eoq analysis under stochastic production and …vkulkarn/papers/eoqjap.pdf · eoq analysis under...

TRANSCRIPT

Applied Probability Trust (18 August 2005)

EOQ ANALYSIS UNDER STOCHASTIC

PRODUCTION AND DEMAND RATES

VIDYADHAR KULKARNI,∗ UNC-Chapel Hill

KEQI YAN,∗∗ UNC-Chapel Hill

Abstract

In this paper we study a type of production-inventory system in which the

production and demand rates are modulated by a background state process

modeled as a finite state Continuous Time Markov Chain (CTMC). When the

production rate exceeds the demand rate, the inventory level increases, and

when the demand rate exceeds the production rate, it decreases. When the

inventory level reaches zero, an order is placed from an external supplier, and

it arrives instantaneously. We model this system as a bivariate Markovian

stochastic process and derive the limiting distribution of the inventory level.

Assuming linear holding costs and fixed ordering costs, we show that the

classical deterministic Economic Order Quantity (EOQ) policy minimizes the

long-run average cost if one replaces the deterministic demand rate by the

expected demand - production rate in steady state. Finally, we extend the

model to allow backlogging.

Keywords: inventory theory, CTMC, uniform distribution, optimal ordering

policy, EOQ

AMS 2000 Subject Classification: Primary 90B05

Secondary 60J25

1. Introduction

In this paper we study a production-inventory model operating in a stochastic

environment that is modulated by a finite state CTMC. A production rate and a

demand rate are associated with each state of the CTMC. The inventory on hand thus

fluctuates according to the state of the CTMC. Once the inventory level drops to 0 a

∗ Postal address: Department of Statistics and Operations Research, University of North Carolina,

Chapel Hill, NC, 27599, USA

1

2 V. Kulkarni and K. Yan

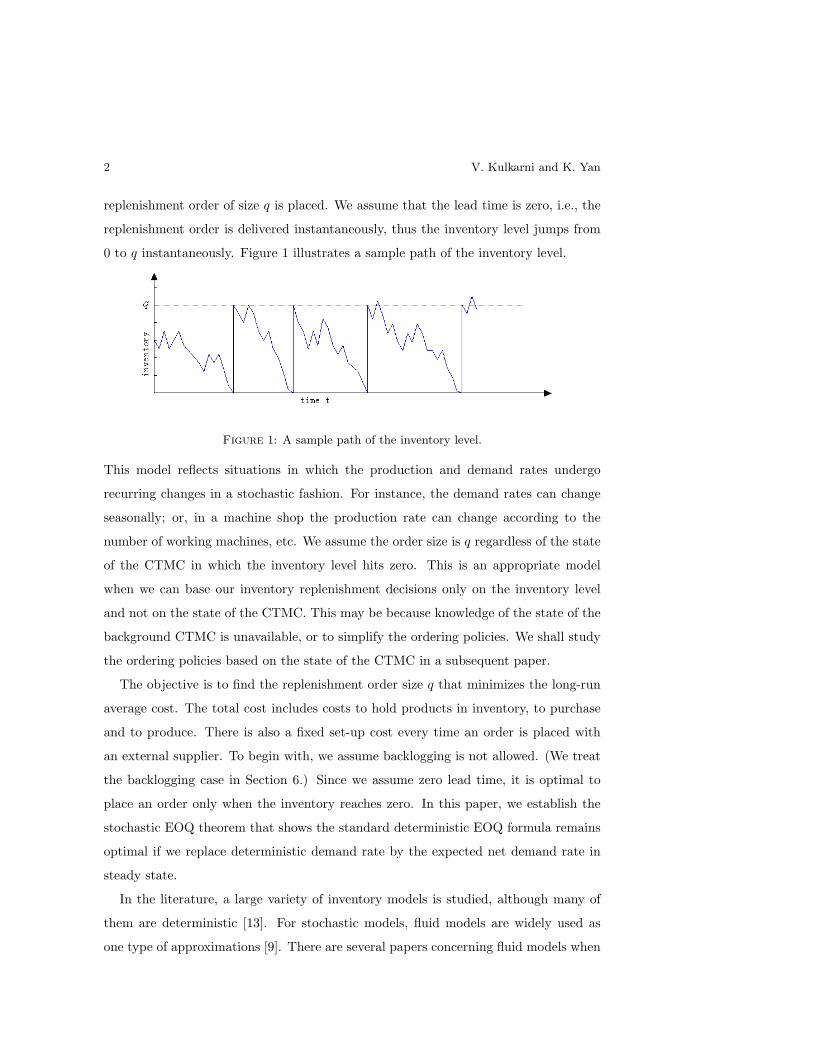

replenishment order of size q is placed. We assume that the lead time is zero, i.e., the

replenishment order is delivered instantaneously, thus the inventory level jumps from

0 to q instantaneously. Figure 1 illustrates a sample path of the inventory level.

Figure 1: A sample path of the inventory level.

This model reflects situations in which the production and demand rates undergo

recurring changes in a stochastic fashion. For instance, the demand rates can change

seasonally; or, in a machine shop the production rate can change according to the

number of working machines, etc. We assume the order size is q regardless of the state

of the CTMC in which the inventory level hits zero. This is an appropriate model

when we can base our inventory replenishment decisions only on the inventory level

and not on the state of the CTMC. This may be because knowledge of the state of the

background CTMC is unavailable, or to simplify the ordering policies. We shall study

the ordering policies based on the state of the CTMC in a subsequent paper.

The objective is to find the replenishment order size q that minimizes the long-run

average cost. The total cost includes costs to hold products in inventory, to purchase

and to produce. There is also a fixed set-up cost every time an order is placed with

an external supplier. To begin with, we assume backlogging is not allowed. (We treat

the backlogging case in Section 6.) Since we assume zero lead time, it is optimal to

place an order only when the inventory reaches zero. In this paper, we establish the

stochastic EOQ theorem that shows the standard deterministic EOQ formula remains

optimal if we replace deterministic demand rate by the expected net demand rate in

steady state.

In the literature, a large variety of inventory models is studied, although many of

them are deterministic [13]. For stochastic models, fluid models are widely used as

one type of approximations [9]. There are several papers concerning fluid models when

EOQ Analysis under Stochastic Production and Demand Rates 3

the production and demand rates depend on the inventory level [1]. As for the cases

when the production and demand rates are determined by the system environmental

state, Berman, Stadje, and Perry recently studied an EOQ model with a two-state

random environment [2]. They consider order sizes that depend on the state of the

environmental state and derived the EOQ policy to optimize the system revenue/cost.

In the general n-state systems, Browne and Zipkin studied a model with continuous

demand driven by a Markov process [3], which can be regarded as a special case of

the model in this paper. Similarly, the clearing processes [11] can be regarded as the

reverse of the inventory level process in a special case when the production rate is

always less than or equal to the demand rate. In that case we show that the inventory

level in steady state is uniformly distributed. However, the stationary distribution of

the content in a clearing system has been proved to be uniform in [4] only under certain

conditions. These conditions are too restrictive and are not satisfied by our model. In

[11] and [12] the authors show that the limiting distribution of the content in a clearing

system is almost never uniform. In this context our result about asymptotically uniform

distribution is even more unexpected.

The rest of this paper is organized as follows. In section 2, we describe the model

mathematically. In Section 3 we derive a system of differential equations for the joint

distribution function of the inventory level and environmental state in steady state and

then solve the equations. We give explicit expressions for two special examples: one

is when the production rate is always less than or equal to the demand rate for every

state. The other is a two-state model and we consider two cases: when the production

rate is less than or equal to the demand rate, or not. In section 4 we compute the

long-run average cost. In section 5, we present the optimal order size q∗ that minimizes

this cost. We show the optimality of a stochastic version of the classical EOQ policy.

Furthermore, in section 6 we extend the results to a more general case that allows

backorders. We show that all the results for the limiting behaviors and expected costs

hold in this new model, and the optimal policy is equivalent to the classical backlogging

EOQ in deterministic models under certain conditions.

4 V. Kulkarni and K. Yan

2. The model

Consider a production-inventory system that is modulated by a stochastic process

{Z(t), t ≥ 0} on state space S = {1, 2, ..., n}. We assume that {Z(t), t ≥ 0} is an

irreducible CTMC on {1, 2, ..., n} with rate matrix Q = [qij ]. When Z(t) is in state i,

the production occurs continuously at rate ri, and there is a demand at rate di. The

net production rate is thus Ri = ri−di. Note that Ri may be negative or positive. Let

X(t) be the inventory level at time t. Then as long as Z(t) = i, {X(t), t ≥ 0} changes

at rate Ri. When X(t) reaches zero we place an order of size q > 0 from an external

supplier who delivers it instantaneously.

Let

π = [π1, π2, · · · , πn] (2.1)

be the limiting distribution of the CTMC, i.e., it is the unique solution to

πQ = 0, π · e = 1,

where e = [1, ..., 1]t is an n-dimensional column vector of ones. The system is stable if

the expected net input raten∑

i=0

πiRi < 0. Let R = diag(R1, ..., Rn). Then the stability

condition can be written in matrix form as follows

πRe < 0. (2.2)

We assume that this stability condition holds for the rest of this paper.

Next we consider costs to operate the system. The total cost consists of three parts:

holding cost, ordering cost, and production cost. We need the following notation to

describe the costs in subsequent sections:

h: cost to hold one item in inventory for one unit of time;

k: fixed set-up cost whenever an order is placed;

p1: cost to purchase one item from the external supplier;

p2: cost to produce one item.

We are interested in computing the optimal order size q∗ that minimizes the long-run

total cost per unit of time. We first need to compute the complementary cumulative

distribution function of the inventory level in steady state. We do this in the next

section.

EOQ Analysis under Stochastic Production and Demand Rates 5

3. Limiting behavior of the inventory level process

In this section we analyze the limiting distribution of the inventory level by a system

of differential equations and solve it with a group of boundary conditions.

3.1. Differential equations

Denote

Gj(t, x) := P{X(t) > x,Z(t) = j}, x ≥ 0, t ≥ 0, j ∈ S.

Assume the stability condition (2.2) thus the following limit exists:

Gj(x) := limt→∞

P{X(t) > x,Z(t) = j}, x ≥ 0, t ≥ 0, j ∈ S.

In this section we show how to compute Gj(x). The following theorem gives the

differential equations satisfied by

G(x) := (G1(x), ..., Gn(x)) .

We use the notation

G′(x) :=(

dG1(x)dx

, ...,dGn(x)

dx

).

Theorem 3.1. The limiting distribution G(x) satisfies

G′(x)R = G(x)Q + β, x ≤ q, (3.1a)

G′(x)R = G(x)Q, x > q, (3.1b)

where the row vector β is given by β := G′(0)R. The boundary conditions are given by

Gj(q+) = Gj(q−), ∀j : Rj 6= 0 (3.2a)

G′j(0) = 0, ∀j : Rj > 0, (3.2b)

G(0)e = 1. (3.2c)

Proof. The differential equations follow from the standard derivation of Chapman

Kolmogorov equations for Markov processes, and hence we omit the details. See [6].

The boundary condition (3.2b) holds because 1/G′j(0) can be seen to be the expected

time between two consecutive visits by the {(X(t), Z(t)), t ≥ 0} process to the state

(0, j). If Rj > 0, this mean time is infinity. Hence G′j(0) = 0 when Rj > 0.

6 V. Kulkarni and K. Yan

The boundary condition Gj(q+) = Gj(q−) for all state j with Rj 6= 0 is obvious

from the fact that there is no probability mass at (q, j) unless Rj = 0. If Rj = 0, it is

easy to show that the probability mass P{X = q, Z = j} satisfies

P{X = q, Z = j}∑k 6=j

qjk =∑

i:Ri<0

G′i(0)Ri.

Thus the boundary condition (3.2a) does not hold for state j if Rj = 0.

3.2. Solution to the differential equations

In this section we derive the solution to the differential equations given in Theorem

3.1. First consider the homogeneous equations G′(x)R = G(x)Q. Let (λ, φ) be an

(eigenvalue, eigenvector) pair that solves

φQ = λφR. (3.3)

Let

m = |{i : Ri 6= 0}|.

Then it is known that there are exactly m pairs (λi, φi), 1 ≤ i ≤ m, that satisfy

Equation (3.3). Assume that they are distinct. Exactly one of the eigenvalues is zero,

and the eigenvector corresponding to this eigenvalue is π, the stationary vector of Q

[7]. Assume that λ1 = 0 and φ1 = π.

We need the following matrix notation

Λ := diag(λ1, λ2, ..., λm), (3.4)

and

Φ :=[φT

1 , φT2 , ..., φT

m

]T. (3.5)

Lemma 3.1. The general solution to the homogeneous equations G′(x)R = G(x)Q

is given by G(x) = ceΛxΦ, where c = (c1, c2, ..., cm) is a constant row vector to be

determined by boundary conditions.

Proof. See [7].

Now take into consideration the non-homogeneous equations G′(x)R = G(x)Q + β.

We have the following theorem.

EOQ Analysis under Stochastic Production and Demand Rates 7

Theorem 3.2. The solution to the differential equations in Theorem 3.1 is given by

G(x) = ceΛxΦ + sxπ + d, if x ≤ q,

G(x) = aeΛxΦ, if x > q,

where the m dimensional row vectors a, c, the n dimensional row vectors d and the

scalar s are the unique solution to the following system of linear equations:

cΛΦR + sπR + dQ = 0, (3.6a)

(aeΛqΦ− ceΛqΦ− sqπ − d)IR 6=0 = 0, (3.6b)

ai = 0, ∀i : λi ≥ 0, (3.6c)m∑

i=0

ciλiφij + sπj = 0, ∀j : Rj > 0, (3.6d)

(cΦ + d)e = 1, (3.6e)

where ai (ci) is the i-th entry of the vector a (c), and IR 6=0 is the modified identity

matrix that has 1 as its j-th diagonal entry if Rj 6= 0, and 0 otherwise.

Proof. According to Lemma 3.1, the homogenous equations (3.1b) have solutions of

form G(x) = ceΛxΦ. It can be shown that the nonhomogeneous equations (3.1a) have

solutions of form

G(x) = ceΛxΦ + sxπ + d (3.7)

if and only if sxπ +d is a particular solution to (3.1a). Thus, using sxπ +d into (3.1a),

we get

sπR = sxπQ + dQ + β

= dQ + β.(3.8)

The last equation holds because πQ = 0.

Sinceβ = G′(0)R

= (cΛΦ + sπ)R,

using β into (3.8) we obtain

sπR = dQ + (cΛΦ + sπ)R,

which can be rearranged to get Equation (3.6a).

8 V. Kulkarni and K. Yan

Suppose when x > q, G(x) has a solution of the form G(x) = aeΛxΦ, where a is

another constant vector.

The boundary condition in Equation (3.2a) reduces to

(aeΛqΦ)IR 6=0 = (ceΛqΦ + sqπ + d)IR 6=0. (3.9)

Rearranging (3.9) we get (3.6b).

Furthermore, boundedness of G(x) as x → ∞ implies Equation (3.6c). Equation

(3.6d) and (3.6e) follow directly from boundary conditions (3.2b) and (3.2c).

The total number of unknown coefficients (a, c, s, d) is 2m + n + 1. Notice that

number of nontrivial equations in (3.6b) is m, and the sum of the number of nontrivial

equations in (3.6c) and (3.6d) is m [7]. Hence we have 2m+n+1 nontrivial equations

to determine a unique solution for the unknown coefficients.

3.3. Examples

Next we study some special cases in which the limiting distributions are interesting.

3.3.1. R ≤ 0 We consider a special case when the production rate never exceeds

the demand rate, and hence the inventory never increases between replenishments.

Without loss of generality assume that X(0) = q. Then it is clear that X(t) ∈ [0, q]

for all t ≥ 0. The next theorem gives the steady-state distribution of X(t).

Theorem 3.3. When R ≤ 0,

G(x) = (1− x

q)π, 0 ≤ x ≤ q. (3.10)

Proof. This is a special case of the model in section 3. The inventory level is always

in [0, q] thus the differential equations reduce to

G′(x)R = G(x)Q + β, (3.11)

where

β = G′(0)R,

with boundary conditions:

G(q) = 0 (3.12a)

G(0)e = 1. (3.12b)

EOQ Analysis under Stochastic Production and Demand Rates 9

It is easy to verify that (3.10) is the solution to the differential equation system (3.11)

with boundary conditions (3.12a) and (3.12b).

Remark 1. Theorem 3.3 implies that in steady state, the inventory level is uniformly

distributed on [0, q], and is independent of Z. This is indeed an unusual and interesting

result. The fact that X is U(0, q) is consistent with the results in [3].

3.3.2. A two-state example Consider a machine shop with only one machine. The

production rate is r when the machine is up, and it fails after an exp(µ) amount of

time. When it is down, there is no production, and it takes exp(λ) amount of time to

fix it. The demand occurs at a constant rate d 6= r no matter whether the machine

is up or down. When the inventory reaches zero, an external supply of amount q is

ordered and arrives instantaneously.

This is a special case with the following parameters:

Q =

−λ λ

µ −µ

, R =

−d 0

0 r − d

.

The matrices Λ (Equation 3.4), Φ (Equation 3.5) and π (Equation 2.1) are given by

Λ =

0 0

0 θ

, Φ =

µ λ

r − d d

,π = (π1, π2)

=(

µλ+µ , λ

λ+µ

),

where

θ =λ(d− r) + dµ

d− r

is the only nonzero eigenvalue.

The stability condition of Equation (2.2) reduces to

λ(r − d)− µd < 0.

Note that θ < 0 if the system is stable. We consider two cases.

Case 1: r > d. In this case, when the machine is up the production rate is greater

than the demand rate. Thus the inventory level hits zero only when the machine is

10 V. Kulkarni and K. Yan

down. We give explicit expressions for the limiting distributions.

Gdown(x) =

1θ π1(eθx − 1

q eθ(x−q)) x > q,

π1(r−d)qθd eθx − π1x + π1

q (1− r−dλ+µ −

rπ2θd ) 0 ≤ x ≤ q,

Gup(x) =

r−dθd π1(eθx − 1

q eθ(x−q)) x > q,

π1qθ eθx − π2x + π1

q (π1π2

+ r−dλ+µ −

rπ1θd ) 0 ≤ x ≤ q.

Case 2: r < d. In this case the inventory level can hit zero when the machine is either

up or down. This is a special case of the model in section 3.3.1. The solution is given

by

Gdown(x) =(

1− 1qx

)µ

λ + µ, 0 ≤ x ≤ q,

Gup(x) =(

1− 1qx

)λ

λ + µ, 0 ≤ x ≤ q.

4. Cost rate calculations

In this section we consider the costs to operate the above system and calculate the

long-run average cost per unit of time.

Let ch(q), co(q) and cp(q) be the steady-state holding, ordering and production cost

rates respectively as functions of the order quantity q. The total cost rate c(q) is hence

given by

c(q) = ch(q) + co(q) + cp(q). (4.1)

The next theorem shows how to compute these cost rates in terms of the limiting

distribution G(x). Let

R̃ := diag(r1, r2, ..., rn),

and

Λ̃ = diag(0,1λ2

, · · · ,1λn

).

Theorem 4.1. The steady-state cost rates are given by

ch(q) = h[(c− a)Λ̃eΛqΦ +

s

2πq2 + (d + c1π)q − cΛ̃Φ

]e,

co(q) = (k + p1q)(cΛΦ + sπ)Re,

cp(q) = p2(cΦ + d)R̃e.

EOQ Analysis under Stochastic Production and Demand Rates 11

Proof. (1) Holding cost rate.

ch(q) =h∑

i

∫ ∞

x=0

Gi(x)dx

=h

[∫ q

x=0

(ceΛxΦ + sπx + d)dx +∫ ∞

x=q

aeΛxΦdx

]e

=h[(c− a)Λ̃eΛqΦ +

s

2πq2 + (d + c1π)q − cΛ̃Φ

]e.

(2) Ordering cost. First consider the number of jumps of the inventory level from 0 to

q during a small time interval (t, t + δ). Notice that when the {Z(t), t ≥ 0} process is

in a state i with negative Ri and X(t) < −Riδ, the number of jumps is 1; otherwise,

it is zero. Thus we have

E( number of jumps in[t, t + δ]) =∑i

P{X(t) ≤ −Riδ, Z(t) = i}

=∑i

(Gi(0)−Gi(−Riδ)).

Hence

limt→∞

limδ→0

1δ E( number of jumps in[t, t + δ]) =

∑i

limδ→0

Gi(0)−Gi(−Riδ)δ

=∑i

RiG′i(0)

= G′(0)Re.

Thus the ordering cost rate is

co(q) = (k + p1q) limt→∞

limδ→0

1δ E( number of jumps in[t, t + δ])

= (k + p1q)G′(0)Re

= (k + p1q)(cΛΦ + sπ)Re.

(3) Production cost rate. In steady state, the probability that the environmental

process is in state i is given by Gi(0). The production cost rate is p2ri when the

environmental process is in state i. Thus the production cost rate is given by

cp(q) =∑i∈S

p2riGi(0)

= p2G(0)R̃e

= p2(cΦ + d)R̃e.

5. Optimal order size

In this section, we demonstrate the primary result of this paper. We use sample

path method to show that the total cost rate c(q) is a convex function of q and that the

12 V. Kulkarni and K. Yan

equivalent of the classical deterministic EOQ formula remains optimal in this stochastic

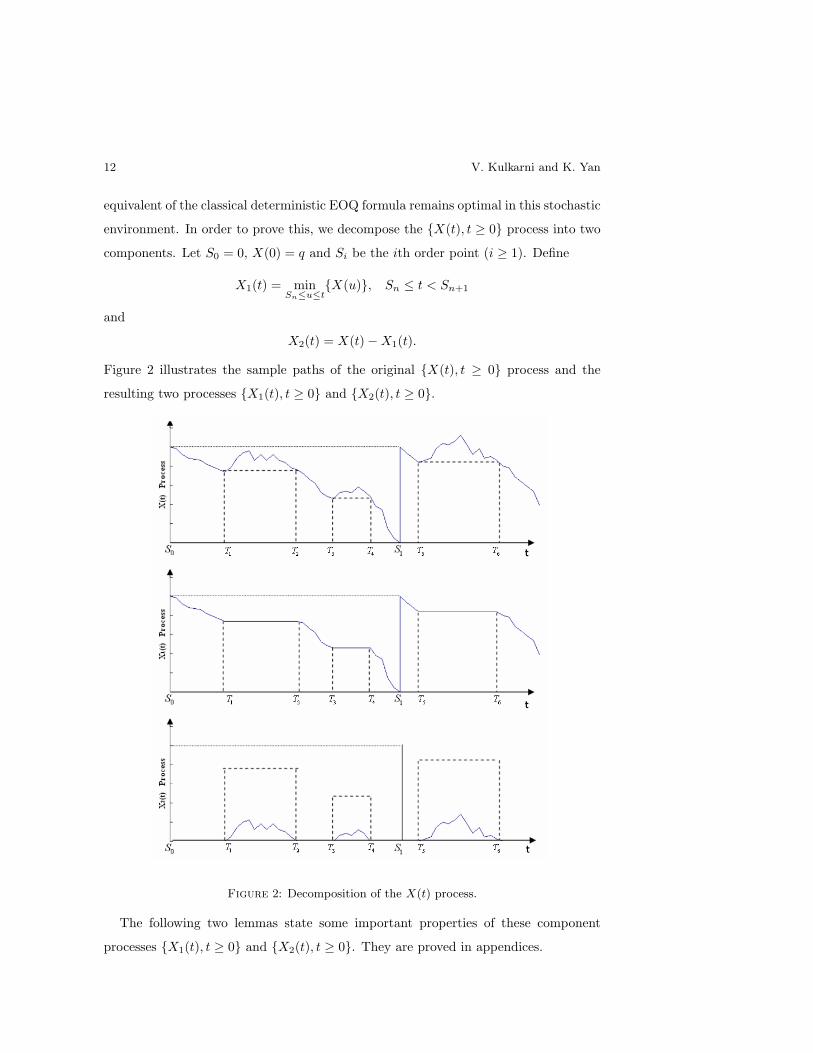

environment. In order to prove this, we decompose the {X(t), t ≥ 0} process into two

components. Let S0 = 0, X(0) = q and Si be the ith order point (i ≥ 1). Define

X1(t) = minSn≤u≤t

{X(u)}, Sn ≤ t < Sn+1

and

X2(t) = X(t)−X1(t).

Figure 2 illustrates the sample paths of the original {X(t), t ≥ 0} process and the

resulting two processes {X1(t), t ≥ 0} and {X2(t), t ≥ 0}.

Figure 2: Decomposition of the X(t) process.

The following two lemmas state some important properties of these component

processes {X1(t), t ≥ 0} and {X2(t), t ≥ 0}. They are proved in appendices.

EOQ Analysis under Stochastic Production and Demand Rates 13

Lemma 5.1. The process {X2(t), t ≥ 0} is independent of q.

Lemma 5.2. The limiting distribution of the process {X1(t), t ≥ 0} is uniform over

[0, q].

Now with these two lammas, we are ready to give the main result of this section.

Theorem 5.1. Let ∆ be the expected net demand rate (i.e., demand rate -production

rate) in steady state, given by

∆ = −∑

i

πiRi. (5.1)

Suppose ∆ > 0. Then the optimal order size q∗ that minimizes the total cost rate c(q)

is given by

q∗ =

√2k∆h

. (5.2)

Proof. From Equation 4.1 the total cost rate is given by

c(q) = ch(q) + co(q) + cp(q)

= hE(X) +k + p1q

E(Si − Si−1)+ cp(q).

First we calculate ch(q).

ch(q) = hE(X)

= h(E(X1) + E(X2)).

According to Lemma 5.2, {X1(t), t ≥ 0} is uniformly distributed on [0, q] in steady

state. Thus E(X1) = q2 . Also, according to Lemma 5.1, we know that {X2(t), t ≥ 0} is

independent of q. Since we have assumed the stability of {X(t), t ≥ 0}, it is clear that

{X2(t), t ≥ 0} has a limiting distribution and it is independent of q. Hence E(X2) is

independent of q.

Next we calculate co(q). From the results on renewal reward processes we get

co(q) =k + p1q

Ei(Si − Si−1).

In steady state, the average net demand during a cycle time (Si, Si−1) has to be equal

to the amount of the external supply. Hence we have

Ei(Si − Si−1)∆ = q.

14 V. Kulkarni and K. Yan

Thus

co(q) =(k + p1q)∆

q

=k∆q

+ p1∆.

Since cp(q) = pi

∑πiri, it is independent of q.

Thus the total cost rate is

c(q) =hq

2+

k∆q

+ C,

where C = hE(X2)+p1∆+cp(q) is independent of q. Clearly, C(q) is a convex function

of q, and it is minimized at q∗ given by 5.2.

Remark 2. The optimal order quantity q∗ of Equation (5.2) is the classical EOQ

formula with the deterministic demand rate replaced by the steady-state expected net

demand rate.

A machine shop example. Consider a machine shop that has n independent and

identical machines, each behaving as described in section 3.3.2. Each machine has its

own repair person. Let Z(t) be the number of working machines at time t. Thus the

CTMC {Z(t), t ≥ 0} has n+1 states, i.e., S = {0, 1, ..., n}. Suppose the demand rate is

directly proportional to the number of machines. Thus we have di = n and ri = i ·r for

all i ∈ S, where r is the production rate of one working machine. Next we investigate

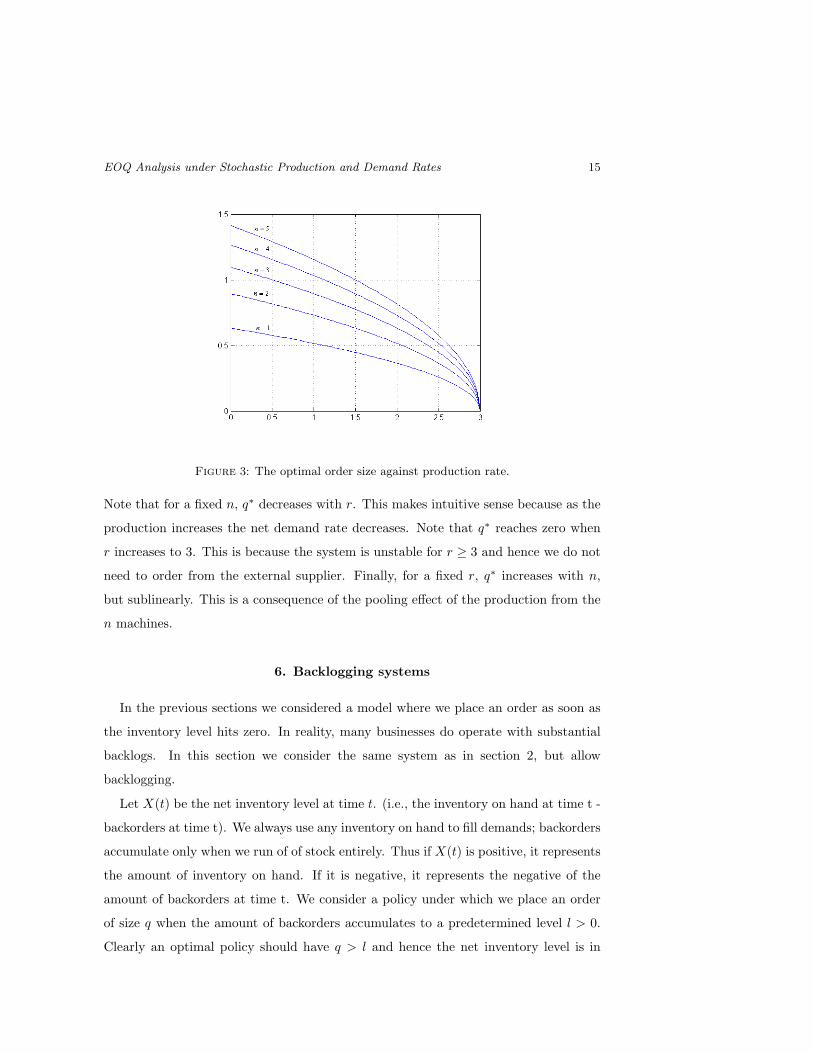

the effect of the production rate increases on the optimal order size q∗. Consider a

system with λ = 1, µ = 2, h = 10, k = 2, p1 = 8 and p2 = 5. We plot the optimal

values of q∗ in Figure 3 for 1 ≤ n ≤ 5 and r varying in (0, 3).

EOQ Analysis under Stochastic Production and Demand Rates 15

Figure 3: The optimal order size against production rate.

Note that for a fixed n, q∗ decreases with r. This makes intuitive sense because as the

production increases the net demand rate decreases. Note that q∗ reaches zero when

r increases to 3. This is because the system is unstable for r ≥ 3 and hence we do not

need to order from the external supplier. Finally, for a fixed r, q∗ increases with n,

but sublinearly. This is a consequence of the pooling effect of the production from the

n machines.

6. Backlogging systems

In the previous sections we considered a model where we place an order as soon as

the inventory level hits zero. In reality, many businesses do operate with substantial

backlogs. In this section we consider the same system as in section 2, but allow

backlogging.

Let X(t) be the net inventory level at time t. (i.e., the inventory on hand at time t -

backorders at time t). We always use any inventory on hand to fill demands; backorders

accumulate only when we run of of stock entirely. Thus if X(t) is positive, it represents

the amount of inventory on hand. If it is negative, it represents the negative of the

amount of backorders at time t. We consider a policy under which we place an order

of size q when the amount of backorders accumulates to a predetermined level l > 0.

Clearly an optimal policy should have q > l and hence the net inventory level is in

16 V. Kulkarni and K. Yan

(−l,∞). Figure 4 illustrates a typical sample path of the {X(t), t ≥ 0} process.

Figure 4: The inventory level process when allowing backlogging.

Note that under this policy, the stability condition is the same as in (2.2).

Let

Hj(x) = limt→∞

P (X(t) > x,Z(t) = j).

The next theorem shows how to compute H(x) = [H1(x),H2(x), . . . ,Hn(x)].

Theorem 6.1. Let G(x)(x ≥ 0) be as in Theorem 3.2. Thus

H(x) = G(x + l), x ≥ −l.

Proof. Follows from the fact that the sample path of the inventory level process

with backorder level l is identical to that without the backorder shifted down by l.

Now suppose it costs b to backlog one unit of demand for one unit of time. Let

cb(q, l), ch(q, l), co(q, l) and cp(q, l) be the steady state backlogging, holding, ordering

and producing cost rates respectively as functions of the order quantity q and reorder

level l. The total cost rate c(q, l) is thus given by

c(q, l) = cb(q, l) + ch(q, l) + co(q, l) + cp(q, l).

The next theorem shows how to compute the cost rates.

Theorem 6.2. The steady-state cost rates are given by

cb(q, l) = b[cΛ̃(I − eΛ(−l))Φ− s

2πl2 + (d + c1π)l

]e,

ch(q, l) = h[(cΛ̃− aΛ̃)eΛ(q−l)Φ− s

2π(q − l)2 + (d + c1π)(q − l)− cΛ̃Φ

]e,

co(q, l) = (k + p1q)(cΛΦ + sπ)Re,

cp(q, l) = p2(cΦ + d)Re,

EOQ Analysis under Stochastic Production and Demand Rates 17

where a, c, s and d are the coefficients in the expression of H(x) corresponding to

Theorem 3.2.

Proof. Follow the same steps in the proof of Theorem 4.1.

The next theorem gives the stochastic version of the EOQ formula with backloggings.

Theorem 6.3. Let ∆ be as in Equation (5.1), ∆ > 0. Then the optimal order size q∗

and reorder position l∗ are given by

q∗ =

√2k(b + h)∆

hb(6.1)

l∗ =(

h

b + h

)q∗. (6.2)

Proof. Follow the same analysis as in Theorem 5.1.

In particular, when R ≤ 0, {X(t), t ≥ 0} has uniform distribution on (−l, q − l) in

steady state, and is independent of Z, thus

H(x) =(

q − l − x

q

)π, −l ≤ x ≤ q − l,

and the long-run average cost is

c(q, l) =[(

(b + h)l2

2q+

hq

2− hl

)π − k

qπR− p1πR + p2πR̃

]e.

This is consistent with the results in deterministic models [13].

7. Conclusion and future work

We have studied a type of inventory models with or without backlogging having

production and demand rates modulated by a background stochastic process. External

replenishment orders are placed at appropriate times and arrive instantaneously. In

this paper we have modeled this system as a bivariate Markovian stochastic process

and derived the limiting distribution of the inventory level. We have established a

stochastic EOQ theorem that shows the optimality of the classical EOQ policy in this

stochastic environment.

We can study three extensions of this system. In the current analysis, the order size

is not allowed to depend on the state of the CTMC when the inventory level hits zero.

18 V. Kulkarni and K. Yan

Clearly, if that information is available, it would lower the costs if the order size can

be made dependent on that information. Berman, Stadje, and Perry have studied such

a two state system [2]. However, more work on deriving the optimal scenario in more

general systems is needed.

Secondly, in this paper we have assumed zero lead times. This assumption is

reasonable when lead times are short enough to be neglected. It would be interesting

to study this system with nonzero lead times. We feel that iid exponential lead times

may lead to tractable analysis.

Clearly, the results of this paper remain valid if the background process is a semi-

Markov process with Phase-type distributions [10]. This can be shown by constructing

an appropriate larger CTMC. Since Phase-type distributions are dense in the set of all

continuous distributions on [0,∞), it follows that the results hold for a semi-Markov

background process with continuous sojourn times. We believe that the results hold for

more general semi-Markov processes as long as the sample paths of the {X(t), t ≥ 0}

process are not periodic with probability one. Rigorous proof of this remains to be

shown.

Appendix A. Proof of lemma 5.1

Proof. Let S+ and S− be two subsets of S defined as S+ = {i ∈ S : Ri ≥ 0}, and

S− = {i ∈ S : Ri < 0}. Assume that Z(0) ∈ S− and define

T1 = min{t ≥ 0 : Z(t) ∈ S+}.

Regardless of the value of q, X(t) always decreases over (0, T1), except for possible

jumps of size q when it hits zero. Thus X2(t) is zero over (0, T1). T1 is independent of

q and hence {X2(t), t ∈ [0, T1)} is independent of q.

Now define

T2 = min{t > T1 : X(t) = X(T1)}.

Note that T2 is also independent of q, X2(T1) = X2(T2) = 0 and X2(t) > 0 for

t ∈ (T1, T2). The sample path of {X(t), t ∈ (T1, T2)} is independent of q, since X(t)

never reaches 0 for any t ∈ (T1, T2). Thus the sample path of {X2(t), t ∈ (T1, T2)} is

independent of q.

EOQ Analysis under Stochastic Production and Demand Rates 19

Define

T2n+1 = min{t ≥ T2n : Z(t) ∈ S+},

and

T2n+2 = min{t ≥ T2n+1 : X(t) = X(T2n+1)}.

Since {X2(t), t ≥ 0} goes through these two cycles alternately over (T2n, T2n+1) and

(T2n+1, T2n+2) independently, it is clear that {X2(t), t ≥ 0} is independent of q.

Appendix B. Proof of lemma 5.2

Proof. First note that the sample paths of {X1(t), t ≥ 0} have right derivative

everywhere. Define I(t) = 0 if the right derivative of X1(t) is strictly negative at t,

and I(t) = 1 if the right derivative of X1(t) is zero at t. Now

limt→∞

P (X1(t) ≤ x)

= limt→∞

P (X1(t) ≤ x)|I(t) = 0)P (I(t) = 0) + limt→∞

P (X1(t) ≤ x)|I(t) = 1)P (I(t) = 1).

(B.1)

Next we will show that

limt→∞

P (X1(t) ≤ x|I(t) = ζ) = x/q, ζ ∈ {0, 1}. (B.2)

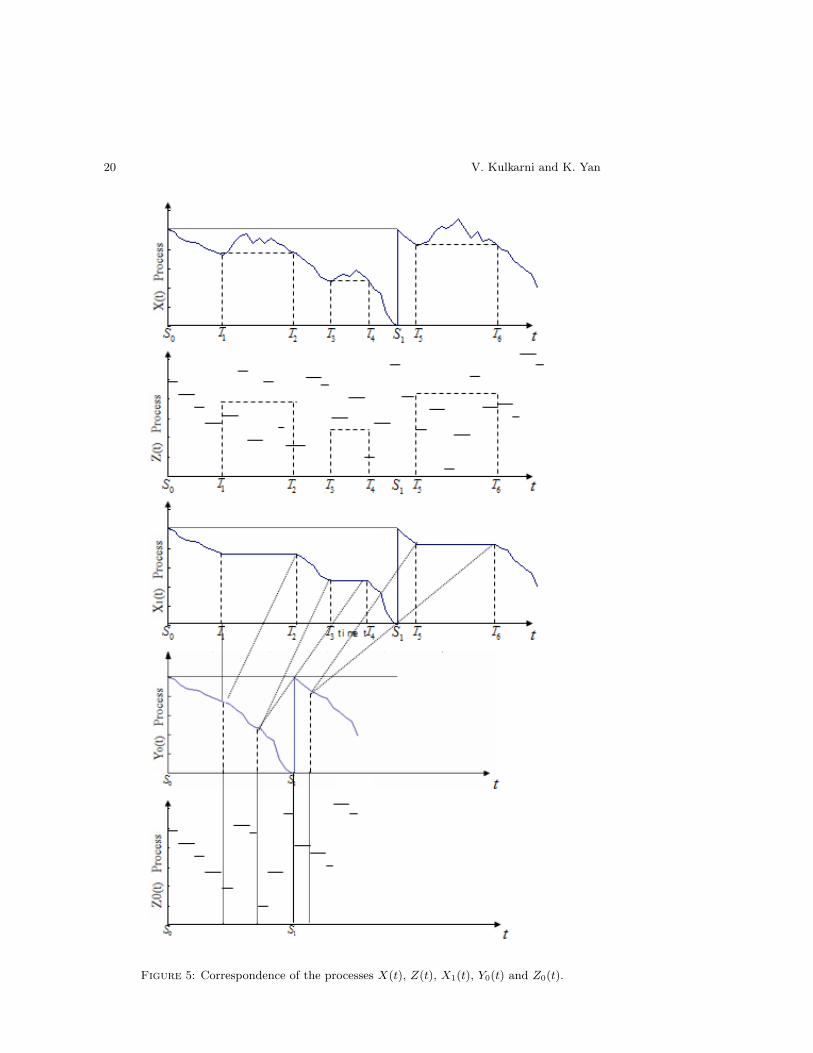

First we construct two new processes {Y0(t), t ≥ 0} and {Z0(t), t ≥ 0} by eliminating

the segments of the sample paths of {X1(t), t ≥ 0} and {Z(t), t ≥ 0} over the time

intervals (T2n+1, T2n+2] for all n ≥ 0. The sample paths of the {Y0(t), t ≥ 0} and

{Z0(t), t ≥ 0} processes corresponding to the sample paths of {X1(t), t ≥ 0} and

{Z(t), t ≥ 0} are shown in Figure 5. From Figure 5 we can see that {Y0, t ≥ 0} can be

thought of as a fluid model modulated by the stochastic process {Z0(t), t ≥ 0} with

state space S−. It can be seen that {Z0(t), t ≥ 0} is a CTMC with generator matrix

Q̂ = [q̂ij ], (i, j ∈ S−) given by

q̂ij = qij +∑

k∈S+

qikηkj , i, j ∈ S−,

where

ηkj = P (Z(T2n+2) = j|Z(T2n+1) = k), k ∈ S+, j ∈ S−.

20 V. Kulkarni and K. Yan

Figure 5: Correspondence of the processes X(t), Z(t), X1(t), Y0(t) and Z0(t).

EOQ Analysis under Stochastic Production and Demand Rates 21

Thus the {(Y0(t), Z0(t)), t ≥ 0} process satisfies the hypothesis of Theorem 3.3. Hence

it follows that

limt→∞

P (Y0(t) ≤ x,Z0(t) = i) =x

qπ̂i, (B.3)

where π̂i is the limiting distribution of the CTMC with generator matrix Q̂. However,

our construction of the Y0 process implies that

limt→∞

P (Y0(t) ≤ x,Z0(t) = i) = limt →∞

P (X1(t) ≤ x|I(t) = 0).

This proves Equation (B.2) for ζ = 0.

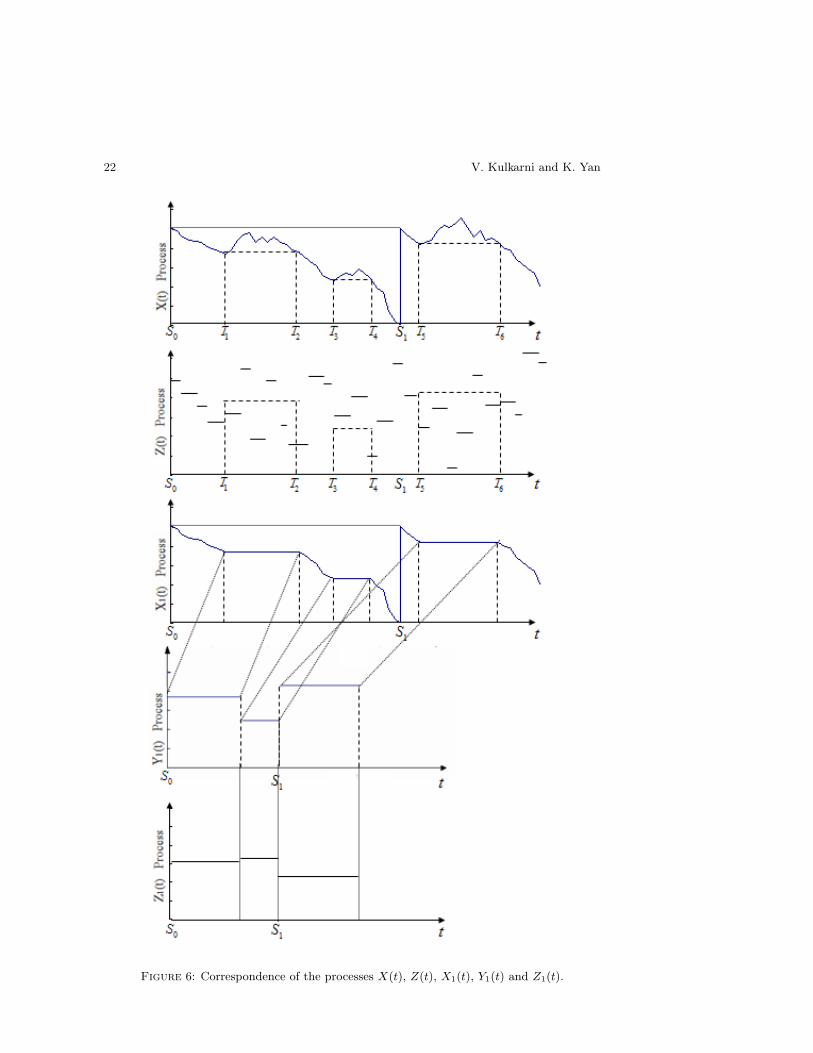

Now for ζ = 1, we define Y1,n = X1(T+2n+1) and Z1,n = Z(T+

2n+1), for n ≥ 0.

Now construct a semi-Markov process (SMP) {(Z1(t), Y1(t)), t ≥ 0} with embedded

DTMC {(Z1,n, Y1,n), n ≥ 0}, so that the n-th sojourn time of this SMP is given by

T2n+2−T2n+1. Clearly the sample path of {Y1(t), t ≥ 0} is identical to the one obtained

by eliminating the segments of the sample path of {X1(t), t ≥ 0} over the intervals

(T2n, T2n+1] for all n ≥ 0. Figure 6 illustrates the sample paths of the {Y1(t), t ≥ 0}

and {Z1(t), t ≥ 0} processes corresponding to the sample paths of {X1(t), t ≥ 0} and

{Z(t), t ≥ 0} processes.

Define

f(j, x)dx = limt→∞

P{Z(t) = j, x ≤ Y1(t) ≤ x + dx}.

According to the theory of SMP [6],

f(j, x)dx =π(j, x)u(j, x)dx∑

k∈S+

∫ q

y=0π(k, y)u(k, y)dy

, (B.4)

where

π(j, x)dx = limn→∞

P{Z1,n = j, x ≤ Y1,n ≤ x + dx},

and u(j, x) is the expected sojourn time of the SMP in state (j, x). Clearly u(j, x) is

independent of x, hence we denote u(j, x) as τj for all x.

Let

g(i, x)dx = limt→∞

P{Z(t) = i, x ≤ Y0(t) ≤ x + dx}, (i ∈ S−).

From Equation (B.3), we see that

g(i, x) =π̂i

q, (i ∈ S−). (B.5)

22 V. Kulkarni and K. Yan

Figure 6: Correspondence of the processes X(t), Z(t), X1(t), Y1(t) and Z1(t).

EOQ Analysis under Stochastic Production and Demand Rates 23

Hence using Equation (B.5),

π(j, x) =∑i∈S−

g(i, x)qij =1q

∑i∈S−

π̂iqij . (B.6)

Substituting Equation (B.6) into (B.4), we have

f(j, x) =

1q

∑i∈S−

π̂iqijτj

∑k∈S+

q∫y=0

1q

∑i∈S−

π̂iqikτkdy

=1q·

∑i∈S−

π̂iqijτj∑k∈S+

∑i∈S−

π̂iqikτk.

Thus the limiting probability density function of {Y1(t), t ≥ 0} process is given by

f(x) =∑

j∈S+

f(j, x) (B.7)

=1q·

∑j∈S+

∑i∈S−

π̂q̂ijτj∑k∈S+

∑i∈S−

π̂q̂ikτk(B.8)

=1q. (B.9)

Equation (B.9) indicates the limiting distribution of {Y1(t), t ≥ 0} is uniform over

[0, q]. This proves Equation (B.2) for j = 1. Hence from (B.1)

limt→∞

P (X1(t) ≤ x) =x

q.

This proves Lemma 5.2.

References

[1] Berman, O. and Perry, D. (2004). An EOQ model with state dependent demand rate. Eur.

J. Operat. Res. In Press.

[2] Berman, O., Stadje, W. and Perry, D. (2005). A Fluid EOQ Model with a Two-State Random

Environment.

[3] Browne, S. and Zipkin, P. (1991). Inventory Models with Continuous Stochastic Demands.

Ann. Appl. Prob. 1, 419–435.

[4] El-Taha, M. (2002). A Sample-Path Condition for the Asymptotic Uniform Distribution of

Clearing Processes. Optimization. 51, 965–975.

24 V. Kulkarni and K. Yan

[5] Kella, O. and Whitt, W. (1992). A storage model with a two state random environment.

Operat. Res. 40, 257–262.

[6] Kulkarni, V. G. (1995). Modeling and Analysis of Stochastic Systems. Chapman and Hall,

London.

[7] Kulkarni, V. G. (1997). Fluid models for single buffer systems, in: J. H. Dshalalow

(Ed.), Frontiers in Queueing, Models and Applications in Science and Engineering, Ed. J.H.

Dshalalow, CRC Press, Boca Raton, FL, 321–338.

[8] Kulkarni, V. G. and Tzenova, E. (2002). Mean first passage times in fluid queues. Operat.

Res. Lett. 30, 308–318.

[9] Mitra, D. (1988). Stochastic theory of a fluid model of producers and consumers coupled by a

buffer. Adv. Appl. Prob. 20, 646–676.

[10] Neuts, M. F. (1981). Matrix Geometric Solutions in Stochastic Models. Johns Hopkins

University Press, Baltimore, MD.

[11] Serfozo, R. and Stidham, S. (1978). Semi-stationary clearing processes. Stoch. Proc. Appl. 6,

165–178.

[12] Whitt, W. (1981). The stationary distribution of a stochastic clearing process. Operat. Res. 29,

294–308.

[13] Zipkin, P. (2000). Foundations of Inventory Management. McGraw-Hill, Boston.