green mini-grids in sub-saharan africa

TRANSCRIPT

Green Mini-Grids in Sub-Saharan Africa:

Analysis of Barriers to Growth and the Potential Role of the African Development Bank

in Supporting the Sector

Green Mini-Grids Market Development Programme GMG MDP Document Series: n°1 December 2016

2 GMG MDP Document Series: n°1

Disclaimer

The views expressed in this publication are those of the authors and do not necessarily reflect the views of the African Develop-

ment Bank Group (AfDB). The AfDB does not guarantee the accuracy of the data included in this publication and accepts no

responsibility for any consequence of their use.

By making any designation of or reference to a particular territory or geographic area, or by using the term “country” in this do-

cument, AfDB does not intend to make any judgment as to the legal or other status of any territory or area.

AfDB encourages printing or copying of the information in this report exclusively for personal and non-commercial use, with pro-

per acknowledgment of the AfDB. Users are restricted from reselling, redistributing or creating derivative works for commercial

purposes without the express written consent of the AfDB.

Photos Credits:

Energy 4 Impact

3GMG MDP Document Series: n°1

Introduction to the Green Mini-Grids Market Development Programme Document Series

This paper, and subsequent papers in the Green Mini-Grid Market Development Programme (GMG MDP) document series,

analyses the issues involved with developing green mini-grids for rural electrification. These are mini-grids powered by renewable

energy resources – solar radiation, wind, hydropower or biomass – either exclusively or in combination with diesel generation.

Mini-grids are not a new phenomenon in Africa. Almost all national utilities own and operate diesel-powered generating facilities

not connected to the main grid, which supply electricity to secondary towns and larger villages. This solution to rural electrifica-

tion inevitably results in significant financial losses for the utility, as it is required to sell power at prices much below the cost of

production and delivery. Moreover, it leaves the most remote towns and villages unelectrified. The latest Sustainable Energy for All

(SE4All) Global Tracking Framework estimates that the urban-rural divide in access to electricity in Africa is as high as 450 percent

(69 urban compared to 15 percent rural access).

There are three principal options for providing new connections to currently unserved populations in Africa, namely: i) extension

of the national grid: ii) installation of separate “mini” grids to operate independently from the main grid, and: iii) stand-alone gene-

rating systems that supply individual consumers. The most cost-effective approach for powering mini-grids is to use renewable

energy sources, which are widely available across Africa. However, the development of GMGs is not without challenges. Barriers

to the growth of private sector mini-grids in Africa include gaps in the policy and regulatory framework, the lack of proven business

models, the lack of market data and linkages, the lack of capacity of key stakeholders, and the lack of access to finance.

In response to these challenges, the SE4All Africa Hub at the African Development Bank (AfDB) designed and launched Phase

1 of the GMG MDP in 2015, with grant funding from the AfDB’s Sustainable Energy Fund for Africa (SEFA). The GMG MDP is a

pan-African platform that addresses the technical, policy, financial and market barriers confronting the emerging GMG sector. It is

part of a larger DFID-funded GMG Africa Programme, which also includes GMG initiatives in Kenya and Tanzania; country-specific

GMG policy development through SEFA; and an Action Learning and Exchange component being implemented by the Energy

Sector Management Assistance Program (ESMAP) at the World Bank.

The International Energy Agency (IEA) has predicted (in Africa Energy Outlook 2014) that by 2040, 70 percent of new rural elec-

tricity supply in Africa will be from stand-alone systems and mini-grids. The GMG MDP, SE4All, SEFA, ESMAP and similar pro-

grammes, which are contributing to falling costs, technological advancements and more efficiencies in GMG development, will

help to ensure that up to two thirds of this supply will be powered by renewables.

The goals of the green mini-grids programme, in all its aspects, is central to AfDB’s mission of spurring sustainable economic

development, social progress and poverty reduction in its regional member countries (RMCs). Indeed, off-grid and mini-grid solu-

tions are a key component of the AfDB’s New Deal on Energy for Africa, launched by the Bank’s president in January 2016. The

New Deal is a transformative, partnership-driven effort with an aspirational goal of achieving universal access to energy in Africa

by 2025.

This report was prepared by the firms Energy 4 Impact and INENSUS at the request of the AfDB. It was written by Peter Wes-

ton, Shashank Verma, Linda Onyango and Abishek Bharadwaj of Energy 4 Impact and Nico Peterschmidt and Michael Rohrer

of INENSUS. Energy 4 Impact, based in London, is a non-profit organization that advises off-grid energy businesses, in order to

reduce poverty through accelerated access to energy. INENSUS GmbH is a German consultancy firm focused on private sec-

tor-driven mini-grid electrification.

The content of this report was reviewed by Jeff Felten of the AfDB’s GMG team and cleared by Dr. Daniel-Alexander Schroth,

SE4All Africa Hub Coordinator at the AfDB. The report was edited by Deborah Davis.

4 GMG MDP Document Series: n°1

AC Alternating Current

AFD Agence Française de Développement

AGF African Guarantee Fund

AREF African Renewable Energy Fund

DC Direct Current

DCA Development Credit Authority (USAID)

DFI Development Finance Institution

EnDEV Energizing Development

ERC Energy Regulatory Commission

ESIA Environmental and Social Impact Assessment

GMG Green Mini-Grid

IEA International Energy Agency

IPP Independent Power Producer

KIS Kalangala Infrastructure Services Ltd

LOC Line of Credit

NGO Non-Governmental Organization

MNO Multiple Network Operators

MOU Memorandum of Understanding

MWh Megawatt hour

MWp Megawatt peak

OBA Output-Based Aid

OPIC Overseas Private Investment Corporation

PPA Power Purchase Agreement

PPP Public-Private Partnership

PRI Political Risk Insurance

REA Rural Electrification Authority

REPP Renewable Energy Performance Platform

SE4All Sustainable Energy for All

SEFA Sustainable Energy Fund for Africa

SUNREF Sustainable Use of Natural Resources and Energy Finance

TEDAP Tanzania Energy Development and Access Program

VAT Value-Added Tax

Abbreviations and Acronyms

5GMG MDP Document Series: n°1

1. EXECUTIVE SUMMARY

• Barriers to growth of mini-grids • Recommendations

2. INTRODUCTION

2.1 Context

2.2 Terms of reference

2.3 Background on mini-grids

3. BARRIERS TO THE DEVELOPMENT OF MINI-GRIDS, AND POSSIBLE SOLUTIONS

3.1 Introduction

3.2 Gaps in policy and regulation

3.2.1 Cost-reflective tariffs 3.2.2 Licensing and permits 3.2.3 Expansion of the main grid 3.2.4 Other regulatory issues

3.3 Lack of viable business models

3.3.1 Ownership models 3.3.2 Size models 3.3.3 Customer models 3.3.4 Demand management strategy 3.3.5 Promoting productive end use 3.3.6 Customer relationship and payment models

3.4 Lack of data and market linkages

3.4.1 Lack of statistical data 3.4.2 Lack of market linkage with communities 3.4.3 Lack of market linkage with productive use customers

3.5 Lack of capacity

3.6 Access to finance

3.6.1 Lack of right capital 3.6.2 Foreign exchange risk 3.6.3 Power purchase agreements 3.6.4 End user finance

4. RECOMMENDATIONS

4.1 Key recommendations

4.2 Financial assistance

4.2.1 Grants and subsidies 4.2.2 Concessional loans 4.2.3 Foreign exchange risk 4.2.4 Guarantees and insurance

4.3 Technical assistance

ANNEX 1: TECHNICAL ASSISTANCE THEMES FOR DEVELOPERS ANNEX 2: CONTRIBUTORS ANNEX 3: BIBLIOGRAPHY

Contents 7 7 9 11 11 11 11

13 13 13 13 14 15 16 16 16 17 18 19 20 21 21 21 22 22 22 22 24 25 25 25

27

27

29

29 29 30 30

31 33 34 35

6 GMG MDP Document Series: n°1

7GMG MDP Document Series: n°1

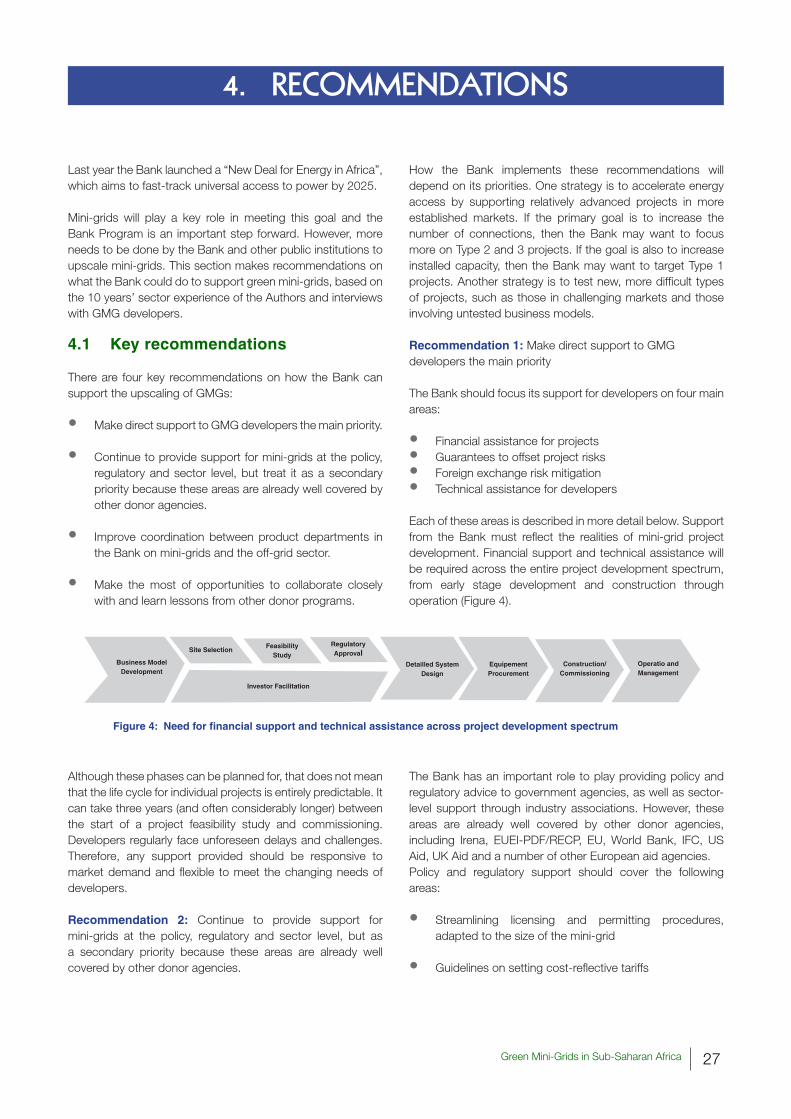

The African Development Bank (the “Bank”) has engaged the services of Energy4Impact (formerly GVEP International) and INENSUS GmbH to prepare a report analysing the main barriers to scaling up green mini-grids (GMGs) in Africa; how developers are overcoming these barriers; and what the Bank should do to support the sector. This is the first deliverable of the Business Development Support Business Line of the Bank’s Green Mini-Grid Africa Market Development Program (the “Bank Program”).

Barriers to growth of mini-grids

There are five main barriers to the growth of private sector mini-grids in Africa (mini-grids ranging in size from a few kilowatts up to 10MW). The most important for developers are (a) gaps in the policy and regulatory framework, specifically issues related to tariffs, licensing and arrival of the national grid. Other significant hurdles include (b) lack of proven business models; (c) lack of market data and linkages; (d) lack of capacity of key stakeholders; and (e) lack of access to finance.

The first and most important set of barriers relates to tariffs, licensing and arrival of the national grid. Most African countries have a uniform national tariff, which means that household consumers are charged the same tariff regardless of whether they are connected to the national grid or to a state-owned mini-grid in a remote rural area. The electricity generated from mini-grids is generally more expensive than grid power. While state-owned mini-grids are cross-subsidised, private mini-grids need to make a return on their investment, and therefore require cost-reflective tariffs to be viable. Some countries allow cost-reflective tariffs but many do not, and this holds back the growth of private mini-grids. Moreover, in countries that have specific regulations for private mini-grid operators, such as Kenya and Tanzania, the process of obtaining licences is often lengthy, bureaucratic and unclear. There are numerous government agencies involved and they often have overlapping responsibilities. To mitigate the tariff and licensing risks, developers may decide to develop smaller mini-grids (less than 100kWp) that are exempt from the regulatory regime, although such projects have other problems such as less legal protection and potential for local political interference.

The risk of a mini-grid being taken over by an expanding national grid is a major concern for private investors. Most African governments provide little information on grid expansion plans, and very few have clear rules on how mini-grids will be integrated into the grid and how mini-grid owners will be compensated if the grid arrives. These risks can be mitigated by selecting mini-grid sites that are located far from

the grid, or in areas such as islands where expansion of the grid is not economically feasible. However, these remote areas tend to have less economic activity to support a mini-grid.

The lack of a proven business model is the second major deterrent for private mini-grid investors. Business models may differ according to ownership (public, private, community, hybrids such as public-private partnerships); size of mini-grid (a few kilowatts to 10 megawatts); and customer target (households, small businesses or large anchor clients).

The most scalable model is the public-private partnership (PPP), which is any mini-grid that is funded, developed and operated through a partnership of public and private entities. For example, a government entity such as a rural electrification authority may develop and own the distribution, while a private investor owns the generation, operates the plant, and sells power to end users. There is no perfect model for PPPs. On the one hand, the more a mini-grid is supported by grants and subsidies, the lower the tariffs required by private investors and the more affordable they are to end users. On the other hand, the more a mini-grid depends on grants for its viability, the more difficult it is to expand the capacity of the mini-grid to meet increasing demand. This is because grants are usually only available for newly established mini-grids rather than expansions, and end users are unlikely to accept significantly increased tariffs to fund expansions. With a few exceptions such as direct current (DC)-based pico solar systems, which can power a few small household appliances for short periods of time, purely private projects are unlikely to be viable without subsidies to cover the cost of the distribution and part of the project development costs. The tariffs required by private investors will often be unaffordable if there are no subsidies. On the other hand, purely public isolated mini-grids are relatively expensive for public budgets to build and maintain versus grid-connected assets.

Mini-grids that focus on industry and businesses are more likely to reach a critical mass of customers and cover their fixed costs than those that focus only on households. This is why developers of smaller mini-grids (those under 1MW, especially under 100kW) often spend time promoting productive, income-generating uses for electricity. Larger mini-grids (those over 1MW) may sell their electricity through a power purchase agreement (PPA) to an anchor client such as a government entity or small industrial operation such as a telecom tower or flower farm. These larger mini-grids are likely to have more predictable cash flow and their construction and expansion may be easier to finance than mini-grids targeting smaller customers. However, there are relatively few anchor clients in rural Africa, and this is why it is critical for mini-grids to promote

1. EXECUTIVE SUMMARY

8 GMG MDP Document Series: n°1

consumption by smaller commercial users (for example, the village mill, pumps for horticulture, bars and restaurants).Matching electricity demand with supply is important for the project economics of mini-grids, particularly solar mini-grids, which generate only in daylight hours. Given the relatively small number of mini-grid customers and the homogeneity of the customer base (mostly households and household-based industries), it is important to identify customers such as grinding mills and wood or metal workshops that have the flexibility to actively manage their consumption to when solar irradiation is high. Demand management can be encouraged through tariff incentives and load scheduling, although to be effective, these need to be combined with good customer relations and reliable billing systems. New technologies such as mobile money payments and remote monitoring and control systems are important tools for customer-friendly demand management.

The third major obstacle for private investors is the lack of up-to-date and reliable data and market linkages with the community and income-generating users. At the national and regional level, there is limited data on grid expansion and policy and regulations. At the local level, there is generally little information on local demand and income levels, a situation further complicated by the seasonal migration of workers. Historical data on renewable resources is another problem for hydro, wind and biomass projects, if not so much for solar. Developers are getting around some of these problems by using GIS-based tools to fill data gaps. Others, particularly solar developers, are starting projects with diesel generators and small grids (which have lower upfront capital requirements) in order to assess demand before they invest in solar panels and larger grids.

Community engagement is another major challenge for developers. It takes time and money to understand the needs and priorities of the community. There should ideally be a vehicle through which the developer can negotiate and communicate with the community, for example a village power committee or whatever governance structure is most appropriate for the community concerned. As explained above, it is also critical to establish links with productive end users because they will help the mini-grid reach the critical mass of sales needed to cover the project’s fixed costs.

The fourth major deterrent for private investors is the lack of skills and experience at all levels of the mini-grid market, including public institutions, developers, financial institutions and local engineers and project management staff. This is a common theme across many industries in SSA, although the relative immaturity and rural nature of the mini-grid sector makes the situation more acute.

The fifth significant obstacle to mini-grids is lack of access to finance. Most mini-grids are financed through a mix of grants and subsidies, commercial equity and, in a few

rare cases, loans. Most mini-grids get at least 30 percent of their funding from grants, but many of these are inflexible, have high transaction costs, and suffer from disbursement delays, which can cause cash-flow problems for developers, most of whom require equity investment to build pilot projects and work out their business models. However, many commercial investors are put off by the lack of a proven, scalable business model in the sector, the low risk-adjusted returns and lack of successful exits. Despite these challenges, strategic investors such as Enel, EON, Engie and Caterpillar are investing in the sector, which suggests the sector is getting more mature.

Accessing credit is even more challenging for mini-grid developers than other types of financing. Most commercial banks are risk averse and are reluctant to lend until the risks described in this report have been mitigated. Local banks, in particular, have limited experience with cash flow lending and require high collateral from corporate borrowers. International lenders are concerned about the foreign exchange risk and are put off by the small ticket size of mini-grids. Development financing institutions (DFIs) may partly fill the gap, although their high transaction costs are not well suited to small projects.

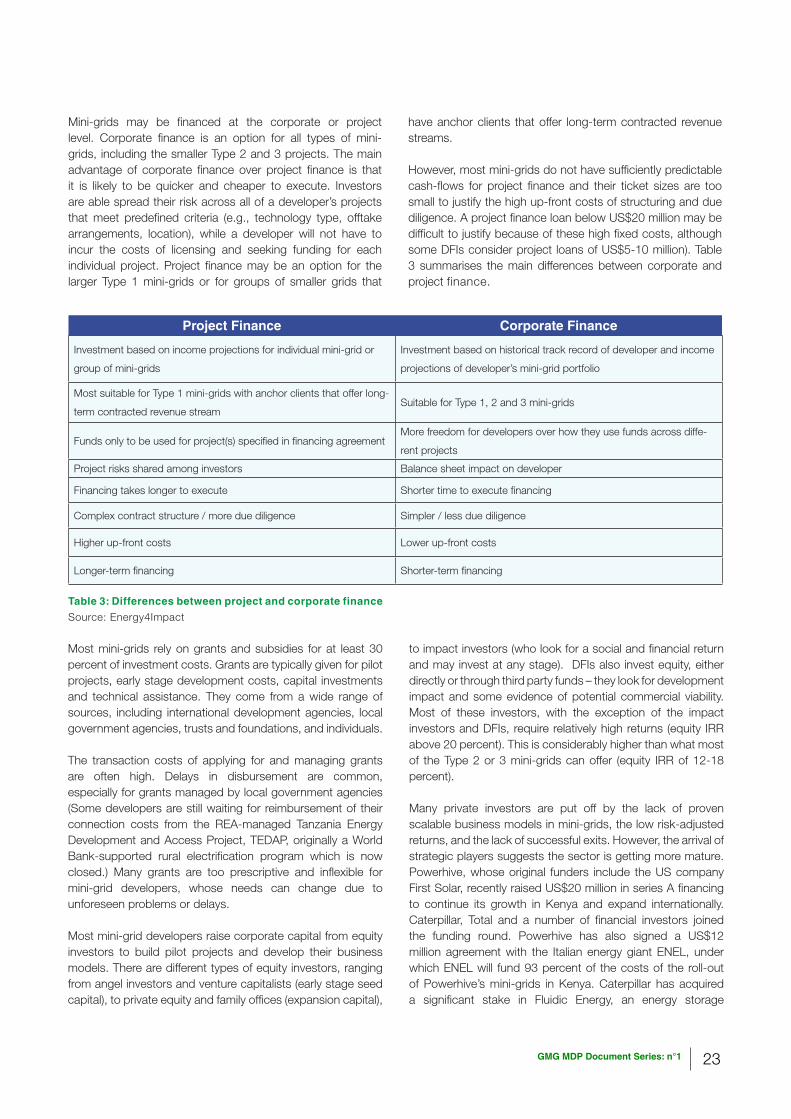

While project finance may be a good option for larger mini-grids (above 1 MW) with anchor clients that provide contracted, long-term revenue streams, experience has shown that most mini-grids do not have sufficiently predictable cash-flows for project finance, and are too small to justify the high up-front structuring and due diligence costs. However, for a creditworthy developer, smaller mini-grids can often be financed at the corporate level. Corporate finance is an option for all types of mini-grids, including smaller projects (less than 100 kW), and is likely to be quicker and cheaper to execute than project finance.

Another serious financing barrier is foreign exchange risk. Most of the capital costs of mini-grids are in hard currency, while their revenues are in local currency. This creates a currency mismatch for projects funded in hard currency. Mini-grids lose value in hard currency terms if the local currency loses value against it—although notably, this is not an issue for mini-grids located in the two CFA franc zones of Francophone Africa because their currency is pegged to the euro. There are a number of ways to hedge currency risk. Part of the solution is to use the operating costs of the mini-grid as a natural hedge. A mini-grid with sales in country has a natural hedge on its currency risk if its expenses are also in that currency. However, most of the foreign exchange risk will have to be hedged elsewhere. The next best solution is a local currency loan. However, such loans are often not available for the reasons explained above and, where they are available, the terms are often unattractive or unaffordable (high collateral, short tenure, above-market interest rates).

9GMG MDP Document Series: n°1

Another option is to borrow in hard currency and to purchase a hedging product to protect against the devaluation of the local currency, but this may well prove more expensive than a local currency loan. Some developers may simply choose to borrow in hard currency and take the risk of adverse currency movements. However, they face the risk of the mini-grid going out of business if the local currency devalues significantly. Increasing tariffs to offset currency losses (when they occur) is unlikely to be accepted by mini-grid customers or regulators.

There are many other challenges related to financing. Power purchase agreements for larger mini-grids may not be bankable and are often delayed. Yet without a PPA, the mini-grid will struggle to raise funding. Another challenge is end-user finance. Households and businesses may require support to cover the up-front cost of connection and inside electrical installation. To stimulate demand and solidify their customer base, some developers may provide short-term loans to help end users, particularly productive ones, to purchase electrical equipment.

Recommendations

Based on the analysis, there are four key recommendations for how the Bank can support the upscaling of GMGs:

1. Make direct support to GMG developers the main priority. Ensure that the support is flexible so it can be tailored to the changing needs of developers.

2. Continue to provide support at the policy, regulatory and sector levels, but this support can be a lower priority because these areas are already well covered by other donor agencies.

3. Improve coordination between the Bank’s mini-grid and off-grid product departments. This is important because the needs and priorities of mini-grids are very different from those of utility-scale power projects, which have been the traditional focus of the Bank.

4. Make the most of opportunities to collaborate closely with and learn lessons from other donor programs.

The Bank should focus its support for developers on financial assistance, foreign exchange risk mitigation, guarantees, and technical assistance. Financial assistance should include both grants and concessional loans. Developers require grants for early-stage development, construction and installation, and operational investments such as new connections and equipment for productive end users. They need concessional loans with low interest rate, long tenure and in local currency.

These loans could be provided directly by the Bank or through other channels, including credit lines to local banks. Where local currency loans are not possible, the Bank should consider other solutions to hedge the foreign exchange risk, such as a contingent line of credit to cover the risk. It is also important that the Bank offset other mini-grid risks through loan guarantees and specific risk guarantees. These guarantees could be triggered by events such as future grid extension, lower-than-expected revenues from productive users, and late payment by anchor clients.The current Bank Program is strongly focused on providing technical assistance to GMG developers. The support required will vary according to the level of experience and financial capability of each developer. Some will require light-touch support, while others will need more intensive support and possibly support on the ground.

Developers require four main types of technical assistance services: technical and engineering support; business and financial advice; legal and compliance advice; and market scoping, development and community engagement. The developers interviewed for this study indicated that assistance should focus on three areas:

• Transaction advisory services (helping developers to take projects through their development life cycle to reach financial closure)

• Early stage support (project feasibility and development work)

• End user support (promotion of productive end use and training).

Apart from general support services, developers made a few specific requests of the Bank, including:

• Publishing a best practice guide to mini-grid development and operation

• Providing technical assistance to local government agencies responsible for managing donor money, in order to introduce more transparency in their grant approval and disbursement processes

• Collaborating with other donors that manage grant and technical assistance programs for mini-grids. The idea is that these grant-funded projects will have a better chance of being realised if they have access to the technical assistance of the Bank’s GMG program.

GMG MDP Document Series: n°110

GMG MDP Document Series: n°1 11

2.1 Context

This report has been prepared by Energy4Impact (formerly GVEP International) and INENSUS (the “Authors”) for the African Development Bank (the “Bank”). It is the first of four deliverables for the Business Development Support Business Line of the Bank’s Green Mini-Grid (GMG) Africa Market Development Program (the “Bank Program”). For the second and third deliverables, the Authors will design, implement, manage and populate an online, interactive information portal for GMG developers in Africa. For the final deliverable, they will provide technical assistance to a select number of GMG developers.

2.2 Terms of reference

The Authors, each firm an GMG expert with more than 10 years of experience working with GMGs on the ground, were asked by the Bank to analyse the main barriers to scaling up green mini-grids in Africa, and what the Bank can do to overcome these barriers. The methodology consisted of a literature review and interviews with 22 developers of GMGs in 14 African countries (see Annex 2 for list). The first part of the report identifies the market, regulatory, financial and technical barriers to GMG development on the continent, and how they can be overcome. The second part makes recommendations

on how the Bank can support GMG developers through financial and technical assistance.

2.3 Background on mini-grids

The future of rural electrification depends on mini-grids. According to the International Energy Agency (IEA), electricity from green mini-grids will be the best solution for more than half of the rural population currently without access to power. Despite this bold prediction, very few mini-grids have been successfully deployed in Africa.

A mini-grid, also sometimes referred to as a micro-grid or nano-grid, is a set of small-scale electricity generators and possibly energy storage systems connected to a distribution network that supplies electricity to a small, localised group of customers and operates independently from the national transmission grid. They range in a size from a few kilowatts (kW) up to 10 megawatts (MW).

Mini-grids can be operated by state utilities, private companies, community-based organisations, or a mix of all three. They can run on diesel or renewables (solar PV, hydro, wind, biomass) or as renewable-diesel hybrids. However, the main barriers to private green mini-grids are not about technology – all the renewable technologies used are proven – but rather a combination of regulatory, market and finance issues.

2. INTRODUCTION

GMG MDP Document Series: n°112

13GMG MDP Document Series: n°1

3.1 Introduction

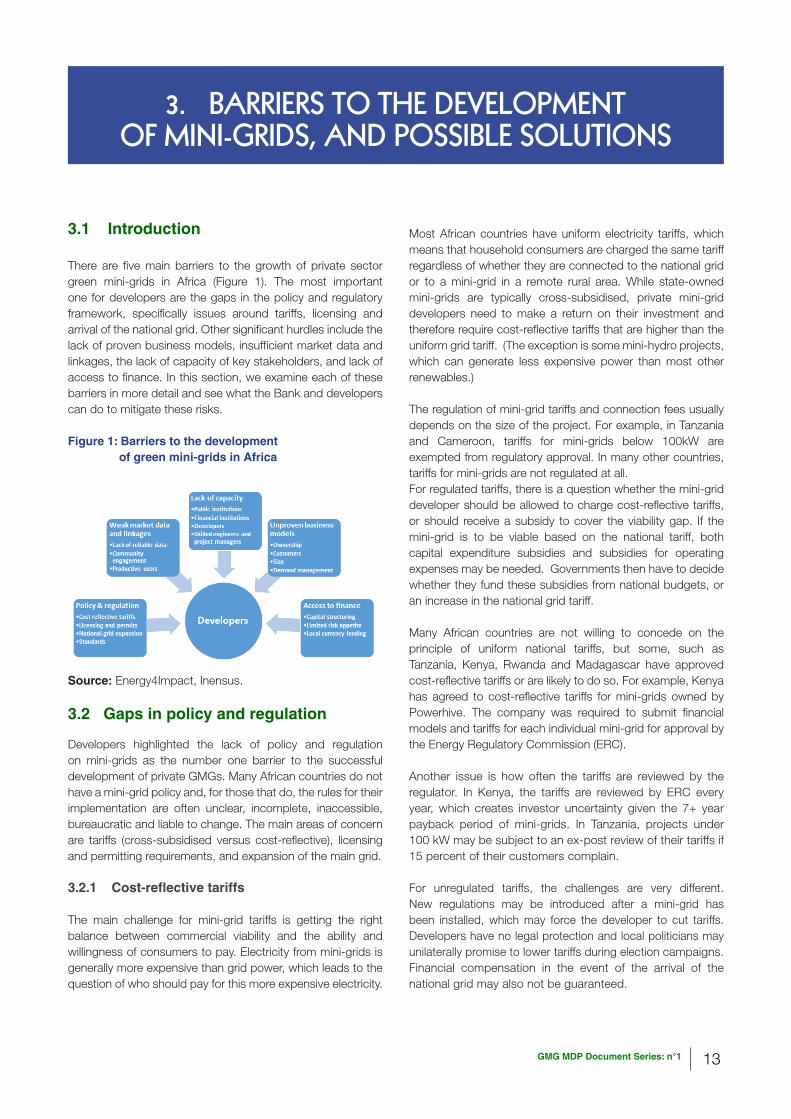

There are five main barriers to the growth of private sector green mini-grids in Africa (Figure 1). The most important one for developers are the gaps in the policy and regulatory framework, specifically issues around tariffs, licensing and arrival of the national grid. Other significant hurdles include the lack of proven business models, insufficient market data and linkages, the lack of capacity of key stakeholders, and lack of access to finance. In this section, we examine each of these barriers in more detail and see what the Bank and developers can do to mitigate these risks.

Figure 1: Barriers to the development of green mini-grids in Africa

Source: Energy4Impact, Inensus.

3.2 Gaps in policy and regulation

Developers highlighted the lack of policy and regulation on mini-grids as the number one barrier to the successful development of private GMGs. Many African countries do not have a mini-grid policy and, for those that do, the rules for their implementation are often unclear, incomplete, inaccessible, bureaucratic and liable to change. The main areas of concern are tariffs (cross-subsidised versus cost-reflective), licensing and permitting requirements, and expansion of the main grid.

3.2.1 Cost-reflective tariffs

The main challenge for mini-grid tariffs is getting the right balance between commercial viability and the ability and willingness of consumers to pay. Electricity from mini-grids is generally more expensive than grid power, which leads to the question of who should pay for this more expensive electricity.

Most African countries have uniform electricity tariffs, which means that household consumers are charged the same tariff regardless of whether they are connected to the national grid or to a mini-grid in a remote rural area. While state-owned mini-grids are typically cross-subsidised, private mini-grid developers need to make a return on their investment and therefore require cost-reflective tariffs that are higher than the uniform grid tariff. (The exception is some mini-hydro projects, which can generate less expensive power than most other renewables.)

The regulation of mini-grid tariffs and connection fees usually depends on the size of the project. For example, in Tanzania and Cameroon, tariffs for mini-grids below 100kW are exempted from regulatory approval. In many other countries, tariffs for mini-grids are not regulated at all. For regulated tariffs, there is a question whether the mini-grid developer should be allowed to charge cost-reflective tariffs, or should receive a subsidy to cover the viability gap. If the mini-grid is to be viable based on the national tariff, both capital expenditure subsidies and subsidies for operating expenses may be needed. Governments then have to decide whether they fund these subsidies from national budgets, or an increase in the national grid tariff.

Many African countries are not willing to concede on the principle of uniform national tariffs, but some, such as Tanzania, Kenya, Rwanda and Madagascar have approved cost-reflective tariffs or are likely to do so. For example, Kenya has agreed to cost-reflective tariffs for mini-grids owned by Powerhive. The company was required to submit financial models and tariffs for each individual mini-grid for approval by the Energy Regulatory Commission (ERC).

Another issue is how often the tariffs are reviewed by the regulator. In Kenya, the tariffs are reviewed by ERC every year, which creates investor uncertainty given the 7+ year payback period of mini-grids. In Tanzania, projects under 100 kW may be subject to an ex-post review of their tariffs if 15 percent of their customers complain.

For unregulated tariffs, the challenges are very different. New regulations may be introduced after a mini-grid has been installed, which may force the developer to cut tariffs. Developers have no legal protection and local politicians may unilaterally promise to lower tariffs during election campaigns. Financial compensation in the event of the arrival of the national grid may also not be guaranteed.

3. BARRIERS TO THE DEVELOPMENT OF MINI-GRIDS, AND POSSIBLE SOLUTIONS

14 GMG MDP Document Series: n°1

Tips for developers

• Lobbying for cost-reflective tariffs should be a top priority.

• Convert per kWh tariffs into time or flat rate tariffs because they are generally unregulated. However, the main drawback of such tariffs is that they encourage greater and less efficient electricity usage by households.

In extreme cases, the flat rate may not cover the costs of electricity production and consumers may not accept an increase. There is also a risk that the regulator may eventually ask about the cost per kWh and decide to regulate such tariffs.

• Sell services to productive users rather than selling the electricity itself, to reduce the likelihood of the tariff being regulated. For example, sell water rather than electricity for water pumping, or sell mechanical energy to mills rather than electricity for the milling machines. (This means that mini-grids have to operate secondary businesses.)

Tips for governments and regulators

• Introduce laws and regulations for cost-reflective tariffs to minimise the potential for intervention by new government administrations.

• Provide tariff guarantees for up to 15 years to improve revenue certainty and attract long-term capital into mini-grids.

3.2.2 Licensing and permits

Another challenge for developers is the bureaucracy and lack of clarity around the licensing and permitting of mini-grids. Depending on the type of project, licences may be required for the generation, distribution and sale of electricity. For largerprojects,developers may also need to negotiate a concession contract or power purchase agreement.

The licensing and permitting process is frequently designed for larger utility-scale projects and may be too long and costly for mini-grids. In addition to the licences, other documents that may be required include certificates of incorporation, land lease or ownership documents, construction permits, environmental and social impact assessments (ESIAs), health and safety certificates, water use rights (for hydro projects) and rights of way. Titles to land are often unclear, and getting way leaves can take time. Some developers end up making informal agreements with community leaders in order to gain access to land where distribution wires and poles need to be installed.

Moreover, approvals are often required from multiple different agencies with overlapping responsibilities. In Kenya, three government agencies are involved in providing licences and permits (the Ministry of Energy, ERC and the county government). Depending on the type of project, further approvals may be required from the National Environmental Management Authority, Ministry of Lands (for way leaves), Water Resource Management Authority (for hydro) and the Kenya Civil Aviation Authority (for wind). The licensing and permitting process can take up to three years, and developers are required to submit separate applications for each site. In Mali, one agency (AMADER) takes all the major decisions on mini-grids, and this has played a big part in the successful deployment of mini-grids in the country. In Tanzania, developers are unhappy with the process for ESIAs, which can take up to nine months.

Developers also complain about the cost of obtaining separate licences for each mini-grid site. They argue that it would be more cost-efficient to have a single licence that covers a portfolio of similar sites (e.g., same technology, same region, same business model). There are also issues around the licence fees themselves. In Uganda, for example, the licence for a mini-grid of 10kW costs the same as the licence for a 500 kW mini-grid.

There have been several cases in East Africa of unregulated mini-grids being built on sites for which another developer is seeking a licence. In some cases, governments have stepped in to resolve the dispute. In others, politicians have been reluctant to stop the illegal projects because they bring much- needed electricity to rural populations and are “good for votes”.

Consideration needs to be given to the issue of licence transfers. Investors are likely be deterred if they cannot transfer a licence to a potential buyer. Potential lenders may also want to have the right to step in when a project underperforms and transfer its licence to a new operator.Most countries in Africa have not yet developed laws and regulations for private investment in mini-grids. In Senegal, there are rules for mini-grids but not for private sector investment in mini-grids. In Nigeria, there are plans for new regulations that could exempt mini-grids under 100 kW from tariff approval. In Benin, mini-grid regulations could be passed by the end of 2017. In Mali, most mini-grids are concessions financed by grants, although there are moves to bring private investment into the sector. In Rwanda, there are new regulations for mini-grids, but not so many large rural communities without electricity, so the market is relatively limited. In Sierra Leone, there are currently no laws to allow private investors to supply end users. In Uganda, there are mini-grid regulations, but the administrative procedures are burdensome.

15GMG MDP Document Series: n°1

Tips for developers

• Develop very small micro-grids which do not require a licence, for example up to 100 kW in Tanzania and up to 20kW in Mali, bearing in mind that unlicensed projects have fewer legal protections and are susceptible to local political interference. Also, smaller mini-grids may not be able to support large enough productive loads to make the project economically viable (see section 3.3.3).

Tips for governments and regulators

• Keep licensing requirements as minimal and as streamlined as possible.

• Keep the number of agencies approving licences and permits to a minimum, and avoid overlapping roles and responsibilities.

• Allow single licence applications for multiple sites.

3.2.3 Expansion of the main grid

Grid expansion is a major concern for mini-grid developers. Most national grid operators are state owned, and many are very poor at providing information on the timing and location of planned grid expansions. Some countries such as Tanzania and Namibia do publish their plans, but these plans are often overtaken by political considerations.

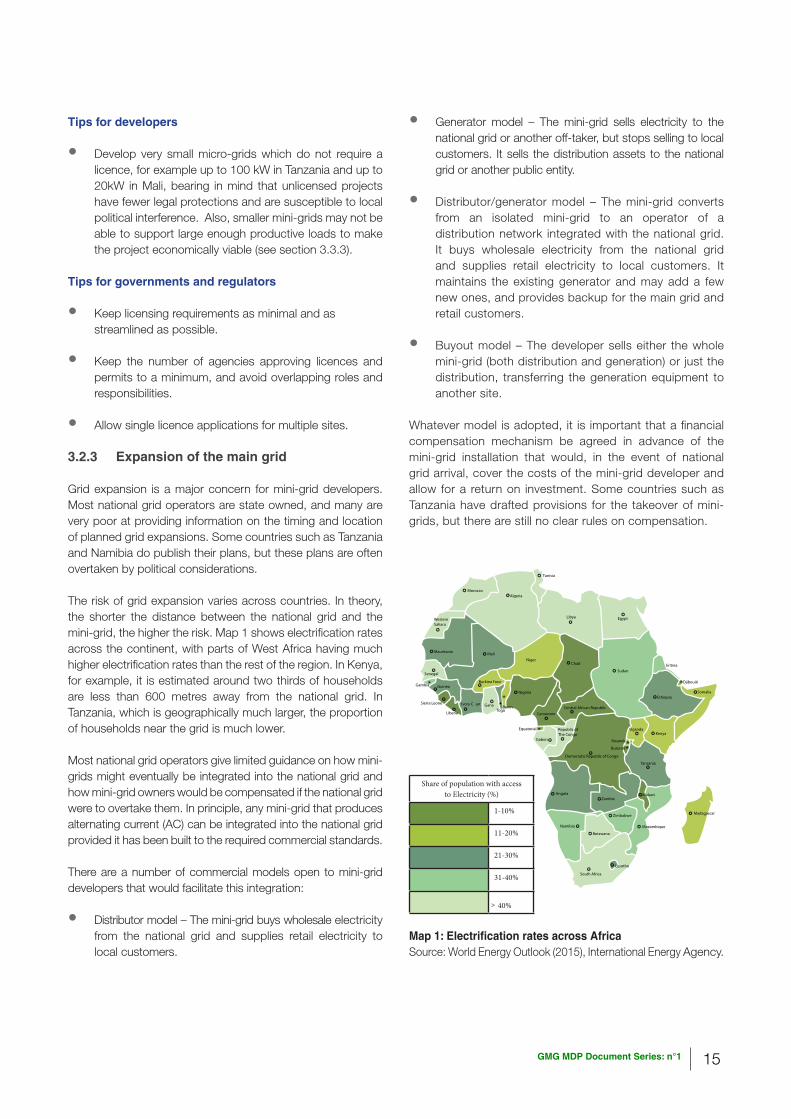

The risk of grid expansion varies across countries. In theory, the shorter the distance between the national grid and the mini-grid, the higher the risk. Map 1 shows electrification rates across the continent, with parts of West Africa having much higher electrification rates than the rest of the region. In Kenya, for example, it is estimated around two thirds of households are less than 600 metres away from the national grid. In Tanzania, which is geographically much larger, the proportion of households near the grid is much lower.

Most national grid operators give limited guidance on how mini-grids might eventually be integrated into the national grid and how mini-grid owners would be compensated if the national grid were to overtake them. In principle, any mini-grid that produces alternating current (AC) can be integrated into the national grid provided it has been built to the required commercial standards.

There are a number of commercial models open to mini-grid developers that would facilitate this integration:

• Distributor model – The mini-grid buys wholesale electricity from the national grid and supplies retail electricity to local customers.

• Generator model – The mini-grid sells electricity to the national grid or another off-taker, but stops selling to local customers. It sells the distribution assets to the national grid or another public entity.

• Distributor/generator model – The mini-grid converts from an isolated mini-grid to an operator of a distribution network integrated with the national grid. It buys wholesale electricity from the national grid and supplies retail electricity to local customers. It maintains the existing generator and may add a few new ones, and provides backup for the main grid and retail customers.

• Buyout model – The developer sells either the whole mini-grid (both distribution and generation) or just the distribution, transferring the generation equipment to another site.

Whatever model is adopted, it is important that a financial compensation mechanism be agreed in advance of the mini-grid installation that would, in the event of national grid arrival, cover the costs of the mini-grid developer and allow for a return on investment. Some countries such as Tanzania have drafted provisions for the takeover of mini-grids, but there are still no clear rules on compensation.

Map 1: Electrification rates across AfricaSource: World Energy Outlook (2015), International Energy Agency.

Share of population with access to Electricity (%)

1-10%

11-20%

21-30%

31-40%

40%^

16 GMG MDP Document Series: n°1

Tips for developers

• Select mini-grid sites either a long way from the national grid or in areas where grid expansion may not be economically feasible, such as islands. However, remote sites are likely to have less economic activity and less potential for productive use of electricity.

• Develop mini-grids that are technically compatible with the national grid and therefore not likely to end up in competition with the state utility or rural electrification authority (REA).

Tips for governments and regulators

• Improve communication of grid expansion plans.

• Establish technical standards for integration of mini-grids into the national grid.

• Establish rules on financial compensation for the takeover of mini-grids. Make sure that any incentives such as feed-in tariffs are linked to the installation date of the mini-grid’s generation assets and not to the date of connection to the main grid.

• Consider using grants to finance the distribution systems of private mini-grids to ensure they are built to national grid standards.

3.2.4 Other regulatory issues

Other important regulatory issues that deter investments in mini-grids include the lack of:

• Consumer protection (to guarantee that products and services supplied to end users are safe)

• Technical regulation (to ensure safe and reliable operation of the mini-grids)

• Quality of service regulation (to ensure the quality, availability and continuity of electricity supply).

Some investors prefer to invest only in the mini-grid kit rather than in a scheme that includes end-user connections because of concerns about health and safety and associated reputation risks. Fiscal policy and regulations (e.g., for taxes, import duties and subsidies) pose another challenge for mini-grids. In Rwanda, for example, mini-grids are disadvantaged against solar home systems because sales of electricity are required to pay a value-added tax (VAT), while sales of solar home systems are not. Also, solar home systems do not pay any import duties, while some non-solar components of mini-grids are taxed. (Solar components of mini-grids are not taxed.) There are also specific taxes for different types

of technologies. In some countries, for example, water taxes can account for up to half the operation costs of mini-hydro projects.

3.3 Lack of viable business models

There is currently no proven business model for mini-grid development in Africa. Many models have been tried, but none has been a great success. The models vary by ownership, size, and customer target. Matching electricity demand with supply is critical for mini-grid project economics, particularly for solar projects, which only generate in daylight hours.

3.3.1 Ownership models

None of the established owner-operator models – public utility, community or non-governmental organisation (NGO), private, or hybrid such as a public-private partnership (PPP) ¬– has worked particularly well. However, the one with the most potential for scale-up is the PPP.

In a typical public utility model, the utility owns and manages all aspects of the mini-grid, which is often run on expensive diesel. It is financed by public funds and usually charges the uniform national tariff, which is cross subsidised by customers connected to the main grid. This is not a sustainable strategy for capital-constrained utilities. Many have therefore shifted their focus away from mini-grids to other priorities such as increasing connections in areas already served by the main grid. This has resulted in many mini-grids being poorly maintained and short of funds to invest in replacement kit.

In the community model, the community or a local NGO owns and manages the mini-grid for the benefit of community members. These mini-grids are typically financed by grants and small in-kind contributions such as land, labour and materials. These mini-grids set tariffs to only cover operation and maintenance costs, retaining a small percentage to cover replacement parts. Most are budget-constrained and do not generate sufficient profits to scale up. They are generally operated by local teams with little professional oversight, resulting in poor maintenance and lengthy repair times. Funds allocated for replacement parts are frequently diverted to non-essential tasks for local political reasons.

In the private model, a private investor builds, owns and operates the mini-grid. The funding usually comes from a mix of private sources and grants. The grants are important to cover the cost of the distribution network and a portion of the project development costs. They are also important to keep tariffs at an affordable level. (Pico solar systems based on DC electricity may not require grants because customers are willing to pay more per kWh.) Some mini-grids may not be able to offer affordable tariffs to productive users or guarantee the reliable supply that these users need in the absence of

17GMG MDP Document Series: n°1

government subsidies, and may therefore struggle to gain the acceptance of consumers and policymakers. Examples of private players include Powerhive in Kenya and Mesh Power in Rwanda. They have operated successfully due to the ability to charge cost-reflective tariffs.

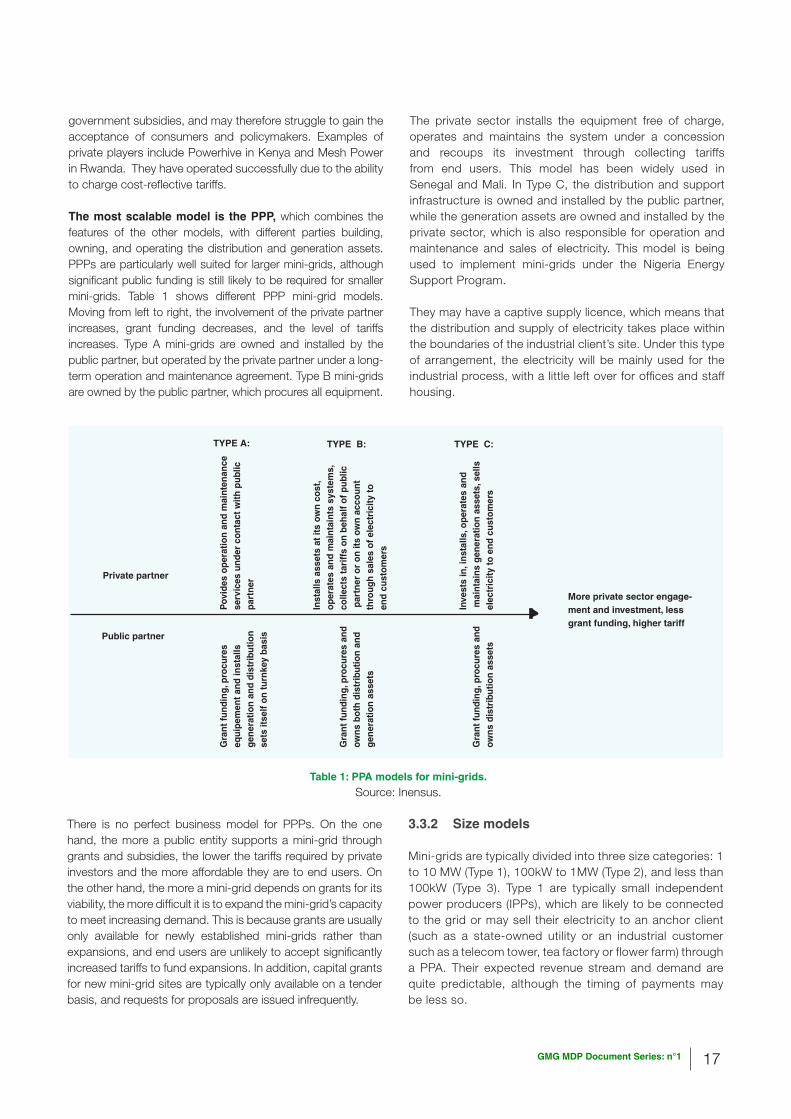

The most scalable model is the PPP, which combines the features of the other models, with different parties building, owning, and operating the distribution and generation assets. PPPs are particularly well suited for larger mini-grids, although significant public funding is still likely to be required for smaller mini-grids. Table 1 shows different PPP mini-grid models. Moving from left to right, the involvement of the private partner increases, grant funding decreases, and the level of tariffs increases. Type A mini-grids are owned and installed by the public partner, but operated by the private partner under a long-term operation and maintenance agreement. Type B mini-grids are owned by the public partner, which procures all equipment.

The private sector installs the equipment free of charge, operates and maintains the system under a concession and recoups its investment through collecting tariffs from end users. This model has been widely used in Senegal and Mali. In Type C, the distribution and support infrastructure is owned and installed by the public partner, while the generation assets are owned and installed by the private sector, which is also responsible for operation and maintenance and sales of electricity. This model is being used to implement mini-grids under the Nigeria Energy Support Program.

They may have a captive supply licence, which means that the distribution and supply of electricity takes place within the boundaries of the industrial client’s site. Under this type of arrangement, the electricity will be mainly used for the industrial process, with a little left over for offices and staff housing.

There is no perfect business model for PPPs. On the one hand, the more a public entity supports a mini-grid through grants and subsidies, the lower the tariffs required by private investors and the more affordable they are to end users. On the other hand, the more a mini-grid depends on grants for its viability, the more difficult it is to expand the mini-grid’s capacity to meet increasing demand. This is because grants are usually only available for newly established mini-grids rather than expansions, and end users are unlikely to accept significantly increased tariffs to fund expansions. In addition, capital grants for new mini-grid sites are typically only available on a tender basis, and requests for proposals are issued infrequently.

3.3.2 Size models

Mini-grids are typically divided into three size categories: 1 to 10 MW (Type 1), 100kW to 1MW (Type 2), and less than 100kW (Type 3). Type 1 are typically small independent power producers (IPPs), which are likely to be connected to the grid or may sell their electricity to an anchor client (such as a state-owned utility or an industrial customer such as a telecom tower, tea factory or flower farm) through a PPA. Their expected revenue stream and demand are quite predictable, although the timing of payments may be less so.

Table 1: PPA models for mini-grids.

Source: Inensus.

Pov

ides

ope

ratio

n an

d m

aint

enan

cese

rvic

es u

nder

con

tact

with

pub

lic

part

ner

Inst

alls

ass

ets

at it

s ow

n co

st,

oper

ates

and

mai

ntai

nts

syst

ems,

co

llect

s ta

riff

s on

beh

alf o

f pub

lic p

artn

er o

r on

its

own

acco

unt

thro

ugh

sale

s of

ele

ctri

city

to

end

cust

omer

s

Inve

sts

in, i

nsta

lls, o

pera

tes

and

mai

ntai

ns g

ener

atio

n as

sets

, sel

ls

elec

tric

ity to

end

cus

tom

ers

Gra

nt fu

ndin

g, p

rocu

res

equi

pem

ent a

nd in

stal

ls

gen

erat

ion

and

dist

ribu

tion

sets

itse

lf on

turn

key

basi

s

Gra

nt fu

ndin

g, p

rocu

res

and

ow

ns b

oth

dist

ribu

tion

and

gen

erat

ion

asse

ts G

rant

fund

ing,

pro

cure

s an

d ow

ns d

istr

ibut

ion

asse

ts

More private sector engage-ment and investment, less grant funding, higher tariff

Private partner

Public partner

TYPE A: TYPE B: TYPE C:

v

18 GMG MDP Document Series: n°1

Type 1 mini-grids will not typically require a retail supply licence if they do not sell electricity outside the industrial site. Depending on the track record of the developer and the economics of the project, they may be able to attract corporate or project finance (see Section 3.6.6). Potential difficulties include the creditworthiness of the off-taker, the bankability of the PPA, and the threat of future competition from grid power.

Type 2 projects are too small to be structured as traditional IPPs, but may be structured as micro-concessions or micro-IPPs, and are large enough to fall under licensing and tariff regulations. In some countries such as Kenya, Type 2 mini-grids have been delivered mainly through a public ownership model, but private sector models do exist, for example in Tanzania.

Type 3 projects have the most potential customers and include small mini-grids, micro-grids and nano-grids. These projects run mainly on solar, are relatively easy to mobilise, often have low-voltage distribution grids covering small areas, and do not necessarily provide grid-quality electricity. There are no standard business models for Type 3 projects, but the more successful projects generally have cost-reflective tariffs and light regulation (see sections 3.2.1 and 3.2.2). They are generally better suited to corporate financing than project financing (i.e., financing at the level of the developer rather than the project) due to the small size of the projects and the lack of long-term contracted revenues (see Section 3.6.6).

Tips for developers

• Type 1 – Select a strong, creditworthy off-taker, preferably one that has a reputation for paying on time.

• Types 2 and 3 – Select sites in areas of high population density where customers are willing and able to pay.

• Types 2 and 3 – Ensure tariffs are high enough to speed up repayment of loans (target should be below 10 years). Quick repayment is particularly important for projects not protected by a licence.

3.3.3 Customer models

There are a number of ways in which mini-grids can cover their fixed costs and reach a critical mass of customers.The first approach is called “clustering”. Here the developer bundles several unconnected micro-grid sites that are located close together under one operational platform in order to save on overhead.

The second approach is the “ABC” model. Here the developer sells to a large industrial customer or group of industrials with reliable cash flows. This has the advantage of diversifying the customer case and supporting local economic development:

• “A” are Anchor customers with large consumer loads, such as processing and manufacturing plants, telecom towers, flower farms, hotels, resorts, and mines.

• “B” are income-generating Business customers with (a) productive loads such as grind mills, saw mills, wood or metal-working shops, welders, blenders and oil pressers; (b) agricultural loads such as irrigation pumps, cold storage and food processing; and (c) commercial loads such as shops, bars, ice makers, bakers, internet cafes, mobile phone chargers and energy kiosks.

• “C” stands for Community such as households, churches and community centres. In the ABC model, these make up a relatively small proportion of the mini-grid’s revenues.

There are no rules on what the minimum size of a mini-grid should be. According to Inensus, solar mini-grids would typically need more than 5,000 household customers to cover their fixed costs, but may still struggle to compete for household customers against solar home systems. Selling to larger productive users may be a better strategy because their demand requirements are higher than the power range of most solar home systems. In this case, the minimum capacity for a viable solar mini-grid is likely to be 20-50 kWp.Unfortunately, there are relatively few large anchor clients located in rural areas of Africa, and this is one reason why mini-grids have not taken off. It is also why it is so important for mini-grids to promote consumption by productive users.

Telecom towers have played an important role as anchor clients in the development of mini-grids in India, but have not done so far in Africa. Most towers in India are located near population centres and are operated by private companies serving multiple network operators (MNOs). In Africa, telecom towers are often located in sparsely populated areas, operated by the MNOs themselves, and require developers to sign contracts for at least 100 towers, which will only work for mini-grids developed at scale. MNOs also have very stringent requirements for service and availability of power, and the high- specification mini-grids needed to serve them may not be viable.

Despite these challenges, the ABC model still appears to offer the best potential marketing strategy for scaling mini-grids. Take the case of Fluidic Energy, an energy storage technology company backed by Caterpillar and the family behind Walmart. Fluidic recently signed an agreement with the Government of Madagascar to supply solar PV and battery storage mini-grids to 100 remote communities (7.5 MWp of PV panels and 45 MWh of energy storage).

They are also exploring with the local Caterpillar dealer the possibility of local in-country manufacturing (assembly). What makes Fluidic interesting is that it has already sold storage batteries to nearly 12 major telecom companies in developing

19GMG MDP Document Series: n°1

countries, including in Africa, so there may still be hope for telecom companies to be anchor clients for African mini-grids.

3.3.4 Demand management strategy

Matching electricity demand with supply is particularly important for mini-grids. Clearly the more of the electricity production that can be sold, the better the economics of the project. However, it is difficult for mini-grids to achieve this balance because demand can be volatile due to the relatively small number of customers and modest financial means of the customer base.

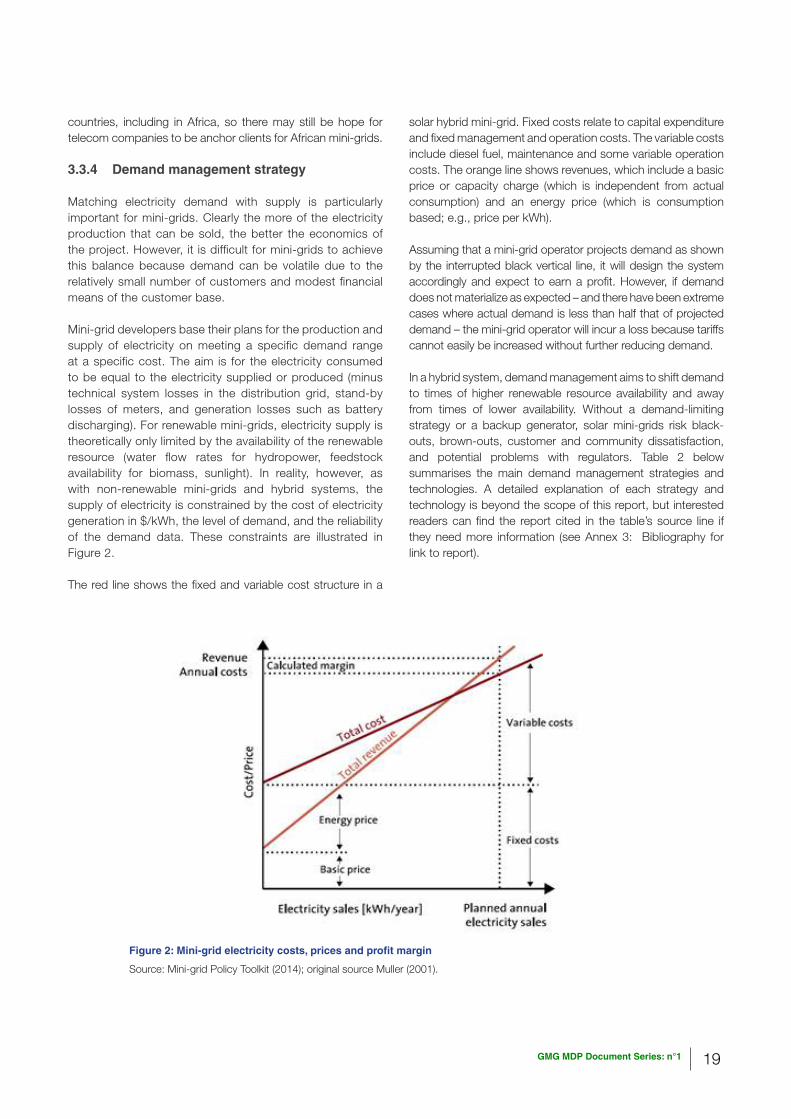

Mini-grid developers base their plans for the production and supply of electricity on meeting a specific demand range at a specific cost. The aim is for the electricity consumed to be equal to the electricity supplied or produced (minus technical system losses in the distribution grid, stand-by losses of meters, and generation losses such as battery discharging). For renewable mini-grids, electricity supply is theoretically only limited by the availability of the renewable resource (water flow rates for hydropower, feedstock availability for biomass, sunlight). In reality, however, as with non-renewable mini-grids and hybrid systems, the supply of electricity is constrained by the cost of electricity generation in $/kWh, the level of demand, and the reliability of the demand data. These constraints are illustrated in Figure 2.

The red line shows the fixed and variable cost structure in a

solar hybrid mini-grid. Fixed costs relate to capital expenditure and fixed management and operation costs. The variable costs include diesel fuel, maintenance and some variable operation costs. The orange line shows revenues, which include a basic price or capacity charge (which is independent from actual consumption) and an energy price (which is consumption based; e.g., price per kWh).

Assuming that a mini-grid operator projects demand as shown by the interrupted black vertical line, it will design the system accordingly and expect to earn a profit. However, if demand does not materialize as expected – and there have been extreme cases where actual demand is less than half that of projected demand – the mini-grid operator will incur a loss because tariffs cannot easily be increased without further reducing demand.

In a hybrid system, demand management aims to shift demand to times of higher renewable resource availability and away from times of lower availability. Without a demand-limiting strategy or a backup generator, solar mini-grids risk black-outs, brown-outs, customer and community dissatisfaction, and potential problems with regulators. Table 2 below summarises the main demand management strategies and technologies. A detailed explanation of each strategy and technology is beyond the scope of this report, but interested readers can find the report cited in the table’s source line if they need more information (see Annex 3: Bibliography for link to report).

Figure 2: Mini-grid electricity costs, prices and profit margin

Source: Mini-grid Policy Toolkit (2014); original source Muller (2001).

20 GMG MDP Document Series: n°1

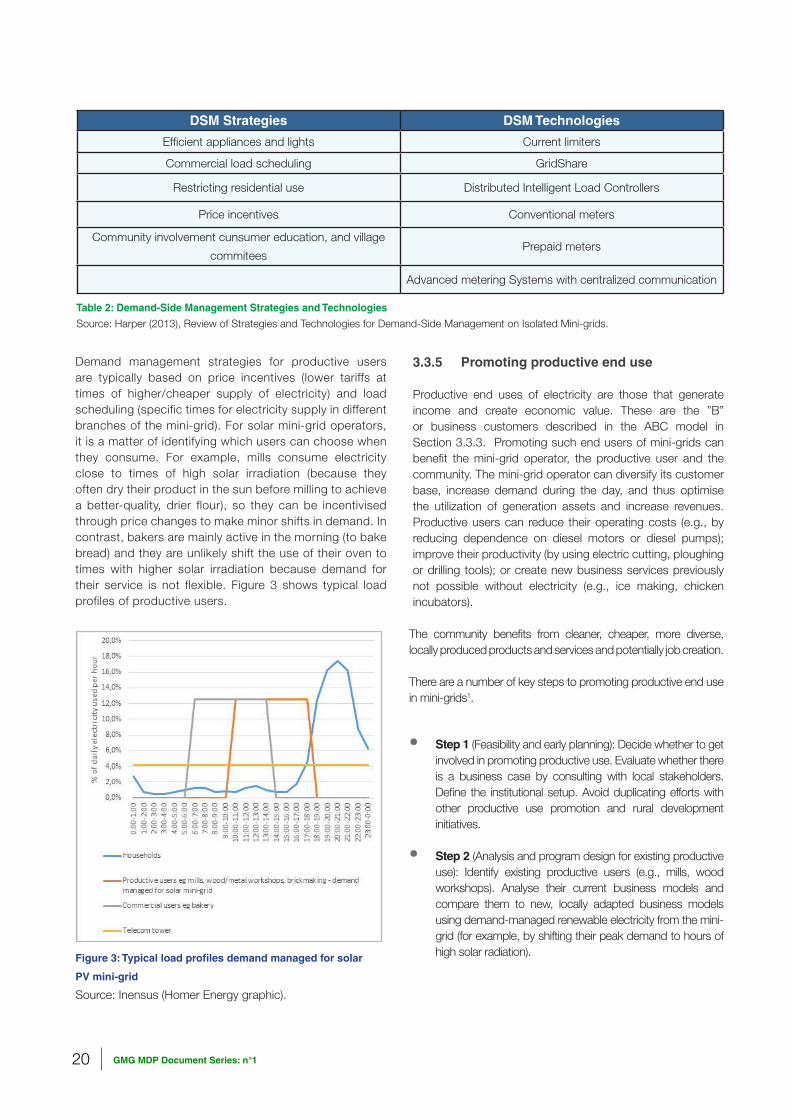

Demand management strategies for productive users are typically based on price incentives (lower tariffs at times of higher/cheaper supply of electricity) and load scheduling (specific times for electricity supply in different branches of the mini-grid). For solar mini-grid operators, it is a matter of identifying which users can choose when they consume. For example, mills consume electricity close to times of high solar irradiation (because they often dry their product in the sun before milling to achieve a better-quality, drier flour), so they can be incentivised through price changes to make minor shifts in demand. In contrast, bakers are mainly active in the morning (to bake bread) and they are unlikely shift the use of their oven to times with higher solar irradiation because demand for their service is not flexible. Figure 3 shows typical load profiles of productive users.

3.3.5 Promoting productive end use

Productive end uses of electricity are those that generate income and create economic value. These are the ”B” or business customers described in the ABC model in Section 3.3.3. Promoting such end users of mini-grids can benefit the mini-grid operator, the productive user and the community. The mini-grid operator can diversify its customer base, increase demand during the day, and thus optimise the utilization of generation assets and increase revenues. Productive users can reduce their operating costs (e.g., by reducing dependence on diesel motors or diesel pumps); improve their productivity (by using electric cutting, ploughing or drilling tools); or create new business services previously not possible without electricity (e.g., ice making, chicken incubators).

Figure 3: Typical load profiles demand managed for solar

PV mini-grid

Source: Inensus (Homer Energy graphic).

Table 2: Demand-Side Management Strategies and Technologies

Source: Harper (2013), Review of Strategies and Technologies for Demand-Side Management on Isolated Mini-grids.

The community benefits from cleaner, cheaper, more diverse, locally produced products and services and potentially job creation.

There are a number of key steps to promoting productive end use in mini-grids1.

• Step 1 (Feasibility and early planning): Decide whether to get involved in promoting productive use. Evaluate whether there is a business case by consulting with local stakeholders. Define the institutional setup. Avoid duplicating efforts with other productive use promotion and rural development initiatives.

• Step 2 (Analysis and program design for existing productive use): Identify existing productive users (e.g., mills, wood workshops). Analyse their current business models and compare them to new, locally adapted business models using demand-managed renewable electricity from the mini-grid (for example, by shifting their peak demand to hours of high solar radiation).

DSM Strategies DSM Technologies

Efficient appliances and lights Current limiters

Commercial load scheduling GridShare

Restricting residential use Distributed Intelligent Load Controllers

Price incentives Conventional meters

Community involvement cunsumer education, and village

commiteesPrepaid meters

Advanced metering Systems with centralized communication

21GMG MDP Document Series: n°1

• Step 3 (Analysis and program design for new productive use): Identify potential new productive users (e.g., farmers willing to use load-managed irrigation). Develop business models, and seek business partners/investors (possibly through setting up investor forums with the community and regional public authorities).

• Step 4 (Implementation): Raise awareness of productive electricity use. Provide technical assistance to productive users. Facilitate access to development funding for technical assistance and new equipment for users, such as electric motors and pumps. Ensure that the mini-grid is technically ready to support productive users. If the grid is not well designed, connections to electric motors can cause voltage fluctuations, which can have a negative impact on other grid customers and reduce the life of their appliances.

• Step 5 (Monitoring and evaluation): Set clear objectives and assess impacts. Monitor institutions and macro results. Feed results back to improve future planning.

Tips for developers

• Start developing productive use of electricity as soon as possible. For solar mini-grids, prioritise larger productive users that can be demand managed, such as mills and wood or metal workshops.

• Lobby donors and governments for funds to promote productive end use.

3.3.6 Customer relationship and payment models

One of the critical success factors in any mini-grid is good customer relationship management and payment collection. It is important to understand the social fabric of the community and to adjust the revenue collection mechanism to local conditions. It is also important to have a functioning and reliable billing system. New technologies such as mobile payments and remote monitoring and control systems have shown promise. In Kenya, for example, many mini-grids now use smart meters, which link the electricity supply equipment to prepayment services that go through M-Pesa, a mobile money transfer system. Payments are recorded and cashless, and made directly to the account of the owner of the mini-grid, which reduces the potential – and perceived potential – for financial impropriety.

Productive users need a stable tariff because a sharp increase (e.g., more than 10 percent) can drive their businesses into bankruptcy.

3.4 Lack of data and market linkages

3.4.1 Lack of statistical data

One of the challenges for private investors in mini-grids is the lack of reliable data. On both the national and regional level, there is often limited information on grid expansion plans and the policy and regulatory framework. In addition, macro-economic data and national census numbers are frequently out of date and are susceptible to political manipulation.

At the site level, there is often limited data on the key parameters needed to make an investment decision. These parameters include the number and average income of village residents; location and type (semi industrial or industrial) of productive businesses; location of education and health facilities; and the GPS locations of the villages and their distance from the national grid. The quality of data can be further compromised by factors such as the seasonality of businesses such as agriculture, the migration of workers, and tribal conflicts (which can lead to large numbers of people leaving a village). Another challenge is the lack of historic data on renewable resources. This is not a problem for solar mini-grids, but it is critical for hydro, wind and biomass projects.

Tips for developers

• Spend time locally to get your demand assessment right.

• Consider starting a mini-grid project with a diesel generator (low capital expenditure, high operating expenditure) and a small grid, and then add renewable generation assets (high capital expenditure, low operating expenditure) as demand increases.

• Check GIS-based market tools available to developers of mini-grids that use renewables or hybrid systems. Please refer to the Carbon Trust report, “Evaluation of Methodologies and Best Practices Available for Assessing GMG Potential”, which was commissioned by the Bank as part of the Bank Program.

• Check country information services. Tanzania, for example,

has developed market-based information tools to encourage developers to invest in the country. These include information on the national grid system (both existing and lines under construction), and a national electrification plan. There are also websites showing the electrification status of every single village in the country (http://www.gimsys.net/irep/SIG/th_Reseau/default.asp) and socio-economic data on the regions (http://tanzania.opendataforafrica.org/).

1The five-step approach is based on INENSUS’ experience as a mini-grid developer and on GIZ-EUEI-PDF (2011), “Productive Use of Energy (PRODUSE): A Manual for Electrification Practitioners.”

22 GMG MDP Document Series: n°1

3.4.2 Lack of market inkage with communities

It is important for mini-grid developers to take time to understand the needs and priorities of communities and make sure that their projects have broad local support. This is particularly important for the smaller Type 3 projects, where the public sector is likely to have limited involvement in day-to-day project management. In some cases, developers will approach communities to set up mini-grids based on pre-selected criteria (e.g., distance from the national grid, population size, existing businesses and infrastructure). In other cases, communities will reach out to the developers to set up mini-grids in their area.

Developers need to weigh the cost of early and lengthy community engagement as part of their due diligence, against the risk of future trouble if they do not do engage sufficiently to ensure community buy-in. Renewable World spent around two years working with six communities before the company installed some of the first community-owned micro-grids in Kenya. Most developers, however, can only afford a few months of this early engagement and may want to outsource this work to local NGOs.

Consideration needs to be given to how the private developer communicates with the community on issues such as tariffs and system usage. An organisational structure that works in one community may not work in another. For example, in the Lake Victoria region in Kenya, a legally empowered community-based organisation may be the best vehicle for communication, but in other parts of the country, a cooperative or a respected community figure may be a better option.

Tips for developers

• Spend enough time on early community engagement.

• Help communities set up village power committees (or another appropriate governance structure) in order to have a clear point of contact for negotiations and local information campaigns.

3.4.3 Lack of market linkage with productive use customers

As discussed in sections 3.3.3 and 3.3.5, demand from small industry and businesses – the productive users of electricity – is one of the key success factors for Type 2 and 3 mini-grids. Without linkage to these users, mini-grids are unlikely to reach the critical level of sales necessary to cover their fixed costs. In addition to community engagement, linkages with productive users can be promoted through forums, information campaigns and other means.

3.5 Lack of capacity

The market for private investment in mini-grids is still relatively immature, and this is reflected in the lack of skills and experience of public institutions, developers, financial institutions, and local project staff. Technical assistance and capacity building are therefore critical if mini-grids are to be scaled up.

Public institutions often do not have the capacity to efficiently manage and regulate the development and operation of mini-grids. Many are budget constrained and lack the human resources to execute laws and regulations. A lack of coordination among public agencies can cause project delays.

Many developers have limited experience with the complexities of mini-grids. Some have no prior business experience, while others have experience only with larger power projects or in different sectors. There is also a lack of skilled labour to manage and operate the mini-grids. Well-trained and certified electrical engineers and technicians are often in short supply, and experienced local project managers and developers are expensive and hard to find.

Tips for developers

• Develop in-house training programs for local employees, avoid being overly dependent on a single employee for key activities, and invest in retention of skilled staff.

3.6 Access to finance

Access to finance is a big hurdle for mini-grids. There are a number of challenges:

• Lack of capital – Problems include the high administrative burden and inflexibility of grants, the limited risk tolerance of commercial investors, the small ticket size of transactions, and the lack of capacity of financing institutions and developers

• Foreign exchange risk – Local currency loans with attractive terms are often not available.

• PPAs – These are prone to delays and may not be bankable.

3.6.1 Lack of right capital

Mini-grids are financed through a combination of grants and subsidies, commercial equity and loans. The choice of financial instrument and type of investor depends on the type of project (pilot or scalable model) and the stage of project development.

23GMG MDP Document Series: n°1

Project Finance Corporate Finance

Investment based on income projections for individual mini-grid or

group of mini-grids

Investment based on historical track record of developer and income

projections of developer’s mini-grid portfolio

Most suitable for Type 1 mini-grids with anchor clients that offer long-

term contracted revenue streamSuitable for Type 1, 2 and 3 mini-grids

Funds only to be used for project(s) specified in financing agreementMore freedom for developers over how they use funds across diffe-

rent projects

Project risks shared among investors Balance sheet impact on developer

Financing takes longer to execute Shorter time to execute financing

Complex contract structure / more due diligence Simpler / less due diligence

Higher up-front costs Lower up-front costs

Longer-term financing Shorter-term financing

Table 3: Differences between project and corporate finance

Source: Energy4Impact

Most mini-grids rely on grants and subsidies for at least 30 percent of investment costs. Grants are typically given for pilot projects, early stage development costs, capital investments and technical assistance. They come from a wide range of sources, including international development agencies, local government agencies, trusts and foundations, and individuals.

The transaction costs of applying for and managing grants are often high. Delays in disbursement are common, especially for grants managed by local government agencies (Some developers are still waiting for reimbursement of their connection costs from the REA-managed Tanzania Energy Development and Access Project, TEDAP, originally a World Bank-supported rural electrification program which is now closed.) Many grants are too prescriptive and inflexible for mini-grid developers, whose needs can change due to unforeseen problems or delays.

Most mini-grid developers raise corporate capital from equity investors to build pilot projects and develop their business models. There are different types of equity investors, ranging from angel investors and venture capitalists (early stage seed capital), to private equity and family offices (expansion capital),

to impact investors (who look for a social and financial return and may invest at any stage). DFIs also invest equity, either directly or through third party funds – they look for development impact and some evidence of potential commercial viability. Most of these investors, with the exception of the impact investors and DFIs, require relatively high returns (equity IRR above 20 percent). This is considerably higher than what most of the Type 2 or 3 mini-grids can offer (equity IRR of 12-18 percent).

Many private investors are put off by the lack of proven scalable business models in mini-grids, the low risk-adjusted returns, and the lack of successful exits. However, the arrival of strategic players suggests the sector is getting more mature. Powerhive, whose original funders include the US company First Solar, recently raised US$20 million in series A financing to continue its growth in Kenya and expand internationally. Caterpillar, Total and a number of financial investors joined the funding round. Powerhive has also signed a US$12 million agreement with the Italian energy giant ENEL, under which ENEL will fund 93 percent of the costs of the roll-out of Powerhive’s mini-grids in Kenya. Caterpillar has acquired a significant stake in Fluidic Energy, an energy storage

Mini-grids may be financed at the corporate or project level. Corporate finance is an option for all types of mini-grids, including the smaller Type 2 and 3 projects. The main advantage of corporate finance over project finance is that it is likely to be quicker and cheaper to execute. Investors are able spread their risk across all of a developer’s projects that meet predefined criteria (e.g., technology type, offtake arrangements, location), while a developer will not have to incur the costs of licensing and seeking funding for each individual project. Project finance may be an option for the larger Type 1 mini-grids or for groups of smaller grids that

have anchor clients that offer long-term contracted revenue streams.

However, most mini-grids do not have sufficiently predictable cash-flows for project finance and their ticket sizes are too small to justify the high up-front costs of structuring and due diligence. A project finance loan below US$20 million may be difficult to justify because of these high fixed costs, although some DFIs consider project loans of US$5-10 million). Table 3 summarises the main differences between corporate and project finance.

24 GMG MDP Document Series: n°1

technology company that also develops mini-grids. RP Global, an Austrian developer of utility-scale power plants, recently bought a significant stake in Jumeme, a Tanzanian mini-grid project company. Other strategic investors in mini-grids include EON of Germany, Engie of France and InfraCo Africa, a DFI.

Most mini-grid projects are still not ready for commercial loans, which are important for scaling up the sector. Commercial banks are risk averse and are reluctant to lend to mini-grids until the business model is proven and the main project risks are mitigated (cost-reflective tariffs, guarantees in the advent of main grid connection, significant foreign exchange fluctuations, etc.). Local banks have limited experience with energy projects and require significant collateral for corporate lending. International lenders are concerned about foreign exchange risk and are put off by the small ticket size. Further, developers are not familiar with commercial lenders and not aware of the needs of different lender types and how to approach them.