for live program only irc 1367 s corporation stock...

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext.1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

IRC 1367 S Corporation Stock and Debt Basis Adjustments:

New IRS Practice Unit Guidance

WEDNESDAY, JANUARY 17, 2018, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

JANUARY 17, 2018

IRC 1367 S Corporation Stock and Debt Basis Adjustments

Brian T. Lovett, CPA, JD, Partner

WithumSmith+Brown, East Brunswick, N.J.

Lindsey Serrate, CPA, Managing Director

True Partners Consulting, Chicago

Robert W. Jamison, CPA, Professor Emeritus of Accounting

Indiana University, Kelley School of Business, Indianapolis

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

IRC 1367 S Corporation Stock and Debt Basis

I. §1367 and Regulatory Guidance

II. Mechanics of Calculating Stock Basis

III. Debt Basis Rules and Structuring

A. Debt basis rules and calculations

B. Debt transactions subject to IRS challenge and disallowance

C. Reducing existing debt basis

D. Substantiating Debt Basis

IV. Common Errors in Adjustments that Increase or Decrease Stock Basis

A. Basis adjustments for income or losses not claimed on tax return

B. Basis treatment of life insurance premiums

C. Tax credits

D. Certain tax credit bonds

Agenda

Part I Section 1367 and Regulatory

Guidance

Robert W. Jamison, CPA

Acknowledgement

Copyright © Robert W. Jamison 8

• This material is based on the author’s work in preparing annual updates for S Corporation Taxation, revised annually by CCH, Incorporated, and for CCH Expert Treatise Library: Federal Taxation of Subchapter S Corporations.

• Call 1-800-248-3248, or go to http://tax.cchgroup.com for additional information.

• Permission has been granted by the publisher to use these materials in this course. • https://www.cchgroup.com/roles/corporations/direct-tax/research/cch-

expert-treatise-library-s -corporation-taxation (requires subscription to access)

• https://www.cchgroup.com/store/products/s-corporation-taxation-2018-prod-10029985-0009/book-softcover-item-1-10029985-0009.

• https://www.cchgroup.com/store/products/s-corporation-taxation-2018-prod-10029985-0009/book-ebook-item-1-10024481-0005.

IRC § 1367, in context

Copyright © Robert W. Jamison 9

• Subchapter S does not define basis in stock or debt.

• However Section 1367 defines certain adjustments to basis of stock or debt.

• Section 1367 is intertwined with some other rules in Subchapter S

Relationship of Corporate Income and Loss, Shareholder Income and Loss, Shareholder Basis and Distributions

Copyright © Robert W. Jamison 10

Corporation:

Taxable Income

Sec. 1363

Corporation:

Accumulated Adjustments

Sec. 1368(e)

Shareholder:

Taxable Income

Sec. 1366

Shareholder:

Basis Adjustments

Sec. 1367

Separate,

Bottom line,

Exclusions,

Nontaxable

Must include taxable,

No negative basis

No exempt

income or

related

expense,

may be negative.

Relationship of Corporate Income and Loss, Shareholder Income and Loss, Shareholder Basis and Distributions

Copyright © Robert W. Jamison 11

Corporation:

Accumulated

Adjustments

Sec. 1368(e)

Shareholder:

Taxable Income

Sec. 1366

Shareholder:

Basis

Adjustments

Sec. 1367

Corporation:

Taxable Income

Sec. 1363

Affects

lossses

Affects

Basis

Affects

Income

Statutory Requirements:

Copyright © Robert W. Jamison 12

• Under IRC §1366:

• Gross income of an S-corporation shareholder shall include the pro rata share

of gross income from the corporation.

• The shareholder’s allowed losses and deductions cannot exceed the

shareholder’s basis in stock and debt.

• Disallowed losses and deductions will carry forward.

• Under IRC §1367:

• Specific rules govern how a shareholder’s basis is to be adjusted.

• Shareholders are required to maintain adequate books and records to substantiate basis.

Stock Basis, In General

Copyright © Robert W. Jamison 13

• If the shareholder purchased the stock (and debt), the initial basis is cost. [Code Sec. 1012]

• Stock received as a gift generally has basis equal to the donor’s basis. [Code Sec. 1015(a)] • However, basis for determining loss is limited to the fair market value on the

date of the gift. [Code Sec. 1015(a)]

• Regulations provide that the basis for pass-through loss limitations to the donee is the same as his or her basis for loss on disposition of the stock. [Reg. §1.1366-2(a)(6)]

• There may also be adjustments for any gift tax paid by the donor. [Code Sec. 1015(d)]

Stock Basis, In General

Copyright © Robert W. Jamison 14

• If the stock was received in a §351 incorporation, the shareholder takes a substituted basis from the property given to the corporation. [Code Sec. 358]

• If the stock was received in a tax-free reorganization the shareholder takes a basis equal to the basis of stock surrendered in the exchange. [Code Sec. 358]

Stock Basis, In General

Copyright © Robert W. Jamison 15

• If the stock was received via death, the basis is fair market value on the date of the decedent's death or on the alternate valuation date. [Code Sec. 1014] • However, basis does not incude any items that would be inocme in respect of

a decedent if held by an individual. [Code Sec. 1366(b)(4)]

• There are also special rules that may apply if the deceased shareholder died in 2010. [(Repealed) Code Sec. 1022]

Debt Basis, in General

Copyright © Robert W. Jamison 16

• For an arrangement to qualify as debt basis, the must be indebtedness from the corporation to the shareholder. [Code Sec. 1366(d)(1)(B)]

• To qualify, there must be bona fide indebtedness from the corporation to the shareholder, determined under general legal principles. [Reg. §1.1366-2(a)(2)(i)]

• Guarantee of a debt made by another lender does not give the guarantor debt basis. [Reg. §1.1366-2(a)(2)(ii)]

Adjustments to Stock Basis

Copyright © Robert W. Jamison 17

• For all taxable years beginning after 1996, adjustments occur in the following order: 1. Start with basis at the end of the prior year.

2. Next add all income items, including bottom-line, separately reported and tax-exempt income. [Code Sec. 1367(a)] • However, do not add any income that must be applied to debt basis in a year follwong a

reduciton of debt basis. [Code Sec. 1367(b)(2)(B)]

• The result is the basis available for tax free distributions.

3. Then subtract distributions (other than dividends from the corporation’s accumulated earnings and profits). [Code Sec. 1367(a)(2)(A)

• Do not reduce basis to a negative number.

• If the distributions exceed basis, the excess is treated as a capital gain. [Code Sec. 1367

• The result is basis available for losses.

General Ordering Rule [Regs. §1.1367-1(f)]

Copyright © Robert W. Jamison 18

• The shareholder reduces basis for per se disallowed items, before considering the potentially deductible expenses and losses. • If the per se disallowed items do not exceed available basis, the shareholder

reduces basis for all of these amounts.

• If the per se disallowed items exceed available basis, the shareholder reduces basis to zero.

• There is no carryforward of any excess.

• After reducing basis for disallowed items, the shareholder reduces for deductible items. • If the deductible items do not exceed available basis, the shareholder

reduces basis for all of these amounts.

• If the deductible items exceed available basis, the shareholder reduces basis to zero.

• The shareholder carries any excess items forward.

Elective Ordering Rule [Regs. §1.1367-1(g)]

Copyright © Robert W. Jamison 19

• The shareholder reduces basis for the potentially deductible expenses and losses. • If the deductible items do not exceed available basis, the shareholder

reduces basis for all of these amounts.

• If the deductible items exceed available basis, the shareholder reduces basis to zero.

• The shareholder carries any excess items forward.

• The shareholder reduces basis for per se disallowed items, before considering the potentially deductible expenses and losses. • If the per se disallowed items do not exceed available basis, the shareholder

reduces basis for all of these amounts.

• If the per se disallowed items exceed available basis, the shareholder reduces basis to zero.

• The shareholder must carry any excess nondeductible items forward

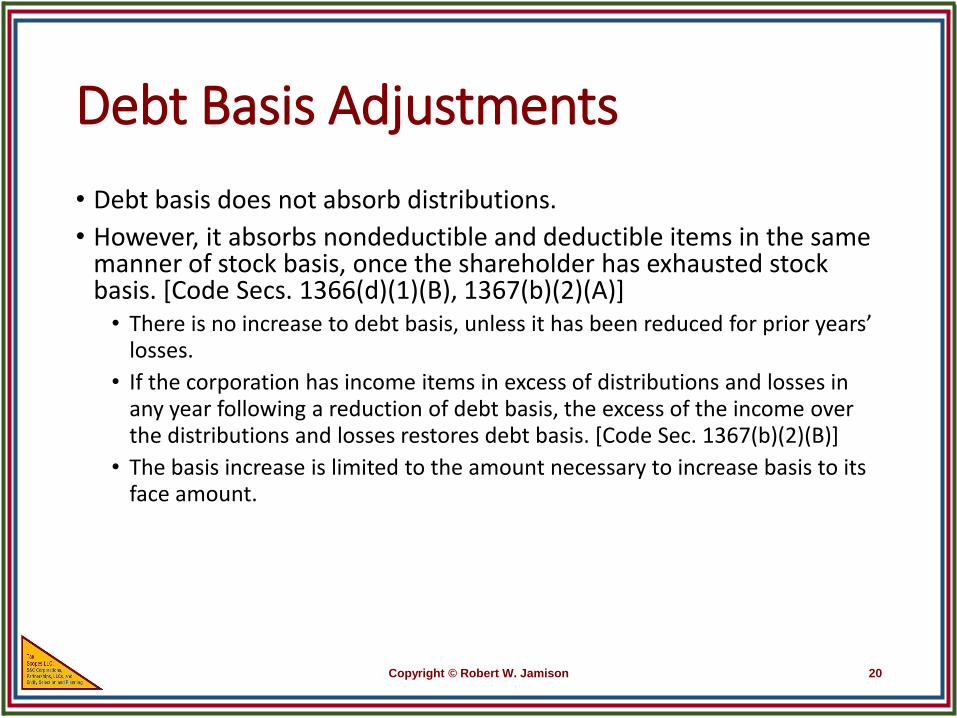

Debt Basis Adjustments

Copyright © Robert W. Jamison 20

• Debt basis does not absorb distributions.

• However, it absorbs nondeductible and deductible items in the same manner of stock basis, once the shareholder has exhausted stock basis. [Code Secs. 1366(d)(1)(B), 1367(b)(2)(A)] • There is no increase to debt basis, unless it has been reduced for prior years’

losses.

• If the corporation has income items in excess of distributions and losses in any year following a reduction of debt basis, the excess of the income over the distributions and losses restores debt basis. [Code Sec. 1367(b)(2)(B)]

• The basis increase is limited to the amount necessary to increase basis to its face amount.

IRS Requirements:

Copyright © Robert W. Jamison 21

• According to the instructions for filing Schedule E, a shareholder is required to attach a schedule showing stock and debt basis for any year that a shareholder deducts an aggregate loss.

• The Schedule E instructions then direct the shareholder to the Schedule K-1 instructions for the details of that basis tracking.

• This responsibility is solely on the shareholder. The S corporation is not required to track shareholder basis.

• History of noncompliance has resulted in over $10 million of misreported losses according to a December 2009 GAO report on the tax gap.

Potential Reasons for Noncompliance

Copyright © Robert W. Jamison 22

• Missing or Incomplete Initial Basis information

• Inherited or gifted stock basis records not provided to new corporate owner.

• New clients without prior basis schedules where client may no longer have access to prior year information.

• Lack of knowledge or misapplication of the basis tracking and basis adjustment ordering rules.

• Deliberate disregard.

Internal Revenue Service Response

Copyright © Robert W. Jamison 23

Included in the January 31, 2017 rollout of Audit Campaigns from the LB&I division was the “S Corporation Losses Claimed in Excess of Basis Campaign” which includes:

• Development of technical content to aid examining agents

• Issue-based examinations

• Soft letters encouraging voluntary self-correction

• Stakeholder outreach programs

• Creation of a new form for shareholders to assist in properly computing their basis

• See LB&I Concept Unit: Knowledge Base – S Corporations – see “Reference Materials”.

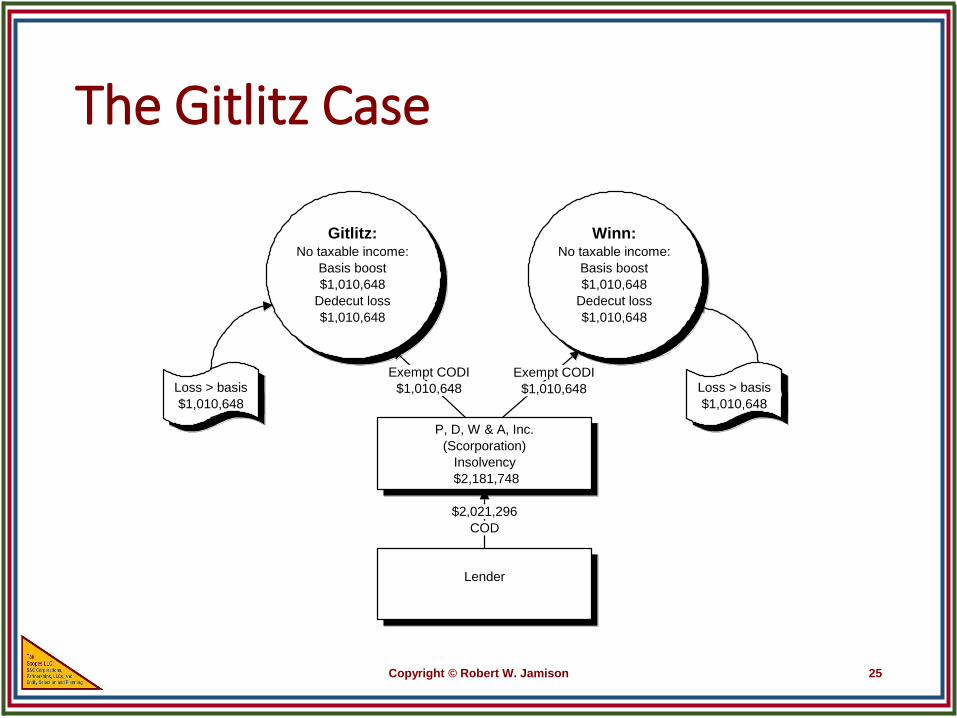

The Gitlitz Case

Copyright © Robert W. Jamison 24

• Gitlitz and Winn were equal shareholders in P. D. W. & A., an S corporation.

• Each shareholder had suspended losses of approximately $1 million.

• The corporation realized Cancellation of Debt Income of approximately $2 million.

• Due to insolvency, P. D. W. & A. properly excluded the income

• Gitlitz and Winn used their shares of this tax-exempt income to claim enough basis to deduct their suspended losses from prior years.

The Gitlitz Case

Copyright © Robert W. Jamison 25

P, D, W & A, Inc.

(Scorporation)

Insolvency

$2,181,748

Gitlitz:No taxable income:

Basis boost

$1,010,648

Dedecut loss

$1,010,648

Winn:No taxable income:

Basis boost

$1,010,648

Dedecut loss

$1,010,648

Lender

$2,021,296

COD

Loss > basis

$1,010,648

Loss > basis

$1,010,648

Exempt CODI

$1,010,648

Exempt CODI

$1,010,648

The Gitlitz Case

Copyright © Robert W. Jamison 26

• Tax Court Position on Cancellation of Debt Income.

• The Tax Court, in the 1997 Winn case, ruled that corporate level COD income excluded under §108 is, in fact, tax exempt income within the meaning of §1366. [Winn v. Comm'r, TC Memo. 1997-286] • Thus, a shareholder was allowed to increase basis for excluded §108

income, and use that basis to deduct previously suspended losses.

• The Winn victory in 1997 turned out to be illusionary. The Tax Court revisited the issue several times in 1998.

• Several courts later decided that the language of §108(d)(7) precludes the pass-through of COD income from S corporation to shareholder.

The Gitlitz Case

Copyright © Robert W. Jamison 27

• Split Circuit Positions on Cancellation-Of-Debt Income • By 1999, the effect of an S corporation’s cancellation of debt on shareholder

basis had become one of the most hotly litigated issues.

• By early 2000, there was a conflict among the Circuit Courts of Appeal.

The Gitlitz Case

Copyright © Robert W. Jamison 28

• The Supreme Court stated that COD income did pass-through to shareholders, even though it was not included in gross income. [2001-1 USTC ¶50,147]

• Justice Thomas stated clearly, “The statute's plain language establishes that excluded discharged debt is an “item of income,” which passes through to shareholders and increases their bases in an S corporation's stock. Section 61(a)(12) states that discharge of indebtedness is included in gross income. And section 108(a) provides only that the discharge ceases to be included in gross income when the S corporation is insolvent, not that it ceases to be an item of income, as the Commissioner contends.”

Treatment of Cancellation of Debt Income of S Corporations, post 2001

Copyright © Robert W. Jamison 29

• The Job Creation and Worker Assistance Act of 2002 amended Code Section 108 to provide that shareholders are not allowed to increase basis for their portions of an S corporation's excluded COD income. [§108(d)(7)(A)]

• This rule is effective for discharges of indebtedness after October 11, 2001.

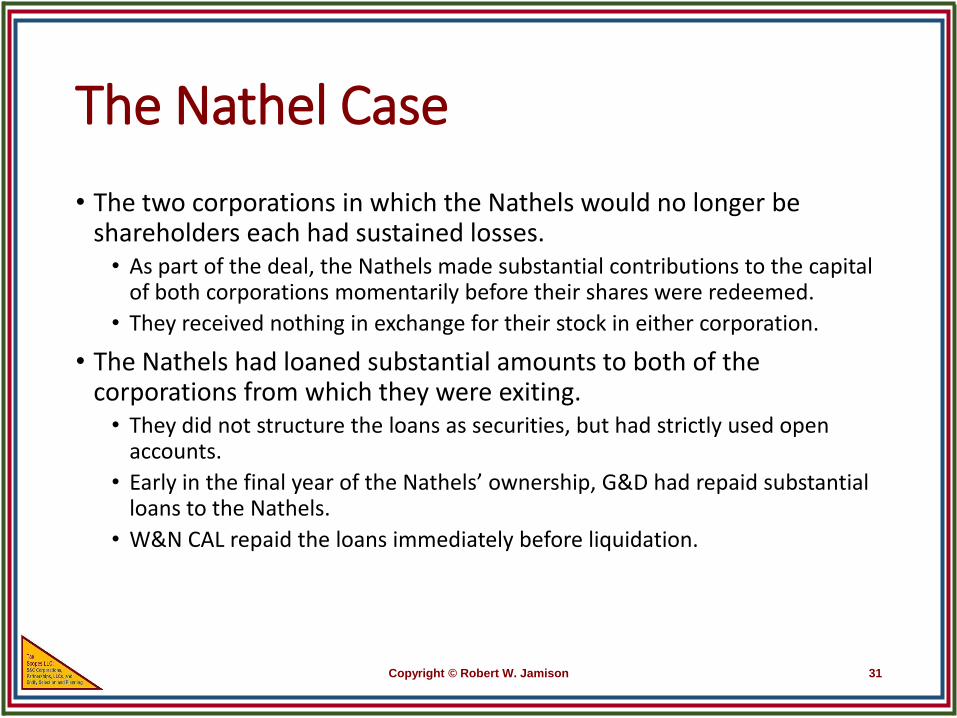

The Nathel Case

Copyright © Robert W. Jamison 30

• The case of Nathel v. Commissioner demonstrates that open account loans and contributions to capital can provide some unfortunate tax results. [Nathel v. Comm’r, 131 T.C. No. 17 (2008) aff’d at 2010-1 USTC ¶ 50,443 (2nd Cir.) Cert. denied.] • Ira and Sheldon Nathel had been shareholders in three S corporations, at

least two of which had sustained losses.

• The Nathels and the third shareholder had decided to split up ownership of the corporations.

• As a result the Nathels were to be the sole shareholders of one corporation (G&D), the other party was to be the sole shareholder of a second corporation (W&N), and the third corporation (W&N CAL) was to be liquidated.

The Nathel Case

Copyright © Robert W. Jamison 31

• The two corporations in which the Nathels would no longer be shareholders each had sustained losses. • As part of the deal, the Nathels made substantial contributions to the capital

of both corporations momentarily before their shares were redeemed.

• They received nothing in exchange for their stock in either corporation.

• The Nathels had loaned substantial amounts to both of the corporations from which they were exiting. • They did not structure the loans as securities, but had strictly used open

accounts.

• Early in the final year of the Nathels’ ownership, G&D had repaid substantial loans to the Nathels.

• W&N CAL repaid the loans immediately before liquidation.

Nathel Transactions with W&N CAL in 2001

Copyright © Robert W. Jamison 32

Nathel Transactions with W&N CAL in 2001 (Cont.)

Copyright © Robert W. Jamison 33

The Ball Case

Copyright © Robert W. Jamison 34

• Another attempt to expand the doctrine of tax-exempt income appeared in the case of R Ball for R Ball III v. Commissioner. [R Ball for R Ball III v. Comm’r, T.C. Memo. 2013-39.] • In this case several shareholders owned all of the stock of an S corporation

and all of the stock in a C corporation.

• They contributed all of their C corporation shares to the S corporation in a Section 351 exchange.

• Several years later the S corporation elected QSub status for its subsidiary.

• This election was treated in the same manner as a Section 332 liquidation, in which neither the parent not the subsidiary recognizes any gain or loss.

The Ball Case

Copyright © Robert W. Jamison 35

• Following the Gitlitz rationale, the shareholders reasoned that gains from dealing in property are expressly included in gross income. • Moreover, Section 331 requires that a shareholder must recognize gain or

loss when receiving property in complete liquidation of a corporation.

• However, Section 332 requires nonrecognition on the receipt of property by a parent corporation from a liquidated subsidiary.

• Thus when the parent corporation is an S corporation the unrecognized gain should be treated as tax-exempt income, and should pass through to the shareholders.

• However, the court held that Section 332 is not a subset of Section 331, but is an entirely different transaction.

• Therefore the shareholders were not able to adjust their S corporation stock basis for the unrecognized gain realized by the parent corporation on the deemed liquidation of its subsidiary.

The Maguire Case

Copyright © Robert W. Jamison 36

• The Maguire family owned two S corporations. • One was a used car dealership (Auto Acceptance) and the other was a finance

company (CNAC). • The dealership financed purchases for its customers and the financed company

purchased the notes from the dealer.

• One of the shareholders needed additional basis to absorb losses from Auto Acceptance. • Apparently there was no basis problem for CNAC, either because the

shareholders had ample basis in that corporation or because CNAC was profitable. • The shareholders had planned to take cash distributions from CNAC and

contribute the cash to Auto Acceptance. • However, the cash flow of CNAC was not sufficient to support this action.

• Therefore they devised a plan whereby CNAC distributed the notes that had originated from the seller financing by Auto Acceptance. • The case states that each shareholder had sufficient stock basis in CNAC to absorb

the distributions of the notes.

Maguire Corporation Relationships

Copyright © Robert W. Jamison 37

The Back-to-back Distribution and Contribution in Maguire

Copyright © Robert W. Jamison 38

The Maguire Case

Copyright © Robert W. Jamison 39

• One shareholder (son) loaned his portion of the receivables to the other shareholder (his father). • The father then contributed the receivables to Auto Acceptance.

• The IRS disallowed the basis augmentation, on the theory that the distribution and contribution might never have taken place, and were merely bookkeeping entries. • Thus, according to the IRS, the shareholder lacked basis in Auto Acceptance, because he had

made no economic outlay.

• However, the corporate resolutions and other documentation provided solid evidence that the transfers had real substance, and occurred before the end of each of the three years covered by the case. • The distributions from CNAC caused the shareholders to sacrifice future distributions from

that corporation. • The contribution of the receivables to Auto Acceptance deprived the shareholders of the

right to receive the cash from the collection of those receivables.

• Therefore the economic outlay occurred.

• Thus the shareholders were allowed basis for deduction of losses. [Maguire v, Comm’r, TC Memo 2012-160]

II. Mechanics of Calculating Stock Basis

Lindsey Serrate, Managing Director True Partners Consulting, LLC

Mechanics of calculating stock basis

Recent Tax Court Case Decisions

Common errors in adjustments that increase or decrease stock basis – Basis adjustments for income or losses not claimed on

tax return

– Basis treatment of life insurance premiums

– Tax credits

IRC 1367 S Corporation Stock and Debt Basis - Agenda

Treasury Regulation §1.1367-1

Importance of stock basis

– Stock basis is very important for S-Corp shareholders

– Quantifies shareholder’s investment

– Measures the amount a shareholder can withdraw without taxable income or gain (operating or liquidating distributions)

– Equals the shareholders economic investment in the S-Corp

– Ability to claim tax losses (deductibility)

– Gain or loss on disposition of full or partial S-Corp stock

– Ownership changes

Tracking basis often neglected

Maintaining basis recommended

Difficult to create stock basis retrospectively

II. Mechanics of Calculating Stock Basis

Basis mechanics work like a cash drawer – Contributions and earnings are deposits

– Losses and distributions are withdrawals

– Basis can never go negative

– Basis begins at stock acquisition – track from day one

Basis built on increases / decreases: – Increases:

• Amount paid for S-Corp stock

• Property contributed

• Basis of C corporation stock at the time of S conversion

• Capital contributions

• Ordinary income

• Investment income and gains

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

43

– Decreases:

• Distributions

• Losses and expenses

• §179 deductions

• Charitable contributions

• Non-deductible expenses

• Current year losses – regardless of passive loss (§469) or other disallowed / suspended losses

• credits

Historical tax basis schedules are not always correct – Goldsmith case

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

44

Ordering rules for computing stock basis:

1. Increased for income items and excess depletion;

2. Decreased for distributions (usually non-dividends)

3. Decreased for non-deductible, non-capital expenses and depletion; and

4. Decreased for items of loss and deduction.

When determining taxability of a non-dividend distribution, shareholder considers basis not debt.

Loss and deduction items exceeding shareholder’s basis, excess permitted to be deducted up to shareholder’s basis in personal loans made to S-Corp.

Reduction of basis: Loss and deduction items in excess of stock basis permitted by debt basis – debt basis is reduced accordingly.

Reduced basis debt repaid to shareholder by S-Corp is taxable to shareholder.

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

45

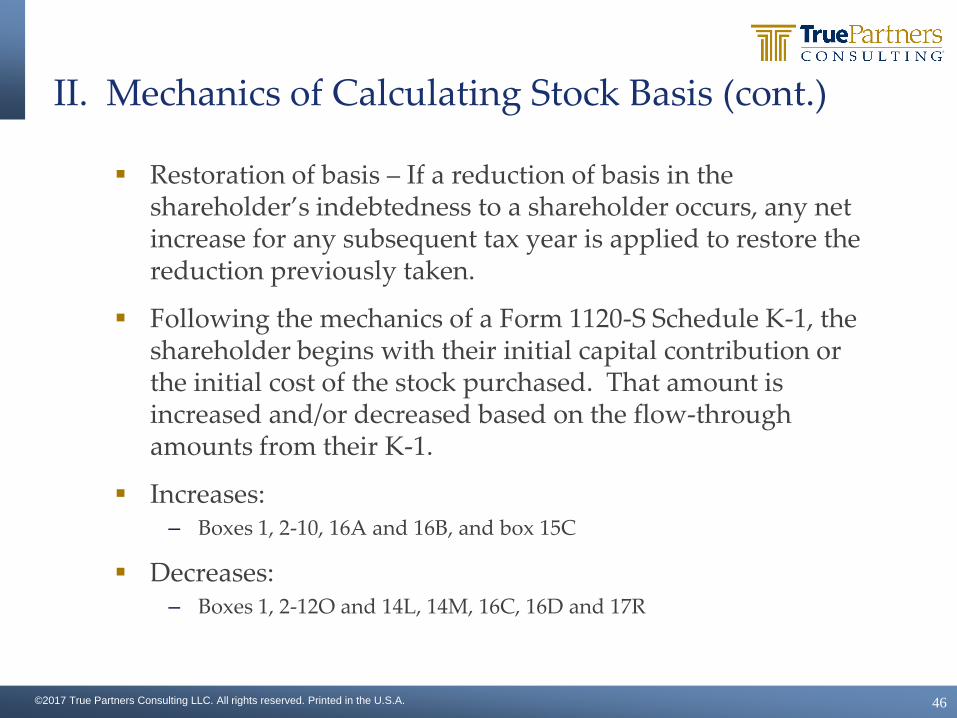

Restoration of basis – If a reduction of basis in the shareholder’s indebtedness to a shareholder occurs, any net increase for any subsequent tax year is applied to restore the reduction previously taken.

Following the mechanics of a Form 1120-S Schedule K-1, the shareholder begins with their initial capital contribution or the initial cost of the stock purchased. That amount is increased and/or decreased based on the flow-through amounts from their K-1.

Increases: – Boxes 1, 2-10, 16A and 16B, and box 15C

Decreases: – Boxes 1, 2-12O and 14L, 14M, 16C, 16D and 17R

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

46

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

47

At the end of its taxable year, an S corporation’s ordinary income was $150,000 and it had the following separately stated or non-deductible items:

Dividend Income 1,000 (Sch. K-1, Box 5a) Long-Term Capital Gain 15,000 (Sch. K-1, Box 8a) Charitable Contributions 12,000 (Sch. K-1, Box 12(A)) Officer’s Life Insurance Premiums 10,000 (Sch. K-1, Box 16(C))

Adjustments made to the sole shareholder’s stock basis would be as follows: Item Stock Basis Adjustments Ordinary Income 150,000 Dividend Income 1,000 Long-Term Capital Gain 15,000 Officer’s Life Insurance Premiums (10,000) Charitable Contributions (12,000) Net Increase to Shareholder’s Stock Basis 144,000

II. Mechanics of Calculating Stock Basis (cont.) Shareholder Stock Basis Example

Eric sole S-Corp shareholder, starts year with $15,000 stock basis, received a 2017 K-1

Ordinary business loss (20,000) (Sch. K-1, Box 1) Net section 1231 gain 4,000 (Sch. K-1, Box 9) Cash Contributions (50%) 5,000 (Sch. K-1, Box 12A) Non-deductible expenses 1,000 (Sch. K-1, Box 16C) Distributions 12,000 (Sch. K-1, Box 16D)

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

48

Shareholder Stock Basis Example – exceeding basis

Adjustments made to the sole shareholder’s stock basis would be as follows: Item Stock Basis Adjustments 1 January 2017 Stock Basis 15,000 Plus: Net section 1231 gain 4,000 Stock Basis before Distributions 19,000 Less: Non-dividend distributions (12,000) Stock Basis before non-deductible expenses 7,000 Less: Non-deductible expenses (1,000) Equals: Stock Basis before Loss & Deductions 6,000 Less: Ordinary business loss 2 (exceeds basis) (4,800) Less: Cash Contributions3 (1,200) Equals December 31, 2017 Stock Basis -0-_______________________________________________

2 - 20,000/25,000 * 6,000 = (4,800) ordinary loss 3 - 5,000/25,000 * 6,000 = (1,200) cash contribution

Wiley v. Dept. of Revenue, No. TC-MD 160036N (Apr. 28, 2017)

The issue in this case is whether the distribution from an LLC is taxable to the partner receiving the distribution. In 2008, Adams Lumber, an S Corporation, transferred its interest in Mid-Valley, LLC to RASA, LLC.

RASA, LLC reported a distribution of $192,790 to Wiley (a 50% partner) on its 2010 tax return, Wiley’s capital account decreased to zero. The schedule K-1 issued by the S Corporation to Wiley for 2008 does not reflect a distribution to Wiley.

Wiley claims that the $192,790 distribution is not taxable, the Department disagrees.

The Department’s issue is with the basis account maintained by the S Corporation.

Per IRC §1367(a)(2)(A), shareholders of an S Corporation must reduce their basis to reflect distributions.

Wiley’s basis in RASA, LLC cannot be proven, as the initial contribution into RASA claimed by Wiley is the interest in Mid-Valley, LLC.

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

49

Recent Tax Court Case Decisions

II. Mechanics of Calculating Stock Basis (cont.)

Bob Ron

Adams Lumber

S-Corp

Mid Valley, LLC

William Wiley

2007

50%

32.5%

17.5%

Recent Tax Court Case Decisions Wiley v. Department of Revenue

II. Mechanics of Calculating Stock Basis (cont.)

Mid Valley, LLC

Jill Wiley

2008

50% 50%

Recent Tax Court Case Decisions Wiley v. Department of Revenue

RASA, LLC

Bob

Wy’East

Ron

Goldsmith v. Commissioner, 113 T.C.M. (CCH) 1090 (Jan. 26, 2017)

The issue in this case is whether the plaintiff is entitled to additional increases in his basis in his S Corporation stock.

Goldsmith & Associates (G&A) (1997 law firm) was treated as an S Corporation for federal tax purposes.

Goldsmith and his firm in extreme financial difficulty.

Goldsmith claimed a number of unsubstantiated payments and advances increasing his basis in G&A stock and the company’s deducted losses on his personal return.

The Court ruled that Goldsmith did not fully prove the increases in basis during the years in question.

II. Mechanics of Calculating Stock Basis (cont.)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

52

Recent Tax Court Case Decisions

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

54

SM

S Corporation Debt Basis Rules and Structuring By: Brian T. Lovett, CPA, CGMA, JD

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

55

SM

Basis in Debt

Loan must be directly from the S/H to the S corporation. • Different from partnerships, where partners get

basis for their share of partnership debt

Guaranteeing S corporation debt doesn’t get S/H basis until they are called upon to fulfill the obligation. (See William A. Perry, 392 F.2d 458 (8th Cir. 1968, new regs would confirm).

Actual economic outlay is required (Or is it?) Mere journal entries won’t cut it. (See Oren, 2004-1 USTC 50,165 (8th Cir. 2004)

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

56

SM

Basis in Debt

Intercompany loans don’t create basis (see Bergman)

Circular loans (from bank-shareholder-loss S corp-related S corp-shareholder-bank) do not create basis (Kaplan, TC Memo 2005-219)

FINAL REGULATIONS: Do away with the “economic outlay

requirement.” As long as a reconfiguring of debt created a true debtor-creditor relationship between the S corporation and the shareholder, it gives the shareholder debt basis.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

57

SM

Fixing a Debt Basis Problem

A owns 100% of S Co1 and S Co2. S Co1 generates large losses, while S Co2 generates profits and has a lot of cash.

A has been funding S Co1 by having S Co2 make loans to S Co1.

Does this give A basis in S Co1?

• No, the loan must be directly from A to S Co1.

• How should A fix it?

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

58

SM

Fixing a Debt Basis Problem

Simply make journal entries to cancel the note between S Co1 and SCo2 and make it owed from S Co1 to A? • No, risk of IRS attack.

Use a circular flow of cash (S Co1 uses cash to pay off S Co2, S Co2 loans the cash to A, and then A loans the cash back to S Co1?) • No, risk of IRS attack.

Have S Co2 distribute the note receivable to A, and reduce A’s basis in S Co2 accordingly? • Under the final regulations, S Co2 would be permitted to

distribute the receivable from S Co1 to A, creating a debtor-creditor relationship between S Co1 and A. This would give A basis in the S Co1 debt of $100,000, even though A made no economic outlay. Also see Maguire v. Comissioner, T.C. Memo 2012-160.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

59

SM

Planning for S Corporations

If S/H needs to borrow money from a bank to loan to S corporation and create basis, advise them to:

1. Borrow money from bank in return for note.

2. Re-loan the proceeds to S corp in exchange for S corp’s note.

3. S corp should give S/H a security interest in its property to secure S corp note.

4. A should pledge S corp’s note to the bank to secure S/H’s note.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

60

SM

Utilizing Debt Basis

• Debt basis is reduced only after stock basis is taken to zero. §1367(b)(2)

• Debt basis has no bearing on gain or loss form the sale of stock or the taxability of distribution; it is only available to utilize losses.

• If taxpayer has multiple debts, reduce basis of each debt in proportion to each debt’s basis as a percentage of total debt basis.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

61

SM

Problem 3: Utilizing Debt Basis

A owns 100% of S corp. On 1/1/2017, A had a stock basis of $25,000 and debt basis of $50,000.

During 2017, S corp had the following: • Non-separately stated loss ($41,000)

• LTCG $5,000

• § 1231 Loss ($6,000).

How much loss can A absorb?

What is A’s adjusted basis on 12/31/17?

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

62

SM

Problem 3: Utilizing Debt Basis

Stock Debt

Beginning Basis $25,000 $50,000

Increase stock basis for income

$5,000

Decrease for losses ($30,000)

Ending stock basis $0

Use remaining loss against debt basis

($17,000)

Ending debt basis $33,000

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

63

SM

Repayment of debt

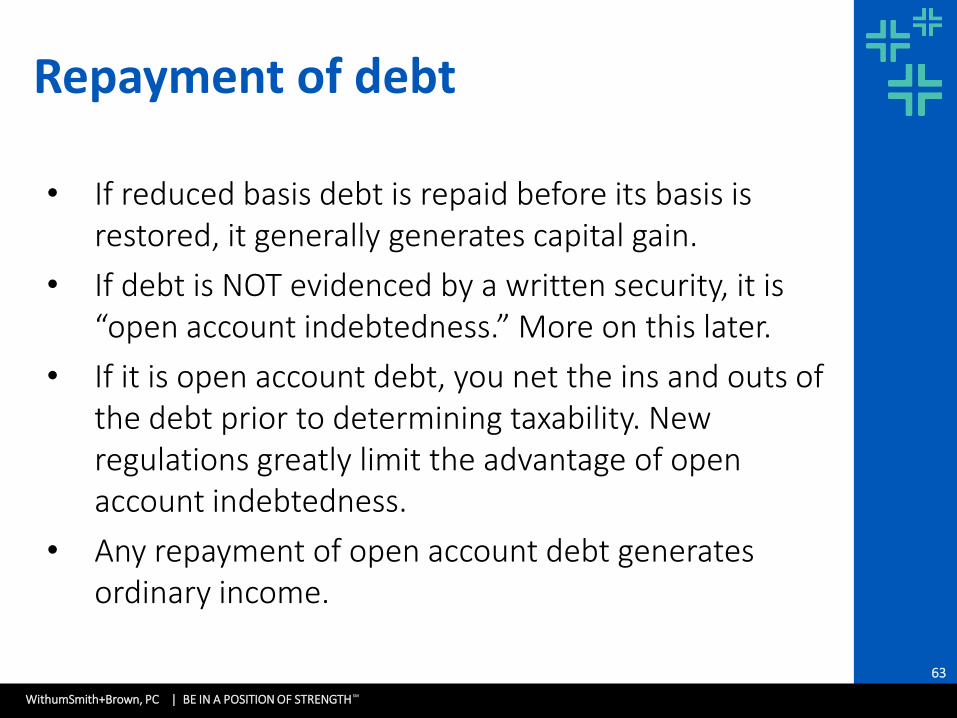

• If reduced basis debt is repaid before its basis is restored, it generally generates capital gain.

• If debt is NOT evidenced by a written security, it is “open account indebtedness.” More on this later.

• If it is open account debt, you net the ins and outs of the debt prior to determining taxability. New regulations greatly limit the advantage of open account indebtedness.

• Any repayment of open account debt generates ordinary income.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

64

SM

Restoring Reduced Basis Debt

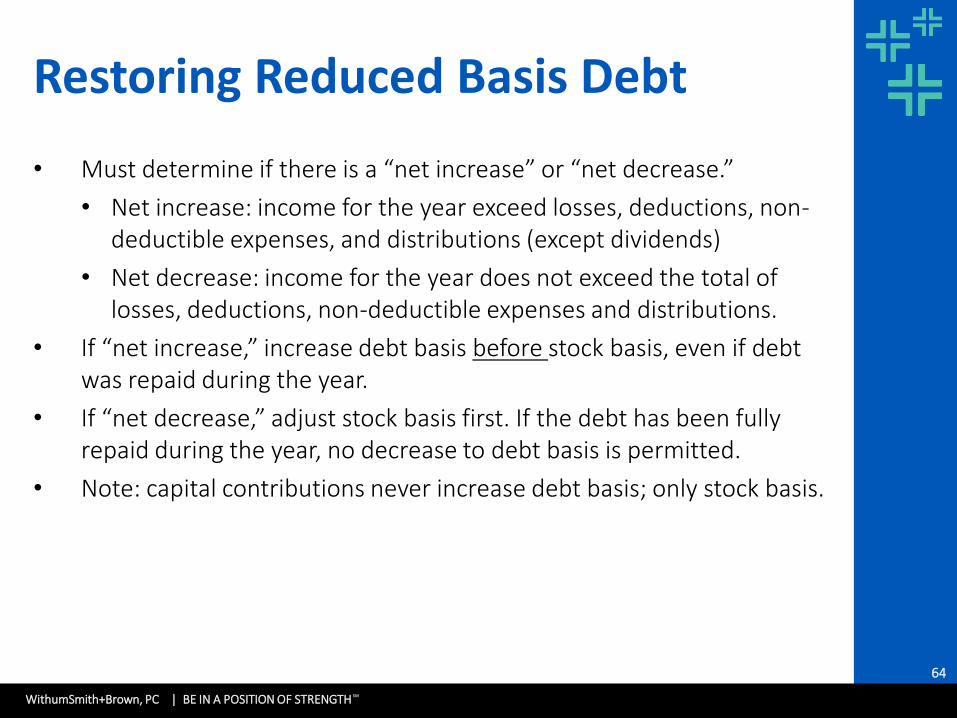

• Must determine if there is a “net increase” or “net decrease.”

• Net increase: income for the year exceed losses, deductions, non-deductible expenses, and distributions (except dividends)

• Net decrease: income for the year does not exceed the total of losses, deductions, non-deductible expenses and distributions.

• If “net increase,” increase debt basis before stock basis, even if debt was repaid during the year.

• If “net decrease,” adjust stock basis first. If the debt has been fully repaid during the year, no decrease to debt basis is permitted.

• Note: capital contributions never increase debt basis; only stock basis.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

65

SM

Problem 3: continued

When A has zero stock basis and has reduced its $50,000 debt basis to $33,000, the corporation repays the debt.

A has income of $17,000 and loss of ($7,000) for year of repayment.

Since A has a net increase for year, it increases debt basis by $10,000 to $43,000 immediately before repayment.

This results in only $7,000 of capital gain.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

66

SM

Repayment of Reduced Basis Debt

Example: A owns 100% of S Co. A has $0 stock basis on 1/1/2017. In 2016, A loaned $50,000 to S Co., but A has used $17,000 of losses against the debt basis and reduced the basis to $33,000. In 2017, S Co. allocates to A: • Nonseparately stated income: $41,500 • LTCG: $4,500 • Section 1231 loss: ($6,000) • Distribution: ($18,000) A has a “net increase” of $22,000. Thus, A first increases the basis of the note by $17,000 from $33,000 to $50,000. The remaining $5,000 of net increase increases A’s stock basis from $0 to $5,000.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

67

SM

Repayment of Reduced Basis Debt

Stock Debt

Beginning Basis $0 $33,000

Net increase of $22,000 is allocated first to debt until reaches face value of $50,000

$17,000

Remaining $5,000 of net increase is allocated to stock $5,000

Ending Basis $5,000 $50,000

Note: If the debt were repaid during the year – even if were repaid on January 1st – A would recognize no gain on the repayment because the debt was fully replenished at the end of the year.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

68

SM

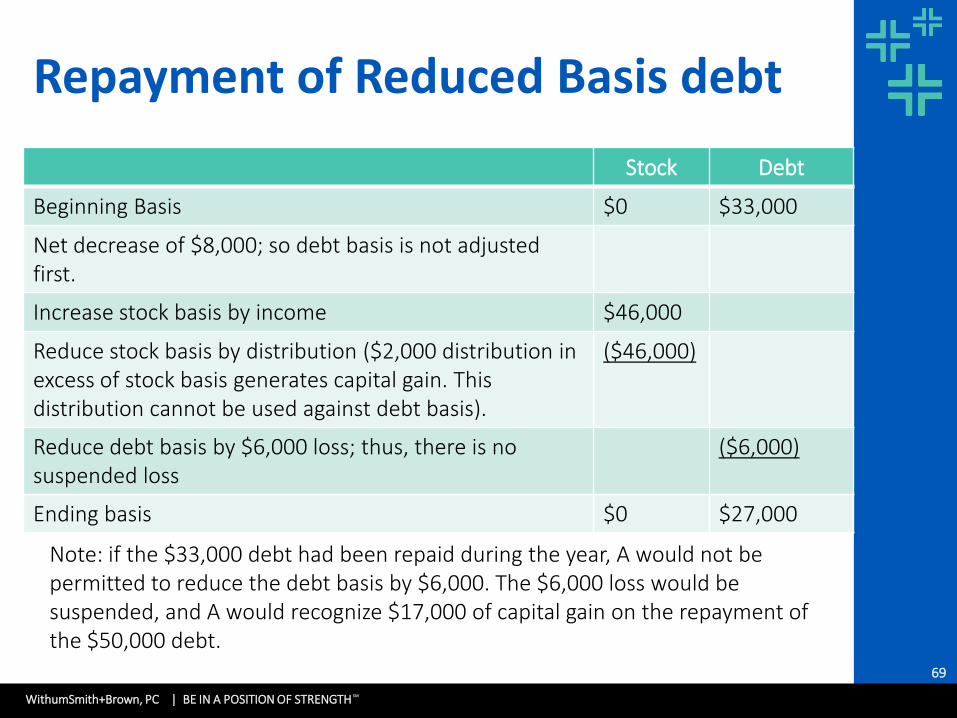

Repayment of Reduced Basis Debt

Example: Same as the previous example, except A receives a distribution of $48,000.

• A has a “net decrease “of $8,000. ($41,400 + $4,500 - $6,000 - $48,000) Thus, A does not increase his basis in the loan. Instead, A increases his stock basis from $0 to $46,000 to account for the income. Next, A reduces the stock basis to $0 for the distribution, and $2,000 of distribution exceeds basis and generates capital gain under §1368.

Finally, A’s $6,000 of Section 1231 loss cannot be used against A’s stock basis, because it has been reduced to $0. A can use the losses against his debt basis of $33,000 and further reduce his debt basis to $27,000.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

69

SM

Repayment of Reduced Basis debt

Stock Debt

Beginning Basis $0 $33,000

Net decrease of $8,000; so debt basis is not adjusted first.

Increase stock basis by income $46,000

Reduce stock basis by distribution ($2,000 distribution in excess of stock basis generates capital gain. This distribution cannot be used against debt basis).

($46,000)

Reduce debt basis by $6,000 loss; thus, there is no suspended loss

($6,000)

Ending basis $0 $27,000

Note: if the $33,000 debt had been repaid during the year, A would not be permitted to reduce the debt basis by $6,000. The $6,000 loss would be suspended, and A would recognize $17,000 of capital gain on the repayment of the $50,000 debt.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

70

SM

Partial Repayment of Debt

Trap for the unwary: A shareholder will recognize gain on the partial repayment of reduced basis debt, even if the amount repaid is less than the shareholder’s total basis in the debt.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

71

SM

Repayment of Reduced Basis Debt

Example: A loaned S Co. $100,000 in 2016. Losses have reduced the basis to $45,000 on 1/1/2017. On 7/1/2017, S Co. repays $30,000 of the loan. S Co. passes through $10,000 of income and a $15,000 distribution during 2017. • Because there is no “net increase,” the basis of the repaid debt is not

increased during the year. • A increases stock basis from $0 to $10,000 for the income, reduces it by

$10,000 for the distribution, and $5,000 of the distribution triggers capital gain.

• On the partial repayment of the debt, gain is computed as follows: $100,000 (face amount) - $45,000 (basis) * $30,000=$16,500 $100,000 (face amount) • Thus, even though the repayment is less than A’s basis in the loan, S/H must

recognize $16,500 of gain on the repayment. The other $13,500 of the repayment reduces A’s basis in the note from $45,000 to $31,500.

• If S Co. had also allocated to A a loss during the year, A would be permitted to use the loss against his remaining debt basis of $31,500.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

72

SM

Repayment of Debt with Multiple Loans

If shareholder has made multiple loans:

• First use any net increase to increase the basis of any debt that was repaid during the year.

• Next, increase the basis of the remaining loans in proportion to the amount that the basis of each outstanding debt has been reduced.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

73

SM

Brooks v. Commissioner

• Taxpayer had losses in S corp and no debt basis.

• If taxpayer had a ($500,000) loss coming in year 1, on December 31st, they would loan $500,000 to the company to create debt basis.

• On January 2nd of year 2, taxpayer would repay the debt.

• At end of year 2, if taxpayer now anticipated a ($300,000) loss for the year, they would loan $800,000 to the corporation, enough to reinstate their $500,000 debt basis from year 1 and create $300,000 additional basis to take the year 2 loss.

• If the debt were treated as non-open account debt, the repayment of the $500,000 debt in year 2 would have generated capital gain to shareholder ($500,000 repayment less $0 debt basis)

• Because taxpayer successfully argued that debt was open account debt, Tax Court allowed them to “net” the ($500,000) repayment and $800,000 of new debt in year 2, meaning no repayment occurred (net new debt created of $300,000).

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

74

SM

IRS Response

IRS did NOT like the results in Brooks.

Created new regs under Treas. Reg. § 1.1367-2

New regulations say if the outstanding debt at the end of any year exceeds $25,000, the debt is NOT treated as open account debt.

This takes away Brooks transactions, as repayment of reduced basis non-open account debt will generate immediate capital gain to shareholder if debt basis isn’t replenished.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

75

SM

Open Account Debt Final Reg. §1.1367-2

2008 Final Regulations: • Limit open account debt to aggregate advances (net of

repayment on the advances) that do not exceed $25,000 ($10,000 was proposed).

• Open account debt treated as a single indebtedness.

• Make determination at year end (proposed regs required a daily “running balance”).

Effective for advances made on or after 10/20/08. Prior advances treated separately, and old rules apply to them.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

76

SM

Open Account Debt Example

T is a 50% shareholder in Sco and has a zero basis in her stock. On 6/1/09 T advances to Sco $16,000 which is not evidenced by a written instrument. In 2009 there is no net increase that would increase basis for T. At the end of 2009, the debt does not exceed the $25,000 threshold and T carries forward to 2010 $16,000 as open account debt.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

77

SM

Open Account Debt Example

Same facts except on 12/31/09, T’s basis in the $16,000 open account debt was reduced to $8,000 due to losses. On 4/1/10 Sco repays T $4,000 and on 9/1/10 T advances Sco an additional $6,000. Assume no net increase to increase T’s basis in 2010. • Net the $4,000 repayment and the $6,000 advance, so net advance is

$2,000. No basis in the debt was restored in 2010, but since there is a net advance, no gain is recognized.

• T has $18,000 of open account debt to carry to 2011.

WithumSmith+Brown, PC | BE IN A POSITION OF STRENGTH

78

SM

Open Account Debt Example

Same facts where T carries $18,000 of open account debt to 2011.

• On 2/1/11, Sco repays $5,000 of the debt. On 3/1/11, T advances Sco $20,000.

• Net the 2011 advances and repayments to result in a net advance of $15,000.

• The debt is increased to $33,000 at the close of 2011. The open account debt now exceeds the $25,000 threshold and for any subsequent year the $33,000 of debt is treated as debt evidenced by a separate written instrument.

IV. Common errors in adjustments that increase or decrease stock basis

Lindsey Serrate, Managing Director True Partners Consulting, LLC

A. Basis adjustments for income or losses not claimed on tax

return

B. Basis treatment of life insurance premiums

C. Tax credits

IV. Common errors in adjustments that increase or decrease stock basis

S-Corp shareholder’s basis is increased by items of income and excess depletion and decreased by distributions, losses, deductions, non-deductibles and depletion.

S-Corp shareholder’s basis is not increased by unreported items of income (IRC 1367(b)(1)). – “only to the extent such amount is included in the

shareholder’s gross income”.

If a return is not required to be filed, stock basis is increased by the income.

IV. Common errors in adjustments that increase or decrease stock basis A. Basis adjustments for income or losses not claimed on tax return

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

82

Shareholder’s basis is reduced regardless of whether or not deduction or loss was taken (no tax benefit)

Basis is reduced even if loss is deferred

Only non-dividend distributions reduce stock basis not dividend distributions.

IV. Common errors in adjustments that increase or decrease stock basis A. Basis adjustments for income or losses not claimed on tax return

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

83

S-Corp purchases life insurance on a shareholder or key employee where S-Corp is direct or indirect beneficiary.

Non-deductible expenses (e.g. non-deductible life insurance premiums) passed through to S-Corp shareholder reduce stock basis.

Insurance proceeds are not includible in income (except for CSV policies).

Whole life policies with investment features – only portions attributable to death benefit reduces shareholder basis. (statement from insurance co).

If no statement is available – premium equal to CSV = investment feature and remaining portion to the insurance coverage.

Example: whole life policy, corporate premiums $8,000/ annum. CSV increases by $3,000. Reduce stock basis by $5,000. At point when CSV > premiums no stock basis reduction is required.

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

84

IV. Common errors in adjustments that increase or decrease stock basis B. Basis treatment of life insurance premiums

See Rev. Rul. 2009-13 for sale or cashed in policy

When policy is sold, gain can be part ordinary and part capital (if gain > CSV).

Deceased shareholder stock purchase to avoid unwanted family and friend shareholders via life insurance proceeds.

– Life insurance proceeds are tax-exempt income (if no premium deductions were taken) – increases stock basis.

– If multiple shareholders – following factors dictate each shareholders basis increase.

• S-Corp method of accounting (determine when t/e income earned)

• Date life insurance proceeds were received (income reported on this date)

• Method of income allocation (close books or per/share- per/day)

• Per share/ per day – proceeds allocated to shareholders based upon shares held and # days held

• Closing books method – date as described in buy/sell agreement – divides allocation by seller/buyer

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

85

IV. Common errors in adjustments that increase or decrease stock basis B. Basis treatment of life insurance premiums (cont.)

IRC 50 and Treas. Reg. §1.45D-1

Shareholder may claim tax credits passed through on Sch. K-1 regardless of shareholder’s stock basis.

– 2 scenarios when tax credit decreases basis:

a) Credits requiring a reduction of expense

b) Credits requiring a reduction in an asset’s basis

Example of a) – Research credit – reduces expenses by credit – creating non-deductible expense reducing shareholder basis.

Example of b) – New Markets Tax Credit – reduces the basis of the investment asset and the S-Corp stock. (Does not create a Sch. K-1 non-deductible expense – remember to adjust basis)

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

86

IV. Common errors in adjustments that increase or decrease stock basis C. Tax credits

Foreign tax credits – shareholders double taxed in foreign and U.S.

– Prevent double taxation – FTC or deduction (treaty permitting).

– Foreign taxes passed through on Sch. K-1 line 14L/M - paid or accrued reduces shareholder basis.

Renewable Energy tax credits

– Tax Cuts and Jobs Act retained production and ITCs for wind and solar energy (phase outs: wind 2020 and solar 2022) – compete against coal and natural gas.

– Base Erosion Anti-Abuse Tax (“BEAT”) intended to prevent multi-nationals from abusing tax code, limits ability for renewable energy industry to claim a portion of production or investment credits – fallout remains unclear.

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

87

IV. Common errors in adjustments that increase or decrease stock basis C. Tax credits

Qualified business income (“QBI”) - the net amount of items of income gain deduction and loss of a trade or business.

Business must be conducted with U.S. to qualify. Service businesses are restricted – MFJ at $315K ($100K phase-out and single $157,500 $50K phase-out).

Investment related items, guaranteed payments and reasonable compensation are excluded.

QBI deduction taken below the line and reduces taxable income but not AGI. Cannot exceed 20% of the excess of individual’s taxable income over cap gains. QBI deduction reduces taxable income and basis due to taxable income effect.

If QBI less than zero – carried forward and treated as a loss from qualified business in the next year.

Taxpayers with income above thresholds limitation on wages paid or wages paid + capital element.

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

88

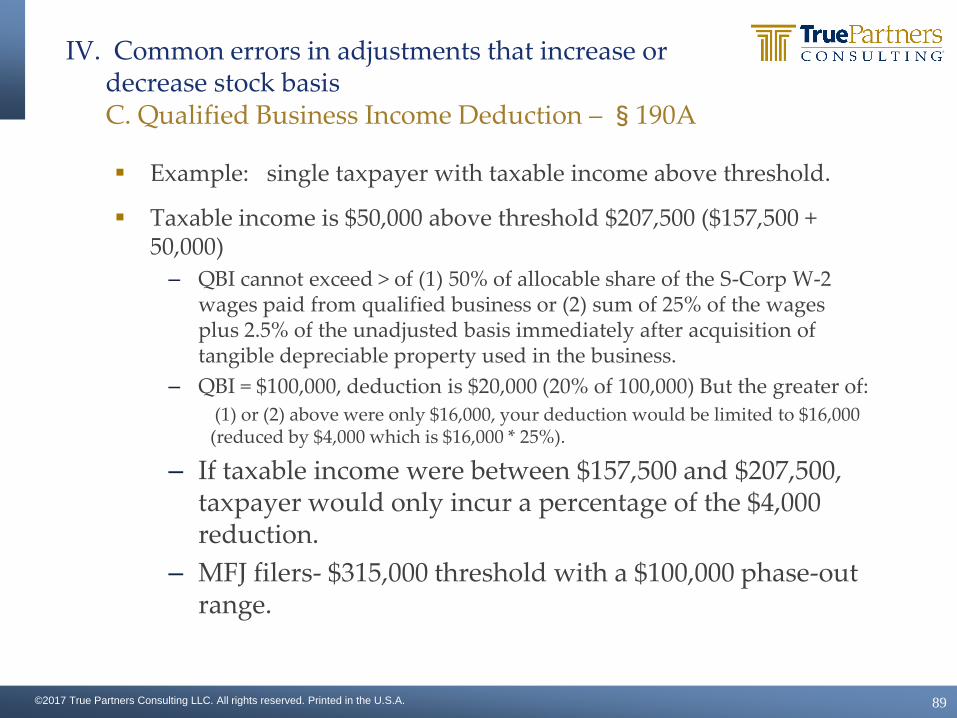

IV. Common errors in adjustments that increase or decrease stock basis C. Qualified Business Income Deduction – §190A

Example: single taxpayer with taxable income above threshold.

Taxable income is $50,000 above threshold $207,500 ($157,500 + 50,000)

– QBI cannot exceed > of (1) 50% of allocable share of the S-Corp W-2 wages paid from qualified business or (2) sum of 25% of the wages plus 2.5% of the unadjusted basis immediately after acquisition of tangible depreciable property used in the business.

– QBI = $100,000, deduction is $20,000 (20% of 100,000) But the greater of:

(1) or (2) above were only $16,000, your deduction would be limited to $16,000 (reduced by $4,000 which is $16,000 * 25%).

– If taxable income were between $157,500 and $207,500, taxpayer would only incur a percentage of the $4,000 reduction.

– MFJ filers- $315,000 threshold with a $100,000 phase-out range.

©2017 True Partners Consulting LLC. All rights reserved. Printed in the U.S.A.

89

IV. Common errors in adjustments that increase or decrease stock basis C. Qualified Business Income Deduction – §190A

IV. Common errors in adjustments that increase or decrease stock basis: D. Tax Credit Bonds

Copyright © Robert W. Jamison 90

• For several years the Internal Revenue Code authorized certain recipients to receive tax credits in lieu of interest payment on certain bonds issued by states and agencies thereof.

• These included: • Clean renewable energy bonds [Code Sec. 54], • Qualified zone academy bonds (QZABs) issued before 10/4/2008 [Code

Sec. 54E], • Gulf credit bonds, [Code Sec. 1400N] • Build America bonds, [Code Sec. 54AA] and • Qualified tax-credit bonds, which encompass:

• Qualified forestry conservation bonds [Code Sec. 54B]; • QZABs issued after 10/3/2008; [Code Sec. 54E] • New clean energy conservation bonds; [Code Sec. 54C] • Qualified energy conservation bonds; [Code Sec. 54D] and • Qualified school construction bonds. [Code Sec. 54F]

IV. Common errors in adjustments that increase or decrease stock basis: D. Tax Credit Bonds

Copyright © Robert W. Jamison 91

• There were certain rules that applied to the holders, including a requirement to report an amount related to the credit as phantom income, in the form of interest.

• Individuals report this phantom income on Schedule B.

• Unlike most interest on state and local obligations this income is taxable.

• Moreover, there is no actual cash received, other than the benefit from the credit.

• The Tax Cuts and Jobs Act repealed the authority of agencies to issue these bonds after 2017.

IV. Common errors in adjustments that increase or decrease stock basis: D. Tax Credit Bonds

Copyright © Robert W. Jamison 92

• When an S corporation or partnership is the holder of a tax credit bond, there are some divergent rules that apply, almost on a random basis.

• For some of the credits, the deemed interest is treated as taxable income and is matched by an equal and offsetting nondeductible basis reduction.

• For other credits there is no effect of the deemed interest on basis, either as an increase or a decrease, and the allocated credit is treated as a distribution.

• For discussion and examples, see Examples 5, 6 and 7 in IRS: LB&I Concept Unit Knowledge Base – S Corporations – see “Reference Materials”.