financial statements 2020 - pioneer energy

TRANSCRIPT

2O2O FinancialReport For the year ended

31 March 2O2O

22 O 2 O F I N A N C I A L R E P O R T

Contents

Directory 3

Directors’ Statutory Report 4

Directors’ Responsibility Statement 5

Consolidated Income Statement 6

Consolidated Statement of Comprehensive Income 7

Consolidated Statement of Changes in Equity 8

Consolidated Statement of Financial Position 9

Consolidated Cash Flow Statement 10

Notes to the Consolidated Financial Statements 11

Audit Report 44

32 O 2 O F I N A N C I A L R E P O R T

Directory

Nature of BusinessThe Group’s business is primarily the generation of electricity, owning, operating and developing small hydro power stations, wind generation and landfill gas sites and offering energy solutions for industrial clients at a range of sites throughout New Zealand. The principal objective of the Group is to operate as a successful business as defined in section 36 of the Energy Companies Act 1992.

Board of DirectorsS Heal (Chairman)W McNabb (retired 17 September 2019)N LewisR HewettW MoranN Crauford (appointed 17 September 2019)

AuditorsDeloitte Limited

SolicitorBuddle Findlay

Registration No.DN/613390

Registered Office11 Ellis StreetPO Box 275Alexandra

42 O 2 O F I N A N C I A L R E P O R T

Directors’ Statutory Report

4

PIONEER ENERGY LIMITED DIRECTORS’ STATUTORY REPORT Surplus after Tax: The Group’s net deficit after taxation for the year was $10.567 million (2019 (restated): surplus $12.506 million). Directors’ Fees Directors’ fees in respect of the year ended 31 March, 2020 were as follows: PEL Joint Ventures S Heal $88,167 $3,000 W McNabb $20,058 - N Lewis $44,083 $20,000 R Hewett $44,083 $33,000 W Moran $48,142 - N Crauford $22,250 - There were no requests from directors to use Group information received in their capacity as Directors, which could not otherwise have been made available to them. The Group has arranged Directors’ and Officers’ liability insurance. For and on behalf of the Directors

_______________________ _____________________ S Heal W Moran Chairman Director Date: 7 July 2020 Date: 7 July 2020

52 O 2 O F I N A N C I A L R E P O R T

Directors’ Responsibility Statement

5

PIONEER ENERGY LIMITED DIRECTORS’ RESPONSIBILITY STATEMENT The Directors of Pioneer Energy Limited are pleased to present to shareholders and other interested parties the consolidated financial statements for the year ending 31 March, 2020. No disclosure has been made in respect of section 211(1)(g) of the Companies Act 1993 following a unanimous decision by the shareholders in accordance with section 211(3) of the Act. The Consolidated Financial Statements are signed on behalf of the Board by:

_______________________ _____________________ S Heal W Moran Chairman Director Date: 7 July 2020 Date: 7 July 2020

62 O 2 O F I N A N C I A L R E P O R T

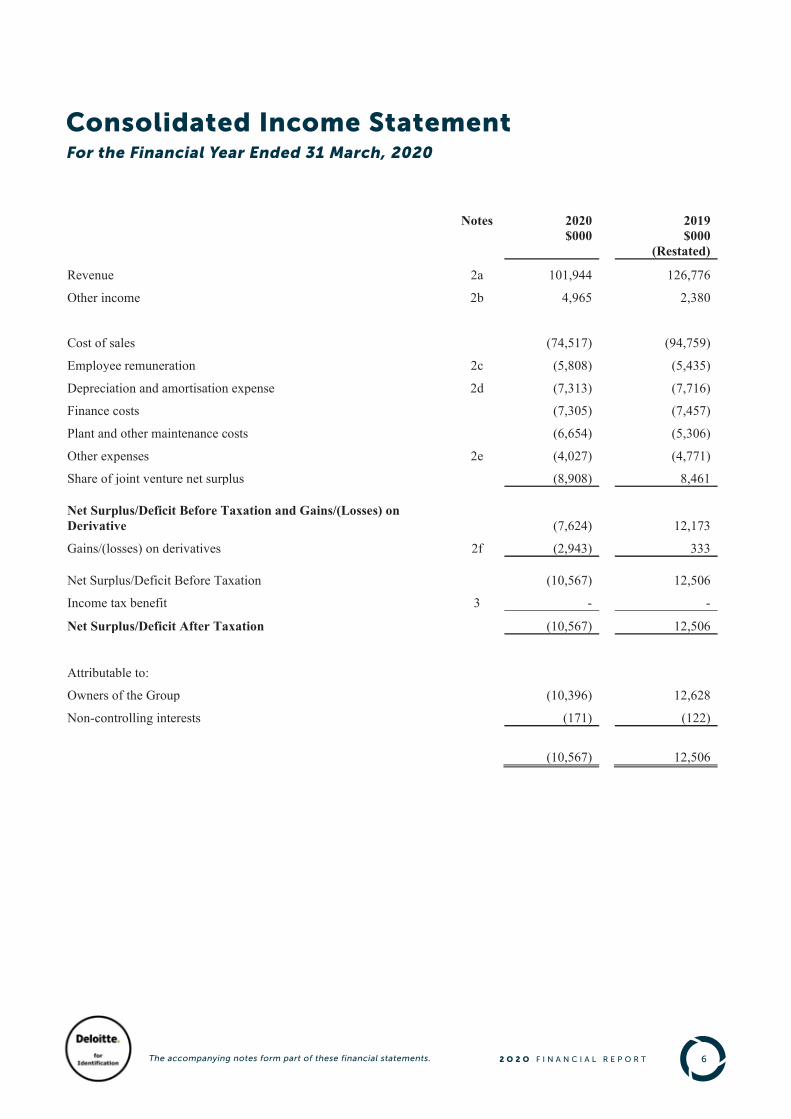

Consolidated Income StatementFor the Financial Year Ended 31 March, 2020

6

PIONEER ENERGY LIMITED CONSOLIDATED INCOME STATEMENT For the Financial Year Ended 31 March, 2020

Notes 2020 2019

$000

$000

(Restated)

Revenue 2a 101,944 126,776

Other income 2b 4,965 2,380

Cost of sales (74,517) (94,759)

Employee remuneration 2c (5,808) (5,435)

Depreciation and amortisation expense 2d (7,313) (7,716)

Finance costs (7,305) (7,457)

Plant and other maintenance costs (6,654) (5,306)

Other expenses 2e (4,027) (4,771)

Share of joint venture net surplus (8,908) 8,461 Net Surplus/Deficit Before Taxation and Gains/(Losses) on Derivative (7,624) 12,173

Gains/(losses) on derivatives 2f (2,943) 333

Net Surplus/Deficit Before Taxation

(10,567) 12,506

Income tax benefit 3 - -

Net Surplus/Deficit After Taxation (10,567) 12,506

Attributable to:

Owners of the Group (10,396) 12,628

Non-controlling interests (171) (122)

(10,567) 12,506

The accompanying notes form part of these financial statements.

The accompanying notes form part of these financial statements.

72 O 2 O F I N A N C I A L R E P O R T

Consolidated Statement of Comprehensive IncomeFor the Financial Year Ended 31 March, 2020

7

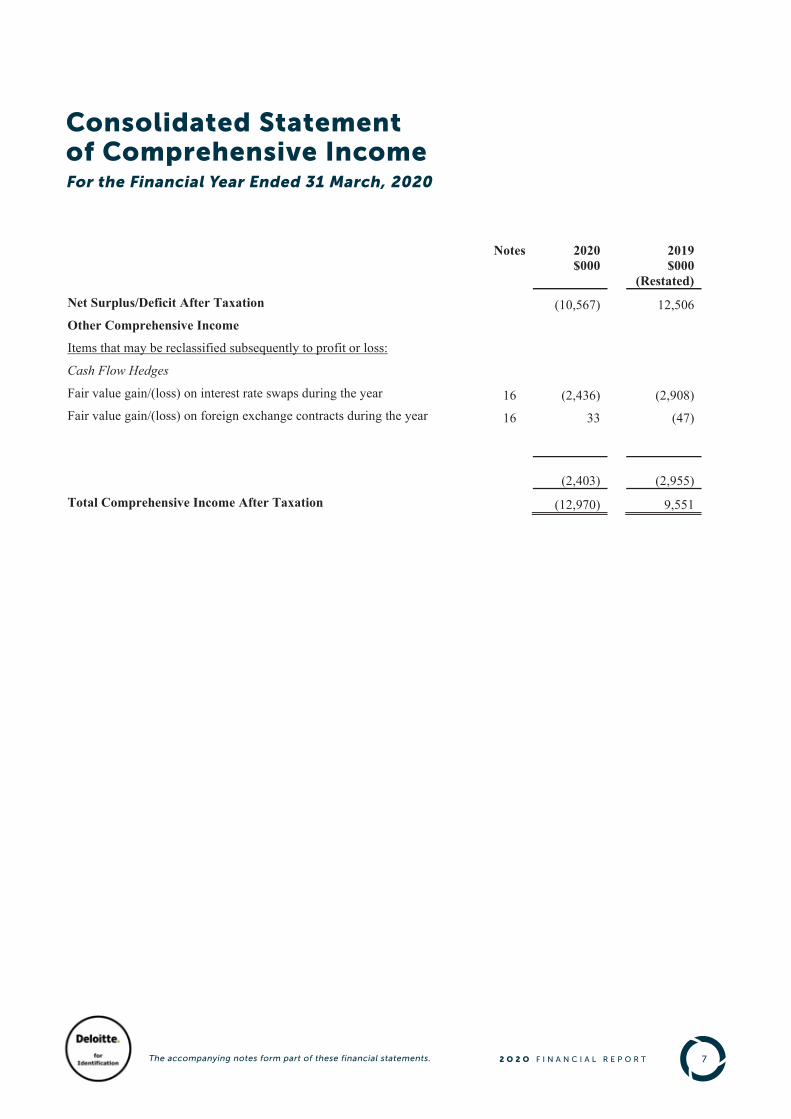

PIONEER ENERGY LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME For the Financial Year Ended 31 March, 2020

Notes 2020 2019

$000

$000

(Restated) Net Surplus/Deficit After Taxation (10,567) 12,506 Other Comprehensive Income Items that may be reclassified subsequently to profit or loss: Cash Flow Hedges Fair value gain/(loss) on interest rate swaps during the year 16 (2,436) (2,908) Fair value gain/(loss) on foreign exchange contracts during the year 16 33 (47)

(2,403)

(2,955) Total Comprehensive Income After Taxation (12,970) 9,551

The accompanying notes form part of these financial statements.

The accompanying notes form part of these financial statements.

82 O 2 O F I N A N C I A L R E P O R T

Consolidated Statement of Changes in EquityFor the Financial Year Ended 31 March, 2020

8

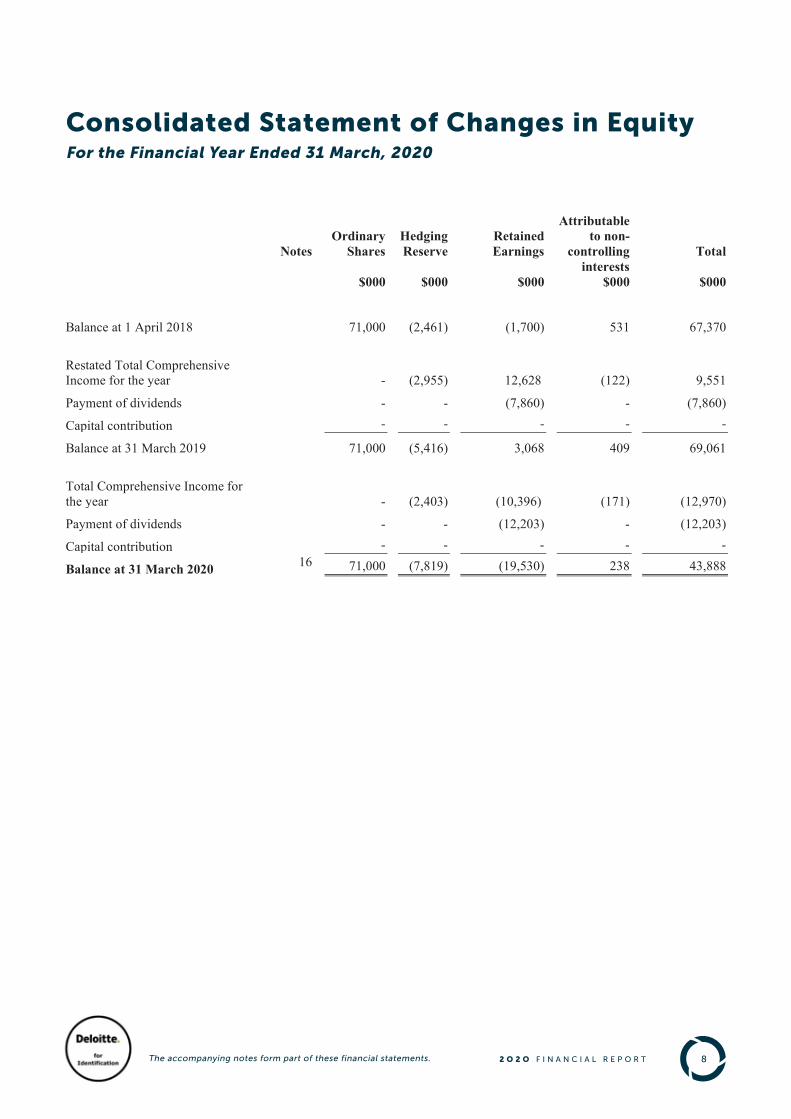

PIONEER ENERGY LIMITED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY For the Financial Year Ended 31 March, 2020

Notes

Ordinary

Shares

$000

Hedging Reserve

$000

Retained Earnings

$000

Attributable to non-

controlling interests

$000

Total

$000

Balance at 1 April 2018 71,000 (2,461) (1,700) 531 67,370 Restated Total Comprehensive Income for the year - (2,955)

12,628 (122) 9,551

Payment of dividends - - (7,860) - (7,860)

Capital contribution - - - - -

Balance at 31 March 2019 71,000 (5,416) 3,068 409 69,061

Total Comprehensive Income for the year

- (2,403) (10,396) (171) (12,970)

Payment of dividends - - (12,203) - (12,203)

Capital contribution - - - - -

Balance at 31 March 2020 16 71,000 (7,819) (19,530) 238 43,888

The accompanying notes form part of these financial statements.

The accompanying notes form part of these financial statements.

92 O 2 O F I N A N C I A L R E P O R T

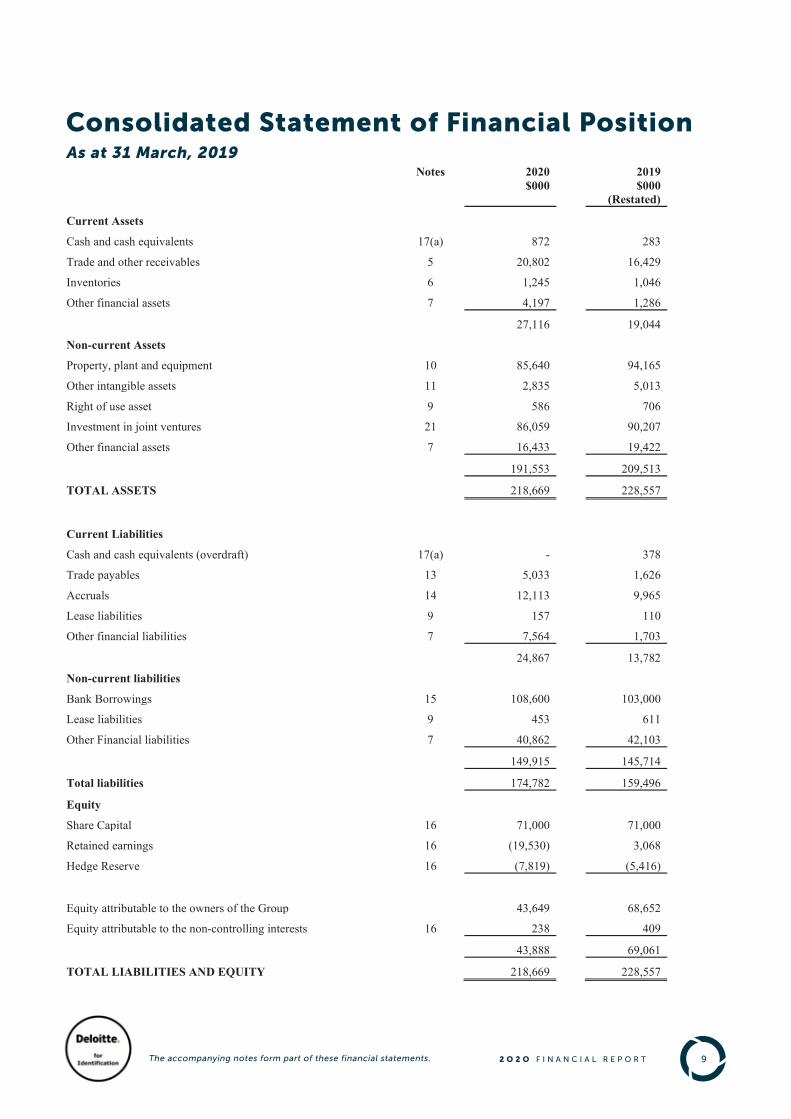

Consolidated Statement of Financial Position As at 31 March, 2019

The accompanying notes form part of these financial statements.

9

PIONEER ENERGY LIMITED CONSOLIDATED STATEMENT OF FINANCIAL POSITION As at 31 March, 2020

Notes 2020 2019

$000

$000

(Restated)

Current Assets

Cash and cash equivalents 17(a) 872 283

Trade and other receivables 5 20,802 16,429

Inventories 6 1,245 1,046

Other financial assets 7 4,197 1,286

27,116 19,044

Non-current Assets

Property, plant and equipment 10 85,640 94,165

Other intangible assets 11 2,835 5,013

Right of use asset 9 586 706

Investment in joint ventures 21 86,059 90,207

Other financial assets 7 16,433 19,422

191,553 209,513

TOTAL ASSETS 218,669 228,557

Current Liabilities

Cash and cash equivalents (overdraft) 17(a) - 378

Trade payables 13 5,033 1,626

Accruals 14 12,113 9,965

Lease liabilities 9 157 110

Other financial liabilities 7 7,564 1,703

24,867 13,782

Non-current liabilities

Bank Borrowings 15 108,600 103,000

Lease liabilities 9 453 611

Other Financial liabilities 7 40,862 42,103

149,915 145,714

Total liabilities 174,782 159,496

Equity

Share Capital 16 71,000 71,000

Retained earnings 16 (19,530) 3,068

Hedge Reserve 16 (7,819) (5,416)

Equity attributable to the owners of the Group 43,649 68,652

Equity attributable to the non-controlling interests 16 238 409

43,888 69,061

TOTAL LIABILITIES AND EQUITY 218,669 228,557 The accompanying notes form part of these financial statements.

1 02 O 2 O F I N A N C I A L R E P O R T

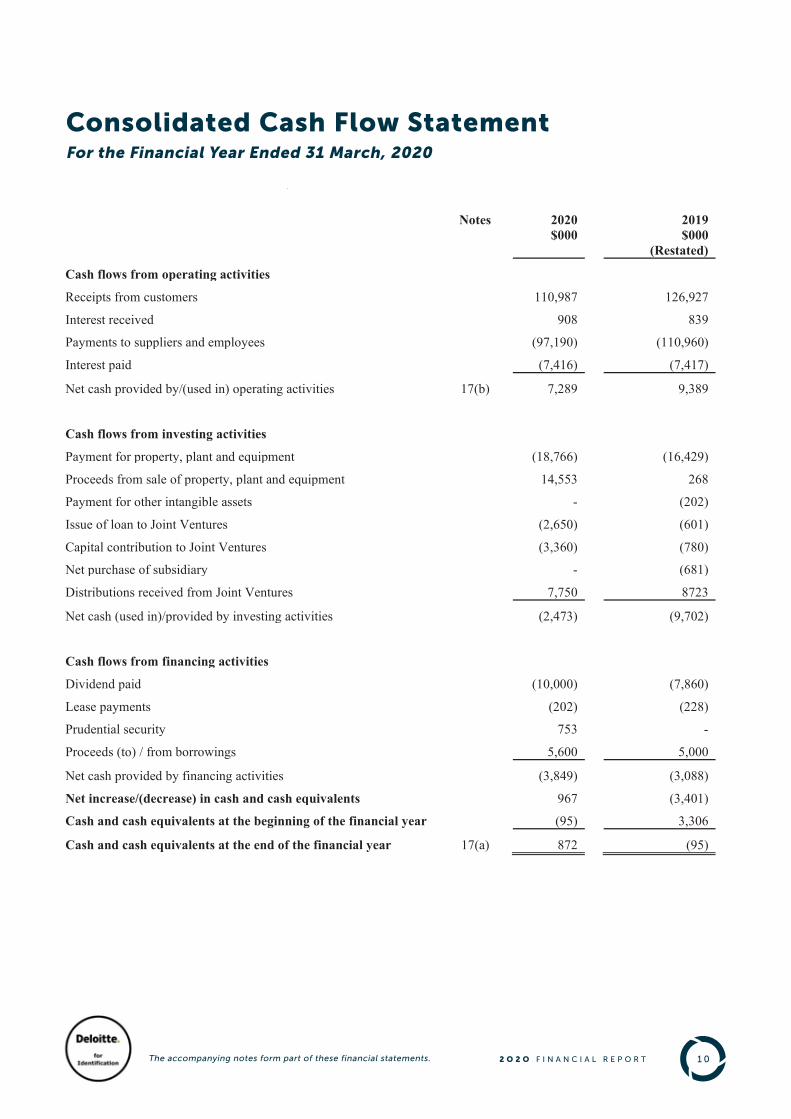

Consolidated Cash Flow StatementFor the Financial Year Ended 31 March, 2020

10

PIONEER ENERGY LIMITED CONSOLIDATED CASH FLOW STATEMENT For the Financial Year Ended 31 March, 2020

Notes 2020 2019

$000

$000

(Restated)

Cash flows from operating activities

Receipts from customers 110,987 126,927

Interest received 908 839

Payments to suppliers and employees (97,190) (110,960)

Interest paid (7,416) (7,417)

Net cash provided by/(used in) operating activities 17(b) 7,289 9,389

Cash flows from investing activities

Payment for property, plant and equipment (18,766) (16,429)

Proceeds from sale of property, plant and equipment 14,553 268

Payment for other intangible assets - (202)

Issue of loan to Joint Ventures (2,650) (601)

Capital contribution to Joint Ventures (3,360) (780)

Net purchase of subsidiary - (681)

Distributions received from Joint Ventures 7,750 8723

Net cash (used in)/provided by investing activities (2,473) (9,702)

Cash flows from financing activities

Dividend paid (10,000) (7,860)

Lease payments (202) (228)

Prudential security 753 -

Proceeds (to) / from borrowings 5,600 5,000

Net cash provided by financing activities (3,849) (3,088)

Net increase/(decrease) in cash and cash equivalents 967 (3,401)

Cash and cash equivalents at the beginning of the financial year (95) 3,306

Cash and cash equivalents at the end of the financial year 17(a) 872 (95) The accompanying notes form part of these financial statements.

The accompanying notes form part of these financial statements.

1 12 O 2 O F I N A N C I A L R E P O R T

Notes to the Consolidated Financial Statements For the Financial Year Ended 31 March, 2020

11

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

1. SUMMARY OF ACCOUNTING POLICIES

Reporting Entity

Pioneer Energy Limited (PEL, Parent, or the Company) is incorporated and domiciled in New Zealand. Its principal activities relate to the generation of electricity, owning, operating and developing small hydro power stations, wind generation and landfill gas sites and offering energy solutions for industrial clients at a range of sites throughout New Zealand. The principal objective of the Company is to operate as a successful business as defined in section 36 of the Energy Companies Act 1992. These consolidated financial statements are for the Company and its subsidiaries (together referred to as the Group).

Pioneer Energy Limited’s consolidated financial statements comply with the Financial Reporting Act 2013, the Companies Act 1993 and the Energy Companies Act 1992.

Pioneer Energy Limited is 100% owned by Central Lakes Trust. Accordingly, Central Lakes Trust is the ultimate parent of the Group.

The consolidated financial statements were authorised for issue by the directors on the 7 July 2020.

Statement of Compliance

The financial statements have been prepared in accordance with Generally Accepted Accounting Practice in New Zealand (“NZ GAAP”).

The Group is eligible to apply Tier 2 For-profit Accounting Standards (New Zealand equivalents to International Financial Reporting Standards – Reduced Disclosure Regime (‘NZ IFRS RDR’)) on the basis that it does not have public accountability and is not a large for-profit public sector entity. The Group has elected to report in accordance with NZ IFRS RDR and has applied disclosure concessions.

Basis of Preparation

The financial statements have been prepared on the basis of historical cost, except for the revaluation of certain assets and liabilities as identified in the following accounting policies. Cost is based on the fair values of the consideration given in exchange for assets.

Accounting policies are selected and applied in a manner which ensures that the resulting financial information satisfies the concepts of relevance and reliability, thereby ensuring that the substance of the underlying transactions or other events is reported.

The financial statements are presented in New Zealand dollars, rounded to the nearest thousand ($’000).

The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements.

Critical Judgements, Estimates and Assumptions

In the application of the Group’s accounting policies, the directors are required to make judgements, estimates and assumptions about carrying values of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an on-going basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

Consolidated Cash Flow Statement

1 22 O 2 O F I N A N C I A L R E P O R T

12

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

The significant judgements, estimates and assumptions made in the preparation of these financial statements are outlined below:

• Impairment Assessment of Generation and Heat Property, Plant and Equipment and Investments

At the end of each reporting period the Group assesses whether there is any indication that its assets may be impaired. In the event that any such indication exists, the Group shall estimate the recoverable amount of the assets. In the current year, to assess whether there was any indication that an assets may be impaired the Group obtained an independent valuation using the discounted cash flow model.

• Depreciation

In determining the appropriate depreciation rate to apply against property, plant and equipment management are required to make estimates regarding the useful lives and residual values of property, plant and equipment. The Group reviews the estimated useful lives of property, plant and equipment at the end of each annual reporting period. The estimates used by management in determining the depreciation rate may ultimately be different to the actual pattern of use. In the event these estimates differ to the actual pattern of use the depreciation charge recognised may be more or less than what would have been charged had this information been available at the time of determining the estimate.

• Valuation of electricity derivative financial instruments The valuation of the electricity derivative contracts relies on an internally developed pricing methodology. Agreed prices are compared against publicly available ASX and Energy Link forward hedge prices over the agreement period in order to determine a fair value of each derivative. Assumptions that can have a significant impact on the fair value are the publicly available forecasted spot price at each grid exit point and unobservable forecast volumes to be delivered.

• Borrowing Costs

Judgement has been applied to calculate the proportion of borrowings related to qualifying assets and the capitalisation period. Judgement has also been exercised to determine that borrowing costs that have been expensed are not attributable to qualifying assets.

• Investments in joint ventures Southern Generation Limited Partnership, Pulse Energy Alliance Limited Partnership, Dairy Creek Limited Partnership, Ecotricity Limited Partnership and Ecogas Limited Partnership are limited liability partnerships whose legal form confers separation between the parties to the joint arrangement and the company itself. Furthermore, there is no contractual arrangement or any other facts and circumstances that indicate that the parties to the joint arrangement have rights to the assets and obligations for the liabilities of the joint arrangement. Accordingly, Southern Generation Limited Partnership, Pulse Energy Alliance Limited Partnership, Dairy Creek Limited Partnership, Ecotricity Limited Partnership and Ecogas Limited Partnership are classified as joint ventures of the Group.

1 32 O 2 O F I N A N C I A L R E P O R T

13

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Significant Accounting Policies The following significant accounting policies have been adopted in the preparation and presentation of the financial statements:

Basis of Consolidation The consolidated financial statements incorporate the financial statements of the Group and entities (including structured entities) controlled by the Group and its subsidiaries. Control is achieved when the Group:

• Has power over the investee; • Is exposed, or has rights, to variable returns from its involvement with the investee; and • Has the ability to use its power to affect its returns.

The Group reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above.

Business Combinations Acquisitions of subsidiaries and businesses are accounted for using the purchase method. The cost of the business combination is measured as the aggregate of the fair values (at the date of exchange) of assets given, liabilities incurred or assumed, and equity instruments issued by the Group in exchange for control of the acquiree. The acquiree’s identifiable assets, liabilities and contingent liabilities that meet the conditions for recognition under NZ IFRS 3 Business Combinations are recognised at their fair values at the acquisition date, except for non-current assets (or disposal groups) that are classified as held for sale in accordance with NZ IFRS 5 Non-current Assets Held for Sale and Discontinued Operations, which are recognised and measured at fair value less costs to sell. Goodwill arising on acquisition is recognised as an asset and initially measured at cost, being the excess of the cost of the business combination over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities recognised. If, after reassessment, the Group’s interest in the net fair value of the acquiree’s identifiable assets, liabilities and contingent liabilities exceeds the cost of the business combination, the excess is recognised immediately in profit or loss. Non-controlling interests that present ownership interests and entitle their holders to a proportionate share of the entity's net assets in the event of liquidation may be initially measured either at fair value or at the non-controlling interests' proportionate share of the recognised amounts of the acquiree's identifiable net assets. The choice of measurement basis is made on a transaction-by-transaction basis. Revenue Recognition Revenue is measured at the fair value of the consideration received or receivable in relation to the below three material revenue streams, net of variable considerations i.e discounts and GST. Consumption of electricity is measured and billed each month. Payment is due in respect of the sales in the month following the service being provided. A receivable is recognised by the Group reflecting the amount owing for sales provided. Generation revenue Generation revenue relates to the sale of generation electricity from its own generation plants i.e. hydroelectric dams, wind farms and etc. This revenue is influenced by the quantity of generation and the spot price and is recognised on an accruals basis at the time of generation. Retail revenue Retail revenue relates to the sale of purchased electricity (from the national grid) to retail customers. It is derived from a wide range of contracted customers (small to large commercial, industrial and residential). This revenue is influenced by the quantity of electricity consumed and the spot price and is recognised at the time of the electricity consumption by the customer. Customer consumption of electricity is measured and billed in line with meter reading schedules for non-half hourly and half hourly metered customers, accordingly retail revenue includes an estimated accrual for services provided not billed at the end of the reporting period.

1 42 O 2 O F I N A N C I A L R E P O R T

14

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Revenue Recognition – (cont.) Energy revenue Energy revenue relates to the sale of steam, heat, coal and wood to industrial/commercial customers under fixed term contractual arrangements. Pricing has a fixed component and a variable component based on a fixed rate multiplied by the quantity of energy consumed. Energy revenue is recognised over time as the customer simultaneously receives and consumes the benefits provided using a volume-based measure. Avoided cost of transmission Avoided cost of transmission revenue is recognised over time as the distributor simultaneously receives and consumes the benefits provided by the Group’s performance of the service. Revenue is recognised as the service is provided using a time-based measure. Payment is due in respect of the avoided cost of transmission in the month following the service being provided. A receivable is recognised by the Group reflecting the amount owing for services provided. Interest income is recognised on a time proportionate basis using the effective interest method. Other Gains and Losses Net gains or losses on the sale of property plant and equipment are recognised when unconditional title has transferred, and it is probable that the Group will receive the consideration due. Leases The Group assess whether a contract is or contains a lease, at the inception of the contract. The Group recognises a right-of-use asset and a corresponding lease liability with respect to all lease arrangements in which it is the lessee, except for short-term leases, defined as leases with a lease term of 12 months or less, and leases of low value assets. For these leases, the Group recognises the lease payments as an operating expense on a straight-line basis over the term of the lease unless another systematic basis is more representative of the time pattern in which economic benefits from the leased assets are consumed. The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted by using the rate implicit in the lease. If the rate cannot be readily determined, the Group uses its incremental borrowing rate (IBR). The lease liability is subsequently measured by increasing the carrying amount to reflect interest on the liability, using the effective interest method, and by reducing the carrying amount to reflect the lease payments made. The right-of-use assets comprise the initial measurement of the corresponding lease liability, lease payments made at or before the commencement day and any initial direct costs. They are subsequently measured at cost less accumulated depreciation and impairment losses. Right-of-use assets are depreciated over the shorter period of lease term or useful life of the underlying asset. The Group applies NZ IAS 36 to determine whether a right-of-use asset is impaired and accounts for any identified impairment loss as described on page 19. The estimation of the IBR relies on the Directors considering the credit risk of the Group. If the credit risk faced by the Group differs from what is estimated, the IBR may differ, and consequently the future net present value of the lease cash flows may be over or understated. The determination of lease term relies on the Directors view of the likelihood of any lease renewal options being renewed. If the lease renewal options included and then not taken up, or are not included and are taken up, the net present value of the lease cash flows may be over or understated. Finance Costs Includes Interest expense and other expenses directly associated to bank funding. Interest expense is accrued on a time basis using the effective interest method. Borrowing Costs Borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added to the cost of those assets until such time as the assets are substantially ready for their intended use or sale. All other borrowing costs are recognised in the profit and loss in the period in which they are incurred.

1 52 O 2 O F I N A N C I A L R E P O R T

15

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Taxation As Pioneer Energy Limited’s sole shareholder is a charitable organisation and the Companies within the Group were granted exemption from Income Tax under Section CB 4(1)(e) of the Income Tax Act 1994 (replaced with Section CW 42(1) of the Income Tax Act 2007). Charitable status was effective from 23 October, 2002. Accordingly, income earned after 23 October, 2002 is exempt from taxation. Goods and Services Tax Revenues, expenses, assets and liabilities are recognised net of the amount of goods and services tax (GST), except for receivables and payables which are recognised inclusive of GST. Cash and Cash Equivalents Cash and cash equivalents comprise cash on hand and cash held in banks. Cash and Cash equivalents are initially recognised at fair value and subsequently measured at amortised cost. Trade Receivables Trade receivables are amounts due from customers for merchandise sold or services performed in the ordinary course of business. If collection is expected in one year or less (or in the normal operating cycle of the business if longer), they are classified as current assets. If not, they are presented as non-current assets. Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Collectability and change of credit risk of trade receivables is reviewed on an on-going basis. Debts which are known to be uncollectible are written off. The Group makes use of a simplified approach in accounting for trade and other receivables and records the loss allowance as lifetime expected credit losses. These are the expected shortfalls in contractual cash flows, considering the potential for default at any point during the life of the financial instrument. The Group uses its historical experience, external indicators and forward-looking information to calculate the lifetime expected credit losses (ECL). Financial Instruments Financial assets and financial liabilities are recognised on the Group’s Statement of Financial Position when the Group becomes a party to contractual provisions of the instrument. (i) Financial Assets Financial Assets are classified into the following specified categories: financial assets at fair value through profit or loss, fair value through other comprehensive income and amortised cost. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition. Amortised Cost Debt instruments that meet the following conditions are measured subsequently at amortised cost:

• the financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows; and

• the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Trade and other receivables are classified as ‘amortised cost’. Trade and other receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment. Fair Value Through Other Comprehensive Income (FVTOCI) Debt instruments that meet the following conditions are measured subsequently at fair value through other comprehensive income (FVTOCI):

• the financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling the financial assets; and

• the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

1 62 O 2 O F I N A N C I A L R E P O R T

16

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Financial Instruments (cont.) (i) Financial Assets (cont.) Financial Assets at Fair Value Through Profit or Loss (FVTPL) By default, all other financial assets are measured subsequently at fair value through profit or loss (FVTPL). Despite the foregoing, the Group may make the following irrevocable election/designation at initial recognition of a financial asset:

• the Group may irrevocably elect to present subsequent changes in fair value of an equity investment in other comprehensive income if certain criteria are met; and

• the Group may irrevocably designate a debt investment that meets the amortised cost or FVTOCI criteria as measured at FVTPL if doing so eliminates or significantly reduces an accounting mismatch.

Impairment of Financial Assets The Group recognises a loss allowance for expected credit losses on financial assets measured at amortised costs (including trade receivables and related party loans), investments in debt instruments that are measured at amortised cost or at FVTOCI, lease receivables, and contract assets, as well as on financial guarantee contracts. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition of the respective financial instrument. The Group always recognises lifetime ECL for trade receivables, contract assets and lease receivables. The expected credit losses on these financial assets are estimated using a provision matrix based on the Group’s historical credit loss experience, adjusted for factors that are specific to the debtors, general economic conditions and an assessment of both the current as well as the forecast direction of conditions at the reporting date, including time value of money where appropriate. For all other financial instruments, the Group recognises lifetime ECL when there has been a significant increase in credit risk since initial recognition. However, if the credit risk on the financial instrument has not increased significantly since initial recognition, the Group measures the loss allowance for that financial instrument at an amount equal to 12‑month ECL. Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast, 12‑month ECL represents the portion of lifetime ECL that is expected to result from default events on a financial instrument that are possible within 12 months after the reporting date. The Group writes off a financial asset when there is information indicating that the debtor is in severe financial difficulty and there is no realistic prospect of recovery, e.g. when the debtor has been placed under liquidation or has entered into bankruptcy proceedings, or in the case of trade receivables, when the amounts are over two years past due, whichever occurs sooner. Financial assets written off may still be subject to enforcement activities under the Group’s recovery procedures, taking into account legal advice where appropriate. Any recoveries made are recognised in profit or loss. (ii) Financial Liabilities Trade and Other Payables Trade payables and other accounts payable are recognised when the Group becomes obliged to make future payments resulting from the purchase of goods and services. Trade and other payables are initially recognised at fair value and are subsequently measured at amortised cost, using the effective interest method. Borrowings Borrowings are recorded initially at fair value, net of transaction costs. Subsequent to initial recognition, borrowings are measured at amortised cost with any difference between the initial recognised amount and the redemption value being recognised in the Income Statement over the period of the borrowing using the effective interest method.

1 72 O 2 O F I N A N C I A L R E P O R T

17

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Financial Instruments (cont.) (iii) Derivative Financial Instruments The Group enters into certain derivative financial instruments (electricity contracts) to manage its exposure to movements in the spot price for electricity. The Group also enters into certain derivative financial instruments to manage its exposure to movements in the foreign exchange rate and interest rates. The Group does not hold derivative financial instruments for speculative purposes. Derivatives are initially recognised at fair value on the date a derivative contract is entered into and are subsequently remeasured to their fair value at each balance date. The resulting gain or loss is recognised in profit and loss immediately unless the derivative is designated and effective as a hedging instrument, in which event, the timing of the recognition in profit and loss depends on the nature of the hedge relationship. Realised gains and losses are recognised within generation revenue on an accruals basis for electricity contracts. A derivative with a positive fair value is recognised as a financial asset whereas a derivative with a negative fair value is recognised as a financial liability. A derivative is presented as a non‑current asset or a non‑current liability if the remaining maturity of the instrument is more than 12 months and it is not expected to be realised or settled within 12 months. Other derivatives are presented as current assets or current liabilities. The electricity derivatives are not designated as an effective hedge relationship. The foreign currency forward contracts and interest rate swaps are accounted for as effective cash flow hedges. At the inception of the hedge relationship, the Group documents the relationship between the hedging instrument and the hedged item, along with its risk management objectives and its strategy for undertaking various hedge transactions. Furthermore, at the inception of the hedge and on an ongoing basis, the Group documents whether the hedging instrument is effective in offsetting changes in fair values or cash flows of the hedged item attributable to the hedged risk, which is when the hedging relationships meet all of the following hedge effectiveness requirements:

• there is an economic relationship between the hedged item and the hedging instrument; • the effect of credit risk does not dominate the value changes that result from that economic relationship; and • the hedge ratio of the hedging relationship is the same as that resulting from the quantity of the hedged item that the

Group actually hedges and the quantity of the hedging instrument that the Group actually uses to hedge that quantity of hedged item.

Hedge accounting is discontinued when the hedging instrument expires or is sold, terminated or exercised, or no longer qualifies for hedge accounting. The effective portion of changes in the fair value of foreign currency forward contracts and interest rate swaps that are hedge accounted are designated as cash flow hedges and are recognised in other comprehensive income and accumulate as a separate component of equity in the hedging reserve. The gain or loss relating to the ineffective portion is recognised immediately in profit or loss. Changes in the fair value of the foreign currency forward contracts that are not hedge accounted are recorded in the profit and loss. Inventories Inventories are valued at the lower of cost and net realisable value.

1 82 O 2 O F I N A N C I A L R E P O R T

18

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Property, Plant & Equipment Cost Property, plant and equipment is recorded at cost less accumulated depreciation and any accumulated impairment losses. Cost includes expenditure that is directly attributable to the acquisition of the assets and capitalised borrowing costs. Where an asset is acquired for no cost, or for a nominal cost, it is recognised at fair value at the date of acquisition. Depreciation Depreciation is provided on straight-line basis for the heat plant assets. For all other assets, both the diminishing value and straight-line method have been adopted using the respective rates set out below. Expenditure incurred to maintain these assets at full operating capability is charged to the Consolidated Income Statement in the period incurred. Any capital expenditure incurred subsequent to the commissioning of fixed assets is capitalised to the asset at the time it is incurred. The cost of internally constructed assets comprises direct labour, materials, transport and overhead apportioned on the basis of labour and plant costs. The estimated useful lives of the major asset classes have been estimated as follows:

Rate Method Land Nil Land improvements 1.5 - 11.4% DV& SL Buildings and civil Assets 2 - 15% DV& SL Computer equipment 4 - 100% DV& SL Furniture & fittings 7.8 - 100% DV& SL Generation plant 1 - 80.4% DV& SL Heat plant 8 - 44% SL Motor vehicles 8 - 21.6% DV& SL Office equipment 7 - 48% DV& SL Other equipment & tools 8 - 67% DV& SL

The estimated useful lives, residual values and depreciation method are reviewed at the end of each annual reporting period. Disposal An item of property, plant and equipment is derecognised upon disposal or recognised as impaired when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on de-recognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the Consolidated Income Statement in the period the asset is derecognised. Assets Classified as Held for Sale Non-current assets are classified as held for sale if their carrying amount will be recovered principally through a sale transaction rather than through continuing use. This condition is regarded as met only when the asset (or disposal group) is available for immediate sale in its present condition subject only to terms that are usual and customary for sales of such asset (or disposal group) and its sale is highly probable. Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classification. Non-current assets classified as held for sale are measured at the lower of their previous carrying amount and fair value less costs to sell.

1 92 O 2 O F I N A N C I A L R E P O R T

19

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Intangible Assets Intangible Assets Separately Acquired Intangible assets acquired separately are reported at cost less accumulated amortisation and accumulated impairment losses. Amortisation is charged on a straight-line basis over their estimated useful lives. The estimated useful lives, residual values and amortisation method are reviewed at the end of each reporting period, with the effect of any changes in estimate being accounted for on a prospective basis.

• Computer software up to 3 years • Matiri consent up to 30 years • Retail up to 5 years • Asset management up to 7 years

Intangible Asset Acquired in a Business Combination Finite life intangible assets acquired in a business combination are identified and recognised separately from goodwill where they satisfy the definition of an intangible asset and their fair values can be measured reliably. The cost of such intangible assets is their fair value at the acquisition date. Subsequent to initial recognition, intangible assets acquired in a business combination are reported at cost less accumulated amortisation and accumulated impairment losses, on the same basis as intangible assets acquired separately.

• Customer contract (Heat Supply contract – Bromley, Christchurch) up to 13 years • Rights to Silverstream LFG (Consent to extract gas) up to 25 years • Customer Acquisition (Electricity supply contracts as purchased) up to 8 years

Impairment of Non-Financial Assets excluding Goodwill At each balance date or when events or changes in circumstances indicate that the carrying amount exceeds its recoverable amount, the Group reviews the recoverability of the carrying amounts of its tangible and intangible assets to determine whether they have suffered an impairment loss. The recoverable amount is the higher of an asset’s fair value less costs to sell, and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows that are largely independent of the cash flows from other assets or group of assets (cash generating units). An impairment loss is recognised immediately in the Consolidated Income Statement, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease. Non-financial assets that suffered impairment are reviewed for possible reversal of the impairment at each reporting date. A reversal of an impairment loss is recognised immediately in the Consolidated Income Statement, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase. Provisions Provisions are recognised when the Group has a present obligation arising from past events, the future sacrifice of economic benefits is probable, and the amount of the provision can be measured reliably. The amount recognised as a provision is the best estimate of the consideration required to settle the present obligation at reporting date, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows. When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognised as an asset if it is virtually certain that recovery will be received, and the amount of the receivable can be measured reliably.

2 02 O 2 O F I N A N C I A L R E P O R T

20

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Employee Benefits Provision is made for benefits accruing to employees in respect of wages and salaries, annual leave, long service leave, and sick leave when it is probable that settlement will be required, and the cost is capable of being measured reliably. Provisions made in respect of employee benefits expected to be settled within 12 months are measured at their nominal values using the remuneration rate expected to apply at the time of settlement. Provisions made in respect of employee benefits which are not expected to be settled within 12 months are measured as the present value of the estimated future cash outflows to be made by the Group in respect of services provided by employees up to reporting date. Cash Flow Statement Operating activities include cash received from all income sources of the Group and record the cash payments made for the supply of goods and services. Investing activities are those activities relating to the acquisition and disposal of non-current assets. Financing activities comprise the change in equity and debt structure of the Group. Investment in Joint Ventures A joint venture is a joint arrangement whereby the parties that have joint control of the arrangement have rights to the net assets of the joint arrangement. Joint control is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require unanimous consent of the parties sharing control. The results and assets and liabilities of joint ventures are incorporated in these consolidated financial statements using the equity method of accounting, except when the investment, or a portion thereof, is classified as held for sale, in which case it is accounted for in accordance with NZ IFRS 5. Under the equity method, an investment in a joint venture is initially recognised in the consolidated statement of financial position at cost and adjusted thereafter to recognise the Group's share of the profit or loss and other comprehensive income of the joint venture. When the Group's share of losses of a joint venture exceeds the Group's interest in that joint venture (which includes any long-term interests that, in substance, form part of the Group's net investment in the joint venture), the Group discontinues recognising its share of further losses. Additional losses are recognised only to the extent that the Group has incurred legal or constructive obligations or made payments on behalf of the joint venture. An investment in a joint venture is accounted for using the equity method from the date on which the investee becomes a joint venture. On acquisition of the investment in a joint venture, any excess of the cost of the investment over the Group's share of the net fair value of the identifiable assets and liabilities of the investee is recognised as goodwill, which is included within the carrying amount of the investment. Any excess of the Group's share of the net fair value of the identifiable assets and liabilities over the cost of the investment, after reassessment, is recognised immediately in profit or loss in the period in which the investment is acquired. When a group entity transacts with a joint venture of the Group, profits and losses resulting from the transactions with the associate or joint venture are recognised in the Group's consolidated financial statements only to the extent of interests in joint venture that are not related to the Group. Comparatives When the presentation or classification of items is changed, comparative amounts are reclassified unless the reclassification is impracticable.

2 12 O 2 O F I N A N C I A L R E P O R T

21

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Changes in accounting policies and disclosures In the current period, the Group, for the first time, has applied NZ IFRS 16 Leases (as issued by the IASB in January 2016). NZ IFRS 16 introduces new or amended requirements with respect to lease accounting. It introduces significant changes to the lessee accounting by removing the distinction between operating and finance leases and requiring the recognition of a right-of-use asset and a lease liability at commencement for all leases, except for short-term leases and leases of low value assets. Details of the new requirements and impact of the adoption of NZ IFRS 16 on the Group’s consolidated financial statements are described in note 9. The date of initial application of NZ IFRS 16 for the Group is 1 April 2019. The Group has applied NZ IFRS 16 using the full retrospective approach, with restatement of prior periods. The effect of this change is discussed in note 9. Impact of the new definition of a lease The Group has made use of the practical expedient available on transition to NZ IFRS 16 not to reassess whether a contract is or may contain a lease. Accordingly, the definition of a lease in accordance with IAS 17 and IFRIC 4 will continue to be applied to those leases entered or modified before 1 April 2019. The change in definition of a lease mainly relates to the concept of control. NZ IFRS 16 determines whether a contract contains a lease on the basis of whether the customer has the right to control the use of an identified asset for a period of time in exchange for consideration. The Group applies the definition of a lease and related guidance set out in NZ IFRS 16 to all lease contracts entered into or modified on or after 1 April 2019. The first time application of NZ IFRS 16 does not significantly change the scope of contracts that meet the definition of a lease for the Group. Impact on lessee accounting NZ IFRS 16 changes how the Group accounts for leases previously classified as operating leases under NZ IAS 17, which were off balance sheet. Applying NZ IFRS 16 for all leases, except as noted below, the Group:

• Recognises right-of-use assets and lease liabilities in the balance sheet, initially measured at the present value of future lease payments;

• Recognises depreciation of right-of-use assets and interest on lease liabilities in the statement of comprehensive income; and

• Separates the total amount of cash paid into a principal portion, presented within financing activities, and interest, presented within operating activities, in the Consolidated Statement of Cash Flows.

Under NZ IFRS 16, right-of-use assets are tested for impairment in accordance with NZ IAS 36 Impairment of Assets. This replaces the previous requirement to recognise a provision for onerous lease contracts. For short-term leases with a lease term of 12 months or less, and leases of low-value assets, such as personal computers and office furniture, the Group has opted to apply the recognition exemption as allowed under NZ IFRS 16 and recognise the lease expense on a straight line basis. The expense is presented within other expenses in the Consolidated Statement of Financial Performance. The main difference between NZ IFRS 16 and NZ IAS 17 with respect to assets formally held under a finance lease is the measurement of residual value guarantees provided by a lessee to a lessor. NZ IFRS 16 requires that the Group recognises as part of if its lease liability only the amount expected to be payable under a residual value guarantee, rather than the maximum amount guaranteed as required by NZ IAS 17. This change did not have a material effect on the Group’s consolidated financial statements.

2 22 O 2 O F I N A N C I A L R E P O R T

22

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 1. SUMMARY OF ACCOUNTING POLICIES (CONT.)

Standards and Interpretations in Issue Not Yet Adopted There are no NZ IFRS standards or interpretations that are not yet effective that would be expected to have a material impact on the Company.

2 32 O 2 O F I N A N C I A L R E P O R T

23

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

Notes 2020 2019

$000 $000

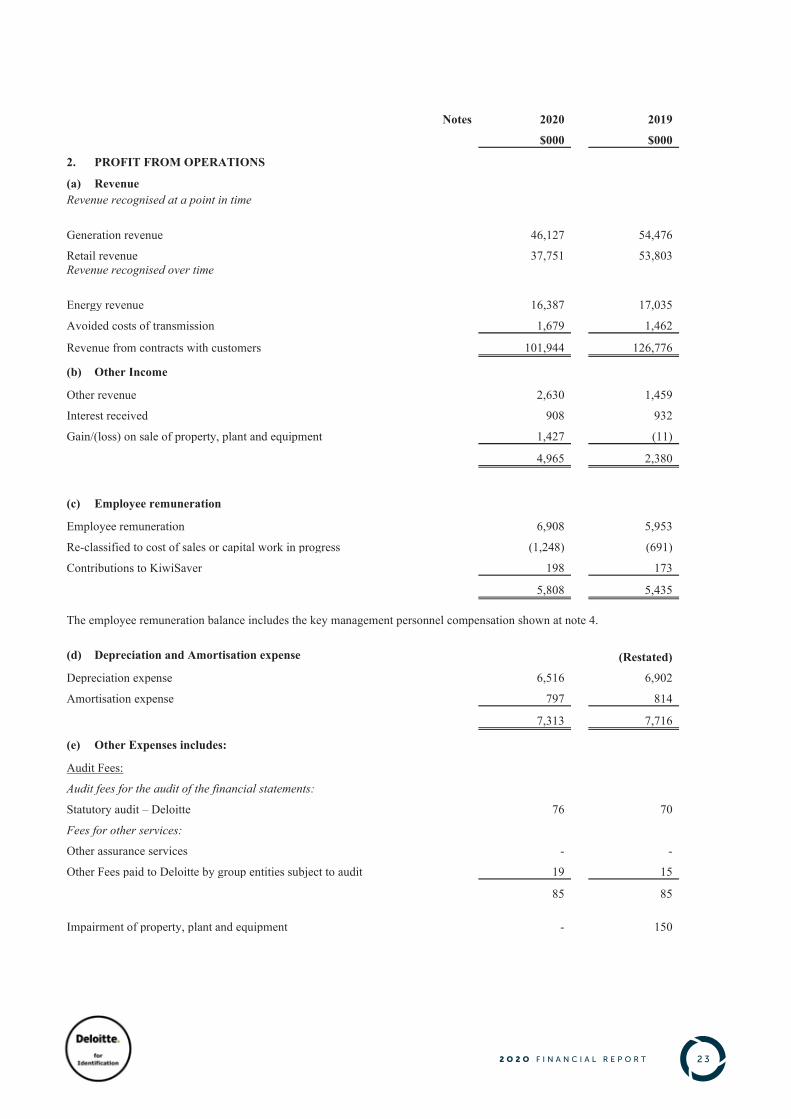

2. PROFIT FROM OPERATIONS

(a) Revenue Revenue recognised at a point in time

Generation revenue 46,127 54,476

Retail revenue 37,751 53,803 Revenue recognised over time

Energy revenue 16,387 17,035

Avoided costs of transmission 1,679 1,462

Revenue from contracts with customers 101,944 126,776

(b) Other Income

Other revenue 2,630 1,459

Interest received 908 932

Gain/(loss) on sale of property, plant and equipment 1,427 (11)

4,965 2,380

(c) Employee remuneration

Employee remuneration 6,908 5,953

Re-classified to cost of sales or capital work in progress (1,248) (691)

Contributions to KiwiSaver 198 173

5,808 5,435

The employee remuneration balance includes the key management personnel compensation shown at note 4.

(d) Depreciation and Amortisation expense (Restated)

Depreciation expense 6,516 6,902

Amortisation expense 797 814

7,313 7,716

(e) Other Expenses includes:

Audit Fees:

Audit fees for the audit of the financial statements:

Statutory audit – Deloitte 76 70

Fees for other services:

Other assurance services - -

Other Fees paid to Deloitte by group entities subject to audit 19 15

85 85 Impairment of property, plant and equipment - 150

2 42 O 2 O F I N A N C I A L R E P O R T

24

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

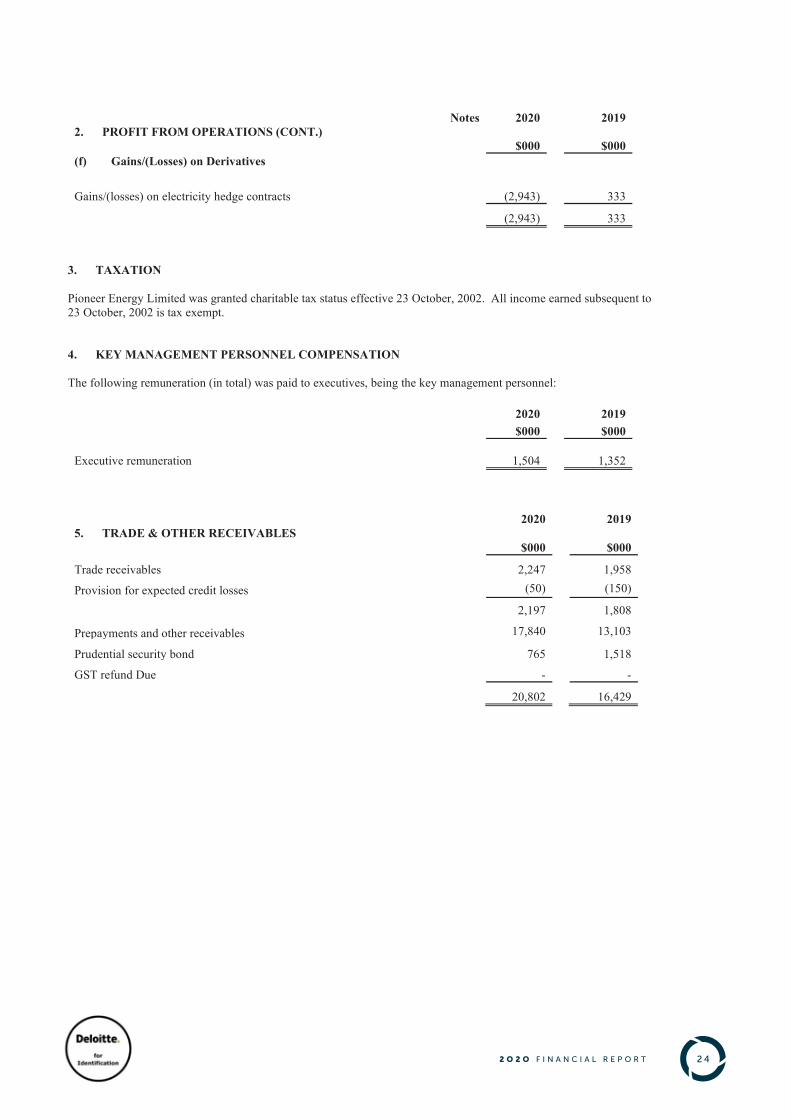

Notes 2020 2019 2. PROFIT FROM OPERATIONS (CONT.) $000 $000 (f) Gains/(Losses) on Derivatives

Gains/(losses) on electricity hedge contracts (2,943) 333

(2,943) 333

3. TAXATION Pioneer Energy Limited was granted charitable tax status effective 23 October, 2002. All income earned subsequent to 23 October, 2002 is tax exempt. 4. KEY MANAGEMENT PERSONNEL COMPENSATION The following remuneration (in total) was paid to executives, being the key management personnel:

2020 2019 $000 $000

Executive remuneration

1,504 1,352

2020 2019 5. TRADE & OTHER RECEIVABLES

$000 $000

Trade receivables 2,247 1,958

Provision for expected credit losses (50) (150)

2,197 1,808

Prepayments and other receivables 17,840 13,103

Prudential security bond 765 1,518

GST refund Due - -

20,802 16,429

2 52 O 2 O F I N A N C I A L R E P O R T

25

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

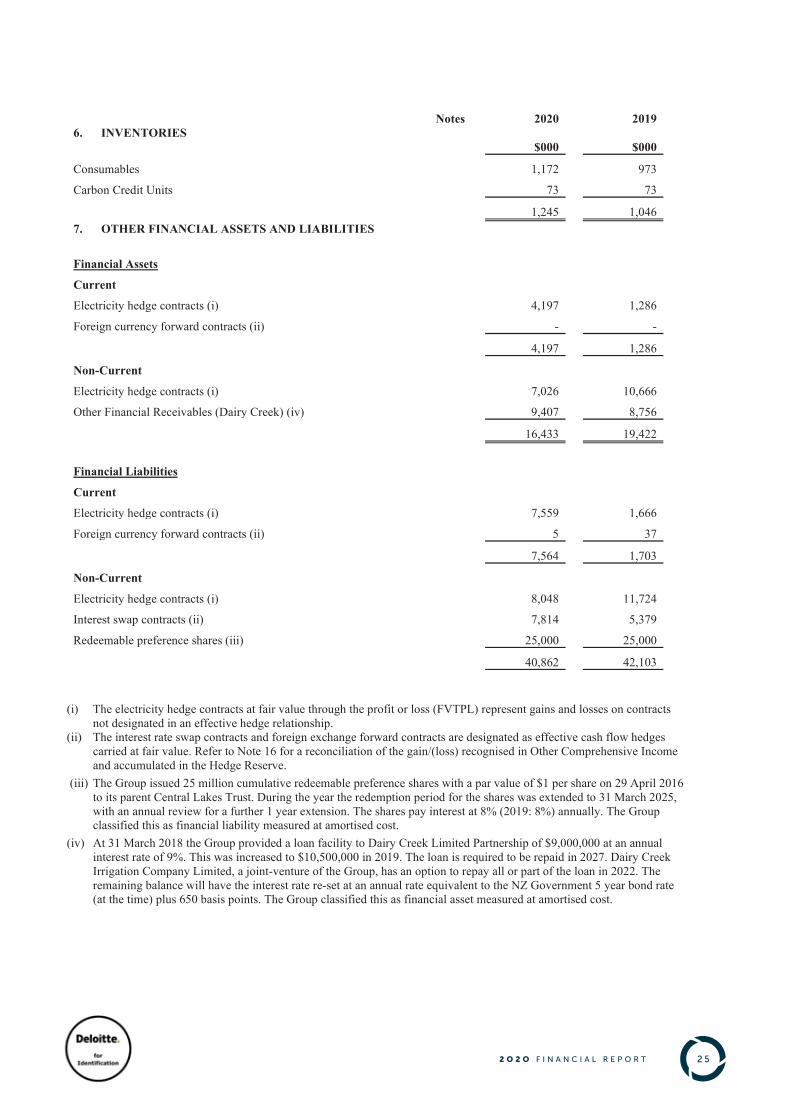

Notes 2020 2019 6. INVENTORIES

$000 $000

Consumables 1,172 973

Carbon Credit Units 73 73

1,245 1,046 7. OTHER FINANCIAL ASSETS AND LIABILITIES

Financial Assets

Current

Electricity hedge contracts (i) 4,197 1,286

Foreign currency forward contracts (ii) - -

4,197 1,286

Non-Current

Electricity hedge contracts (i) 7,026 10,666

Other Financial Receivables (Dairy Creek) (iv) 9,407 8,756

16,433 19,422 Financial Liabilities

Current

Electricity hedge contracts (i) 7,559 1,666

Foreign currency forward contracts (ii) 5 37

7,564 1,703

Non-Current

Electricity hedge contracts (i) 8,048 11,724

Interest swap contracts (ii) 7,814 5,379

Redeemable preference shares (iii) 25,000 25,000

40,862 42,103

(i) The electricity hedge contracts at fair value through the profit or loss (FVTPL) represent gains and losses on contracts

not designated in an effective hedge relationship. (ii) The interest rate swap contracts and foreign exchange forward contracts are designated as effective cash flow hedges

carried at fair value. Refer to Note 16 for a reconciliation of the gain/(loss) recognised in Other Comprehensive Income and accumulated in the Hedge Reserve.

(iii) The Group issued 25 million cumulative redeemable preference shares with a par value of $1 per share on 29 April 2016 to its parent Central Lakes Trust. During the year the redemption period for the shares was extended to 31 March 2025, with an annual review for a further 1 year extension. The shares pay interest at 8% (2019: 8%) annually. The Group classified this as financial liability measured at amortised cost.

(iv) At 31 March 2018 the Group provided a loan facility to Dairy Creek Limited Partnership of $9,000,000 at an annual interest rate of 9%. This was increased to $10,500,000 in 2019. The loan is required to be repaid in 2027. Dairy Creek Irrigation Company Limited, a joint-venture of the Group, has an option to repay all or part of the loan in 2022. The remaining balance will have the interest rate re-set at an annual rate equivalent to the NZ Government 5 year bond rate (at the time) plus 650 basis points. The Group classified this as financial asset measured at amortised cost.

2 62 O 2 O F I N A N C I A L R E P O R T

26

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

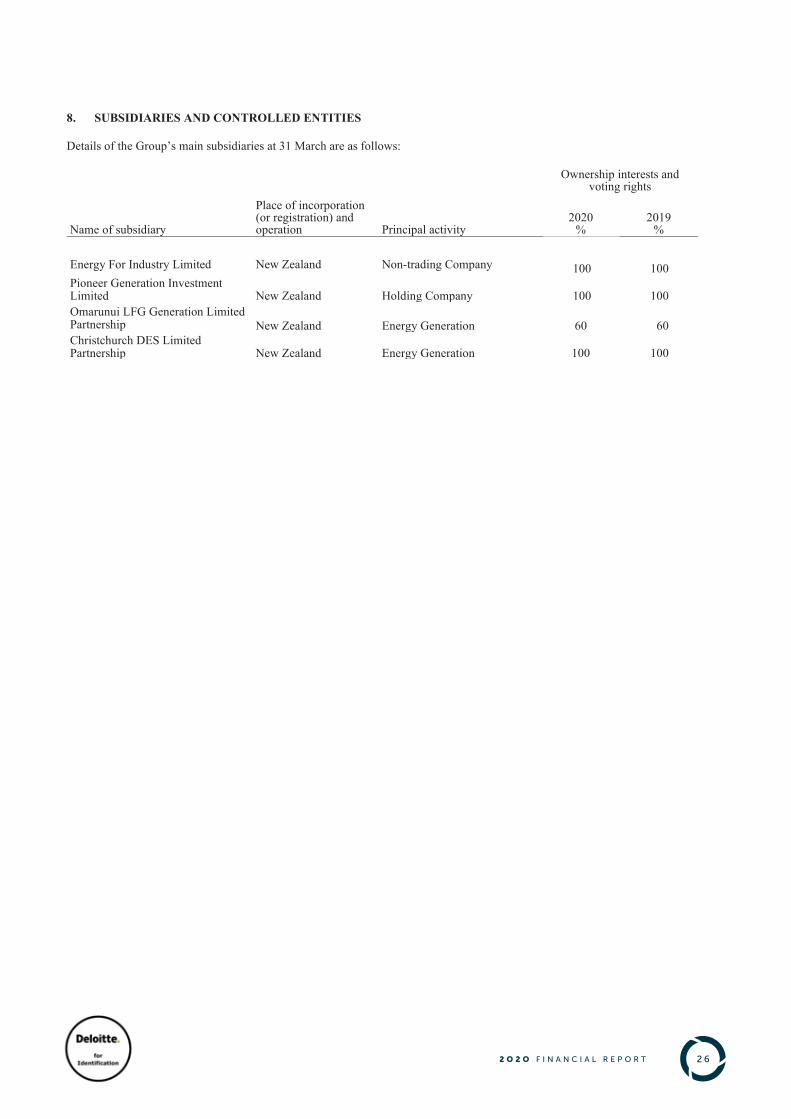

8. SUBSIDIARIES AND CONTROLLED ENTITIES Details of the Group’s main subsidiaries at 31 March are as follows:

Ownership interests and

voting rights

Name of subsidiary

Place of incorporation (or registration) and operation Principal activity

2020 %

2019 %

Energy For Industry Limited New Zealand Non-trading Company 100 100 Pioneer Generation Investment Limited

New Zealand

Holding Company 100 100

Omarunui LFG Generation Limited Partnership New Zealand Energy Generation 60

60

Christchurch DES Limited Partnership

New Zealand

Energy Generation 100 100

27

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

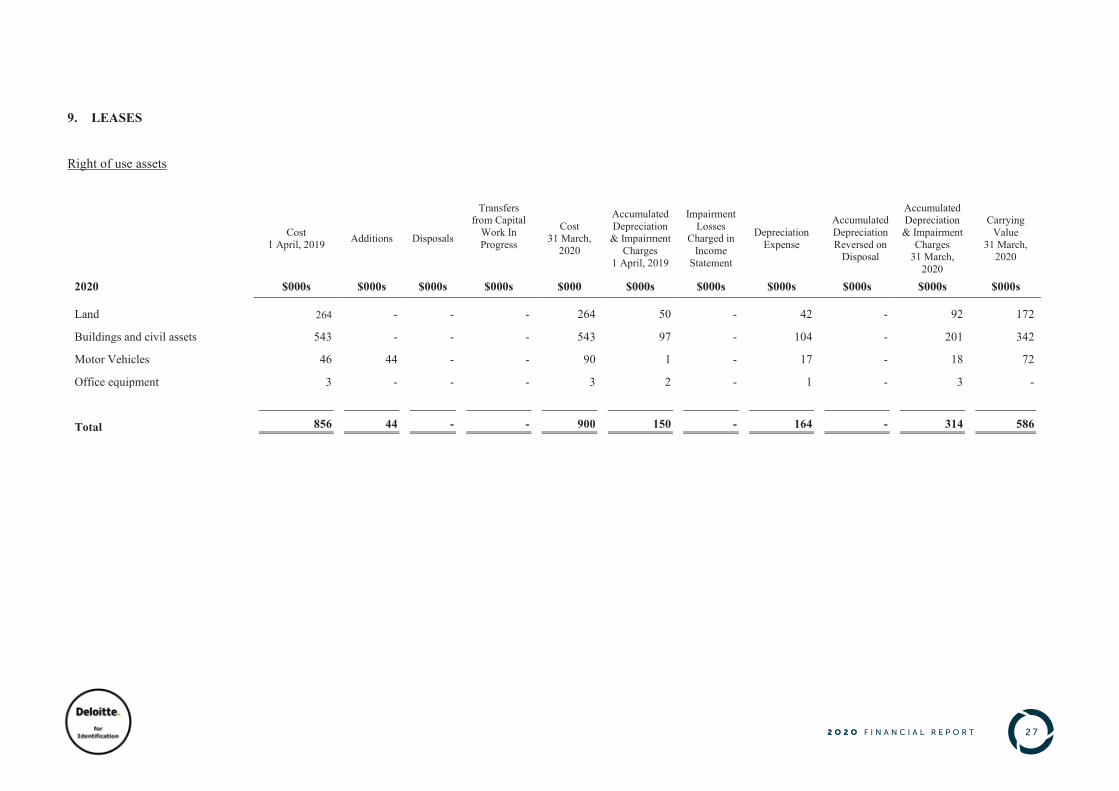

9. LEASES Right of use assets

Cost 1 April, 2019 Additions Disposals

Transfers from Capital

Work In Progress

Cost 31 March,

2020

Accumulated Depreciation

& Impairment Charges

1 April, 2019

Impairment Losses

Charged in Income

Statement

Depreciation Expense

Accumulated Depreciation Reversed on

Disposal

Accumulated Depreciation

& Impairment Charges

31 March, 2020

Carrying Value

31 March, 2020

2020 $000s $000s $000s $000s $000 $000s $000s $000s $000s $000s $000s

Land 264 - - - 264 50 - 42 - 92 172

Buildings and civil assets 543 - - - 543 97 - 104 - 201 342

Motor Vehicles 46 44 - - 90 1 - 17 - 18 72

Office equipment 3 - - - 3 2 - 1 - 3 -

Total 856 44 - - 900 150 - 164 - 314 586

2 72 O 2 O F I N A N C I A L R E P O R T

2 82 O 2 O F I N A N C I A L R E P O R T

28

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

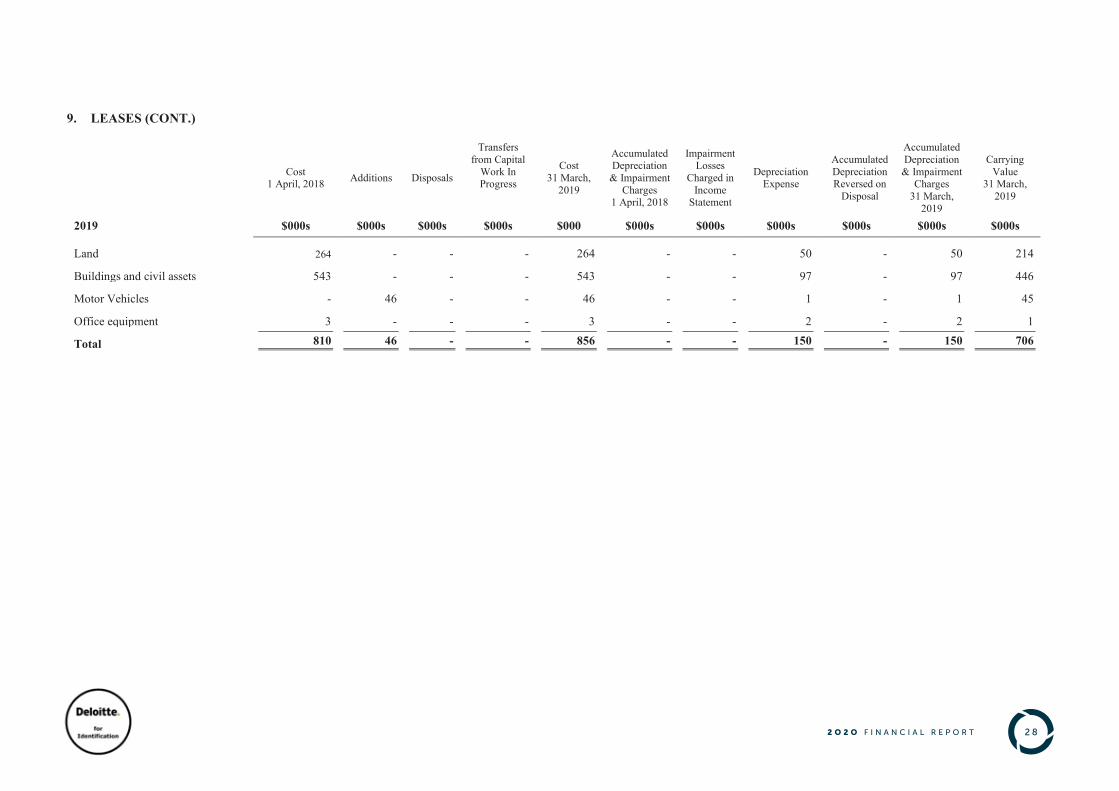

9. LEASES (CONT.)

Cost 1 April, 2018 Additions Disposals

Transfers from Capital

Work In Progress

Cost 31 March,

2019

Accumulated Depreciation

& Impairment Charges

1 April, 2018

Impairment Losses

Charged in Income

Statement

Depreciation Expense

Accumulated Depreciation Reversed on

Disposal

Accumulated Depreciation

& Impairment Charges

31 March, 2019

Carrying Value

31 March, 2019

2019 $000s $000s $000s $000s $000 $000s $000s $000s $000s $000s $000s

Land 264 - - - 264 - - 50 - 50 214

Buildings and civil assets 543 - - - 543 - - 97 - 97 446

Motor Vehicles - 46 - - 46 - - 1 - 1 45

Office equipment 3 - - - 3 - - 2 - 2 1

Total 810 46 - - 856 - - 150 - 150 706

2 92 O 2 O F I N A N C I A L R E P O R T

29

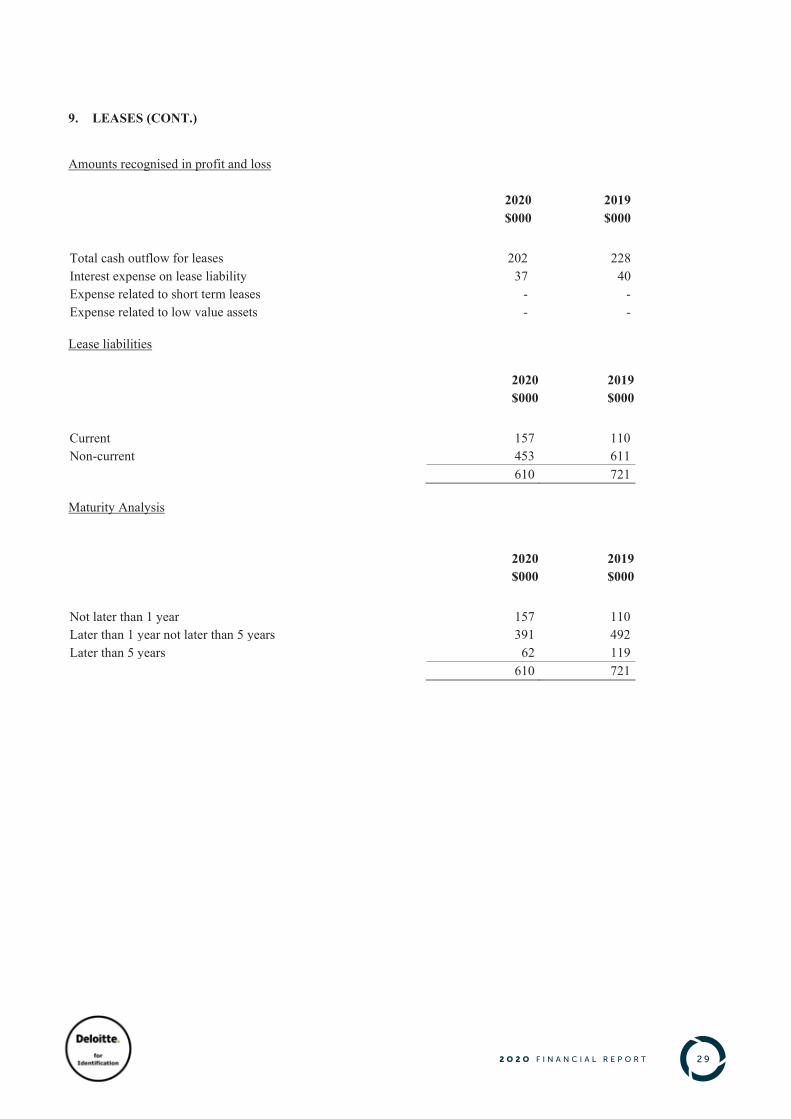

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 9. LEASES (CONT.) Amounts recognised in profit and loss

2020 2019

$000 $000

Total cash outflow for leases 202 228 Interest expense on lease liability 37 40 Expense related to short term leases - - Expense related to low value assets - - Lease liabilities

2020 2019

$000 $000

Current 157 110 Non-current 453 611

610 721 Maturity Analysis

2020 2019

$000 $000

Not later than 1 year 157 110 Later than 1 year not later than 5 years 391 492 Later than 5 years 62 119

610 721

3 02 O 2 O F I N A N C I A L R E P O R T

30

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 9. LEASES (CONT.) Transition to NZ IFRS 16 The Group has adopted NZ IFRS 16 on 1 April 2018 using the full retrospective method and as such have not restated comparatives. At transition, lease liabilities were measured at the present value of the remaining lease payments, discounted at the Group’s weighted average incremental borrowing rate (IBR). Management has reviewed applicable leases for renewal options and any options have been assessed on a case by case basis on the likelihood of being renewed. Right-of-use assets at the date of initial application for leases previously classified as operating leases have been calculated as an amount equal to the lease liability, plus any prepaid lease payments or less accrued lease payments. Other practical expedients applied by the Group in measuring the lease liabilities and right-of-use assets at transition are the following:

• The practical expedient that states that an entity is not required to reassess whether a contract is, or contains, a lease at the date of initial application;

• The Group excluded initial direct costs for any existing leases; • The Group excluded leases with a term that ended during the period; • The Group has applied a single discount rate to leases in similar jurisdictions and with similar lease terms.

Impact of adoption of NZ IFRS 16 The adoption of NZ IFRS 16 has had an immaterial impact on the statement of financial performance of the Group. The fully retrospective application of NZ IFRS 16 results in the combined depreciation and interest expense for any lease in the early years of its term being higher than the operating expense previously recognised. The impact of the retrospective application of NZ IFRS 16 on the 2019 statement of financial performance from the previously reported balances is; an increase in depreciation expense of $150,000, an increase in finance costs of $40,000 and a decrease in other expenses of $175,000. This has resulted in a $15,000 decrease in the previously reported 2019 net surplus. The adoption of NZ IFRS 16 has had no net impact on the Group’s statement of cash flows, however it has resulted in the reclassification of cash flows from lease arrangements. Payments for operating leases under NZ IAS 17 were included within ‘payments to suppliers and employees’ in operating cash flows. Payments for leases are now split between payments for interest, included in operating cash flows, and payments that reduce the principal balance of a lease liability, included in financing cash flows. The adoption of NZ IFRS 16 has had an immaterial impact on the statement of financial position of the Group. For the restated balance sheet as at 31 March 2019, this includes an increase in total assets by $706,000 and total liabilities by $721,000, with a $150,000 reduction in retained earnings. The decrease in retained earnings is as a result of the acceleration of lease interest expense in the early years of leases.

31

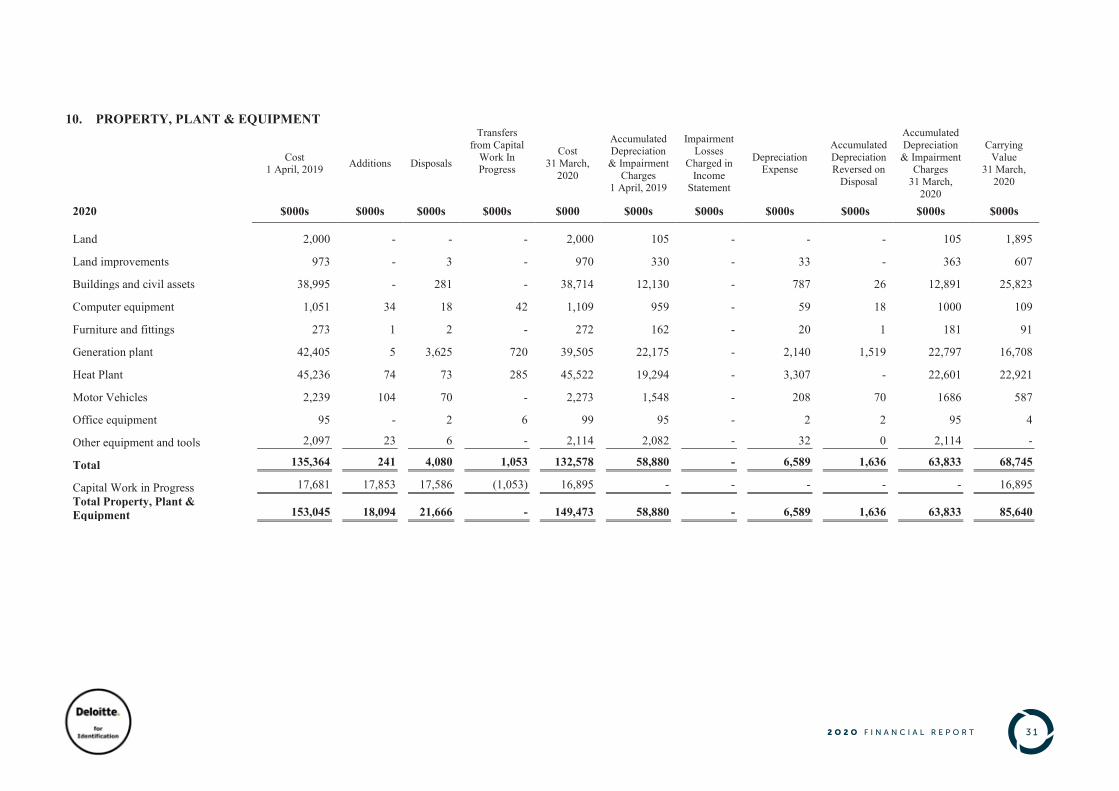

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 10. PROPERTY, PLANT & EQUIPMENT

Cost 1 April, 2019 Additions Disposals

Transfers from Capital

Work In Progress

Cost 31 March,

2020

Accumulated Depreciation

& Impairment Charges

1 April, 2019

Impairment Losses

Charged in Income

Statement

Depreciation Expense

Accumulated Depreciation Reversed on

Disposal

Accumulated Depreciation

& Impairment Charges

31 March, 2020

Carrying Value

31 March, 2020

2020 $000s $000s $000s $000s $000 $000s $000s $000s $000s $000s $000s

Land 2,000 - - - 2,000 105 - - - 105 1,895

Land improvements 973 - 3 - 970 330 - 33 - 363 607

Buildings and civil assets 38,995 - 281 - 38,714 12,130 - 787 26 12,891 25,823

Computer equipment 1,051 34 18 42 1,109 959 - 59 18 1000 109

Furniture and fittings 273 1 2 - 272 162 - 20 1 181 91

Generation plant 42,405 5 3,625 720 39,505 22,175 - 2,140 1,519 22,797 16,708

Heat Plant 45,236 74 73 285 45,522 19,294 - 3,307 - 22,601 22,921

Motor Vehicles 2,239 104 70 - 2,273 1,548 - 208 70 1686 587

Office equipment 95 - 2 6 99 95 - 2 2 95 4

Other equipment and tools 2,097 23 6 - 2,114 2,082 - 32 0 2,114 -

Total 135,364 241 4,080 1,053 132,578 58,880 - 6,589 1,636 63,833 68,745

Capital Work in Progress 17,681 17,853 17,586 (1,053) 16,895 - - - - - 16,895 Total Property, Plant & Equipment 153,045 18,094 21,666 - 149,473 58,880 - 6,589 1,636 63,833 85,640

3 12 O 2 O F I N A N C I A L R E P O R T

3 22 O 2 O F I N A N C I A L R E P O R T

32

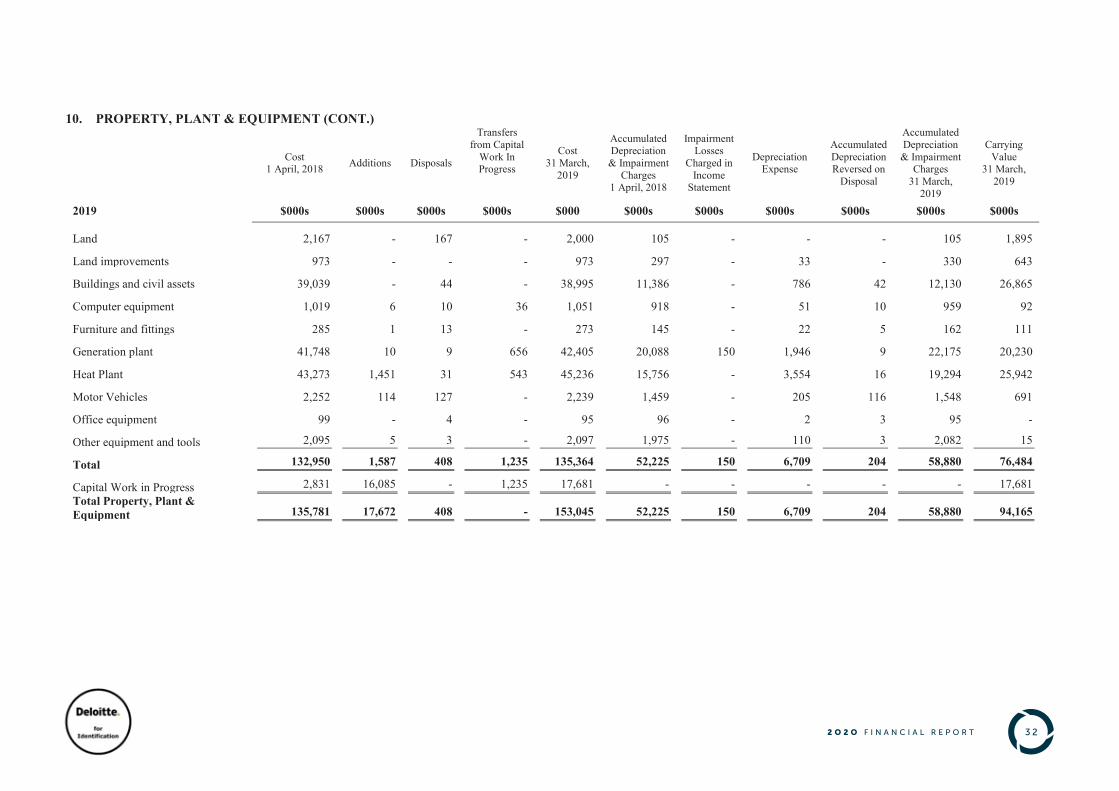

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 10. PROPERTY, PLANT & EQUIPMENT (CONT.)

Cost 1 April, 2018 Additions Disposals

Transfers from Capital

Work In Progress

Cost 31 March,

2019

Accumulated Depreciation

& Impairment Charges

1 April, 2018

Impairment Losses

Charged in Income

Statement

Depreciation Expense

Accumulated Depreciation Reversed on

Disposal

Accumulated Depreciation

& Impairment Charges

31 March, 2019

Carrying Value

31 March, 2019

2019 $000s $000s $000s $000s $000 $000s $000s $000s $000s $000s $000s

Land 2,167 - 167 - 2,000 105 - - - 105 1,895

Land improvements 973 - - - 973 297 - 33 - 330 643

Buildings and civil assets 39,039 - 44 - 38,995 11,386 - 786 42 12,130 26,865

Computer equipment 1,019 6 10 36 1,051 918 - 51 10 959 92

Furniture and fittings 285 1 13 - 273 145 - 22 5 162 111

Generation plant 41,748 10 9 656 42,405 20,088 150 1,946 9 22,175 20,230

Heat Plant 43,273 1,451 31 543 45,236 15,756 - 3,554 16 19,294 25,942

Motor Vehicles 2,252 114 127 - 2,239 1,459 - 205 116 1,548 691

Office equipment 99 - 4 - 95 96 - 2 3 95 -

Other equipment and tools 2,095 5 3 - 2,097 1,975 - 110 3 2,082 15

Total 132,950 1,587 408 1,235 135,364 52,225 150 6,709 204 58,880 76,484

Capital Work in Progress 2,831 16,085 - 1,235 17,681 - - - - - 17,681 Total Property, Plant & Equipment 135,781 17,672 408 - 153,045 52,225 150 6,709 204 58,880 94,165

33

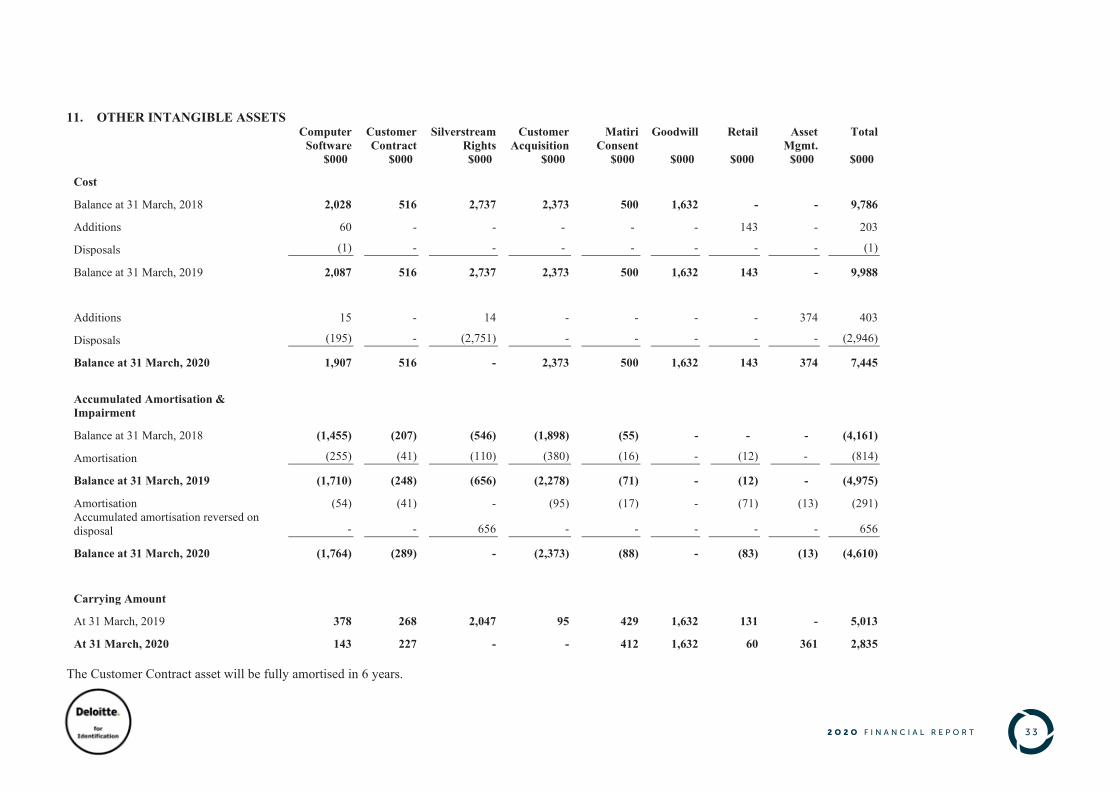

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 11. OTHER INTANGIBLE ASSETS

Computer Software

$000)

Customer Contract

$000)

Silverstream Rights $000)

Customer Acquisition

$000)

Matiri Consent

$000)

Goodwill

$000)

Retail

$000)

Asset Mgmt.

$000)

Total

$000)

Cost

Balance at 31 March, 2018 2,028 516 2,737 2,373 500 1,632 - - 9,786

Additions 60 - - -) -) - 143 - 203

Disposals (1) - - -) -) - - - (1)

Balance at 31 March, 2019 2,087 516 2,737 2,373 500 1,632 143 - 9,988

Additions 15 - 14 - - - - 374 403

Disposals (195) - (2,751) - - - - - (2,946)

Balance at 31 March, 2020 1,907 516 - 2,373 500 1,632 143 374 7,445

Accumulated Amortisation & Impairment

Balance at 31 March, 2018 (1,455) (207) (546) (1,898) (55) - - - (4,161)

Amortisation (255) (41) (110) (380) (16) - (12) - (814)

Balance at 31 March, 2019 (1,710) (248) (656) (2,278) (71) - (12) - (4,975)

Amortisation (54) (41) - (95) (17) - (71) (13) (291) Accumulated amortisation reversed on disposal - - 656 - - - - - 656

Balance at 31 March, 2020 (1,764) (289) - (2,373) (88) - (83) (13) (4,610)

Carrying Amount

At 31 March, 2019 378 268 2,047 95 429 1,632 131 - 5,013

At 31 March, 2020 143 227 - - 412 1,632 60 361 2,835 The Customer Contract asset will be fully amortised in 6 years.

3 32 O 2 O F I N A N C I A L R E P O R T

3 42 O 2 O F I N A N C I A L R E P O R T

34

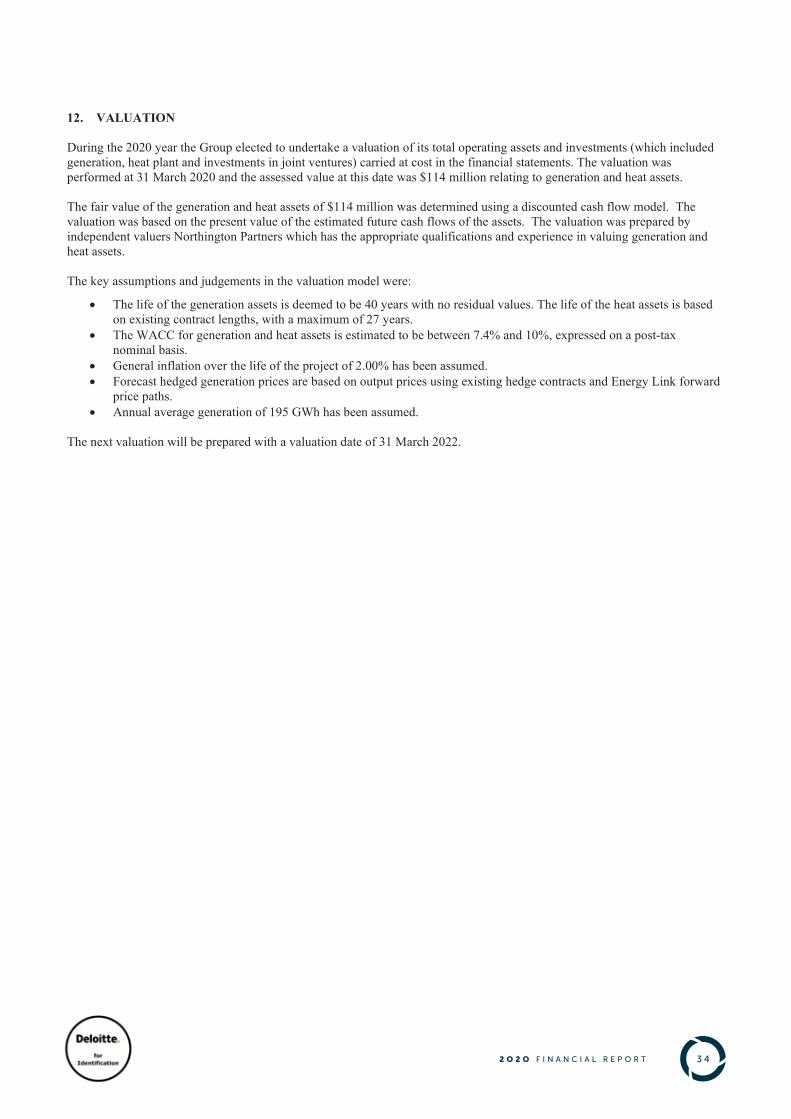

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 12. VALUATION During the 2020 year the Group elected to undertake a valuation of its total operating assets and investments (which included generation, heat plant and investments in joint ventures) carried at cost in the financial statements. The valuation was performed at 31 March 2020 and the assessed value at this date was $114 million relating to generation and heat assets. The fair value of the generation and heat assets of $114 million was determined using a discounted cash flow model. The valuation was based on the present value of the estimated future cash flows of the assets. The valuation was prepared by independent valuers Northington Partners which has the appropriate qualifications and experience in valuing generation and heat assets. The key assumptions and judgements in the valuation model were:

• The life of the generation assets is deemed to be 40 years with no residual values. The life of the heat assets is based on existing contract lengths, with a maximum of 27 years.

• The WACC for generation and heat assets is estimated to be between 7.4% and 10%, expressed on a post-tax nominal basis.

• General inflation over the life of the project of 2.00% has been assumed. • Forecast hedged generation prices are based on output prices using existing hedge contracts and Energy Link forward

price paths. • Annual average generation of 195 GWh has been assumed.

The next valuation will be prepared with a valuation date of 31 March 2022.

3 52 O 2 O F I N A N C I A L R E P O R T

35

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

Notes 2020 2019

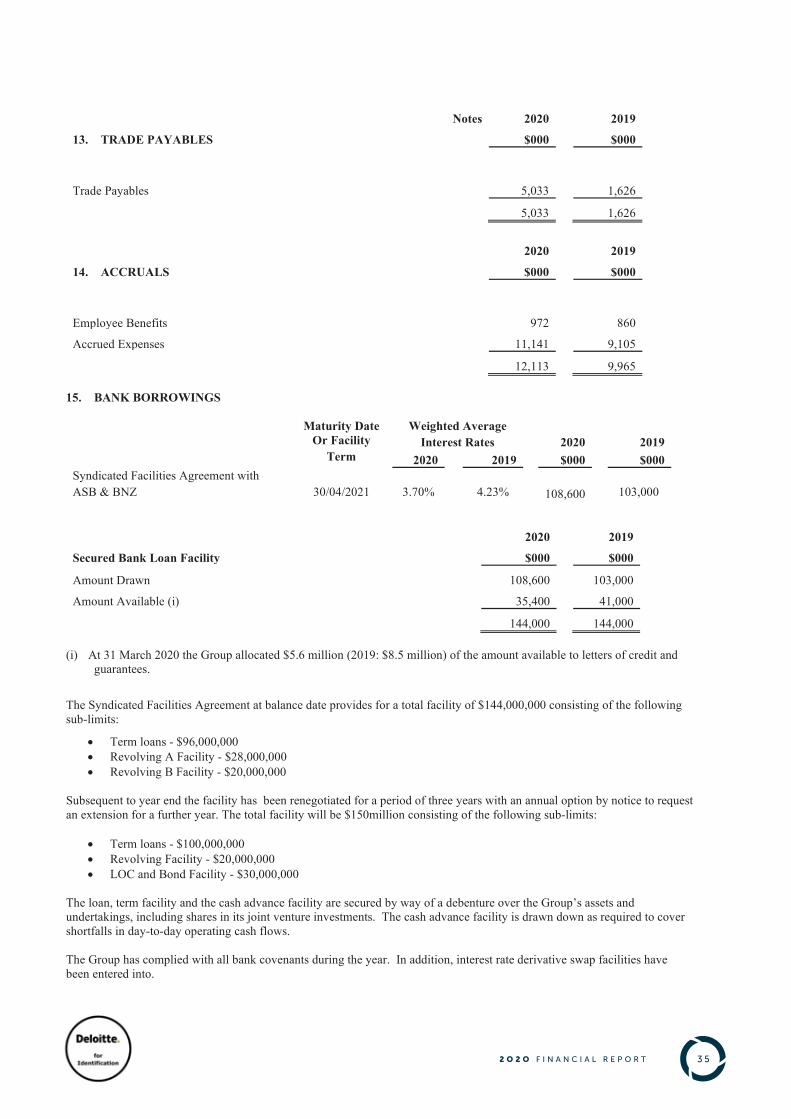

13. TRADE PAYABLES $000 $000

Trade Payables 5,033 1,626

5,033 1,626

2020 2019

14. ACCRUALS $000 $000

Employee Benefits 972 860

Accrued Expenses 11,141 9,105

12,113 9,965 15. BANK BORROWINGS

Maturity Date Or Facility

Weighted Average Interest Rates 2020 2019

Term 2020 2019 $000 $000 Syndicated Facilities Agreement with ASB & BNZ 30/04/2021 3.70%

4.23%

108,600 103,000

2020 2019

Secured Bank Loan Facility $000 $000

Amount Drawn 108,600 103,000

Amount Available (i) 35,400 41,000

144,000 144,000 (i) At 31 March 2020 the Group allocated $5.6 million (2019: $8.5 million) of the amount available to letters of credit and

guarantees.

The Syndicated Facilities Agreement at balance date provides for a total facility of $144,000,000 consisting of the following sub-limits:

• Term loans - $96,000,000 • Revolving A Facility - $28,000,000 • Revolving B Facility - $20,000,000

Subsequent to year end the facility has been renegotiated for a period of three years with an annual option by notice to request an extension for a further year. The total facility will be $150million consisting of the following sub-limits:

• Term loans - $100,000,000 • Revolving Facility - $20,000,000 • LOC and Bond Facility - $30,000,000

The loan, term facility and the cash advance facility are secured by way of a debenture over the Group’s assets and undertakings, including shares in its joint venture investments. The cash advance facility is drawn down as required to cover shortfalls in day-to-day operating cash flows. The Group has complied with all bank covenants during the year. In addition, interest rate derivative swap facilities have been entered into.

3 62 O 2 O F I N A N C I A L R E P O R T

36

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020

Notes 2020 2019

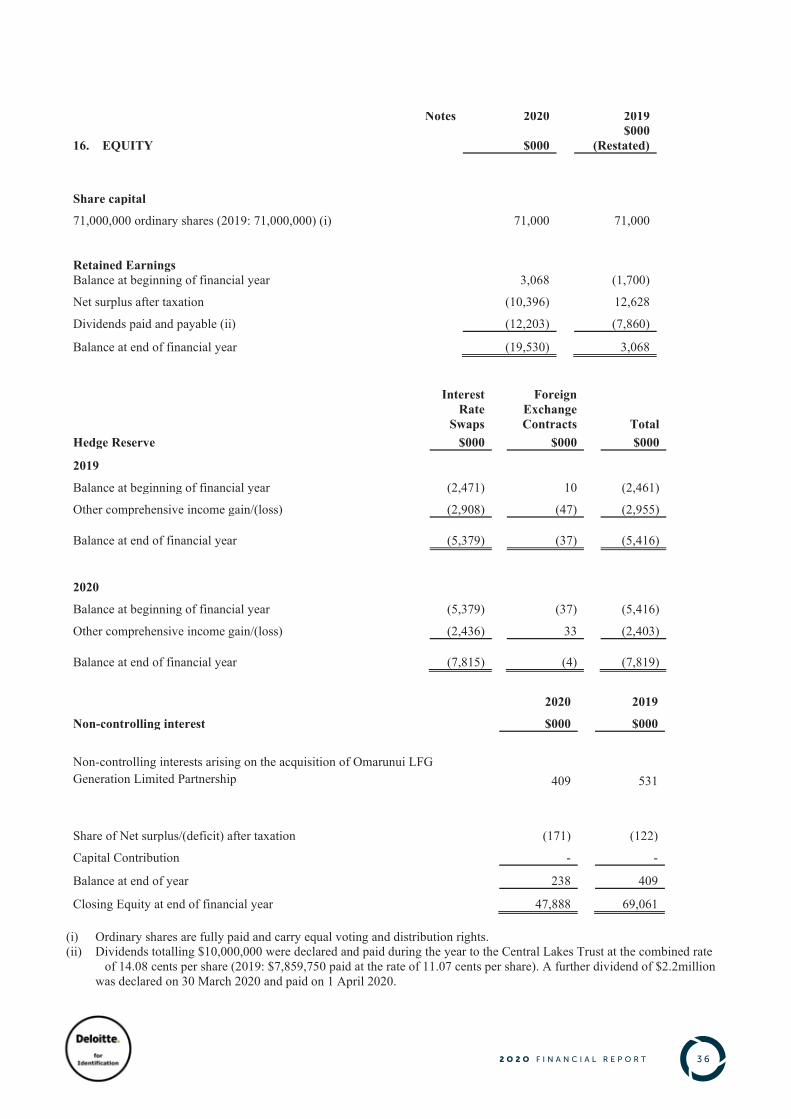

16. EQUITY $000 $000

(Restated)

Share capital

71,000,000 ordinary shares (2019: 71,000,000) (i) 71,000 71,000 Retained Earnings Balance at beginning of financial year 3,068 (1,700)

Net surplus after taxation (10,396) 12,628

Dividends paid and payable (ii) (12,203) (7,860)

Balance at end of financial year (19,530) 3,068

Interest Rate

Swaps

Foreign Exchange Contracts Total

Hedge Reserve $000 $000 $000

2019

Balance at beginning of financial year (2,471) 10 (2,461)

Other comprehensive income gain/(loss) (2,908) (47) (2,955)

Balance at end of financial year

(5,379) (37) (5,416)

2020

Balance at beginning of financial year (5,379) (37) (5,416)

Other comprehensive income gain/(loss) (2,436) 33 (2,403)

Balance at end of financial year

(7,815) (4) (7,819)

2020 2019

Non-controlling interest $000 $000

Non-controlling interests arising on the acquisition of Omarunui LFG Generation Limited Partnership 409 531

Share of Net surplus/(deficit) after taxation (171) (122)

Capital Contribution - -

Balance at end of year 238 409

Closing Equity at end of financial year 47,888 69,061 (i) Ordinary shares are fully paid and carry equal voting and distribution rights. (ii) Dividends totalling $10,000,000 were declared and paid during the year to the Central Lakes Trust at the combined rate

of 14.08 cents per share (2019: $7,859,750 paid at the rate of 11.07 cents per share). A further dividend of $2.2million was declared on 30 March 2020 and paid on 1 April 2020.

3 72 O 2 O F I N A N C I A L R E P O R T

37

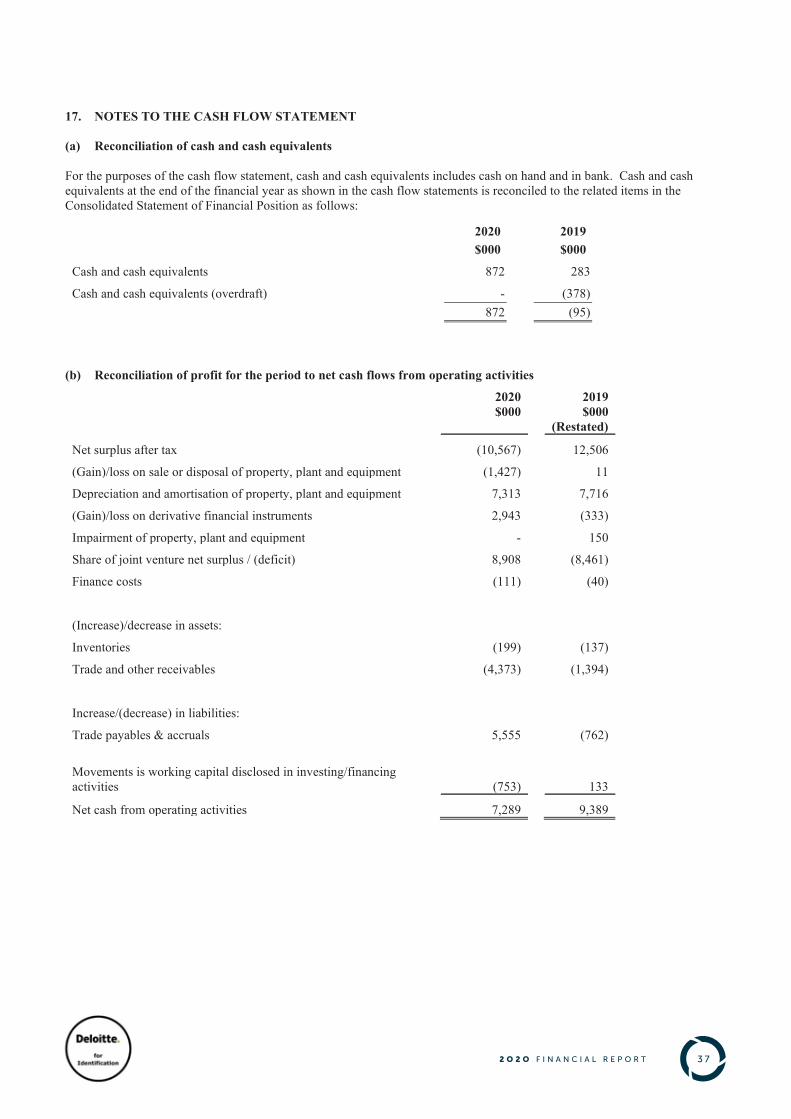

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 17. NOTES TO THE CASH FLOW STATEMENT (a) Reconciliation of cash and cash equivalents For the purposes of the cash flow statement, cash and cash equivalents includes cash on hand and in bank. Cash and cash equivalents at the end of the financial year as shown in the cash flow statements is reconciled to the related items in the Consolidated Statement of Financial Position as follows:

2020) 2019) $000) $000)

Cash and cash equivalents 872 283

Cash and cash equivalents (overdraft) - (378)

872 (95)

(b) Reconciliation of profit for the period to net cash flows from operating activities

2020 2019

$000

$000

(Restated)

Net surplus after tax (10,567) 12,506

(Gain)/loss on sale or disposal of property, plant and equipment (1,427) 11

Depreciation and amortisation of property, plant and equipment 7,313 7,716

(Gain)/loss on derivative financial instruments 2,943 (333)

Impairment of property, plant and equipment - 150

Share of joint venture net surplus / (deficit) 8,908 (8,461)

Finance costs (111) (40)

(Increase)/decrease in assets:

Inventories (199) (137)

Trade and other receivables (4,373) (1,394)

Increase/(decrease) in liabilities:

Trade payables & accruals 5,555 (762)

Movements is working capital disclosed in investing/financing activities (753) 133

Net cash from operating activities 7,289 9,389

3 82 O 2 O F I N A N C I A L R E P O R T

38

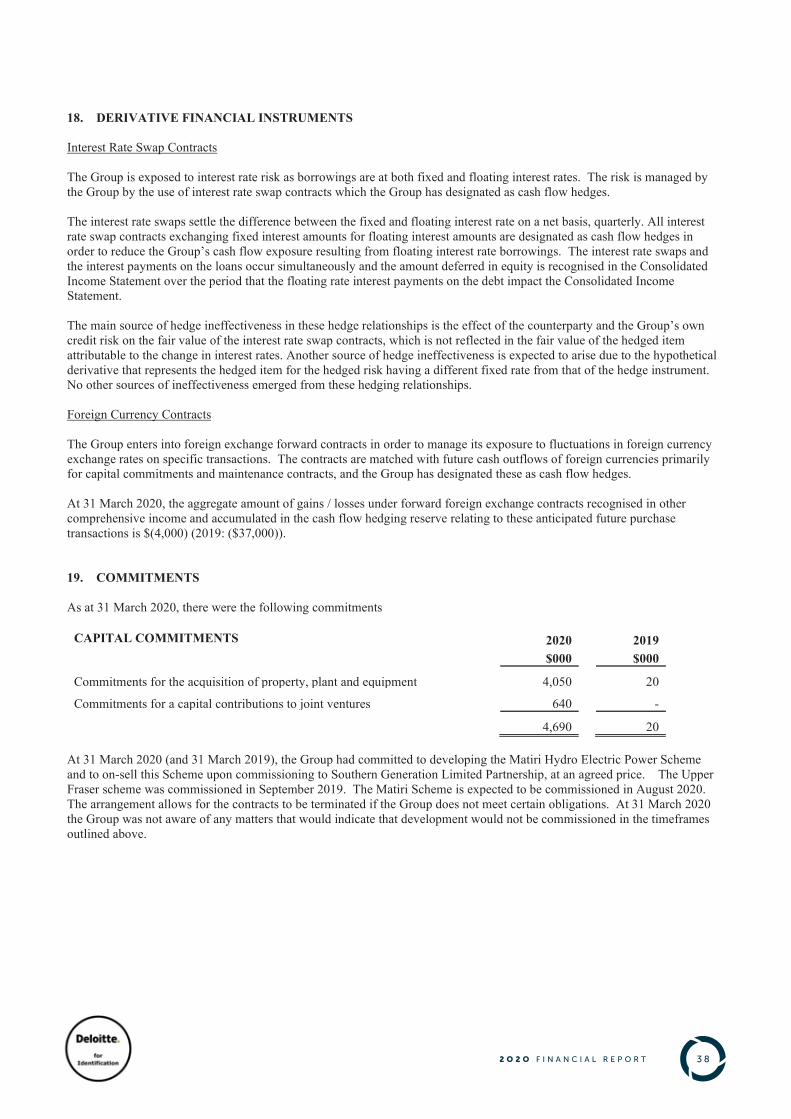

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 18. DERIVATIVE FINANCIAL INSTRUMENTS Interest Rate Swap Contracts The Group is exposed to interest rate risk as borrowings are at both fixed and floating interest rates. The risk is managed by the Group by the use of interest rate swap contracts which the Group has designated as cash flow hedges. The interest rate swaps settle the difference between the fixed and floating interest rate on a net basis, quarterly. All interest rate swap contracts exchanging fixed interest amounts for floating interest amounts are designated as cash flow hedges in order to reduce the Group’s cash flow exposure resulting from floating interest rate borrowings. The interest rate swaps and the interest payments on the loans occur simultaneously and the amount deferred in equity is recognised in the Consolidated Income Statement over the period that the floating rate interest payments on the debt impact the Consolidated Income Statement. The main source of hedge ineffectiveness in these hedge relationships is the effect of the counterparty and the Group’s own credit risk on the fair value of the interest rate swap contracts, which is not reflected in the fair value of the hedged item attributable to the change in interest rates. Another source of hedge ineffectiveness is expected to arise due to the hypothetical derivative that represents the hedged item for the hedged risk having a different fixed rate from that of the hedge instrument. No other sources of ineffectiveness emerged from these hedging relationships. Foreign Currency Contracts The Group enters into foreign exchange forward contracts in order to manage its exposure to fluctuations in foreign currency exchange rates on specific transactions. The contracts are matched with future cash outflows of foreign currencies primarily for capital commitments and maintenance contracts, and the Group has designated these as cash flow hedges. At 31 March 2020, the aggregate amount of gains / losses under forward foreign exchange contracts recognised in other comprehensive income and accumulated in the cash flow hedging reserve relating to these anticipated future purchase transactions is $(4,000) (2019: ($37,000)). 19. COMMITMENTS As at 31 March 2020, there were the following commitments

CAPITAL COMMITMENTS 2020 2019 $000 $000

Commitments for the acquisition of property, plant and equipment 4,050 20

Commitments for a capital contributions to joint ventures 640 -

4,690 20 At 31 March 2020 (and 31 March 2019), the Group had committed to developing the Matiri Hydro Electric Power Scheme and to on-sell this Scheme upon commissioning to Southern Generation Limited Partnership, at an agreed price. The Upper Fraser scheme was commissioned in September 2019. The Matiri Scheme is expected to be commissioned in August 2020. The arrangement allows for the contracts to be terminated if the Group does not meet certain obligations. At 31 March 2020 the Group was not aware of any matters that would indicate that development would not be commissioned in the timeframes outlined above.

3 92 O 2 O F I N A N C I A L R E P O R T

39

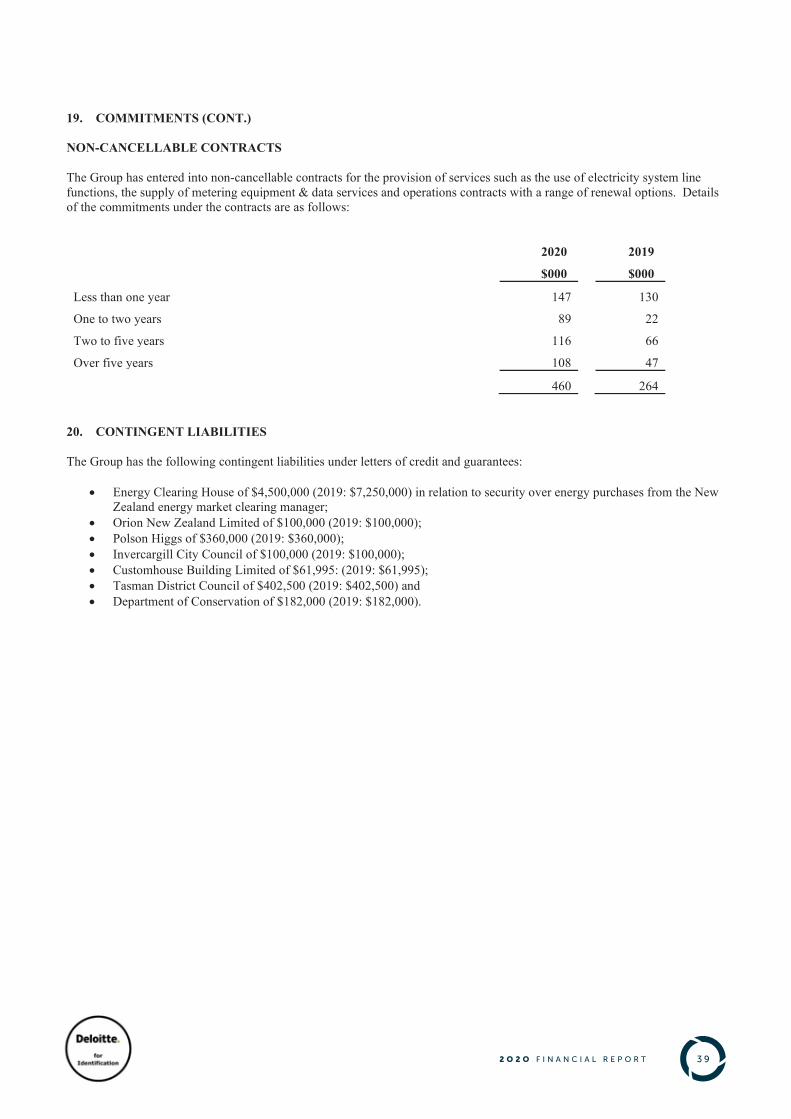

PIONEER ENERGY LIMITED NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Financial Year Ended 31 March, 2020 19. COMMITMENTS (CONT.)

NON-CANCELLABLE CONTRACTS The Group has entered into non-cancellable contracts for the provision of services such as the use of electricity system line functions, the supply of metering equipment & data services and operations contracts with a range of renewal options. Details of the commitments under the contracts are as follows:

2020) 2019)

$000) $000)

Less than one year 147 130

One to two years 89 22

Two to five years 116 66

Over five years 108 47

460 264 20. CONTINGENT LIABILITIES The Group has the following contingent liabilities under letters of credit and guarantees: