gary l. witten, cfp, chfc financial planner securities offered through, member sipc. c09-0428-017...

TRANSCRIPT

Gary L. Witten, CFP, ChFCFinancial Planner

Securities offered through <BD Name>, member SIPC. C09-0428-017

Retirement Readiness

Looking at the Road AheadLooking at the Road Ahead

Retirement - Insurance - Investments 2

Important Information

Insurance products, annuities and retirement plan funding issued by (third party administrative services may also be provided by) ING Life Insurance and Annuity Company ( Windsor, CT). Securities are distributed by ING Financial Advisers, LLC (member SIPC), Windsor, CT or through other broker/dealers with which it has selling agreements. Annuities may also be issued by ReliaStar Life Insurance Company (Minneapolis, MN) and ReliaStar Life Insurance Company of New York (Woodbury, NY). Variable annuities issued by ReliaStar Life Insurance Company are distributed by ING Financial Advisers, LLC. Variable annuities issued by ING USA Annuity and Life Insurance Company and ReliaStar Life Insurance Company of New York are distributed by Directed Service, LLC. Only ING Life Insurance Annuity Company and ReliaStar Life Insurance Company of New York are admitted and issue products in the state of New York. All companies are members of the ING Family of companies.

© 2009 ING North America Insurance Corporation.

Retirement - Insurance - Investments 3

Important Information

Insurance products, annuities and retirement plan funding issued by (third party administrative services may also be provided by) ING Life Insurance and Annuity Company ( Windsor, CT). Securities are distributed by ING Financial Advisers, LLC (member SIPC), Windsor, CT or through other broker/dealers with which it has selling agreements. Annuities may also be issued by ING USA Annuity and Life Insurance Company (Des Moines, IA) and are distributed by Directed Services, LLC. All companies are members of the ING Family of companies.

© 2009 ING North America Insurance Corporation.

Retirement - Insurance - Investments 4

Important Information

Securities and [financial planning] offered through ING Financial Advisers, LLC (member SIPC), One Orange Way, Windsor, CT, 06095-4774.

© 2009 ING North America Insurance Corporation.

Retirement - Insurance - Investments 5

Important Information

Recordkeeping and Plan administrative services provided by ING Institutional Plan Services, LLC.

© 2009 ING North America Insurance Corporation.

Retirement - Insurance - Investments 6

Important Information

Framewor(k) and (k)Choice Recordkeeping and Plan administrative services provided by ING Institutional Plan Services, LLC. Mutual funds offered through ING Financial Advisers, LLC (member SIPC).

© 2009 ING North America Insurance Corporation.

Retirement - Insurance - Investments 7

Important Information (continued)

Variable annuities, group annuities or funding agreements are long-term investments designed for retirement purposes. If withdrawals are taken prior to age 59 1/2, an IRA 10% premature distribution penalty tax may apply. Money taken from the annuity will be taxed as ordinary income in the year the money is distributed. An annuity does not provide any additional tax deferral benefit, as tax deferral is provided by the plan. Annuities may be subject to additional fees and expenses to which other tax-qualified funding vehicles may not be subject. However, an annuity does provide other features and benefits, such as lifetime income payments and death benefits, which may be valuable to you.

Variable investments, of any kind, are not guaranteed and are subject to investment risk including the possible loss of principal. The investment return and principal value of the security will fluctuate so that when redeemed, it may be worth more of less than the original investment. In addition, there is no guarantee that any variable investment option will meet its stated objective.

For 403(b)(1) annuities, the Internal Revenue Code (IRC) generally prohibits withdrawals of 403(b) salary reduction contributions and earnings on such contributions prior to death, disability and age 50 ½, severance of employment, or financial hardship. Amounts held in a 403(b)(1) annuity as of 12/31/1988 are “grandfathered” and are not subject to these restrictions. For 403(b)(7) custodial accounts, the IRC generally prohibits withdrawals of any contributions and attributable earnings prior to death, disability, age 59 ½, severance of employment, or financial hardship. For both 403(b)(1) annuities and 403(b)(7) custodial accounts, the amount available for hardship is limited to the lesser of the amount necessary to relieve the hardship, or the account value as of 12/31/1988, plus the amount of any salary reduction contributions made after 12/31/1988 (exclusive of any earnings).

You should consider the investment objectives, risk, and charges and expenses of the investment options carefully before investing. Fund prospectuses contain this and other information and can be obtained by contacting your local ING representative. Please read carefully before investing.

Retirement - Insurance - Investments 8

Important Information (continued)

Variable annuities, group annuities or funding agreements are long-term investments designed for retirement purposes. If withdrawals are taken prior to age 59 1/2, an IRA 10% premature distribution penalty tax may apply. Money taken from the annuity will be taxed as ordinary income in the year the money is distributed. An annuity does not provide any additional tax deferral benefit, as tax deferral is provided by the plan. Annuities may be subject to additional fees and expenses to which other tax-qualified funding vehicles may not be subject. However, an annuity does provide other features and benefits, such as lifetime income payments and death benefits, which may be valuable to you.

Variable investments, of any kind, are not guaranteed and are subject to investment risk including the possible loss of principal. The investment return and principal value of the security will fluctuate so that when redeemed, it may be worth more of less than the original investment. In addition, there is no guarantee that any variable investment option will meet its stated objective.

For 403(b)(1) annuities, the Internal Revenue Code (IRC) generally prohibits withdrawals of 403(b) salary reduction contributions and earnings on such contributions prior to death, disability and age 50 ½, severance of employment, or financial hardship. Amounts held in a 403(b)(1) annuity as of 12/31/1988 are “grandfathered” and are not subject to these restrictions. For 403(b)(7) custodial accounts, the IRC generally prohibits withdrawals of any contributions and attributable earnings prior to death, disability, age 59 ½, severance of employment, or financial hardship. For both 403(b)(1) annuities and 403(b)(7) custodial accounts, the amount available for hardship is limited to the lesser of the amount necessary to relieve the hardship, or the account value as of 12/31/1988, plus the amount of any salary reduction contributions made after 12/31/1988 (exclusive of any earnings).

All Guarantees are based on the financial strength and claims-paying ability of the issuing insurance company, who is solely responsible for all obligations under its policies.

You should consider the investment objectives, risk, and charges and expenses of the investment options carefully before investing. Fund prospectuses contain this and other information and can be obtained by contacting your local ING representative. Please read carefully before investing.

Retirement - Insurance - Investments 9

Important Information (continued)

You should consider the investment objectives, risk, and charges and expenses of the investment options carefully before investing. Fund prospectuses contain this and other information and can be obtained by contacting your local ING representative. Please read carefully before investing.

Retirement - Insurance - Investments 10

Important Information (continued)

This presentation/seminar contains information regarding insurance products for sale.

Retirement - Insurance - Investments 11

Retirement is a Beginning… Not a Destination

• Volunteer

• Spend time with family

• Travel

• Try new hobbies

• Start a new business

• Embark on a new career

Will Your Retirement Income Last the Journey?

Retirement - Insurance - Investments 12

Roadblocks to Retirement Income Success

You Can Navigate Them.

Retirement - Insurance - Investments 13

65 70 75 80 85

50% of females age 65will live past age 88.

50% of males age 65will live past age 84.

Based on Annuity 2000 Mortality Table assuming relatively good health (2005).

We’re Living Longer than Ever Anticipated

Retirement - Insurance - Investments 14

Is there a Downside to a Long Life?

($1,500,000)

($1,000,000)

($500,000)

$0

$500,000

$1,000,000

$1,500,000

Age 60 Age 65 Age 70 Age 75 Age 80 Age 85 Age 90

Retirement Income Need Retirement Savings

The example mentioned above is hypothetical and assumes an annual growth rate of 6% for illustrative purposes only and is not intended to project the performance of any specific investment. Actual rates of return will vary over time.

Retirement - Insurance - Investments 15

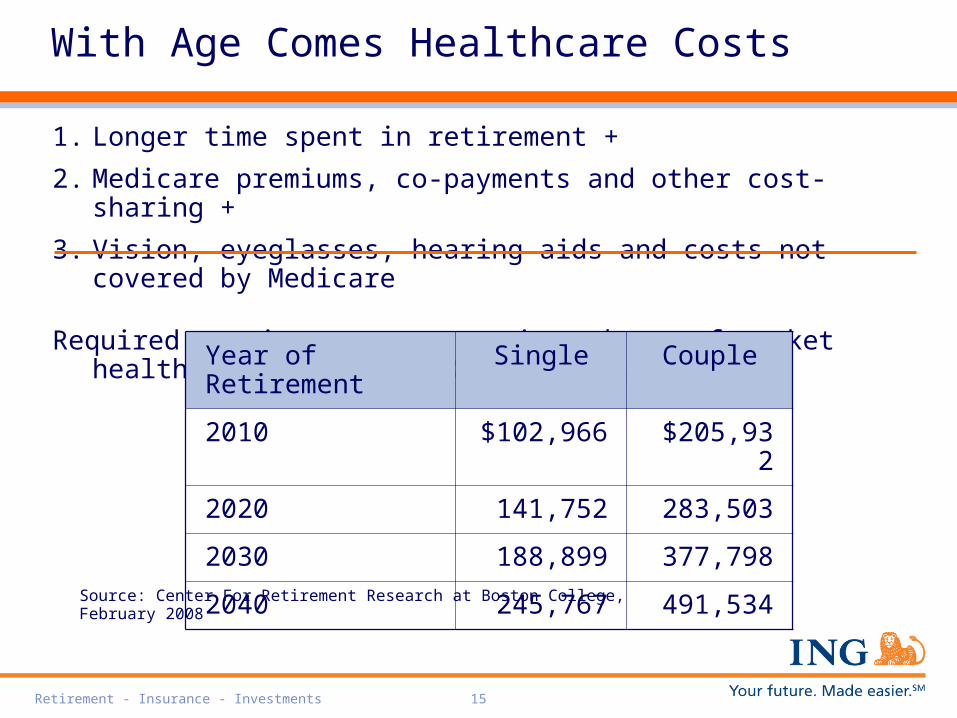

With Age Comes Healthcare Costs

1. Longer time spent in retirement +

2. Medicare premiums, co-payments and other cost-sharing +

3. Vision, eyeglasses, hearing aids and costs not covered by Medicare

Required annuity to cover projected out-of-pocket health care costs, 2010-2040, 2007 dollars:

Year of Retirement Single Couple

2010 $102,966 $205,932

2020 141,752 283,503

2030 188,899 377,798

2040 245,767 491,534

Source: Center For Retirement Research at Boston College, February 2008

Retirement - Insurance - Investments 16

Navigating Retirement Healthcare Costs

• Consider working longer

• Step up retirement savings

• Watch weight and exercise more

Retirement - Insurance - Investments 18

Recognize the Corrosive Power of Inflation

How much will your current income be worth in 20 years?

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$0 Today In 5 years In 10 years In 15 years In 20 years

$30,000$25,878

$22,323

$19,256$16,610

Retirement - Insurance - Investments 19

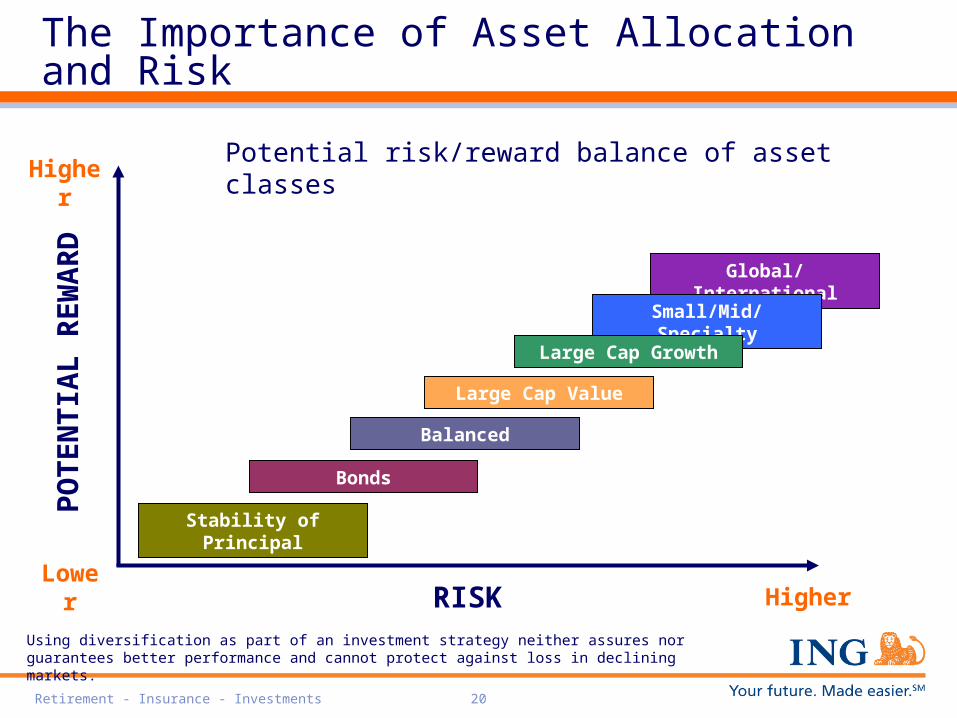

The Importance of Asset Allocation and Risk

Retirement - Insurance - Investments 20

The Importance of Asset Allocation and Risk

Potential risk/reward balance of asset classes

Global/International

Small/Mid/Specialty

Large Cap Growth

Large Cap Value

Stability of Principal

Bonds

Balanced

LowerRISK

Higher

PO

TE

NT

IAL

RE

WA

RD

Higher

Using diversification as part of an investment strategy neither assures nor guarantees better performance and cannot protect against loss in declining markets.

Retirement - Insurance - Investments 21

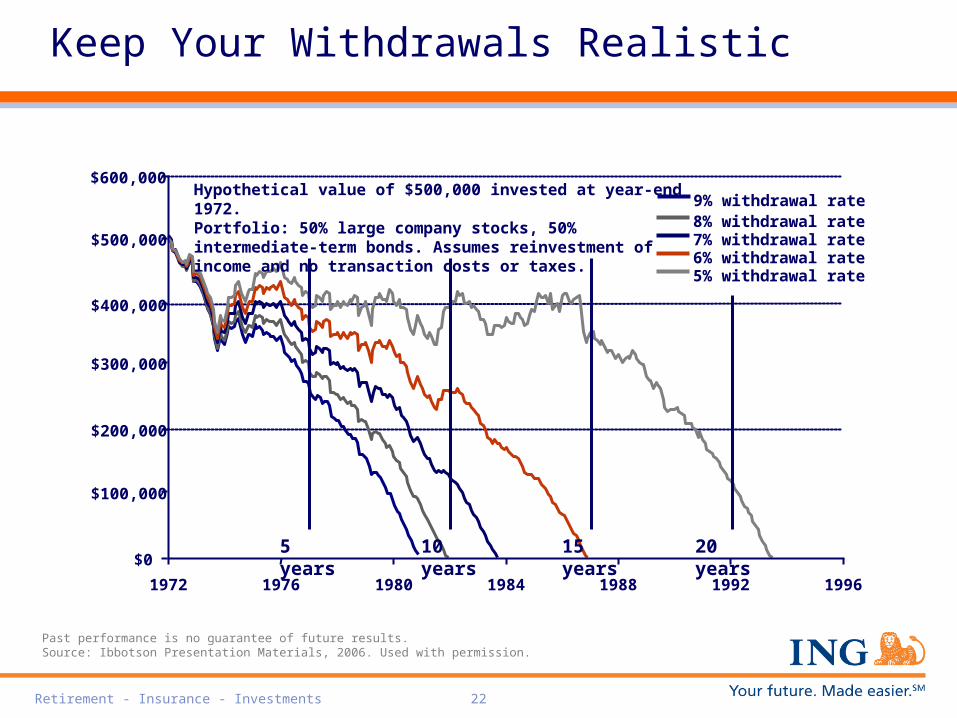

Get an Early Start

• Start saving early

• Save for the long run

• Poor performance in the early years of retirement can drastically impact the lifespan of retirement assets.

• The results can follow you throughout retirement

Retirement - Insurance - Investments 22

$100,000

$300,000

$500,000

$600,000

$0

$400,000

$200,000

1976 1980 1984 19961988 19921972

5% withdrawal rate

9% withdrawal rate8% withdrawal rate7% withdrawal rate6% withdrawal rate

Hypothetical value of $500,000 invested at year-end 1972.Portfolio: 50% large company stocks, 50% intermediate-term bonds. Assumes reinvestment of income and no transaction costs or taxes.

5 years 10 years 20 years15 years

Past performance is no guarantee of future results.Source: Ibbotson Presentation Materials, 2006. Used with permission.

Keep Your Withdrawals Realistic

Retirement - Insurance - Investments 23

Important Information

Standard & Poor's 500 Composite Total Return Index - The Standard & Poor's (S&P) 500 index is a market-value-weighted unmanaged index covering the stock of 500 industrial, utility, transportation and financial companies. The index return includes the reinvestment of dividends and is considered to be representative of the performance of large capitalization companies of the U.S. markets.

Barclays Capital U.S. Aggregate Bond Total Return Index - The Barclays Capital U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Retirement - Insurance - Investments 24

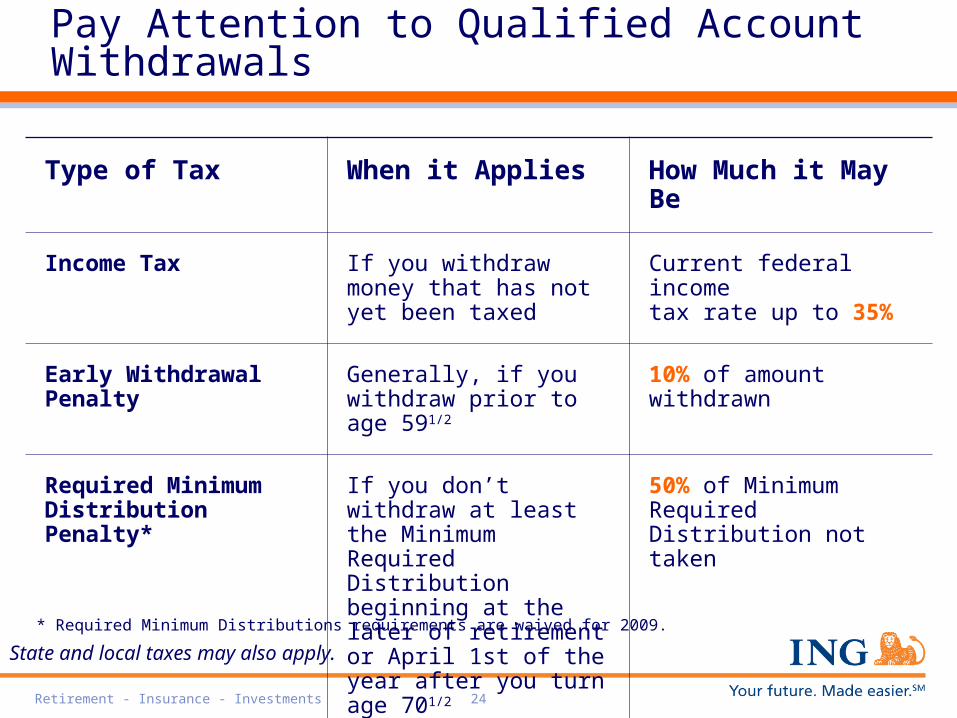

Pay Attention to Qualified Account Withdrawals

State and local taxes may also apply.

Type of Tax When it Applies How Much it May Be

Income Tax If you withdraw money that has not yet been taxed

Current federal incometax rate up to 35%

Early Withdrawal Penalty

Generally, if you withdraw prior to age 591/2

10% of amount withdrawn

Required Minimum Distribution Penalty*

If you don’t withdraw at least the Minimum Required Distribution beginning at the later of retirement or April 1st of the year after you turn age 701/2

50% of Minimum Required Distribution not taken

* Required Minimum Distributions requirements are waived for 2009.

Retirement - Insurance - Investments 25

Withdrawals from Qualified Accounts at 70½

• The IRS requires a minimum distribution (RMD) when you reach age 70½

• Failure to withdraw or withdrawing too little leads to a 50% penalty tax on the amount that you should have withdrawn

Consider Mary:Mary’s RMD $8,000

Her actual withdrawal $3,000

Discrepancy $5,000

IRS penalty $2,500

Retirement - Insurance - Investments 26

Be in Sync with Your Spouse/Partner

• Take the time to discuss your personal retirement goals

• Identify what you want to do and map out the cost

• Identify and consolidate your retirement assets

• Create a retirement spending plan

• Determine appropriate options for social security and pensions

Make sure you and your spouse/partner are on the same road

Retirement - Insurance - Investments 27

Direct Route to Retirement Income

Retirement - Insurance - Investments 28

Keys for Success

• Plot your destination

• Make sure your spouse/partner is on board

• Track your planning progress

• Create and follow a retirement income roadmap

Retirement - Insurance - Investments 29

Plot Your Destination

Five to ten years before you retire, ask yourself…

Where will you live?

What will you do?

How will you live?

How do you expect your health will hold up?

How long do you expect to live?

Retirement - Insurance - Investments 30

If you don't know where you are going, you might wind up someplace else.

-Yogi Berra

Retirement - Insurance - Investments 31

Test-Drive Your Plan

• Evaluate your current retirement savings plan and identify whether increased savings are needed (catch-up provisions may be available)

• Compare to the goals and needs you desire and identify gaps

• How will you replace your paycheck?

• Pension and Social Security benefits may not be enough to maintain pre-retirement income levels

Are you on track?

Retirement - Insurance - Investments 32

Social Security Administration, Office of Policy Data, Fast Facts & Figures About Social Security, 2006, Aggregate Income, By Source, 2004, Released September 2006

Map Out Your Retirement Income Strategy

Social Security provides about 40 percent of the average retiree’s monthly income

Where will your retirement income come from?

On average, pensions provide about 20 percent of the typical retiree’s income

Retirement - Insurance - Investments 33

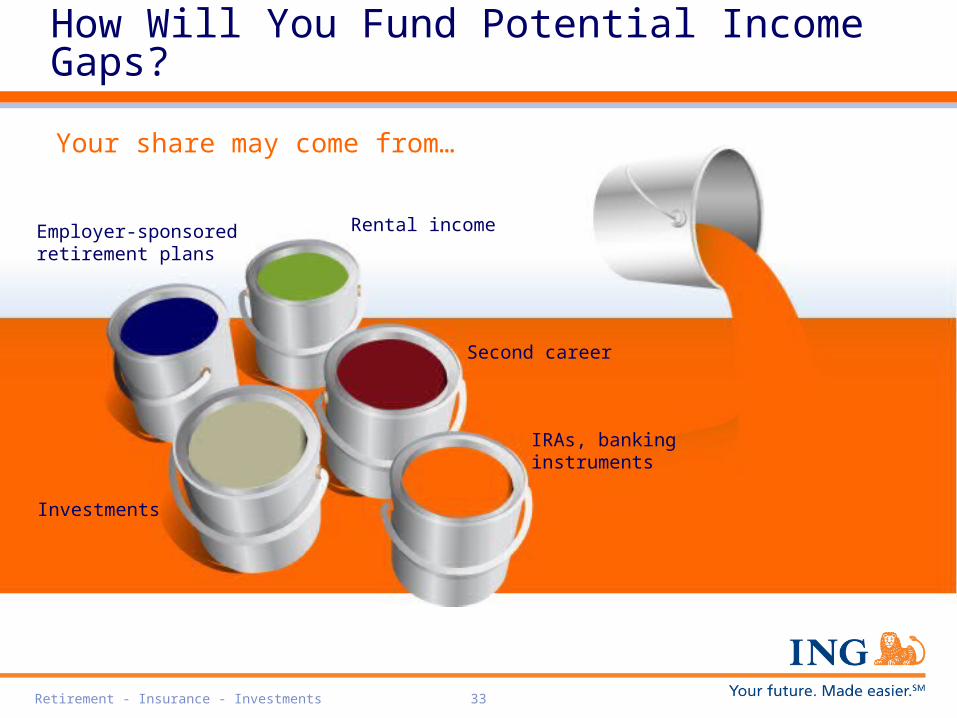

Second career

Rental income

IRAs, banking instruments

Investments

Employer-sponsored retirement plans

How Will You Fund Potential Income Gaps?

Your share may come from…

Retirement - Insurance - Investments 34

Create Your Retirement Income Roadmap

In retirement, it’s all about smart money management

Retirement - Insurance - Investments 35

Organize Your Resources

1. Create an emergency fund to cover up to 6 months’ expenses

2. Separate remaining assets

A. Short-term money to cover necessary expenses

B. Mid-term money for discretionary expenses

C. Long-term money to grow and potentially replenish other sources

Retirement - Insurance - Investments 36

Short-term: Checking Account, Emergencies

Manage Cash Flow to Maintain Your Income

Income Producing Growth Long Term Asset Allocation

Consolidation of assets

Fill

In Flow

Pension and Social Security

Mid-term:Income Producing

Long- term: GrowthPotential

Fill

Cover Essential Retirement Expenses Cover Discretionary Expenses

Purchasing Power Preservation

Retirement - Insurance - Investments 37

Short-term money

Use Short-term Money to Cover Necessary Expenses

Typical income needs:

• Food

• Housing

• Utilities

• Taxes

• Insurance

• Emergency reserves

• Essential living expenses

Short-term: Checking Account, Emergencies

Retirement - Insurance - Investments 38

Mid-term money

Fill the Mid-term Money Source Next

Typical income needs:

Money needed to refill the short-term money account and pay for:

• Travel

• Entertainment

• Housing

• Car/repairs

• EducationMid-term:Income Producing

Retirement - Insurance - Investments 39

Long-term money

Stash Some Cash Away for the Long-Term

Typical income needs:

Money needed to refill the mid-term money account and provide for:

• Potential long-term growth

• Additional income to compensate for inflation and longevity

Using asset allocation as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss in declining markets

Long- term: GrowthPotential

Retirement - Insurance - Investments 40

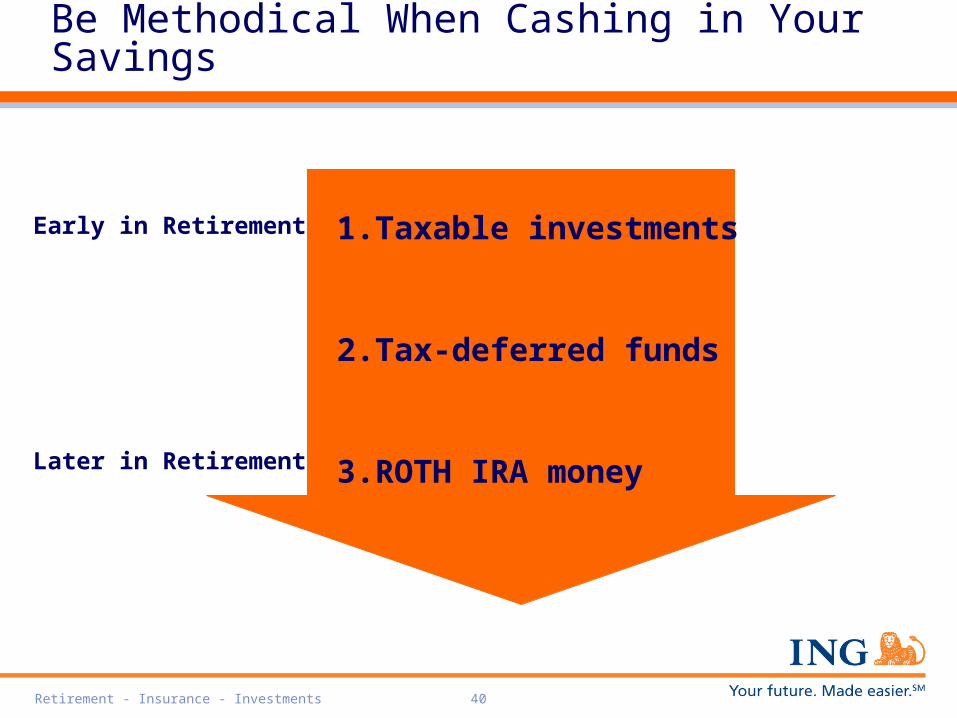

Be Methodical When Cashing in Your Savings

1. Taxable investments

2. Tax-deferred funds

3. ROTH IRA money

Early in Retirement

Later in Retirement

Retirement - Insurance - Investments 41

Upon separation from service, you have the following options:

• Keep your money in your retirement plan

• Rollover to an IRA

• Take an income payout option

Options for Defined Contribution Plans

Retirement - Insurance - Investments 42

Itinerary for Your Retirement Income Journey

• Cover short-term needs first

• Be ready for emergencies

• Convert personal savings to income, if needed

• Hold back money for niceties

• Invest some money for growth

Retirement - Insurance - Investments 4315

Retirement… You Can Get There from Here

Retirement - Insurance - Investments 44

Road-Side Assistance When You Need It

Gary L. Witten, CFP, ChFC

ING

716-626-3928 • [email protected] •www.GLWitten.com