final project mukesh g

TRANSCRIPT

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 1/62

K.J. SOMAIYA COLLEGE OF ARTS AND COMMERCE

VIDYAVIHAR, MUMBAI-400 077

PROJECT ON

“MOBILE BANKING’’

BANKING AND INSURANCE

SEMESTER- V (2011-2012)

SUBMITTED

In part fulfillment of the requirement for the Award of the degree of Bachelor of Commerce Banking and Insurance

BY:

MUKESH GUPTA

ROLL NO:16

1

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 2/62

K.J. SOMAIYA COLLEGE OF ARTS AND COMMERCEVidyavihar, Mumbai-400077.

CERTIFICATE

This is to certify that MR. MUKESH .B. GUPTA of B.COM BANKING

AND INSURANCE SEMESTER –V (2011-2012) has

successfully completed the project on MOBILE BANKING under the guidance of Dr. SMITA DAYAL

_______________ CO-ORDINATOR PRINCIPAL

(Dr. SMITA DAYAL) (Dr. Mrs. SUDHA VYAS)

INTERNAL EXAMINER EXTERNAL EXAMINER

PROJECT GUIDE(Dr. SMITA DAYAL)

2

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 3/62

DECLARATION:

I MUKESH GUPTA student of B.COM- BANKING AND

INSURANCE SEMESTER -V (2011-2012) hereby declare

that I have completed project on, MOBILE BANKING”.

Wherever the data/information have been taken from any book or other sourcesthe same have been mentioned in bibliography.

The information submitted is true and original to the best of my knowledge.

SIGNATURE OF STUDENT

MUKESH GUPTA(ROLLNO. 16)

3

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 4/62

ACKNOWLEDGEMENT

I have a great pleasure in presenting our project on MOBILE BANKING.

I sincerely thank with deep sense of gratitude to Dr. SMITA DAYAL, our guide

for her kind co-operation for the fulfillment of the project.

I am highly indebted to our Principal Dr. Mrs. SUDHA VYAS & our Vice

Principal Dr. MAYURESH MULE who took keen interest and allowed us to

perform this project.

I would also like to thank our seniors, librarians who sincerely helped me getting this

information and, last not the least our college for a big reason that we are here in frontof you presenting this project.SIGNATURE OF STUDENT,

MUKESH GUPTA

(ROLLNO: 16)

4

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 5/62

INDEX

SR NO CONTENT PAGE NO

1. INTRODUCTION TO BANKING

i) MEANING

ii) DEFINITION

iii) HISTORY

iv) CURRENT SITUATION OF BANKING IN

INDIA

6-7

8

9

10

11

2. INTRODUCTION OF MOBILE BANKING.

i) OBJECTIVES

ii) FEATURES

12-13

14

15

3. CONSIDERATION WHEN IMPLEMENTING

MOBILE BANKING

16

4. MARKETING FOR MOBILE BANKING 17

5. GUIDELINES AND CONSIDERATION BANKS.

i) REGISTRATION OF MOBILE BANKING

ii) SECURITY ISSUE

18

20

21-22

6. SERVICES 23-25

7. ADVANTAGES OF MOBILE BANKING 26-28

8. LIST OF BANK PROVIDING MOBILE BANKING 29

9. HOW WE CAN USE THE MOBILE BANKING 30-31

10. VARIOUS METHOD OF USING MOBILE

BANKING

32-38

11. QUESTION AND ANSWER OF THE FOLLOWING 39-45

12. TERMS AND CONDITION GOVERNING MOBILE

BANKING FACILITY

46-59

13. RELIANCE INFOCOM , INDIA 60

5

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 6/62

14. RECOMMENDATION 61

15. BIBLIOGRAPHY 62

1. BANKING

Banking has become a part and parcel of our day-to-day life. Today, banks offer an

easy access to a common man. They carry out variety of functions apart from their main

functions of accepting deposits and lending. Banking is a service industry. Banks provide

financial services to the people, business and industries. Merchant banking, money transfer,

credit cards, ATMs are some of the important financial services provided by the modern

banks.

Without a sound and effective banking system in India it cannot have a healthy

economy. The banking system of India should not only be hassle free but it should be able to

meet new challenges posed by the technology and any other external and internal factors.

For the past three decades India's banking system has several outstanding

achievements to its credit. The most striking is its extensive reach. It is no longer confined to

only metropolitans or cosmopolitans in India. In fact, Indian banking system has reached

even to the remote corners of the country. This is one of the main reasons of India's growth

process.

Not long ago, an account holder had to wait for hours at the bank counters for getting

a draft or for withdrawing his own money. Today, he has a choice. Gone are days when the

most efficient bank transferred money from one branch to other in two days. Now it is simple

as instant messaging or dials a pizza. Money has become the order of the day.

6

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 7/62

The name Bank derives from the Italian word Banco "desk/bench", used during the

Renaissance by Florentines bankers, who used to make their transactions above a desk

covered by a green tablecloth. However, there are traces of banking activity even in ancient

times.

In fact, the word traces its origins back to the Ancient Roman Empire, where

moneylenders would set up their stalls in the middle of enclosed courtyards called macella on

a long bench called a banco, from which the words banco and bank are derived. As a

moneychanger, the merchant at the banco did not so much invest money as merely convert

the foreign currency into the only legal tender in Rome- that of the Imperial Mint.

7

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 8/62

MEANING OF BANKING

A Bank is a financial institution which accepts deposits from the public and lends the

funds to the people or institution that need funds. It is like reservoir. It collects the savings of

some people and gives this money to others who use them productively. In the process, the

bank earns interest out of which it pays interest to the depositors.

8

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 9/62

DEFINITION OF BANKING

In India “BANKING” has been defined by a statute, viz., the Banking Regulation Act,

1949 (vide Section 5 b, c) as follows:

“Accepting, for the purpose of lending or investment, of deposits of money from

the public, repayable on demand or otherwise, and withdrawal by cheque, draft, and

order or otherwise” (section 5 b)

A banking company is “a company which transacts the business of banking in

India” (section 5 c)

9

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 10/62

HISTORY OF BANKING

Banking in India originated in the first decade of 18th century. The first banks were

The General Bank of India, which started in 1786, and Bank of Hindustan, both of which are

now defunct. The oldest bank in existence in India is the State Bank of India, which

originated in the "The Bank of Bengal" in Calcutta in June 1806. This was one of the three

presidency banks, the other two being the Bank of Bombay and the Bank of Madras. The

presidency banks were established under charters from the British East India Company. They

merged in 1925 to form the Imperial Bank of India, which, upon India's independence,

became the State Bank of India. For many years the Presidency banks acted as quasi-central

banks, as did their successors. The Reserve Bank of India formally took on the responsibility

of regulating the Indian banking sector from 1935. After India's independence in 1947, the

Reserve Bank was nationalized and given broader powers.

10

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 11/62

CURRENT SITUATION OF BANKING IN INDIA

Currently (2008), banking in India is generally fairly mature in terms of supply, product range and reach-even though reach in rural India still remains a challenge for the

private sector and foreign banks. In terms of quality of assets and capital adequacy, Indian

banks are considered to have clean, strong and transparent balance sheets relative to other

banks in comparable economies in its region. The Reserve Bank of India is an autonomous

body, with minimal pressure from the government. The stated policy of the Bank on the

Indian Rupee is to manage volatility but without any fixed exchange rate-and this has mostly

been true.

With the growth in the Indian economy expected to be strong for quite some time-

especially in its services sector-the demand for banking services, especially retail banking,

mortgages and investment services are expected to be strong. One may also expect M&As,

takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its

stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first time an

investor has been allowed to hold more than 5% in a private sector bank since the RBI

announced norms in 2005 that any stake exceeding 5% in the private sector banks would

need to be vetted by them.

Currently, India has 88 scheduled commercial banks (SCBs) - 28 public sector banks

(that is with the Government of India holding a stake), 29 private banks (these do not have

government stake; they may be publicly listed and traded on stock exchanges) and 31 foreign

banks. They have a combined network of over 53,000 branches and 17,000 ATMs.

11

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 12/62

2. MOBILE BANKING

INTRODUCTION

The kind of banking and financial service that gives a real-time mobile access to

customer on the move is called mobile banking the services being offered through mobile

phone.

Mobile banking to the banking activity that are carried out on mobile (cell) phones

that is banking is enabled even while a person is on the move

In modern times, information exchange takes place at great speed. The dependence of

people on computing devices such as computers, cellular phone, pager, facsimile machine, e-

mail and internet is growing at galloping rate. Such as growth has made the real time

exchange of information a reality. At the same time it has also thrown challenges to modern

enterprises. Which prompt them to act in a proactive manner so as to stay competitive in the

business world. The constant innovation happening in the realm of electronic banking and

financial services has contributed to a new development called ‘mobile banking’ this may be

attributed to the forth coming demand from the mobile workforce. The increasingly growing

number of mobile workforce has really given a cutting edge to the progress of the electronic

banking.

The mobile banking refers to the facility allowed by certain banks in India whereby

the mobile phone holder can undertake certain banking transaction through their mobile

phones. This value added services has very little human interface and private banks like

ICICI, HDFC etc. have started offering this service. The customer is required to type a text

message on the mobile phone which travel through the server of the cell phone service provider to bank’s internet service; information is retrieved and routed back the same way in

15-30 second. To avail the service, the client has to fill up form at any of bank’s branches and

bank informs the cellular service provider to activate the module instantly.

The information which includes checking of account balance, request for a Cheque

book, stop payment instruction, changing primary operation account, request for current

periods’ account statement to the mailed and access summaries of last three transactions

performed on the account.

12

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 13/62

The number of people using mobile banking services has increased. While the trend is

growing, lack of awareness of services, apart from perceived security issues are inhibiting

faster takeoff. “Data Quest”.

It was clear at the start itself that this would be a battle focused not on technology, but

on the mindset of the target audience. Over two years after the launch of mobile banking

services in the country, that bridge has been reached and many are beginning to walk those

cautious steps across it. Yes, the usage of mobile banking services is increasing, and fast

against data quest’s estimated user base of under 10,000 for mobile banking services in 2000,

there are over 120,000 today who SMS from their banking. Even our survey despite targeting

a respondent profile that would bring in more positive answers than negative (see

methodology), threw up very low usage numbers. Also, e-commerce as a medium of

purchasing and transacting has not really caught on, and the basket of mobile banking

offerings is, in itself, very limited. The good news the technology backbone is in place, and

getting better. There’s CDMA, there’s GSM. Forget their battles on the mobile telephony

front from the consumer’s point of view; he never had it so good.

The recent price cuts are also likely to help, “say banking experts, adding that this will

lead to “increasing willingness to move on to mobile, and therefore, to the value-added

services that most operators offer today”

The Internet is revolutionizing the way the financial industry conducts business,

empowering organization with new business model and new ways to interact with customers.

The ability to perform banking transactions online banks and brokers who offer personalized

services through their web portals. This increased competition is driving traditional financial

institutions to find new ways to add value to their product and services, gain competitive

advantage and increase customer loyalty while also attracting new, high-value client.

13

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 14/62

OBJECTIVES

Mobile and wireless technology, combined with the wide variety of portable devices

available today, enable new revenue opportunities for financial services organizations. This

provides a new channel that can be used to refresh and expand the customer base, attract

prime customers and enhance loyalty. With mobile and wireless technology, banks can offer

a wide possibility of services to their customers, from the freedom of paying bills while stuck

in traffic, to receiving notification of a change in stock price while having lunch, the

challenge, then is how to turn these possibilities into a reality for the customers.

Table

BENEFITS DESCRIPTION

Grow new customer base and

markets

Developing wireless application and services targeted at the

mobile mass market will allow attracting new, high-value

customers into mobile banking portal and expanding the reach

to global markets.

Increase share of customer

wallet

The convenience of having personalized wireless access to

critical financial information is an invaluable service for

customers on the move enabling the execution of time-sensitive

financial transaction anywhere, anytime, provides the

opportunity to strengthen the relationships with existing

customers. This ultimately results in an increased share of the

customers’ transactions preventing them from taking a portion

of their financial business elsewhere.

Grow assets, number of

transaction and fees.

Granting customer flexible access to financial information and

accounts enables them to perform transaction and accounts

enable them to perform transaction when it’s most convenient

for them. As a result, they have the opportunity to conduct

transactions more frequently, driving increased revenue from

fees.

14

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 15/62

FEATURES

Mobile Customers: - those who use ‘mobile telephony’ use mobile banking

service. Mobile telephony is used through mobile phones.

M – Commerce: - mobile banking is a part of m – Commerce whereby business

and trade takes place through mobile on-line. Those mobile users who became on line

internet users do M – Commerce.

Technology based: - Mobile banking are based on technology of development.

Mobile banking makes use of internet for transmission, transaction & delivery of bankingservices. The network provide the required software support.

Services: -Mobile banking offers the entire internet-based banking services such

as on-line account opening, account verification, funds transfer etc.

Eligibility: - At present, mobile banking is extended only to individual customer

having account with any branch of a particular bank that offers internet banking facility.Further, it is also required that the customer is registered as on internet banking customer.

Application: - In order to avail the facility of mobile banking, an application duly

filled is to be submitted to the bank. The application is invariably made available in the

official website of the bank.

15

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 16/62

3. CONSIDERATION WHEN IMPLEMENTING

MOBILE BANKING

The creation of mobile services is more efficient and effective when financial

institution enters in alliance with mobile operators. The appropriate choice for each player

depends on their combined customer base and the share of market each one brings to the

alliance.

The choices are then if one bank should establish alliance with one or many mobile

operator. The theories on the evolution of these types of alliances show that the most usal

beginning is from one to one. However, the dominant strategy will converge in the long term

to a many to many alliance model.

For large bank the most convenient strategy is to begin with a closed system; an

alliance with one telecommunication company and initially closed to user outside the

combined customer base. This will allow the alliance to lock in big customers before other

players begin to enter the market. At least one or two condition is needed to maintain the

closed system working: a critical mass of customers, or strategic adventure in the operating

area.Banks with not so large customer base or that do not want to risk being the first

movers in a closed system, would prefer to implement open system alliance and try to capture

a larger market share.

The decision about the most appropriate alliance to chose will depend on the

particular of the bank implementing the mobile services and the availability of appropriate

partners for telecommunication operation.

In the same way when choosing wireless platform the critical consideration are theconnectivity with the back –end system and the market several solutions in a short period of

time. There are currently in the market several solution based upon different technology and

budget requirements.

16

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 17/62

4. MARKETING FOR MOBILE BANKING

Mobile Banking is poised to become the big killer mobile application arena.However, banks going mobile the first time need to trend the path cautiously. The Biggest

decision that banks need to make is the channel that they will support their services on.

Mobile Banking through an SMS based service would require the lowest amount of

effort, in terms of cost and time, but will not be able to support the full breath of transaction

based services. However in market like India, where a bulk of the mobile population user’s

phones can only support SMS based services, this might be the only option left.

On the other hand a market heavily segmented by the type and complexity of mobile

phone using might be good place to roll of WAP based mobile applications. WAP based

services can let go of the need to customized usability to the profile of each mobile phone.

The trade off being that it cannot take advantage of the full breadth of features that a mobile

phone might offer.

Mobile application standalone clients bring-along the burden of supporting multiple

mobile device profile. According to the Gartner group, a leading wireless computing

consulting organization, mobile banking services will have to support a minimum of 50

different device profiles in the near future. However, currently the best user experience,

depending on the capabilities of a mobile phone, is possible only by using a standalone client.

Mobile banking has the potential to do the mobile phone, what E-Mail did to the internet

mobile application based banking is poised to be a big M-Commerce features, and if south

Korea’s foray into mass mobile banking is any indication, mobile banking could well be the

driving factor to increase sales of high and Mobile phone nevertheless bank’s need to take a

hard and deep look into the mobile usage patterns among their target customers and enables

their mobile service on a technology with reaches out the majority of their customer.

17

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 18/62

5. GUIDELINES AND CONSIDERATION BANKS

Some guidelines and consideration banks need to follow implementing wireless

banking are:

Application servers should be easy to install, configure and add new services.

Client application must be easy to install, customized, and add new handheld

devices.

Integration with other servers and back end services must be easy to implement.

The advantages of using standard protocol are attainable mainly through open

system.

For smaller financial institution, like credit unions, the outsourcing of the wireless

services can solve most of the impediments they would face. Besides the lack of resources

and expertise, other reasons for outsourcing are:

Financial institution will not divert from it core business.

Improve the time to implement the services.

Cost and budget can be predicated with more accuracy.

Wireless services will use the latest in technology.

18

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 19/62

Using mobile banking facility you can:

Check your balance

Check on your last three transaction

Request for a statement

Request for a cheque book

Enquire on a cheque status

Instruct stop cheque payment.

View fixed deposit detail...And much more.

You can also pay your utility bills using the bill pay facility all you to do is instruct us

to pay your bills and the amount rates instantly deducted online from our account.

19

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 20/62

R EGISTRATION OF MOBILE BANKING

It is usually required that the customer who register for internet banking also register

for mobile banking. To register, you have to provide mobile number in the subscription page

of mobile banking requests. Provide your number in the format country code number. To

register and use the mobile banking service it is incumbent that the following requirements

are:-

Essential Requirement

Service is available only to an existing customer of the branch availing

internet banking services.

Registration for internet banking and mobile banking services.

Available for the individual customer.

Need for owning a mobile phone; if “WAP (wireless application protocol).

Banking is to be availed; the mobile phone should be WAP enabled whose browser is capable

of sending referrer URL.

20

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 21/62

SECURITY ISSUE

The security for the use of mobile banking is ensured by the use of “password”.Password is nothing but the secret code of identification of a uses. The customer user is given

a “login ID” and a “password” on the registration for internet banking. The login ID and the

password need to be changed by the internet banking registration.

In the case of WAP banking, one should use the same user login ID and transaction

password with which access to the internet banking service is made. However, your user ID

needs to be enabled by the bank for WAP banking on the basis of the application submitted

for the same. This is essential for availing the WAP banking. In the case of SMS Banking, the

bank will first enable the user ID for SMS facility on the basis of the

Application for the same. Only then the customer can access the domain of the

banking company.

Accessing SMS banking through internet login password is not allowed. A customer

can access SMS banking only through SMS password. Which is exclusive however, with

internet login password, one can access the domain of the banking company through internet

banking or WAP banking using the WAP enable mobile phone.

For the first time, one can choose the SMS password only in the relevant domain of

the bank by accessing through internet. Subsequently SMS password can be changed through

an SMS on the mobile phone also. However; it is not possible to change the WAP Password

separately. Change of WAP password happens automatically with the change in internet

login password.

Registration is required for mobile banking when the cell. Number is changed from

the one already registered. Before the change of the cell number, it is possible for the

customer to withdraw from SMS Banking, using the necessary option. The customer need to

take up with the bank, after getting the new cell number, duly informing the internet banking

ID and the new cell number. Bank will accordingly register the new cell number.

Currently, there is not a security standard; companies have implemented many

solutions even thought the trend is to use smart cards as the utmost security technology. The

solutions currently implemented are the following:

21

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 22/62

Limit in the type of transaction in order to reduce the risk of the cardholder.

For example, funds transfer to third parties.

Secure network architecture. The more common security used is PKI (public

key infrastructure) an encryption used for PDA’s and smart phones, PKI consist of two keys,

a public key and a private key, used to authenticated the user and encrypt the data.

Smart cards as a digital identification and mobile phone (card reader are the

highest technology in the terms of security).

22

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 23/62

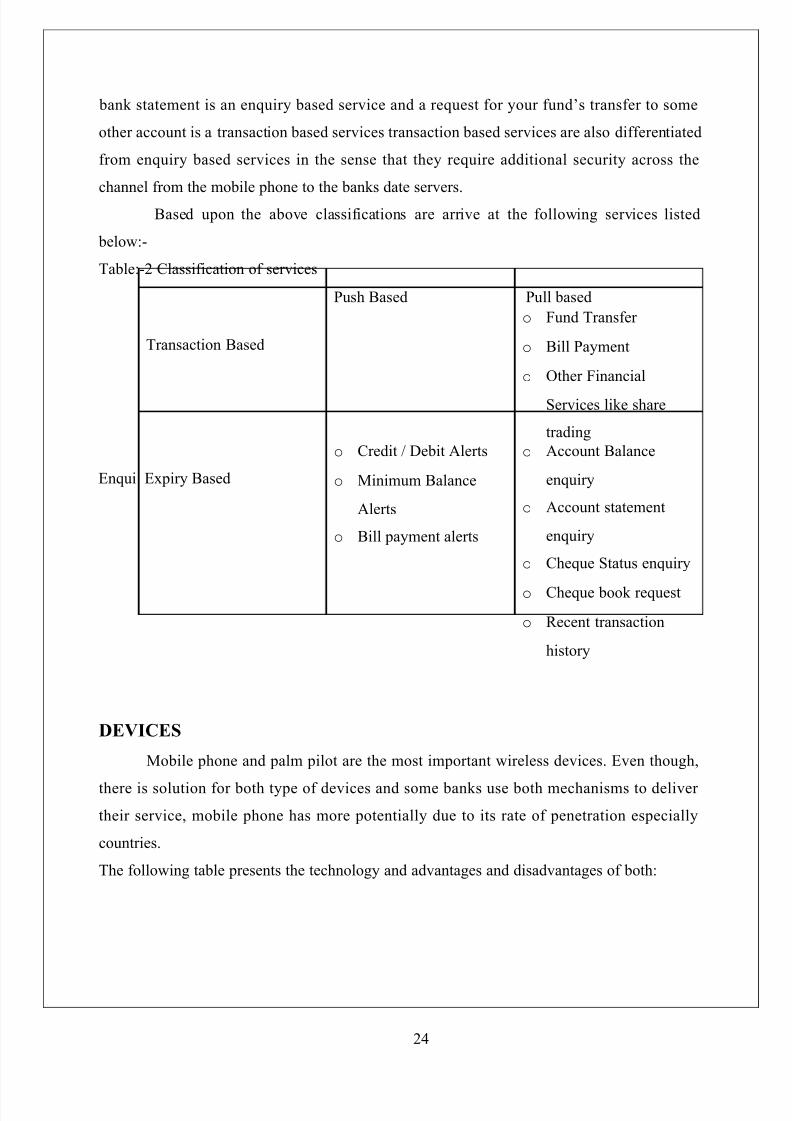

6. SERVICES

The services that mobile banking can offer are the following:

Account balance enquiry.

Account statement enquiry.

Cheque status enquiry.

Cheque book requests.

Fund transfer between accounts.

Credit/debit alert.

Minimum balance alerts.

Bill payment alerts.

Recent transaction history request.

Information request like internet rates exchange rates.

One way to classify this service depending on the originator of a service session is the

push/pull nature. ‘Push’ is when the bank sends out information based upon an agreed set of

rules, for example your banks send out an alert when your account balance goes below a

thousand level.” pull” when the customer explicitly request a service or information from the

bank so a request for your last five transaction statement is a pull based offering.

The other way to categorize the mobile banking services by the nature of the service,

gives us two kind of services:- Transaction based on enquiry based so a request for your

23

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 24/62

bank statement is an enquiry based service and a request for your fund’s transfer to some

other account is a transaction based services transaction based services are also differentiated

from enquiry based services in the sense that they require additional security across the

channel from the mobile phone to the banks date servers.

Based upon the above classifications are arrive at the following services listed

below:-

Table:-2 Classification of services

Push Based Pull based

Transaction Based

o Fund Transfer

o Bill Payment

o Other Financial

Services like share

trading

Enqui Expiry Based

o Credit / Debit Alerts

o Minimum Balance

Alerts

o Bill payment alerts

o Account Balance

enquiry

o Account statement

enquiry

o Cheque Status enquiry

o Cheque book request

o Recent transaction

history

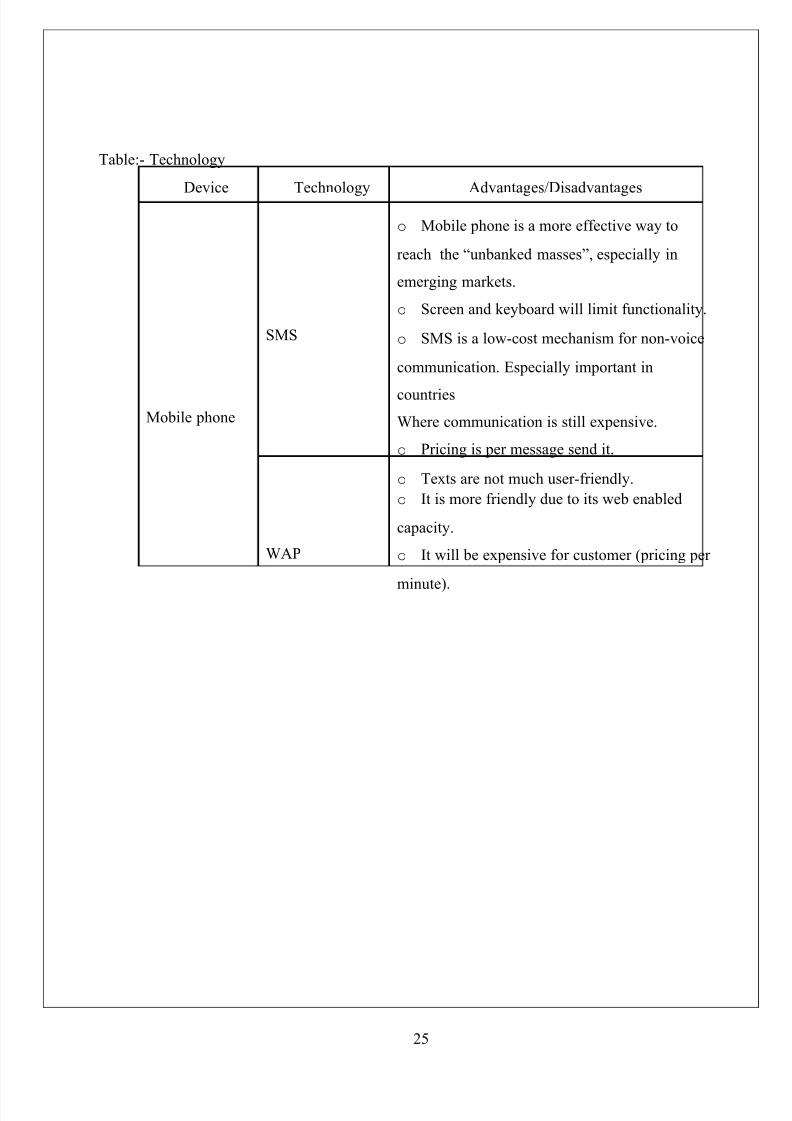

DEVICES

Mobile phone and palm pilot are the most important wireless devices. Even though,

there is solution for both type of devices and some banks use both mechanisms to deliver

their service, mobile phone has more potentially due to its rate of penetration especially

countries.

The following table presents the technology and advantages and disadvantages of both:

24

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 25/62

Table:- Technology

Device Technology Advantages/Disadvantages

Mobile phone

SMS

o Mobile phone is a more effective way to

reach the “unbanked masses”, especially in

emerging markets.

o Screen and keyboard will limit functionality.

o SMS is a low-cost mechanism for non-voice

communication. Especially important in

countries

Where communication is still expensive.

o Pricing is per message send it.

o Texts are not much user-friendly.

WAP

o It is more friendly due to its web enabled

capacity.

o It will be expensive for customer (pricing per

minute).

25

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 26/62

7. ADVANTAGES OF MOBILE BANKING

The biggest advantages that mobile banking after to banks is that it drastically cut

down the costs of providing services to the customers. For example an average teller or phone

transaction costs about $2.36 each whereas an electronic transaction costs only about $0.10

each additionally this new channel gives the bank ability to cross-sell, up-sell their other

complex banking products and services such as vehicle loans, credit each etc.

For service providers, mobile banking offers the next surest way to achieve growth.

Countries like Korea where mobile penetration is nearing saturation mobile banking is

helping services provider increase revenue from the now static sub- scriber base. Also service

provider are increasingly using the complexity of their supported mobile banking services to

attract new customer and retain old ones

Control your finances, wherever you are in your wireless carrier’s digital coverage area.

Real-time access through a secure connection.

Private and convenient- no need to visit branch, or be near a personal

computer telephone.

Transfer money while on the move.

Pay your bills at your convenience.

Check your balance before making a purchase.

Do your banking in a secure, discreet and convenient environment.

Easy to use software and interface, with full customer support.

To protect your privacy, the information transmitted between your palm handheld

and royal bank is encrypted.

Access your banking information using your own secret password.

Your privacy and security is priority

26

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 27/62

Mobile banking with palm handhelds is safe, reliable and secure. All data between the

palm device and royal bank is encrypted, meaning that it is scrambled into an unreadable

format during transmission, preventing the risk of the data being intercepted by a third party.

This is the same state of the art technology used in online banking.

No one can view your information; in fact, no data is ever permanently stored on your

palm device, so if you lend it, no one will be able to “find” any of your personal information.

These features also help ensure the security of mobile banking with palm handhelds:

If for some reason your palm handheld shuts itself off with your banking

information displayed, the application will reset to the sign-on screen.

Online banking will time-out if there is no activity from the palm handheld. You

will then need to sign on again with your password.

You can lock your palm handheld, so that only your own secret password can be

used to “unlock” it every time it is used.

27

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 28/62

HOW TO USE THE SERVICS

For Example: - RELIANCE MOBILE

Step 1 Go to R World

Step 2 Go to ‘More Services’ Option

Step 3 Select ‘Finance’ option

Step 4 Select ‘mobile bank’ option

Step 5 select ‘ICICI BANK’ Option

Step 6 Accept Disclaimer

28

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 29/62

8. LIST OF BANK PROVIDING MOBILE BANKING

ICICI BANK

HDFC BANK

PUNJAB NATIONAL BANK

BANK OF BARODA

UNIT TRUST OF INDIA

DENA BANK

KOTAK MAHINDRA BANK

DEVELOPMENT CREDIT BANK

STATE BANK OF INDIA

HSBC BANK

YES BANK

29

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 30/62

9. HOW WE CAN USE MOBILE BANKING

How mobile banking works for you?

Mobile banking works through a set of text messages. All you need to do is to type in the

specified code for the transaction as a text message and send it to a pre – designated number.

You will receive the response in the form of a text message on your mobile phone screen

within a few seconds.

Who can apply this mobile banking?

If you are an account holder of any bank as well as a subscriber of any of the mobile phone

service providers tied up with HDFC Bank, you can take advantage of this facility.

One document is all it takes to apply!

If you are opening an account with the bank, you can apply for mobile banking through the

account opening document. If you already have an account with the bank, you can apply for

mobile banking through the combined direct banking channels application form.

What transaction can I do through mobile banking?

Mobile banking is extremely easy. Just punch in a few letter and routine banking transactions

will be complete.

How does mobile banking works?

Mobile banking works through a series of text message (SMS)

30

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 31/62

Once you have activated this service, all you need to do is type in the

specified code for the service you want to avail.

You will receive the response in the form of text message on your mobile phone screen within a few seconds.

Does mobile banking with palm work everywhere?

It will work in major urban center and surrounding areas. For specific areas of

coverage, please consult your wireless carrier. Most wireless carriers publish maps of their

areas on their web sites.

31

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 32/62

10. VARIOUS METHOD OF USING MOBILE BANKING

ICICI BANK Mobile banking can be divided into two broad categories:

Request Facility

Alert Facility

REQUEST FACILITY:

ICICI BANK mobile banking requests enable to query for account information or

perform bank transactions. You can query for your account balance, request for the last 3

transactions. Order for new cheque book, inquire for a cheque status, issue a stop cheque

request, change of primary account and make payment for your bill under this facility.

If you hold an ICICI BANK HPCL Debit Card, you can also query your debit card reward

points by just sending a SMS request.

ALERT FACILITY:

Under ICICI BANK mobile banking alert, you get alerted when the events you have

subscribed for get triggered. You can subscribed for receiving SMS alert when your salary

gets credited, when your bank account is debited / credited with Rs.5000/- or more as

specified by you, your balance falls below / goes above a specified limit or when a cheque

bounces.

Under the alert facility, you will get alert only when the events you have subscribed

for information as and when you desire.

CREDIT CARD SERVICES

ICICI BANK mobile banking services for credit card can be divided into two board

categories:

REQUEST FACILITY

32

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 33/62

ALERT FACILITY

The request facility enables you to check your credit card balance, fetch reward points

for redemption, view details of last payment, and get payment due date.

On subscription to credit card alerts, you get alerted when the events you have

subscribed for get triggered. You can subscribe for receiving SMS alerts for due date

reminders, and when you are approaching your credit limit.

Under the alert facility, you will get alerts only when the events you have subscribed for gets

triggered unlike the request facility where you can request for information as and when

desired.

33

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 34/62

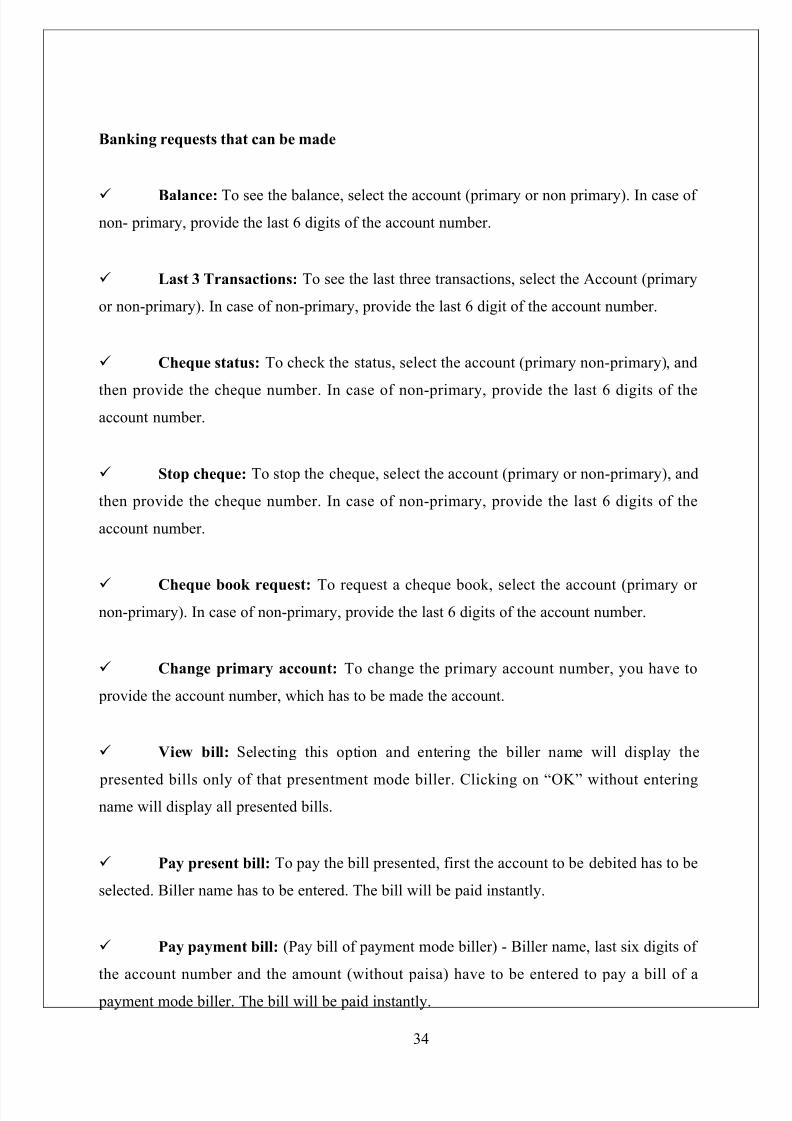

Banking requests that can be made

Balance: To see the balance, select the account (primary or non primary). In case of

non- primary, provide the last 6 digits of the account number.

Last 3 Transactions: To see the last three transactions, select the Account (primary

or non-primary). In case of non-primary, provide the last 6 digit of the account number.

Cheque status: To check the status, select the account (primary non-primary), and

then provide the cheque number. In case of non-primary, provide the last 6 digits of theaccount number.

Stop cheque: To stop the cheque, select the account (primary or non-primary), and

then provide the cheque number. In case of non-primary, provide the last 6 digits of the

account number.

Cheque book request: To request a cheque book, select the account (primary or non-primary). In case of non-primary, provide the last 6 digits of the account number.

Change primary account: To change the primary account number, you have to

provide the account number, which has to be made the account.

View bill: Selecting this option and entering the biller name will display the

presented bills only of that presentment mode biller. Clicking on “OK” without enteringname will display all presented bills.

Pay present bill: To pay the bill presented, first the account to be debited has to be

selected. Biller name has to be entered. The bill will be paid instantly.

Pay payment bill: (Pay bill of payment mode biller) - Biller name, last six digits of

the account number and the amount (without paisa) have to be entered to pay a bill of a payment mode biller. The bill will be paid instantly.

34

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 35/62

Find ATM / Find branch: Pin code of the desired area has to be entered to get the

nearest ATM / Branch. for eg :- if you wish to find an ICICI Bank ATM in Andheri,

Mumbai, you would have to select Find ATM& enter the pin code of Andheri.(E) 400058

Get quote: You have to provide the ICICI direct stock code to get the details. (This

facility is available to customer who has registered for this facility with ICICI direct.)

About : This option gives you the basic information about the service as under

To register contact ICICI Bank or visit www.icicibank.com

To make query select option from the menu and click “request”.ICICI BANK Partners with reliance India mobile to launch mobile banking service

ICICI Bank, India’s second largest bank, in association with reliance info com,

India’s largest mobile service provider, today launched a truly interactive mobile banking

service in India.

July 14, 2004, Mumbai – ICICI Bank customers through their reliance mobile

handsets can now avail of a gamut of banking services free of charge. The services can be

accessed directly from R World on the handset. A customer can view their ICICI Bank

account balance, get mini statement and make requests for cheque books. Apart from viewing

presented bills, a customer can also pay bills by direct debit to the bank account. The service

also enables a customer to locate an ATM or bank branch. On selecting any of these, the

customer is connected directly to the bank and the result is displayed instantly on the handset.

To avail the mobile banking service, a customer can register at any of the ICICI Bank

branches, dial the call center or through internet banking.

“With alliance” ICICI Bank leveraged technology to synergies the benefits of a

mobile phone with ICICI Banking services. This will improved the customer with a

convenient anytime-anywhere banking environment R-World’s menu driven process offers

the convenience of banking, while being on the move. The highly advanced and intuitive

user- interface features of the R-World, available to the more than 7 million RIM users,

35

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 36/62

makes mobile banking practical and user-friendly. R-World ensures the subscriber receives

answer to request immediately within the same session.

The java-based R-World suite of reliance India mobile internet application unique in

India and the world. Around 7 million subscribers all over India currently use R-World.,

which offers a range of innovation services on reliance India mobile that helps its customer to

access information, communication, entertainment, and transaction based application on the

move.

36

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 37/62

Indian mobile provider partners with bank to offer services

INDIA – Are mobile phones a competitor – or a complement – to ATMs?Maybe a little both, judging from a news release from mobile phone provider reliance info

com limited. According to the release, ICICI Bank, in a partnership with reliance, on July 21

launched an interactive mobile banking service in India.

Using their reliance India mobile handsets, ICICI Bank customers can access several banking

services; including viewing their account balance, getting mini statements and making

request for check books. Customers can also view presented bills and make payments via a

direct debit to their bank accounts. There is no charge for the services.

However, the service also enables a customer to locate an ATM or bank branch. With

this option, the customer is connected directly to the bank and the result is displayed instantly

on the handset.

However, the service also enables a customer to locate an ATM or bank branch. With

this option, the customer is connected directly to the bank and the result is displayed instantly

on the handset. Customer can sign up for the service at any ICICI Bank branch, or through

the call center or the internet.

“With this alliance, we have leveraged technology to synergize the benefits of a

mobile phone with our banking services, which will provide the customer with a convenient

anytime – anywhere banking environment.

Reliance India mobile’s internet applications, including the new ICICI services, are

built upon proprietary java – based R-world suite. According to the release, 7 million

subscribers across India use R-world to access information, communication, entertainment

and transaction – based application.

37

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 38/62

COMPARING WITH OTHER BANK FOR MOBILE BANKING

Actually, I am doing project on mobile banking from ICICI BANK. This bank had

started mobile banking in the year 2001. From 2001 to 2007 this bank started making profit

continuously.

I want to compare the ICICI BANK with other leading bank for example: - HDFC,

HSBC etc. HDFC was the first bank to start a mobile banking in India for example: - RIM

has included ICICI BANK along with HDFC bank for mobile banking through R- WORLD.

Since I have an HDFC BANK a/c, I registered for this service with HDFC BANK and cancheck my account details and carry out select transaction using R-WORLD. However, much

to my surprise there seems to be no password/PIN security for accessing to my bank account!

That means whoever has even brief access to my mobile has access to my bank account! So if

it ever stolen. Or even in cases to the account and could even carry out transaction!!!

It’s really surprising that they have overlooked this very important security loophole!

Is this the same for people who have registered with ICICI?

Anybody concerned about this?

38

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 39/62

11. QUESTION & ANSWER OF THE FOLLOWING

What is ICICI mobile banking? Why should I apply for same?

» ICICI mobile banking keeps you informed about the significant transactions in your

bank, credit card and demat accounts promptly such as:

Bank Alerts – salary credit, debit / credit of large amounts as specified by you and cheque

bounce.

Credit Card Alerts – Approaching credit limit and due date of payment of credit card bill.

Demat Alerts – shares debited and credited in your account etc.

ICICI Bank mobile banking facility keeps you updated while you are on the move.

What are ICICI mobile banking alerts?

» ICICI bank mobile banking alerts is a facility through which you can receive latest

information about your bank. Credit Card and Accounts.

Alerts are sent to your mobile phone number as registered by you with the bank.

Can I avail of the ICICI mobile banking facility?

» All ICICI Bank customers having savings bank account, credit card (not being an add

on card) and demat account can avail of this facility. As and when alerts are introduced for

other ICICI Bank products, we shall intimate you through our website.

What are the alerts that I can subscribe for?

39

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 40/62

» Currently, we are providing the following alerts based on your account(s) with us:

Banking Alerts

1. Credit to your bank account of any amount of rs.5000/- or above as specified by you.

2. Debit to your bank account of any amount of rs.5000/- or above as specified by you.3. Salary credit to the bank account.

4. Cheque deposited in your bank account but bounced.

5. Account balance below a specified amount.

This will be subject to the appearance of the word ‘salary’ in the narration of salary credit.

Credit Card Alerts

1. Payment due date reminder on your next credit card bill.

2. Your credit card spending reaches the limited set for your credit

card (approaching credit limit).

Demat Alerts

1. Demat account getting credited.

2. Demat account getting debited.

3. Pledge creation and closure.

4. Rejection of instruction submitted.

In future, we would be introducing more alerts, for which we shall intimate you through our

website,

How often will I receive the alerts?

» Depending on the type of alerts selected, you will receive the alert(s)

As and when the particular event happens. However, in case of approaching credit limit, the

alert is sent at the end of the day.

40

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 41/62

How can I subscribe to ICICI bank mobile banking?

»

You can subscribe to ICICI Bank mobile banking by any one of the following means:Login to www.icicibank.com and go to banking section for banking alerts and credit card

section for credit card alerts.

Call up our 24 hours customer care centre and request for subscription for bank alerts, credit

card alerts and demat alerts. Our customer care centre representatives will take you through

the identification process and subscribe you to ICICI Bank mobile banking.

Are there any other prerequisites for availing ICICI Bank mobile banking

facility?

» For mobile alerts, you also need to have a mobile phone with a connection on which

these SMS alerts can be sent to you.

In case your mobile phone service provider does not support SMS facility, this facility may

not be available for you. Kindly contact your mobile phone service provider to enable SMS

facility

Do I need a special phone for mobile alerts?

» No, all you require is a normal GSM/CDMA mobile phone to receive mobile alerts.

Kindly note that the CDMA mobile phone service provider should have activated SMS

facility for you to avail this facility.

How will I know that I have received an ICICI Bank mobile banking alerts?

» Mobile alerts would be received on your mobile phone. The message alert tone set by

you will indicate that a new message has arrived.

41

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 42/62

Can I access the alerts when I am abroad?

»

You need to ensure that you have subscribed for international roaming facility for your mobile phone connection and you have switched your mobile phone on.

What should I do in case I change my mobile phone number?

» For banking alerts and credit card alerts you may simply login to www.icicibank.com

or contact our 24 hour customer care centre for banking alerts, credit cards alerts and demat

alerts to update our records.

Are there any charges for the facility?

» Mobile banking is now a non chargeable service.

All updates of the fees would be put up on our website

www.icicibank.com/pfuser/channels/mobile.htm for reference. ICICI Bank reserves the right

to change the charge for this facility.

What should I do if I have further queries on this facility?

» For any further queries on ICICI Bank alert facility, you may call our 24 hour

customer care centre or write to the account manager for clarification of the same. To write to

the account manager, login to www.icicibank.com, go to the banking section for the option

“write to account manager”. You may also write to account manager at

Briefly describe “ICICI Bank application”.

» Application name is ICICI Bank. This application is a mobile banking application.

User can perform various function like balance inquiry, last three transactions etc. using RIM

42

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 43/62

phone. In mobile banking, banking transaction is presented as text on customer mobile phone

screen as opposed to hearing a message through the phone.

Whom is it targeted for?

» It is designed to meet the needs of mobile users who want the ease and convenience of

anywhere, anytime access to their ICICI Bank account using RIM phone.

What are the benefits for this application?

» Customer is not required to go the bank/ATM for doing the transaction that can be

done using this application.

This transaction can be carried out on 24x7 bases.

How does a user use various features in this application? (please describe your

application usage in detail)

» User has to launch the application through R World. User has to accept the disclaimer

and then he is shown the list as given below:

Balance inquiry

User can view his balance using this option.

Last three transactions

User can select this option to view the last three transactions.

Cheque status inquiry

User can view the status of cheque issued by him/her.

Stop cheque request

User can use this option to stop payment of a cheque issued by him/her

Change of primary account

User can use this option to change the primary account. Primary account is

the main account of the user on which he wishes to carry out mobile banking

transactions.

43

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 44/62

Cheque book request

User uses this option for requesting for a cheque book. Only one such request

will be accepted at a time. Subsequent request can be accepted only when previewsrequest have been fulfilled.

Latest stock quotes

User uses this option for requesting latest stock quotes.

What happens if someone calls me when I am accessing “application name”

»

User can attend to call. After the call is completed user can start using the applicationfrom the same point.

Can I SMS Particular data from my handset while using “ICICI Bank”

» No, presently this facility is not available in this application.

Can I Save Particular data from my handset while using “ICIC Bank”

» Yes the data pertaining to the last option gets saved on the handset. This data can be

accessed using “History” option.

44

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 45/62

Can I print particular information from my handset using “application name”

» No

Is there a password?

» No, you do not require a password.

45

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 46/62

12. TERMS & CONDITION GOVERNING MOBILE

BANKING FACILITY

Definitions:

“Account” mean Bank account &/or credit card account &/or any other type of account so

maintained by the customer with ICICI Bank or any of its affiliate for which the facility is

being offered or may be offered in future (each an “Account” and collectively “Account”)

“Affiliate” of ICICI Bank mean and include:

Any company which is the holding of the company or subsidiary of ICICI

Bank, or

A person under the control of or under common control with ICICI

Bank, or

Any person, in which ICICI Bank has a direct or beneficial interest or control

in more than 26% of the voting securities of such person for the purpose of this definition of

affiliate and terms and condition, “control” together with grammatical variation when used

with respect to any person, means the power to direct the management and policies of such

person, directly or indirectly, whether through the ownership of the vote carrying securities,

by contract or otherwise howsoever; and “person” means a company, corporation, a

partnership, trust or any other entity or organization or other body whatsoever.

“Customer” mean a customer of ICICI Bank or of an affiliate or any person who has applied

for any product/service of ICICI Bank.

“ICICI BANK” mean ICICI Bank limited, a company incorporated under the companies act

1956 and licensed as a bank under banking regulation act, 1949 having its registered office at

landmark, race course

46

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 47/62

Circle, Vadodara 390 007 and corporate office at ICICI Bank towers, Bandra-Kurla-

Complex, Mumbai- 400 051.

“Facility” mean mobile banking facility (which provides the Customers, services such as

information relating to account(s), details about transactions and such other services as may

be provided on the mobile phone number by ICICI Bank or otherwise for the purpose of

availing the facility.

“Mobile Phone Number” means the number specified by the customer on the website,

through the call centre or in writing either through any form provided by ICICI Bank or

otherwise for the purpose of availing the facility.

“Personal Information” means the information about the customer obtained in connection

with the facility.

“Website” refers to www.icicibank.com or any other website as may be notified by ICICI

bank from time to time.

In this document all reference to Customer in masculine gender shall be deemed to include

the feminine gender.

APPLICABILITY OF TERMS AND CONDITIONS

These terms and conditions together with the application made by the Customers and

as accepted by ICICI Bank shall form the contract between the Customers and ICICI Bank,

and shall be further subject to such terms as ICICI Bank may agree with the other service

providers. These terms and conditions shall be in addition to and not in derogation of the

terms and conditions governing ICICI Bank Phone banking, ICICI Bank Internet banking and

relating to any account of the Customer and / or any other product/services provided by ICICI

Bank and its Affiliates.

47

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 48/62

APPLICATION

The Customer shall apply to ICICI Bank for use of the Facility (and/or for any

changes to the option available under the Facility) by use of ICICI Bank phone banking or

ICICI Bank internet banking services or by any other method as provided by ICICI Bank

from time to time including application through forms as prescribed by ICICI Bank from time

to time for use of the Facility.

Application for the Facility made by use of ICICI Bank phone banking or ICICI Bank

internet banking services shall be accepted only after authentication of the Customers through

any mode of verification as may be discretion of ICICI Bank.

The Facility shall be activated after a minimum of 2 working days from the date of

receipt of the application on the Website or at the call centre. In case of application submitted

on the printed format as may be prescribed by ICICI Bank, the Facility shall be activated

after a minimum of 7 working days from the date of receipt of the application at operation

cell, Mumbai.

ELIGIBLE CUSTOMERS

The customers desirous of using the Facility should be either a sole Account holder or

authorized to act independently. In case of joint account, the written mandate of other account

holders authorizing the Customers to use the Facility would be required. All or any

transaction arising from the use of the Facility in the joint account shall be binding on all the

joint account holders, jointly and severally. An Account in the name of the minor, in which a

minor is a joint account holder or any account where the mode of operation is joint, is not

eligible for Facility.

AVAILABILITY & DISCLOSURE

48

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 49/62

ICICI Bank shall endeavor to the Customer through the facility, such services as

ICICI Bank may decide from time to time. ICICI Bank reserves the right to decide what

services may be offered to a Customer on each Account and such offers may differ from

Customer to customer. ICICI Bank May also make addition / deletion to the services offered

through the Facility at its sole discretion. Only those Account opened with the Affiliates of

ICICI Bank and attached to the respective Customer’s ID will be accessible through the

Facility.

The Facility is made available to the request, at the sole discretion of ICICI Bank and

may be discontinued by ICICI Bank at any time, without notice. ICICI Bank reserves the

right to offer the Facility for those Customers who are availing the services of specific

cellular services providers only. The Facility is currently to only to the Customers holding

Accounts with ICICI Bank’s branches in India. ICICI Bank shall have the discretion to offer

the facility to Non Resident Indians subject to application laws.

The access of the Customers to the Facility shall be restricted to Customer availing

the Facility through the Mobile Phone Number. The instruction of the customer by means of

the Customer shall be effected only after authentication of the Customer by means of

verification of the Mobile Phone Numbers and/or through verification of TPIN/password

allotted ICICI Bank to the Customer or through any other mode of verification as may be

stipulated at the discretion of ICICI Bank.

ICICI Bank shall endeavor to carry out the instruction promptly provided that ICICI

Bank shall not be responsible for the delay in carrying out the instructions due to any reason

whatsoever including failure of operational system or due to any requirement of law.

AUTHORITY TO ICICI BANK

The Customers irrevocably and unconditionally authorizes ICICI Bank to access all

his Accounts for effecting or other transaction of the Customer through the Facility. The

Customer further authorizes ICICI Bank accepting/executing request of the Customers.

RECORDS

49

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 50/62

All records of ICICI Bank generates by the transaction arising out of use of the

Facility, including the time of the transaction recorded shall be conclusive proof of the

genuineness and accuracy of the transactions. The authority to record the transaction details is

hereby expressly granted by the customers to ICICI Bank.

INSTRUCTIONS

All instruction for availing the services under the Facility shall be provided through

the Mobile Phone Number in the manner indicated by ICICI Bank. The Customers is also

responsible for the accuracy and authenticity of the instruction provided to ICICI Bank and

the same shall be considered to be sufficient for availing of the services under the Facility.

Where ICICI Bank considers the instruction to be inconsistent or contradictory it may

seek clarification from the Customers before acting on any instruction of the Customers or act

upon any such instruction as it may deem fit. The Customers and ICICI Bank shall have the

right to suspend the services under the Facility if ICICI Bank has reason to believe that the

Customer’s instruction may lead to direct or indirect loss or may require an indemnity from

the Customers before continuing to operate the Facility.

The Customers accepts that all information / instruction will be transmitted to and / or

stored at various locations and be accessed by personal of ICICI Bank (and its Affiliates).

ICICI Bank is authorized to provide any information or details relating to the Customers or to

third party to Facilitate

The providing of the Facility and so far as is necessary to give effect to any

instructions. Accuracy of Information the Customers undertakes to provide accurate

information wherever required and shall be responsible for the correctness of information

provided by him to ICICI Bank at all times including for the purposes of availing of the

facility. ICICI Bank shall not be liable for consequences arising out of erroneous information

supplied by the Customer. If the Customer suspects that there is an error in the information

supplied by Bank to him, he shall advise ICICI Bank as soon as possible on a best effort

basis.

50

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 51/62

While ICICI Bank and its Affiliates will take all reasonable steps to ensure the

accuracy of the information supplied to the Customer, ICICI Bank and its Affiliates shall not

be liable for any inadvertent error, which results in the providing of inaccurate information.

The Customer shall hold ICICI Bank harmless against any loss, damages etc. that may

incurred / suffered by the customer if the information supplied to the Customer turns out be

inaccurate / incorrect.

DISCLAIMER OF LIABILITY

ICICI Bank shall not be responsible for any failure on the part of the Customer to

utilize the Facility due to the Customer not being within the geographical range within which

the Facility is offered; If the Customer has reason to believe that his mobile phone number

is / has been allotted to another person and / or there has been an unauthorized transaction in

his account ICICI and / or his mobile phone is lost, he shall immediately inform ICICI Bank

under acknowledgment about the same.

The Customer agrees that ICICI Bank shall not be liable if

(a) The Customer has breached any of the terms and condition herein or

(b) The Customer has contributed to or the loss is a result of failure on part of the

Customer to advise ICICI Bank within a reasonable time about unauthorized access of or

erroneous transaction in the Account; or

(c) As a result of failure on part of the customer to advise ICICI Bank of a change in or

termination of the Customer’s Mobile Phone numbers.

The customer agrees that the access of the Facility shall be only through the Mobile

Phone Number and the Customer or not, shall be deemed to have originated from the

customer. Under no Circumstance, ICICI Bank shall be held liable if the Facility is not

available for reasons including but not limited to natural calamities, legal restraints, faults in

the telecomm nation network or natural failure, or any other reason beyond the control of

ICICI Bank.ICICI Bank shall not be liable under any circumstance for any damages

whatsoever Whether such damages are direct , indirect, incidental consequential and

irrespective of whether any claim is based on loss of revenue, interruption of business or any

loss of any character or nature whatsoever and Whether sustained by the Customer or by any

other person. Illegal or improper use of the Facility shall render the Customer liable for

51

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 52/62

payment of financial charges as decided by ICICI Bank or will result in suspension of the

Facility to the Customer.ICICI Bank is in no way liable for any error or omission in the

services provided by any cellular or any third party services provider (whether appointed by

ICICI Bank in that behalf or otherwise) to the Customer, Which may affect the Facility.

ICICI Bank does not warrant the confidentiality or security of the messages whether

personal or otherwise transmitted through the facility. ICICI Bank makes no warranty or

representation of any kind in relation to the system and the network or their function or

performance or for any loss or damage whenever and however suffered or incurred by the

Customer or by any person resulting from or in connection with the Facility Without

limitation to the other provision of this terms and condition, ICICI Bank, its employees, agent

or contractors, shall not be liable for and in respect of any loss or damage whether direct,

indirect or consequential, including but not limited to loss of revenue, profit, business,

contracts, anticipated savings or goodwill, loss of use or value of any equipment including

software, whether foreseeable or not, suffered by the Customer or any person howsoever

arising of ICICI Bank in receiving and processing the request and in formulating and

returning responses or any failure, delay, interruption, suspension, restriction, or error in

transmission of any information or message to and from the telecommunication equipment of

the customer and the network of any cellular service provider and ICICI Bank’s system or

any breakdown, interruption, suspension or failure of the telecommunication equipment of

the Customer, ICICI Bank’s system or the network of any cellular services as is necessary to

provided in this terms and conditions, for any dispute between the customer and a cellular

services provider or third party services provider(whether appointed by ICICI Bank in that

behalf or otherwise).

The Customer agrees that ICICI Bank and / or its Affiliates may hold and process his

personal information concerning his Accounts on computer or otherwise in connection with

the Facility as well as for analysis, credit scoring and marketing. The Customer also agrees

ICICI Bank may disclose, in strict confidence, to other institution, such information as may

be reasonably necessary for reasons inclusive of but not limited to the participation in any

telecommunication or electronic clearing network, in compliance with legal directive, for

credit rating by recognized credit rating by recognized credit scoring agencies, and for

directive, for credit rating by recognized credit scoring agencies, and for fraud prevention.

52

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 53/62

The Customer shall not interfere with or misuse in any manner whatsoever the facility

and in the event of any damages to ICICI Bank for the use of the Facility.

ICICI BANK will not be liable for:

(a) Any unauthorized use of the Customer’s TPIN, icicibank.com password or

mobile phone or for fraudulent, duplicate or erroneous instruction given by use of the

Customer’s TPIN,icicibank.com password or mobile phone number;

(b) Acting in good faith on any instructions received by ICICI BANK;

(c) Error, default, delay or inability of ICICI BANK to act on all or any of the

instructions

(d) Loss of any information/instructions in transmission;

(e) Unauthorized access by any other person to any information / instructions

given by the Customer or breach of confidentiality;

(f) ICICI BANK will not be concerned with any dispute between the customer

and any cellular services provided and / or any third party providing by ICICI BANK. ICICI

BANK makes no representative or gives no warranty with respect to the quality of the service

provided by any cellular service provider. ICICI BANK shall not be liable for the oversight

on part of the Customer to update himself with the addition of services which have been

included in the facility and specific services for each product as may be provided on the

website of ICICI BANK and as will be available with the authorized call centers of ICICI

BANK.

INDEMNITY

In consideration of ICICI BANK providing the Facility, the customer agree to

indemnify and keep safe, harmless and indemnified ICICI BANK from and against all action,

claims, demands, proceedings, loss, damages, costs, charges and expenses whatsoever ICICI

BANK may incur, sustain, suffer or be put to at any time as a consequence of acting on or

omitting or refusing to act on any instruction given by use of the facility.

53

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 54/62

The Customer hold ICICI BANK/ its Affiliates harmless against any loss incurred by

the Customer due to failure to provide the services offered under the Facility or any delay in

providing the services due to any failure or discrepancy in the network of the cellular service

provider.

The Customer agrees to indemnify and hold ICICI BANK harmless for any losses

occurring as a result of the:

i. The customer permitting any third parties to use the Facility.

ii. The Customer permitting any other person to have access to his mobile phone or a

consequence of leaving the mobile phone unattended or loss of mobile phone.

FEES

ICICI BANK shall have the discretion to charge such fees as it may deem fit from

time to time and may at its sole discretion, revise the fees for use of any or all of the Facility,

by notice to the customers. The Customer may at any time discontinue or unsubscribe to the

said facility. The Customer shall be liable for payment of such airtime or other charges which

may be levied by any cellular service provider in connection with availing of the Facility and

ICICI BANK is in no way concerned with the same. The charges payable by the Customer is

exclusive of the amount payable to any cellular service provider and would be debited from

the account of the Customer on a monthly basis. The Customer shall be required to refer to

the schedule of fees put up on the Website from time to time.

MODIFICATION

ICICI BANK has the absolute discretion to amend or supplement any of the terms and

conditions at any time and will endeavor to give prior notice of fifteen days by email or by

displaying on the Website depending upon the discretion of ICICI BANK, whichever

feasible, and such amended terms and condition will thereupon apply to and be binding on

the Customer.

54

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 55/62

TERMINATION

The Customer may request for termination of the Facility any time by giving a written

notice of at least 15 days to ICICI BANK. He Customer will remain responsible for any

transaction made through his mobile phone number through the facility prior to the of such

cancellation of facility ICICI BANK may, at its discretion, withdraw temporarily or terminate

the facility, either wholly or in part, at any time without giving prior notice to the Customer.

ICICI BANK may, without prior notice, suspend the facility at any time during which any

maintenance work or repair is required to be carried out or in case of any emergency or for

Security reasons, which require the suspension of the Facility.ICICI BANK, shall endeavor to

give a reasonable notice for withdrawal or termination of the Facility. The closure of all

Account of the Customer will automatically terminate the facility.ICICI BANK may suspend

or terminate facility without prior notice if the Customer has breached these terms and

conditions or ICICI BANK learns of the death, bankruptcy or lack of legal capacity of the

customer.

NOTICES

ICICI BANK and the customer may give notice under these terms and condition

electronically to the mailbox of the Customer (which will be regarded as being in writing) or

in writing by delivering them by hand or sending them by post to the last address given by the

Customer and in to ICICI BANK at its office at 3 rd floor, south tower, ICICI BANK towers,

Bandra-Kurla-Complex, Mumbai 400 051. In addition, ICICI bank shall also provide notice

of general nature regarding the facility and terms and conditions, which are application to all

customers of the Facility, on its website and/ or also by means the customized messages sent

to the Customer over his mobile phone as short messaging service (“SMS”).such notice will

be deemed to have been served individually to each Customer.

GOVERNING LAW

55

8/4/2019 Final Project Mukesh g

http://slidepdf.com/reader/full/final-project-mukesh-g 56/62

Any dispute or differences arising out of or in connection with the facility shall be

subject to the exclusive jurisdiction of the courts of Mumbai.

ICICI BANK accepts no liability whatsoever, direct or indirect for non compliance

with the laws of any country other than that of India. The mere fact that the Facility can be

accessed by a Customer in a country other than India does not imply that the laws of the said