how retail banks and investment companies are using ... · combined with advanced analytics provide...

TRANSCRIPT

Location Intelligence in the Financial Industry Q3 2017 | Prox.Report: State Of The Proximity & Location Industry

How retail banks and investment companies are using proximity and location data

© Unacast 2017 1

About the Report 2 PSPi Hardware Companies 18

Message from the CEO & Co-founder 3 PSPi Software Companies 19

Executive Summary 4 Proximity Sensors Deployed Globally 20

How Investment Companies Leverage Location and Proximity Data 5 Beacon Standards: iBeacon vs Eddystone 21

How Retail Banks Optimize Costs and Drive Customer Loyalty 6 Proximity Technology and Software 22

Location Data and Technology in the Financial Industry: Use Cases 7 Proximity Products and Services 23

The State of Proximity 14 Industry Verticals 24

Proximity Solution Providers by Country 15 Categories of Proximity Solution Providers 25

Proximity Solution Provider index (PSPi) 17

TABLE OF CONTENTS

© Unacast 2017 2

ABOUT THE REPORT

PurposeEvery Prox.Report aims to provide a state-of-the-industry update while also educating the market about the ever-growing, evolving proximity industry. In addition to industry status, each report zeroes in on a specific theme, taking a deep dive into the area of focus and showcasing real-life use cases from the companies that have signed up to Proximity.Directory.

UseAll information in the report is free to use and share, as our main goal is to give insights to the industry and educate the market.

Want access to more?Interested in more details about the report? Please get in touch with us at [email protected]

About UnacastUnacast the leading location and proximity data platform, built the Real World Graph™ to understand how people and places are connected. Unacast data empowers the next generation of data-driven industries with unique and highly accurate data sets and insights, built on a foundation of double-deterministic™ proximity data.

© Unacast 2017 3

MESSAGE FROM THE CEO & CO-FOUNDER

THOMAS WALLECEO & Co-founder of Unacast

Customer expectations have shifted across many industries, and the financial services industry is noexception. To survive and thrive in the digital economy, retail banks should provide personalized, fast,and simple services to their clients. Location data and context allow commercial banks to improveefficiency, optimize locations and modify services offered within the branches. Banking apps,empowered by proximity technologies - such as beacons, geofences, and NFC tags - allow mobilepayments, accommodate communication with customers, and help develop loyalty.

Location and proximity data allows investment companies to make better decisions. We all rememberhow Foursquare predicted Chipotle’s financial performance in 2016 by analyzing foot traffic. This wasjust a beginning. As the world is increasingly sensored up, investment companies turn to the newsources of alternative data to get the most out of the market. In addition to foot traffic, alternative datasources include credit card transactions, data from IoT-equipped devices, asset tracking algorithms,agricultural sensors, and much more.

Retail banks and hedge funds are the pioneers of the financial industry, having already started mininglocation and proximity data. In this report, we explain how they benefit from it and touch on what thefuture holds.

Best,

Thomas

© Unacast 2017 4

EXECUTIVE SUMMARY

Location data and context allow commercial banks to improve efficiency,optimize locations of branches and ATMs, and modify services offeredwithin the branches.

Banking apps, empowered by proximity technologies - such as beacons,geofences, and NFC tags - accommodate mobile payments, facilitatecommunication with customers, and help develop loyalty.

Location and proximity data from smartphones, IoT connected devices, andsensors allows investment companies to differentiate their portfolios, avoidrisky trade, and maximize profits.

457 companies from 58 different countries are registered onProximity.Directory. North America and Europe are leading the game with77% of the total number of companies coming from there.

Matching location data on where consumers live, work, shop, andentertain with contextual information, such as card transactions anddemographic distribution, allows financial institutions make betterdecision.

As of Q3 2017 17,300,000 sensors are registered onProximity.Directory

Swirl remains an absolute leader among the software companies accordingto the Proximity Solution Provider index (PSPi). Kontakt.io is number onein the PSPi hardware category.

© Unacast 2017 5

INVESTMENT COMPANIES MAKE SMARTER DECISIONS LEVERAGING PROXIMITY AND LOCATION DATA

Investment companies identified the value of location data a long time ago. Untilrecently, they would send someone to the big box retailers to count cars in theparking lots and visitors coming in and out. Based on this information, investorsmade financial predictions for companies and industries. Location and proximitydata allow these companies to obtain similar information but with moresophistication and on a larger scale, which brings fortune telling on the stockmarket to the end.

Credit card transaction data is a widely used source for analyzing consumerbuying-behavior and forecasting company revenues. However, alone, it can bringconfusion and mispredictions because consumers who pay with cash arecompletely missed. In the US, cash is the most frequently form of payment ,accounting for 32% of the total transactions. Consumers use debit cards for 27 %of their transactions and credit cards for 21 % of transactions in 2015 (source).

A rapid growth in the number of smartphones, IoT connected devices, andproximity sensors has led to an explosion of alternative data sources that enrichinvestment models with new insights, often in real-time. Investors are now able tocreate new economic indicators for better decision-making by drawing variouscorrelations. Location and proximity data allow investment companies to createdifferentiated portfolios, avoid risky crowded trade, and maximize their short- andlong-term profits.

Identifies trends by providing insights on where consumers

shop, in which hotels stay, what restaurants visit, and more

Mobile Data

IoT Sensor Data Satellite DataMeasures supply and demand for

resources and services in real-time through beacons, Wi-Fi, geofences, and other sensors

deployed in smart cities, logistics, manufacturing, and agriculture

Image data from satellites allows, for example, to count the number of cars near the big box retailers

© Unacast 2017 6

RETAIL BANKS USE LOCATION AND PROXIMITY TECHNOLOGIESTO OPTIMIZE COSTS AND DRIVE CUSTOMER LOYALTY

Branch Optimization ATM Optimization Consumer Loyalty

Which locations to close? Where to locate newbranches? Which services to offer in-branch andhow to train bank employees? What sales targetsto set? Proximity and location data helps toanswer these questions by revealing volume offoot traffic and identifying under- and over-servedareas. Matching location data on where clientslive, work, shop, and entertain with contextualinformation, such as card transactions anddemographic distribution, allows banks to makebetter decision.

Too many ATMs at one location drive upoperational costs, while too few limit the ability toprovide adequate service to the customers.Strategic placement of ATMs is easy with locationand proximity data. It identifies the factors whichdetermine the use of ATMs in a certain area. Adaytime/nighttime population, a concentration ofhigh-income households, commercial buildings,competitive service providers are just some of themany factors that should be considered whenplacing ATMs.

Location and proximity technologies are a crucialpart of the strategy to win loyalty and gain marketshare. Consumers are likely to switch banks iftheir requirements are not met. They expectproducts tailored to their needs because they havemore options to choose from. Mobile technologiescombined with advanced analytics provide anopportunity to engage with consumers at the rightplace and at the right time.

Retail banks are facing several issues. First, low consumer interest rates lead to low margins. Second, technological shifts result in the declining number of in-branch transactions and rising digital and mobile self-services. Third, banking products are becoming commodities while consumer needs are getting more diverse. To stand out, banks need to personalize and differentiate their offerings. What is the solution? Location and proximity technologies.

On the one hand, location data allow banks to improve efficiencies, identify underserved markets, and maximize profitability. On the other hand, proximity technology facilitates engagement and enhances customer touch points, which develops loyalty and leads to increasing market share.

LOCATION TECHNOLOGY IN THE FINANCIAL IDUSTRY

© Unacast 2017 7

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 8

In May 2013, Danske Bank launched their mobile banking app for transferring money between individuals. This was followed in 2016 with theintroduction of a mobile wallet to MobilePay along with instore payment acceptance devices in store. To support this, Netclearance suppliedDanske Bank with the MobilePay terminal. As of today, more than 3.4 million Danes use the MobilePay app making it the number one applicationin Denmark, outpacing Facebook and Whatsapp. The MobilePay BLE terminal enables consumers to pay using the MobilePay mobile wallet app atthe checkout at many of the nation's retail outlets.

The MobilePay terminal improves the overall experience in general stores, which is often characterized with long queues and hustle. TheMobilePay app enables customers to pay quickly and as safely as payment by cash and credit cards. The solution does not require expensivetechnology or equipment that is expensive or difficult to access for customers and shops - and is intuitive to use and easy to understand.

How does it work?

• Customer opens the MobilePay app and enters their personal code

• Customer holds their mobile at the MobilePay terminal upon checkout or scanner QR code

• The customer receives the payment amount in his MobilePay app from the terminal

• The customer authorizes the payment on the app

The MobilePay terminal is connected to existing POS systems in the same way as conventional credit card terminals. If the customer hasMobilePay installed on their mobile phone, an integrated BLE beacon will activate the app only when it's time to pay. The customer isautomatically checked in and connected to the cash register when the phone is held within a range of approximately 10 cm from the MobilePayterminal. The payment can also be activated via a built-in NFC chip or by scanning the box QR code. The MobilePay terminal is a generic solutionthat supports all known protocols for mobile payment.

• 3.4 million app users of Mobile Pay, 9 out of 10 smartphones in Denmark have the app

• Over 30,000 MobilePayboxes deployed in Denmark in major stores, retailers and QSR’s

• $12bn US transacted through the MobilePaynetwork in the first year

DenmarkOBJECTIVE: To enable BLE mobile payments at Point of Sale from iOS and Android devices using the same payment terminal

DANSKE BANKUse case provided by NetClearance

Beacons

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 9

MyOrder App is owned and run by Rabobank, the largest bank in the Netherlands. It enables users to order and pay with their phone at over 14,500locations throughout the country — restaurants, bars, cinemas, carwashes, parking lots and more. According to research conducted by MyOrder, theservice their customers were least aware of was in-app parking payments. In order to educate their users and drive transactions, MyOrder decidedto implement the geofencing software of Plot Projects.

With Plot Projects, MyOrder was able to set up a location-based notifications campaign informing users about the diverse locations where they canpay for parking through the app. For this campaign, users were notified when entering new participating parking zones. This campaign took placeacross 25 cities in the Netherlands. The campaign was set up as follows: geofences were created around each city’s paid parking zone andnotifications were triggered as users entered those predefined zones, reminding them of the available payment service. For example, a user drivingto Amsterdam would receive a notification when entering the paid parking area: “Welcome to Amsterdam! Use MyOrder to pay for parking in thiscity.”

To assure the campaign was relevant and avoided spamming, MyOrder didn’t target users in their city of residence and limited the frequency ofnotifications to only once per paid parking zone. Practically, this means a user working in Amsterdam, and travelling there every day, wouldreceive the notification only once. No matter how often he then re-enters this area, no further communication will be triggered. The user would,however, be notified about parking payment services if he went on to drive to other participating areas. New geofences were added as the parkingpayment service expanded to new cities.

• 69% of users were notified about in-app parking payment

• 18% of users subsequently opened the location-based notifications

• 47% of these opens converted to mobile payments

GeofencingOBJECTIVE: Drive mobile payments for parking fees

RABOBANKUse case provided by Plot Projects

Netherlands

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 10

Citibank ran a pilot program with Gimbal to help solve some of the primary challenges that Citi was facing. These challenges included finding away to provide a more hyper-targeted mobile experience relevant to their customer’s time and place, the ability to offer a new and secure way toopen ATM doors, and the future capability of creating alerts for branches when VIP customers enter their banking centers.

Over 60,000 Citibank customers with the Citi Mobile app (which had the Gimbal SDK installed) opted-in to be a part of the pilot program. To helpsolve the challenge of a new and secure way to open ATM doors, Gimbal beacons were installed at select Citibank branch locations in NY, NJ, andCT for cardless ATM entry. Using Bluetooth technology, customers could enter the ATM lobbies after hours with their iPhones and Apple Watchesacting as digital “keys.” Upon approaching a branch, the customer’s device detected the presence of a beacon which would then trigger an alertasking if they would like to enter. When the customer selected “unlock,” the ATM lobby door would allow them to enter without swiping a card.

Along with beacon technology, Citi utilized Gimbal’s geofencing technology for Citi sponsored events such as the Today Show/Citi SummerConcert Series. Through Gimbal’s Manager software, Citi could pinpoint and draw custom polygonal geofences in order to message Citi app userswho were near Rockefeller Plaza and other Manhattan areas that were part of the Citi Concert Series. When users crossed these geofences, theywould receive a relevant message from Citi around the event.

• Location based updates on Citibank events and special offers such as the Citi Dining program and advanced giveaways

• Increased customer engagement and foot traffic to the Today Show and Concert Series

• An opportunity for Citi to listen and learn from their customers

CITIBANKUse case provided by Gimbal

United States

OBJECTIVE: To make the customer banking experience easier and more secure through innovative mobile technologies Geofencing Beacons

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 11

Türkiye İş Bankası is the one of largest banks in Turkey with 13 million customers and 1.350 branches. Banking industry is shifting toward mobile.Everyday more people are using mobile apps and mobile payments instead of physical cards. İş Bankası wanted to introduce better ways towithdraw cash using their mobile banking application ( İş Cep). They first introduced QR codes for this purpose. However, the users still needed tocapture the QR code and due to reflection on the screen, the process could not be completed in some cases. Moreover, the customers still need topress “9” on the ATM to generate QR code.

In order to solve this problem, Poi Labs developed a special USB BLE beacon. It is both powered and controlled by the ATM. When there is a cashwithdrawal request available nearby, the ATM controls the beacon and it broadcasts a unique signal. The customers do not need to touch the ATM;they only need to login İş Cep mobile app, select the amount and tab their device on the Bluetooth label available on the ATMs. The process iscompleted in seconds.

Currently customers can use this technology in 2.500 ATMs across Turkey, before the end of 2017 the system will be available in 5.000 + ATMs.

Cash withdrawal via Bluetooth is simple. First customers need to download the mobile banking app İşCep* and they can withdraw cash byfollowing the steps:

• Login İşCep and select “Withdraw Money”

• Select “With Bluetooth” option

• Chose the account and enter the amount desired

• Tap the phone to the bluetooth field

• Take the money

• Time required to withdraw cash is reduced by % 65

• The solution created a seamless customer experience

TurkeyOBJECTIVE: Reduce cash withdrawal process time with a unique and better experience

TÜRKIYE İŞ BANKASIUse case provided by Poi Labs

Beacons

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 12

Bank of America, which serves approximately 46 million consumer and small business relationships at 4,600 banking centers and 15,900 ATMsadopted mapping technologies to identify locations of its branches in low-income neighbourhoods to meet its Community Reinvestment (CRA)commitments. CRA act states that “regulated financial institutions have continuing and affirmative obligations to help meet the credit needs of thelocal communities in which they are chartered.” The act establishes a regulatory regime for monitoring the level of lending, investments, andservices in low- and moderate-income neighborhoods traditionally underserved by lending institutions.

The geographic analysis application helped the bank gain important insights into target markets and strengthen its commitment to CRAcompliance, while impacting site selection decision-making in those areas.

In a six step process the client first identifies all Census tracts that contain Bank of America branches and creates a map layer to display thisinformation. Then, the system searches for and shows all of the Census tracts adjacent to those tracts with branches. Then the system determineswhich tracts within the “adjacent tract” list are comprised of low- to moderate-income neighborhoods. The software’s distance calculator is used tochart the distance between all current banking centers and their adjacent tracts located in low income markets. Branches located within a specificproximity, as defined by federal regulators, to low income neighborhoods earn valuable CRA credits for the bank. As a precautionary measure, it isnecessary to make sure the identified route between a branch and its adjacent low income neighborhood does not include any man-made or naturalobstacles, such as a water boundary or major thruway, which might hinder customers’ travel to and from these locations.

• 25% time cuts compared to manual audit of a network of banking centers

• Easy mapping, visualization, and analysis of geospatial measurements

• Maximization of the CRA compliance score

OBJECTIVE: to identify locations of the banking centers in low income neighborhoods in order to receive an outstanding ranking on CRA compliance while maintaining bottom-line profitability

BANK OF AMERICAUse case from Pitney Bowes Business Insight

GIS

Netherlands

SOLUTION BY TECHNOLOGY USED GEOGRAPHY

RESULTS

© Unacast 2017 13

In Turkey, digital conveniences are commonplace; the country is one of the largest mobile banking markets in the world with 21 million bankable digital customers over the age of 18. To keep pace with a digital age Garanti wanted to deliver innovative services centered around the needs and aspirations of users.

Accenture created iGaranti, an "atomized" service that has 23 different applications that leverage big data analytics and can be personalized for each user. iGaranti places an emphasis on live feeds of information and data visualization, and takes advantage of smartphone and tablet capabilities, including voice, camera and location settings. The Turkish bank is revolutionizing mobile banking with the launch of iGaranti, the world’s first socially integrated mobile banking suite. Rather than a single mobile application, Accenture designed iGaranti as a series of applications that aggregates wallet, savings, loans and other applications, allowing users to customize their experience according to their needs.

Garanti is personalizing the relationship between its customers and their finances, giving users control over their money:• iGaranti provides live updates and financial offers in real-time• Users can send payments to friends through Facebook, send relevant offers across social networks, and redeem location-based shopping offers

while on the move• Users can make in-store payments from multiple credit cards

iGaranti also allows users to securely pre-alert a bank machine to their arrival, eliminating the need for a physical card.

• iGaranti was downloaded more than 100,000 times in the first month after its launch

• More than 110,000 active users

OBJECTIVE: to personalize the relationship with clients and their finances by giving clients more control over their money

GARANTI BANKUse case from Accenture

BeaconsGeofencing

App

Netherlands

© Unacast 2017 14

The information contained in the following section has been aggregated from data provided by Proximity.Directory members.

THE STATE OF PROXIMITY

© Unacast 2017 15

457 companies from 58 different countries are registered onProximity.Directory.

North America and Europe are leading the game with 77% of thetotal number of companies coming from there. The rest of theworld accounts for just over 20% of the total number ofregistered providers.

More and more companies from emerging markets recognize theopportunities of location and proximity solutions. Since the Q22017, the number of companies from Africa increased by 80%,from South America by 56% and from Asia by 24%.

PROXIMITY SOLUTION PROVIDERS BY COUNTRYGlobal distribution of Proximity Solution Providers

Europe 39%

NorthAmerica 38%

Asia 15%

SouthAmerica 3%

Oceania 3%

Africa 2%

© Unacast 2017 16

PROXIMITY SOLUTION PROVIDERS BY COUNTRYGlobal distribution of Proximity Solution Providers

The United States is leading the provider race, with 152 registeredcompanies coming from the country. The United Kingdom is secondwith 53 companies, and Canada is third with 22 companies. India is onthe fourth place with 18 companies. Since the last quarter, Q2 2017,the number of companies from India doubled.

If we consider the geographic area of the leading countries, we see thatthe UK is 14 times more sensored up than the the US and 41 timesmore than Canada.

United States 33 % United Kingdom 12 %

Canada 5 %

India 4 %

France 3 %

Italy 3 %

Spain 3 %

Australia 3 %

Germany 2 %Netherlands 2 %

Norway 2 %China 2 %

Other 26 %

The PSP index is based on the information provided in company profiles and is not a scoring of the companies’ success.

The following measurements are taken into account for the ranking: whether the company is in commercial or pilot stage (max 2points), clients (max 1), sensors deployed (max 2), number of employees (max 0.5), geographic presence (max 0,5), number ofuse cases in the profile (max 3), when PSP last updated the profile (max 1). It is possible to get a total maximum of 10 points,and the scorings are weighed differently depending on what is most important. For example, having a company at a commercialstage is a more important aspect compared to the number of employees. In order to be classified at a commercial stage, it ismandatory to have at least one commercially launched use case in addition to listed client(s) in the Proximity.Directory profile.

We split the results into hardware and platform to make the comparison more valid.

You can see how companies have moved compared to the previous quarter with anincrease/decrease value in the number next to the score.

© Unacast 2017 17

PROXIMITY SOLUTION PROVIDER INDEXMethodology

© Unacast 2017 18

PROXIMITY SOLUTION PROVIDER INDEX (PSPi)Hardware Companies

PSPi HARDWARE

1. Kontakt.io (Poland)

2. Estimote (UK)

3. Cisco Meraki (US)

4. BlueUp (Italy)

5. Shenzhen Minew (China)

-- 8.65 (-)

-- 7.5 (-)

-- 5.7 (-)

-- 5.2 (new)

-- 5.25 (-)

The top-3 leaders of the PSPi hardware ranking have not changed theirpositions during the past year.

A newly registered company appears to be on the 5th place, which isShenzhen Minew Technologies. Founded in 2007 in China, thecompany produces a wide variety of sensors, including beacons formeasuring temperature and humidity, accelerometers, anti-lost devices,asset tracking systems, wearables, and other.

(+/-) Difference in company ranking compared to previous quarter

© Unacast 2017 19

PROXIMITY SOLUTION PROVIDER INDEX (PSPi)Software Companies

PSPi PLATFORM

The top-3 leaders in the PSPi software category have slightly changedthe positions since the Q2 2017, however, Swirl remains an absoluteleader for more than a year.

Three new companies have climbed up to the top-10 this quarter: PlotProjects, Purple - Intelligent Spaces, and Leantegra. Plot Projectsfocuses on geofencing & beacon marketing software for mobile appsand marketing automation platforms.

Purple’s cloud based solution allows in-depth understanding ofphysical spaces and customers by providing an access to a highlyreliable Wi-Fi experience.

Leantegra develops software and hardware products for location-basedadvertising and real-time asset tracking.

(+/-) Difference in company ranking compared to previous quarter4,1(+1) 4,1 (-7) 4,25 (+58) 4,25 (-8) 4,3 (-9) 4,4 (-6) 4,4 (+63) 4,55 (+3) 4,55 (+4) 4,7 (+2) 4,9 (0) 4,9 (+95)5,1 (-2) 5,25 (-2)

5,85 (new) 6,05 (+64) 6,1 (-1) 6,25 (-1) 6,4 (+2)

7,85 (-)

20. Zoniz

19. inBeacon

18. Xtremepush

17. OnyxBeacon

16. Blesh

15. Signal360

14. Poi Labs

13. BluVision

12. Gimbal

11. Aloompa

10. Leantegra

9. Aruba

8. Smart Beacon

7. Proxama

6. Purple - Intelligent Spaces

5. Plot Projects

4. Beaconinside GmbH

3. Tamoco

2. Spark Compass

1. Swirl

© Unacast 2017 20

879,500

3,349,000 (+281%)

5,103,500 (+52%)

6,201,000 (+22%)

8,273,500 (+33%)

11,770,500 (+42%)

13,074,000 (+11%)

14,486,000 (+11%)

15,176,500 (+5%)

17,300,000 (+14%)

Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017

PROXIMITY SENSORS DEPLOYED GLOBALLY

14% increase in sensor growth in Q3 2017

Faster increase in the number of sensors deployed: 14% in the Q32017 compared to the Q2 2017.

The world is sensored up further, and as of Q3 2017, 17,300,000sensors are registered on Proximity.Directory. 58% of these sensors arebeacons, 25% are Wi-Fi points, and 17% - NFC sensors. Compared tothe previous quarter, the number of Wi-Fi sensors deployed increasedby 47% and the number of NFC sensors by 33%, while the number ofbeacons remained stable.

SENSORS DEPLOYED GLOBALLY

(+/-) Difference in company ranking compared to previous quarter

© Unacast 2017 21

POPULARITY OF DIFFERENT BEACON STANDARDS% of total Proximity.Directory members supporting a beacon standard

Q2 2017Q1 2017Q4 2016Q3 2016Q3 2016Q1 2016Q4 2015Q3 2015Q2 2015

56%56%56%55%49%

5%

25%

38%

45%

96% 96%93%

90% 89% 90% 88%87% 86%

BEACON STANDARDS: iBEACON VS EDDYSTONE

More emphasis on Apple as Google continues to push

iBeacon can trigger notifications within mobile apps installed on auser’s device and is natively supported on iOS.

Google’s Eddystone can not only trigger notifications in mobile appsbut also in URLs in browsers on smartphones. Eddystone protocol issupported by both, iOS and Android.

Proximity Solution Providers do not want to exclusively choosebetween iBeacon and Eddystone as most of the companies work withboth protocols depending on the use cases. Eddystone is currentlysupported by the 55% of the industry while iBeacon by 83%.

53%

83%

Q3 2017

Q3 2017

Q2 2017

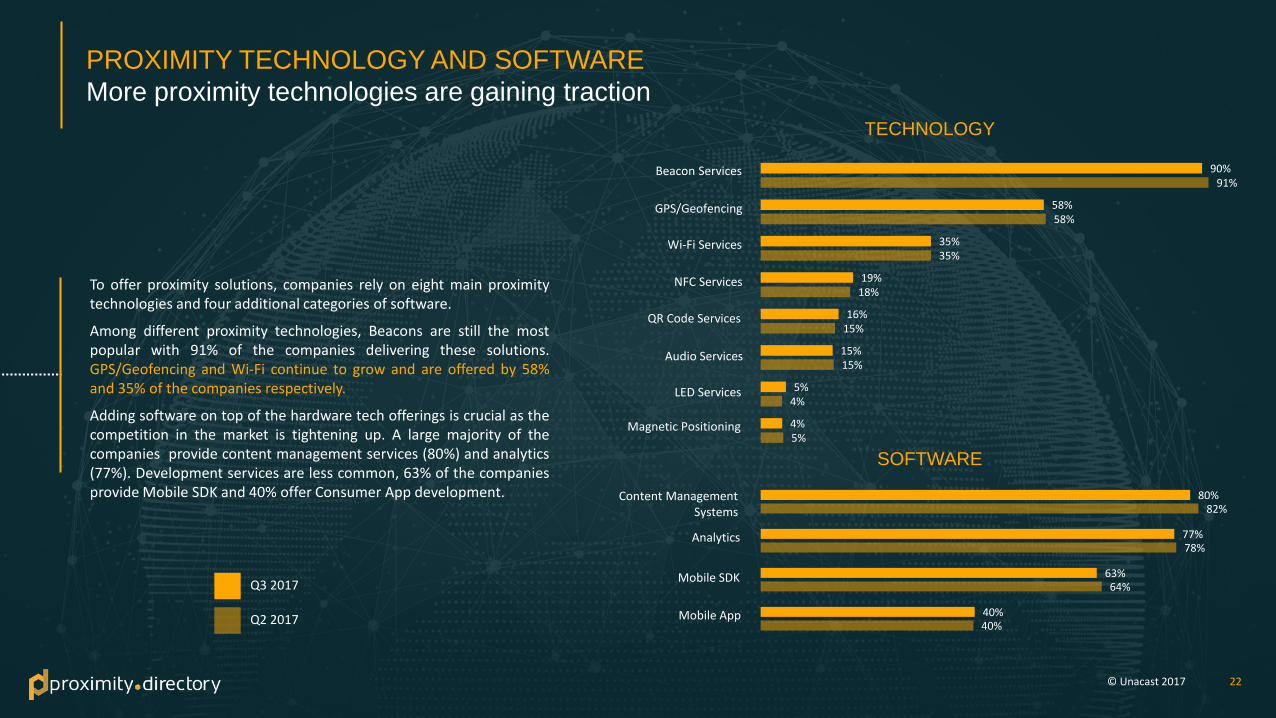

To offer proximity solutions, companies rely on eight main proximitytechnologies and four additional categories of software.

Among different proximity technologies, Beacons are still the mostpopular with 91% of the companies delivering these solutions.GPS/Geofencing and Wi-Fi continue to grow and are offered by 58%and 35% of the companies respectively.

Adding software on top of the hardware tech offerings is crucial as thecompetition in the market is tightening up. A large majority of thecompanies provide content management services (80%) and analytics(77%). Development services are less common, 63% of the companiesprovide Mobile SDK and 40% offer Consumer App development.

PROXIMITY TECHNOLOGY AND SOFTWARE

More proximity technologies are gaining traction

© Unacast 2017 22

LED Services

TECHNOLOGY

SOFTWARE

Beacon Services

GPS/Geofencing

NFC Services

QR Code Services

Magnetic Positioning

Content Management Systems

Analytics

Mobile SDK

Audio Services

Mobile App

5%

4%

15%

15%

18%

35%

58%

91%

4%

5%

15%

16%

19%

35%

58%

90%

Wi-Fi Services

40%

64%

78%

82%

40%

63%

77%

80%

As the value and demand for location and proximity data is growing,PSPs offer more products and services.

Products can be split into seven main and three additional categories.The most commonly offered services are mobile communication,indoor navigation, and proximity advertising networks. This relates tothe fact that most of the clients of PSPs are from retail-relatedverticals.

Many PSPs provide solutions to their clients through offeringadditional services such as project management, consulting, andestablished beacon networks.

Established beacon networks let third-party brands deliver hypertargeted advertising through existing sensor infrastructure, monetizegathered data, and drive sales through online retargeting campaigns.

18%

19%

26%

30%

43%

54%

75%

19%

20%

25%

30%

43%

52%

72%

47%

50%

55%

47%

50%

55%

© Unacast 2017 23

PROXIMITY PRODUCTS AND SERVICES

PSPs continue to add value to their product portfolios

PRODUCTS

SERVICES

Q3 2017 Q2 2017

MobileCommunication

Indoor Navigation

Proximity Advertising Networks

Online Retargeting

Mobile Payments

Digital Signage

Data Monetization

Project Management

Beacon Networks

Consulting Services

Q3 2017

Q2 2017

INDUSTRY VERTICALS

PSPs decide to enter new industries and markets

© Unacast 2017 24

Proximity.Directory covers 19 industry verticals where proximity and location technologies are leveraged. Retail, shopping malls, hotels & tourism, airports, and sports stadiums are the top five verticals where we see companies operating.

PSPs continues to diversify their product offerings and enter new markets. Since the technology and analytics can be adapted across different industries, companies serve clients from multiple verticals.

72%

66%

54%

50%

48%

51%

49%

44%

42%

40%

39%

41%

37%

36%

34%

35%

32%

29%

28%

74%

68%

55%

53%

50%

52%

49%

46%

44%

42%

40%

41%

38%

37%

35%

35%

33%

30%

27%

Retail

Shopping Malls

Hotels & Tourism

Cafe & Restaurant

Stadiums & Sports

Museums

Airports

Concerts & Festivals

Conference

Transportation

Themeparks & Zoos

Healthcare

Cinema & Theatre

Automotive

Education

Banking

Real Estate

Gas & Service Stations

Logistics

© Unacast 2017 25

40 %Platform

PSP CATEGORIES

IN DIRECTORY

6 %Consulting

33 %Platform & Hardware

10 %Hardware

7 %App

184 companies are focused on providing platform solutions.Proximity platform is used to offer products like mobilecommunication, proximity advertising networks, datamonetization, indoor navigation, digital signage, onlineretargeting and mobile payments. Examples of proximityplatforms include Footmarks and Plot Projects.

31 proximity solution providers focus mainly on hardware.Proximity hardware provider typically provides beacons, NFC, Wi-Fi, RFID or other sensors. To manage the hardware, tools for fleetmanagement and SDKs are provided. Examples of proximityhardware providers are Kontakt.io and Estimote.

151 members in the directory provide both a proximity platformand hardware. Examples of platform and hardware providers areSignal360 and Gimbal.

47 members focus on providing and distributing proximity apps(which are essentially proximity platforms). Examples of theseapps are ShopAdvisor and Check.

18 companies focus on proximity solutions consulting, such asHeyBuy.

3 %Other

CATEGORIES OF PROXIMITY SOLUTION PROVIDERS

There are five types of market players in the proximity industry

© Unacast 2017 26

HELP SPREAD THE WORDOur goal is to educate the world on proximity and location technology. If you find the report useful, you can

contribute by by hitting the below share buttons!

READ PREVIOUS REPORTS