nelcast limited cmp - spark capitalmailers.sparkcapital.in/uploads/mukesh/nelcast_june 2015.pdf ·...

TRANSCRIPT

Nelcast Limited CMP

Rs. 35

Stock Performance (%)

1m 3m 12m

Nelcast -14% 5% 0%

Sensex -2% -7% 5%

BSE Auto -4% -7% 21%

Financial Summary

Year Revenues (Rs. mn) EBITDA (Rs. mn) EBITDA Margin Adj. PAT (Rs. mn) Adj. EPS (Rs.) P/E(x) EV/EBITDA(x)

FY15 5,466 469 8.6% 219 2.5 13.9 7.3

FY16E 6,583 625 9.5% 333 3.8 9.2 5.5

FY17E 7,952 875 11.0% 517 5.9 5.9 3.7

Date June 19, 2015

Market Data

SENSEX 26833

Nifty 8092

Bloomberg NELC IN

Shares o/s 87mn

Market Cap Rs. 3bn

52-wk High-Low Rs. 48-26

3m Avg. Daily Vol Rs. 2mn

Index member BSESMCAP

Latest shareholding (%)

Promoters 74.4

Institutions 0.1

Public 25.5

Company Update Nelcast is India’s largest iron casting manufacturer, supplying primarily to tractors (~40% of revenue) and MHCVs

(~60%). FY12 was the last year when both the tractors and MHCV industry recorded a positive growth; we believe

Nelcast is well poised to benefit from the expected recovery in both tractors (from 2HFY16) and MHCVs in FY16

and FY17. This coupled with the company’s expected growth in exports and non-auto (rail) is expected to drive

steep revenue growth. Furthermore, scrap steel (key raw material) prices have weakened considerably, providing

margin cushion. We believe the stock is attractively placed at sub-6x FY17 P/E (FY15 PE at 14x)

Key beneficiary of growth in multi-axle CVs: Nelcast primarily supplies wheel hubs, differential carriers and axle

housings to CVs. These parts are typically load bearings components and are not expected to move to aluminum castings

(globally iron castings are used). Moreover, content per vehicle increases significantly as the number of axles/wheels per

vehicle increases. Multi-axle (MAV) CAGR (FY13-FY15) was 3% vs. de-growth of 16% for MHCVs. We expect MAVs to

continue outgrowing overall CVs. Nelcast caters to ~60% of Ashok Leyland’s requirement and recently started supplies to

Bharat Benz. We expect overall MHCV volume CAGR of 21% from FY15-FY17 and hence the growth for Nelcast’s MHCV

revenues should be higher. We factor in 20% CV revenue CAGR for Nelcast and believe there is an upside to our estimate.

Tractors to see recovery in 2HFY16: Use of iron casting is higher in tractors vs. CVs as typically users prefer tractors to

be as heavy as possible. Key components supplied include transmission case, axle housing, hydraulic lift cover among

others. Nelcast caters to ~60% of TAFE’s requirement and also supplies to Escorts and other smaller players. Supply to

M&M is negligible as the company sources iron castings primarily from group company, Mahindra Hinoday. We expect

tractor volumes to recover from 2HFY16 and post a ~7% CAGR from FY15-FY17.

Margins to improve in-line with recovery: Over the last 15 years, we have seen Nelcast’s margin record a steep pick-up

in-line with cyclical recovery in tractors and CVs. We have witnessed the company’s EBITDA margin peak at ~12.5% in

FY08 and in FY12. Current capacity utilization stands at ~50% and with improving volumes for MHCVs and Tractors, we

conservatively expect EBITDA to improve to 11% in FY17 from 8.6% in FY15. With improvement in higher tonnage

vehicles, the variable expenses are also expected to reduce as a % of sales and hence there is an upside to our estimate.

Exports and others: Currently exports and other segments are negligible, however with new orders from Daimler and

American Axles (Thailand), the company expect a steep growth in exports. Nelcast has also recently started supplies of

‘base plates’ for metro rail. The company targets ~10% of revenues from exports and other segments by FY17.

Good balance sheet with a net debt/equity of 0.1x, negligible capex requirement over the next two years bode well for the

company. We expect post tax RoCEs to improve to 13% in FY17 from ~7% in FY15 (~15% in FY12)

Levered to recovery in MHCV and tractors

MUKESH SARAF [email protected] +91 44 4344 0041

ROHIT KRISHNA [email protected] +91 44 4344 0020 Find Spark Research on Bloomberg (SPAK <go>),

Thomson First Call, Reuters Knowledge and Factset

Page 1

Nelcast Limited CMP

Rs. 35

Corporate Factsheet

Promoter Background

Nelcast Limited was set up in 1985 by Mr. Radhakrishna Reddy and is engaged in the business of manufacture of ferrous

castings. The company has a production capacity of 150,000 MT per annum and can produce parts ranging from 0.5 to 260

Kgs. Machining division was set up in 2008.

Business The company primarily caters to the heavy commercial vehicle and tractor segment. Product portfolio includes wheel hubs,

axle housing, brackets, cylinder heads and blocks.

Management

Mr. P. Deepak – Managing Director

Double masters in Engineering from Northwestern University, USA and MBA at Kellogg School of Management; four years of

industrial experience including at Federal-Mogul Corp, USA

Mr. Vijaya Bhaskar Reddy – Dy. Managing Director

Graduate in Law and Member of Institute of Chartered Accountants of India; he has been with Nelcast since its inception and

has a total of 32 years of experience

Presence The company has manufacturing facilities at Gudur, Andhra Pradesh and Ponneri, Tamil Nadu.

Corporate Structure The promoters’ stake in Nelcast Limited 74.4% as of March 2015. Nelcast has 97.5% in NC Energy which is in the business of

development and sale of power plant.

Revenue Model The company derived 60% of its revenue in FY15 from the heavy commercial vehicle segment and 37% from the tractors

segment. Non-auto and exports contributed to ~Rs.50mn in FY15.

Key Success Factors One of the biggest players in the segment, long standing relationship with most OEMs, conservative and prudent management

Credit Rating ICRA A (Long-term) and A1 (Short-term)

Corporate Bankers State Bank of India, Kotak Mahindra, Standard Chartered, HSBC

Auditors J.B. Reddy, Hyderabad

Corporate Office TTK Road, Alwarpet, Chennai

Page 2

Nelcast Limited CMP

Rs. 35

TYPES OF

CASTING

Sand Casting Die Casting

Centrifugal Casting

Used for production of large parts

Mold shaped using natural or synthetic

sand and mold cavity is made of metal or

wood

Surface of sand castings are rough due to

surface impurities

Machining is mostly required

Metal is forced into mold at a high pressure

Used for production of multiple identical

parts

Better surface finish and increased

dimensional accuracy

Might not require machining to get the

dimensions

Die casting molds take longer time to

produce are expensive as it is made from

hardened steel Used for industrial applications where durabilty

of parts are very important

As molten metal is poured a permanent mold

spins at high speeds around its axis

Molten metal moves towards the mold walls

due to centrifugal force, solidifies after cooling,

producing a fine part

Parts produced this way are usually resistant to

atmospheric corrosion

Nelcast primarily does Sand Casting

Page 3

Nelcast Limited CMP

Rs. 35 Product Portfolio

Page 4

Commercial Vehicles

Wheel Hubs Brake Drums Differential Carriers & Axle Housing

Slide Support Shackles Brackets

Railways

Inserts/Shoulders for Concrete Sleepers

Tractors

Transmission Case Centre Housing Rear Axle Housing Hydraulic Lift Cover

Nelcast Limited CMP

Rs. 35

Growth in CVs and Tractor industries has mostly moved in the same direction, leading to high revenue volatility

Source: SIAM, Spark Capital

Segment Breakup between CV and Tractor

Source: Company, Spark Capital

Revenue growth remains volatile driven by end markets

Source: Company, Spark Capital

Primarily caters to CV and Tractor markets

CV 80%

Tractors 20%

CV 60%

Tractors 40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

0

1000

2000

3000

4000

5000

6000

7000

Revenue Revenue yoy %

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Tractors yoy % HCV yoy %

Page 5

FY 05 FY 15

Nelcast Limited CMP

Rs. 35

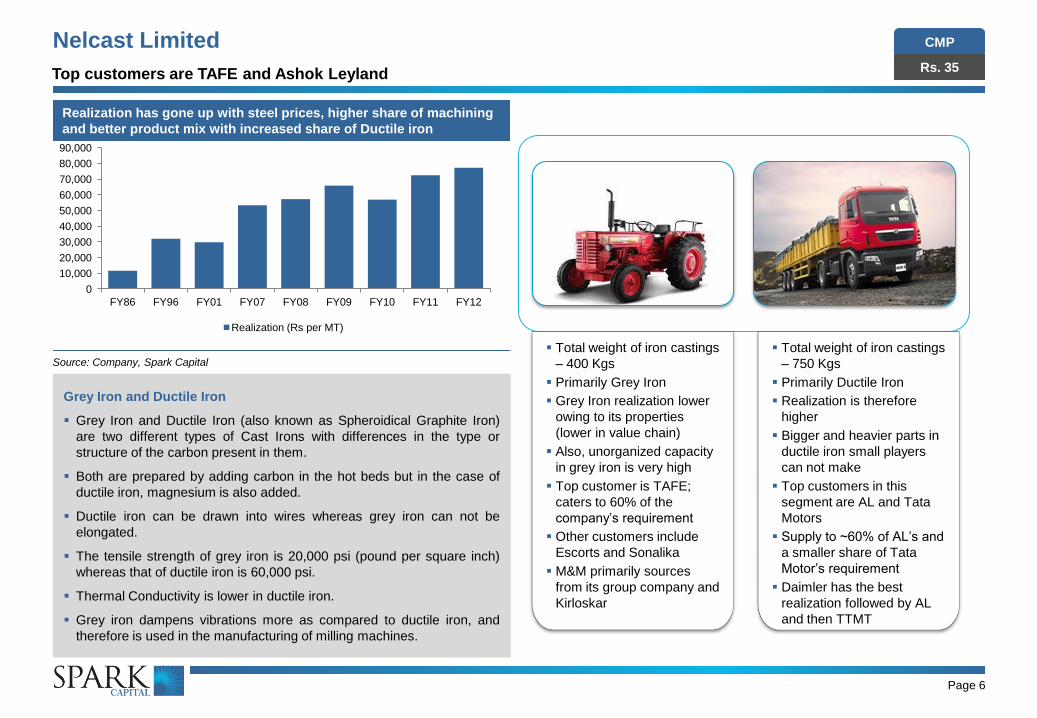

Realization has gone up with steel prices, higher share of machining

and better product mix with increased share of Ductile iron

Source: Company, Spark Capital

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY86 FY96 FY01 FY07 FY08 FY09 FY10 FY11 FY12

Realization (Rs per MT)

Grey Iron and Ductile Iron

Grey Iron and Ductile Iron (also known as Spheroidical Graphite Iron)

are two different types of Cast Irons with differences in the type or

structure of the carbon present in them.

Both are prepared by adding carbon in the hot beds but in the case of

ductile iron, magnesium is also added.

Ductile iron can be drawn into wires whereas grey iron can not be

elongated.

The tensile strength of grey iron is 20,000 psi (pound per square inch)

whereas that of ductile iron is 60,000 psi.

Thermal Conductivity is lower in ductile iron.

Grey iron dampens vibrations more as compared to ductile iron, and

therefore is used in the manufacturing of milling machines.

Total weight of iron castings

– 400 Kgs

Primarily Grey Iron

Grey Iron realization lower

owing to its properties

(lower in value chain)

Also, unorganized capacity

in grey iron is very high

Top customer is TAFE;

caters to 60% of the

company’s requirement

Other customers include

Escorts and Sonalika

M&M primarily sources

from its group company and

Kirloskar

Total weight of iron castings

– 750 Kgs

Primarily Ductile Iron

Realization is therefore

higher

Bigger and heavier parts in

ductile iron small players

can not make

Top customers in this

segment are AL and Tata

Motors

Supply to ~60% of AL’s and

a smaller share of Tata

Motor’s requirement

Daimler has the best

realization followed by AL

and then TTMT

Page 6

Top customers are TAFE and Ashok Leyland

Nelcast Limited CMP

Rs. 35

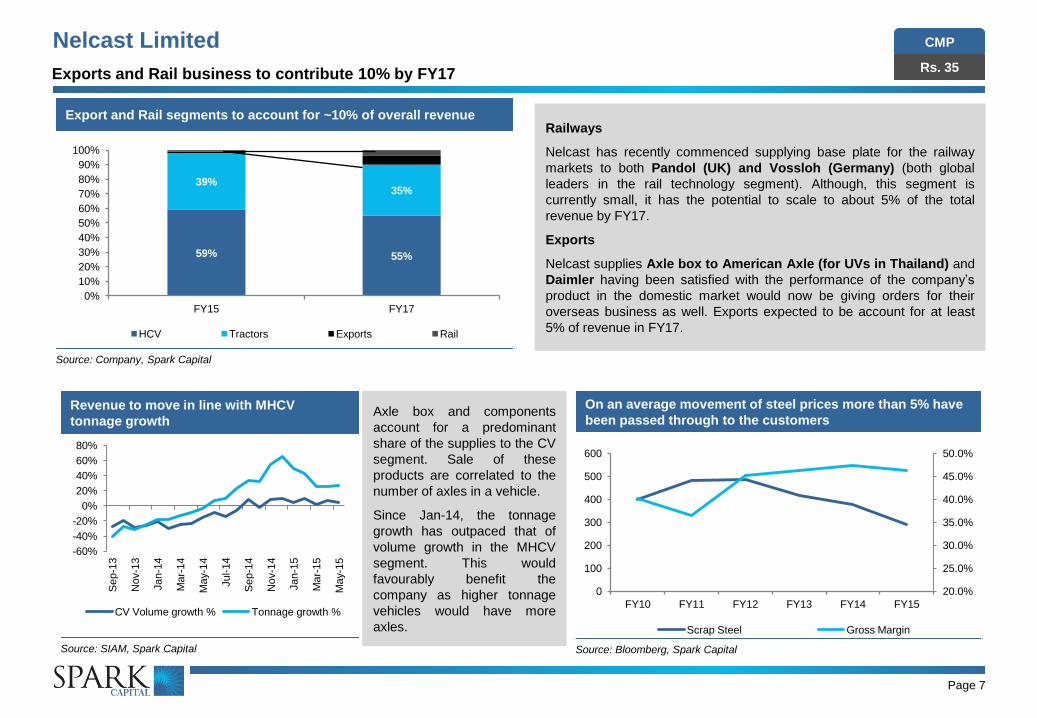

Export and Rail segments to account for ~10% of overall revenue

Source: Company, Spark Capital

59% 55%

39% 35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY15 FY17

HCV Tractors Exports Rail

Revenue to move in line with MHCV

tonnage growth

Source: SIAM, Spark Capital

Page 7

Railways

Nelcast has recently commenced supplying base plate for the railway

markets to both Pandol (UK) and Vossloh (Germany) (both global

leaders in the rail technology segment). Although, this segment is

currently small, it has the potential to scale to about 5% of the total

revenue by FY17.

Exports

Nelcast supplies Axle box to American Axle (for UVs in Thailand) and

Daimler having been satisfied with the performance of the company’s

product in the domestic market would now be giving orders for their

overseas business as well. Exports expected to be account for at least

5% of revenue in FY17.

-60%

-40%

-20%

0%

20%

40%

60%

80%

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

CV Volume growth % Tonnage growth %

Axle box and components

account for a predominant

share of the supplies to the CV

segment. Sale of these

products are correlated to the

number of axles in a vehicle.

Since Jan-14, the tonnage

growth has outpaced that of

volume growth in the MHCV

segment. This would

favourably benefit the

company as higher tonnage

vehicles would have more

axles.

On an average movement of steel prices more than 5% have

been passed through to the customers

Source: Bloomberg, Spark Capital

Exports and Rail business to contribute 10% by FY17

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0

100

200

300

400

500

600

FY10 FY11 FY12 FY13 FY14 FY15

Scrap Steel Gross Margin

Nelcast Limited CMP

Rs. 35

EBITDA % has moved closely with the revenue growth; expect non-

linear growth in EBITDA in the next two years

Source: Company, SIAM, Spark Capital

Power and fuel cost contribute the most in ‘other expenditure’

Source: Company, Spark Capital

Power cost does not proportionately increase with production; hence

as utilization improves expect power cost % to reduce

Source: Company, Spark Capital

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

100

200

300

400

500

600

700

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

Net Sales Power cost %

12.3% 17.2% 16.2%

6.1%

6.8% 6.6% 3.6%

3.2% 2.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

FY 2012 FY 2013 FY 2014

Power and fuel Mfg Expenses Consumption of stores

Repairs Freight and forwarding Others

Page 8

Operating leverage to lead to sharp uptick in profitability

0%

2%

4%

6%

8%

10%

12%

14%

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16E

FY

17E

EBITDA %

-40%

-20%

0%

20%

40%

60%

80%

100%

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16E

FY

17E

Revenue yoy % Tractors yoy % MHCV yoy %

Nelcast Limited CMP

Rs. 35

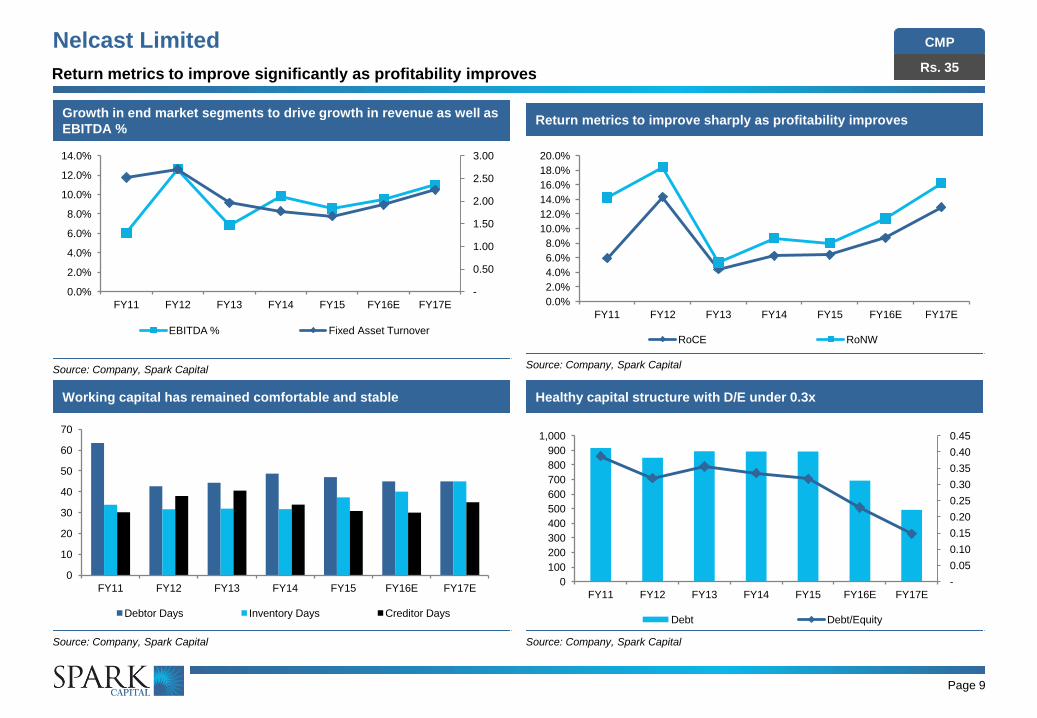

Return metrics to improve sharply as profitability improves

Source: Company, Spark Capital

Growth in end market segments to drive growth in revenue as well as

EBITDA %

Source: Company, Spark Capital

Working capital has remained comfortable and stable

Source: Company, Spark Capital

Healthy capital structure with D/E under 0.3x

Source: Company, Spark Capital

Return metrics to improve significantly as profitability improves

Page 9

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0

100

200

300

400

500

600

700

800

900

1,000

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Debt Debt/Equity

0

10

20

30

40

50

60

70

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Debtor Days Inventory Days Creditor Days

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

RoCE RoNW

-

0.50

1.00

1.50

2.00

2.50

3.00

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

EBITDA % Fixed Asset Turnover

Nelcast Limited CMP

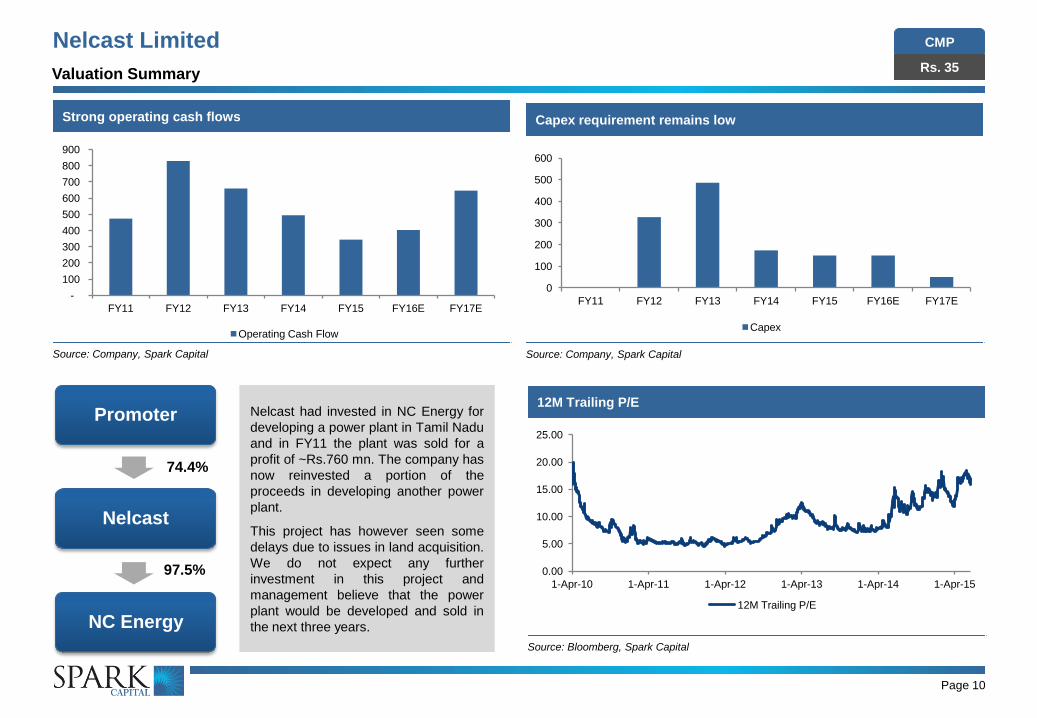

Rs. 35 Valuation Summary

Promoter

Nelcast

NC Energy

74.4%

97.5%

Page 10

Nelcast had invested in NC Energy for

developing a power plant in Tamil Nadu

and in FY11 the plant was sold for a

profit of ~Rs.760 mn. The company has

now reinvested a portion of the

proceeds in developing another power

plant.

This project has however seen some

delays due to issues in land acquisition.

We do not expect any further

investment in this project and

management believe that the power

plant would be developed and sold in

the next three years.

12M Trailing P/E

Source: Bloomberg, Spark Capital

0.00

5.00

10.00

15.00

20.00

25.00

1-Apr-10 1-Apr-11 1-Apr-12 1-Apr-13 1-Apr-14 1-Apr-15

12M Trailing P/E

Capex requirement remains low

Source: Company, Spark Capital

Strong operating cash flows

Source: Company, Spark Capital

-

100

200

300

400

500

600

700

800

900

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Operating Cash Flow

0

100

200

300

400

500

600

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Capex

Nelcast Limited CMP

Rs. 35

Page 11

Financial Summary

Abridged Financial Statements Key metrics

Rs. mn FY12 FY13 FY14 FY15E FY16E FY17E FY12 FY13 FY14 FY15E FY16E FY17E

Profit & Loss Growth ratios

Revenues 6,543 5,095 5,176 5,466 6,583 7,952 Revenues 29.0% -22.1% 1.6% 5.6% 20.4% 20.8%

Manufacturing & Other Expenses 5,719 4,747 4,666 4,997 5,958 7,077 EBITDA 167.4% -57.7% 46.2% -8.0% 33.4% 39.9%

EBITDA 824 349 510 469 625 875 PAT 57.1% -69.9% 61.7% -2.4% 51.6% 55.5%

Depreciation 110 111 128 127 132 134 Margins

EBIT 714 238 381 342 493 741 EBITDA 12.6% 6.8% 9.8% 8.6% 9.5% 11.0%

Net Interest Exp / (inc) 36 31 19 47 31 22 EBIT 10.9% 4.7% 7.4% 6.3% 7.5% 9.3%

Profit Before Tax 679 207 363 295 462 719 PAT 7.1% 2.7% 4.3% 4.0% 5.1% 6.5%

Tax 216 68 138 76 129 201 Leverage & WC ratios

Adjusted Net Profit 463 139 225 219 333 517 Debt to equity (x) 0.3 0.4 0.3 0.3 0.2 0.1

Balance Sheet (Rs. mn) Current ratio (x) 2.1 1.9 2.1 2.0 2.1 2.1

Shareholders Equity 2,660 2,516 2,670 2,816 3,029 3,341 Debtor days (Sales) 43 44 49 47 45 45

Loan funds 850 894 892 892 692 492 Inventory days (Sales) 32 32 32 37 40 45

Sources of funds 3,509 3,655 3,877 4,052 4,065 4,177 Creditor Days (Sales) 38 41 34 31 30 35

Net block 1,902 1,870 2,332 2,355 2,373 2,289 Performance & turnover ratios

Investments 6 205 256 316 316 316 RoACE 14.3% 4.5% 6.3% 6.4% 8.8% 12.9%

Capital WIP 37 435 19 47 47 47 RoAE 18.4% 5.4% 8.7% 8.0% 11.4% 16.2%

Current assets, loans & advances 2,442 1,883 1,984 2,140 2,227 2,645 Total asset turnover (x) 1.4 1.0 1.0 1.0 1.1 1.3

Current liabilities & provisions 877 740 713 806 898 1,119 Fixed asset turnover (x) 2.7 2.0 1.8 1.7 1.9 2.2

Net Current Assets 1,565 1,144 1,271 1,334 1,329 1,526 Valuation metrics

Application of funds 3,509 3,655 3,877 4,052 4,065 4,177 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 87.0 87.0 87.0 87.0 87.0 87.0

Cash flows from operations 625 604 427 267 274 445 Market capitalisation (Rs. mn) 3,045 3,045 3,045 3,045 3,045 3,045

Capex (327) (486) (174) (150) (150) (50) Enterprise value (Rs. mn) 3,268 3,457 3,416 3,444 3,428 3,238

Free Cash Flow 298 119 254 117 124 395 EV/EBIDTA (x) 4.0 9.9 6.7 7.3 5.5 3.7

Cash flows from investments (322) (665) (213) (210) (150) (50) Adj. Per-share earnings (Rs.) 5.3 1.6 2.6 2.5 3.8 5.9

Cash flows from financing (200) (84) (175) (73) (320) (405) Price-earnings multiple (x) 6.6 21.9 13.5 13.9 9.2 5.9

Cash & Cash equivalents 626 481 520 504 309 299 Dividend yield (%) 5.1% 1.4% 2.0% 2.0% 3.3% 5.6%

35

Nelcast Limited CMP

Rs. 35 Disclaimer

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities and

infrastructure advisory services. Spark Capital is registered with SEBI as a Stock Broker and Category 1 Merchant Banker.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in the last five years. We

have not been debarred from doing business by any Stock Exchange/SEBI or any other authorities, nor has our certificate of registration been cancelled by SEBI at any point of

time.

Spark Capital has a subsidiary Spark Investment Advisors (India) Private Limited which is engaged in the services of providing investment advisory services and is registered

with SEBI as Investment Advisor. Spark Capital has also an associate company Spark Infra Advisors (India) Private Limited which is engaged in providing infrastructure

advisory services.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should

be construed as investment or financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of

companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies

referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This

document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published,

copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in

any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Spark Capital

and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to

a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such applicable restrictions. This

material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this

document. Spark Capital , its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or

deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit

investment banking or other business from, any company referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark

Capital. While we would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information.

Also, there may be regulatory, compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective

directors, employees, agents or representatives shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents

or any errors or discrepancies herein or for any decisions or actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or

damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of

or reliance on this report.

Absolute

Rating

Interpretation

BUY Stock expected to provide positive returns of >15% over a 1-year horizon REDUCE Stock expected to provide returns of <5% – -10% over a 1-year

horizon

ADD Stock expected to provide positive returns of >5% – <15% over a 1-year

horizon SELL Stock expected to fall >10% over a 1-year horizon

Page 12

Nelcast Limited CMP

Rs. 35 Disclaimer (Cont’d)

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency,

Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Disclosure of interest statement Yes/No

Analyst financial interest in the company No

Group/directors ownership of the subject company covered No

Investment banking relationship with the company covered No

Spark Capital’s ownership/any other financial interest in the company covered No

Associates of Spark Capital’s ownership more than 1% in the company covered No

Any other material conflict of interest at the time of publishing the research report No

Receipt of compensation by Spark Capital or its Associate Companies from the subject company covered for in the last twelve months:

Managing/co-managing public offering of securities

Investment banking/merchant banking/brokerage services

products or services other than those above

in connection with research report

No

Whether Research Analyst has served as an officer, director or employee of the subject company covered No

Whether the Research Analyst or Research Entity has been engaged in market making activity of the Subject Company; No

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research

analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under

the Securities Exchange Act of 1934, as amended) only by Auerbach Grayson, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange

Act of 1934, as amended). Auerbach Grayson accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities

discussed in the research material may do so through Auerbach Grayson. All responsibility for the distribution of this report by Auerbach Grayson, LLC in the US shall be borne

by Auerbach Grayson, LLC. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in the US. This report is not directed at you

if Spark Capital Advisors (India) Private Limited or Auerbach Grayson, LLC is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available

to you. You should satisfy yourself before reading it that Auerbach Grayson, LLC and Spark Capital Advisors (India) Private Limited are permitted to provide research material

concerning investment to you under relevant legislation and regulations;

Page 13