global climate change and its distributional impacts maurizio bussolo, rafael de hoyos, denis...

TRANSCRIPT

Global Climate Change and its Distributional Impacts

Maurizio Bussolo, Rafael de Hoyos, Denis Medvedev and Dominique van der MensbruggheThe World Bank

“Future of the Global Economy”11th Annual Conference on Global Economic AnalysisHelsinki, 12-14 June, 2008

ENVISAGE: Model featuresENVISAGE: Model features• Standard dynamic global CGE.• Flexible aggregation (regions and sectors) and time frame.• 2001 GTAP-based base year including IEA-based energy

demand and trade (MTOE) and estimates of CO2 emissions by sector and fuel (shifting to 2004).

• Integrated climate module with links from emissions to radiative forcing to temperature change.

• Flexible energy demand system.• Flexible emissions control—carbon taxes, caps, cap and trade,

demand exemptions.

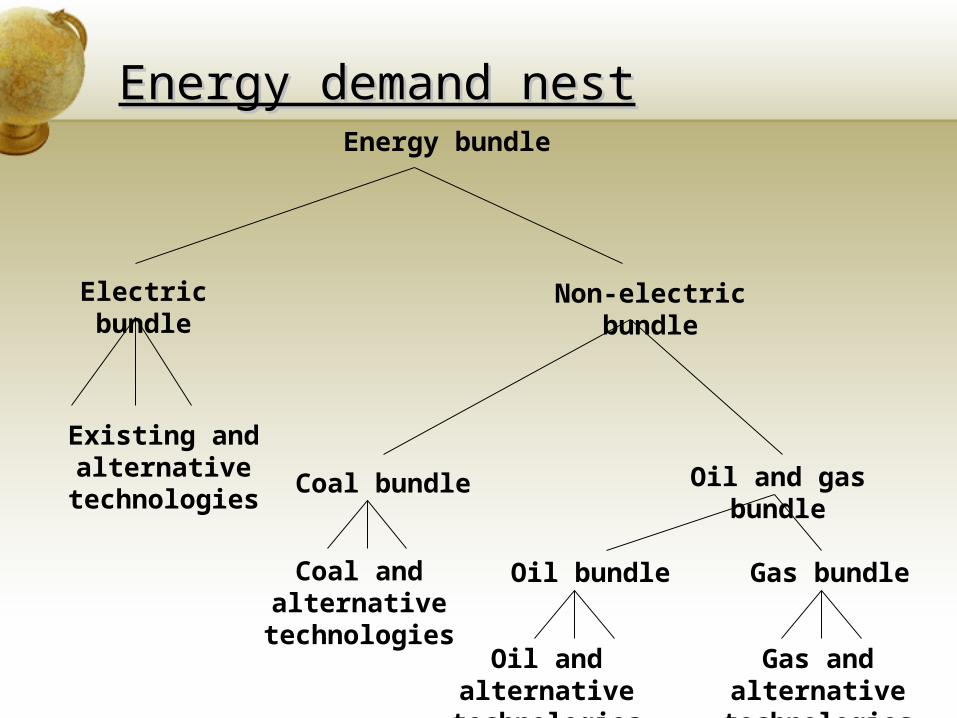

Energy demand nestEnergy demand nestEnergy bundle

Electric bundle

Existing and alternative technologies

Non-electric bundle

Coal bundle Oil and gas bundle

Coal and alternative technologies

Oil bundle Gas bundle

Oil and alternative technologies

Gas and alternative technologies

Three scenariosThree scenarios• Baseline, or business-as-usual, with climate change damages• Baseline without climate change damages.• Global mitigation scenario—targetting 500 ppm concentration

by 2050

Key baseline assumptionsKey baseline assumptions• UN population forecast—labor force growth equated to

growth of working age population (15-65).• Savings rate driven by growth and youth and elderly

dependency rates.• Trend productivity in agriculture is exogenous (2.5% per

annum), with temperature-based damage function.• Productivity in manufacturing is higher than in services (2%).• Productivity is calibrated through 2015 and then fixed.• Autonomous energy efficiency improvement (AEEI) increases

by 1% per annum (in all regions and sectors).• Capital account is exogenous.

Source: Simulations with World Bank’s ENVISAGE model.

0

1

2

3

4

5

6

7

8

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Pe

rce

nt

pe

r a

nn

um

0

20

40

60

80

100

120

140

160

$2

00

1 trillio

n

Developing, right-axis

Developing growth rate, left-axis

High-income growth rate, left-axis

Baseline GDP

Developed, right-axis

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Pe

rce

nt

pe

r a

nn

um

0

5

10

15

20

25

30

35

40

GtC

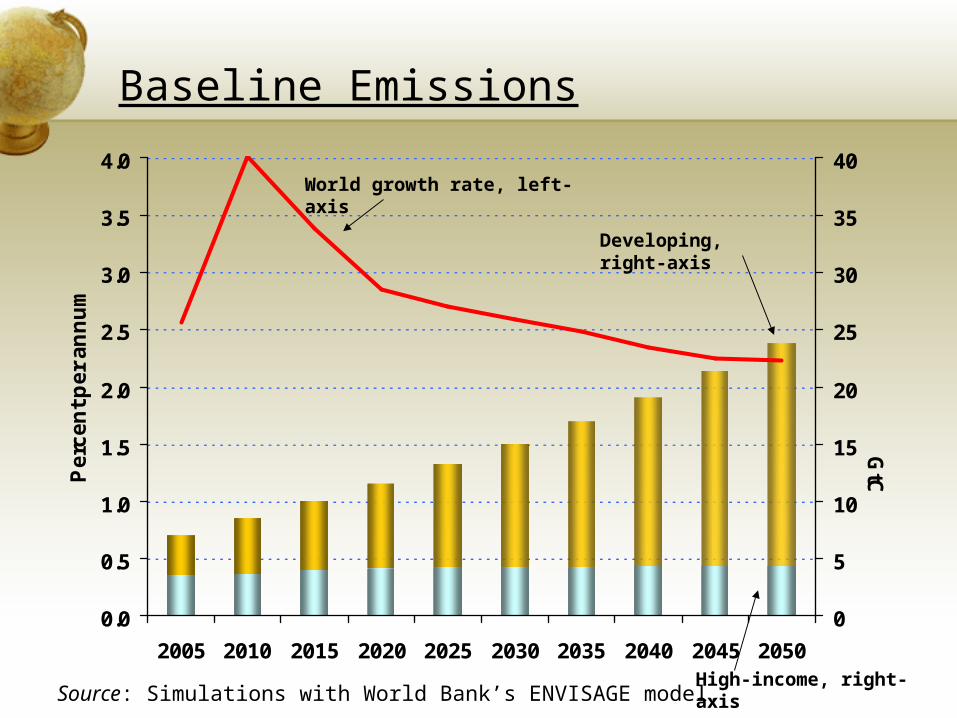

Source: Simulations with World Bank’s ENVISAGE model.

Developing, right-axis

High-income, right-axis

World growth rate, left-axis

Baseline Emissions

Concentration, forcing and temperature

0

100

200

300

400

500

600

2001 2010 2020 2030 2040 2050

Conc

rent

ation

ppm

0

1

2

3

4

5

6

Radiative forcing (W

/m2) and tem

perature (°C)

Concentration Forcing

Temperature

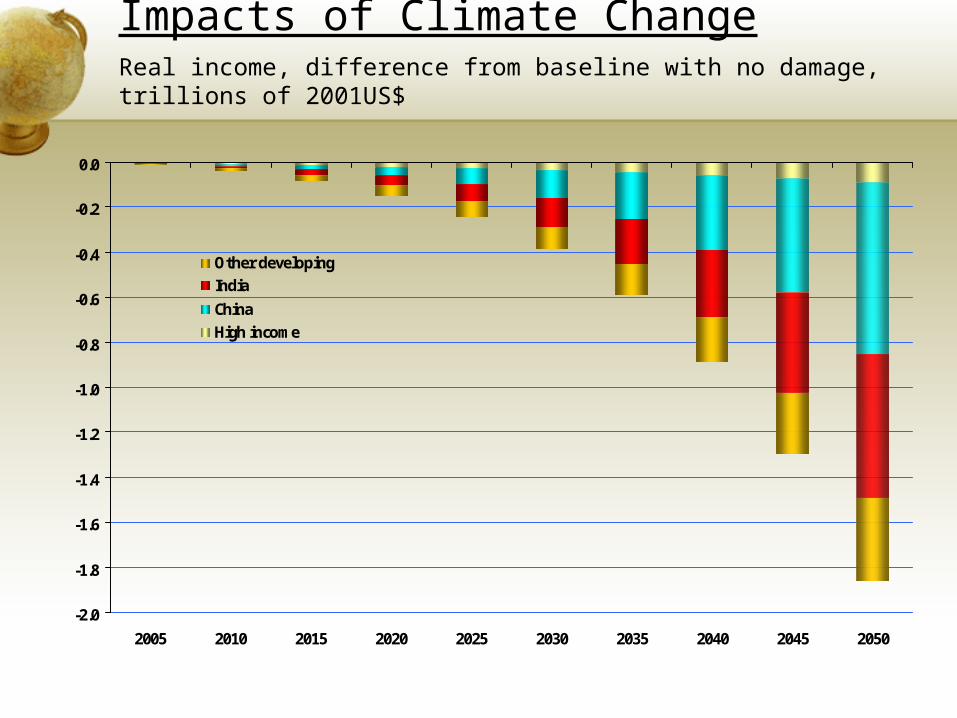

Impacts of Climate ChangeReal income, difference from baseline with no damage, trillions of 2001US$

-2.0

-1.8

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Other developingIndiaChinaHigh income

Impacts of Climate ChangeReal income, perce nt difference from baseline with no damage in 2050

-7 -6 -5 -4 -3 -2 -1 0 1 2

Canada

Rest of MENA

United States

Japan

Rest of high income

EU 27 and EFTA

Indonesia and Malaysia

Brazil

Russia

Rest of LAC

Rest of Europe and Central Asia

MENA Energy exporters

Rest of South Asia

Rest of developing East Asia

Sub Saharan Africa

Other LAC energy exporters

China

India

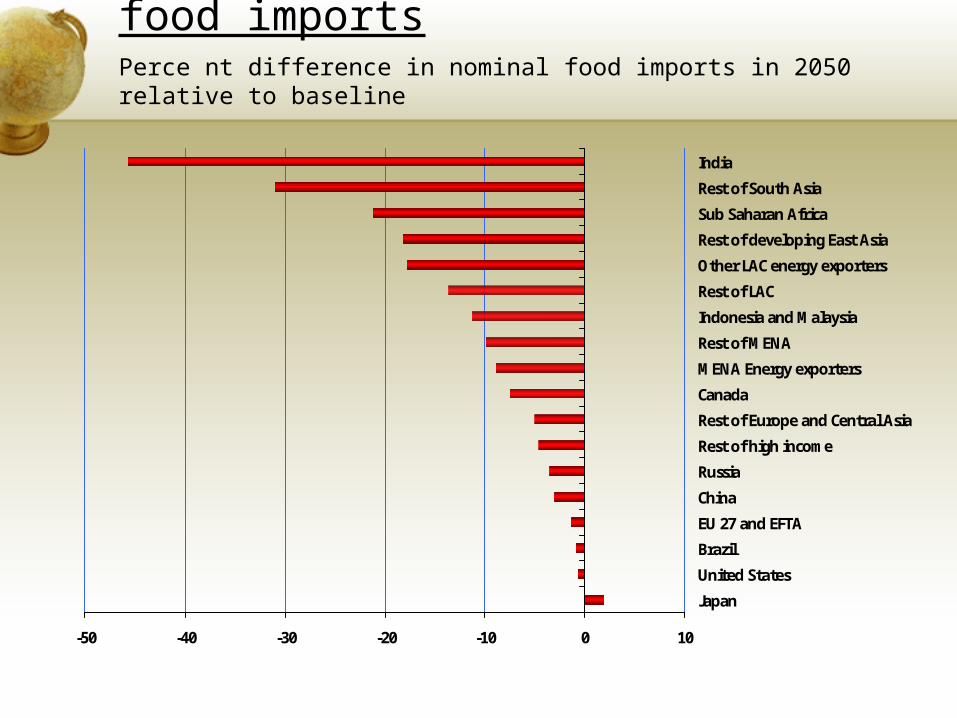

Climate change damages and food importsPerce nt difference in nominal food imports in 2050 relative to baseline

-50 -40 -30 -20 -10 0 10

Japan

United States

Brazil

EU 27 and EFTA

China

Russia

Rest of high income

Rest of Europe and Central Asia

Canada

MENA Energy exporters

Rest of MENA

Indonesia and Malaysia

Rest of LAC

Other LAC energy exporters

Rest of developing East Asia

Sub Saharan Africa

Rest of South Asia

India

Percent reduction in emissionsPerce nt reduction in CO2 emissions relative to baseline in 2050

-90 -80 -70 -60 -50 -40 -30 -20 -10 0

Brazil

Japan

Other LAC energy exportersRest of MENA

EU 27 and EFTASub Saharan Africa

Rest of South Asia

Indonesia and MalaysiaMENA Energy exporters

Canada

Rest of high incomeRussia

United States

Rest of developing East AsiaRest of LAC

Rest of Europe and Central AsiaWorld total

India

China

$93 per ton of carbon in 2050

Real income losses/gains from mitigationPerce nt change in real income relative to baseline in 2050

-8 -6 -4 -2 0 2 4

Canada

Rest of MENA

United States

Japan

Rest of high income

EU 27 and EFTA

Indonesia and Malaysia

Brazil

Russia

Rest of LAC

Rest of Europe and Central Asia

MENA Energy exporters

Rest of South Asia

Rest of developing East Asia

Sub Saharan Africa

Other LAC energy exporters

China

India

Climate change damages

Mitigation

Global income distribution

0.0

0.1

0.1

0.2

0.2

0.3

0.3

0.4

0.4

0.5

0 2 4 6 8 10

Den

sity

of l

og(h

ouse

hold

per

cap

ita

inco

me

or

cons

umpti

on, 1

993

PPP)

Observed (2000)BaU (2050)BaUnd (2050)

Note: BaU = baseline, BaUnd = baseline with no damages.Source: Simulations with World Bank’s GIDD model.

Percent of total number of poor

0

20

40

60

80

100

2000 BaU, 2050 BaUnd, 2050 GBL, 2050

Poor in agriculture

Poor in non-agriculture

Note: BaU = baseline, BaUnd = baseline with no damages, GBL = global mitigation scenario.Source: Simulations with World Bank’s GIDD model.

Climate change impacts on poverty

Percentage change in real income or consumption

-5

0

5

10

15

20

0 20 40 60 80 100

No damages from climate changeGlobal mitigation via uniform tax

Source: Simulations with World Bank’s GIDD model.

Growth incidence of climate damages and mitigation

Composition of 10 percent of global population most affected by climate change

Non-agricultural households in EasternEurope and Central Asia

Agricultural households in LatinAmerica and the Caribbean

Non-agricultural households in LatinAmerica and the Caribbean

Agricultural households in South Asia

Non-agricultural households in SouthAsia

Source: Simulations with World Bank’s GIDD model.

Incidence of damages from climate change

Take away messagesTake away messages• Standard SRES ‘worse case’ baseline scenarios are too

optimistic• Staying at 550 ppm will require a major effort• Negative effects from climate change on agricultural output

will be significant with income, trade and poverty impacts• No major cost from ‘modest’ mitigation efforts• Poor are hardest hit from climate change

• Caveats -- many