buglass report

included a ‘high level’ Rate of Return analysis on respondents, concluding that the 2017 changes

resulted in negative Rates of Return for participants. This point was further illustrated in evidence

submitted to the NI Affairs Select Committee where one respondent stated that his current business

has no “call for employees” having had initially “20 employees at peak”. This downsizing was due to

difficulties meeting the financial commitments (undertaken on the basis of RHI guarantees. The same

respondent noted that, “one of my customers, is replacing his Biomass Boilers with Oil Boilers, if this

trend continues along with all the other pressures that we are facing I cannot see a future in my business

which will result in defaulting in over £1 million of borrowings36”.

Boiler operation creates demand for wood pellets/support services and the rebate payments received

bring a monetary benefit into the local economy. In a scheme closure scenario, or indeed, under the

current scheme operation structure, the hardships being felt by participants, as identified in the Buglass

report, can be reasonably assumed to lead to redundancies and business closures (partial or complete)

– see above for evidence submitted to the NI Affairs Select Committee. These impacts will be more

widely felt through the supply chains with a multiplier effect, leading to potential further

closures/redundancies at wood pellet and installation providers.

Grant Thornton have calculated the economic impact of the installations on the rural economy. As

mentioned in Section 2, 1,124 boilers are installed in business related to the Agriculture sector37. Many

more installations are in rural areas (Figure 2). Analysis of installation quotations and invoices from

boiler installers supports a conclusion that a 99Kwh boiler cost an average of £47,21338 excluding VAT.

The total direct economic contribution of boiler installations therefore equates to £57.32m (for the

purposes of calculation, all boilers are assumed to be 99Kwh39). It should be noted, that the above

figure only focusses on the installation undertaken in the Agriculture sector and so the impact across

the whole rural community will be larger than these figures.

Converting this impact figure from turnover to GVA is achieved through application of a Turnover/GVA

ratio produced via the NI Annual Business Inquiry (ABI). For this analysis, Grant Thornton have used

the Manufacturing Turnover to GVA ratio between 2008 and 2018 (47%), due to the repair and

maintenance of non-domestic central heating systems categorised within this broad SIC code. The

result is GVA of £27.15m, with this being generated over the period 2013 to 2016.

33 Workforce Jobs by Industry (SIC 2007) - Seasonally Adjusted; NOMIS (September 2020); https://www.nomisweb.co.uk/query/construct/submit.asp?forward=yes&menuopt=201&subcomp= 34 Workforce Jobs by Industry (SIC 2007) - Seasonally Adjusted; NOMIS (September 2020); https://www.nomisweb.co.uk/query/construct/submit.asp?forward=yes&menuopt=201&subcomp= 35 Northern Ireland Non-Domestic Renewable Heat Incentive: Research into Hardship; Buglass Energy Advisory (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/buglass-report-rhi-non-domestic-hardship-research. 36 Written evidence submitted to the NI Affairs Select Committee 37 NI Non-Domestic RHI Scheme Analysis 31 March 2019; Department for the Economy (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/statutory-information-non-domestic-rhi-analysis.pdf 38 Installation cost above based upon receipts compiled from installers and invoices from participants 39 There have been 1,761 installations for boilers sized 20 to 99Kwh out of a total 1,991 accredited installations [Non-Domestic Renewable Heat Incentive Scheme: Future of the Scheme Consultation Document; Department for the Economy (2021); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/RHI-scheme-future-consultation-document.pdf]

16

Beyond this direct impact, there will be wider economic benefits through supply chain purchases and

other activity generated via boilers. We estimate these indirect effects using the NI Supply Use Tables

produced by NISRA. Using the ‘Repair and installation of machinery and equipment’ multiplier, the total

economic contribution of an installation of RHI boilers in the rural economy will result in a total GVA

generation of £33.06m. This assessment is an illustrative impact of the installation of boilers only.

Subsequent to the installation, there is an ongoing need for fuel i.e. wood pellets, etc. and maintenance.

Applying the same economic calculator approach to these operational costs will generate GVA of

£7.08m per annum. If the scheme was to terminate with no further payments, this would represent a

significant amount of GVA forgone to both installers, participants and the wider NI economy.

3.2 Promotion of the Circular Economy

Having established the direct economic contributions of the RHI scheme to the economy, it is also

important to highlight the economic contribution of RHI boilers in the move towards a ‘circular economy’.

Recently, the move to adopt and implement a ‘circular economy’ has received widespread traction and

has prompted many countries or economic blocs to adopt this ethos. Indeed, the EU recently adopted

a ‘Circular Economy Plan’ as part of their wider ‘Climate Action Plan’, which sets out the aim to recycle

55% municipal waste by 2025, 60% by 2030 and 65% by 2035 respectively40. Similar action has been

taken by the UK Government41 , which will drive towards an economic system in which all resources

are used for as long as possible, reducing wastage and any unnecessary resource wastage.

Many reports and studies have pointed towards the link between biomass boilers and the burning of

wood pellets to the overall ‘circular economy’, This point is captured well in ‘Biomass for the Circular

Economy’ which notes that Biomass is ‘essential for achieving a circular economy’42. Wood pellets are

manufactured from ‘wood co-products’ such as saw dust and bark, essentially the waste product of

other wood products. Turning this by-product (which would otherwise be disposed of) into usable

renewable energy sources is consistent with promoting the movement towards a ‘circular economy’.

This is in stark contrast to what some would consider to be the ‘linear economy’ and the use of fossil

fuels, where “fossil fuels, are generally used just once” meaning this “raw material from the earth can

no longer enter the cycle”. As such, the “extraction of fossil raw materials can be curbed in various ways

by, for instance, using renewable raw materials (biomass)”, which will promote and create a “closed”

cycle of carbon with these cycles having a short circulation time. For example, wood harvested under

a willow plantation used as fuel will release carbon dioxide, however within years the same quantity of

carbon expelled will be reabsorbed and stored in wood.

Additionally, as outlined by Balcas, the UK and Ireland’s largest wood pellet provider, to enable carbon

capture and promote sustainability, for every 1 tree cut down it is replaced with 4 additional trees. This,

via Photosynthesis, which captures the released carbon dioxide, converts it to sugars used for plant

growth and releases oxygen back into the atmosphere and replaces the carbon burnt by wood pellets,

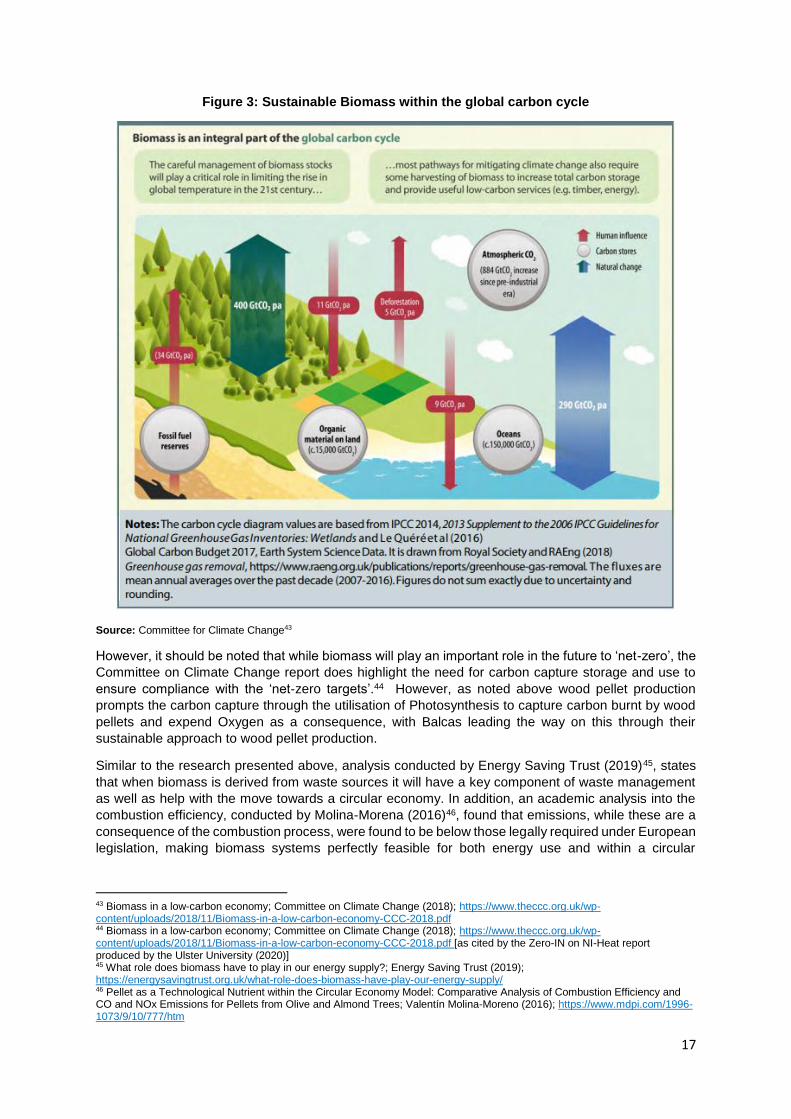

thus promoting a sustainable carbon capture system. Figure 3, which has been taken from a Committee

on Climate Change report on ‘Biomass in a low-carbon economy’, shows the global carbon cycle and

the important role biomass plays in this. Biomass such as woodland, etc. will be vital in the future

regulation of carbon release and thus future global temperature impacts.

40 EU Circular Economy Action Plan, European Commission (2019); https://ec.europa.eu/environment/circular-economy/ 41 Circular Economy Package policy statement; GOV.UK (2020); https://www.gov.uk/government/publications/circular-economy-package-policy-statement/circular-economy-package-policy-statement 42 Biomass for the Circular Economy; van Groenetijn et al; https://biobasedeconomy.nl/wp-content/uploads/2019/11/Biomass-for-the-circular-economy-EN-site.pdf

17

Figure 3: Sustainable Biomass within the global carbon cycle

Source: Committee for Climate Change43

However, it should be noted that while biomass will play an important role in the future to ‘net-zero’, the

Committee on Climate Change report does highlight the need for carbon capture storage and use to

ensure compliance with the ‘net-zero targets’.44 However, as noted above wood pellet production

prompts the carbon capture through the utilisation of Photosynthesis to capture carbon burnt by wood

pellets and expend Oxygen as a consequence, with Balcas leading the way on this through their

sustainable approach to wood pellet production.

Similar to the research presented above, analysis conducted by Energy Saving Trust (2019)45, states

that when biomass is derived from waste sources it will have a key component of waste management

as well as help with the move towards a circular economy. In addition, an academic analysis into the

combustion efficiency, conducted by Molina-Morena (2016)46, found that emissions, while these are a

consequence of the combustion process, were found to be below those legally required under European

legislation, making biomass systems perfectly feasible for both energy use and within a circular

43 Biomass in a low-carbon economy; Committee on Climate Change (2018); https://www.theccc.org.uk/wp-content/uploads/2018/11/Biomass-in-a-low-carbon-economy-CCC-2018.pdf 44 Biomass in a low-carbon economy; Committee on Climate Change (2018); https://www.theccc.org.uk/wp-content/uploads/2018/11/Biomass-in-a-low-carbon-economy-CCC-2018.pdf [as cited by the Zero-IN on NI-Heat report produced by the Ulster University (2020)] 45 What role does biomass have to play in our energy supply?; Energy Saving Trust (2019); https://energysavingtrust.org.uk/what-role-does-biomass-have-play-our-energy-supply/ 46 Pellet as a Technological Nutrient within the Circular Economy Model: Comparative Analysis of Combustion Efficiency and CO and NOx Emissions for Pellets from Olive and Almond Trees; Valentín Molina-Moreno (2016); https://www.mdpi.com/1996-1073/9/10/777/htm

18

economy. All accredited boilers in the RHI scheme meet both EU and the Department for Environment,

Agriculture & Rural Affairs emission standards.

If the scheme terminates with no further payments to boiler owners, reversion to fossil fuels will reverse

progress outlined above.

19

4. What are the Environmental and Social Impacts of Biomass?

20

4. What are the

Environmental and

Social Impacts of

Biomass?

4.1 The Carbon Impact

Given the RHI scheme’s cost issues and subsequent focus of the RHI Inquiry around public monies, it

is important to remember that environmental goals were at the core of the RHI scheme. Having

considered the economic rationale for biomass boilers, arguably it is more pertinent to confirm the

environmental rationale. While the burning of wood pellets will produce both carbon dioxide and

nitrogen dioxide, the amount of carbon dioxide and nitrogen dioxide produced over the lifetime of a

boiler is the same amount reabsorbed by plant life, resulting in net-zero emissions47. A Life Cycle

Analysis (LCA) study was conducted by Jeswani et al (2019)48, which found that solid biomass boilers

could reduce “global warming potential as well as depletion of fossil resources and the ozone layer by

>90%”. However, the authors do note that while the biomass boilers provide significant environmental

benefits in terms of carbon reduction, etc. the price differential is substantial, with the cost of biomass

heat being 23% more expensive than heat from gas boilers. As such, they recommend the continued

incentivisation of biomass heat.

The adoption of biomass energy and heat has seen significant expansion across the whole of the UK.

To highlight this trend, the Office for National Statistics (ONS) conducted analysis49 into the adoption of

biomass between 2010 and 2017, noting that the proportion of energy generated from renewable and

waste sources increased to more than 10% of the total in 2017; more than the energy produced by oil

and coal. Figure 4 shows the trend in total energy consumption across the UK between 2010 and 2017.

47 How Does Green Boiler Technology Affect The Environment?; Green Journal (2016); https://www.greenjournal.co.uk/2016/12/how-does-green-boiler-technology-affect-the-environment/#:~:text=Environmental%20Impact%20of%20Biomass%20Boilers,emissions%20(CO2%20and%20NO2).&text=With%20proper%20use%20of%20biomass,can%20be%20used%20as%20compost. 48 Environmental and Economic Sustainability of Biomass Heat in the UK; Harish Kumar Jeswani, Andrew Whiting & Adisa Azapagic (2019); https://onlinelibrary.wiley.com/doi/full/10.1002/ente.201901044 49 A burning issue: biomass is the biggest source of renewable energy consumed in the UK; Office for National Statistics (2019); https://www.ons.gov.uk/economy/environmentalaccounts/articles/aburningissuebiomassisthebiggestsourceofrenewableenergyconsumedintheuk/2019-08-30#:~:text=In%202017%2C%20greenhouse%20gas%20emissions,20%20million%20tonnes%20in%202017.

21

Figure 4: UK Total Energy Consumption by Fuel Type, UK, 2010-17

Source: Office for National Statistics (ONS) & Grant Thornton Analysis

Of the ‘renewable and waste sources’ energy generation, almost 40% has been provided by biomass

related sources, showing the significant contribution of biomass to the UK and EU’s strategy in reducing

their usage of fossil fuels to generate both heat and energy i.e. electricity. All fossil fuels used in NI are

imported. A North-South Inter-Parliamentary Association report assessed this position and noted the

island of Ireland’s dependence on imported energy noting that oil accounted “for 59% of final energy

consumption in Ireland, all of which is imported”. The report also goes on to state that increasing

renewable sources specifically for Northern Ireland “may reduce its reliance imported fuels therefore

enhancing security of supply50”.

The increased popularity of wood pellets has translated to the significant importing of wood pellets to

the UK (Figure 5). There has been a substantial increase in wood pellet imports between 2010 and

2018 with current wood pellet imports amounting to 7.8m tonnes, up from 0.6m tonnes in 2010. In NI

the market demand for wood pellets was mostly satisfied by both Balcas and Doherty, together

supplying more than 70% of the demand at peak with the remaining being satisfied by imports from the

rest of Europe. As for wood chip, all of this demand was met from indigenous forest and SCR Willow

plantation. It should be noted however, that NI has some of the sparsest level of woodland among all

of Europe, with only 6.5% being covered compared to 37% for the EU51. To address security of supply

and to ensure the continued promotion of renewable heat attraction, etc. the Strategic Framework for

Energy committed to the “increased growing of energy crops” to promote environmental impact and “to

ensure that biomass production can be optimised”52.

This scale of importing of wood pellets has received significant criticism as it is viewed by critics as

being counter to sustainable energy (the DRAX power station in England is a live example of how

importing wood pellets can undermine carbon reduction aims). However, the ONS do illustrate that

biomass can be considered a renewable energy source, as the growth of plants/trees help to remove

50 Energy Security; North South Inter-Parliamentary Association (2013); http://www.niassembly.gov.uk/globalassets/documents/raise/publications/2013/north_south/13213.pdf 51 Inquiry into the Adaptation of Agriculture and Forestry to Climate Change: The EU Policy Response: Supplementary Memorandum: EU Woodland; House of Lords; https://www.parliament.uk/globalassets/documents/documents/upload/wtd10.pdf 52 A Strategic Framework for Northern Ireland: Energy; Department for Enterprise, Trade and Investment (2010); https://www.economy-ni.gov.uk/sites/default/files/publications/deti/sef%202010.pdf

0

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016 2017

% o

f En

erg

y P

rod

uce

d b

y Fu

el

Renewable and waste sources Coal Natural gas Oil Other

22

greenhouse gases from the atmosphere. In addition, the development of carbon capture and storage

will have a role in contributing to the UK’s aim to move towards a ‘net-zero’ emissions.

Figure 5: Wood Pellet Imports, UK, 2010-18

Source: Office for National Statistics (ONS) & Grant Thornton Analysis

The issue around the importing of wood pellets into NI appears to be less of an issue. Balcas, the main

seller of wood pellets in NI, produce local wood pellets, eradicating any need for imports (and associated

travel carbon footprint). As part of their commitment to sustainability, Balcas plant and harvest

sustainable trees which are used to produce wood pellets. It is estimated that for every one tree used

for pellets four trees are planted in its place.

4.2 The Social Impact

The promotion of sustainable and environmentally friendly fuels will not only have an impact

economically and environmentally, but there will also be wider social impacts.

A Sustainable Energy Source

Unlike the counterfactual fuels such as oil and gas, renewable energies such as biomass are more

widely available and accessible locally. Fossil fuels are much more unevenly distributed throughout the

globe, with some countries having a higher concentration compared to others, resulting in high levels

of fossil fuel importing. For example, since 2005, the UK has generally been an energy importer53.

As such, the ability to be able to produce energy at ‘home’ and not need to be reliant on importing

energy from other countries is a significant boost to future sustainability and green objectives.

Additionally, the potential to produce your own energy provides additional economic opportunities

through the development of R&D and innovation as well as potential employment creation.

However, as noted within the 2018 DfE consultation report, many participants showed a preference to

revert to the original 2012 tariffs as it was felt that the proposed 2017 tariffs would make the running of

biomass boiler unviable to operate beyond the tier 1 threshold in comparison to LPG. It was stated that

53 UK energy: how much, what type and where from?; Office for national Statistics (2016); https://www.ons.gov.uk/economy/environmentalaccounts/articles/ukenergyhowmuchwhattypeandwherefrom/2016-08-15

0

1

2

3

4

5

6

7

8

9

2010 2011 2012 2013 2014 2015 2016 2017 2018

Mill

ion

To

nn

es

23

many had ‘already’ reverted to LPG or that the ‘unattractive’ disparity between LPG and biomass has

the potential to lead to RHI participants to revert to fossil fuels54.

The cost of LPG fuel was quoted in correspondence55 between the then Permanent Secretary of the

Department and a then MLA, with the cost of LPG stated as 4.5p/KwH, in comparison to the wood fuel

cost used by Ricardo of 3.26p/KwH (boiler efficiency of 93%). Ricardo’s wood fuel costs were based on

£150 per tonne for wood pellets.

However, biomass boiler efficiency averages 77% (net)56, resulting in an actual wood pellet price of

4.2p/KwH – assuming £150 per tonne of wood pellets (the £150 per tonne figure is used here solely for

ease of comparison to Ricardo). The findings in the Buglass Report reflect how, due to the cuts in tariffs

and debt obligations, biomass boiler owners are now starting to think about reversion to oil or LPG gas

as the cost of maintaining and feeding the biomass boiler has become too much to bear in the absence

of meaningful incentives57.

Such a scenario could lead to the reversal of self-sustainability and the provision of fuels which can be

sourced nearby. In comparison, a reversion to fossil fuels will only heighten import dependency. To

highlight this point, estimates provided by wood pellet producers suggest that they sell 119,889 tonnes

of wood chip/pellets/firewood/logs per year. If the NI RHI scheme is closed, or if tariffs render biomass

unviable, demand for these 30,000 tonnes of firewood, c.90,000 tonnes of wood pellets/chip and

110,000 tonnes of logs will be significantly, perhaps completely, replaced by fossil fuels, if low tariff

rates remain in place.

In a worst-case scenario, carbon emissions will rise significantly. Analysis conducted by the UK

Government58 estimate that under biomass fuel the FuelMixCO2Factor is zero, whereas with the use of

Fuel Oil it stands at 0.27. This highlights the potential climate and emissions effect of replacing biomass

with Oil as some installers have proposed.

To illustrate the carbon impact, Grant Thornton have calculated the total carbon that could be emitted

under fossil fuel consumption if, as some have suggested, they revert to fossil fuels. The Buglass

Energy Advisory report noted that 23% of respondents to the survey had already switched or were close

to switching back to fossil fuels59. This reversion to fossil fuels started when the 2017 tariffs were

introduced. The 2019 tariff review accelerated this and scheme closure would in all likelihood see a

further rapid acceleration. Our assessment sets out a range of scenarios based on different reversion

rates and across a 99Kw and 199Kw boiler range.

The total KwH per annum for each boiler size is 208,280.2KwH (99Kw boiler) and 261,665.1KwH

(199Kw boiler). To provide context on the total requirement in wood pellets to fuel these boilers we have

divided by the Net Calorific Value (NCV) for wood pellets as presented by the ENplus requirements for

wood pellets60 (4,600 KwH/tonne), which gives a requirement of 45.28 tons per annum (99Kw boiler)

and 56.88 tons per annum (199Kw boiler). We note that boiler efficiency rates vary by season and real

world operation (see section 6.7) but we do nott adjust for efficiency rates here.

Table 2 below shows current wood pellet usage across all of the boilers currently in operation in NI,

with total pellet consumption amounting to 90,000 tonnes per annum. If all biomass boilers were

54 The Future of the Northern Ireland Non-Domestic Renewable Heat Incentive Scheme; Department for the Economy (2019); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/rhi-non-domestic-consultation-report.pdf 55 Impact of Changes to Renewable Heat Subsidy; Department for the Economy; Reference: SCOR-0246-2019 56 Measurement of the in-situ performance of solid biomass boilers; KIWA (2018); https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/831083/Full_technical_report.pdf 57 Northern Ireland Non-Domestic Renewable Heat Incentive: Research into Hardship; Buglass Energy Advisory (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/buglass-report-rhi-non-domestic-hardship-research. 58 2019 Government Greenhouse Gas Conversion Factors for Company Reporting; Department for Business, Energy & Industrial Strategy (2019); https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/904215/2019-ghg-conversion-factors-methodology-v01-02.pdf 59 Northern Ireland Non-Domestic Renewable Heat Incentive: Research into Hardship; Buglass Energy Advisory (2020); https://www.economy-ni.gov.uk/sites/default/files/publications/economy/buglass-report-rhi-non-domestic-hardship-research. 60 Net Calorific Value stated as 4.6KwH/kg [Quality Certification Scheme For Wood Pellets, ENplus (2015); https://enplus-pellets.eu/en-in/component/attachments/?task=download&id=103]

24

replaced by kerosene boilers this would result in 35,000 tonnes of kerosene oil being used per annum.

In addition, we have calculated the amount of carbon emissions produced based upon a range of

reversion to fossil fuel rates (e.g. 30% of participants reverting through to 90% reverting to fossil fuels).

To do this we used conversion factors sourced through DEFRA and provided by the Wood Sustainability

Paper to calculate carbon emissions, with carbon factors of 0.04kg/CO2/KwH (wood pellets) and

0.29kg/CO2/KwH (oil)61 being used. We estimate that if all participants (1,948) reverted to kerosene,

this will generate 120,557 tonnes of CO2 in comparison to 16,629 tonnes for wood pellets. Grant

Thornton have used kerosene oil as the basis for reversion to fossil fuels, as this is the counterfactual

fuel used in the Department’s tariff calculations. We do not agree that Kerosene is the appropriate

counterfactual but it is applied here to drive the comparisons. Across each scenario in Table 2, if

participants revert to kerosene oil, they will generate more carbon compared to burning wood pellets.

For example, if 30% of RHI participants reverted to kerosene this would see carbon emissions be

36,167 tonnes compared to only 11,640 tonnes for those that continue to burn wood pellets per annum.

Table 2: Impact of Oil displacing Biomass Wood Pellet Usage & CO2 Emissions, NI

Wood Pellets replaced by Fossil Fuels (Tons per annum)

Boiler Size

100% of Participants

remain on Wood Pellets

70% of Participants

remain on Wood Pellets

40% of Participants

remain on Wood Pellets

10% of Participants

remain on Wood Pellets

99Kw 79,735 55,815 31,894 7,974

199Kw 10,637 7,446 4,255 1,064

Total 90,372 63,261 36,149 9,037

Lost Pellet sales

-27,112 -54,223 -81,335

Carbon Emissions from Wood Pellets (0.04kg/CO2/KwH) Tonnes

100% of Participants

remain on Wood Pellets

70% of Participants

remain on Wood Pellets

40% of Participants

remain on Wood Pellets

10% of Participants

remain on Wood Pellets

99Kw 14,671 10,270 5,869 1,467

199Kw 1,957 1,370 783 196

Total 16,629 11,640 6,651 1,663

Carbon Emissions from Kerosene Oil (0.29kg/CO2/KwH) Tonnes 100% of

Participants revert to Kerosene

30% of Participants revert

to Kerosene

60% of Participants revert

to Kerosene

90% of Participants revert

to Kerosene

99Kw 106,367 31,910 63,820 95,730

199Kw 14,190 4,257 8,514 12,771

Total 120,557 36,167 72,334 108,501 Source: Department for the Economy, Wood Sustainability Paper & Grant Thornton Analysis

61 Delivering the UK’s renewable heat objectives through wood fuel Sustainability Position Paper; CPL Renewables et al (2014); https://www.land-energy.com/wp-content/uploads/2018/10/sustainability.pdf. We understand that carbon emissions associated with delivery of wood pellets is included in those carbon calculations but not included in carbon emission calculations for oil.

25

Improvement of Quality of Life

While biomass will help reduce Greenhouse Gas Emissions, this is dependent on the production of

Carbon Capture technologies or the provision of sustainable forestry (biomass stock)62. However, under

the process of wood chip/pellet generation, sustainable afforestation will occur, as highlighted by

Balcas. Carbon emissions generated under biomass combustion will/could, therefore, be reabsorbed

by the additional trees implanted through the natural carbon capture and storage process –

photosynthesis.

The production and burning of biomass fuels can help reduce the level of Greenhouse Gas emissions,

through absorption by newly planted trees, potentially resulting in no new increase in atmospheric

carbon63. This is a key feature of short cycle carbon process, in which plants/trees play a key role in the

absorption of carbon dioxide from the atmosphere, converting this into oxygen. Typically, the short

carbon cycle occurs over a period of decades to centuries while the long carbon cycle carbon is passed

between the Earth’s surface through rocks and oceans and the atmosphere over a period of millennia.

Fossil fuels contribute to the continuation of long cycle carbon by releasing carbon emissions from

carbon stores that have been held on the Earth’s surface for millions of years. In comparison, wood

pellets are part of the ‘biogenic’ cycle (Figure 3 above). Additionally, biomass is part of the ‘biogenic’

cycle which gets reabsorbed, ‘maintaining’ current levels in comparison to adding to carbon levels, as

occurs under the combustion of fossil fuels64.

Additionally, demand for wood pellets production reduces the potential for trees to rot in forests. As

tress or plants rot, methane is produced, which is a significantly more “potent” emission than carbon

dioxide.65.

Areas of ‘Unintended Consequence’

There is the potential for ‘unintended consequences’ if the scheme is closed. For example, the UK retail

sector recently agreed to commit to “reach net zero carbon emissions by 2040”, with both retail and

their “supply chains” being the focus66. As many as 63 retailers including Aldi, Lidl, M&S, etc. have

already pledged their support. Morrison’s the UK’s fourth largest supermarket chain in March set out

the aim to ensure a net zero target across all supply chains by 203067. This is directly relevant to RHI

participants. If the scheme is removed, the intention of a significant proportion of RHI participants would

be to revert to fossil fuels (as stated in the Buglass Report), but this may cause an issue should they

wish to accept contracts to supply with the UK retailers who are committed to net zero. To highlight this

point Figure 8b below shows the tariff rates for the GB scheme over by each accreditation date.

If the scheme is closed and a compensatory figure is provided to participants, the tax treatment of this

award will have a further impact on cash flow and will have a further detrimental impact upon the future

sustainability of businesses/projects. This needs to be considered in the calculation of any

compensation package, bearing in mind debt servicing and related costs. It should be noted that for

those that had taken a loan out during the latter years of the scheme, the post-tax lump sum may be

insufficient to cover any debt serviced.

What should also be noted is that while the compensation figure is to be paid to all groups/accredited

boilers, the determination of the compensation rate varies by group. For example, the proposal is that

medium boilers (20-199Kw) will be paid a compensation based upon the 2021 tariffs, while all other

62 Biomass in a low-carbon economy; Committee on Climate Change (2018); https://www.theccc.org.uk/wp-content/uploads/2018/11/Biomass-in-a-low-carbon-economy-CCC-2018.pdf 63 Societal Benefits of Biofuels in Europe; ETIP Bioenergy; https://www.etipbioenergy.eu/sustainability/societal-benefits-of-biofuels 64 Fossil vs. Biogenic CO2 emissions; IEA Bioenergy; https://www.ieabioenergy.com/iea-publications/faq/woodybiomass/biogenic-co2/ 65 Methane: The other important greenhouse gas; Environmental Defence Fund; https://www.edf.org/climate/methane-other-important-greenhouse-gas#:~:text=In%20the%20first%20two%20decades,more%20potent%20than%20carbon%20dioxide.&text=While%20methane%20doesn't%20linger,how%20effectively%20it%20absorbs%20heat. 66 UK retail launches target of net zero emissions by 2040; The Grocer (2020); https://www.thegrocer.co.uk/stores/uk-retail-launches-target-of-net-zero-emissions-by-2040/650181.article 67 Morrison’s makes 2030 net zero farm produce pledge; James Sillars: Sky News (2021); https://news.sky.com/story/morrisons-ploughs-2030-net-zero-farm-produce-pledge-12239733

26

installations will be based on the original grandfathered tariffs, uprated by inflation. It is unclear from the

consultation document as to the rationale for the differing compensation rates. It is also worth

considering that if the scheme is terminated for all participants then this could generate an additional

120,557 tonnes of long-carbon cycle emissions per annum, resulting in 1.8m tonnes over next 15 years.

27

5. How has DfE developed the consultation process?

28

5. How has DfE developed

the consultation

process?

5.1 Introduction

This section of the report will focus on the consultation document proposed by the Department. More

specifically this section/chapter of the report will examine how the options proposed for the ‘future’ for

the Non-Domestic RHI scheme have been arrived at. The four options proposed for the future of the

Non-Domestic RHI scheme in the Departmental Consultation document are;

- Option 1: Scheme remains operational for current participants with present tariffs for all

technologies (status quo);

- Option 2: Scheme remains operational for current participants with all tariffs subject to review

and adjustment as necessary;

- Option 3: Scheme closure with no further payments made to participants; or

- Option 4: Scheme closure with compensation paid to legitimate current participants.

5.2 Option 1 – ‘Status Quo’

Under Option 1, the Department propose the continued usage of 2019 tariffs. While this Option is

referred to as the ‘status quo’, the 2019 tariff proposals are subject to judicial review, with hearings to

begin in April 2021. The use of 2019 tariffs as the ‘status quo’ seems inappropriate, given their

challenged status. ‘Status quo’ tariffs might be more accurately defined as the tariffs that are

operational, or more fairly based on the original 2012 ‘grandfathered tariffs’.

Under this option all participants would be subject to ongoing obligations and regulations as set out in

the 2019 tariff act. However, these tariffs will differ to the tariff agreements entered into based on the

2012 tariff. To show the current tariff rate that would have been in place if the 2012 tariffs remained

applicable, we have increased the original 2012 tariff rates by inflation (RPI), as per the 2012 legislation.

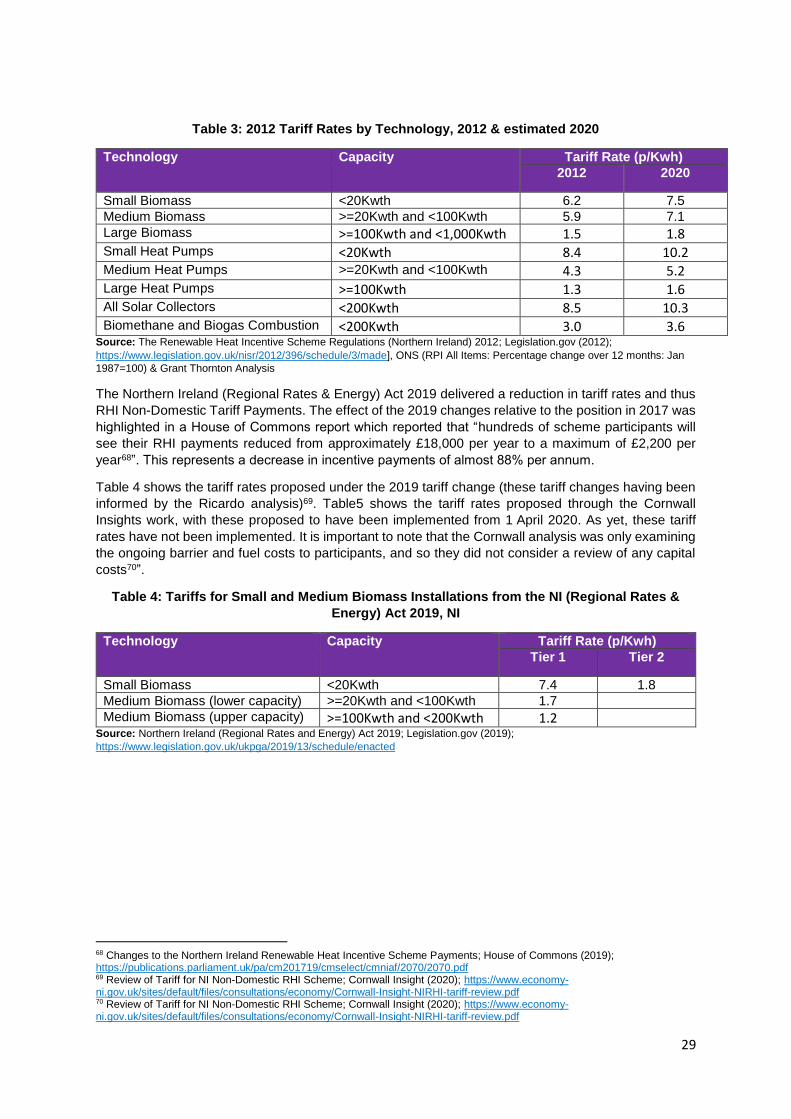

Table 3 below shows the tariff rates in 2012 and 2020 (estimated) for all technologies.

29

Table 3: 2012 Tariff Rates by Technology, 2012 & estimated 2020

Technology Capacity Tariff Rate (p/Kwh)

2012 2020

Small Biomass <20Kwth 6.2 7.5

Medium Biomass >=20Kwth and <100Kwth 5.9 7.1

Large Biomass >=100Kwth and <1,000Kwth 1.5 1.8 Small Heat Pumps <20Kwth 8.4 10.2 Medium Heat Pumps >=20Kwth and <100Kwth 4.3 5.2 Large Heat Pumps >=100Kwth 1.3 1.6 All Solar Collectors <200Kwth 8.5 10.3 Biomethane and Biogas Combustion <200Kwth 3.0 3.6

Source: The Renewable Heat Incentive Scheme Regulations (Northern Ireland) 2012; Legislation.gov (2012);

https://www.legislation.gov.uk/nisr/2012/396/schedule/3/made], ONS (RPI All Items: Percentage change over 12 months: Jan

1987=100) & Grant Thornton Analysis

The Northern Ireland (Regional Rates & Energy) Act 2019 delivered a reduction in tariff rates and thus

RHI Non-Domestic Tariff Payments. The effect of the 2019 changes relative to the position in 2017 was

highlighted in a House of Commons report which reported that “hundreds of scheme participants will

see their RHI payments reduced from approximately £18,000 per year to a maximum of £2,200 per

year68”. This represents a decrease in incentive payments of almost 88% per annum.

Table 4 shows the tariff rates proposed under the 2019 tariff change (these tariff changes having been

informed by the Ricardo analysis)69. Table5 shows the tariff rates proposed through the Cornwall

Insights work, with these proposed to have been implemented from 1 April 2020. As yet, these tariff

rates have not been implemented. It is important to note that the Cornwall analysis was only examining

the ongoing barrier and fuel costs to participants, and so they did not consider a review of any capital

costs70”.

Table 4: Tariffs for Small and Medium Biomass Installations from the NI (Regional Rates &

Energy) Act 2019, NI

Technology Capacity Tariff Rate (p/Kwh)

Tier 1 Tier 2

Small Biomass <20Kwth 7.4 1.8

Medium Biomass (lower capacity) >=20Kwth and <100Kwth 1.7

Medium Biomass (upper capacity) >=100Kwth and <200Kwth 1.2 Source: Northern Ireland (Regional Rates and Energy) Act 2019; Legislation.gov (2019);

https://www.legislation.gov.uk/ukpga/2019/13/schedule/enacted

68 Changes to the Northern Ireland Renewable Heat Incentive Scheme Payments; House of Commons (2019); https://publications.parliament.uk/pa/cm201719/cmselect/cmniaf/2070/2070.pdf 69 Review of Tariff for NI Non-Domestic RHI Scheme; Cornwall Insight (2020); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/Cornwall-Insight-NIRHI-tariff-review.pdf 70 Review of Tariff for NI Non-Domestic RHI Scheme; Cornwall Insight (2020); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/Cornwall-Insight-NIRHI-tariff-review.pdf

30

Table 5: Medium Biomass Boiler Tariffs from 1 April 2020 (Not Currently Implemented)

Source: Department for the Economy [Non- Domestic Renewable Heat Incentive Scheme: 2020 RHI Tariff Review Consultation Report; Department for the Economy (2021); https://www.economy-ni.gov.uk/sites/default/files/consultations/economy/Annex-B-rhi-tariff-review-consultation-report.pdf] Note: The full breakdown of tariff rates by technology can be seen on Appendix 1

The Department stated in submissions for the House of Commons report that the need for the cut in

tariff rates was to ensure compliance with EU State aid regulations. The Scheme had been granted

State aid approval based upon a rate of return of 12%; however the Department stated that, as part of

the Ricardo tariffs,71 some participants have received far in excess of this figure72. As such, this

prompted the review into tariff rates and proposals for the 2019 Act. This review was undertaken by

Cornwall Insights who did not re-examine the capital costs. The reason given for this was highlighted

as part of a letter exchange between the Department and a participant, “Examination of capital costs

did not form part of Cornwall Insight’s tariff review, having previously been considered as part of

Ricardo’s work73”. However, as mentioned, the Ricardo analysis focussed on the installation cost of

boilers (£35k), and not on the significant associated capital costs. The full costs of installation would

have been available via the Department’s auditing process and should have been available for the

Cornwall review.

The House of Common’s NI Affairs Select Committee Inquiry honed in on this 12% rate of return and

several other points of concern, noting ‘The matter of what the European Commission approved in 2012

is a crucial one. The Department has maintained that its hands were tied and that it had to reduce

payments in order to comply with the Commission’s state aid approval. We acknowledge that the

Department has had to balance the reduction in payments with the risk of further detrimental action by

the Commission. The EU Commission stated, in December 2018, that there was insufficient evidence

at that stage to approve a higher rate of return. If there is now scope to challenge the Commission on

its interpretation and offer further evidence then we encourage the Department to do so…A major

concern for scheme participants has been that the Department’s methodology for calculating the new

NI RHI tariffs is incorrect... In calculating the new tariffs, the Department for the Economy has focused

on a narrow range of costs to participants, such as the cost of a boiler and some associated costs. The

Department has also used kerosene as the only counterfactual for fuel costs. The NI RHI scheme was,

from the outset, different to the GB scheme and to the proposed RoI scheme. However, we are deeply