equities for the long term 2014

TRANSCRIPT

Growth of $1.00 1971-2014

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

19

71

19

75

19

79

19

83

19

87

19

91

19

95

19

99

20

03

20

07

20

11

Stocks 10.7%

Bonds 7.7%

T-Bills 5.2%

CPI 4.2%

Long-Term Investors are Rewarded for

Taking Risk

Source: Russell, Bloomberg, Morningstar

Growth of $1.00 1941-1970

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

19

41

19

44

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

Stocks 12.2%

Bonds 1.9%

T-Bills 2.3%

CPI 3.5%

Long-Term Favorable Stock Returns is

not a Recent Phenomenon

Source: Bloomberg, Morningstar

Earnings Growth Drives Stock Prices

S&P 500 vs. Earnings

-100

50

200

350

500

650

800

950

1100

1250

1400

1550

1700

1850

2000

2150

2300

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

S&P 500

E.P.S.

Source: Standard & Poors

Over Shorter Periods, Stocks and Bonds

Can and Have Declined

Time Period Stocks Nasdaq Bonds

1973 /74 -48% -58% -

1978/81 - - -6%

1987 -35% -40% -

1990 -21% -27% -

1994 - - -8%

1998 -22% - -

1999 - - -9%

2000/02 -50% -78% -

2007/09 -57% -55% -

2011 -19% -19% -

Source: Russell, Bloomberg, Standard & Poors

Bear Markets are Followed By Bull

Rallies

Bear Market Decline 3 Years Following

1929/32 -63% 68%

1937 -34% 16%

1940/41 -22% 79%

1973 /74 -48% 58%

1987 -35% 48%

1990 -21% 55%

2000/02 -50% 54%

2007/09 -57% 86%

2011 -19% 79%

Source: Bloomberg, Yahoo Finance

The “Herd” Tends to Sell at the Bottom

Performance Fund Flows

1994/95 - Bonds - 8% -$50B

1999/00 - Bonds - 9% -$60B

1999/00 - Value -15% -$80B

2001/02 - Growth -60% -$26B

2007/09 – Stocks -57% -$412B

Maintaining an Investment Program is

Essential to Achieving Investment

Objectives

Source: Bloomberg, Smith Barney

A Longer Investment Time Horizon Equals a Greater Likelihood of Outperformance

0%

20%

40%

60%

80%

100%

1 Year 5 Years 10 Years 20 Years 30 Years

Relative Performance 1931-2014

Stocks Beat Bonds Stocks Beat T-Bills Bonds Beat T-Bills

Source: Russell, Bloomberg, Standard & Poors, Morningstar

Even Better from 1950

Volatility Decreases Over Time

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 Y

r Sto

cks

5 Y

r Sto

cks

10 Y

r Sto

cks

20 Y

r Sto

cks

30 Y

r Sto

cks

1 Y

r Bon

ds

5 Y

r Bon

ds

10 Y

r Bon

ds

20 Y

r Bon

ds

30 Y

r Bon

ds

1 Y

r T-B

ills

5 Y

r T-B

ills

10 Y

r T-B

ills

20 Y

r T-B

ills

30 Y

r T-B

ills

Average High Low

Investment Return Ranges 1930-2014

Source: Russell, Bloomberg. Standard & Poors, Morningstar

Risk Also Decreases Over TimeStandard Deviation of Investment

Returns Over Time

0.00%

5.00%

10.00%

15.00%

20.00%

1 Year 5 Year 10

Year

20

Year

30

Year

Stocks

Bonds

T-Bills

Source: Russell, Bloomberg, Standard & Poors, Morningstar

Stock Return Cycles Over Time

Returns Tend to Experience Waves

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

19

04

19

10

19

16

19

22

19

28

19

34

19

40

19

46

19

52

19

58

19

64

19

70

19

76

19

82

19

88

19

94

20

00

20

06

20

12

5-Year 10-Year 20-Year

Source: Bloomberg, Standard & Poors, Morningstar

Performance Cycles are Hard to Predict

3.40%

15.20%

-12.60%

0.40%

-12.30%-11.00%

1.30%

-4.60%

4.80%

-11.90%

10.70%7.80%

16.60%

-8.80%

-15.20%

4.60%

-1.20%

1.50%

-4.70%

23.10%25.80%

-29.40%

-14.77%-12.37%

-0.20%

-10.00%

-1.70%

-12.90%

12.00%

-1.50%

17.52%

1.20%2.25%

-2.25%

0.95%

-0.40%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

Value Vs. Growth

Annual Returns 1979-2009

Returns on Russell 1000 Growth Minus Russell 1000 Value

Source: Russell

Value Beats Growth

Growth Beats Value

Dow Jones vs. Earning

50

75

100

125

150

175

200

225

250

275

300

325

1921 1922 1923 1924 1925 1926 1927 1928 1929

2

4

6

8

10

12

14

16

18

20

Dow Jones E.P.S.

Secular Bull – The Roaring 20’s

Dow Jones vs. Earnings

50

75

100

125

150

175

200

225

250

275

300

325

350

1929

1931

1933

1935

1937

1939

1941

1943

1945

1947

1949

1951

1953

-1

2

5

8

11

14

17

20

23

26

29

32

35

Dow Jones E.P.S.

Consolidation - The Great Depression &

WWII

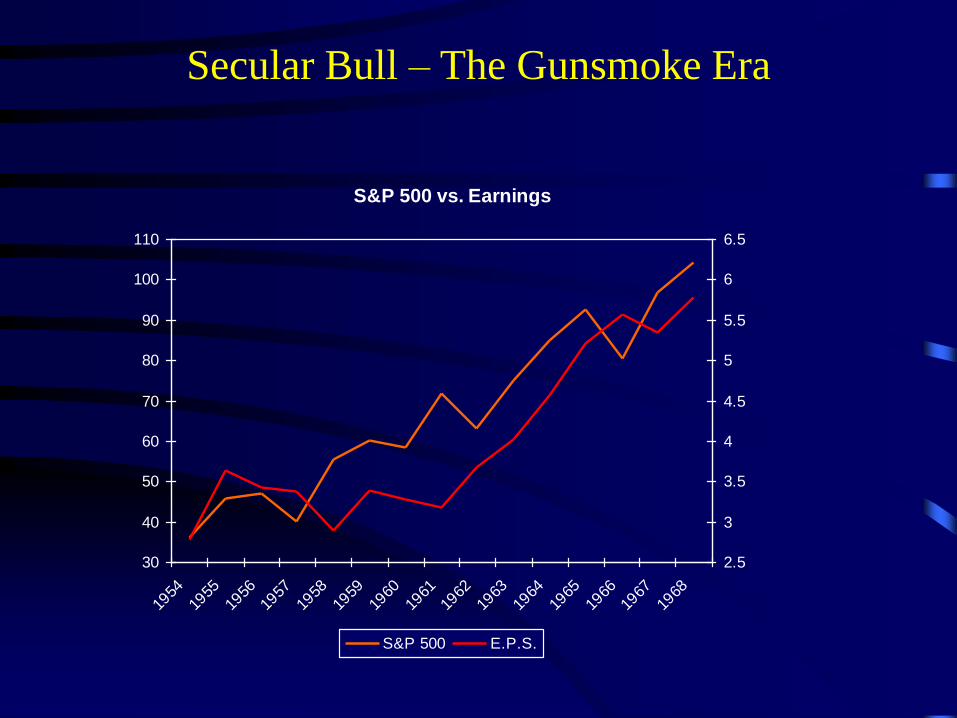

S&P 500 vs. Earnings

30

40

50

60

70

80

90

100

110

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

2.5

3

3.5

4

4.5

5

5.5

6

6.5

S&P 500 E.P.S.

Secular Bull – The Gunsmoke Era

S&P 500 vs. Earnings

60

70

80

90

100

110

120

1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979

4

5

6

7

8

9

10

11

12

13

14

15

S&P 500 E.P.S.

Consolidation – Stagflation & Oil

Embargo

S&P 500 vs. Earnings

100

200

300

400

500

600

700

800

900

1000

1100

1200

1300

1400

1500

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

10

15

20

25

30

35

40

45

50

55

60

65

70

75

S&P 500 E.P.S.

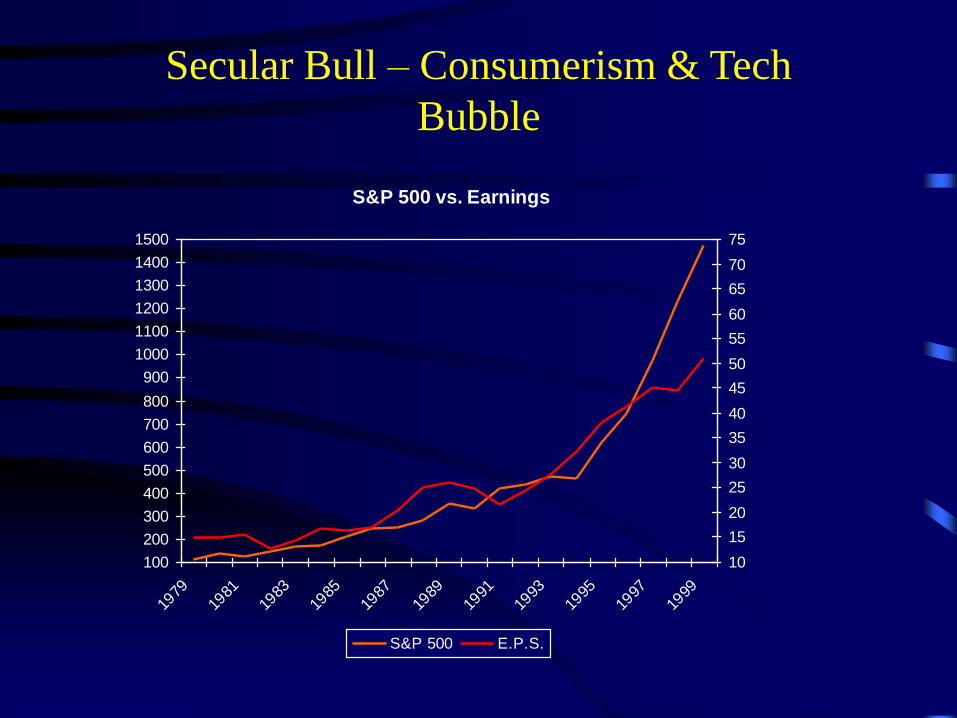

Secular Bull – Consumerism & Tech

Bubble

S&P 500 vs. Earnings

800.00

850.00

900.00

950.00

1,000.00

1,050.00

1,100.00

1,150.00

1,200.00

1,250.00

1,300.00

1,350.00

1,400.00

1,450.00

1,500.00

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

40

45

50

55

60

65

70

75

80

85

90

95

100

S&P 500 E.P.S.

Secular Bear – Bursting Bubbles &

Financial Crisis

S&P 500 vs. Earnings

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

2200

2009 2010 2011 2012 2013 2014

50

60

70

80

90

100

110

120

S&P 500 E.P.S.

Secular Bull – Monetary Easing and

Stimulus

Small and Mid-Cap Stocks Have Beaten Large-Caps Over the Long-Term

Growth of $1.00

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

$180.00

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

Large Cap 10.5% Mid-Cap 12.5% Small-Cap 11.8%

Source: RussellSmall-Caps Have Not Compensate For Higher Risk!

The Power of Compounding

1984-2014

$2,551,000

$3,709,000

$2,228,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

Future Value of $100,000

Large 11.4%

Mid 12.8%

Small 10.9%

Small % Increases = Big Dollars Over Time!Source: Russell

Smaller Companies Can Grow Faster

Smaller Base of Earnings

Greater Opportunity

for Market Share Gains

Emerging Industries

Industry Consolidators

Entrepreneurial Managements

The Main Difference Between Mid-Caps

and Small-Caps … RISK!

Standard Deviation (30 Year)

Mid-Cap 18.4%

Small-Cap 18.8%

Stock Liquidity (Avg. Daily Volume)

Mid-Cap 3,000K

Small-Cap 500K

Profitable Business Models

Russell Mid-Cap 11.5%

Russell Small-Cap 26.0%

Source: Russell, Thomson Financial, as of 2009

Large Industries Become Dominated by a Few

Quality Companies

• Automobiles

– Ford, General Motors, Volkswagon, Toyota

• Retail

– WalMart, Home Depot, Costco

• Computing

– Apple, Microsoft, Oracle, Cisco, Intel

Preference for standards and economies of scale lead to industry consolidation.

Active vs. Passive Management

• Active Management = Not an Index Fund•Active management can potentially beat the indexes.•Fees, style and taxes must also be considered.•Most Active Managers do not beat their indexes after fees and taxes.•Active management satisfies the desire to gamble.

• Passive Management = Index Funds•Index funds own all of a specific market segment.•Index funds deliver market rates of returns at low cost.•Index funds are generally highly tax efficient.•Index funds allow for diversification by size, style, country, etc.•Index funds beat most active mutual funds over the long-term.

Evaluating Active Managers

Performance should be measured net of fees and taxes relative to the proper style index.

• Style

– Large-cap vs. Large-cap. Mid-Cap vs. Mid-

Cap. Value vs. Value. Int’l vs. Int’l. etc.

• Net of fees and taxes

– You pay fees and taxes. What is left is your

real return.

• Data Sources for Index/Benchmark Results

– Russell.com, Morningstar, Yahoo Finance

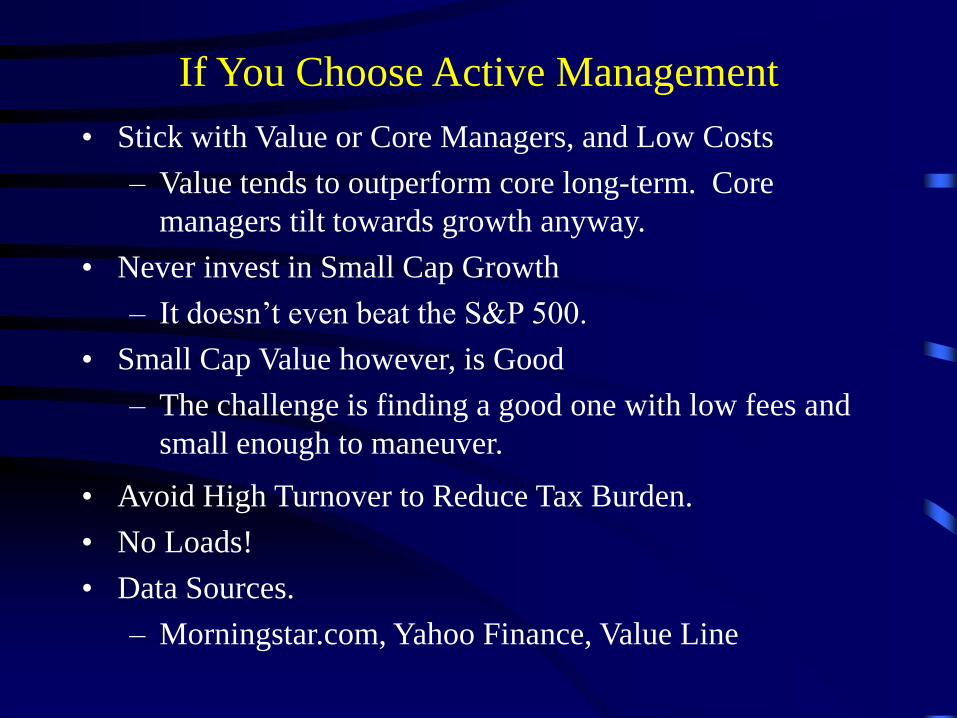

If You Choose Active Management

• Stick with Value or Core Managers, and Low Costs

– Value tends to outperform core long-term. Core

managers tilt towards growth anyway.

• Never invest in Small Cap Growth

– It doesn’t even beat the S&P 500.

• Small Cap Value however, is Good

– The challenge is finding a good one with low fees and

small enough to maneuver.

• Avoid High Turnover to Reduce Tax Burden.

• No Loads!

• Data Sources.

– Morningstar.com, Yahoo Finance, Value Line

Don’t Overdiversify!

• Benefits can be obtained with a handful of asset categories.

• Cash and Money Markets

– Most Conservative, lowest long-term return.

• Bonds/Fixed Income

– Provides interest income, preserves capital.

– Stick with intermediate investment grade (high quality).

– Use stocks for risk vs. high yield “junk bonds”.

• Equities/Stocks/Mutual Funds/Index Funds/ETF’s

– Higher risk, higher return. Returns through capital appreciation.

– Requires a long-term strategy.

• Int’l Stocks - It only takes a little.

– Important for the future as global economy develops.

– Stick with Index Funds or ETF’s.

29 Years Summary Results

Returns vs. Risk

100

Mix of Stocks/Bonds/Cash 100/0/0 0/100/0 0/0/100 90/0/10 80/15/5 70/25/5 60/35/5 50/45/5 40/55/5 30/65/5 20/75/5 10/85/5

Average Return 12.46% 7.55% 3.77% 11.58% 11.44% 11.05% 10.63% 10.16% 9.68% 9.14% 8.58% 7.99%

Std. Deviation 19.2 8.5 2.5 16.3 14.8 13.3 11.9 10.6 9.6 8.7 8.1 7.9

Return/risk 0.65 0.89 1.48 0.71 0.77 0.83 0.89 0.95 1.01 1.05 1.06 1.01

Worst 1 Year Return -42.6% -8.6% 0.1% -36.7% -31.9% -27.3% -22.7% -18.0% -13.4% -8.8% -5.9% -6.4%

Worst Absolute 3 Yr Return -23.1% 8.2% 0.4% -18.6% -13.7% -9.2% -5.0% -0.7% 3.3% 7.1% 10.8% 12.1%

$100,000 compounded over

29 years, in '000s 3,014$ 825$ 292$ 2,401$ 2,311$ 2,087$ 1,870$ 1,654$ 1,459$ 1,264$ 1,087$ 930$

Note: The stocks component of the allocation consists of 40% Largecap Blend (think S&P 500), 40% Midcap Value index and

20% Emerging Markets index. Stocks within the mixture are rebalanced annually, as are the total portfolios. Bonds are

represented by the Barclay’s Capital U.S. Aggregate bond index. Cash is represented using 90 day Treasury Bill returns. For

example the 30/65/5 column is 30% stocks (of the above indicated constituents), 65% bonds and 5% cash/T-bills.

Even Conservative Investor Should Own Some Equities

30% in Equities Had Higher Returns With Similar Risk Profile to Bonds Only

Key Variables to Retirement Planning

• Required annual income at retirement.

– Consider basic needs, healthcare, vacations, hobbies, taxes, etc.

• Income sources at retirement (Soc. Sec., consulting, etc.).

– Required savings at retirement = 20 to 25 times required pre-tax

income from savings.

• Years remaining to retirement.

• Current savings and continued annual savings.

• Required rate of return - determines required risk.

• Tools to help calculate:

– Quicken, Microsoft Money, Yahoo Finance

A Little Savings Goes a Long Way

• Assumptions:

– Starting Value = $10,000

– Annual Contribution = $5,000 (IRA Limit)

• Just over $400 per month.

– Annual Rate of Return = 8%

• Stock market returned 9.6% last century.

– Time Horizon = 25 years

• Future Value = $434,000

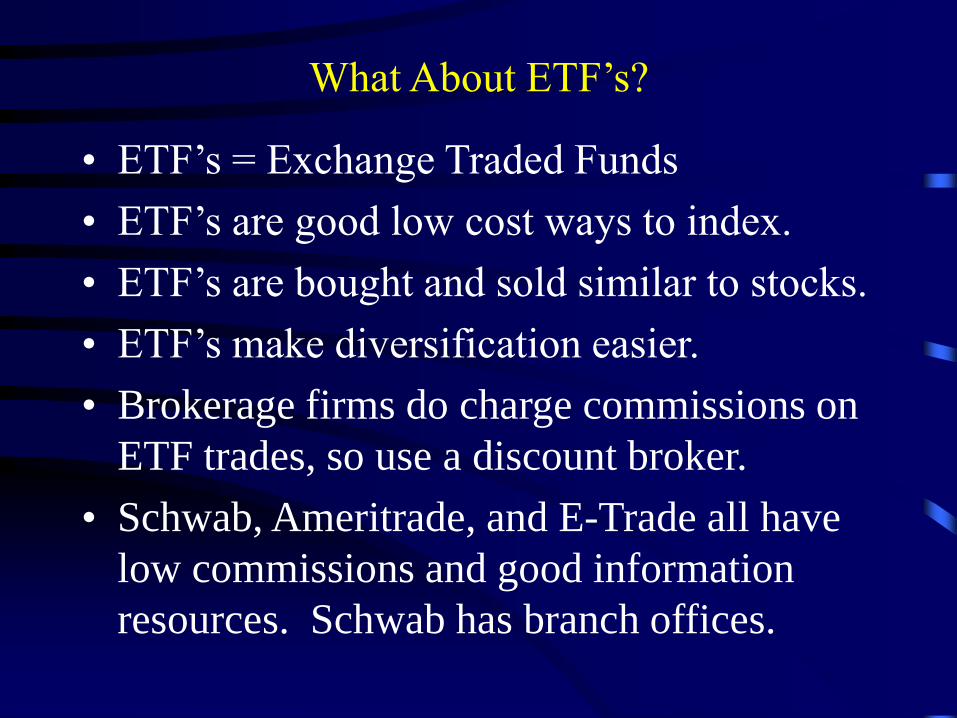

What About ETF’s?

• ETF’s = Exchange Traded Funds

• ETF’s are good low cost ways to index.

• ETF’s are bought and sold similar to stocks.

• ETF’s make diversification easier.

• Brokerage firms do charge commissions on

ETF trades, so use a discount broker.

• Schwab, Ameritrade, and E-Trade all have

low commissions and good information

resources. Schwab has branch offices.