multipurpose shipping report toepfer transport’s

TRANSCRIPT

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 1 May 15, 2019

Dear Reader,

The time charter market as well as the TMI have developed well while the demand situation indicates a significant slowdown of growth for the upcoming months. It remains unclear if and when the rates will be affected by this slowdown but we anticipate that the next 12-18 months may be challenging.

Zeamarine and Spliethoff are again making the biggest headlines, with Spliethoff’s further take-over of ex-HHL tonnage and Zeamarine changing its shareholder structure.

Another big issue in the coming months will be the exit of Nord LB from ship finance. Many MPP vessels are affected and the consequences for owners, operators, market values and the charter markets very much depend on the strategy the bank will pursue to achieve the exit goals.

The Toepfer Transport MPP report is now three years old and this is the first issue to be created under a new “Head of Research”. After three years it is time to start a comprehensive review of the report, and a new person in charge might add another perspective to our perception of the market.

You, our clients and readers, are very much invited to give us your positive and negative feedback on the report, to share your ideas and desires with us and to help us to deliver the most useful regular compilation of market information to you.

You can reach us by phone, by email ([email protected]) and on our brand-new Linkedin page http://linkedin.com/company/toepfertransport. Our MPP Team will also be present at the Breakbulk Europe in Bremen and we would be pleased to meet you there.

In the past three years “The times they are a-changing” has been the MPP market's catchy tune and it looks like this will continue, even if the pace of change slows down a bit. We anticipate movements on the vessel ownership side as well as on the newbuilding side and are looking forward to exciting weeks.

Yours sincerely,

TOEPFER TRANSPORT

CONTENT

TC Market Page 2 Newbuildings Page 4 S & P Highlights Page 5 Industry News Page 7 Top Market Player Page 8 Fleet Statistic Page 11 Cargo Demand Page 13 Quarterly Focus Page 15 Editorial Page 17

QUARTERLY HEADLINES - Nord/LB to exit ship finance within the next two to three years.- Zeaborn takes over the shares of New Mountain Capital in Zeamarine.- Spliethoff doubles the number of vessels taken over from bankrupt Hansa Heavylift.

ISSUE NO. 9 TOEPFER TRANSPORT’S MULTIPURPOSE SHIPPING REPORT

ISSUE NO. 13

TOEPFER TRANSPORT GMBH HAMBURG I SINGAPORE I SHANGHAI

CONTACT:

Telephone: +49 (0)40 32 58 210 [email protected]

VISITING:

Alstertor 1 I D-20095 Hamburg www.toepfer-transport.com

Registered subscription copy for: Subscription N

o. 17-89-TMI sent: 15.05.2019

This is a personalised passwort protected copy any unauthorised re-distribution is prohibited SAMPLE

TOEPFER TRANSPORT PAGE 2 May 15, 2019

MULTIPURPOSE SHIPPING REPORT

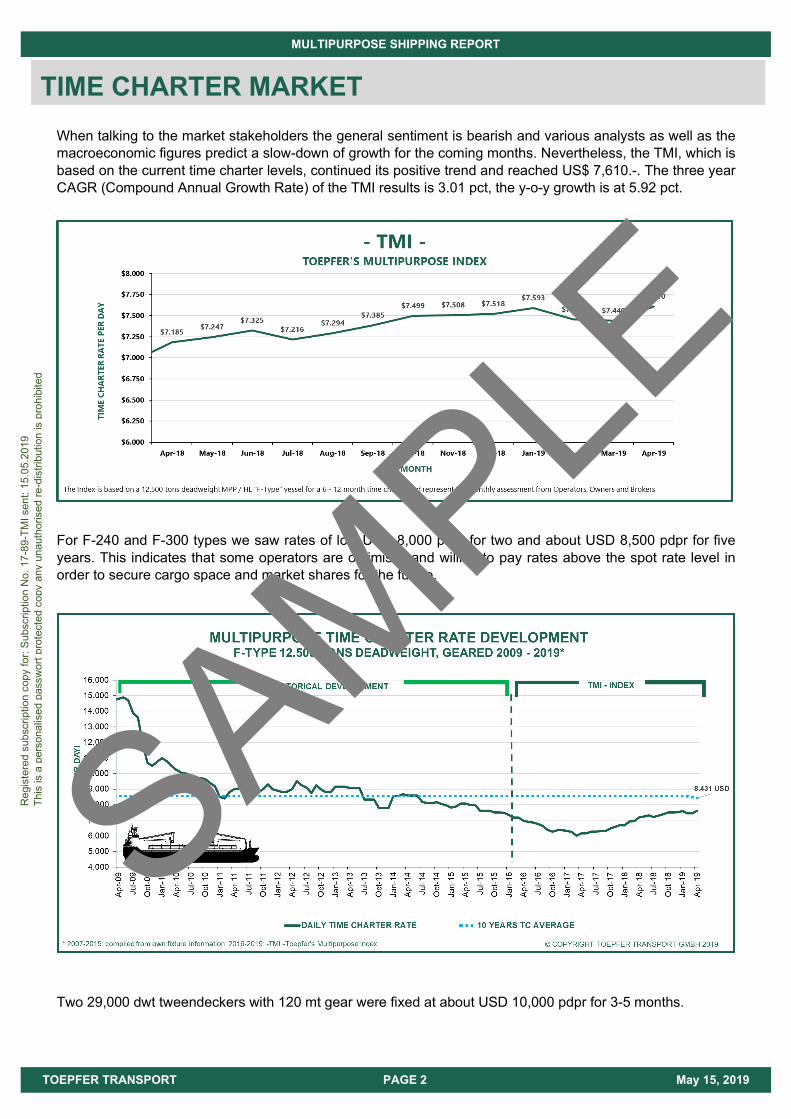

When talking to the market stakeholders the general sentiment is bearish and various analysts as well as the macroeconomic figures predict a slow-down of growth for the coming months. Nevertheless, the TMI, which is based on the current time charter levels, continued its positive trend and reached US$ 7,610.-. The three year CAGR (Compound Annual Growth Rate) of the TMI results is 3.01 pct, the y-o-y growth is at 5.92 pct.

For F-240 and F-300 types we saw rates of low USD 8,000 pdpr for two and about USD 8,500 pdpr for five years. This indicates that some operators are optimistic and willing to pay rates above the spot rate level in order to secure cargo space and market shares for the future.

Two 29,000 dwt tweendeckers with 120 mt gear were fixed at about USD 10,000 pdpr for 3-5 months.

TIME CHARTER MARKET

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 3 May 15, 2019

It is unclear if the predicted slowdown of economic growth will be reflected in upcoming MPP / HL time charter fixtures.

NAME DWAT BUILT MAX LIFTING GEAR ACCOUNT PERIOD LAYDAYS RATE US$BBC Congo 12.767 2009 300 mt 2 x 150 mt dship tct 45 - 60 days Mar 19 10.250Zea Walawe 12.337 2010 160 mt 2 x 80 mt, 1 x 45 mt dship tct Cont-FE Mar 19 rgn 8.450Celine C 12.959 2011 160 mt 2 x 80 mt dship tct Feb 19 rgn 8.400Helvetia 12.792 2005 240 mt 2 x 120 mt dship extended 12 mos Feb 19 7.500Louise Auerbach 12.651 2007 300 mt 2 x 150 mt dship 12 mos Mar 19 7.500Kingcup 28.261 2011 240 mt 2 x 120 mt, 1 x 45 mt BBC 3-5 mos Feb 19 rgn 10.000Kingfisher 28.341 2012 240 mt 2 x 120 mt, 1 x 45 mt BBC 3-5 mos Feb 19 rgn 10.000F-300 12.780 300 mt 2 x 150 mt Spliethoff 4-6 mos Mar 19 rgn 7.800F-300 12.780 300 mt 2 x 150 mt Spliethoff 4-6 mos Mar 19 rgn 7.800

TIME CHARTER FIXTURES

TIME CHARTER MARKET CONTINUED

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 4 May 15, 2019

With MV “Mick”, dship Carriers and HS Schiffahrt received their first out of four newbuildings ordered at Taizhou Sanfu Shipyard in 2018. The F-500 type vessel features 2 x 250 mt gear and a hold over 75 metres in length. The next vessel of this series is scheduled to be delivered in summer 2019 with two more sisters following in 2020. The vessels had initially been ordered by Zeaborn and were later cancelled due to heavy delays. Together with five vessels on order for Briese Germany, Taizou Sanfu has eight F-500 types in the orderbook. Briese is also discussing with the yard an additional order for five further F-500 types without ice class. (See our remarks on BBC Louise in the sales section)

In our last issue we relied on a press release from CSSC group which announced an order of eight newbuildings for Zeamarine at CSSC’s Hudong-Zhonghua (six units) and Huangpu Wenchong (two units) shipyards. We have to withdraw this information as the deal was not yet firm and there is still uncertainty as to whether it will ever firm up.

NYK is enquiring about 12600 dwt heavylift newbuildings with bridge forward design and 400 mt gear from Chinese yards.

Toepfer Transport is a panel member of the Chinese newbuilding price index (https://cnpi.org.cn/english/) which decreased for the first time in 20 months. For the MPP market this does not automatically lead to lower prices, but it indicates an increase in opportunities as the yards are looking for improved capacity utilisation.

We are monitoring many newbuilding enquiries which have some way to go before coming to fruition. At the current income levels, the quoted asset prices do not sustain suitable finance (if available) and sufficient return. Either the prices have to go down or the charter rates have to go up.

NAME DWAT BUILT MAX LIFTING GEAR OWNER SHIPYARD DATE PRICE US$NEW ORDERED VESSELS

No firm orders have been placed

NAME DWAT BUILT MAX LIFTING GEAR OWNER SHIPYARD DATE PRICE US$Mick 12.325 2019 500 mt 2 x 250 mt dship Carriers Taizhou Sanfu Shipyard Apr 19 18.70Zea Falcon 13.230 2019 900 mt 2 x 450 mt CSSC Leasing Huangpu Wenchong Shipyard Mar 19 40.00Zea Flash 13.230 2019 900 mt 2 x 450 mt CSSC Leasing Hudong Zhonghua Shipbuilding Feb 19 40.00Zea Focus 13.230 2019 900 mt 2 x 450 mt CSSC Leasing Hudong Zhonghua Shipbuilding Apr 19 40.00

DELIVERED VESSELS

DEADWEIGHT MAX LIFTING NO. CRANES CONTRACT 2002 CONTRACT 2007 CONTRACT 2011 CONTRACT 2015 JANUARY 2019 APRIL 20199.000 120 / 160 mt 2 9.50 20.00 14.00 15.00 14.00 14.00

12.500 500 mt 2 14.50 29.00 18.50 19.50 21.50 21.5030.000 700 mt 3-4 29.00 45.00 39.50 41.00 33.00 32

The above prices are for guidance only as these strongly depend on crane capacity and design / quality / makers list.

ASSET NEWBUILDING PRICES IN US$ MILLIONS

NEWBUILDINGS

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 5 May 15, 2019

Spliethoff doubled to ten the number of vessels taken over after the insolvency of Hansa Heavylift by taking over five P-Types. Four vessels have been taken over, renamed and reflagged to the Dutch Flag already. One additional vessel is still pending due to documentation issues. Here are the new names of the vessels:

While it was published by brokers that MV BBC Louise (2018 blt “New Great Dane F500 type”) was sold by Taizhou Sanfu Shipyard at a price of USD 18 million, our sources reported that the sale to German buyers is not yet finalised. The price level is said to be slightly below USD 18 million. This price level might be part of a kind of package deal together with a possible new building order for five additional F-500 at the shipyard. (See our newbuilding section)

The ARA Hamburg, ex BBC New York, which was said to be part of Nord LB’s 42 vessel MPP Portfolio, was picked up by ARA Shipping at USD 4.85 million. The deviation from our standard value assessment for 10 year old 9000 dwt ships, which is currently at USD 7 million, is reportedly caused by the vessel's poor condition.

Name ex-Name Type HandoverHudsongracht HHL Elbe F-300* Feb 2019Humbergracht HHL Tyne F-300* Jan 2019Heerengracht HHL Amur F-360 Jan 2019Houtmangracht HHL Mississippi F-360 Jan 2019Prinsengracht HHL New York P2-800 Jan 2019Pietersgracht HHL Kobe P2-800 Mar 2019tba HHL Rio de Janeiro P2-800 pendingPauwgracht HHL Richards Bay P2-1400 Mar 2019Paleisgracht HHL Tokyo P2-1400 Mar 2019Pijlgracht HHL Lagos P2-1400 Apr 2019Poolgracht HHL Fremantle P2-1400 Mar 2019

* BBC Campana Type

SPLIETHOFF FLEET ADDITIONS

NAME DWAT BUILT MAX LIFTING GEAR SELLER BUYER DATE PRICE US$SCM Elpida 7.725 2000 160 mt 2 x 80 mt Krey Schiffahrt undisclosed Apr 19 3.25HHL Kobe 19.863 2012 800 mt 2 x 400 mt; 1 x 120 mt Hansa HL / Commerzbank Spliethoff Group Mar 19HHL Rio de Janeiro 20.170 2009 800 mt 2 x 400 mt; 1 x 120 mt Hansa HL / Nord LB Spliethoff Group Mar 19HHL Richards Bay 19.329 2010 1400 mt 2 x 700 mt; 1 x 180 mt Hansa HL / Commerzbank Spliethoff Group Mar 19HHL Tokyo 19.496 2011 1400 mt 2 x 700 mt; 1 x 180 mt Hansa HL / Commerzbank Spliethoff Group Mar 19HHL Lagos 19.379 2011 1400 mt 2 x 700 mt; 1 x 180 mt Hansa HL / Commerzbank Spliethoff Group Mar 19HHL Fremantle 19.381 2011 1400 mt 2 x 700 mt; 1 x 180 mt Hansa HL / Commerzbank Spliethoff Group Mar 19BBC New York 9.770 2012 160 mt 2 x 80 mt Ems-Leda Shipping ARA Shipping, Netherlands Feb 19 4.85*Nordkap 8.275 2000 160 mt 2 x 80 mt Krey Schiffahrt undisclosed Jan 19 low 3* discount due to vessels condition

S & P DEALS

DEADWEIGHT MAX LIFTING NO. CRANES SALE 2002 SALE 2007 SALE 2011 SALE 2015 JANUARY 2019 APRIL 20199.000 120 / 160 mt 2 4.00 11.50 10.50 6.00 7.00 7.00

12.500 240 / 360 mt 2 6.00 14.50 13.50 8.50 7.75 7.7530.000 640 / 700 mt 3-4 10.00 28.50 19.50 10.50 12.00 12.00

The above prices are for guidance only as these strongly depend on crane capacity and design / quality / makers list.

ASSET 2ND HAND PRICES 10 YEARS OLD IN US$ MILLIONS

SALE & PURCHASE

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 6 May 15, 2019

NAME DWAT BUILT MAX LIFTING GEAR OWNER SHIPYARD DATE PRICE US$SCRAPPED OR LOST VESSELS

No removals have been reported

SALE & PURCHASE continued

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 7 May 15, 2019

In our last issue, the Industry News started with the insolvency proceedings against Hansa Heavylift which marked the exit of the PE investor Oaktree Capital Management from the company.

Yet another PE investor opted to exit their MPP investment but in a less dramatic way. Almost eleven years after investing in significant shares in Intermarine, New Mountain Capital chose to sell their remaining shares in Intermarine’s sucessor Zeamarine to its majority shareholder Zeaborn. With other equity funds usually operating on a five to seven years investment horizon, eleven years is an impressive holding period for a PE investor and therefore this step was expectable. At the same time, André Grikitis, the founder of Intermarine, CEO of Zeamarine and a personality who very much shaped the modern MPP market (and an important mentor to the author of these lines), stepped down “to spend more time with his family and to pursue other business ventures”.

Two former Intermarine executives, Lars Bonnesen and Christian Monsted, became shareholders in United Heavylift (UHL). Lars Bonnesen will be appointed as new Managing Director, while Christian Monsted will act as General Manager focusing on the development of international markets. Andreas Rolner, head of the projects department, together with UHL’s CFO Nicolas Dallmann, will be promoted to Managing Directors. UHL’s founder Lars Rolner will withdraw from UHL and take on the role of Managing Director at UHL’s holding company, United Shipping Group.

INDUSTRY NEWS

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 8 May 15, 2019

Struggling Nord LB, which held a Non-Performing shipping loan (NPL) portfolio of EUR 7.5 billion by the end of 2018, received an injection of EUR 3.7 billion new capital from its shareholders German Savings Banks Association (DSGV) and the state of Lower Saxony. The money is designated to be used for restructuring purposes. Restructuring in this case includes the bank deciding to fully exit ship financing within the next two to three years. A dedicated restructuring unit will be set up for this task. A significant amount of MPP vessels will be affected by the exit.

On April 10, Nord LB announced the completion of the sale of the EUR 2.6 billion shipping NPL portfolio known as “Big Ben” to an affiliate of Cerberus Capital. “Big Ben” comprises no fewer than 263 ships (including some MPP tonnage), bringing Nord LB’s NPL portfolio down to abt. EUR 4.9 billion. Cerberus’ intended average holding period for the 263 vessels is 18 months only.

As stated in our last issue, the projected sale of a Nord LB NPL portfolio of 42 MPP vessels to Auerbach failed due to various commercial and legal reasons. There are rumours that at least one German owner is about to restructure financing of 13 vessels from this portfolio. We anticipate further activity regarding MPP vessels financed by Nord LB in the next few months.

INDUSTRY NEWS CONTINUED

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 9 May 15, 2019

MACS and UAL have launched a joint service from Europe to East Africa serving Antwerp, Rotterdam, Hamburg, Nacala and Pemba with additional ports on inducement. The service targets Containers, Break Bulk, Project Cargo, Heavy Lifts and Neobulk Cargoes and will start with monthly sailings. Furthermore, UAL was appointed to act as sales agent for MACS in Houston.

At the same time, UAL also teamed up with BOCS by means of charter agreements to combine their liner services to West Africa. The alliance hopes to increase port coverage and the number of sailings while reducing the transit time. The offices, agencies and brand identities of both companies will remain unchanged.

DS Multibulk redelivered its chartered fleet and is now operating only one vessel, DS Wisconsin (a 2004 built F-240 type). The downsizing of the fleet is said to be accompanied by a corresponding reduction in staff.

The Hamburg-based maritime crowd investment start-up Marvest raised abt. EUR 1.1 million which will be used as mezzanine capital (subordinated loan) to refinance a portion of the equity used by an Auerbach controlled SPV to purchase the MV “Louise Auerbach” (2007 blt F-300). The competing platform New Shore Invest, on the other hand, intends to target eco newbuildings.

INDUSTRY NEWS CONTINUED

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 10 May 15, 2019

Ernst Russ Group and Peter Döhle Schiffahrts-KG sold their shares in technical manager Hammonia Reederei to Scandinavian investors. Hammonia is the technical manager of 17 MPP Vessels, most of them operated by Zeamarine, and also active in other market sectors.

Arkon Shipping & Projects was appointed by Rhenus Projects Logistics as their central chartering desk for worldwide project and heavylift cargoes. Rhenus became a shareholder in Arkon Shipping in 2017. At the same time, Arkon Shipping & Projects was appointed as representatives and commercial agents for Hass Logistic Ghana and Hass Freight Ghana. Hass Logistics offers agency services in all Ghanaian Ports while Hass Freight targets logistics services (local and governmental) for the Offshore, O&G, energy and breakbulk business. The owner of Hass Logistics is Hass Holding who own EuroAfrica Lines, a carrier offering a breakbulk liner service from North Europe to West Africa, a container feeder service from Poland to the UK, as well as two RoPax Services from Poland to Sweden.

Spliethoff’s HL brand BigLift, which also operates deck carriers, entered into a cooperation agreement with Chung Yang Shipping. BigLift will commercially operate Chung Yang’s four heavy load deck carriers. (See our quarterly focus)

INDUSTRY NEWS CONTINUED

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 11 May 15, 2019

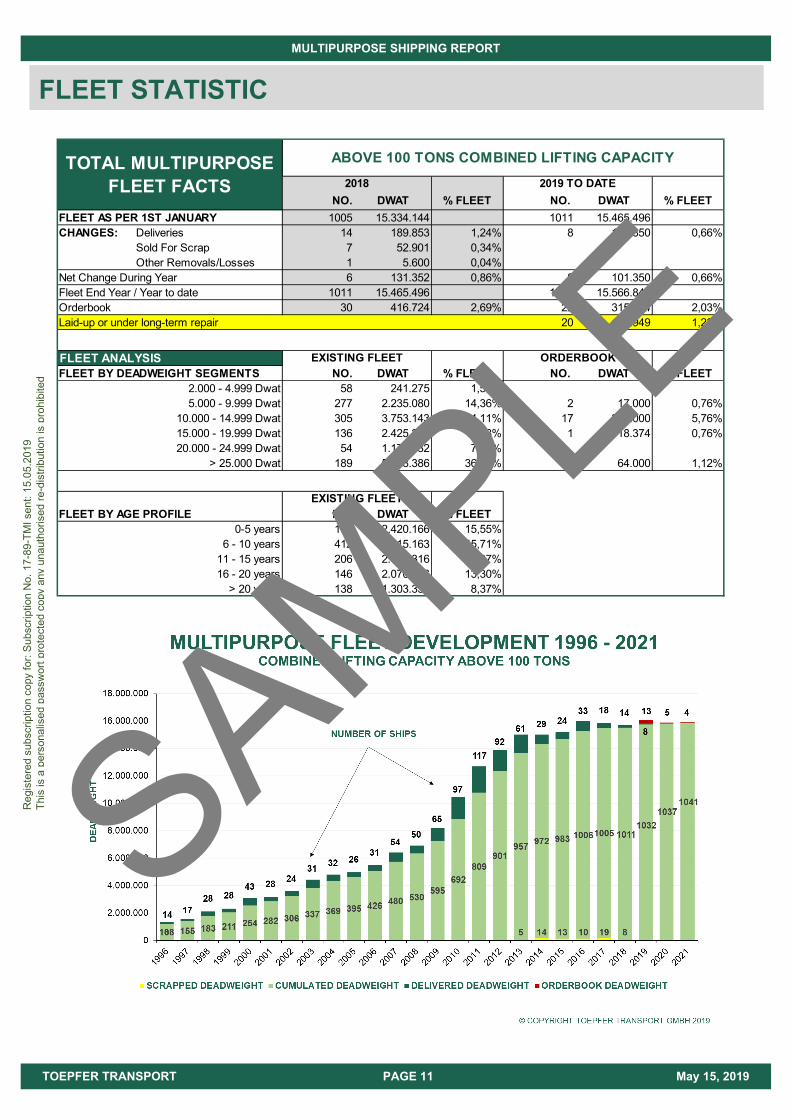

NO. DWAT % FLEET NO. DWAT % FLEETFLEET AS PER 1ST JANUARY 1005 15.334.144 1011 15.465.496CHANGES: Deliveries 14 189.853 1,24% 8 101.350 0,66%

Sold For Scrap 7 52.901 0,34% 0 0 0,00%Other Removals/Losses 1 5.600 0,04% 0 0 0,00%

Net Change During Year 6 131.352 0,86% 8 101.350 0,66%Fleet End Year / Year to date 1011 15.465.496 1019 15.566.846Orderbook 30 416.724 2,69% 22 315.374 2,03%Laid-up or under long-term repair 20 190.949 1,23%

FLEET ANALYSISFLEET BY DEADWEIGHT SEGMENTS NO. DWAT % FLEET NO. DWAT % FLEET

2.000 - 4.999 Dwat 58 241.275 1,55% 0 0 0,00%5.000 - 9.999 Dwat 277 2.235.080 14,36% 2 17.000 0,76%

10.000 - 14.999 Dwat 305 3.753.143 24,11% 17 216.000 5,76%15.000 - 19.999 Dwat 136 2.425.229 15,58% 1 18.374 0,76%20.000 - 24.999 Dwat 54 1.173.732 7,54% 0 0 0,00%

> 25.000 Dwat 189 5.738.386 36,86% 2 64.000 1,12%

FLEET BY AGE PROFILE NO. DWAT % FLEET0-5 years 117 2.420.166 15,55%

6 - 10 years 412 7.115.163 45,71%11 - 15 years 206 2.657.316 17,07%16 - 20 years 146 2.070.866 13,30%

> 20 years 138 1.303.336 8,37%

EXISTING FLEET

TOTAL MULTIPURPOSE FLEET FACTS

ABOVE 100 TONS COMBINED LIFTING CAPACITY2018 2019 TO DATE

EXISTING FLEET ORDERBOOK

FLEET STATISTIC

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 12 May 15, 2019

NO. DWAT % FLEET NO. DWAT % FLEETFLEET AS PER 1ST JANUARY 413 6.822.362 419 6.889.560CHANGES: Deliveries 8 88.642 1,30% 8 101.350 1,47%

Sold For Scrap 2 21.444 0,31% 0 0 0,00%Other Removals/Losses 0 0 0,00% 0 0 0,00%

Net Change During Year 6 67.198 0,98% 8 101.350 1,47%Fleet End Year / Year to date 419 6.889.560 427 6.990.910Orderbook 28 352.724 5,12% 20 251.374 3,60%Laid-up or under long-term repair 6 52.618 0,75%

FLEET ANALYSISFLEET BY DEADWEIGHT SEGMENTS NO. DWAT % FLEET NO. DWAT % FLEET

2.000 - 4.999 Dwat 10 39.844 0,57% 0 0 0,00%5.000 - 9.999 Dwat 97 788.746 11,28% 2 17.000 2,16%

10.000 - 14.999 Dwat 147 1.860.534 26,61% 17 216.000 11,61%15.000 - 19.999 Dwat 63 1.149.430 16,44% 1 18.374 1,60%20.000 - 24.999 Dwat 20 441.056 6,31% 0 0 0,00%

> 25.000 Dwat 90 2.711.300 38,78% 0 0 0,00%

FLEET BY AGE PROFILE NO. DWAT % FLEET0-5 years 59 1.187.282 16,98%

6 - 10 years 181 3.310.243 47,35%11 - 15 years 96 1.246.667 17,83%16 - 20 years 60 892.709 12,77%

> 20 years 31 354.010 5,06%

EXISTING FLEET

TOTAL MULTIPURPOSE FLEET FACTS

ABOVE 240 TONS COMBINED LIFTING CAPACITY2018 2019 TO DATE

EXISTING FLEET ORDERBOOK

FLEET STATISTIC continued

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 13 May 15, 2019

CARGO DEMAND CHARTS

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 14 May 15, 2019

CARGO DEMAND CHARTS CONTINUED

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 15 May 15, 2019

Let’s talk about disruption The theory of disruptive innovation was developed by Harvard professor Clayton M. Christensen and later (as long ago as 1997) made popular by his book “The Innovators Dilemma”. He was working on research in the disk-drive industry. (Anyone with children might now imagine the bizarre fascination you are confronted with when talking about disk drives to teenagers growing up with solid state memory and cloud technology.)

The Christensen Institute described it as follows: “The theory explains the phenomenon by which an innovation transforms an existing market or sector by introducing simplicity, convenience, accessibility, and affordability where complication and high cost are the status quo. Initially, a disruptive innovation is formed in a niche market that may appear unattractive or inconsequential to industry incumbents, but eventually the new product or idea completely redefines the industry.” (source: https://www.christenseninstitute.org/key-concepts/disruptive-innovation-2/)

Niche market? … Ah! That is how we usually describe MPP - so let’s share a few thoughts and ideas about what is going on in the world that may affect our business.

A Change of approach. We see more and more shippers and operators questioning if project cargoes by nature require highly sophisticated vessels with specialised versatile gear. Why not go simple with easy to build and less complicated vessels with lower asset prices, like, e.g., a deck carrier?

In December we saw a Chinese deck carrier loading 156(!) MHI Vestas V120 blades, each 60 metres in length, in one shipment on one vessel from Dafeng, China to Ferrol, Spain (Video: https://www.youtube.com/watch?v=JCls1oHJcMU). The vessel is owned by a Chinese government outfit named Guangzhou Salvage (GZ Salvage) and was booked and operated by United Heavy Lift/United Wind Logistics (UWL) who act as commercial agents for the GZ Salvage heavy load deck carrier fleet in Europe. Due to the bridge forward design and special frames it was possible to stack the blades five tiers high. UWL is experienced in using deck carriers for Wind-Power shipments. They operate the small deck carrier Vestwind in European on- and offshore wind power and have two similar vessels with optional dynamic positioning capabilities on order at a Chinese yard.

After the four sister deck-carrier venture with Roll Group was dissolved, Big Lift operated their two sisters on their own and further expanded their always big presence in energy infrastructure logistics. Similar to UWL’s cooperation, Big Lift recently teamed up with the Korean deck carrier operator Chung Yang and will commercially operate Chung Yang’s heavy load deck carriers.

Deck carriers are, from a construction point of view, less complex and cheaper to build than conventional MPP vessels. Furthermore a steadily increasing number of ports now offer high crane capacities to serve gearless vessels. The comparatively low asset prices for the vessels as well as the scale effects which can be achieved by offering large deck space with high stack loads (no hold below…) enable the operators to offer very competitive rates for the cargo. Disruptive innovations are not innovations that improve good products. They make products, in this case breakbulk transportation, more accessible and affordable. They create a new market, which may disrupt an existing and working market. For certain cargoes, deck carriers more and more turn out to be serious competition for MPP vessels and a new deck carrier market gets more and more established.

Last week Cosco received a 62,000 dwt pulp carrier from the Group’s own shipyard, Cosco Heavy Industries, at Dalian. It is the first vessel of a series of nine ships. As the commodity flow in the pulp trade is very imbalanced, the rates for the vessels usually include the costs for ballasting back to the loading area. Any cargo taken on the back haul helps to improve the rates as well as the income. The new vessels are therefore equipped with two 75-ton swl single-boom cranes and one 2 x 75-ton swl twin-boom crane with a maximum lifting capacity of 150 tons. Cosco aims to load Breakbulk and Project cargoes on the ships to achieve a good profit contribution on the backhaul of the pulp trade. (Please find more about the pulp trade in our last issue)

QUARTERLY FOCUS

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 16 May 15, 2019

Additive manufacturing (i.e. 3D printing and similar methods) is a mixed blessing. Huismann recently announced that they have sold the first two class approved (ABS) off-shore crane hooks which have been crafted by additive manufacturing. The hooks have SWL of 36 mt and the production was much faster than it would have been with forging or casting (Video: https://www.youtube.com/watch?v=RK1tZoiPF8c). Additive manufacturing will increase the speed and lower the costs for building ships and cargo equipment in the future. At the same time it will facilitate local production of complex structures and systems which then do not have to be carried by ships to remote destinations. While transportation technology will benefit from additive manufacturing, it might at the same time very probably endanger the demand for transportation of manufactured goods.

The deglobalisation of manufacturing goes along with a political deglobalisation and protectionism which can be seen in various countries (e.g. “Brexit”, “America First”, Trade Wars etc.) and may become a risk to trade. There is a correlation between our business and free trade. Protective measures for local economies may be based on good grounds, but should always remain reasonable from a global perspective.

Our niche market is in a consolidation process which is driven by weak markets and the necessity to lower costs. One key aspect of the consolidation is the realisation of economies of scale. But when reaching a certain size this may turn into what economists call “diseconomies of scale”, a situation in which the effort to operate a large structure gets more expensive than the cost savings which result from the large scale. The more diverse a company is, the faster such a situation may appear.

Another aspect of consolidation is the possible creation of a cluster-risk. The MPP market tends to be too small to create operators and owners that are “too big to fail”. The past shows some good, clear examples of this thesis. The larger the market stakeholders get, the larger will be the impact for all stakeholders if one of them fails.

Finally, we look at digitalisation. The shipping media is full of news about new digital market platforms, block chain initiatives and digital freight forwarders. This all started in the late 1990s and none of them so far proved to be as disruptive as predicted. One of the reasons for this situation is that they offered a limited level of added value and innovation and mostly focused on enhancing well established workflows and methods instead of re-thinking them. This has a lot to do with the complexity of our business, which gets even more complicated when going down to the niches.

The most promising digital solutions are the ones which focus on the prevailing problems of shipping, like “Marvest” and “New Shore Capital”, who try to raise equity and/or mezzanine capital for ship finance by means of crowd funding. These pioneers are trying to establish a more successful “digital” approach to our business by tackling the gap owners face when seeking finance for ships while at the same time offering an interesting product for small-scale investors.

All the above mentioned things and many more will sooner or later lead to disruption and transformation of our business. Nobody knows how and when and what measures have to be taken to adapt to it. Luckily, this is how shipping and especially MPP has always been and what drives us and makes us enjoy our daily work: A permanent and exciting challenge.

* * * * *

QUARTERLY FOCUS continued

Reg

iste

red

subs

crip

tion

copy

for:

Subs

crip

tion

No.

17-

89-T

MI s

ent:

15.0

5.20

19

This

is a

per

sona

lised

pas

swor

t pro

tect

ed c

opy

any

unau

thor

ised

re-d

istri

butio

n is

pro

hibi

ted

SAMPLE

MULTIPURPOSE SHIPPING REPORT

TOEPFER TRANSPORT PAGE 17 May 15, 2019

TOEPFER TRANSPORT'S MULTIPURPOSE SHIPPING REPORT published by:

TOEPFER TRANSPORT GMBH

CONDITIONS OF SALE

Toepfer Transport's Multipurpose Shipping Report is published four times a year and subscriptions are available for an annual fee of currently € 2.950. - excluding VAT.

Within this subscription, the subscriber can register up to 10 individual named e-mail recipients within his organisation. Group e-mails (for example "info@..." or "management@...") will not be considered.

The report is solely issued via email as an individualised, password protected pdf - file. Hard copies are available upon request.

The subscription will be automatically renewed for a further year (i.e. 4 issues) unless the subscriber sends a written cancellation note within 4 weeks after receipt of the 3rd issue of the current subscription period.

Alternatively we offer our Multipurpose Shipping Report for a fee of currently € 950.- excluding VAT per individual report.

To subscribe, unsubscribe or for any further requests related to Toepfer Transport's Multipurpose Shipping Report, please send an e-mail to:

[email protected] with attention Mr. Yorck Niclas Prehm.

The information supplied within our report is believed to be correct but the accuracy thereof is not guaranteed and the Company and its employees cannot accept liability for loss suffered in consequence of reliance on the information provided. Provision of this data does not obviate the need to make further appropriate enquiries and inspections. The information is for the use of the recipient only and is not to be used in any documents without the written permission of Toepfer Transport GmbH.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, except for the inclusion of brief quotations in a review, without prior permission in writing from the publishers.

EDITORIAL AND COMMERCIAL INQUIRIES

TOEPFER TRANSPORT GMBH HAMBURG I SINGAPORE I SHANGHAI

SALE & PURCHASE I NEWBUILDINGS I CHARTERING I MARKET ANALYSIS I VALUATIONS Clemens Toepfer Hannes Hollaender Yorck Niclas Prehm Carlo Brandt Panos Pantelis Yuan Xiaofei Jennifer Shrestha Cornelius Schröder Magnus Andersen Richard Wetzki Johannes Just

SAMPLE