fuedi plenary meeting brussels, november 7th, 2008 mr. ignacio machetti consorcio de compensación...

TRANSCRIPT

FUEDI Plenary MeetingBrussels, november 7th,

2008

Mr. Ignacio MachettiMr. Ignacio MachettiConsorcio de Compensación de Seguros - General ManagerConsorcio de Compensación de Seguros - General Manager

The ‘Consorcio de Compensación de Seguros’:

a public instrument for the Spanish insurance

3

GENERAL CONTENTSGENERAL CONTENTS

I. The ‘Consorcio de Compensación de Seguros’

1. The Institution

2. Its Functions

II. Main features of the ‘extraordinary risks’ system

III. Some statistical data

4

Damages from Civil War (1936-1939)

‘‘Riot RisksRiot Risks Compensation Consortium’ (1941) Compensation Consortium’ (1941)

Provisional insurance tool

Severe damages in

Santander (1941) - fire

Canfranc (1944) - fire

El Ferrol (1944) - fire

Cádiz (1947) - mine explosion

Alcalá de Henares (1948) - gunpowder arsenal explosion

a) Short historical overview

I. The ‘Consorcio de Compensación de Seguros’I. The ‘Consorcio de Compensación de Seguros’

1. The Institution

5

‘‘Consorcio de Compensación de Seguros’Consorcio de Compensación de Seguros’(Law of december 16th, 1954)(Law of december 16th, 1954)

‘‘Consorcio de Compensación de Seguros’Consorcio de Compensación de Seguros’(Law of december 16th, 1954)(Law of december 16th, 1954)

Permanent insurance tool

1. New legal nature2. Board of Directors3. Principles:

- Subsidiarity (no competence: collaboration with the industry)- Flexibility and adaptability- Multi-task institution

Law of december 19th, 1991: Legal Statute

6

Own legal personality

Own assets (independent from the State’s)

Subject to laws regulating privates insurance companies

The CCS is a PUBLIC BUSINESS INSTITUTIONThe CCS is a PUBLIC BUSINESS INSTITUTIONThe CCS is a PUBLIC BUSINESS INSTITUTIONThe CCS is a PUBLIC BUSINESS INSTITUTION

b) Legal nature and structure

7

GENERAL MANAGERGENERAL MANAGER

FINANCIAL DIRECTOR

TECHNICAL & REINSURANCE

DIRECTOR

BOARD OF DIRECTORSBOARD OF DIRECTORS(equal private-public composition)

Chairman:DIRECTORATE-GENERAL FOR INSURANCE AND PENSION FUNDS

BOARD OF DIRECTORSBOARD OF DIRECTORS(equal private-public composition)

Chairman:DIRECTORATE-GENERAL FOR INSURANCE AND PENSION FUNDS

18 REGIONAL OFFICES NETWORK

MINISTRY OF ECONOMY AND FINANCEMINISTRY OF ECONOMY AND FINANCEMINISTRY OF ECONOMY AND FINANCEMINISTRY OF ECONOMY AND FINANCE

SECRETARIAT GENERAL

OPERATIONS DIRECTOR

I.T.

DIRECTOR

8

9 MEMBERS FROM PRIVATE INSURANCE

COMPANIES:

- ALLIANZ

- AXA

- CASER

- CATALANA OCCIDENTE SEGUROS

- ESPAÑA SEGUROS

- GENERALI

- MAPFRE

- MUTUA PELAYO

- VIDACAIXA

CHAIRMANCHAIRMAN(Director-General for Insurance and Pension Funds)

CHAIRMANCHAIRMAN(Director-General for Insurance and Pension Funds)

18 MEMBERS appointed by theMinister of Economy and Finance18 MEMBERS appointed by theMinister of Economy and Finance

9 MEMBERS FROM

THE GOVERNMENT

Board of Directors

9

1. EXTRAORDINARY

RISKS

1. EXTRAORDINARY

RISKS2. MOTOR

INSURANCE

2. MOTOR

INSURANCE3. AGRICULTURAL

INSURANCE

3. AGRICULTURAL

INSURANCE

2.1. INSURANCE DUTIES

2. Its Functions

10

Unidentified vehicles (2nd Directive)

Stolen vehicles (2nd Directive: optional)

Uninsured vehicles(2nd Directive)

Winding-up undertakings

Disputed claims (Controversy)

GUARANTEE FUND:

F.I.V.A. (Insured Vehicles Registry)

Information Centre

NON INSURANCE DUTIES:

Public Vehicles (on request)

Unaccepted (rejected) Private VehiclesDIRECT INSURANCE:

Motor InsuranceMotor Insurance

11

InsuranceContract

POLICYHOLDERSPOLICYHOLDERSPOLICYHOLDERSPOLICYHOLDERS

AGROSEGUROAGROSEGUROAGROSEGUROAGROSEGURO

CCS: 10%

Company 1 _%

Company 2 _%

Company n _%

. . .

ReinsuranceContract

C.C.S.C.C.S.C.C.S.C.C.S.

REINSURANCE:Financial

protection of the system

PREMIUM SUBSIDIZED BY THE PREMIUM SUBSIDIZED BY THE STATE AND REGIONAL STATE AND REGIONAL

GOVERNMENTS (UP TO 50%)GOVERNMENTS (UP TO 50%)

Agricultural Insurance National SystemAgricultural Insurance National System

12

4. WINDING-UP

ACTIVITY

4. WINDING-UP

ACTIVITYAdministration of public

funds for Export Credit

Insurance

Administration of public

funds for Export Credit

Insurance

FIVA (Management of the

National Registry of Insured

Vehicles)

FIVA (Management of the

National Registry of Insured

Vehicles)

2.2. NON INSURANCE DUTIES

13

Floodsand sea dashes

EarthquakesTsunamis

Volcanic eruptionsStorms

(tornadoes and gusts of windabove 135 km./h. included)

Falling of meteorites

TerrorismRebellion

InsurrectionRiots

Mob misbehaviourActions of armed forces

in peacetime

NATURAL PERILSNATURAL PERILS SOCIAL-POLITICAL EVENTSSOCIAL-POLITICAL EVENTS

II. Main features of the ‘extraordinary risks’ systemII. Main features of the ‘extraordinary risks’ system

II.1. What are the ‘extraordinary risks’?

14

INSURANCE POLICYINSURANCE POLICY- Damage to things

- Life or Personal Accidents

INSURANCE POLICYINSURANCE POLICY- Damage to things

- Life or Personal Accidents

2 simultaneous contracts2 simultaneous contracts

ORDINARY RISKS

(fire, theft, etc.)

Private insurer

(Voluntary premium)

EXTRAORDINARY RISKS

(flood, terrorism, etc.)

Consorcio de Compensación de Seguros

(Compulsory premium –surcharge-)

II.2. How are they covered?

15

Only losses from events occurred in Spain + personal injuries from events occurred abroad

Direct material damages (repair or replacement).

Supplementary expenses (mud extraction; demolition and removal; rubble disposal or transport to landfill).

Business interruption.

Death.

Permanent disability.

Temporary disability.

PROPERTYPROPERTY ACCIDENTS and LIFEACCIDENTS and LIFE

II.3. What kind of losses does it compensate for?

16

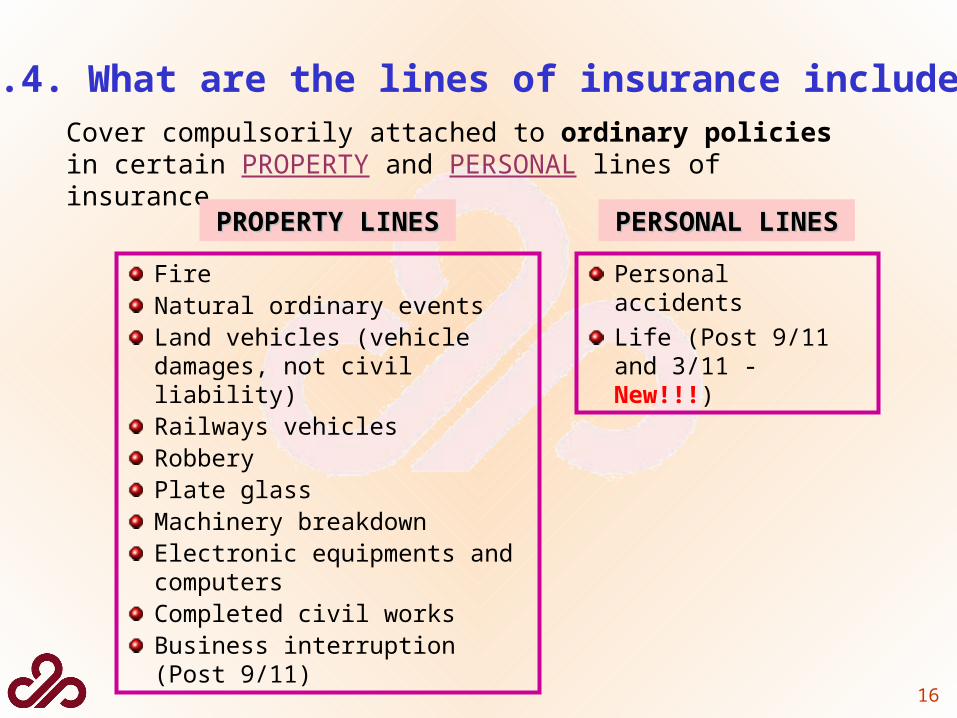

Cover compulsorily attached to ordinary policies in certain PROPERTY and PERSONAL lines of insurance

FireNatural ordinary events Land vehicles (vehicle damages, not civil liability) Railways vehicles RobberyPlate glassMachinery breakdownElectronic equipments and computersCompleted civil worksBusiness interruption (Post 9/11)

Personal accidentsLife (Post 9/11 and 3/11 - New!!!)

PROPERTY LINESPROPERTY LINES PERSONAL LINESPERSONAL LINES

II.4. What are the lines of insurance included?

17

The CCS covers the extraordinary risks through the ordinary policy issued by the company (taking into account the same amount insured and the same compensation conditions):

- The company manages the policy.

- CCS manages the loss claims and compensation (adjustment included).

The ‘Consorcio’ does not directly underwrite the coverage

18

Reference point

The same goods or persons

The same insured capital

The same compensation conditions

establishedin the

ordinarypolicy

For direct material damages (except for cars and housing): 7% of the indemnification amount.

For business interruption: the same deductible established in the ordinary policy.

For personal injuries: None.

Deductibles:

II.5. What are the terms (clauses) of the compensation?

19

The system doesn’t take into account:

the amount of the losses

the number of insured persons affected

the size of the affected area

A previous official declaration about thecatastrophic nature of the event is NOT required

II.6. Objectively defined coverage

20

To be applied on amount insured in the ordinary policy

Insurance companies collect surcharges together with their premiums

Companies will credit surcharges to ‘Consorcio’ on a monthly basis

Collection commission retained by the companies: 5%

II.7. How is it financed?

1st) Compulsory premium (surcharge) in favor of the CCS:

21

SURCHARGE RATES:

a) For property insurances a.1.) Direct damages:

. Housing: 0.09 per thousand. . Offices: 0.14 per thousand. . Business, Shopping centres: 0.18 per thousand. . Industrial risks: 0.25 per thousand. . Motor vehicles: rate according to type of vehicle. . Civil works: rate according to type (up to 1.95 per thousand for

industrial ports).

a.2.) Business interruption: . Housing: 0.005 per thousand on amount insured for material

damages. . Other risks: 0.25 per thousand on amounts insured for business

interruption.

b) For accidents and life insurance: 0.005 per thousand.

22

2nd) Other financial revenues:

Investment returns.

23

Built up with total profits after tax(Amount in 2007: aprox. 4.1 billion €)

Built up with total profits after tax(Amount in 2007: aprox. 4.1 billion €)

IT IS A REAL ‘CATASTROPHE FUND’IT IS A REAL ‘CATASTROPHE FUND’IT IS A REAL ‘CATASTROPHE FUND’IT IS A REAL ‘CATASTROPHE FUND’

Regulations identical to those of the private insurance companies (P. for outstanding claims, P. for unearned premiums…).

Special regulation for the Equalization Reserve.

State Guarantee (never applied).

II.8. Technical Provisions

24

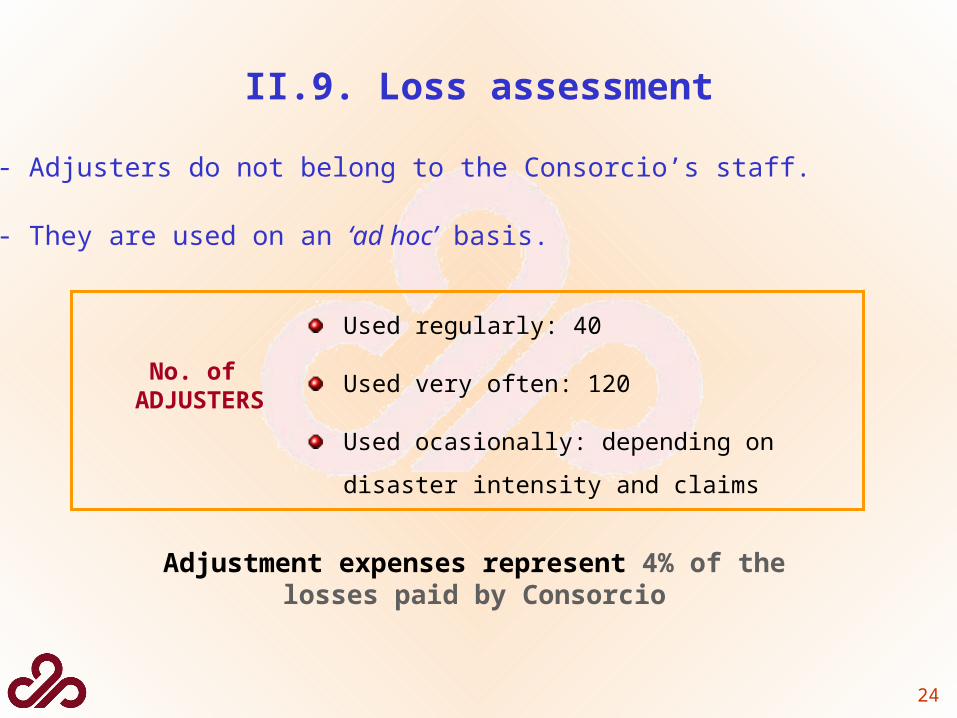

- Adjusters do not belong to the Consorcio’s staff.

- They are used on an ‘ad hoc’ basis.

No. of ADJUSTERS

Used regularly: 40

Used very often: 120

Used ocasionally: depending on disaster

intensity and claims

Adjustment expenses represent 4% of the losses paid by Consorcio

II.9. Loss assessment

25

Total claims distribution per causes Total claims distribution per causes (period 1987 – 2007)Total claims distribution per causes Total claims distribution per causes (period 1987 – 2007)

Flood 2,628,720,690 83.2% 3,814,152 4.9% 2,647,614 49.0%

Earthquake 32,089,519 1.0% 201,328 0.3% 5,044 0.1%

Storms 181,928,364 5.8% - 0.0% 2,598,456 48.0%

Meteorites 91,303 0.0% - 0.0% - 0.0%

Terrorism 246,873,898 7.8% 74,044,487 94.4% 155,071 2.9%

Riots & Mob misbehav.

65,820,383 2.1% 160,256 0.2% 2,665 0.0%

Acts of Armed Forces

1,913,608 0.1% 156,440 0.2% - 0.0%

TOTAL 3,157,437,765 100% 78,376,663 100% 5,408,850 100%Euros Updated

(* ) Period 2004-2007

BUSINESS INTERRUPTION (* )CAUSE

PERSONAL ACCIDENTS

PROPERTY

III. Some statistical dataIII. Some statistical data

26

Loss Ratio Loss Ratio (period 1971 – 2007)Loss Ratio Loss Ratio (period 1971 – 2007)

TOTAL LOSS PAYMENTS RATIO (% )

1971 - 1980 1,025,195,184 849,554,878 82.9%

1981 - 1990 1,531,790,187 2,226,445,127 145.3%

1991 - 2000 3,134,936,477 1,267,151,389 40.4%

2001 427,602,589 191,189,078 44.7%

2002 434,305,350 159,214,909 36.7%

2003 476,470,043 108,646,661 22.8%

2004 506,271,525 128,215,336 25.3%

2005 540,061,003 169,018,745 31.3%

2006 574,029,780 160,182,954 27.9%

2007 600,373,052 216,045,312 36.0%

TOTAL 9,251,035,191 5,475,664,387 59.2%

PREMIUMSYEARS

27

Years with special loss ratioYears with special loss ratio

TOTAL LOSS

PAYMENTS RATIO (% )

1982 130,721,290 369,958,028 283.0%

1983 130,627,719 855,961,645 655.3%

1987 139,466,718 335,963,252 240.9%

1989 210,269,785 273,132,116 129.9%

Euros Updated

PREMIUMSYEARS

28

Premiums and claims distributionPremiums and claims distribution(1971 - 2007)

Premiums and claims distributionPremiums and claims distribution(1971 - 2007)

-

100

200

300

400

500

600

700

800

90071 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07

Mil

lio

ns

Eu

ros

PREMIUMS UPDATED TOTAL PAYMENTS UPDATED

29

• Casualties: 192

• Wounded: 1.122

1.374 Claims1.313 personal injuries

61 material damages

Total compensations taken on by

CCS:

38 mill. €

MARCH 11th, 2004, TERRORIST ATTACKS IN MADRID

30

TERRORIST ATTACK TO TERMINAL 4 IN BARAJAS AIRPORT ON DECEMBER 30th, 2006.

Damages to airport terminal:

• Parking:.................................. 21.50

• Terminal & walkways:............... 4.50

• Debris removal:....................... 3.25

• Loss of profits:………………………….. 3.50

• Miscellaneous:......................... 1.25

TOTAL:.................................. 34.00 mill. €

Damages to vehicles:

• 1,139 vehicles (around 12 mill. €)

• CCS will take on damages under “all risks” and “glass breaking” policies.

TOTAL LOSS: € 46 MILL.

http://www.consorseguros.es