gbs overview & trends - absl€¦ · gbs overview & trends october 2013 absl czech republic...

TRANSCRIPT

GBS Overview & Trends

October 2013

ABSL Czech Republic , Prague

Tom Bangemann

Senior Vice President, Business Transformation

The Hackett Group

Global Business

Services - Insights from

the Leaders State of the Nation

A tale of Two Halves

Tapping new Sources of Value

The Outlook for Offshoring

SSON April 2013-GBS: Insights from the leaders | 3 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Focus on Bottom Line Exceeds Top Line Growth for 2013,… Agility is required to meet profit goals when revenue falls short

49%

68%

74%

77%

77%

82%

82%

83%

88%

88%

90%

Achieve non-financial, social responsibilityand sustainability-related objectives

Grow emerging market presence

Manage enterprise risk

Reduce total supply chain cost

Improve cash flow/working capital

Enhance employee/talent retention anddevelopment

Increase operational agility and flexibility

Reduce overhead cost

Improve customer service/satisfaction

Accelerate revenue growth

Improve operating margin

% of respondents indicating the objective is “Extremely Important or Important” strategy for 2013

What is the importance of each of the following objectives in your enterprise strategy for 2013?

New

Largest

increase

+/- 3% Change from 2012

SSON April 2013-GBS: Insights from the leaders | 4 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Global Business Services – State of the Nation

The multi-functional GBS model is now a well-established and stable trend

Companies increasingly rely on GBS as a cornerstone of the Enterprise Model

End-to-end process integration is high on the agenda

GBS makes an increasing contribution in a customer-facing role

Mixed GBS sourcing models are expected to become a norm

HOWEVER

The Hackett Group is observing a disconnect between the measurable GBS

achievements and stakeholders perceptions

SSON April 2013-GBS: Insights from the leaders | 5 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

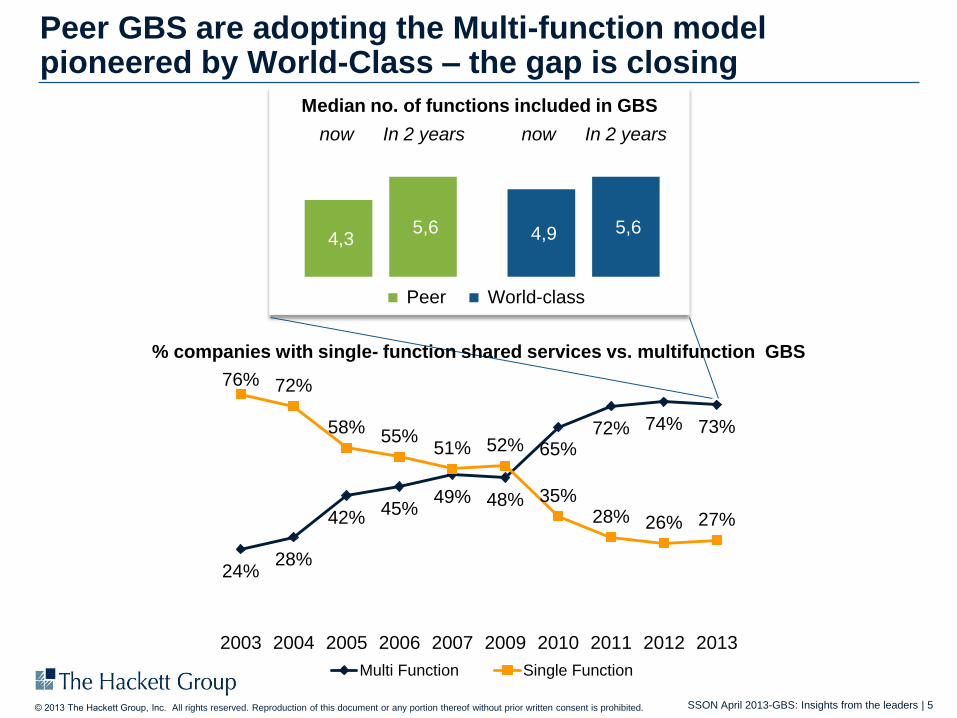

Peer GBS are adopting the Multi-function model pioneered by World-Class – the gap is closing

24% 28%

42% 45%

49% 48%

65% 72% 74% 73%

76% 72%

58% 55%

51% 52%

35% 28% 26% 27%

2003 2004 2005 2006 2007 2009 2010 2011 2012 2013

Multi Function Single Function

now In 2 years now In 2 years

World-class Peer

Median no. of functions included in GBS

4,3 4,9 5,6 5,6

% companies with single- function shared services vs. multifunction GBS

SSON April 2013-GBS: Insights from the leaders | 6 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

The GBS scope of top quartile companies covers more than 50% of activities

To compare, across all G&A functions (Finance, HR, IT, Procurement) ,GBS only have a third of services in scope on average (for median companies)

12%

56%

32%

Finance

44%

46%

10%

HR

11%

68%

20%

IT

14%

40%

46% Procure’t

11%

68%

20%

Corporate

Business Units

GBS

SSON April 2013-GBS: Insights from the leaders | 7 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Companies have pushed the GBS model furthest in Finance

North American HQ’d companies European HQ’d companies AsPac HQ’d companies

0% 20% 40% 60% 80% 100%

Capital and Risk Management

Tax Planning

Tax Filing and Reporting

Specialized Regulatory

External Reporting

Tax Accounting

Planning

Cost Accounting

Forecasting

Business Operations Analysis

Business Performance Reporting

Cash Management

Customer Billing

Credit

Collections

Intercompany Accounting

Fixed Assets

General Ledger

Travel and Expense

Cash Application

Accounts Payable

GBS outside GBS

Service Placement – Finance processes

Service placement by geography

Source: Global Business Services (GBS) performance study, 2013

SSON April 2013-GBS: Insights from the leaders | 8 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

In Procurement, companies have pushed the GBS model more moderately in past, but expected growth is large

Service Placement – Procurement processes

0% 20% 40% 60% 80% 100%

Product Development and Design Support

Function Strategy and Performance Management

Sourcing and Supply Base Strategy

Function Management

Requirements Definition and Supplier Bidding

Supplier Partnering

Supplier Management

External Customer Management

Negotiation and Supplier Contract Creation

Compliance Management

Internal Customer Management

Supplier Scheduling

Supply Data Management

Receipt Processing

Requisition and PO Processing

GBS outside GBS

Service placement by geography

North American HQ’d companies European HQ’d companies AsPac HQ’d companies

Source: Global Business Services (GBS) performance study, 2013

SSON April 2013-GBS: Insights from the leaders | 9 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

World-class GBS balances cost and service

Source: 2013 Hackett Global Business Services Performance Study

Average initial

savings over baseline

costs realized by

world-class GBS

Peer = 19%

35% Average annual recurring

savings realized by

world-class GBS

Peer = 6%

10%

Average annual rate of

customer service

improvement achieved

by GBS organizations

7% Average annual rate of

quality improvement

achieved by GBS

organizations

7%

Percentage of world-

class GBS rated as

“highly effective” in

enterprise agility

Peer = 11%

60%

Global Business

Services - Insights from

the Leaders State of the Nation

A tale of Two Halves

Tapping new Sources of Value

The Outlook for Offshoring

SSON April 2013-GBS: Insights from the leaders | 11 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

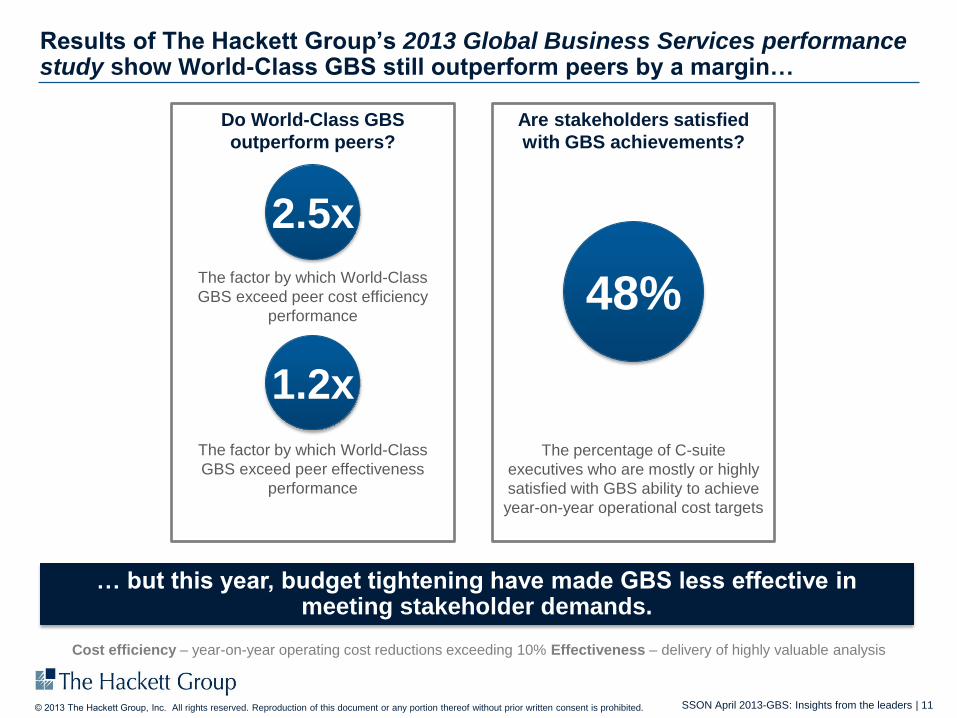

Results of The Hackett Group’s 2013 Global Business Services performance study show World-Class GBS still outperform peers by a margin…

… but this year, budget tightening have made GBS less effective in meeting stakeholder demands.

Are stakeholders satisfied

with GBS achievements?

48%

The percentage of C-suite

executives who are mostly or highly

satisfied with GBS ability to achieve

year-on-year operational cost targets

Do World-Class GBS

outperform peers?

2.5x

The factor by which World-Class

GBS exceed peer cost efficiency

performance

The factor by which World-Class

GBS exceed peer effectiveness

performance

1.2x

Cost efficiency – year-on-year operating cost reductions exceeding 10% Effectiveness – delivery of highly valuable analysis

SSON April 2013-GBS: Insights from the leaders | 12 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

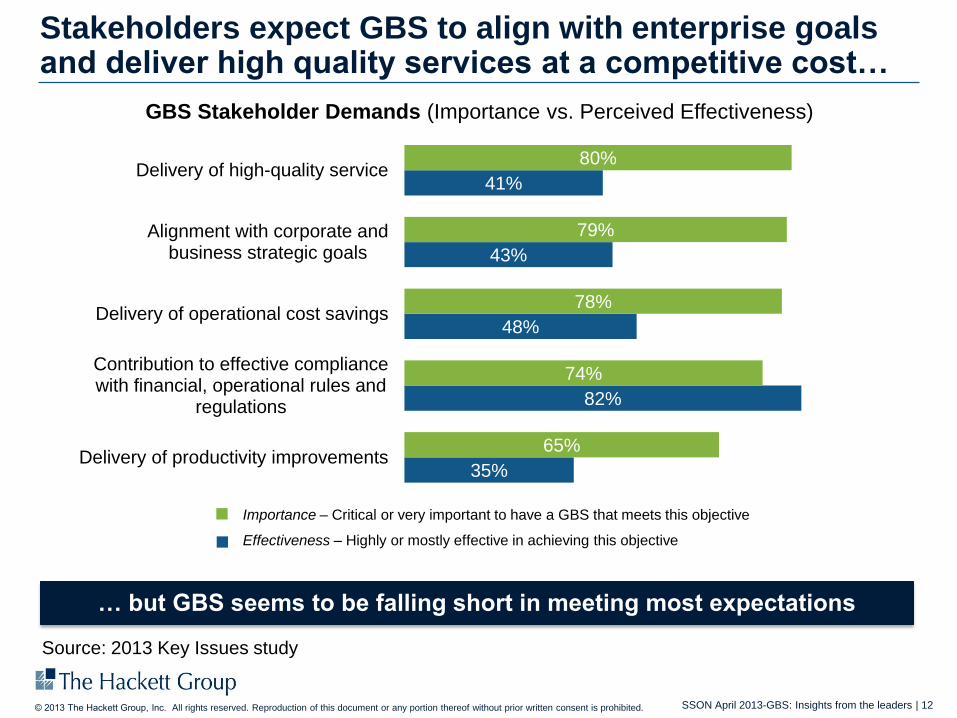

Stakeholders expect GBS to align with enterprise goals and deliver high quality services at a competitive cost…

35%

82%

48%

43%

41%

65%

74%

78%

79%

80%

Delivery of productivity improvements

Contribution to effective compliancewith financial, operational rules and

regulations

Delivery of operational cost savings

Alignment with corporate andbusiness strategic goals

Delivery of high-quality service

GBS Stakeholder Demands (Importance vs. Perceived Effectiveness)

Source: 2013 Key Issues study

Importance – Critical or very important to have a GBS that meets this objective

Effectiveness – Highly or mostly effective in achieving this objective

… but GBS seems to be falling short in meeting most expectations

Global Business

Services - Insights from

the Leaders State of the Nation

A tale of Two Halves

Tapping new Sources of Value

The Outlook for Offshoring

SSON April 2013-GBS: Insights from the leaders | 14 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

The Evolution from Shared Services to Global Business Services

Maturity

Strategic

Business

Enablement

Operating

Excellence

Complexity

Reduction

GBS evolution - selected companies distribution

Shared Services Global Business Services

Examples

Dow Chemical, P&G, Statoil

Examples

GSK, HP, Shell

8%

33%

59%

Source: Global Business Services (GBS) performance study, 2013

Stage

3

Stage

2

Stage

1 Function-centric

Process/Service centric

Value-centric

SSON April 2013-GBS: Insights from the leaders | 15 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Mature GBS with end-to-end focus provide a multitude of efficiency improvement opportunities (in addition to process cost)

Cross-functional savings in end-to-end processes for a typical $10 billion company

Working capital

improvements

Spend reduction improvements

SSON April 2013-GBS: Insights from the leaders | 16 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Finance-led Talent Management Large gaps exist in general business skills required by Finance

Highlighted skills show

the largest imbalance

between importance

and effectiveness

– Change management

– Business acumen

– Relationship

management

– Problem solving skills

Balance of importance and

effectiveness

Data analysis and modeling

Change mgt./process improvement

Business acumen

Rlshp mgt. Problem solving skills

Strategic thinking and analysis

Project/Program management

Vendor/outsourcing management

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 20% 40% 60% 80% 100%

Importance

Eff

ecti

ven

ess

Source: 2011 Finance Talent Mgmt Study

SSON April 2013-GBS: Insights from the leaders | 17 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Service Management is a proven differentiator on the journey towards World-Class

Dedicated service management roles

(% fully implemented)

78%

78%

80%

80%

89%

31%

44%

25%

35%

47%

GBS service design

GBS HR management

Business relationshipmanagement

GBS strategy management

Financial Management

Peer World-class

Stage 2 Stage 1 Stage 3

36% 72% 83%

16% 50% 83%

39% 62% 50%

21% 58% 50%

25% 58%

83%

Global Business

Services - Insights from

the Leaders State of the Nation

A tale of Two Halves

Tapping new Sources of Value

The Outlook for Offshoring

SSON April 2013-GBS: Insights from the leaders | 19 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Europe Americas Asia Oceania Africa Others

Almost 5.000 shared service centres operate globally

SSC-BPO Distribution

in the Database

Regional Distribution of SSCs

1381;

29%

3378;

71%

60; 2% 41; 1% 117; 3%

SSC BPO

1512;

30%

3471;

70%

1815; 52%

898; 26%

540; 16%

Top 5 Global Destinations with BPOs Top 5 Global Destinations with SSCs

274

158

106 96 90

India Poland Philippines United States China

562

401

236 182 166

United States UnitedKingdom

Poland India Germany

SSON April 2013-GBS: Insights from the leaders | 20 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

14

3

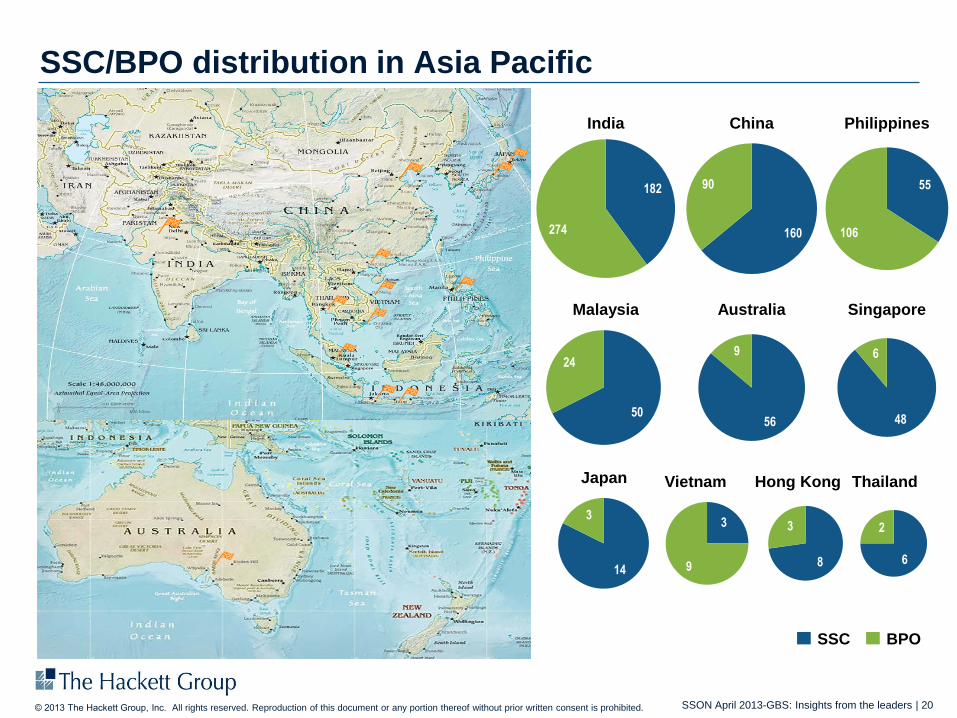

SSC/BPO distribution in Asia Pacific

SSC BPO

India China Philippines

Malaysia Australia Singapore

Vietnam Hong Kong Thailand

3

9

182

274 160

90 55

106

50

24

56

9

48

6

8

3

6

2

Japan

SSON April 2013-GBS: Insights from the leaders | 21 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

236

158

SSC/BPO distribution in CEE

SSC BPO

Poland Czech Republic Hungary

Slovakia Romania Lithuania

Latvia Bulgaria Estonia

93

24

101

26

7

32

14

26

19

11

49

8

28

24

6

30

SSON April 2013-GBS: Insights from the leaders | 22 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

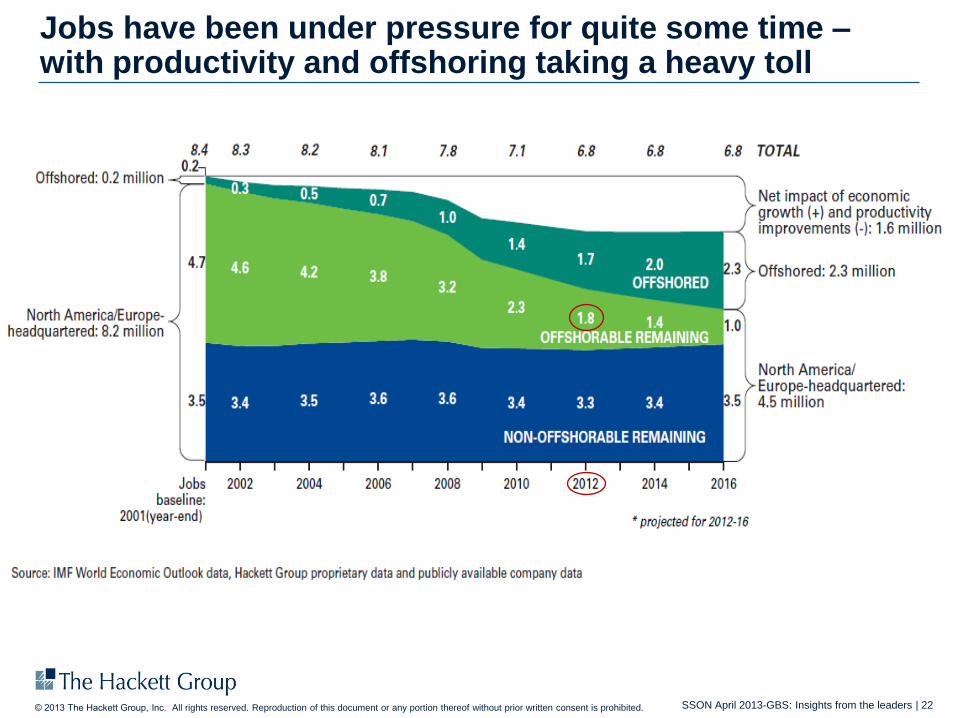

Jobs have been under pressure for quite some time – with productivity and offshoring taking a heavy toll

SSON April 2013-GBS: Insights from the leaders | 23 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Companies with World-Class GBS have high levels of enterprise-wide process standardisation

Enterprise-wide Business Unit Within geographies No or limited standardisation

45%

23%

25%

7%

Peer

85%

12%

3%

World-Class

Level of process standardisation – G&A Functions

World-Class GBS have almost

2x the level of enterprise-wide process

standardisation compared to peers

SSON April 2013-GBS: Insights from the leaders | 24 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

... do they know, and acknowledge it?

Can your GBS Customers pick all three...

SSON April 2013-GBS: Insights from the leaders | 25 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

Contact Information

Tom Bangemann Senior Vice President, Business Transformation

+49 174 3469 974 | Telephone

[email protected] I Email

Amsterdam | Atlanta | Chicago | Frankfurt | Hyderabad | London

Miami | New York | Paris | Philadelphia | San Francisco | Sydney

SSON April 2013-GBS: Insights from the leaders | 26 © 2013 The Hackett Group, Inc. All rights reserved. Reproduction of this document or any portion thereof without prior written consent is prohibited.

www.thehackettgroup.com

Statement of Confidentiality and Usage Restrictions

This document contains trade secrets and other information that is company sensitive, proprietary, and confidential, the disclosure of which would provide a competitive

advantage to others. As a result, the reproduction, copying, or redistribution of this document or the contents contained herein, in whole or in part, for any purpose is strictly

prohibited without the prior written consent of The Hackett Group.

Corporate Headquarters

1001 Brickell Bay Drive

30th Floor

Miami, Florida 33131

TEL: +1 305 375 8005

Amsterdam

Camerastraat 25

1322 BB Almere Amsterdam

TEL: + 31 36 535 00 82

Atlanta

1000 Abernathy Road NW

Suite 1400

Atlanta, GA 30328

TEL: +1 770 225 3600

Chicago

525 W. Monroe Street

Suite 1550

Chicago, IL 60661

TEL: +1 312 325 2900

Frankfurt

Torhaus Westhafen

Speicherstrasse 59

60327 Frankfurt am Main

TEL: +49 69 900 217 0

Hyderabad

8-2-120/112/88&89

1st Floor, Aparna Crest

Road #2, Banjara Hills

Hyderabad 500034

TEL: +91 40 66544000

London

Martin House

5 Martin Lane

London EC4R 0DP

TEL: +44 20 7398 9100

New York

110 Wall Street

17th Floor

New York, NY 10005

TEL: +1 646 354 4400

Paris

8, rue de Port Mahon

75002 Paris

TEL: +33 1 53 43 0400

Philadelphia

225 Washington Street

Conshohocken, PA 19428

TEL: +1 610 234 5500

San Francisco

100 Montgomery Street

Suite 2225

San Francisco, CA 94104

TEL: +1 415 249 3500

Sydney

Suite 403

35 Lime Street

Sydney, NSW2000

Australia

TEL: 1300 457 779 (within Australia)

TEL: +61 2 9299 8830