equaterra advisor and bpo/ito service provider pulse ... · equaterra advisor and bpo/ito service...

TRANSCRIPT

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 1Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

IntroductionEquaTerra is pleased to release the fi ndings of the 1Q08 BPO/ITO EquaTerra advisor and service provider Pulse surveys. Through these surveys, EquaTerra has developed a highly informative gauge that provides quarterly insights into trends and projections on the BPO/ITO market gleaned from its own fi eld advisors, as well as leading global BPO/ITO service providers. EquaTerra’s advisors are the leading experts on business process and information technology outsourcing and are intimately involved on a daily basis with buyer organizations actively exploring or undertaking major outsourcing efforts.

Since their inception in 2004, the EquaTerra BPO/ITO Pulse surveys have yielded insightful market analysis including longitudinal comparisons derived from recurring topical themes. The Pulse surveys capture changes in demand, scope, capacity and related key market indicators. They highlight changes, and the direction of change, in the outsourcing industry as a whole. The surveys focus on where the market is going and how that future direction is changing – or not – compared to prior quarters and years.

EquaTerra also incorporates into this research deliverable additional key quantitative market data and leading indicators from sources outside the Pulse surveys. These sources include, but are not limited to, EquaTerra’s own pipeline, interviews with leading BPO and ITO service providers, and fi ndings from other EquaTerra market research.

This edition of the advisor and service provider Pulse surveys refl ect BPO and ITO market activity during 1Q08 (January through March 2008) and projections for the balance of 2008. Topics evaluated include the following:

• Demand and buying patterns, including the impact of the economic downturn on outsourcing demand

• Deal scope, pricing, contract value and profi tability

• Sales cycles and ramp-up time

• Service provider pursuit and delivery capacity

Additional market research incorporated in this edition of the Pulse survey report includes:

• Outsourcing’s role in making human resources more strategic

• The characteristics and critical success factors of next generation outsourcing

• Trends in mid-market ITO

These surveys focus on BPO, defi ned as the outsourcing of multiple, back-offi ce or general and administrative business processes, vertical industry services, and customer care work, to a third-party service provider and/or ITO services in either a standalone arrangement or integrated with BPO. The primary functional areas covered under the surveys are as follows:

• Customer care/call center

• Finance & accounting

• Human resources

• Information technology

• Knowledge process outsourcing

• Procurement

• Vertical industry business services

The following leading global BPO/ITO service providers were polled for this quarter’s sell-side survey:

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08Featuring Results from the HR Talent and Transformation Study

• Accenture

• ADP

• Capgemini

• Ceridian

• Convergys

• CSC

• ExcellerateHRO

• Fidelity

• Hewlett Packard

• ICG Commerce

• Infosys

• Outsource Partners International

• Perot Systems

• TCS

• T-Systems

• Wipro

• WNS

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 2

Distribution of the EquaTerra Pulse survey reports is controlled by EquaTerra, and is intended for internal use and select delivery to EquaTerra clients, prospects and other marketplace representatives. Questions or comments regarding these surveys should be directed to Stan Lepeak, Managing Director of Research, at [email protected] or +1 203 458 0677.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 3

Table of Contents

I Introduction 1

II Highlights 4

III Market Demand and Market Trends Update 6

IV Economy’s Impact on Outsourcing Demand 8

V Outsourcing Drivers 9

VI Demand Trends by Functional Area 11

VII Advisors: Functional and Process Area Demand 14

VIII Service Providers: Functional and Process Area Demand 14

IX Additional HRO and RPO Research: Talent and Transformation Study 15

X “Next Generation” Outsourcing 18

XI Demand Trends by Industry 20

XII Outsourcing Problem Spots 22

XIII Sales Cycle 24

XIV Pricing Competitiveness 26

XV Deal Scope 27

XVI Service Providers: Contract Profi tability and Ability to Increase Scope 28

XVII Service Provider Capacity 29

XVIII Update on Outsourcing Governance 32

XIX Service Provider Market Update 34

XX Service Providers: Current Deal Portfolio Status 36

XXI Conclusion 39

Appendix — Key Questions by Advisors’ Primary Geography and Outsourcing Focus Area

40

About EquaTerra 41

* Please note this PDF also includes embed-ded bookmarks to help better navigate through the document. For list of bookmarks, please click on “Bookmarks” tab to the left of this PDF.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 4

Highlights – EquaTerra Advisors

Overall BPO/ITO Market DemandSlipped; 52 percent of advisors cite increased demand, down 18 percent quarter over quarter (Q/Q), but up 9 percent year over year (Y/Y); just 5 percent cite demand drop

Service Provider Capacity-Pursuit Improved; constrained/tightening dropped to 23 percent

Service Provider Capacity-Delivery Improved; constrained/tightening fell to 35 percent

Economy’s Impact on Outsourcing55 percent cite economic climate is driving more outsourcing, 30 percent indicate it’s having little/no impact on demand

Outsourcing Drivers55 percent cite process improvement, innovation and transformation growing as a driver

Leading Market Segments1. ITO2. FAO3. HRO

Leading HRO Segments1. Payroll2. Benefi ts3. HRIT

Leading FAO Segments1. AR/C&C2. AP3. General Accounting

Leading ITO Segments1. Infrastructure/Ops2. ADM3. Desktop Services

Leading Procurement Segments1. Order Management2. AP 3. Category Management

Leading Industries1. Pharma/Biotech2. CPG3. Financial Services, Public Sector

Market demand cooled from the fourth quarter of 2007, though it is still growing, supporting expectations for a 2008 stronger than 2006 or 2007. The economic climate in western countries, and especially the U.S., is disrupting sourcing uptake in the short term, but will drive more demand longer term and into 2009. ITO remains the strongest functional area of demand, followed by FAO. Service provider capacity shows signs of improvement, driven by more selectivity in deal pursuit.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 5

Highlights – BPO/ITO Service Providers

New Deal Pipeline GrowthSlipped back; 43 percent of service providers cite increases, down 16 percent over quarter (Q/Q) but up 8 percent year over year (Y/Y)

Demand Next QuarterDown slightly; 50 percent expect increases, down 7 percent Q/Q and 11 percent Y/Y

Sales Cycle Steady; no signs of shortening cycles

Pricing Competitiveness More aggressive; cited by 45 percent, up 22 percent Q/Q, 9 percent Y/Y

Deal ScopeOngoing reduction in scope; 24 percent cite decreases, up 19 percent Q/Q, 11 percent Y/Y; just 19 percent cite increases

Contract Profi tability Stable; 65 percent cite no change, 30 percent improving

Ability to Increase Current Contract ScopeSlipping; 52 percent expect increases, down 14 percent Q/Q and below survey average, some expectations of declines

Service Provider Capacity Solid; 64 percent cite adequate levels

Economy’s Impact on Outsourcing 38 percent cite economic climate is driving more outsourcing, 33 percent indicate it’s having little or no impact on demand

Outsourcing Drivers55 percent cite process improvement, innovation and transformation growing as a driver

Leading Market Segments1. ITO2. HRO3. FAO

Leading HRO Segments1. Payroll 2. HRIT3. Benefi ts

Leading FAO Segments1. AR/C&C2. AP3. General Accounting

Leading ITO Segments1. ADM2. Infrastructure/Ops3. Desktop Services

Leading Procurement Segments1. Order Management 2. AP3. Strategic Sourcing

Leading Industries1. CPG 2. Manufacturing 3. Financial Services

Service providers’ pipelines and expectations for future demand growth slipped 1Q08 over 4Q07, though there is still optimism for better 2008 growth overall. Deal scope declined and pricing became more aggressive, emblematic of an increasingly competitive market and more discerning buyers. Challenging economic times are impacting deal fl ow but not longer term demand.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 6

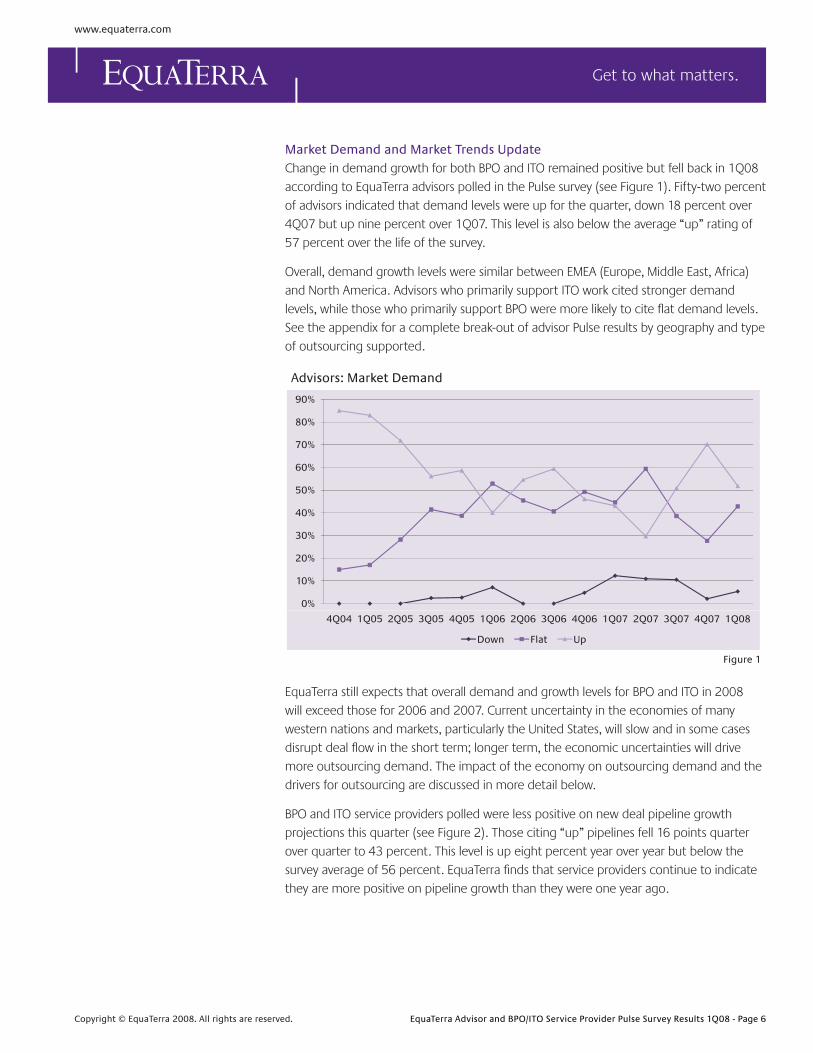

Market Demand and Market Trends UpdateChange in demand growth for both BPO and ITO remained positive but fell back in 1Q08 according to EquaTerra advisors polled in the Pulse survey (see Figure 1). Fifty-two percent of advisors indicated that demand levels were up for the quarter, down 18 percent over 4Q07 but up nine percent over 1Q07. This level is also below the average “up” rating of 57 percent over the life of the survey.

Overall, demand growth levels were similar between EMEA (Europe, Middle East, Africa) and North America. Advisors who primarily support ITO work cited stronger demand levels, while those who primarily support BPO were more likely to cite fl at demand levels. See the appendix for a complete break-out of advisor Pulse results by geography and type of outsourcing supported.

EquaTerra still expects that overall demand and growth levels for BPO and ITO in 2008 will exceed those for 2006 and 2007. Current uncertainty in the economies of many western nations and markets, particularly the United States, will slow and in some cases disrupt deal fl ow in the short term; longer term, the economic uncertainties will drive more outsourcing demand. The impact of the economy on outsourcing demand and the drivers for outsourcing are discussed in more detail below.

BPO and ITO service providers polled were less positive on new deal pipeline growth projections this quarter (see Figure 2). Those citing “up” pipelines fell 16 points quarter over quarter to 43 percent. This level is up eight percent year over year but below the survey average of 56 percent. EquaTerra fi nds that service providers continue to indicate they are more positive on pipeline growth than they were one year ago.

Advisors: Market Demand

80%

90%

50%

60%

70%

30%

40%

0%

10%

20%

4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Down Flat Up

Figure 1

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 7

There are no major variations on pipeline growth assessments based on the profi le of the service providers polled. Results are more a function of specifi c service provider situations and their existing market traction and capacity levels, rather than functional outsourcing areas served.

Service providers were more positive on future outsourcing demand growth (see Figure 3). Fifty percent of polled service providers expect a demand increase next quarter. This response level was down seven percent from 4Q07, and below the survey average of 67 percent. It is important to note that this question is a measure of change in demand growth quarter over quarter, not absolute demand levels.

Service Providers: Demand Trends Next QuarterQ

80%

90%

100%

60%

70%

80%

30%

40%

50%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Decrease Flat Increase

Figure 3

Service Providers: BPO/ITO New Deal Pipeline Projections/ p j

80%

90%

100%

60%

70%

80%

30%

40%

50%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Down Q/Q About the same Up Q/Q

Figure 2

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 8

The fi nal chart in this section (see Figure 4) highlights the general trending in demand over the past 13 quarters. The weighted average is calculated based on response levels from both advisors and service providers for each quarter. Any aggregate totals above the line indicate overall market growth, while totals below the line indicate market contraction. While service providers often cite higher levels of pipeline/demand growth each quarter, the trending between advisors and service providers has been consistent quarter over quarter. This was the third straight quarter and the fourth over the life of the Pulse survey that aggregate advisor demand was greater than that for service providers.

Weighted Aggregate Demand: Advisors & Service Providersg gg g

Market Growth

Market Contraction

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Advisors Service Providers

Figure 4

Economy’s Impact on Outsourcing DemandEquaTerra polled both advisors and service providers this quarter on how the current slowing or recessionary trending in western markets and economies, particularly in the United States, was impacting outsourcing demand. Overall, both advisors and service providers indicated that negative economic and market conditions were likely to drive more outsourcing efforts (see Figure 5).

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 9

Economic Environment's Impact on Outsourcingp g

Little/no impact

Slowing/rethinking outsourcing plans

Driving more outsourcing

0% 10% 20% 30% 40% 50% 60%

Service Providers Advisors

Figure 5

EquaTerra advisors were more likely than service providers (55 percent compared to 38 percent) to cite that the current slowing economy is driving more outsourcing. Advisors operating in the Americas were more likely than those from EMEA to cite more demand for outsourcing. Twenty-nine percent of service providers, compared to 15 percent of advisors, indicated that the economy is causing buyers to slow or rethink outsourcing plans. The difference between advisor and service provider responses is in part due to the stage at which they enter the cycle. Service providers are more focused on deals in the transaction stage, while advisors are more focused on deals in the early planning stage.

Advisors and service providers agreed that longer term (2H08 and into 2009), outsourcing demand would increase because of economic conditions. Both advisors and service providers noted hesitancy among outsourcing buyers in the fall of 2007, but now that the magnitude of economic problems has become clearer, demand for outsourcing will accelerate. There was also consensus that the impact on other more discretionary types of business and IT services, such as consulting, systems integration, and some application development, will face a stronger negative impact in current economy.

Outsourcing DriversCurrent economic conditions are also impacting the reasons why buyers are pursuing outsourcing and the benefi ts they hope to achieve from those efforts. Cost reduction and cost avoidance are naturally key goals sought from outsourcing efforts in down economic times. EquaTerra is seeing in the market, however, that broader business goals as well as buyer sophistication and experience are heavily impacting the benefi ts sought from outsourcing. In some cases, these attributes can outweigh economic factors affecting decision-making and goal-setting.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 10

EquaTerra polled advisors and service providers in 1Q08 on whether buyers today were placing more emphasis on process improvement, innovation and transformation in their outsourcing efforts, or whether they were becoming more focused (or refocused) on cost cutting and cost avoidance. Advisors and service providers were in consensus that process improvement, innovation and transformation were becoming more commonly sought outsourcing goals (see Figure 6).

Focus – Cost Savings vs. Process Improvement & Innovationg p

More emphasis on cost reduction/avoidance

Emphasis has not changed

More emphasis on process imp., innovation & transformation

0% 10% 20% 30% 40% 50% 60%

Service Providers Advisors

Figure 6

This does not imply that cost savings and cost avoidance are no longer major drivers behind outsourcing efforts. Rather, their achievement is not the only thing buyers are seeking. EquaTerra often fi nds, for example, that price is not the fi nal deciding factor in outsourcer selection. That said, to make the “short-list” outsourcers must still exhibit that they can deliver the threshold cost savings buyers are seeking.

Much depends, however, on the buyer and its individual circumstances. Second generation buyers, for example, place more emphasis on process improvement and innovation than those with less experience. As one advisor noted, “As the buyer market matures there is a growing ‘C level’ drive for real process improvement and innovation… not instead of, but in addition to cost avoidance.”

There are also differences between BPO and ITO buyers. HRO buyers, for example, have typically placed strong emphasis on innovation, but to date have more often been disappointed in achieving this goal than peers in other functional areas. HRO buyers today are more often approaching the market with more scaled back – and realistic – process improvement and innovation goals.

While there is a will to pursue process improvement and transformation, the means to do so are still often limited. As one service provider noted, “Not all buyers are prepared to make the needed investments for change management as it relates to process improvement and transformation.”

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 11

Overemphasizing cost savings or cost avoidance, however, can also create problems. Outsourcing buyers fi xated on cost savings can end up suffering in the long run from lower performance levels in functions outsourced, and service providers will inevitably de-prioritize low or negative margin accounts. As one advisor offered, “Governments are worried about defi cits and stakeholders are worried about high fi xed-cost overheads. To ameliorate this they push outsourcing for the wrong reasons, i.e., cost reduction only.”

Demand Trends by Functional AreaDemand trends by functional area (e.g., F&A, HR, and IT) continued in the same direction in 1Q08 as they have over the past few quarters, according to EquaTerra advisors (see Figure 7). As depicted, ITO was the strongest functional demand area, followed by FAO and HRO. HRO demand deceleration has bottomed out, with expectations of improved growth levels over the next 12-18 months. Overall demand for the outsourcing of one or two core HR processes will remain stronger than for comprehensive HRO (e.g., multiple processes) as buyers continue to pursue smaller and more selective outsourcing efforts. This is in part a function of leading HRO service provider capacity constraint, coupled with their lessened appetite for pursuing larger, more complex, and potentially less profi table, deals.

Advisors: Demand by Functional Areay

ITO

HRO

FAO

Other

CC/CRM

Procurement

Other

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06 1Q05

Figure 7

[*Note: A change to how advisors rank process area demand was recently made. In quarters prior to 3Q06, advisors ranked each process area sequentially (one through six) in terms of demand, which led to the cumulative ranking. Starting in 3Q06, advisors selected areas of greatest demand, creating an aggregate ranking. This is the same ranking process employed in the service provider polling.]

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 12

A review of EquaTerra’s own pipeline reinforces these broader market rankings. As of the end of March 2008, the top functional areas represented in the pipeline in terms of absolute number of opportunities (not ultimate total contract value) distributed across the major functional areas were as follows:

• IT: 48 percent

• HR: 17 percent

• Multi-tower: 14 percent

• F&A: 5 percent

• Procurement: 3 percent

• Other: 13 percent

An assessment of the pipeline for deals likely to close later in 2008 shows an uptick in both HRO and multi-tower outsourcing demand.

Service providers’ and EquaTerra advisors’ functional demand rankings were generally in sync in 1Q08 (see Figure 8). ITO was the leading area of demand cited by service providers, followed by HRO and FAO. EquaTerra attributes the somewhat higher HRO levels indicated by service providers compared to advisors to the sample mix of respondent service providers this quarter, as there were a higher number of service providers targeting one to two process HR outsourcing deals.

Service Provider: Demand by Functional Areay

ITO

FAO

HRO

CC/CRM

Other

Procurement

CC/CRM

0% 10% 20% 30% 40% 50%

1Q08 1Q07 1Q06

Figure 8

EquaTerra continues to see an increase in both demand for and supply of emerging general and administrative areas beyond customer care and back-offi ce general and administration BPO. This includes knowledge process outsourcing (KPO) for functions such as engineering, research and development, analytics and legal process work, fi nancial modeling and analytics, and drug development and clinical trials services. Multi-nationals and specialized service providers are also becoming more active in document services, facilities and real estate, and logistics services.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 13

In 1Q08 Pulse responses, both EquaTerra advisors and service providers noted increased demand in a variety of emerging and non-traditional areas, including the following:

• Vertical industry services such as middle-offi ce work in the banking and fi nancial services industries, and industry-specifi c healthcare payer services

• Legal process outsourcing

• Engineering services

• Document, electronic records and imaging services

• Real estate services

• Fleet services

• Remote or offshore IT infrastructure outsourcing services

The charts on the following two pages illustrate outsourcing demand by function and process areas for the four major functional areas polled in the surveys.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 14

Advisors: Functional and Process Area Demand Service Providers: Functional and Process Area Demand

Service Providers: Procurement Outsourcing Demandg

AP

OM/TP

Category Mgmnt

Fin. Rep./Analysis

Strategic Sourcing

Req Approval

Receiving/Inven tory

Mgmnt/Admin.

Other

Fixed Assets

Req.Approval

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07

Figure 16

Service Providers: HRO Demand

HR IT

Payroll

Compensation

Benefits

HR IT

Learning/Training

Recruiting/Talent Mgmnt

Expatriate and Relocation

Workforce Effectiveness

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06 1Q05

Figure 13

Advisors: HRO Demand

Benefits

Payroll

Recruiting/Talent Mgmnt

HR IT

Workforce Effectiveness

Compensation

Learning/Training

Other

Expatriate & Relocation

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06 1Q05

Figure 9

Advisors: Procurement Outsourcing Demandg

AP

Order Mgmnt

Mgmnt/Admin.

Strategic Sourcing

Category Mgmnt

Receiving/Inventory

Fixed Assets

Req. & Approval

Other

Fin. Rep./Analysis

Receiving/Inventory

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07

Figure 12

Service Providers: ITO Demand

ADM

Desktop Services

Infrastructure/Ops

Networks/Telco

Packaged Apps Svcs

Other

Networks/Telco

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06

Figure 15

Advisors: ITO Demand

Infrastructure/Ops

Desktop Services

ADM

Packaged Apps Svcs

Networks/Telco

Other

Packaged Apps Svcs

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06 1Q05

Figure 11

Service Providers: FAO Demand

A t P bl

AR/C&C

General Accoutning

Accounts Payable

Decision Support

Fin, Control, Risk Mgmnt

Other

Travel & Entertainment

0% 10% 20% 30% 40% 50% 60% 70% 80%

1Q08 1Q07 1Q06

Figure 14

Advisors: FAO Demand

A t P bl

AR/C&C

General Accounting

Accounts Payable

Finance, Control, Risk Mgmnt

Travel & Entertainment

Decision Support

Other

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1Q08 1Q07 1Q06 1Q05

Figure 10

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 15

Additional HRO and RPO Research: Talent and Transformation Study EquaTerra recently completed a new market study on how buyers are attempting to transform HR into a more strategic function. The study evaluates specifi c trends and how buyers are using outsourcing (or not) to achieve internal objectives in HR. The study focuses on what it takes to make HR more strategic, the challenges and opportunities HR organizations face in becoming more strategic, and the role that outsourcing and other alternative service delivery models can play in supporting these efforts. This market study was conducted in conjunction with Human Resource Executive® magazine, and is an update to a similar study the two conducted in 2005.

The highlights from this market study are included below. Please contact EquaTerra research ([email protected]) for additional information on the study results.

The market study assessed how respondents – approximately 450 HR leaders, primarily based in North America – viewed their organizations’ HR operations from a strategic perspective. HR groups generally fared well, with 57 percent of respondents indicating that HR is viewed as a strategic asset to their organization, compared to just 18 percent who indicated it is viewed as a cost center. Sixteen percent of respondents indicated executive management did not have a strong opinion on whether HR was strategic, and nine percent indicated management had a mixed view of HR. Among non-HR respondents, however, only 47 percent indicated that executive management viewed HR as a strategic asset, while 27 percent indicated HR was viewed as a cost center.

HR groups must clearly defi ne what strategic means in the context of their own organizations and situations. The study’s fi ndings point toward a growing consensus on what is “strategic HR,” though there are still some differences of opinion between and HR and non-HR executives. When questioned on what would make HR more strategic to their organization, over 70 percent of respondents (see Figure 17) indicated becoming a leader in “total talent management,” which includes recruiting, performance, learning and succession planning. Respondents from larger organizations (more than 5,000 employees) placed even more emphasis on talent management than smaller organizations. Tactical profi ciency and effectiveness in managing core HR processes – where the bulk of daily HR activity is typically spent – ranked fourth. Non-HR respondents ranked tactical profi ciency even lower.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 16

What Makes HR Strategic?g

Leader in Total Talent Management

Strong Partner-Broader Operations

Strong Partner-Strategic Planning

Tactical Proficiency/Effectiveness

Strong Partner-Globalization/Global Expansion

Strong Partner-BD & Sales

0% 10% 20% 30% 40% 50% 60% 70% 80%

Figure 17

The market study assessed the role and value of alternative HR service delivery models in transforming HR to make it more strategic. Adoption rates for shared services and outsourcing varied signifi cantly depending on the HR process addressed and the size and industry of the respondents’ organization. Overall, more organizations had deployed shared services than had undertaken IT outsourcing or business process outsourcing. Larger organizations and those in the commercial sector were more likely to have undertaken ITO and BPO. Payroll and benefi ts administration were the two HR processes most frequently outsourced. Nineteen percent of respondents overall, and 23 percent from organizations with more than 5,000 employees, had undertaken recruitment process outsourcing (RPO).

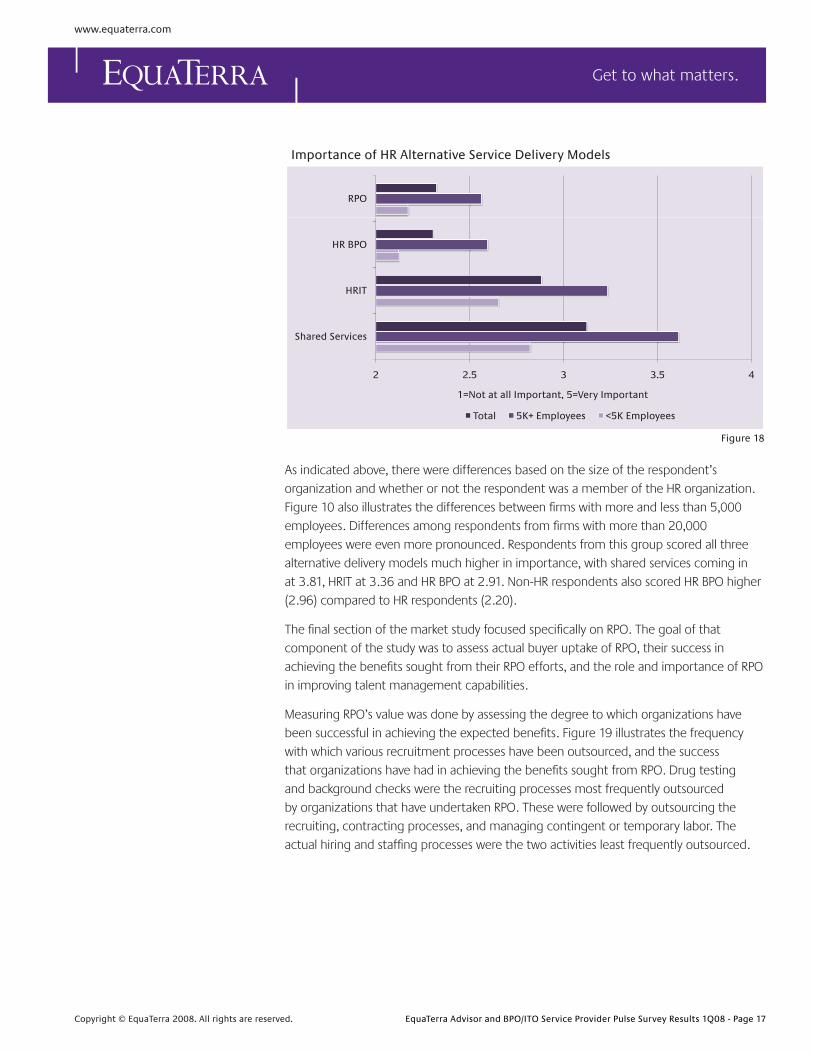

When ranking how important they felt alternative delivery models, such as shared services or outsourcing of IT or business processes, are to transforming HR to make it more strategic, respondents scored each in the mid-to-lower-end of a fi ve-point scale where one represented not at all important and fi ve represented very important (see Figure 18). The use of shared services scored the highest, though only slightly above the mid-point on the scale, and was followed by HRIT and HR BPO in terms of importance.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 17

Importance of HR Alternative Service Delivery Models

RPO

p y

HR BPO

HRIT

2 2.5 3 3.5 4

Shared Services

1=Not at all Important, 5=Very Important

Total 5K+ Employees <5K Employees

Figure 18

As indicated above, there were differences based on the size of the respondent’s organization and whether or not the respondent was a member of the HR organization. Figure 10 also illustrates the differences between fi rms with more and less than 5,000 employees. Differences among respondents from fi rms with more than 20,000 employees were even more pronounced. Respondents from this group scored all three alternative delivery models much higher in importance, with shared services coming in at 3.81, HRIT at 3.36 and HR BPO at 2.91. Non-HR respondents also scored HR BPO higher (2.96) compared to HR respondents (2.20).

The fi nal section of the market study focused specifi cally on RPO. The goal of that component of the study was to assess actual buyer uptake of RPO, their success in achieving the benefi ts sought from their RPO efforts, and the role and importance of RPO in improving talent management capabilities.

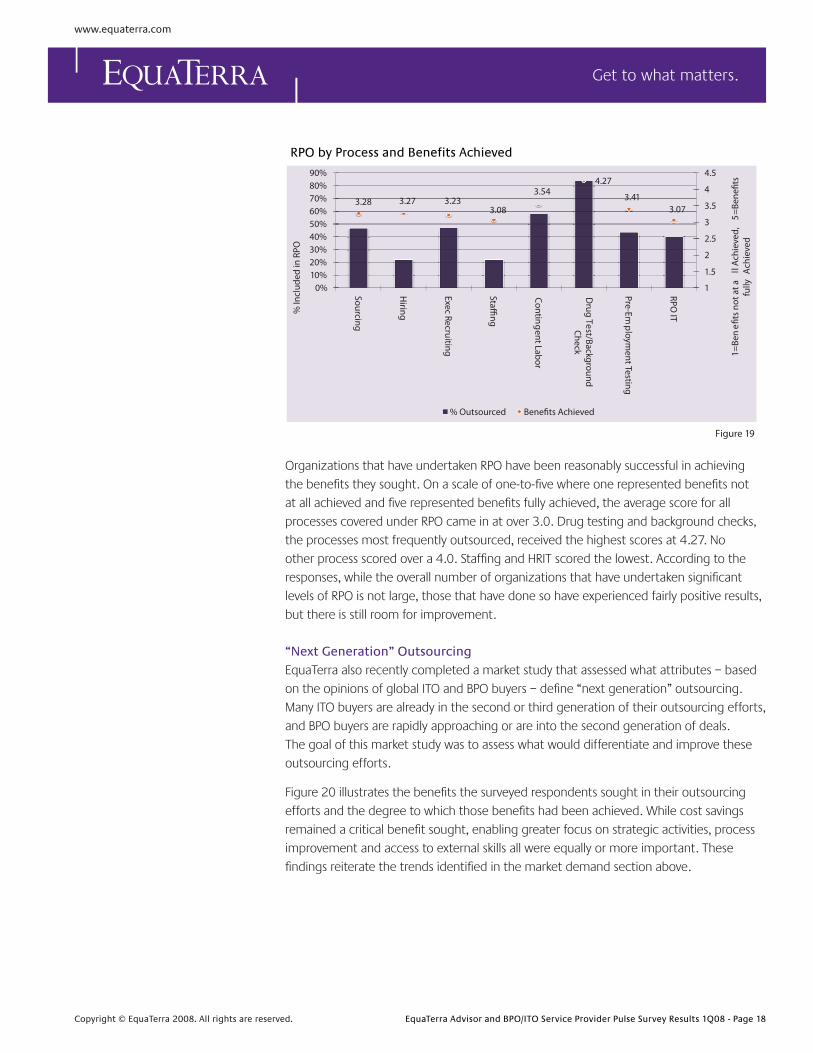

Measuring RPO’s value was done by assessing the degree to which organizations have been successful in achieving the expected benefi ts. Figure 19 illustrates the frequency with which various recruitment processes have been outsourced, and the success that organizations have had in achieving the benefi ts sought from RPO. Drug testing and background checks were the recruiting processes most frequently outsourced by organizations that have undertaken RPO. These were followed by outsourcing the recruiting, contracting processes, and managing contingent or temporary labor. The actual hiring and staffi ng processes were the two activities least frequently outsourced.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 18

3.28 3.27 3.233.08

3.544.27

3.413.07 3.5

4

4.5

60%70%80%90%

5=Be

nefit

s

2

2.5

3

10%20%30%40%50%

ll A

chie

ved,

5

Ach

ieve

d

e1

1.5

0%10%

Sourcing

Hiring

Exec Recruiting

Staffing

Conting

Drug Te

Pre-Emp

RPO IT

efits

not

at a

lfu

lly A

% In

clud

ed in

RPO

g gent Labor

st/BackgroundCheck

ployment Testing

1=Be

ne

% Outsourced Benefits Achieved

Figure 19

RPO by Process and Benefits Achieved

Organizations that have undertaken RPO have been reasonably successful in achieving the benefi ts they sought. On a scale of one-to-fi ve where one represented benefi ts not at all achieved and fi ve represented benefi ts fully achieved, the average score for all processes covered under RPO came in at over 3.0. Drug testing and background checks, the processes most frequently outsourced, received the highest scores at 4.27. No other process scored over a 4.0. Staffi ng and HRIT scored the lowest. According to the responses, while the overall number of organizations that have undertaken signifi cant levels of RPO is not large, those that have done so have experienced fairly positive results, but there is still room for improvement.

“Next Generation” Outsourcing EquaTerra also recently completed a market study that assessed what attributes – based on the opinions of global ITO and BPO buyers – defi ne “next generation” outsourcing. Many ITO buyers are already in the second or third generation of their outsourcing efforts, and BPO buyers are rapidly approaching or are into the second generation of deals. The goal of this market study was to assess what would differentiate and improve these outsourcing efforts.

Figure 20 illustrates the benefi ts the surveyed respondents sought in their outsourcing efforts and the degree to which those benefi ts had been achieved. While cost savings remained a critical benefi t sought, enabling greater focus on strategic activities, process improvement and access to external skills all were equally or more important. These fi ndings reiterate the trends identifi ed in the market demand section above.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 19

Outsourcing Benefits Sought/Achieved

3

3.5

80%

90%100%

Ach

ieve

d

2.5

30%

40%

50%

60%

hie

ved,

5=F

ully

Bu

yers

See

kin

g B

enef

it220% U

nclear

Access to GR

Cost Avoid

Fund Trans

Improve R Im

Responsive

Process Im

Improve P

Access Ext

Reduce Ov

Focus on MA

ct =Not

at a

ll A

ch%

Global/“O

ffsh

oesources

dance

sformational E

f

esults/Shareho

ROI

mprove

eness/Flexibilit

mprovem

ent

rocess Perform

ernal Skills

verall Costs

More Strategic

tivities

1=

re”

fforts

older

y

mance

Benefit Sought Benefit Achieved

Figure 20

70%

The success buyers have had in achieving the desired benefi ts has been mixed to positive. On a scale of one-to-fi ve, where one represented not at all achieved and fi ve represented fully achieved, respondents delivered rankings in the high two to mid-three range. These results are above the norm, but clearly show room for improvement.

This market study also assessed how the characteristics and attributes of second and third generation outsourcing efforts are changing. The changes are being driven both by outsourcing buyers’ increased levels of experience and sophistication as well as the more complex nature of their efforts. Figure 21 highlights the commonly cited characteristics of next generation outsourcing efforts.

Significant process improvement/transformation

Sophisticated management/governance processes

Multi-sourcing

Innovative pricing models

S hi ti t d i

Outsourcing of more strategic processes

Multi-shoring/integrated global sourcing model

Use of global resrouces

Multi-tower outsourcing

More outsourcing overall

Sophisticated sourc ing processes

Less outsourcing overall

Figure 21

0% 10% 20% 30% 40% 50% 60% 70%

“Next Generation” Outsourcing’s Characteristics

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 20

As shown in Figure 21, buyers identifi ed improved outsourcing management and governance capabilities as the key characteristics of next generation outsourcing. These were followed by the enablement of signifi cant process improvement and transformation through outsourcing, and the greater use of innovative pricing models. The emphasis on these highlights the ongoing shift of outsourcing serving just as a tool to reduce costs to a broader-based component of an organization’s overall business strategy.

The fi nal section of this study focused on what buyers would do, or do differently, in next generation outsourcing efforts to better ensure the achievement of benefi ts sought. Figure 22 illustrates what study respondents cited as the critical success factors in second and third generation outsourcing efforts.

"Next Generation" Outsourcing's Critical Success Factorsg

Cultural fit

Governance model

Pricing model

Picking the “best” service provider(s)

Cultural fit

Service provider's IT capabilities

Transition process

Use of global/offshore resources

Sourcing model and process

0 0.2 0.4 0.6 0.8

Service delivery location

Figure 22

Buyers are clearly learning from experience the importance of outsourcing management and governance. EquaTerra has long emphasized the importance of outsourcing governance, but buyers’ appreciation of its importance tends to come only with personal experience and the growth of their outsourcing sophistication. Cultural fi t – another attribute EquaTerra has long cited as important – was the other success factor cited by more than 50 percent of respondents. The degree to which all outsourcing buyers can prioritize and emphasize outsourcing components like governance will determine their ultimate ability to achieve success in their outsourcing efforts.

Demand Trends by IndustryThe two charts (next page) illustrate industry demand as cited by EquaTerra advisors and service providers. Generally, industry rankings have been consistent between the two over the past few quarters.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 21

Demand in the banking, fi nancial services and insurance industry group remains relatively strong, according to both EquaTerra advisors and service providers, although citations have slipped over the past two quarters. While there has been much speculation on the impact of the fall-out from the mortgage and credit crisis regarding demand for outsourcing in the fi nancial services industry, EquaTerra still holds that demand for outsourcing in the fi nancial services market will grow 2Q08 and into 2009, though demand for other types of more discretionary services like consulting will likely fall. EquaTerra also expects the focus of outsourcing efforts to shift more heavily toward cost reduction and cost avoidance, and away from process improvement and transformation, as buyers in this industry segment struggle with downsizing, stagnant market growth and profi tability challenges.

Public sector demand cited by EquaTerra advisors includes outsourcing, process improvement efforts and support for the deployment of shared services. While ITO demand remains strong within the public sector, service providers are winning a diverse range of deals beyond back-offi ce services, including training, operational support and supply chain management work.

Pharma/Biotech

Banking, Fin Svcs, Insurance

CPG, Food/Bev, Retail, Wholesale

Manufacturing

Govt (Fed, State, Local), Edu

Energy/Utilities, Oil & Gas

Manufacturing

0% 10% 20% 30% 40% 50% 60% 70%

1Q08 1Q07 1Q06

Figure 23

Advisors: Demand by Industry – Top Five

Service Providers: Demand by Industry – Top Five

CPG, Food/Bev, Retail, Wholesale

Banking, Fin Svcs, Insurance

Manufacturing

Entertainment/Media, Hospitality

Telco

-10% 0% 10% 20% 30% 40% 50% 60% 70%

1Q08 1Q07 1Q06

Figure 24

High Tech Product/Svcs

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 22

Outsourcing Problem SpotsEquaTerra polled both its advisors and the service provider community on the key advice they are giving buyers to help them achieve success in their outsourcing efforts. Through an analysis of this advice, it is possible to identify both the problem spots in today’s outsourcing market as well as the key contributors to outsourcing success.

Below is a summary of the cited problems, which fall into fi ve major categories. These points can serve as a roadmap for current and prospective buyers of key issues to address when undertaking outsourcing initiatives.

Key advice to buyers from EquaTerra Advisors

• Executive support – “Commitment from the top. It will take strong will and commitment to outsource and

receive positive results. The qualifying item is patience. It will not be perfect out of the box, but with effective planning and sound governance, companies who engage in BPO do not turn back.”

• Planning– “Have a vision, communicate and rally around the vision...then tactically execute to

the vision.”

– “Clear objectives, defi ned results, measure and drive change in order to achieve objectives.”

– “Focus on the sourcing strategy – scope, criteria, model, governance – don’t let cash fl ow drive push you into opportunistic behavior.”

– “Consider the entire outsourcing lifecycle when planning your outsourcing initiatives. Pay particular attention to agreement governance and invest in it so you can realize all the savings you have planned.”

• Service provider relations– “Manage the service provider tightly, with frequent dashboard reporting and status/

resolution update meetings. Buyers must be involved with provider’s daily operations, and must clear internal road blocks to make them successful on your behalf.”

– “Stress the importance of a cooperative/collaborative approach and the critical imperative of implementation.”

– “It is possible to fast track the procurement process via a more collaborative/inclusive approach with tendering suppliers.”

• Business case– “Stress the importance of being realistic about the ‘cost to achieve’ and ‘cost of

governance’, as well as the importance of achieving any fi nancial goals in the early years of a deal (i.e. don’t rely on years 9 and 10 to provide the savings you need!)”

– “The supplier has to make a profi t, and savings can only be made where they are available to be made.”

• Transition and governance– “Don’t under-estimate the resources and effort required to perform a competent

transition of services to the provider.”

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 23

– “Allocate and budget adequate resources for transition and assure that the provider can handle the process when tendered.”

– “Recognize the importance of skilled and robust governance in leveraging the maximum value from your outsourcing arrangements.”

– “Two pieces of advice…governance is key and you must build it before you outsource, and outsourcing is not always (and only) about cost.”

Elaborating and touching on these points, one service provider offered the following analysis: “Buyers often come to us struggling with governance issues from their other outsourcing experiences. They often lack a way to measure and track the real benefi ts of the outsourcing effort, including cost reduction, performance improvement, and customer satisfaction. They also seek better ways to manage the relationship with the service provider to continually improve the relationship and the services delivered. Those companies deciding to outsource wrestle with choosing the right process area to outsource (scope of effort, own/retain vs. outsource boundaries), and selecting the right service provider(s) to partner with.”

“In managing and governing the outsourced efforts, buyers need to ensure they consider the effort in the same way they approach transformation or signifi cant IT projects, and put in place the right resources to manage relationships with service providers. Outsourcing will require buyers to have signifi cant leadership buy-in and participation, ability to measure, manage, and ensure delivery performance of the service provider, and to communicate appropriately to all involved or impacted by the change.”

EquaTerra also polled buyers in the next generation outsourcing study referenced above on what they felt were the biggest impediments to their outsourcing success. Many of today’s, and purportedly yesterday’s, barriers to outsourcing success will still exist going forward. Figure 25 illustrates the leading cited BPO and ITO impediments.

Quality/fit of service providers

Change management

Internal "political" pressure against outsourcing

Retained org./governance challenges

Inade quate /unrealistic business case

Inadequate executive/management support

Loss of faith in outsourcing's value proposition

Meeting compliance regulations

Costs to do the deal

Negative market pressures

Figure 25

10%0% 20% 30% 40% 50% 60%

Impediments to Outsourcing Success

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 24

Change management and governance have long proven challenging to both buyers and service providers. While recognition of these impediments has grown, buyers’ ability to adequately address these issues remains mixed. And although the growing recognition of the importance of change management and governance to outsourcing success is a very positive market development, the bigger challenge for buyers and service providers is improving their capabilities in these critical areas.

Sales CycleFor the purposes of the Pulse surveys, the sales cycle is defi ned as the time period from the release of the RFP to contract signing. Many factors contribute to the length of the sales cycle, including:

• What is being outsourced

• Level of buyer sophistication and experience

• Complexity, size and global reach of the potential outsourcing deal

• Number of service providers competing and the structure of the sourcing process

• Preferred service provider sales pursuit capacity and selectivity

• Whether a sourcing advisor is being used

• Disruption to the sourcing process by turmoil in the buyer account, economic uncertainty, or changing macro-business – all heightened issues in the current market

The Pulse surveys do not measure the absolute length of sales cycles. EquaTerra estimates, however, that for larger deals (those with more than $50 million in total contract value) that are competitively bid, the sales cycle is typically six to 12 months from the time the buyer goes to the market until the deal is closed.

Current market trends are contributing to both shortening and lengthening sales cycles, and in some cases, the effect is for the trends to cancel each other out. Smaller deals pursued by more experienced buyers can lead to shorter sales cycles. On the other hand, the complexities associated with multi-sourcing can complicate the sourcing process and extend the sales cycle, as can consideration of more intricate pricing arrangements. Global deals are also more complex to source. Some of the lengthening of sales cycles is cyclical. A shorter or longer sales cycle, however, is not necessarily a good or bad thing from the buyer’s perspective.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

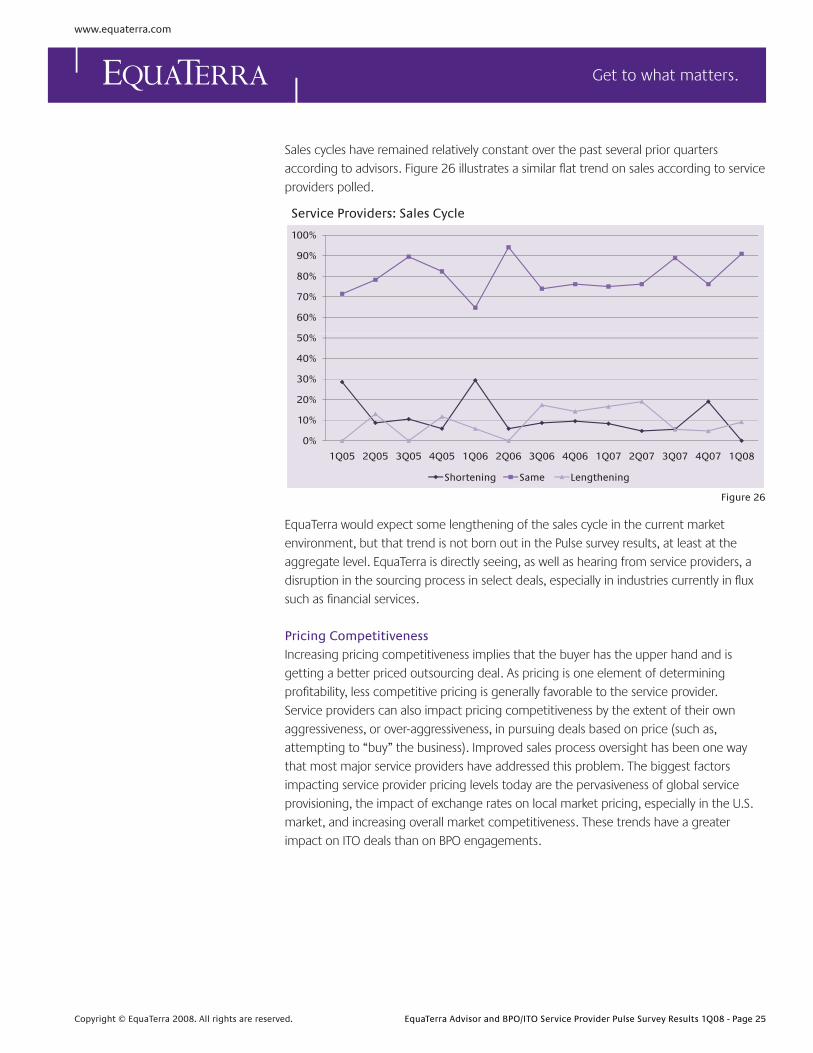

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 25

Sales cycles have remained relatively constant over the past several prior quarters according to advisors. Figure 26 illustrates a similar fl at trend on sales according to service providers polled.

Service Providers: Sales Cycley

80%

90%

100%

60%

70%

80%

30%

40%

50%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Shortening Same Lengthening

Figure 26

EquaTerra would expect some lengthening of the sales cycle in the current market environment, but that trend is not born out in the Pulse survey results, at least at the aggregate level. EquaTerra is directly seeing, as well as hearing from service providers, a disruption in the sourcing process in select deals, especially in industries currently in fl ux such as fi nancial services.

Pricing CompetitivenessIncreasing pricing competitiveness implies that the buyer has the upper hand and is getting a better priced outsourcing deal. As pricing is one element of determining profi tability, less competitive pricing is generally favorable to the service provider. Service providers can also impact pricing competitiveness by the extent of their own aggressiveness, or over-aggressiveness, in pursuing deals based on price (such as, attempting to “buy” the business). Improved sales process oversight has been one way that most major service providers have addressed this problem. The biggest factors impacting service provider pricing levels today are the pervasiveness of global service provisioning, the impact of exchange rates on local market pricing, especially in the U.S. market, and increasing overall market competitiveness. These trends have a greater impact on ITO deals than on BPO engagements.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 26

EquaTerra did not poll its advisors on pricing competitiveness in 1Q08. Over the prior quarters, however, a consistent division existed among EquaTerra advisors relative to the degree of pricing competitiveness in the market. Advisors who primarily support ITO saw more aggressive pricing, while those that support BPO saw less aggressive pricing. BPO, particularly for larger multi-process FAO and HRO deals, remains a seller’s market in terms of pricing. These fi ndings are in sync with broader service provider market trends, relative competitiveness and pressure on several leading BPO service providers to improve margins.

Service providers polled in 1Q08 indicated a rebound in more aggressive pricing (see Figure 27). Forty-fi ve percent of service providers indicated pricing had become more aggressive, up 22 percent quarter over quarter to the highest level since 4Q06. Less than fi ve percent of providers indicated pricing was becoming less aggressive. EquaTerra attributes this increase in pricing competitiveness to buyers’ increased focus on price in tougher economic times, more competition for the business and the globalization of service delivery capabilities leveling the cost playing fi eld.

Service Providers: Contract Pricingg

70%

80%

50%

60%

20%

30%

40%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

More Aggressive Same Less Aggressive

Figure 27

Deal Scope Deal scope is defi ned as the number of processes, users, geographies, etc., included in an outsourcing arrangement. Contract value is usually directly correlated to scope, though the mix of remote/low-cost delivery resources involved will also impact contract value. From the outsourcing buyer’s perspective, understanding trends in scope and contract value helps not only to determine how aggressively other organizations are pursuing outsourcing, but also how to defi ne and construct a viable and potentially optimal-sized deal with a service provider. It is also important for buyers to note the ongoing decline of “mega-deals” (deals with more than $1 billion in total contract value), though market growth has sustained through an increased number of smaller and multi-provider deals.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 27

EquaTerra did not poll its advisors on deal scope in 1Q08. Scope levels have remained fl at to declining for the past several quarters. Services providers again in 1Q08 cited declining scope in new deals in the pipeline (see Figure 28). Just 19 percent of service providers indicated scope was increasing, the lowest level recorded in the life of the Pulse survey, while 24 percent indicated scope was decreasing, the highest level recorded since the inception of the survey.

Service Providers: Scopep

70%

80%

50%

60%

20%

30%

40%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Increased Same Decreased

Figure 28

The reasons for decline in deal scope, or lack of scope growth, include more multi-provider sourcing, buyer preferences for smaller deals, service provider capacity constraints, and less appetite for mega-deals in both the buyer and the provider communities. Increased buyer caution in the current economic environment is also driving down scope.

Indian service providers were somewhat more likely to cite increasing scope. For many of these fi rms, the absolute size of the scope base from which they are starting is smaller given their heritage in the application development and maintenance (ADM) space, which often hosts smaller deals than other types of ITO. Relative to BPO, most Indian providers are still focused on smaller deals, though they are ramping up capabilities. Overall, the trend is toward smaller scope deals in ITO and, more recently, smaller scope BPO deals.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 28

Service Providers: Contract Profi tability and Ability to Increase ScopeSeveral factors impact service provider profi tability, including deal scope, transition costs and time frames, and buyer pricing sophistication. Wage infl ation and exchange rates continue to negatively impact service provider profi tability, particularly fi rms with extensive India-based operations. Exchange rates have stabilized somewhat over the past few quarters. Service providers with a higher mix of remote/low-cost resources are also putting pressure on the profi tability of competitive peers with fewer lower-cost resources. This has long been the case in ITO, and it is becoming more prevalent in BPO. While this is, in part, a multi-national versus India-based service provider issue, as multi-nationals diversify resources geographically and both camps expand offshore outside of India, it is more often a practice or industry-specifi c scenario to determine which provider has the strongest and lowest-cost resources. It is important to note that the Pulse survey question on profi tability addresses existing contracts that have been executed, not new deals in the pipeline.

After several quarters of declining profi tability, service providers’ levels fl attened in 4Q07 and remained at the same levels for 1Q08. Thirty percent of service providers indicated improving existing contract profi tability, the fi rst quarter over quarter increase in one year, but a level still well below the survey average (see Figure 29). So while service providers’ profi tability did not signifi cantly improve, the fi ndings indicate providers are protecting profi tability gains made in earlier quarters.

Service Providers: Profitabilityy

70%

80%

50%

60%

20%

30%

40%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Improving Profitability Same Amount Declining Profitability

Figure 29

Service providers were less optimistic than usual about their ability to increase deal scope within current client accounts. Just 52 percent expected to increase scope in current accounts, down 14 percent quarter over quarter and below the survey average of 68 percent (see Figure 30, next page). Ten percent indicated scope would decline in existing accounts, matching the highest level recorded in the survey. Most Indian service providers were more optimistic on their ability to increase scope, highlighting that they remain very capable of growing business in existing accounts.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 29

Service Providers: Ability to Increase Scopey p

80%

90%

100%

60%

70%

80%

30%

40%

50%

0%

10%

20%

1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Increase Remain Contstant Decline

Figure 30

Service Provider CapacityService provider capacity, as has been noted, is an important factor that impacts other trends such as pricing competitiveness, sales cycle and profi tability. EquaTerra defi nes service provider capacity as the availability of adequate and skilled resources for sales pursuit, engagement and transition/delivery. Capacity constraints are often more prevalent in BPO than ITO given that the BPO market is less mature, and in some respects, more complex. The challenge facing service providers is that quality capacity is in scarce supply and takes time – and multiple outsourcing deals – to develop.

Capacity is also tightly linked to service provider aggressiveness in deal pursuit. When service providers are being more selective and entering into fewer deals, as is often the case in today’s BPO market, they need less capacity for pursuit and delivery. Thus, capacity is intentionally constrained to keep costs down and to match capacity to what is needed to meet demand goals.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 30

Starting in 2Q07, EquaTerra polled its advisors on capacity for sales pursuits, transition and delivery. EquaTerra continues to poll service providers on overall capacity. Figure 31 illustrates capacity levels combined for pursuit and delivery, and Figure 32 separates pursuit and delivery capacity.

70%

50%

60%

70%

30%

40%

50%

10%

20%

30%

0%

10%

4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Constrained/Tightening Unchanged Adequate/Increasing

Figure 31

Advisors: Service Provider Capacity - Overall

Advisors: Service Provider Capacity, Pursuit & Deliveryp y y

70%

80%

60%

70%

40%

50%

60%

40%

50%

20%

30%

20%

30%

0%

10%

0%

10%

4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Constrained/Tightening Unchanged Adequate/IncreasingC/T - Pursuit U - Pursuit A/I - PursuitC/T - Delivery U - Delivery A/I - Delivery

Figure 32

Polled EquaTerra advisors cited an improvement in service provider pursuit capacity in 1Q08. Just 23 percent of EquaTerra advisors who focus on buyer outsourcing assessments and transactions, indicated that service provider capacity is constrained or tightening, down 21 percent for the quarter. Twenty-one percent of advisors, up from seven percent last quarter, indicated that service provider pursuit capacity is adequate or improving. There was little variance between advisors who primarily support BPO compared to those who primarily support ITO.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 31

The primary reason cited for improved pursuit capacity was increased service provider selectivity in deals being pursued. So capacity has not necessarily increased, it is just being more selectively used and applied.

There was some improvement in capacity levels for transition and ongoing service delivery. Thirty-fi ve percent of advisors indicated capacity is constrained, down 12 percent for the quarter and below the survey average of 55 percent. Just 10 percent of advisors, however, indicated delivery capacity was adequate or improving.

Capacity constraint for deal transitions is more a function of a shortage of adequate and skilled resources than of service provider discretion or selectivity. Transition capacity constraints are also impacted by overly complex deals – such as those that include extensive solution customization – and by ineffi cient or inconsistently followed transition processes and methodologies.

Service providers have under-resourced and under-priced BPO transitions in the past, and are readjusting pricing to more fully refl ect actual transition resource needs. More funds enable service providers to invest in more capacity. While buyers may see higher transition prices and transition costs more clearly called out and should vet these costs accordingly, these increased expenditures will often be money well spent. But while better pricing helps, it does not fully address the shortage of skilled resources.

This quarter again shows that service providers are consistently more optimistic on capacity levels. Sixty-four percent of service providers reported that capacity is adequate or increasing, with just fi ve percent indicating tight or constrained capacity (see Figure 33). There are no general trends relative to the type of service provider and their estimates around capacity levels. Differences on capacity levels between advisors and service providers are attributable to the following points:

• Difference of opinion as to what constitutes “adequate” in terms of both quantity and quality

• General mix of overall deals

• Capacity levels at different stages of the sourcing lifecycle (i.e., pursuit versus delivery) and expectations for future capacity into which service providers inherently have more insights

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 32

Service Providers: Service Provider Capacityp y

60%

70%

40%

50%

20%

30%

0%

10%

4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08

Constrained/Tightening Unchanged Adequate/Increasing

Figure 33

Update on Outsourcing Governance EquaTerra continually probes advisors and service providers on the importance of outsourcing management and governance to the success of outsourcing efforts, and to determine what is working and what is not relative to governance. EquaTerra views quality outsourcing governance processes and models, resources and supporting software tools as critical enablers to outsourcing success. EquaTerra market research has consistently found a direct correlation between buyers’ governance capabilities and investments and outsourcing success and satisfaction (see EquaTerra Perspective paper, “Why and How Outsourcing Management and Governance is Critical to Outsourcing Success” http://www.equaterra.com/KR/research/why-and-how-OM-and-Governance-is-Critical-to-Outsourcing-Success.aspx and the EquaTerra market study, “Outsourcing Management and Governance: Building a Foundation for Outsourcing Success” http://www.equaterra/KR/research/omg-MO.aspx).

EquaTerra this quarter polled its advisors on what they believe are the key attributes of next generation outsourcing management and governance. Figure 34 illustrates the identifi ed attributes.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 33

Better planning for outsourcing governance

Managing outsourcing efforts as a portfolio

Greater use of software tools

Gaining greater executive support

Better alignment of goals with governance

M t ff/

Governance best practice processes

More emphasis on colla borative relationships

Greater leverage of third party support

Most buyers will not improve their capabilities

More governance s taff/resources

0% 10% 20% 30% 40% 50% 60%

Other

Figure 34

Defining “Next Generation” Outsourcing Governance

Managing outsourcing efforts as a portfolio, rather than a discrete and independent set of initiatives, was identifi ed as the most important aspect of next generation outsourcing governance. This is not surprising given the proliferation of outsourcing efforts within and across functions by second and third generation buyers. Better upfront planning and preparation for outsourcing governance, commencing during the sourcing process, was also cited as key, as was better alignment of the outsourcing model, resources and investments with the goals of the outsourcing effort. An example of misalignment – which is a common root cause of outsourcing problems and dissatisfaction – is pursuing a complex outsourcing effort focused on innovation while deploying a basic and low budget governance effort.

EquaTerra advisors offered buyers the following points of advice on how to improve their outsourcing governance efforts and capabilities.

• “Continually check to ensure the two parties are aligned. Regularly assess the capability of your governance team and audit the level of adherence to the governance processes. Do you have the right people with the right skills?”

• “Buyers must remember they are not outsourcing their accountability, and they have to fi nd that line between ‘managing’ and ‘governing’ (oversight). This is diffi cult for line managers who are thrust into governance to do.”

• “Don’t force fi t individuals into governance roles – identify the required skills and enlist resources appropriately.”

• “Service credits are not a punitive mechanism. Relationships should not be adversarial. Rather, you should be looking to encourage the right behaviors through a ‘win-win’ approach.”

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 34

• “Don’t over-engineer governance. Make governance something that is real, practical, and can be implemented. Focus your resources on the biggest impact areas by using experienced resources and advisors. Use automated tools to accelerate your governance resources.”

• “Make sure to implement state-of-the art technology to support governance as this will not only increase effectiveness but also reduce governance expenses and thus positively impact the baseline of the outsourcing initiative.”

• “Go for a more integrated approach and a true partnership, instead of only mentioning partnership but managing the relationship as a traditional buyer/seller situation.”

Service Provider Market UpdateEquaTerra polls its advisors on which service providers, in their opinions, are performing best in the market in terms of sales, offering portfolio, execution, delivery and other performance characteristics, as well as which ones face the most challenges in the same areas. Advisors are also asked to elaborate on trends they see relative to service providers excelling or struggling in the market. EquaTerra validates these fi ndings through comparative analysis with other data points, including its own pipeline report and other EquaTerra market studies.

Relative to general service provider trending over the past quarter, EquaTerra advisors identifi ed the following key developments.

• Global capacity constraint among BPO providers for sales pursuit is improving through narrowing of focus, but transition and delivery capacity is constrained

• Signifi cant selectivity among HRO providers for multi-process deals; growing selectivity among all BPO providers relative to larger and multi-tower deals

• Indian service providers continue to make inroads into multi-national accounts and “sweet-spots”, especially through growing business in new areas in existing client accounts; leading/Tier One multi-nationals are responding better/stronger than Tier Two and below fi rms

• Very positive satisfaction levels for Indian service provider clients in ITO (this was born out in the recently released EquaTerra European market service provider performance reports discussed below)

• Better pricing of transition costs for larger deals, especially in BPO

• More emphasis on global portfolio management of deals and clients

• Continued expansion of geographic footprint and delivery capabilities

Please contact EquaTerra Research directly for more detailed feedback on outsourcing service provider performance and capabilities.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 35

EquaTerra, through its acquisition of Morgan Chambers, now offers another key research deliverable on service provider performance. Morgan Chambers has published on an annual basis a series of Service Provider Performance studies. These studies are focused on leading EMEA ITO service providers and are organized by geography (such as the United Kingdom, Benelux, and the Nordics). These studies survey and interview named buyers of specifi c provider services. They provide direct insights into actual service provider performance levels. The reports also assess and interpret general outsourcing demand and activity trends in the markets covered. More information about this report series is available online via the country/region specifi c sections of the EquaTerra/Morgan Chambers web site (www.morganchambers.com/UK/; www.morganchambers/NL/, etc.). Please contact EquaTerra Research for additional details on this research service offering.

Deal Snapshot

EquaTerra estimates that approximately 120 outsourcing deals (ITO, general and administrative BPO, customer care) with greater than $50 million total contract value (TCV) were announced in 1Q08. Average TCV for these deals was approximately $250 million. The number of deals was up approximately 10 percent from 4Q07, but the average TCV slightly declined. Approximately 20 of these deals were for BPO with an average deal size of just under $300 million TCV. From an industry perspective, public sector (national, regional, local) was the most active sector; military/aerospace/defense was also very active. In the commercial sector, telecommunications and banking/fi nancial services were among the most active industries.

When estimating the number of new deals and average TCV, it is important to recognize that some deals are not publicly announced, or the deal details are not provided. The ultimate TCV of a deal is also likely to change over the life of the contract.

Following is a select list of some of the top deals from 1Q08.

Top Deals

• EDS-Telindus consortium award estimated at $825 million (€580 million) over seven years from the Flemish government. The consortium will provide IT services including support and management of end-user infrastructure to ensure the ICT environment’s accessibility to the Flemish government.

• Wipro Infotech win estimated at $600 million over nine years from Aircel (Maxis group company providing telco services in the Indian market). Wipro will take over the IT infrastructure, and develop and manage applications such as retail billing and revenue assurance.

• Computer Sciences Corporation (CSC) win estimated at $544 million over two years from NASA. CSC will manage facility repair and maintenance, utility operations, engineering, construction, and related services. It will also provide operations and maintenance support services.

• Capita Group win estimated at $390 million (£200 million) over 10 years from Marsh Limited to provide back-offi ce administration services.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 36

• SAIC, Battelle and Tetra Tech were among multiple outsourcing services providers that won business with the Air Force Center for Engineering and the Environment. The total value of the contracts is estimated at approximately $3 billion over 10 years if all options are exercised.

• An EDS led consortium, oneMeridian, win estimated at $935 million over eight years from the Infocomm Development Authority of Singapore (IDA). oneMeridian will help the IDA to standardize the public sector computer environment.

• RR Donnelley win estimated at $800 million over seven years from McGraw-Hill Education. RR Donnelley will assist McGraw-Hill in product areas including textbooks and teachers’ editions.

• Hewlett Packard win estimated at $675 million over seven years from Unilever. HP will standardize and optimize the IT environment and manage the client services environment.

• Lockheed Martin-led consortium win estimated at $1 billion over 10 years from the Federal Bureau of Investigation to build and managed the Next Generation Information (NGI) law enforcement biometric system.

• CSC, EDS, Lockheed Martin and Teletech were among the service providers selected by the U.S. General Services Administration to participate in the “USA Contact” program to provide emergency services and related call center services to government bodies and agencies. Total contract value for “USA Contact” is estimated at $2.5 billion over 10 years.

• T-Systems win estimated at $1.5 billion (€1 billion) over fi ve years from Royal Dutch Shell. T-Systems will provide global hosting and data center outsourcing services.

Service Providers: Current Deal Portfolio StatusIn the fi nal section of the Pulse survey, EquaTerra requests that service providers profi le the state of their current deal portfolio from several dimensions:

• Re-competes/Renegotiations

• Cancellations/Non-renewals

• Problem Contracts

Service providers are typically positive in each of these three categories. While troubled or failed outsourcing arrangements are typically well-publicized if the news makes it to the marketplace, the reality is that most outsourcing deals face periodic, and often ongoing, challenges that are ultimately resolved by the buyer and the service provider.

www.equaterra.com

Copyright © EquaTerra 2008. All rights are reserved.

Get to what matters.

EquaTerra Advisor and BPO/ITO Service Provider Pulse Survey Results 1Q08 - Page 37