fourth edition

DESCRIPTION

International Business. Fourth Edition. CHAPTER 10. The International Monetary System. Chapter Focus. Explain how the international monetary system works. Review the system’s evolution. The gold standard. Bretton Woods - 1944. Reasons for the Bretton Woods failure. The present system. - PowerPoint PPT PresentationTRANSCRIPT

Fourth Edition

InternationalBusiness

CHAPTER 10

The International Monetary System

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-3

Chapter Focus

Explain how the international monetary system works.

Review the system’s evolution.The gold standard.Bretton Woods - 1944.

Reasons for the Bretton Woods failure.The present system.

Float versus fixed.

Implications for business.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-4

The International Monetary System

The institutional arrangements that countries adopt to govern exchange rates.Dollar, Euro, Yen and Pound “float” against each other.

Floating exchange rate:Foreign exchange market determines the relative value of a currency.

Some countries use other institutional arrangements to fix their currency’s value.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-5

Some countries use: Pegged exchange rate.

Value of currency is fixed relative to a reference currency.

Dirty float.Hold currency value within some range of a reference currency.

Fixed exchange rate.Set of currencies are fixed against each other at some mutually agreed upon exchange rate.

Require somedegree ofgovernmentintervention.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-6

The Gold Standard

Roots inmercantile

trade.Inconvenient to ship

gold, changed topaper - redeemed

for gold.

Seeking a“balance of trade”

equilibrium.

Pegging currenciesto gold and

guaranteeingconvertibility.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-7

Balance of Trade Equilibrium

Trade Surplus

GoldIncreased

money supply = price

inflation.

Decreased money supply

= price decline.

As prices decline, exportsincrease and trade goes

into equilibrium.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-8

Period Between the Wars: 1918-1939

Countries abandoned gold standard at start of WWI.Costs of war led countries to print money resulting in inflation.

U.S. (‘19), Great Britain (‘25), & France(‘28) returned to gold standard at end of war.

Britain used old rate and priced exports out of the market.U.S. did same. Then changed gold/$ ratio devaluing the dollar to increase exports.

Other countries did same. No faith in currencies.Run on countries gold reserves.

1939 - End of gold standard.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-9

Bretton Woods

1944:44 countries meet in New Hampshire.Fixed exchange rates deemed desirable.

Agree to peg currencies to US dollar that is convertible to gold at $35/oz.

Promise not to devalue currency for trade purposes and will defend currencies.Created:

World Bank International Monetary Fund.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-10

Bretton Woods

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-11

The Role of the IMFWant to avoid problems following WWI.

Discipline:Fixed rate imposes discipline:

Need to maintain rate stops competitive devaluations.Imposes monetary discipline, curtailing inflation.

Flexibility:Lending facility:

Lend foreign currencies to countries having balance-of-payments problems.

Adjustable parities:Allow countries to devalue currencies more than 10% if B of P was in “fundamental disequilibrium’.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-12

The Role of the World Bank

International Bank for Reconstruction and Development (IBRD).Rebuild Europe’s war-torn economies.

Overshadowed by the Marshall Plan.

Turns to ‘development’.Lending money to Third World nations.

Agriculture.Education.Population control.Urban development.

IBRD raises money in bond market and lends at ‘market rate’.

International Development Agency raises money through subscriptions

and lends to very poor countries.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-13

0

5

10

15

20

US Germany Japan Britain France

USGermanyJapanBritainFrance

Largest Contributors

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-14

Collapse of the Fixed Exchange Rate System

Collapsed in 1973.Pressure to devalue dollar led to collapse.

President Johnson financed both the Great Society and Vietnam by printing money.

High inflation.High spending on imports.

President Nixon took dollar off gold standard and kept 10% import tax.Countries agreed to revalue their currencies against the dollar.

Bretton Woods fails when key currency (dollar) is under speculative attack.

Now have a managed-float system.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-15

The Floating Exchange Rate Regime

Jamaica Agreement - 1967Floating rates acceptable.Gold abandoned as reserve asset.IMF quotas increased.

IMF continues role of helping countries cope with macroeconomic and exchange rate problems.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-16

Exchange Rates Since 1973

More volatile:Oil crisis -1971.Loss of confidence in the dollar - 1977-78.Oil crisis - 1979.Unexpected rise in the dollar - 1980-85.Rapid fall of the dollar - 1985-87 and 1993-95.Partial collapse of European Monetary System - 1992.Asian currency crisis - 1997.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-17

90

100

110

120

130

140

150

160

US Dollar Movements

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-18

Fixed versus Floating Exchange Rates

Floating:Monetary policy autonomy.

Restores control to government.

Trade balance adjustments.

Adjust currency to correct trade imbalances.

Fixed:Monetary discipline.Speculation.

Limits speculators.Uncertainty.

Predictable rate movements.

Trade balance adjustments.Argue no linkage between exchange rates and trade.

Linkage between savings and investment.

Which system is better?Evidence is unclear.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-19

IMF Members’ Exchange Rate Policies, 2000

27%

15%

6%24%

4%

20%4%

Free Float

Managed Float

Adjustable Peg

Fixed PegArrangementCurrency BoardArrangementNo separate Tender

Other

27%

15%

6%24%

4%

20%4%

Free Float

Managed Float

Adjustable Peg

Fixed PegArrangementCurrency BoardArrangementNo separate Tender

Other

Figure 10.2

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-20

Target Zones: The European Monetary System in Retrospect

An exchange rate system based on target zones involving a group of countries trying to keep their currencies within a predetermined ‘zone’, of other currencies in the group.Created in 1979:

Create stability by reducing volatility and inflation.

Control inflation by imposing monetary discipline.Coordinate exchange rates between EU and non-EU currencies such as the dollar and yen.

Created the European currency unit (Ecu) and the exchange rate mechanism (ERM) to achieve objectives.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-21

The Ecu and the ERM

Ecu was a basket of EU currencies.

One Ecu = defined % of national currencies.Each national currency given rate versus the Ecu.Mandatory intervention into FX market when currency fluctuates.Defend against speculation.

System performance:1992: pound and lira hit by speculation.Britain and Italy withdraw from EMS.

Changed EMS:Fluctuation bands increased to 15%.Intervention no longer required.

Performance good.Euro introduced.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-22

Crisis Management by the IMF

Role has expanded to meet crisis.Currency crisis.Banking crisis.Foreign debt crisis.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-23

Incidence of Currency Crises1975-1997

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

1975 79 83 87 91 95

Developed

Developing

Number of Currency Crises per Country

Figure 10.3a

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-24

Incidence of Banking Crises 1975-1997

0

0.05

0.1

0.15

0.2

75 77 79 81 83 85 87 89 91 93 95 97

Developed

Developing

Number of Banking Crises per Country

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-25

Mexican Currency Crises of 1995

Peso pegged to U.S. dollar.Mexican producer prices rise by 45% without corresponding exchange rate adjustment.Investments continued ($64B between 1990 -1994.Speculators began selling pesos and government lacked foreign currency reserves to defend it.IMF stepped in.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-26

Peso Movements

0

20

40

60

80

100

120

140

160

Index

= 1

00

Mexico

94 95

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-27

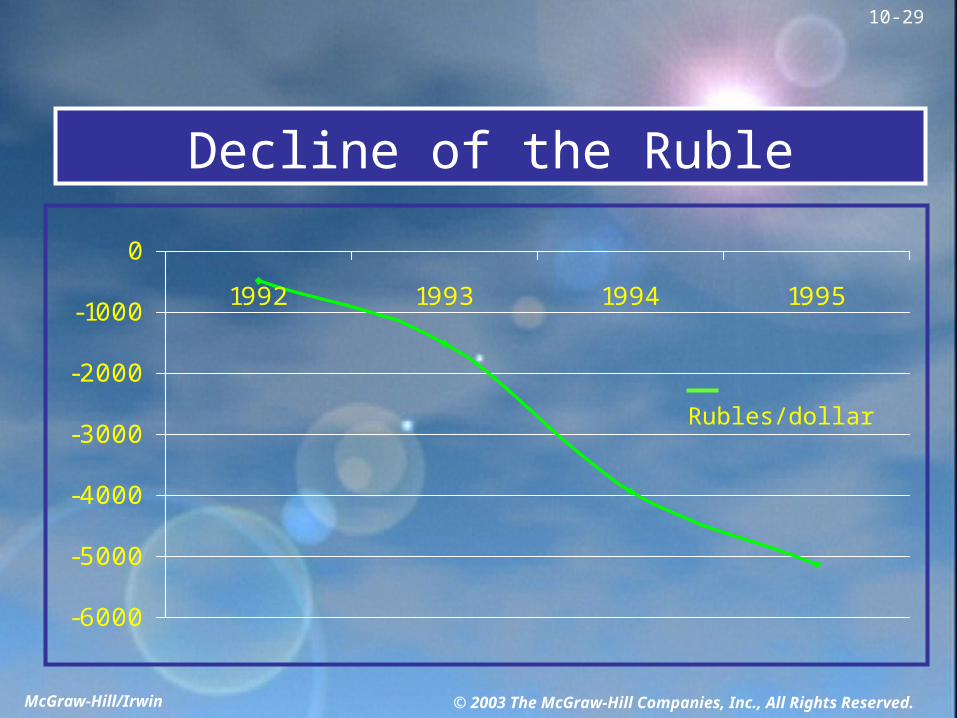

Russian Ruble Crisis

Persistent decline in value of ruble:High inflation.

Artificial low prices in Communist era.Shortage of goods.Liberalized price controls.

Too many rubles chasing too few goods.

Growing public-sector debt.Refusal to raise taxes to pay for government services.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-28

Government ActionsExacerbating the Situation

Defacto devaluation of the ruble.Unilateral restructuring of ruble-denominated public debt.90-day moratorium on foreign credits repayment.Hike in interest rates to defend ruble.Duma rejects measures designed to alleviate problems.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-29

Decline of the Ruble

-6000

-5000

-4000

-3000

-2000

-1000

0

1992 1993 1994 1995

Rubles/dollar

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-30

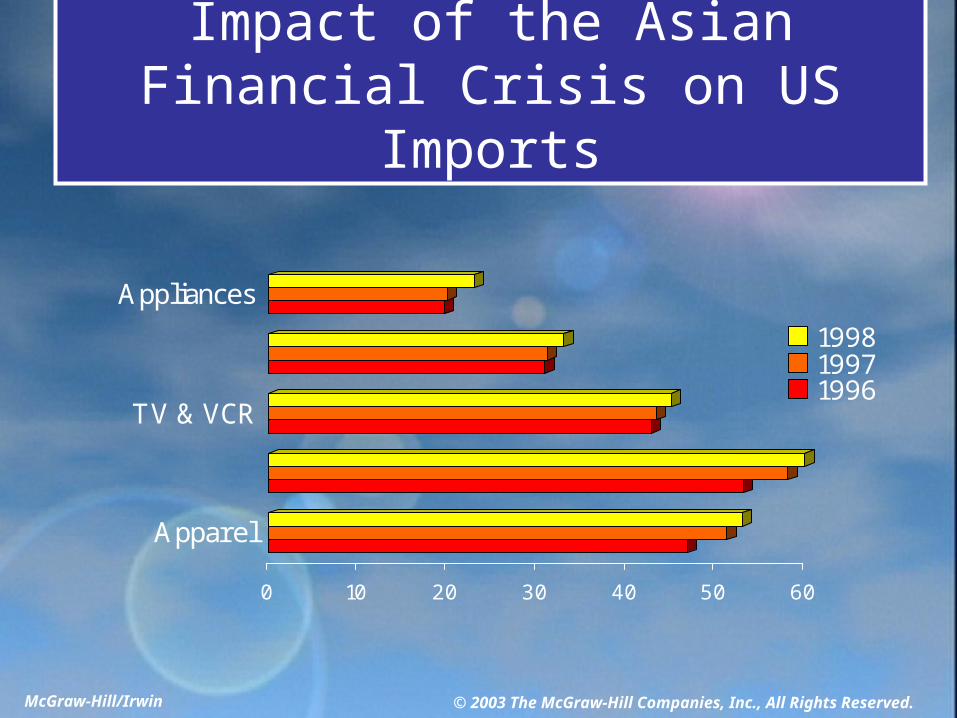

Asian Crisis

1997:Investment boom.Excess capacity.Debt.Expanding imports.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-31

Impact of the Asian Financial Crisis on US Imports

0 10 20 30 40 50 60

Apparel

TV & VCR

Appliances

199819971996

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-32

Devalued Currency

0

20

40

60

80

100

120

Index

= 1

00

Thailand

I ndonesia

S. Korea

1997 1998

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-33

Evaluating the IMF’s Policy Prescriptions

Inappropriate policies:“One size fits all’.Moral hazard:

People behave recklessly when they know they will be saved if things go wrong.

Foreign lending banks could fail.Foreign lending banks have paid price for rash lending.

Lack of Accountability.IMF has grown too powerful.

Unclear as to theappropriatenessof IMF actions.

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

10-34

Implications for Business

Currency management.Business strategy.

Forward exchange market (months not years ahead).Strategic flexibility.

Corporate-government relations.