guide to-procurement-of-new-peaking-capacity-energy-storage-or-combustion-turbines...

TRANSCRIPT

GUIDE TO PROCUREMENT OF FLEXIBLE PEAKING CAPACITY:

ENERGY STORAGE OR COMBUSTION TURBINES?

CHE T LY ON S , EN ER GY S TR A TEG IE S GR OU Pi

OVERVIEW

Coal-fired power plants have been a cheap and reliable source of generation for many

decades. The impact of low cost natural gas, the EPA’s Mercury and Air Toxics Standards

(MATS) and proposed CO2 regulations, and increasing pressure from renewable portfolio

standards – will result in the retirement of 25 percent of U.S. coal-fired generation

before the end of this decade.ii Substitute peaking capacity will be needed to replace

those missing coal-fired power plants. Most of that capacity can be provided by storage.

When generator retirements, new loads, or increasing population call for more peaking

capacity, utility planners often call upon a workhorse utility asset: the simple cycle gas-

fired combustion turbine (CT). Simple cycle CTs are so successful and well accepted that

Public Utility Commissions rarely question a utility’s choice of the venerable CT as a

preferred peaker solution. But times and technologies change, and the power grid’s long

love affair with gas-fired CTs is being challenged by advanced energy storage.

Even as retirement of coal plants accelerates,iii rapid addition of variable renewable

generation is creating the need for far more flexibleiv grid balancing resources. These

trends are forcing utility planners to think harder about the best way to replace and

augment regional peaking capacity. Advanced energy storage is a new and highly

flexible resource that utility planners should now include in their cost-benefit analyses.

The central point of this white paper is concisely expressed by S&C Electric, a respected

integrator and technology provider to the utility and power industry: “With a fleet of

“DES” [Distributed Energy Storage] units supplying stored energy for several hours,

more-expensive ‘peaking generation’ plants may no longer be necessary.”v The author

explores the merits of energy storage versus simple cycle CTs, and offers utility planners

and regulators factors to consider when evaluating whether to buy simple cycle CTs or

energy storage to meet shorter-duration peaking capacity requirements.

A key premise of this white paper is that in areas of the US with vertical markets, energy

storage can be located at utility substations and owned, aggregated and controlled by

utilities to provide significantly more flexible and valuable peaking capacity while also

mitigating stability problems due to solar PV. By providing energy balancing services at

both a regional (transmission) and local (distribution) level with the same storage asset,

the locational value and capacity utilization of storage can be much higher compared to

CTs interconnected at transmission voltage and operated as a central station resource.

Energy Strategies Group Page 2

A major finding is that by 2017, the Capex for a 4-hour storage-based peaker is

projected to be $1,390 per kW installed. When added benefits that accrue from locating

storage on the distribution grid are considered, storage will be roughly competitive with

many conventional simple cycle CTs in 2017 assuming mid-to higher range CT costs. For

CTs at the higher end of the CT cost range, 4-hour storage will be a clear winner.

By 2018 the CapEx of ViZn Energy’s 4-hour flow battery storage solution, which we use

as a proxy for the lowest cost flow battery technologies now being commercialized, is

projected to be essentially the same as that of a conventional simple cycle CT. Given the

added economic benefits of installing storage in distribution, storage will be a disruptive

winner against CTs even assuming a mid-range cost for a simple cycle gas-fired CT.

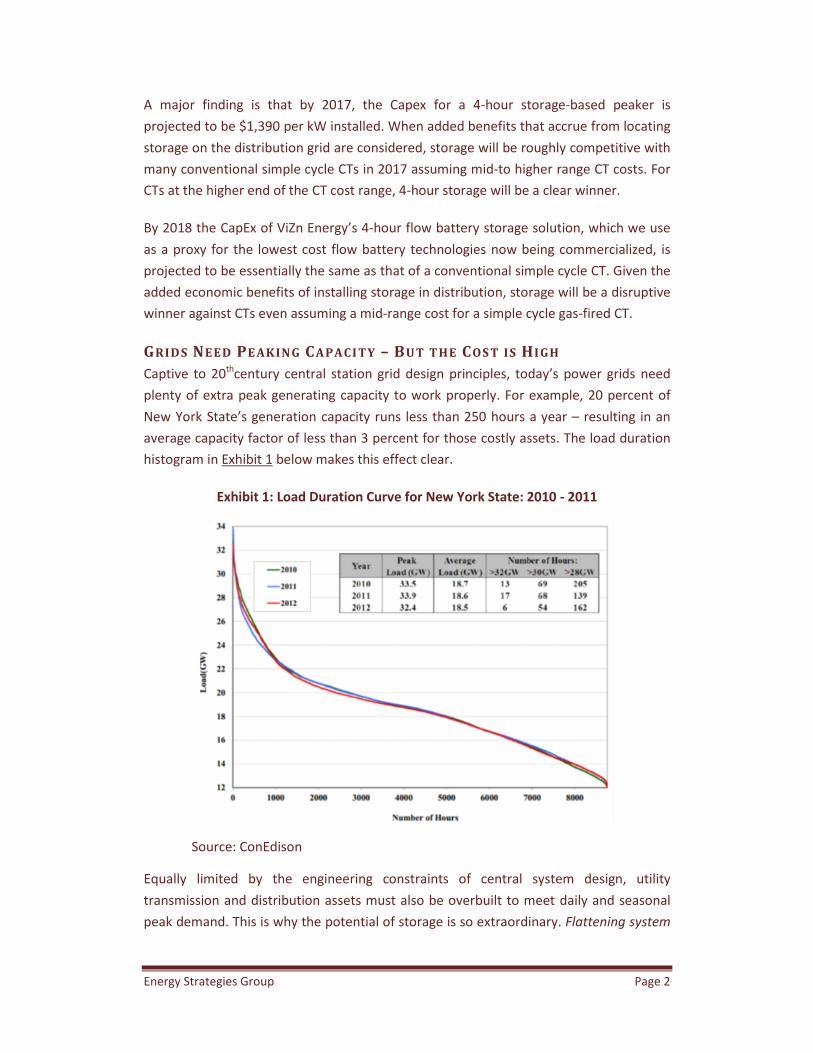

GRIDS NEED PE AKIN G CAPACI TY – BUT THE COS T IS HI GH

Captive to 20thcentury central station grid design principles, today’s power grids need

plenty of extra peak generating capacity to work properly. For example, 20 percent of

New York State’s generation capacity runs less than 250 hours a year – resulting in an

average capacity factor of less than 3 percent for those costly assets. The load duration

histogram in Exhibit 1 below makes this effect clear.

Exhibit 1: Load Duration Curve for New York State: 2010 - 2011

Source: ConEdison

Equally limited by the engineering constraints of central system design, utility

transmission and distribution assets must also be overbuilt to meet daily and seasonal

peak demand. This is why the potential of storage is so extraordinary. Flattening system

Energy Strategies Group Page 3

load with energy storage synergistically reduces the need for all major categories of

utility asset investment, including generation, transmission and distribution.

The value of storage is hardly fresh news to utility planners. Pumped hydro has been a

highly prized utility asset for about half a century. As shown in Exhibit 2 below,

gigawatts of pumped hydro were built in parallel with the build-out of U.S. nuclear

capacity. Storage allows nuclear plants to run as base load resources. With increasing

penetration of a new type of generation – variable renewable solar and wind, adoption

of a new type of energy storage seems not only technically logical but historically

consistent with the paired utilization of nuclear power generation and pumped hydro.

Exhibit 2: Growth of Nuclear Energy and Pumped Hydro: 1960 - 2008

Source: U.S. Energy Information Agency

While pumped storage is understood and accepted, until recently utility executives

dismissed advanced storage as too expensive and technically immature. However, the

cost-performance of battery storage has improved significantly in the last few years. So

too has our understanding of its multiple value streams and locational benefits and our

ability to model and quantify them. Reflecting this progress, and in response to the

growing impacts of variable DG, utility executives are taking a more bullish position on

the practical role they expect energy storage to play in future utility operations.

In its latest survey of the industry, 2014 Strategic Directions: U.S. Electric Industry, over

two-thirds of executives surveyed by Black & Veatch said they believe energy storage

will be the most important single factor facilitating integration of variable wind and

solar resources.vi The second and third most important factors cited by utility executives

Energy Strategies Group Page 4

were “transmission system upgrades” and the addition of “new, flexible conventional

power plants.”

It is not surprising that storage, transmission and generation assets were cited in the top

three solutions for addressing integration challenges posed by renewables. They are

core utility assets, and one or two can almost always substitute for the other(s).

However, one reason for writing this white paper is that utility planners may not fully

appreciate the extent to which advanced storage technology can substitute for some

conventional flexible generation, specifically simple cycle CTs. We will explore this idea

further by first reviewing the important role of CTs as well as their virtues and vices.

HISTO RICAL ROLE OF COM BUS TIO N TURBIN E S – CT VI RTUES AND VICES

The simple cycle CT serves as a proxy or benchmark of choice for capacity resources in

the United States. Indeed, CTs have performance attributes that utilities around the

world know and love. In commercial use for many decades, CT’s are fairly simple

machines whose output characteristics, maintenance requirements and operating costs

are well known. In the historical sense of power reliability, CT’s are considered reliable.

CTs are less expensive compared to their usually more efficient combined cycle

combustion turbine (CCGT) cousins. They have shorter start up times and faster ramp

rates than CCGTs and so are more flexible. CTs can be easily procured from bankable

suppliers. CTs are not always easy to site due to restrictions on air emissions, and they

emit CO2 gas which is now under the scrutiny of the EPA. But the same is true for any

fossil fueled power plant. Exhibit 3 below captures the elegant simplicity of simple cycle

CTs, a feature that makes them nearly ubiquitous in power systems around the world.

Exhibit 3: Combustion Turbine Power Generation: Simple Cycle

Source: Wikipedia

Given their good points, CTs are often selected as the most cost-effective go-to solution

for adding peak power capacity. However, CTs also have their bad points. The capacity

factor of a simple cycle CT peaker is typically less than 10 percent per year, sometimes

less than 5 percent. This reflects their mission and single purpose nature. CT’s are a

proverbial one trick pony. CT’s are also partial to cooler temperatures.

Energy Strategies Group Page 5

As Exhibit 4 below shows, when ambient air temperature rises over approximately 35 F°

they become less efficient. This is generally unacceptable in hotter climates where

cooling loads from air conditioning comprise a large portion of the daily peak. However,

this efficiency loss can be offset by adding Turbine Inlet Air Cooling (TIAC) technologies

at added cost. Air pressure and humidity also impact CT performance.

Exhibit 4: CT Efficiency loss as a Function of Air Temperature

Source: Wikipedia

It’s a good thing that CTs don’t run much because they are thermally inefficient

compared to CCGTs. Most CT peakers range from 30 to 42 percent in efficiency.

With increasing focus on air emissions fossil resources CTs are also getting harder to site

in urban areas. Partial load operation, ramping and start/stops typical of CTs used as

peaking resources increase their emissions of CO2, NOX and SO2.vii Siting CTs outside of

urban areas where they are less likely to violate air resource restrictions is an imperfect

answer. Longer distances between generation and load increase line losses while any

congestion points further reduce the effectiveness of remotely sited generation.

THE NEED FO R MO RE FLEXI BLE CAPACI TY

The changing economics of power production from renewables, especially solar PV, are

driving the need for more flexible capacity. As shown in Exhibit 5 on the following page,

dramatic decreases in the cost of solar PV coupled with innovative financing

mechanisms are increasing the penetration of distributed solar PV at a historically

unprecedented rate.viii Solar PV is already starting to disrupt the traditional cost-of-

service utility business model. Utilities and regulators are looking for ways to adapt.

While solar PV reduces utility revenues based on margins from kilowatt hour energy

sales, energy storage offers a replacement for lost utility revenues. Owned and operated

by utilities, storage can be placed into the rate base and earn long-term low risk returns

on invested capital similar to that afforded utility investments in transmission assets.

Energy Strategies Group Page 6

Exhibit 5: U.S. PV Installation Forecast, 2010 – 2016E

Source: GTM Research, “US Solar Market Insight” Q2 2014 Executive Summary.

Solar resources also create technical impacts that must be mitigated by electric utilities,

including two-way power flows and instability on low voltage distribution circuits and

shortages of flexible ramping capacity across the system. Exhibit 6 below categorizes

these utility concerns from highest to lowest in order of importance.

Exhibit 6: Distribution Circuit Concerns Due to High-Penetration Solar PV

Source: NYISO December 2013 Workshop

Energy Strategies Group Page 7

As the amount of variable renewable resources increases, the grid needs peaking

resources that are more flexible and can better support integration of resources on a

distributed basis. The CPUC reports that negative impacts on grid stability due primarily

to solar PV have started to occur.

As early as 2015, the combined ramping capacity of California’s generation fleet may be

insufficient to maintain stability within desired limits. The California ISO says it needs

another 4,600 MWs of regional ramping capacity to safely integrate forecasted

renewables. The extent of California’s ramping challenge is visible in Exhibit 7 below.

Exhibit 7: California Duck Chart: Growing Need for Flexibility

Source: California ISO

Have Utilities Reached the End of “Peak Centralization”?

As has happened with solar PV, storage is in the early stage of what will prove to be a

disruptive decline in cost over the next 3 to 5 years. This will allow solar PV plus storage

to replace conventional generation, transmission and distribution assets on a large

scale. It will also turn the centralized power grid model inside out.

Rocky Mountain Institute (RMI) recently posed a thought provoking question: “Has the

electric utility industry already reached “peak centralization?”ix RMI is loved by some

and reviled by others for the audacity of such questions. However, based on industry

trends – it is an entirely legitimate question.

Utilities like Duke Energy are repositioning by buying solar businesses to operate on an

unregulated basis. Other utilities like Arizona Public Power are preparing for a possible

S

o

u

r

c

e

:

C

a

l

i

f

o

r

n

i

a

I

S

O

Energy Strategies Group Page 8

180 degree turn in business strategy by proposing to state regulators they be allowed to

own, operate, and earn regulated returns on solar PV located on customer premises.

Storage will simply join the new mix of utility assets. In fact, as this paper was nearing

completion the Arizona PUC and other stakeholders agreed that storage must now be

considered as a companion or a replacement for at least 10 percent of Arizona’s

planned capacity of simple cycle gas peaking plants.

Flexibility of Simple Cycle CTs Versus Energy Storage

While CTs can start and ramp a faster than CCGTs, they are snails compared to energy

storage systems. Their limited speed makes them less suitable for a new mission

becoming critical to the grid: stabilizing distribution circuits negatively impacted by high

penetration solar PV. Even assuming a CT is operating at 100% rated output, the

operating range of storage is typically 2 to 4 times the operating range of a CT. Exhibit 8

below illustrates why this is so.

Exhibit 8: Flexibility of Energy Storage Versus a Gas Peaker

Source: Centralized Capacity Markets in Regional Transmission Organizations and Independent System Operators, Docket No. AD13-7-000, Page 5.

Storage can also switch from charging to discharging in less than 1 second. In

combination with up to a 20 times greater capacity use factor, storage is significantly

more flexible than simple cycle CT peakers.

With the availability of new energy storage technologies, in particular flow batteries,x

utilities have the means to economically meet the increasing need for flexible peaking

Energy Strategies Group Page 9

capacity using 2 to 6 hours of storage. The economics of storage deployed on a central

and distributed basis are explored in the next section.

ECON OMI CS OF CEN TRAL STATI ON AN D DIS TRI BUTED ENERGY STO RAGE

Multiple Value Streams of Energy Storage

Storage can provide a variety of valuable balancing services to the grid. Exhibit 9

illustrates how multiple energy services provided by the same storage asset have the

technical potential to be “stacked” to achieve a positive benefit-cost relationship. While

the chart indicates that the simple sum of all the stacked benefits is greater than the

cost of storage, simultaneously monetizing all these benefits in practice is hard to do.

Exhibit 9: Benefit Stacking as a Simple Sum

Source: Cost-Effectiveness of Energy Storage in California, Application of the EPRI Energy Storage Valuation Tool to Inform the California Public Utility Commission Proceeding R. 10-12-007, EPRI report # 3002001162

Some energy services that storage provides may conflict with one another at least part

of the time. And about half the population of the U.S. is served by utilities that are only

allowed to own one or two of the three basic types of utility assets, but not all three.

Divided ownership of generation, transmission and distribution assets makes it difficult

or impossible to channel all benefits and costs to the storage owner/operator. Analysis

of the economics of storage must take these constraints into consideration.

EPRI Analysis of California’s Use Cases for Storage

California is a leader in efforts to understand how to best apply storage in support of

renewable energy objectives while delivering reliable power on an economic basis. The

California Public Utilities Commission (CPUC) has defined Use Cases for storage and

tasked the Electric Power Research Institute (EPRI) to analyze the economics of those

Energy Strategies Group Page 10

Use Cases. EPRI developed the Energy Storage Valuation Toolxi (ESVT) with Energy and

Environmental Economics (E3) to evaluate the cost-effectiveness of storage in the

California energy market. EPRI’s ESVT modeling tool was used to produce the benefit-

cost analysis shown below for both central station energy storage and distributed

storage for new peaking capacity.

Central Station Energy Storage as a Peaking Resource

Exhibit 10 below provides key assumptions and analysis results for a hypothetical 50

MW, 4-hour Flow Battery applied on a central station basis as a peaking resource using

market conditions projected to occur in California in 2015. EPRI’s analysis found that a

positive benefit-cost ratio can be achieved. Capex breakeven cost for storage was

$2,657 per KW, translating to $664 per kWh of installed storage capacity. Any cost for

storage below that $2,657 breakeven value would yield a positive benefit-cost ratio.

The analysis excluded any additional incentive payments that storage might potentially

receive in the future for its superior flexibility and air emissions characteristics

compared to fossil-based CT peakers.

Exhibit 10: Central Station Energy Storage for Peaking Capacity

Key Assumptions:

• Year = 2015 • California Market • 50 MW, 4 hr battery • Energy and Ancillary Services

prices escalated 3%/yr (CAISO 2011 base yr)

• CapEx = $1,772 / KW • No battery replacements • 11.5% discount rate • 75% round trip efficiency

Key Findings

• Breakeven cost = $2,657 / KW; $664 / kWh

Source: Electric Power Research Institute (EPRI)

Distributed Energy Storage as a Peaking Resource

For its distributed storage Use Case, EPRI and the CPUC identified the following values

that storage can deliver at the substation level:

Electric Supply Capacity (a.k.a. “peak power substitution”)

Electric Energy Time Shift

Energy Strategies Group Page 11

Frequency Regulation

Spinning Reserve

Non-Spinning Reserve

Distribution Upgrade Deferral

In EPRI’s analysis, a first and second priority control scheme was assumed to assess the

economics of performing regional and local energy balancing functions with the same

distributed storage asset:

First priority:

Peak shave annual peak distribution load to offset load growth and defer

upgrade investment

Second priority:

Reserve Top 20 CAISO load hours per month for providing (peaking) energy, and

Co-optimize for profitability between energy and ancillary services

Exhibit 11 on the following page provides key assumptions and analysis results for a

hypothetical 1 MW, 4-hour Flow Battery applied on a distributed to provide energy

services at the local distribution circuit level and also the regional transmission level

peaking resource. As with the example above, market conditions projected to occur in

California in 2015 were assumed.

EPRI’s analysis found that a positive benefit-cost ratio can be achieved. Capex breakeven

cost for storage was $3,100 per KW, translating to $775 per kWh of installed capacity.

Analysis showed that any cost for energy storage below that $4,000 per kW (translating

to $1,000 per kWh installed capacity would yield a positive benefit-cost ratio.

The analysis excluded any additional incentive payments that storage might potentially

receive in the future for its superior flexibility and air emissions compared to fossil-

based CT peaker alternatives.

- This space intentionally blank -

Energy Strategies Group Page 12

Exhibit 11: Distributed Energy Storage for Regional Peaking Capacity and Local

Distribution Circuit Upgrade Deferral and Stability Control

Key Assumptions: • Year = 2015 • California Market • 1 MW, 4 hr battery • Energy and Ancillary Services

prices escalated 3%/yr (CAISO 2011 base yr)

• $279/kW per year upgrade deferral cost

• 2% load growth rate • CapEx = $3100/kW, $775/kWh • No battery replacements • 11.5% discount rate • 75% round trip efficiency • 17 year asset life

Key Findings

• Breakeven cost = $4,000 / KW; $1,000 / kWh

Source: Electric Power Research Institute (EPRI)

Distributed Storage has Higher Value than Central Station Storage

Compared to the central station storage Use Case, the Use Case for storage located at a

utility substation on the distribution grid adds distribution upgrade deferral and circuit

stability control. This results in an extra benefit of $279/kW per year for 17 years.

Further comparing the two Use Cases in Exhibits 10 and 11 above, we see that

breakeven costs for central station storage are $2,657 per KW and $664 per kWh, while

breakeven costs for distributed storage are $4,000 per KW and $1,000 per kWh.

Distributed storage has a much higher value than central station storage. That tells us

where storage should be located to maximize benefits.

The modularity of storage and its low environmental impact are also ideally suited to

incremental deployment over time. These advantages were not specifically captured in

EPRI’s benefit-cost analysis, but they can be significant. Instead of building one larger

resource that may initially be underutilized, multiple smaller resources can be added

incrementally. Grid dynamics often change over time, and phased deployment of

storage allows its locational benefits to be maximized by selecting the highest value

locations based on the grid dynamics occurring in that point in time. Simply deferring

capacity investments, regardless of type, lowers capital investment risks and improves

total return on assets.

Energy Strategies Group Page 13

The modular architecture of energy storage also improves asset reliability and system

resiliency through redundancy. In generation nomenclature, “shaft risk” is a capacity

resource’s probabilistic contribution to loss of load in the event of failure. The shaft risk

of a single large piece of equipment is much higher compared to capacity comprised of

multiple smaller units operating in parallel.

For example, both AES Energy Storage and Beacon Power have reported operational

availability of over 99 percent for their respective 20 MW storage assets performing

frequency regulation. In contrast, the availability of factor for a new 50 MW central

station gas-fired peaker CT is approximately 92% percent based on total annual start-up

and shut down time typical for a gas-fired CT used as a peaker.

But these comparisons still haven’t directly answered our basic question: which is better

as a peaking resource, energy storage (whether central station or distributed) or simple

cycle combustion turbines?

WHI CH IS MO RE COS T-EFFECTIVE AS A PE AKI NG ASSE T: STO RAGE O R CTS?

When we compare the cost-effectiveness of simple cycle CTs with energy storage, initial

Capex doesn’t tell the whole story. The benefits side of the cost-benefit equation must

also be taken into account. Locating storage on the distribution grid captures additional

value from distribution upgrade deferral and circuit stability control. Nevertheless, to

keep things simple and conservative, let us use initial CapEx cost as a starting point.

Simple Cycle Combustion Turbine Cost

There are two basic types of CTs: conventional and advanced. Conventional CT’s are

smaller. A typical size for a conventional CT is 85 MW based on a GE 7 EA frame. Cost

data published by the EIA shows a conventional CT installed in 2012 at $973 per kW of

capacity, excluding sales tax.

A typical size for an advanced CT is 250 MW. Economy of scale factors drive down cost

from $973/kW for a conventional CT to $676/kW for the advanced version. In addition,

combustors in an advanced CT fire at much higher temperature, resulting in a big

improvement in efficiency with heat rates dropping from 10,850 to 9750 BTU/kWh.

Fixed operating cost is also lower for the advanced CT because the staff required is

about the same as for a conventional CT.

The large cost difference between conventional and advanced CTs beg the question:

why buy a conventional CT? The answer is simple: utilities don’t buy more than they

need unless they can share the output of a larger generator. But that option is not

always convenient or even possible.

Also note that there is a big variance in cost depending on where a CT is being installed.

In California, for example, a 100 MW simple gas-fired combustion turbine peaker

Energy Strategies Group Page 14

installed two years ago had a cost of about $1,230/kW.xii This cost is on the extreme

high end of the cost range for simple cycle peakers which can be installed for as little as

$670 per kW. But in urban areas with locational constraints, higher cost of labor, etc.,

costs can be more than twice as much as the lowest end of the CT cost range.

Let’s compare the cost of storage to a conventional (small) peaker, not a larger

advanced CT. Our rationale is simple; simple cycle peakers are installed every year. And

while the cost can be higher or lower depending on location constraints, let’s use $973

per kW capacity because it is on the high side for installed cost for simple cycle peakers,

and storage will succeed in making inroads at that price point first.

On the storage side of things end-use pricing data is more difficult to obtain. However,

projected customer pricing was obtained for a 1 MW / 4-hour solution from ViZn Energy

for its zinc/iron redox flow battery, as shown in Exhibit 12 below. We will use this data

as a proxy for other low cost energy storage technologies now being commercialized.

Exhibit 12: Projected Costs (Price) for a 1 MW, 4-hr Redox Flow Battery

Year Power Energy $/kW $/kWh

2016 $2,194 $549

2017 $1,390 $348

2018 $974 $244

Source: ViZn Energy

As the table above above shows, by 2016 ViZn Energy’s flow battery is still slightly more

than twice the initial cost of a conventional simple cycle CT. The added benefits from

installing storage in distribution would not make up the cost gap. However, in some

situations the cost of a simple cycle peaker will be higher than our mid-cost assumption

for CTs. And some peaking power substitutions will require less than 4 hours of storage.

For example, many municipal and cooperative utilities pay their wholesale generator

suppliers based on tariffs that include demand charges. These demand charges are

similar to what commercial, industrial and residential end-user customers pay in some

parts of the Country. Depending on the shape of the load of a municipal or cooperative

utility, it may be possible to use a less costly 2 or 3 hour storage solution. To summarize

our 2016 comparison, it will require a high degree of selectivity, but storage economics

can be better than some conventional CTs even at 2016 projected storage costs.

By 2017 Capex for a 4-hour storage peaker from ViZn Energy is projected to be $1,390.

With added benefits from locating storage on the distribution grid, in 2017 storage will

be roughly competitive with many CTs conventional assuming mid-range CT costs. For

CTs at the high end of the cost range, 4-hour storage will win.

Energy Strategies Group Page 15

By 2018 the cost of ViZn Energy’s 4-hour storage solution in is essentially identical to

that of a conventional simple cycle peaker. Given the added benefits of installing

storage in distribution, by 2018 storage is a clear winner compared to a typical mid-

range cost for a conventional simple cycle CT.

BARRIE RS TO THE USE OF STO RAGE FO R PEAK PO WER SUBS TITUTI ON

Regulatory Environment

Utilities in regulated markets that own distribution assets (“wires”) are usually

constrained from owning and operating generation assets. Consequently, if storage is

locally classified as a generation asset distribution utilities may be precluded from

owning and operating distributed storage.

Policy trends appear to be headed in a direction that will allow distribution utilities to

eventually own and operate storage assets, but rules and regulations will need to be re-

worked or clarified on a state by state basis since distribution utilities do not fall under

national FERC jurisdiction.

In markets with vertical utilities that own generation, transmission and distribution

there are fewer and probably no fatal barriers to ownership and application of

distributed storage assets as described in this paper. That means that the multiple

values identified in the benefit-cost analysis done by EPRI could actually accrue to the

distribution utility owner. Slightly less than half of the population of the United States

lives in areas served by vertical utilities, so from a storage manufacturer’s point of view

the immediate market opportunity for utility-owned distributed storage is sizable.

Storage can also be interconnected at transmission level and operated on a central

station-only basis. In that case the value is less because stability services are not being

provided to local distribution circuits. However, the benefit-cost analysis done by EPRI

shows that even central station storage used for short duration peaking in the 2 to 4-

hour range can have a positive benefit-cost ratio in the California market.

In special cases storage used as a central station peaking resource may be especially

compelling. For example, in some urban areas ancient coal-fired peakers serve essential

double duty by helping to balance voltage and reactive power in a transmission

constrained load pocket. Many of these decades old coal plants are being forced to

retire due to tougher emissions standards and age. Replacing them with thermal gas-

fired peakers can be impractical due to environmental, political or other local

constraints. In such cases the substitution value of energy storage can be quite strong.

An example that illustrates the above scenario is Long Island Power Authority (LIPA). In

late 2013 LIPA issued an RFP for new generation and demand resources and specifically

included options for up to several hundred megawatts of energy storage. LIPA is the first

Energy Strategies Group Page 16

utility in the United States to attempt to procure long-duration energy storage for

purely market-based reasons. LIPA’s precedent setting RFP is a clear indication of the

perceived commercial potential of energy storage for peak power capacity.

Capacity Payments in Selected Markets

Grid operators must maintain enough capacity to meet forecasted peak daily loads, plus

a reserve margin mandated by NERC for operational safety. In most electricity markets

in the U.S. and many overseas, politicians support some form of price caps on electricity

to keep customers from getting exposed to overly high prices during periods of

maximum electricity demand. Markets with price caps are called “capacity markets” and

include PJM Interconnection, New York ISO and ISO New England.

In capacity markets generators lose money due to price caps, so markets those provide

“capacity payments” to generators that give them money for being available to respond

to demand. But this fix has a flaw. The ratio of annual peak-hour electric demand to

average hourly demand has risen across the US for the last 20 years. For example, in

New England, the highest peak-hour electric demand for 1993 was 52% above the

hourly average level, while in 2012 peak-hour demand rose to 78% above the hourly xiii average level. This increasing peak-hour electric demand ratio means generators are

producing less and less energy. Because energy payments are a generator's primary

source of revenue, the rising ratio of peak-to-average hourly demand is cutting deeper

into generator revenues. According to many stakeholders, this increases the need for

larger capacity payments.

Like generators, storage assets entering capacity markets will need to make sure

capacity payments are high enough (and predictable enough) to justify an investment in

peaking capacity. At present, capacity markets and their payments are unreliable.

Exhibit 13 on the following page illustrates this point.

- This space intentionally blank -

Energy Strategies Group Page 17

Exhibit 13: Historical Price Volatility in Capacity Markets

Source: Centralized Capacity Market Design Elements, FERC Commission Staff

Report AD13-7-000, August 23, 2013

A FERC proceeding is currently underway to try and improve how capacity markets

work. The Energy Storage Association and other stakeholders are engaged in this

proceeding to try and get storage qualified as a capacity resource in capacity markets xiv (PJM, ISO-NE, and NYISO). This will mean developing rules specific to energy storage

resources as was done for frequency regulation ancillary services via FERC Orders 755

and 784. The capacity proceeding should be monitored closely as the outcome will

impact the economics of investing in peaking capacity regardless of the technology used

– whether CTs, Energy Efficiency (EE), Demand Response (DR), or energy storage.

In contrast to markets that utilize capacity payments, Texas allows wholesale electricity

prices to rise to far higher levels based on the theory that if prices are high enough,

investment in new capacity will increase. In turn, greater supply will modulate prices

through increased competition. If market-based prices get high enough storage might

also make economic sense as a peaking asset in Texas and other energy-only markets.xv

Energy Strategies Group Page 18

SUMM ARY AND CON CL USIONS

Lower cost solar PV and its rising penetration in all market segments will have a

profoundly disruptive effect on utility operations and the utility cost-of-service business

model. This has already started to happen. Storage offers a way for utilities to replace

lost revenues premised on margins from kilowatt hour energy sales by placing storage

assets into the rate based and earning low-risk long-term regulated returns on capital.

Because solar PV is highly distributed, simply overlaying storage on a central station

basis won’t maximize grid performance or cost reduction. Storage enables more PV

while mitigating stability problems at the distribution circuit level. Availability of cost

effective and technically proven distributed storage will further accelerate the shift

toward distributed power grid architecture. The central station approach utilities have

used to meet peak power requirements is on the verge of a paradigm shift. Central

station topologies will give way to distributed grid architecture.

The effective range of storage is 2 to 4 times the effective range of a CT based on

nominal capacity. Storage can also switch from charging to discharging in less than 1

second. In combination with up to 20 times greater capacity utilization factor, storage is

significantly more flexible than simple cycle peakers. This flexibility allows distributed

storage to capture multiple value streams with the same peaking asset.

In contrast to simple cycle CTs, storage can easily be applied on a distributed basis.

Aggregated and controlled as a fleet, multiple units of distributed storage can deliver

regional peaking capacity and ancillary services (i.e., frequency regulation, spinning

reserve), distribution circuit stability (i.e., voltage and VAR control, peak power

augmentation), and distribution circuit upgrade deferral.

As occurred with solar PV, costs for energy storage are about to undergo a steep decline

over the next 2 to 3 years. This will disrupt the economic rationale for gas-fired simple

cycle peakers in favor of advanced energy storage.

By 2016, storage economics for flow batteries may be better than some conventional

CTs. But selectivity will be required to find situations where the location-driven cost of

CTs is higher than the national average, and where the shape of the utility load curve

will allow 2 to 3 hour storage solutions to suffice versus a more costly 4 hour solution.

By 2017 Capex for a 4-hour storage peaker is projected to be $1,390. With added

benefits from locating storage on the distribution grid, in 2017 storage will be roughly

competitive with many CTs conventional assuming mid to higher range CT costs. For CTs

at the high end of the cost range, 4-hour storage will be a clear win.

By 2018 the cost of ViZn Energy’s 4-hour storage solution is essentially identical to that

of a conventional simple cycle peaker. Given the added benefits of installing storage in

Energy Strategies Group Page 19

distribution, by 2018 storage will be a winner compared to a typical mid-range cost for a

conventional simple cycle CT and generally disruptive for higher cost simple cycle CTs.

Given these findings, the cost-performance of energy storage should always be

evaluated against CTs for provision of new peaking capacity as a matter of standard

procurement policies. The beginning of what will become a regulatory trend in that

direction is underway in Arizona. In October 2014, the Arizona PUC and other

stakeholders agreed that storage must be considered as a companion or a replacement

for at least 10 percent of Arizona’s planned capacity of simple cycle gas peaking plants.

In summary, the combined impact of low cost distributed solar PV and low cost storage

will both force and allow adoption of decentralized grid architecture. When adding

peaking capacity today, utility planners can choose between assets that better fit the

emerging distributed grid architecture or the old and disappearing centralized approach

to grid design. The choices we make today should be consistent with current and long-

term cost-performance trends in fossil-based generation, solar PV and energy storage.

i Chet Lyons is a Principal at Energy Strategies Group, a Boston-based consulting and project development firm that helps storage developers, manufacturers and investors establish a profitable role in the energy storage industry. A storage industry expert, he is the author of "Grid Scale Energy Storage Opportunities in North America: Applications, Technologies, Suppliers and Business Strategies,” published by Greentech Media. Contact Chet at: (978) 886-3609, [email protected]. Chet would like to acknowledge the generous support of his friend Dale Bradshaw who provided essential real world perspective. With TVA for 29 years as a senior manager of R&D for generation and transmission projects, Dale is currently a Technical Liaison and Consultant for National Rural Electric Cooperative Association (NRECA). He is also a NRECA Cooperative Research Network (CRN) consultant on the value proposition of energy storage. Contact Dale at: (423) 304-9284, [email protected].

ii Source: AllianceBernstein, an energy asset management firm headquartered in New York City.

iii Per AllianceBernstein, the EPA’s Mercury and Air Toxics Standards (MATS) that comes into

effect in 2015 will drive almost immediate retirement of around 50 GW of coal fired capacity generating 180 million MWh annually. 29 states with RPS targets account for two-thirds U.S. total demand. Those states will require that another 165 million MWh of non-hydro renewable energy be placed into production by 2020.

iv “Flexibility” as a resource attribute allow system operators to respond to changing loads,

including the net effects of intermittent renewable generation. It can be provided by gas-fired generation, enhancement of existing resources, responsive loads, new or redefined ancillary services, operational rule changes and energy storage.

v “The Next Next Thing for Distribution Grids? - Distributed Energy Storage,” by Jesse Berst, Smart

Grid News, Jan 23, 2014. Quoting Mike Edmonds, S&C Electric, a leading innovator in integration of utility-scale energy storage.

vi 2014 Strategic Directions: U.S. Electric Industry, Black & Veatch, September, 2014.

Energy Strategies Group Page 20

vii

Impacts of Renewable Generation on Fossil Unit Cycling: Costs and Emissions, NREL, May 20, 2012.

viii For example, in PJM Interconnection, the largest competitive electricity market in the United

States, __ percent of all new generation that filed for an interconnection permit in [year] was either solar or wind.

ix Blog: Consumers at the Gate: Has energy reached “peak centralization?” by Jurriaan Ruys and

Michael Hogan; Rocky Mountain Institute, Sep. 10, 2014.

x In flow batteries, an electrolyte flows through an electrochemical cell to convert stored

chemical energy into electricity during discharge. The process is reversed during the charge cycle. Vanadium redox and zinc-bromine (Zn/Br) mixtures are common chemistries. The liquid electrolyte used for charge-discharge reactions is stored externally and pumped through the cell. This allows the energy capacity of the battery to be increased at a low incremental cost and to be optimally sized for the application. Energy and power are decoupled, since the energy content depends on the amount of electrolyte stored.

xi EPRI’s Energy Storage Valuation Tool (ESVT) was used to produce the benefit-cost analysis

shown in this white paper under the auspices of a CPUC sponsored project. Results were presented by EPRI and E3 (co-developer of the tool) at a CPUC Storage OIR Workshop (R.10-12-007) on 3-25-13. EPRI and E3’s presentation at the Workshop was entitled: “Investigation of Cost-Effectiveness Potential for Select CPUC Inputs and Storage Use Cases in 2015 and 2020.” A copy of EPRI and E3’s presentation is available at: http://www.cpuc.ca.gov/NR/rdonlyres/705DFEA1-9A22-4BFA-889B-A717CD5801C4/0/EPRI_Presentation.pdf.

The ESVT leverages 3 main categories of input data to simulate storage operation and assess cost-effectiveness results: 1) grid service technical requirements defined by electric system needs and benefit calculation inputs; 2) financial assumptions for the storage owner, including discount rate and tax assumptions; and 3) the cost, performance, size, and configuration of the storage system technology. The ESVT then takes user-provided inputs and simulates storage operation to meet all technical requirements of the grid service and maximize its remaining potential in the energy and ancillary service markets. Readers interested in learning more about EPRI’s modeling tool may wish to contact Ben Kaun or Stella Chen within EPRI’s Energy Storage Program.

xii Source: Energy and Environmental Economics (E3), “Distributed Resource Avoided Cost

Calculator.”

xiii Source: United States Energy Information Agency.

xiv FERC Docket No. AD13-7-000 - Centralized Capacity Markets in Regional Transmission

Organizations and Independent System Operators.

xv Texas has a less than adequate reserve margin and recently increased price caps on wholesale

electricity prices to $7,000 per MWh during peak demand. Texas plans raise its price caps again in June 2015, to $9,000 per MWh.

BIBLI OG RAPH Y

The following resources may be of interest to those want to learn more about storage as a substitute for peak power, ancillary services and distribution circuit stabilization:

1. Cost-Effectiveness of Energy Storage in California: Application of the Energy Storage Valuation

Tool to Inform the California Public Utility Commission Proceeding R. 10-12-007. EPRI, Palo Alto,

Energy Strategies Group Page 21

CA: 2013. 3002001162. http://www.cpuc.ca.gov/NR/rdonlyres/1110403D-85B2-4FDB-B927-

5F2EE9507FCA/0/Storage_CostEffectivenessReport_EPRI.pdf.

2. Utility Scale Energy Storage and the Need for Flexible Capacity Metrics; Eric Cutter, Ben Haley,

Jeremy Hargreaves, Jim Williams; Energy and Environmental Economics, +1 415-391-5100;

available at: https://ethree.com/documents/E3_APEN_Bulk_Storage_Web.pdf.

3. 2014 Strategic Directions: U.S. Electric Industry, Black & Veatch, September, 2014. This report

examines the accelerated pace of change affecting the U.S. electric utility industry with a focus

on the market, technology, and regulatory drivers of change. Key issues are analyzed, including

reliability, emerging technologies, renewables integration and infrastructure development. The

report examines industry prospects. Free copy available here: http://bv.com/reports/electric.

4. What the Duck Curve Tells Us About Managing A Green Grid. CAISO. Available at:

http://www.caiso.com/Documents/FlexibleResourcesHelpRenewables_FastFacts.pdf.

5. Qualifying Capacity and Effective Flexible Capacity Calculation Methodologies for Energy Storage

and Supply-Side Demand Response Resources – Draft Staff Proposal, September 13, 2013.

Available at: http://www.cpuc.ca.gov/NR/rdonlyres/59531E27-5A74-4E47-8551-

0FBAB2DB6B0D/0/QCandEFCMethodologies_ESandSupplySideDR.PDF.

6. Distribution Energy Storage -Distributed Storage Peaker - CPUC Energy Storage Use Case Analysis.

Available at: http://www.cpuc.ca.gov/NR/rdonlyres/06E4C603-300A-4B77-85A7-

F0400DAB21A0/0/DistributedUseCasePeaker.pdf . Amanda Brown and Mark Hardin.