fsu oilseeds - raising the curtain thorsten tiedemann toepfer international, hamburg

DESCRIPTION

Vancouver, March 21, 2007 CANOLA – Growing Great 2015!. FSU Oilseeds - Raising the Curtain Thorsten Tiedemann Toepfer International, Hamburg. ACTI‘s Office Locations. 40 offices 900 employees Turnover 40 mln t. Hamburg. Dublin. Warsaw. Rotterdam Antwerp. London. Budapest. Paris. - PowerPoint PPT PresentationTRANSCRIPT

CCC Vancouver March 21, 2007 Chart 1

FSU Oilseeds - Raising the Curtain

Thorsten TiedemannToepfer International, Hamburg

Vancouver,

March 21, 2007 CANOLA –

Growing Great 2015!

CCC Vancouver March 21, 2007 Chart 2

Hamburg

LondonWarsaw

Paris

Madrid

Basle

RotterdamAntwerp

Bucharest

Winnipeg

New Orleans

Minneapolis

Tampa

Athens

RostovKiev

AmmanCairo

Mumbai

Tehran

Manila

Jakarta

Adelaide

Singapore

DalianBeijing

Shanghai

Taipei

Ho Chi Minh City

Bangkok

Sao Paulo

Rosario

Buenos Aires

Budapest

Odessa

Dublin

Montevideo

Sofia

ACTI‘s Office Locations40 offices900 employeesTurnover 40 mln t

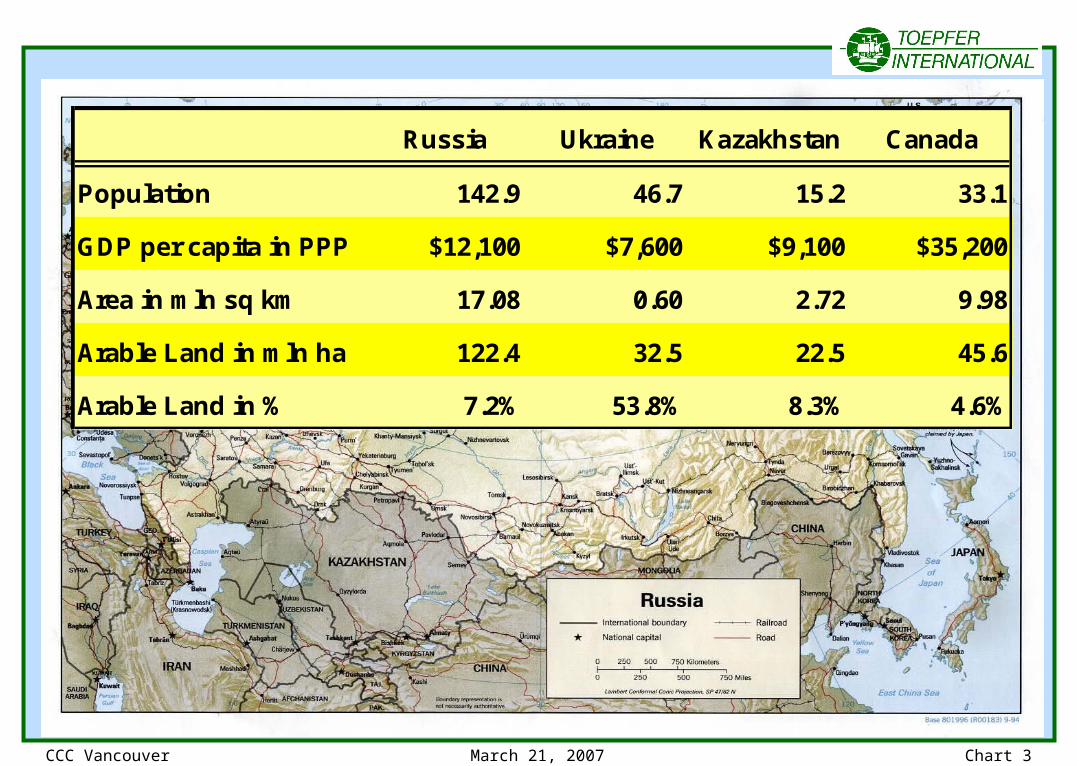

CCC Vancouver March 21, 2007 Chart 3

Russia Ukraine Kazakhstan Canada

Population 142.9 46.7 15.2 33.1

GDP per capita in PPP $12,100 $7,600 $9,100 $35,200

Area in mln sq km 17.08 0.60 2.72 9.98

Arable Land in mln ha 122.4 32.5 22.5 45.6

Arable Land in % 7.2% 53.8% 8.3% 4.6%

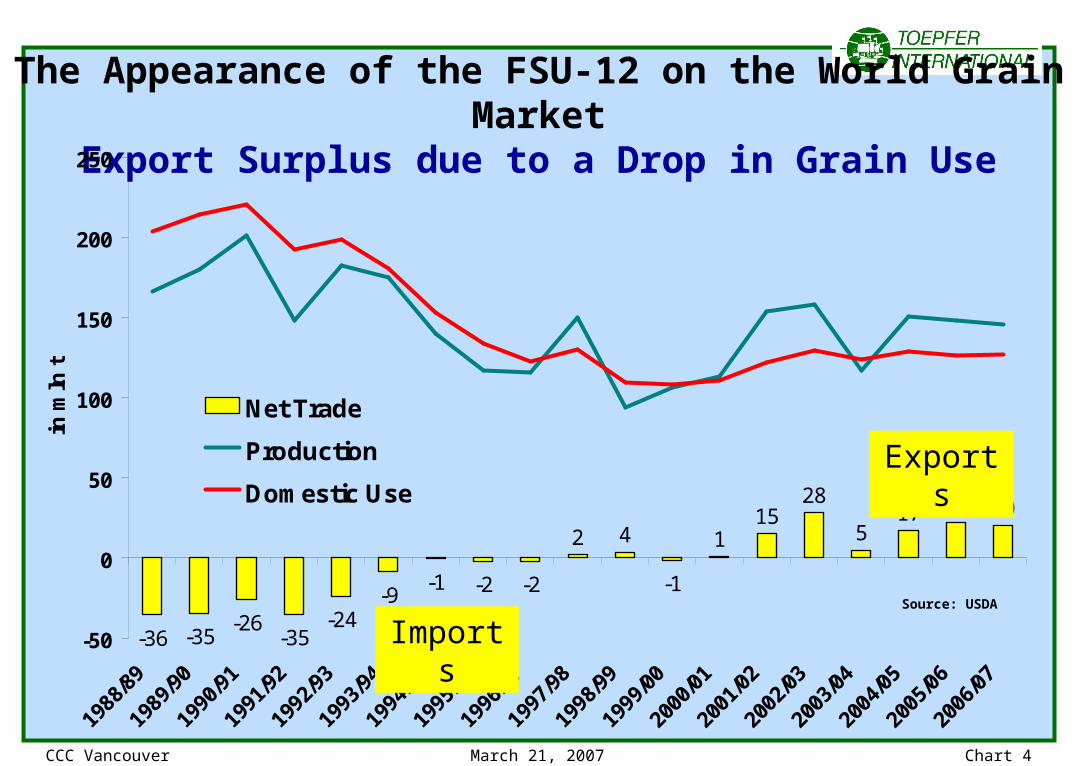

CCC Vancouver March 21, 2007 Chart 4

The Appearance of the FSU-12 on the World Grain MarketExport Surplus due to a Drop in Grain Use

-36 -35-26

-35-24

-9-1 -2 -2

2 4

-1

115

28

517 22 20

-50

0

50

100

150

200

250

1988

/89

1989

/90

1990

/91

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

in m

ln t

Net Trade

Production

Domestic UseExports

ImportsSource: USDA

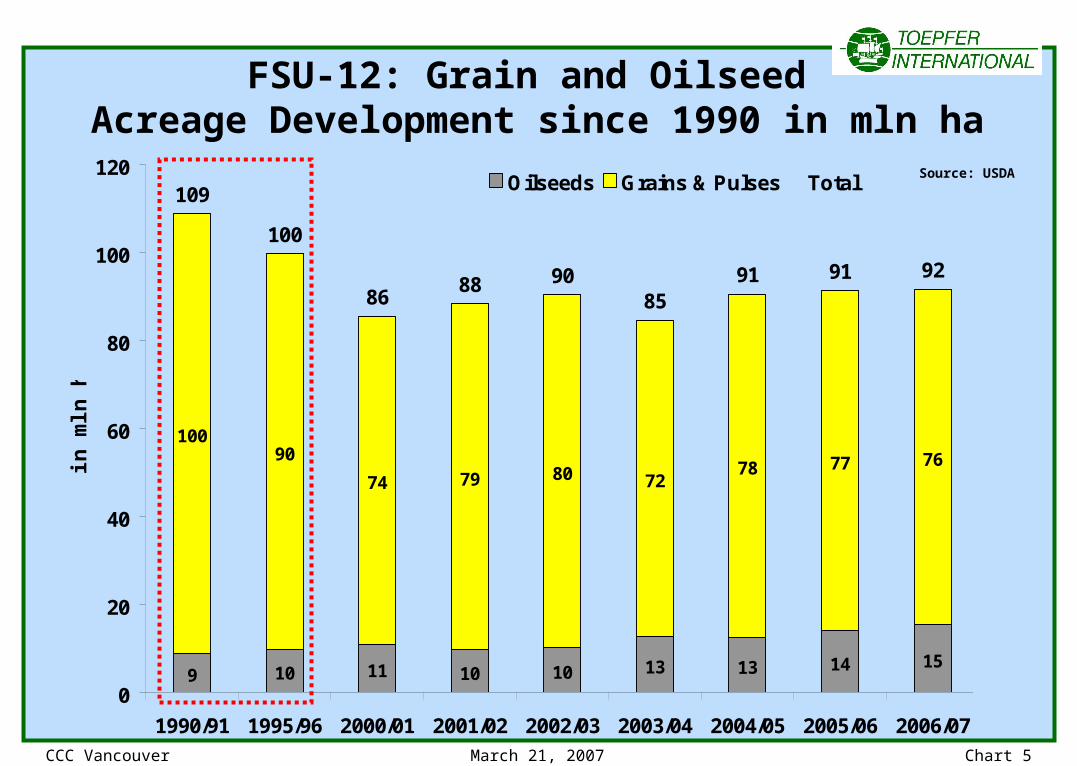

CCC Vancouver March 21, 2007 Chart 5

9 10 11 10 10 13 13 14 15

10090

74 79 80 7278 77 76

109

100

8688 90

8591 91 92

0

20

40

60

80

100

120

1990/91 1995/96 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

in m

ln h

a

Oilseeds Grains & Pulses Total

FSU-12: Grain and Oilseed Acreage Development since 1990 in mln ha

Source: USDA

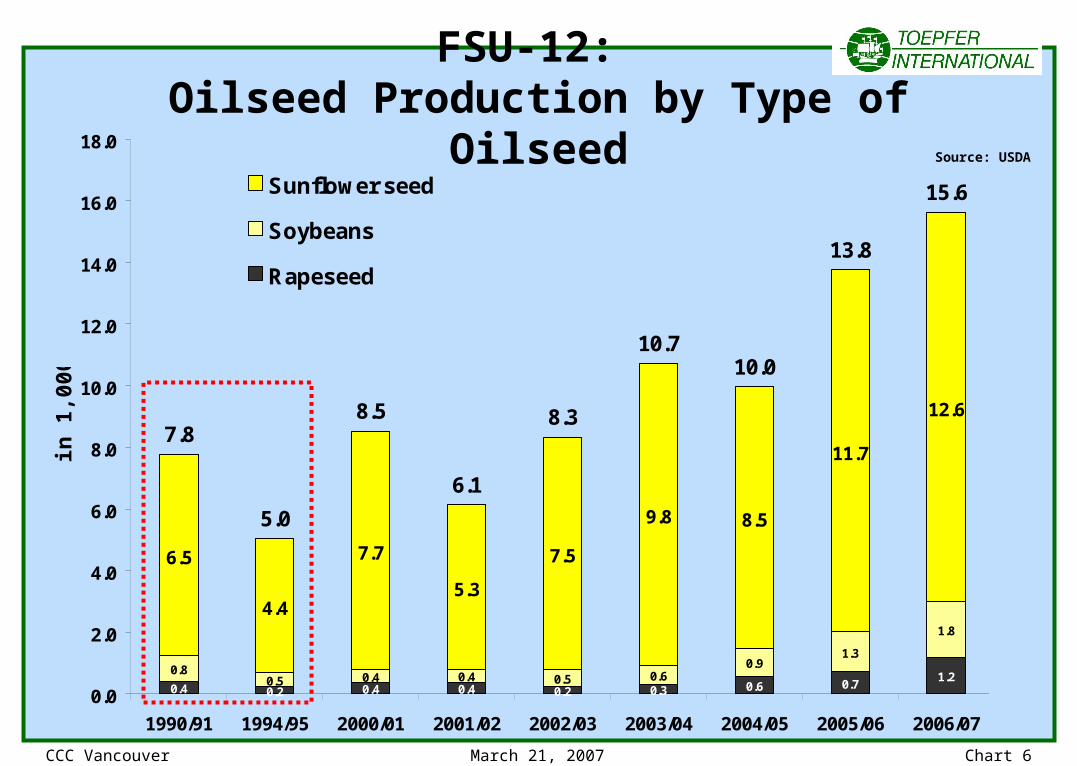

CCC Vancouver March 21, 2007 Chart 6

0.4 0.2 0.4 0.4 0.2 0.3 0.6 0.71.2

0.80.5 0.4 0.4 0.5 0.6

0.91.3

1.8

6.5

4.4

7.7

5.3

7.5

9.8 8.5

11.7

12.67.8

5.0

8.5

6.1

8.3

10.710.0

13.8

15.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1990/91 1994/95 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

in 1

,00

0 t

Sunflower seed

Soybeans

Rapeseed

FSU-12: Oilseed Production by Type of Oilseed

Source: USDA

CCC Vancouver March 21, 2007 Chart 7

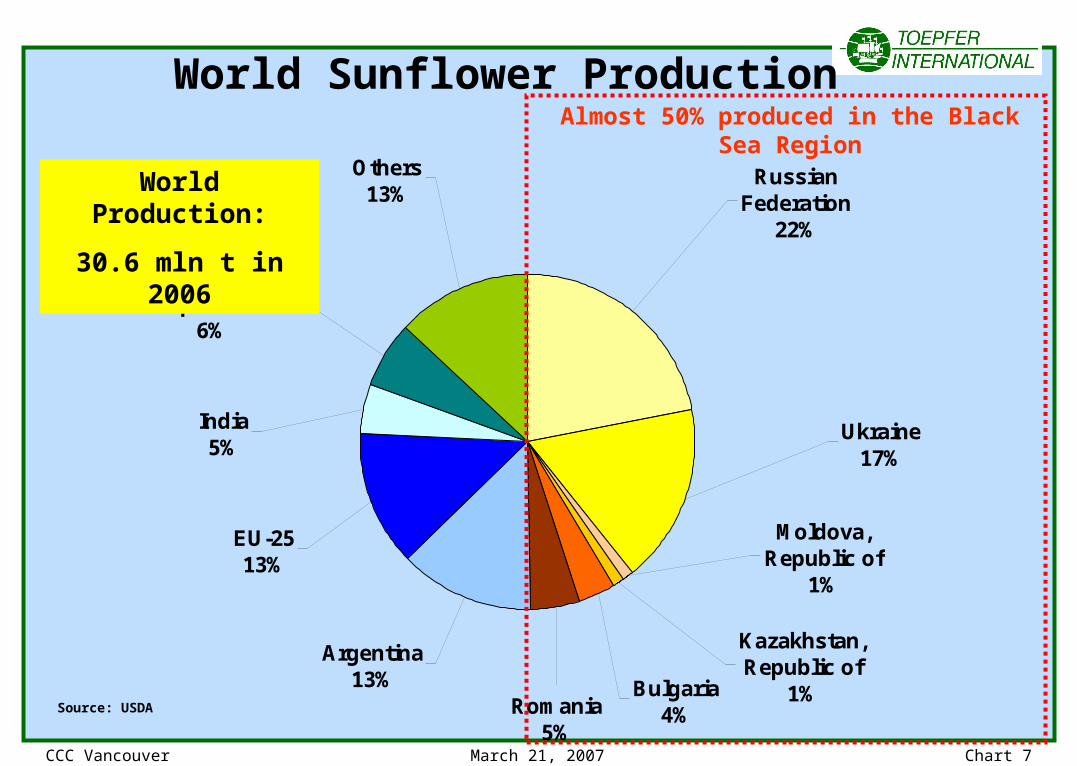

Russian Federation

22%

Ukraine17%

Kazakhstan, Republic of

1%

Moldova, Republic of

1%

Bulgaria4%Romania

5%

EU-2513%

India5%

China, Peoples Republic of

6%

Others13%

Argentina13%

World Sunflower Production

World Production:

30.6 mln t in 2006

Source: USDA

Almost 50% produced in the Black Sea Region

CCC Vancouver March 21, 2007 Chart 8

Russia: Sunflower S&D in mln t

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Area in mln ha 3.4 3.8 4.9 4.7 5.4 5.8

Yield in t/ha 0.78 0.97 1.00 1.03 1.19 1.16

Production 2.7 3.7 4.9 4.8 6.5 6.7

Total Supply 2.7 3.7 4.9 5.1 6.7 7.0

Exports 0.0 0.2 0.3 0.1 0.4 0.4

Crush 2.5 3.3 3.9 4.4 5.6 5.8

Total Use 2.7 3.5 4.3 4.8 6.0 6.3

Source: USDA

CCC Vancouver March 21, 2007 Chart 9

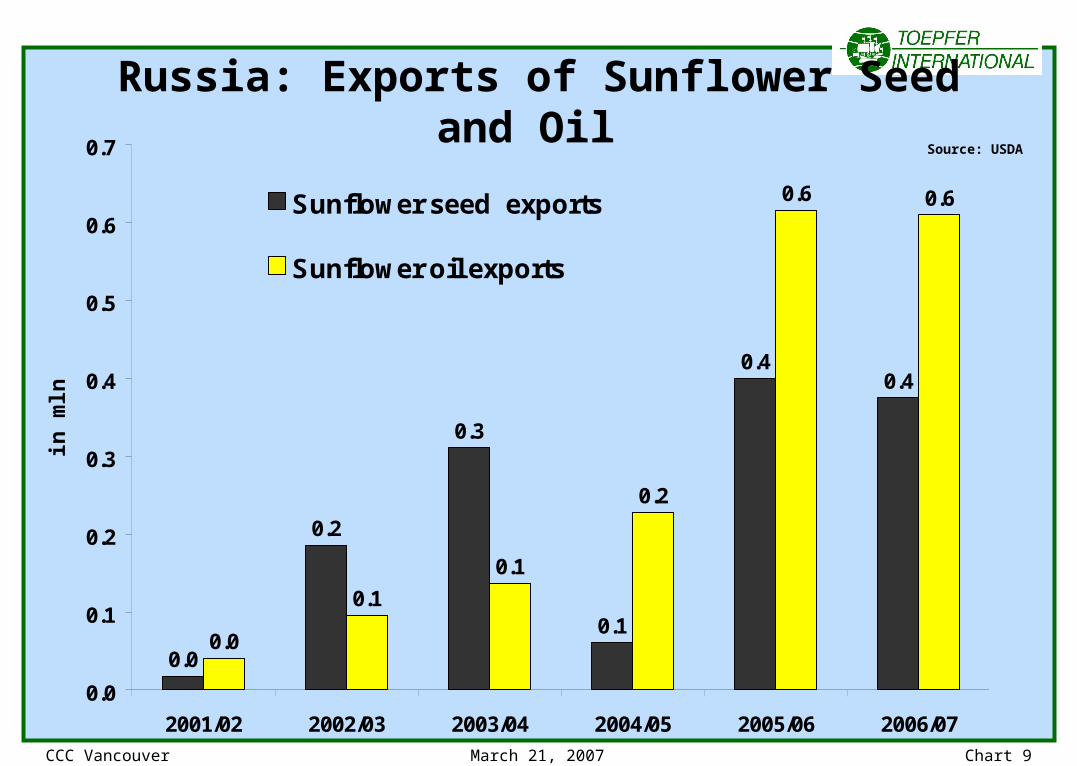

Russia: Exports of Sunflower Seed and Oil Source: USDA

0.0

0.2

0.3

0.1

0.40.4

0.0

0.1

0.1

0.2

0.6 0.6

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

in m

ln t

Sunflower seed exports

Sunflower oil exports

CCC Vancouver March 21, 2007 Chart 10

Ukraine: Sunflower S&D in mln t

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Area in mln ha 2.4 2.7 3.8 3.4 3.7 3.9

Yield in t/ha 0.94 1.20 1.12 0.90 1.27 1.36

Production 2.3 3.3 4.3 3.1 4.7 5.3

Total Supply 2.3 3.3 4.3 3.2 4.8 5.3

Exports 0.1 0.3 0.9 0.0 0.2 0.3

Crush 2.1 2.8 3.2 3.0 4.6 4.9

Total Use 2.2 2.9 3.2 3.0 4.6 4.9

Source: USDA

CCC Vancouver March 21, 2007 Chart 11

Ukraine: Exports of Sunflower Seed and Oil

0.1

0.3

0.9

0.0

0.2 0.30.3

0.91.0

0.6

1.5 1.5

0.0

0.5

1.0

1.5

2.0

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

in m

ln t

Sunflower seed exports

Sunflower oil exports

Source: USDA

CCC Vancouver March 21, 2007 Chart 12

Russia & Ukraine: Projection of Sunflower Production & Trade

• Sunflower acreage reached its peak (crop rotation)• Higher acreage possible in years with grain winter kill etc.• Yield increase due to better varieties (hybrids, high oleic) & farming practices• Crush capacity sufficient to crush the local crop• Seed exports only in very good crop years• Domestic use to increase slightly, exports to increase slightly as well

0.230.62 0.61 0.59 0.65 0.67 0.68

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

in m

ln t

Sunflower Oil Exports

Production

Crush

0.6

1.5 1.5 1.5 1.5 1.6 1.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

in m

ln t

Sunflower Oil Exports

Production

Crush

Projection Russia Projection Ukraine

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 13

Russia & Ukraine: Trends in Rapeseed Production

192276 303

578

781

1,024

1,254

1,485

0.97

1.10

1.24

1.10

1.241.28

1.32 1.35

0

400

800

1,200

1,600

2,000

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

in 1

,00

0 t

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Production

Yield in t/ha

284

654

1,736

1,980

2,313

2,660

51149

0.94

1.17

1.43

1.61

1.75 1.80 1.85 1.90

0

500

1,000

1,500

2,000

2,500

3,000

2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11

in 1

,00

0 t

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Production

Yield in t/ha

• New 00 winter-varieties available

• Royalty problem solved with hybrid seed

• Huge difference between well and poorly managed farms

– Poorly managed: < 1 t/ha– Well managed: > 4 t/ha in Ukraine

• Well managed farms have invested in:– Soil preparation & seeding technology– “Western-style” crop protection– Harvest technology

• Production Development in Russia – Based on export tax of 20 %– Profitability of competing grain– To triple by 2010

• Production development in Ukraine – No export tax so far– Logistics– Production to quadruple by 2010

Russia

Ukraine

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 14

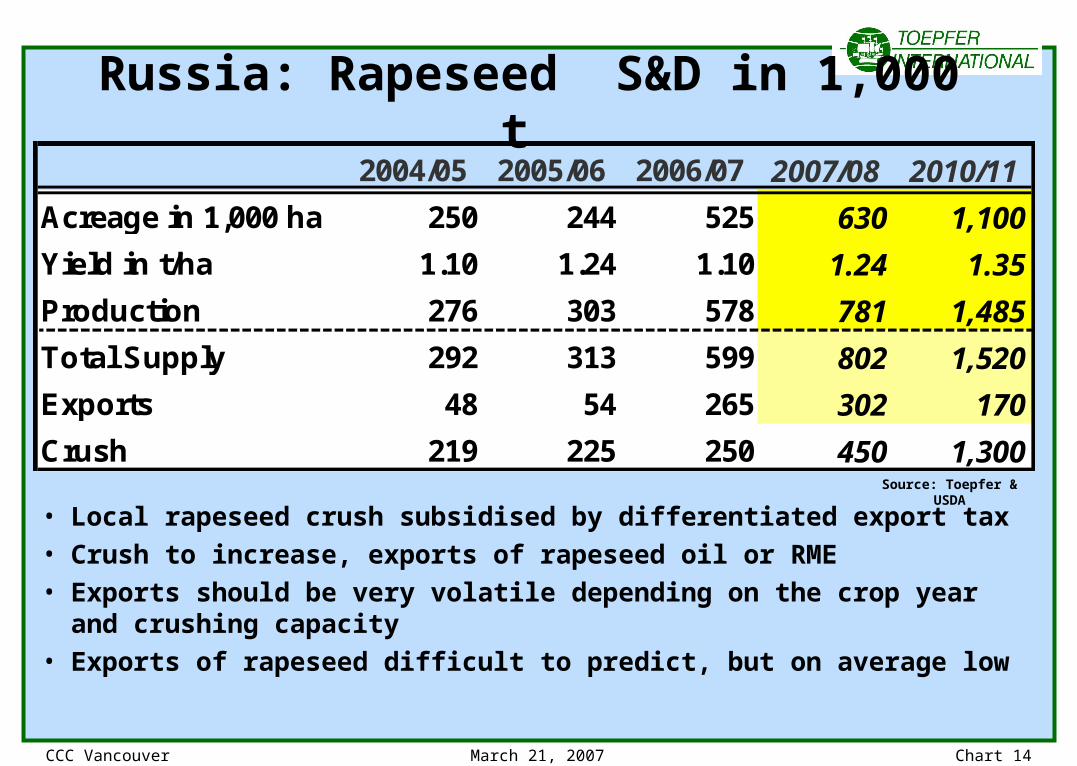

Russia: Rapeseed S&D in 1,000 t 2004/05 2005/06 2006/07 2007/08 2010/11

Acreage in 1,000 ha 250 244 525 630 1,100

Yield in t/ha 1.10 1.24 1.10 1.24 1.35

Production 276 303 578 781 1,485

Total Supply 292 313 599 802 1,520

Exports 48 54 265 302 170

Crush 219 225 250 450 1,300

• Local rapeseed crush subsidised by differentiated export tax• Crush to increase, exports of rapeseed oil or RME• Exports should be very volatile depending on the crop year

and crushing capacity• Exports of rapeseed difficult to predict, but on average low

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 15

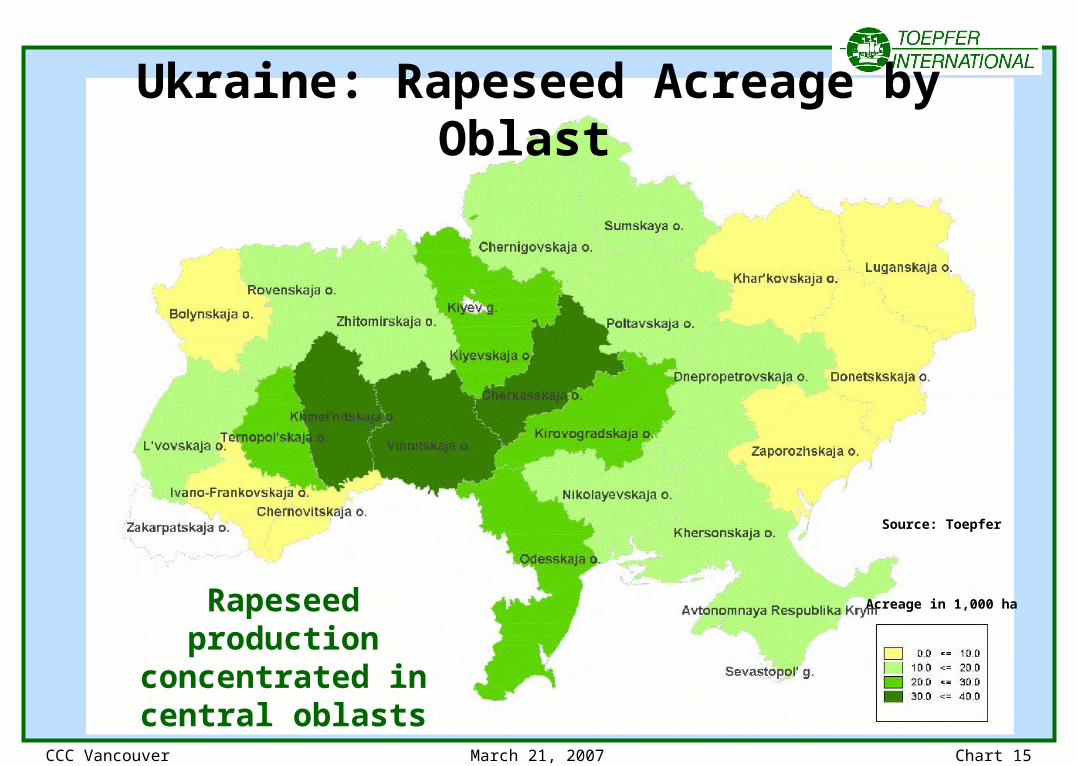

Ukraine: Rapeseed Acreage by Oblast

Rapeseed production concentrated in central oblasts

Source: Toepfer

Acreage in 1,000 ha

CCC Vancouver March 21, 2007 Chart 16

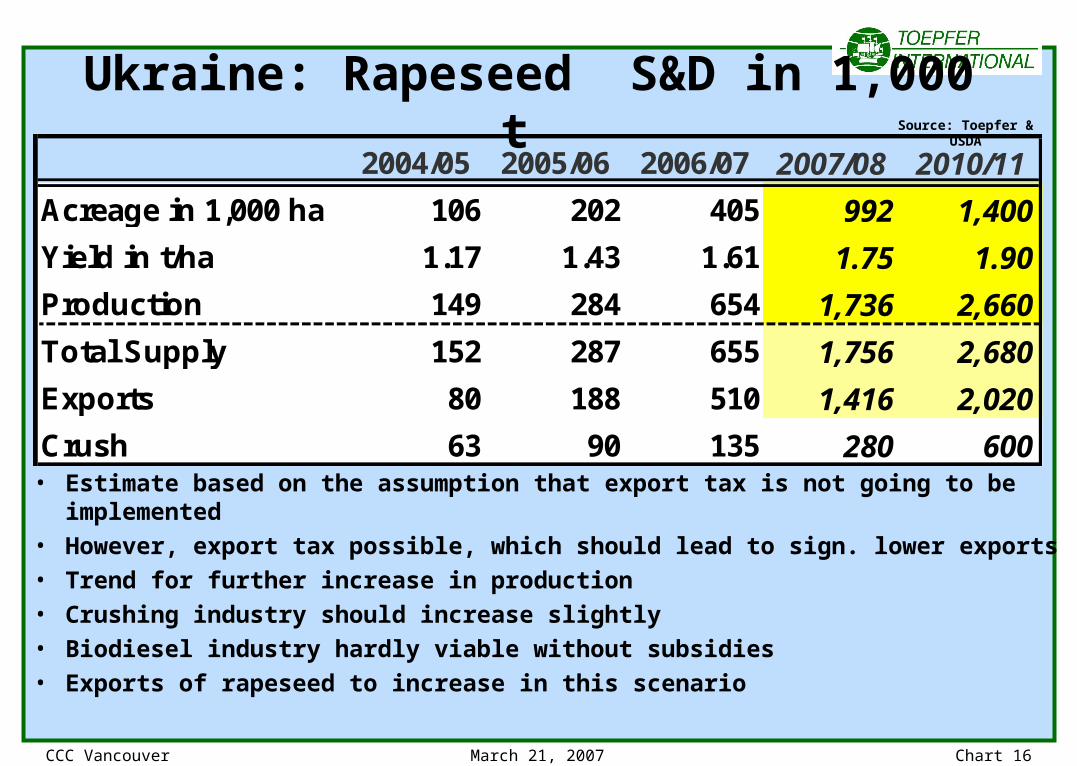

Ukraine: Rapeseed S&D in 1,000 t 2004/05 2005/06 2006/07 2007/08 2010/11

Acreage in 1,000 ha 106 202 405 992 1,400

Yield in t/ha 1.17 1.43 1.61 1.75 1.90

Production 149 284 654 1,736 2,660

Total Supply 152 287 655 1,756 2,680

Exports 80 188 510 1,416 2,020

Crush 63 90 135 280 600• Estimate based on the assumption that export tax is not going to be implemented

• However, export tax possible, which should lead to sign. lower exports

• Trend for further increase in production

• Crushing industry should increase slightly

• Biodiesel industry hardly viable without subsidies

• Exports of rapeseed to increase in this scenario

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 17

Ukraine, the new Competitor on the World Rapeseed Market in 2007/08

(Exports in 1,000 t, Estimates for 2006/07 and 2007/08)

Source: Toepfer

March 14, 2007

Importers 20

07

/08

20

06

/07

20

07

/08

20

06

/07

20

07

/08

20

06

/07

20

07

/08

20

06

/07

20

07

/08

20

06

/07

20

07

/08

20

06

/07

EU 4 4 100 320 10 75 114 544

Bangladesh 60 75 15 15 40 115 90

China 900 650 160 1,060 650

Japan 1,800 2,000 400 200 50 2,250 2,200

Pakistan 100 600 100 50 500 50 750 650

Turkey 0 50 100 16 150 115 250 181

UAE 50 200 50 150 250 200

Mexico 1,000 1,200 100 250 1,350 1,200

USA 1,300 785 1,300 785

not specified 130 130 50 25 50 36 50 40 20 40 300 281

total 5,344 5,694 615 240 350 67 1400 540 30 115 7,739 6,811

Russia TotalCanada Australia EU-27 Ukraine

CCC Vancouver March 21, 2007 Chart 18

Russia: Trends in Soybean Production (in mln t)

• Soybean production in Siberia and Southern Russia to increase• Russian soybean trade negligible, also in the next years• Soybean crush to increase due to strong demand increase for soybean

meal (livestock sector well protected from world market and very profitable, especially poultry production)

Summary: Soybean production to increase but little linkage to world markets

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Production 350 423 393 555 689 900

Import 64 15 1 40 2 2

Export 0 1 1 9 3 5

Crush 410 450 380 546 675 880

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 19

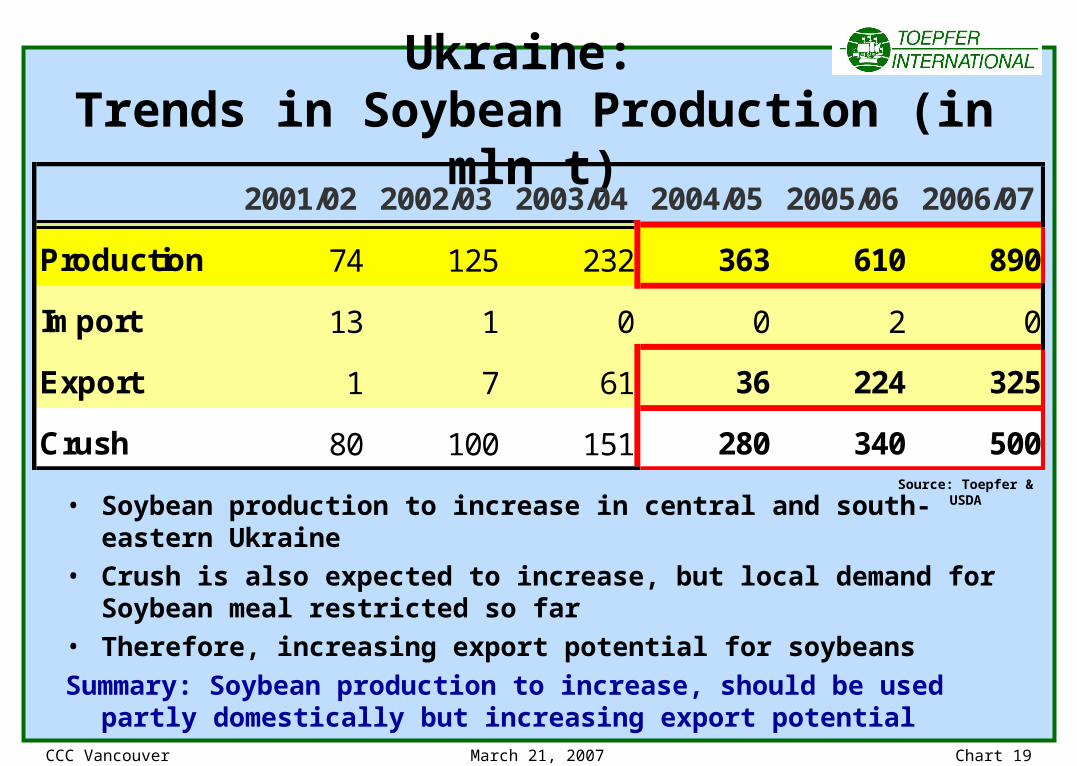

Ukraine: Trends in Soybean Production (in mln t)

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07

Production 74 125 232 363 610 890

Import 13 1 0 0 2 0

Export 1 7 61 36 224 325

Crush 80 100 151 280 340 500

• Soybean production to increase in central and south-eastern Ukraine• Crush is also expected to increase, but local demand for Soybean meal

restricted so far• Therefore, increasing export potential for soybeans

Summary: Soybean production to increase, should be used partly domestically but increasing export potential

Source: Toepfer & USDA

CCC Vancouver March 21, 2007 Chart 20

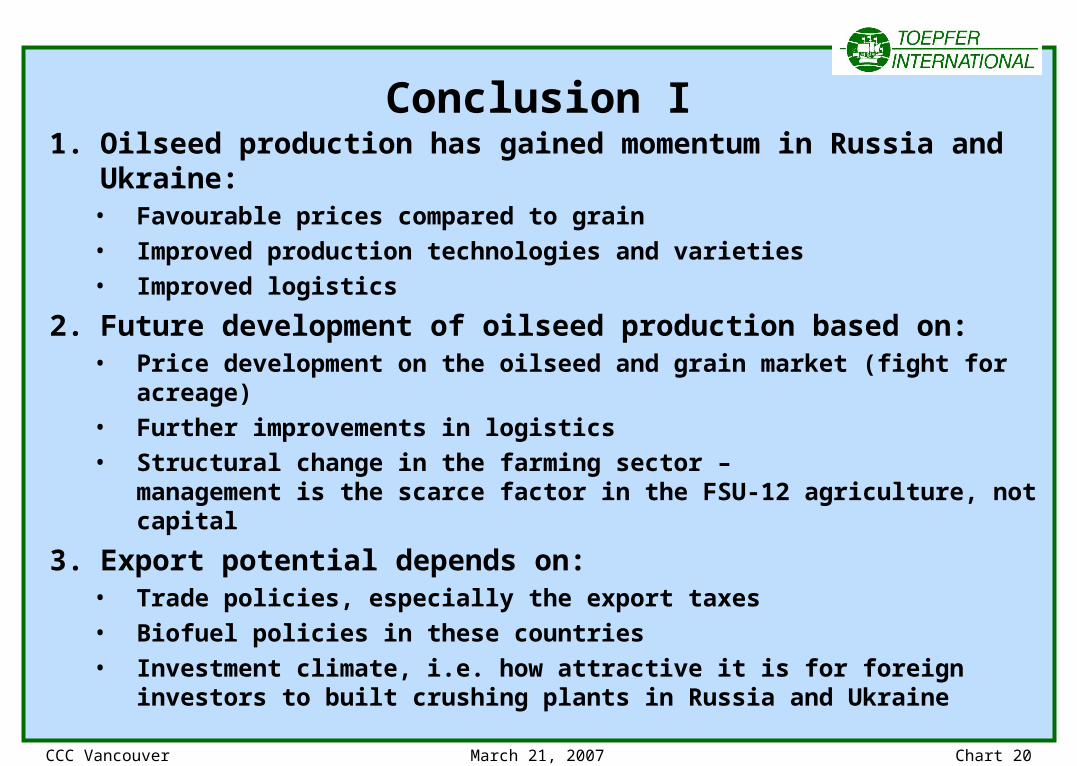

Conclusion I1. Oilseed production has gained momentum in Russia and

Ukraine:• Favourable prices compared to grain• Improved production technologies and varieties • Improved logistics

2. Future development of oilseed production based on:• Price development on the oilseed and grain market (fight for acreage)• Further improvements in logistics • Structural change in the farming sector –

management is the scarce factor in the FSU-12 agriculture, not capital

3. Export potential depends on:• Trade policies, especially the export taxes • Biofuel policies in these countries• Investment climate, i.e. how attractive it is for foreign investors to built

crushing plants in Russia and Ukraine

CCC Vancouver March 21, 2007 Chart 21

Conclusion II4. Impact on the Canadian Canola Industry:• Russia, but especially Ukraine new important

factor in World Rapeseed trade• However, production potential of all countries

urgently needed to meet the world’s ever increasing demand

• Interdependency of grain and oilseed markets• Markets will tell what to grow every year• Canadian farmers in excellent position to react in

spring on the potential competition from the Black Sea region and other exporters