i-ft€ - dcmsme.gov.in · subject: modified exposure draft on guidance note on.accounting for...

TRANSCRIPT

Most-Immediate

No. G-20013/3/2018-19-Budget.Government of India

Ministry of Micro, Small & Medium EnterprisesOffice of the Development Commissioner

(Micro, Small & Medium Enterprises)Budget Division

*****Nirman Bhawan, New Delhi

Dated: 25.05.2018

Office Memorandum

Subject: Modified Exposure Draft on Guidance Note on. Accounting for Fixed Assetsreg.

i-ft€ undersigned -is-d1i-&t"¬ ddto forward h€1"€witn a copv-of-letter-dated -z6:4.l{3{£received from Government Accounting Standards Advisory Board, Office of theComptroller and Auditor General of India, New Delhi on the subject mentioned abovefor information and compliance.

2. All the concerned entities are requested to update their Asset Register inaccordance with the guidelines to enable the Division to submit the consolidatedinformation as and when required.

Encl-. forwarded by email.

~!'F(S.K.Verma)Dy. Director (Budget)

1. JS(ARI)I JS(SME)I JS& ADC(SG)I CCAI DD.G(NG)/DDG (PKM)I ADC (PS)I ADC(SM)IADC(AS)

2. Dir.(SME)I JDC(S8)I Dir (AM)3. Dy. Secy.(ARI) I Dy. Secy(SME)I Dir (OPM) I Dir (RKR)I Dir (SC)I Dir (SA)IDir (RCT)4. All MSME-Dls/ Br. MSME-Dls

All DDs/ADs - % DC(MSME) }All Sectional Staff - 0/0 DC(MSME)Copy to:-

for strict compliance

PSto AS& DC(MSME)

https:llmail.gov.in/iwc_static/layoul/shell.htmJ?lang=en&3.0.1.2.0_15121607"'" 4/2~2018

MQdified Exposure Draft -Guidance Note on Accounting for FixedAssets-reg. [email protected], [email protected], [email protected],chmn@de~~9ov.in,secy-ayust~ nic.in,[email protected],fe,[email protected],[email protected],[email protected], [email protected],s~fy.moc@~i8·in, ,f,[email protected], sec,[email protected],sec~etary:posts@ iQ~1~postwv .in, sefY;Rot@nif:in, sec,[email protected];secy-food~nic.in, s;cy.mca@ Qic.in, secy-cultur,[email protected],d~!~Tcy~nip.!n,fegT;xn90~,giC.in, [email protected],,!s:~hristoph~·~~hqr;q[?o.in, sE)Wes..y@ni~.in, sesY~,oner~riic.in,~~fydwS $Y ni8' in, sibretary,@\TIoes:gov.!n, [email protected],sec -moef nic.iQl'psfs@mee·90y',;iQ,T~fywestr~,rrea'99~,·,in,

a a:gov. cYfPv@mea:gov.in"~.~8yer@~.E)?-.g6v.in,s;[email protected], s~f¥[email protected], [email protected], rsecy@)nic.in,~;CY,'"rnOfpi,~•.nic. in,\g~Qec().~9rnaiI secx,,~f'ff@nic,iQ,[email protected], iida:rsh',2 mail.com, (PS) <;;;,'[email protected]; secy-qpe@nic,in/[email protected], [email protected],

ic.in, T~cy~rban~ri,\,c.iQ:,T,[email protected]'sec .selin .in:'secY8;i,YTst@inic.,in,[email protected],

v.in, [email protected], [email protected],s~fretary-~sm7'~ ~ic,in, s;[email protected], [email protected],secy"[email protected], [email protected], [email protected];s~sy-arpg~riic.in, s,E)w_mop~nic.in, [email protected],sE)SY.,-po nic.in;crb@rb ..... et.gov,in, secyrth@gmaiLcom,eC Ir@

c.inni Rungta

I!!j.Letter to Secretaries_for sending GN Modified_13.4 ... (672kB) I!!j.Modified ED_GN on Accounting for Fixed Assets_13.4 ... (3.1MB)

3i1C\{oftll CH$~C\lIl<H$~C\lIl,~a=rtI CfiT ff~1TR«1 "Guidance Note on Accounting for Fixed Assets" 1!Cf

CH~If(;ja~TCfl/~.~. c=rm flC\'fll fI'ftlq/~ mr ~am-c=r ~ cfi'r ~ q;rcfr ~ Cfif ~~r ~3IT 6"1, ~~ ~ $" *c>r cf; ffc;3t * 3fl1afi tnCRfr 'SICJOl ~ Cfif ~ cR" 1The undersigned has been directed to send the scanned copy of the duly singed letter by Director

GeneraliGA &Member Secretary/GASAB and Modified "Guidance Note on Accounting for Fixed Assets".Kindly send a line of confirmation to this e-mail.

OHice01 the DevelopmentComrwsioner 'M~18)Thisletterhas~~..wte.~n 0 1L~l8

~ g»lR, ~. 'Q1m. ~, 'l'RJ(il, e-office vide N~~~atcd ' .. . .".-

'4R(f~~~liQI8'@1qtlzypcpf~, ~ ~ e -4!tl;t10, ~ ~ \lfLIR' 1Wf, ,@V' ~ r:\\ 2; Officer /Oificlal(CRU)

~~-110124 \...\'5 .1~~~~ -.J \ y"~~~~Manoj Kumar, y./~ ) \.,;Sr. AO., GASAB, n)...1'" \) V\..CY- {>'..J y0/0 The CAG of India, \~ V ~ IJ10, BSZ Marg, New Delhi-110124 cr" ,,_ \'I'Ph. No, 011-23607254

(2.iiihttps:llmail.gOv.in/iw'J.....>4a\iC/layOUUShell.htrrl'}ijlg=en.&3.0.1.2.0_15121607

4'-~b1>1'b '>P...b l~- I.!'fJ ~~

~.:'ffiR ..-..r~7..s:::./~/~.I~ ~ (>I1~~t)\jl/195-2017 (:llfcJT-II)~ : 26.4.2018

:9~ .. j. ~ .:a,<:",,~ ~ ~4 ;;JJ {:;] q~P.. ·*,RCJJ;sr~(~ OJJR.'ij / ~l;,fit· ~:eQfJ, ~

~ \ifIli'l ~l~ ~<..ct)I-l

~: Modified Exposure Draft on Guidance Note on Accounting for Fixed Assets-reg.

CR€>~C\;q / CR€>~C\4I,~ 3"Q" fCl431Ch CR~IJI:Wlq{)~/R~. vet ~ll{q~Gi/~ c);- m QllflcR!ll Q;1

fC;i;TIq; 22.3.2018 em ~af <t ~ m~~ ~ JII$gc;-fi cITe ~ JFhI3R:JI mfCnCOffS Qfl~'8 c);- Chlll~c;-qllGi *~ Ch«f cf'iI Ufthlll Cht 3mCJ=3l .~ tg ~

fcFm dTm m I ~ ~ dll$gc-B G1Tc c);- Chlll~c;-qljGi ~ ~ c);- ~ Jl ~ c))

~ vet ;Hll)\jlGi Jl ~ ~ mQ<:TCh ?;fr eN ~ I

:i4 tI ifllj I,

~Hd~(~ CR~1::1I)

CR~lfCla~fCJ)"/fI".~. 1Jci ~ ~/~

afRO cf; ~ CR6Icl'8jlq:l)~ <m CbI1QfCiat, 1 0 ~ ~m;~ 'CRTJf, ~ ~ - 110124

Office of the Comptroller and Auditor General of India, 10 Bahadur Shah Zafar Marg, New Delhi·110124Phone: 23231440,23231761 Gram ·ARGEL NEW DELHI Web site: www.gasab.govJn

Fax: 23239554,23213346, 23236828.

-a~C5T~ ~T~Of ~T6cffl~ ~It :tiGOVERNMENT ACCOUNTING STANDARDS ADVISORY BOARD'"

No !1.~P.::f.1).1GASAB/Sectt'/Adv. on Assets & Liabilitiesll95-2017 (Vol.-II)Dated: 26.04.2018

To,

1. All the Secretaries to Government of India,2. Secretary/Pro Secretary/Chief/Addl. Chief Secretaries of State Governments,

Finance Department.

Sub: Modified Exposure Draft on Guidance Note on Accounting for Fixed Assets-reg.

Sir/Madam,Reference is invited to this office D. O. letter dated 22.3.2018 of DAf/GA &

Chairperson/GASAB wherein it was requested to start the process of rolling out the

implementation mechanism for the Guidance Note on Accounting for Fixed Assets. This

would avoid unnecessary delays in collection and collation of information about assets for

implementation of this Guidance Note.

In continuation to the same, kindly find attached the modified Guidance Note on

Accounting for Fixed Assets.

Ends: As stated.

Yours faithfully,

~ -(Divya Malhotra)Director General/GA &Member Secretary/GASAB

m«T cTi ~(fj6ICl'<lllq~~ cpr ct>lllfC'lll, 10 ~ ~ ~ iIl<lf, ~. ~ - 1 101 24

Office of the Comptroller and Auditor General of India, 10 Bahadur ShahZafar Marg, New Delhi-110124Phone: 23231440,23231761Gram· ARGEL NEWDELHIWeb site: www.gasab.gov.in ~.~~.~

Fax: 23239554,23213346,23236828.

Modified EXPOSlJRE DRAFTGUIDANCE NOTE ON ACCOUNTING FOR FIXED ASSETS

1. Introduction

1.1. The Finance Accounts of the Union, States and the 'Union Terrftories withLegislatures, reflect information on capita) expenditure as well as on financial assets andliabilities of the Government, However, the information on the fixed assets' of the ~ntity,is 'not ~aptured in.the present system OT cash basis of accounting as such informatiqrl is

.presented merely as capital expenditure, Fixed assets are valuable resources of theentities, It is, therefore, essential that the government entities have complete informationabout their fixed assets for better accountability. This Guig~nce Note wouldfacilitate theavailability ofinformation on Ca.pital Expenditure under Primary Units of Appropriation(PUA) as well as information on the fixed assets that have been acquired or inheritedoverthe years in standardized disclosures.

1.2. The'Twelfth and the Fourteenth Finance Commissions had proposed, inter alia,thfit additional information in the form of Statements should be appended to the t){istiqgsta~¢1J1entsin the Finance Accounts to enable informed decision making, The fiscal~espqnsjbility and BudgetManagement (FRB~1)Act prescribes the preparation of AssetRegister by the entity. The Expenditure Management Commission constituted inSeptember 2014 also recommended that the "Government Should move towards an ITenabled e-Asset Register", Further, as per International Public .'$.e()torAl:coun;tingStandr;trd:Financial Reporting under Cash Basis oj Accounting, an entity is enCcium,_gel:l

. -, ~ . .

to disclose information about its fixed assets.

1.3~ The fixed assets in various government entities are of' diverse nature. Thls,Guidance Note recommends detailed elassificafion of fixed assets as. compared 'to thatprovided under tM extant PUA2 (Object Heads), while leaving sufficient flexibility forentities to add ,additIonal sub-classes of fixed assets in keeping with their nature OT

operations. Similar flexibility is sought to be made available to qepa(tments andministries to disclose "strategic" assets in the Fixed ASSets Register as p~rthe extantpoli9Y Qfgqv~rn!Uentto safeguard national security,

!Definition afFixed Assets at ...5..l.6~.A; per the·prevaiiing Delegation of Financial Power Rules (DFPR), there are only 3 Ob.jectHeads

, 'I

2. Present status

2.1. 'The present system of cash ba,sts of accounting in Goyemment discloses capitalexpenditure up to the Minor Head/ Sub Heads in the Finance AG,counts. The existingStatements provide some inf¢i1nMion on both the current -and cumulative capital'expendjfute on both £inancial~nd phYsicalassets of the Gpverlu:riimts:

2.2~ Two lndian Government Accounting Standards (IGASs) have already beenformulated .by Governmeot Accounting Stahdards Advisory Board'(GASAEl1Viz, lGAS ;c

3: Loans and Advances made by Governments (already notified by Ministry of Finance)and lGAS -9: Government Investments in Equities (under consideration for notificationbyMinistry of Finance) to capture the information on financial assets of'the'Union, Statesand the Union Territories with Legislatures.

2.3. It is seen that complete details of fixed assets owned/under construction/

'consttuct~d/purchased/ac.quired by a Government entity are not :a.vaHablein the 'FinanceAccounts .. Purther, fixed assets Iik:e computers, furniture etc., booked undyf revenueobject heads viz., Office Expenses and Other Administrative Bxpenses are ourrently notcaptured as :c~~ltalexpenditure. In addition, heritage. intangible and 'leased assets are notrecognized and therefore not included iTi the Asset Registers, Further, no. de~tecogniti()nofasset takes place even after the asset is no Jonger in use.

2.4, In the present system of cash basis of accounting, if the purchase and' paymenthappen in different accounting periods, recognition of asset remains a problem, to tbeextent that the asset fails to be recognized in the Asset Registettill pa)!irlent ISmade! evenif the asserhas been delivered and put to use. In some oases, the asset correspotids only tothe capital expenditure incurred and does not reflect the true value to the extent ot theunpaid .liability~

2.S. Due to the fact that the present system of cash ba~is o.f accounting does notte¢o~iz~ fixed assets as such, put recognizes them merely:ascapit<i.r.exp¢ngitun~,CapitalWorks-in-Progress (CWIP) is subsumed in' the capital. expenditure booked ,and both theaccounts and the existing Asset Registers do not separately depict C~pital Works,;inProgress.

2.6. Details like hililvoucher numbers are also not link¢<1; se the inf9rn1ation ln theexisting asset registers is not transaction driven.

.~.

3. Objective

3.1. Tbe qbjective of this Guidance Note isto prescribe the disclosure' reqUIrements forfixed assets for reporting under present system of cash basis of accounting. Compllancewith the disclosure requirements laid down in thi$ Guidance Note would enable

comprehensive and transparent financial reporting with regard lo,capitaLe4pehditufe $:nd'provide ~ir(form~ti9nabout entity's fixed assets including cha:n'ges therein. lienee, th~;o~jective islwin fold, vito"

3.1.1. Preparation of transaction linked Fixed Asset Registers by the Departments (A!1nexutes1 and 2). These Registers would enable providing of detailed information on the'recognition and derecognition of an asset, measurement of its cost by 1\0 entity' anddepiction of various classes of assets, viz. land, building, plant & machinery etc. With

all inherent flexibility for entities to add additional sub-classes of fixed assets keeping.in vi~w thyir nature of.operatiens,

~.l ..Z. Insertion pf a separate annual Statel11ent on Capital Expenditure for A~gursiti6n ofPixed Assets in the Finance Accounts, This statement Woulet be pr~pafl?(,i 'by

" ._.- ~. . -,' .

ag...g.regatil1g·the information at the level of ,PUA (Annexure 3)r» Toe .in(()rmaticlt!.wUI.,,' '. .

flow from. accounts and have direct concordance with extant PUA. It should dypict

annual additions to the capital expenditure and the resultant curfl~l~tiye total.

4. Scope

4.l.This Guidance Note applies to Governments at Union level, State levil and to the UriionTerritories WIth Legislature. The entity that prepares and presents 'Fln~nce Accollntsunder present s,ystem of cash basis of accounting should apply this 'Gtiiclairce Ngtethrough its Admillistratiye and ACCollnting .Authorities to prepare' Fix~dAsset Re~gistet~and the annual Statement on C~pital Expenditure for Acqujsiticm of Fixed Ass~f$ forinsertion. in the Finance Accounts. This Guidance Note applies to all fixed assetsincludingthe following. exceptthose specified in paragraph 4.2:

(i) Infrastructure Assets;

(ii) Her~t(lgeAssets;

(iii) Capital Works in Progress (CWIP);

(iv)lntangibJe Assets except those..mentioned in.paragraph 4.2 (iv)

4.2,"This Guidance Note does not apply to;

(i) Biologiqftl ;,t~setse.g. plants flnd living animals related toagricultural fl:ctiviW;

(ii) Natural resources li~e minerals? oil, natural gas and sirriilat n,on.regeneratiVeresources and spectrum;

'(lii) Ph,::~daSsetSobtait).ecIon shol'tterm lease Qf1essJhan 3 years; and

(tv) lnt~rfiany generated intangible fixed assets, iexqept CQQilput~r software S;l;ndpatents.

5. Definitions

5.1. Thefolldwing terms. ate used in this Guidance Note with the meanings specifiedfor the preparation of the Statement o.rt Capital E:xperiditure for Acq.uisition of FixedAssets (for inclusion in the annual Finance Accounts) and the Fixed Assets Registers, tothe extent relevant:

5.1.1. Book VallIe is the amount atwhich an asset is r~jlef)led /n lh~ Statement on CapitalExpenditufefor Acquisition ofFixed Assets in the Finance Ac:cQu*s and the FfX,etJAssets ~egisters.

5.1.2. CapiiarWOfk$.-Jit-Pr~gres$ (f;Wip) ,s,the expendi[Jjn~ onfi~edassets that are in theprocess. ojconstrl/,cli011 Or i::omplefiQ11lie, not ready flf inttmded use at the time ofincurringof expenditure,

5.1.3. Custodian is:an authority in the entity. J:llat .is·entrusted with nhe responsibility of thefIXed asset.

5.1.4. De~te(:ognitiQn is elimination ojal1 Item offlXed 'asset in the Fixed Assets Registers atthe time o/disposcll e.g. trdnsJer/~tJ[e/dJ$mcmtlingolobsolete assets/wytte-offoj assetetc.

S.L5. entity i~theDepartment/Ministry/Field Urdtfor whichacqotmt.~ areprepttred;

5.1.6. FixedAsset i$ emassesheldfor use in the prod,ilction O1\supplyq!goods or services forreiualto others, or/or adm{nisirative purposes and is eXpef!ed ta be ,YSeilfor more than12mOnths.

5.1.7. lleritage Assets art; fixed assets With hi~'torli:, artistic; scieruific, technologiqal,

geophpsicql or environmefttcil qualities that 'are held and mai'ntatnedprfncipallyjoftheir contribution to k:nowfeage an4 culture! 811C}Z (JS antiques, boob, historic builCiingstlnd archaeologicatslte~ ..

6.1.1. it is probable that future economic benefits or service potenJi~l assoclated withfheasset will flowto the entity; and

6.1.2. cost of the asset can be measured reliably except where Guidance Noterecommends measurement of the assets at nominal value of'Re. 1.• ' _',--:".- " - _, '" '0' _ .• , .' ,.. . . _ " •. "

5.1. 8. Historical cost is cost incurred to acquire, purchase or construct an asset including the

cost incurred to make them ready for intended use.

5.1.9. ImptoyementlUp gradation means additional expenditure on the assets which enhances

their utility by increasing their useful fife and/or capacity.

5.1.10. Intangibk A~ets are identifiable, non-financtaiassets iVit/u)y,tphysical sy,bsfanc,e ego

computer software.

5.1.1,1. Lease is an agreemen: Whereby one ¢nlity (lessor), in return for apayment or ser}es Qf

payments, agrees to transfer the right to USe an asset to anotherentlty (lessee) for {In

'agreed period of time.

5.1.1,2. Legal Ownership ofafixed asset vests with an entity in whose name the asset is

registered or is owned by virtue of the sovereign rights of the Government;

5.1.13. Primary Units of Appropriation is the unit of accounting (Object Heads) in respect ofa

Grant or Appropriation for charged / voted expenditure.

5.1.14. (.f$e/u/ life oj afixed asset is the period over which an asset is expected tobe-used by the

¢,ntity(Or:dinarily~.land has an unlimited useful.life.

6. R.ecognition

6.1. Mitem of fixed asset acquired or constructed should be recognized as explained

hereinafte.r irrthe Fixed Asset Register as arid when:

6.2.1tems of fi~ed asset costing less than the tbfeshold value of R~.$,,000/'- (Rupe~$ p:ve

thoW~and) and/or having useful life of less than 12 months from the date :Qf~(;q41&iti~J1l,shouldb~ reC()gnized as reveijue expenditure.

6.3.LaPG sho\ild be recognised as a fixed asseHrrespective ofits value anq 'shOuldbe feC9raedin the. Fix.~d.As~et .Register, Land component should be recognized s,eparately ,:If?m#1~built-up structure on it wherever they have been acquired separately ol.'·wh~fe the bre;tl<-:upis readiJy available.

6A.ltems such as spare parts, stand-by equipment and stlrvicing-equipment are

recognized as fixed assets in accordance with this Guidance Note when they meet the5

- - -- -- -------

definition of a fixed asset. Otherwise such items are to be classified as Revenue

Expenditure. Where such an item 'qualifies to be recognized as fixed asset (including

consideratianof'threshold value of Rs, 5000/ ..}, it sho\lld be recorded as a separate item

along with the relevant item offixed asset in the Fixed.Assets Register in the field priit.

At the time of consolidation of fixed assets atDepartmelltf,Ministry/State level, 0<;>8t ofallspare parts should be combined with the cost of the main asset in the Fixed Asset

Register.

f).5. Capital Works- in-Progress (CWIP) ...The expenditure on f,~eq ass~ts/pr()je9ts that are

in the process of construction or completion and are llot ready for intended use on the

reporting date, for example, construction of it building or hydro electric power project,

should be recorded under eMP in the Fixed Asset Registers in the given column of the

relevant class offixed assets. On completion 01' commissioning ofthe fixed lisset/project,

the total expenditure of that asset/project should .cease 'W be depicted-in CWlP column, In

cases, where paris of a CWIP projectare independently ready for intended use, the related/proportionate cost of such project should be removed from CWIP. The Executive Authority

.in the entity should conduct an aruma) review (itlclucling physical verification) of allprojects under CWIP to assess their readiness for intended use ana their removal from

'CWIP.

6.6. Items, of fixed assets may be required for safety or- envirQnmental reasons. The

acquisition. of such fixed assets, although not directly increasing the fuMe economic

benefits or service potential of any particular existing items of fixed asset, may be

.necessary for an entity to obtain the future economic benefits or service potential from its

qther assets (e.g, entity's .requirement of a retro-fit new ~prinklet/systelIl fof compliance

with fire safetY .regulations). Such items of fixed assets <qualify for recognition as fixed

assets, because-they enable an entity 10 derive future economic benefits or service potential

from r~r~tep.@$ets illexcess ofwhat could be derived hail those items not been-acquired.

6.7. InfrastructureAssetse.g, Roads, Bridges, usually display some or all of the

following characteristics. They are:

(i) part of a system or network;(ii)cspecialized in nature and do not have alternative uses;

(Hi) immovable; ·and

(Min some cases subject to constraints on disposal.

6.8. Heritage assets are of cultural, environmental or historical significance e.g,

historical buildings and monuments, archaeological sites, conservation areas, and worksof art. T~eir value is unlikely. to be fully reflected in financial terms as they areirreplaceable. It may also be difficult to estimate their useful lives. Governments may

have acquired many heritage assets by various means, includin~ purchase, donation,bequest etc.

6.9. Int~rnany generated intangible assets, viz., computer software shall be recognized

when it Is ready foruse and patents shall be recognized at the time ofregistration with therelevant authority,

6.10. Recognition criteria as above should be applicable mutatis mutandis for preparation

of the Statement on.Capital Expenditure for Acquisition of Fixed Assets.

7. Classification of Fixed Assets

7.1. Fixed assets should broadly be classified as per the classification recoItlin~Med

hereinafter, for inclusion in the Fixed Asset Registers (including CWXP) (Annexures 1

and 2), so that cost of the existing asset could prima-facie flow from the accounts andthere is I,lijifoqn· depiction of the assets across government organizations. It isrecommended to have a broad concordance with the Object Heads iilto the Fixed Asset

Register at the Field Level (Annexure 1) and Consolidated Fixed Assets'R~gister at the

Department! Ministry level (Annexure 2). The Statement on Capital E;xpencliture for

Acquisition of Fixed Assets, however, should have a direct concordance with'the extantPrimary Uriits ofApprQpriadon (Annexure'S).

1.2. The following broad classification of fixed assets should be aOClpte<l.inthe Fixed

Asset Registers depending upon the operations of the entity, .duly ensuring' that an

individual a$set does not find a mention in more than one elass.:

1. LandIl. Buildings

III. Infrastructure Assets including Roads, Bridges, Culverts, Pipelines, permanentWay etc.

IV. Machinery

V. Furniture-Fixtures and Fittings. -

VI. Motor Vehicles including Ships, Railway Rolling Stock, Aircraft, HeavyArmory etc.

7

9otpll!P0S0psIPoqPlnoqsslUaWTltllsll!~Sn01p~dl.lnJO~unOll~flU!m,~iu;:)J0llL'SJ_0Ssn

P0XYJOSStllCl[.I'1!!A0IaJ0tpJ0pUn;\I0}tlmd0Sposojosjppuaprsdnmoura0q~JOlU~:ll!m::Iql

oipua,1.00iun.0lJ}ltJp0Z!mlOO~.JoqPJn9qs'00ss01tl8130snQIUlJQlZluo[uop::ltI!tJlqOSl9SSV'S'8

'dIMOUlO.Ij'p0,'\OUlQJaqPInoq8Sp~fOJdqons

JOSlSOOp!n<:laltlUO!lJodoldf'P::lttllaJaip'~IlpapU0llI!iOJAp~0J.,(Uu~pu0dapU!ampa[old

dIA\:)UJOSlJ13dgstloUJ:'Pltldlundure)olU~X00qlOJpamsneureqp{noqsdIA\:)0U'P'8

'l'QlI19aninAIBU!wOUttlpsmseatnaqPlnoqsl!(uoHlUlSQnOaS

'Sl.lO!lBtIOp'sm8@qons)UO!lBJQPlSUOOAIm:jI\0ql!MpaJInT;lotlS!lassVWX!.'!tlalalJ.M'£'8

.1'011JOanltlAItIm,lUOU

ttlpernssamoqPInOqsl!';}yqtlm.~:jlgosnlOUS!(PJItl[flm,pnpu!)lQS$tlp::lXIj;eJOlSOo010%','8

'lualllls,nfpB!ldpO~lJOJtlMaqlU!10JPQlunoootlQq

pjnoqslUQuqsnfptlIPut1J01AImpUt!dI&Ourp0soios!p0qosItiPln0t@l0ssnusflu!suq:l,1nd

jf1u!l!noo'lljf1UIPn.qstlbOsp.rnMOlPIlletS~OUUApV-uumjoolUt!AQ[Ql"tIlUIpasojosip

aqpjnoqsiunowlJ1juIPuQdalJ}pus''''-ruopiedluholIlll0ql).tlPQZ!ufloo::usll~SStlPQxg'

'::lsnp0pU0lUflOJAP;e01S!l::lssna1:[lPWP!BdUMqlOUsnqanrBAlltlJ~tIlJ1'lSOOIWP01S!q

Sl!It!p0lnSn:mr0qPlnoqsUO!l!tillOO~JJOJSQYHilnoqO!qM10SSBP0X!J]0w0HUV'l'S

S.l3JS!8alIJ3S$VPaxl.!!JOUOHU.lUd3.1d.IoJuO!l!~()aaH(u!}!nI:j.Ulso;JJOluaw3JuS1f,JW'8

'Sl,~ssnJOsstl{nqCB~JOJ,Slaql(),lapunpoqqriI::I~qPlnoqsStpltlI

t·s~MQlaqa$OIppUllAIQltimd;)sp<)luas::lJdaqPIuoqsaAoqBpUt!stpJl1tZ'S"8:·]6Sl~SS13atIl'IM~rlliawliedadl,(.qS!11!W;)ql1Bi;):j.S!1l011slassyp0xHWlep!lO~UOOaql2~d0Jdan4.M.'r'L

·A).llualBtpJO

suop.BladopUt!Sl,UQW0~!nOO.I at[l.IadStlpap!AoJd(;)qABW"Q:J_a's2uwnnqA.tolOt!Jjdoqs)[JOM

's2u!PIlnqaoYJoS'Btpnss1jU!Pl!nqIlBJOSHU:j.::lPaql',silu!PI!nH,l~pun'0ldwexalOd:'Q1'BpdolddBalQqMS[!Ul0P.I01tllIYaJmdeoOlSl;)SSEQl.{lAJ!ssnp-qnsJ0qll1}JABUt"'-mUQUY'£'L

'a$npapU0lU!JOJApU01AllU0pucd~l?u!

S!la,SSBgqlJIU'~lONaoUup!no;)1:[110S'9qdt!.I2umdq!P0U!BldxalaU1.1BUlatp

U!S@PlaSStlpaxyaql19uurnlO?lUUAaIQJJQpun.'(Z~IS~J01G011UY)SlQlS!2~~

SlQSSVP::)X!d:paluPHosuoOpUt!pm.'!aqlUfP0P.l0001aqPlnoqsUOHQi:).ItSUOOl~pUrl_sloafold.IOJQlO.l!puadxQtm!duo;)ql-(dIJ\\O)sS0~OJd-u!-S)[10M,rBl!dB;)'X

SlQSsyallBlpaH'XI

'Ol~lamA\:ijOSsuqonsslassvQrqIZlImiUJ'utASlUawd!nbapal'BIQ.llI2u!pn{oU!SlUQwd!nbn:'nA

relevant column of Annexures 1 & 2. The interest component of lease payments, wherever

separately available, is recognized as revenue expenditure.

8.6. Land acquiredthrough purchase" should be recorded at the purchase price (pending

amount disclosed separately) and other .incidental costs incurred to bring the asset to its

present ¥ond.Jtion should be included in the .cost of land.

8.7.All heritage assets should be identified and measured at historical cost where records are

available otherwise at nominal value of Re.1.

8.8. IntaniibJe assets such as computer software should be measured at cost. For

"intangible fixed assets under-development" through an external agency, the asset should

be disclosed at the amount paid and the .pending amounts should be disclosed separately.

However, internally generated intangible assets, viz., computer software and patents should

be recognized at nominal value of'Re.L'-.

8.9. Elements of cost- the cost of lin item of fixed assets (tangible/intangible)comprises:

8.9.1. Its purchase price, including import duties and non-refundable purchase prices

after deducting discounts and rebates;

8.9.2. Any cost directlyattributable to bringing the asset to the Io~Ettioriand condition

necessary for it to be capable of operating in the manner' intended bymanagement.

8.9.3. Examples of directly attributable cost are:

a) Installation and assembling cost;

b) Initial delivery and handling cost;

c) Cost of.testing the equipment;

d) Cost of employee benefits arising directly from the construction oracquisition of fixed asset;

e) Cost of site pteparation;

f) Professional fee;

g) Registration charges, stamp ciuty etc. in case of purchase Qf)al1cl;

9

h) Compensation p(lid in C(lse of compulsory acquisition of land, cost of

development of land, rehabilitation and resettlement cost necessarily

incurred in case ofcompulsory-acquisition ofland;

8.9.4. Examples of cost that are not included in the Cost of fixed assets:

a) Cost of opening a new fa~ility;

b) Cost of introducing a new product or service (including cost of

advertising and promotional activities);

c) Cost of providing service in-a new location or with a new class of users;

d) Administration cost (including cost of staff''training): and other general

overhe~d cost; .and

e) Costs incurred after the asset is ready for 4se but not P4t to use,

8.10. Some receipts may occur in connection with the construction or development of aproject/asset, Such.receipts insofar as they relate to ongoing capital expenditure accruing

durfugthe process of construction' of a project, should be utilized in reduction of capital

expenditure. After commencement of commercial production or use for services they are

ordinarily recognized as revenuereceipt, except under special rule or order of government

which should require them to be adjusted in the cost',

8.11. The amount of compensation received from third parties for items of fixed assets

that were lost, destroyed Orgiven up is recognised as revenue receipts;

8.12. Interest on amounts borrowed for constructing the asset, until the assetis ready for

intended use, is recognised as component ofcost of constructed item of fixed asset.

8.13. The Statement OIl Capital Expenditure for Acquisition of Fixed Assets depicts

entire capital expenditure incurred on each PUA Therefore, measurement criteria listed

above should be applicable 'mutatis mutant/is on the Statement on Capital Expenditure for

Acquisition of'Flxed Assets.

3 As per Rule 101 ofOFR, 201710

9. Measurement of Cost Subsequent to Initial Recognition

9.1. Entities incur certain costs of day-to-day servicing or an item e.g, the cost of labourand consumables. Under the recognition principle in paragraph 6, an entity recognisessuch 'cqsts~as revenue expenditure and are often described as "'repair and maintenanceexpenditlire".

9.2. Costs Incurred subsequent to initial recognition for enhancing' the utility of anexisting fixed asset e.g. expenditure incurred on surfacing.a road every few years, are tobe included in-the cost of the relevant fixed asset in case they meet the recognition criteriaspecified in the Guidance Note. This principle is applicable even in case of those fixedassets which are initially measured at nominal value of Re.I. The threshold criterion of:R$. 5000/~is also applicable for such subsequent costs.

9.3. The Statement on Capital Expenditure for Acquisition of Fixed AssetS dep,jctsentire capital expenditure incurred on each P'(]A. Therefore, measurement ,Ctiteria·listec1above should be applicable mutatis mutandis on the Statement on Capital Expendjt).lrefor.Aequisitio(lofFixed Assets.

10.Dereeognitioa

10.1. ,. A fixed asset should be deemed to have been de-recognised from the Fixed AssetResisters of an entity

• Oil disposal;

• when no future economic benefits or service potential is e:x:pectedfrom its use; e.g.,on being donated or transferred to any other entity; dismantled! destroyed on beingdeclared as obsolete or abandoned; or

• lost Or destroyed, in natural calamity or accident like cyclone, tsunami, fite, Ptlbncriots, theft etc.

10.2. A fixed asset should be de-recognised after following the que administrative/Jegalprocess and approval of'the competent Authority in the Fixed Asset Registers only.

11.Disdosur~s

11.1. The entity should disclose the following minimum .information for yach class offixed 'assets in the Fixed Asset Registers at the field level:

i, Class of Fixed Asset11

ii, Date of Acquisition!construction 8{, Bill No.iii. Nature of Acquisition (Purchased/Donated! Leased!Granted)iv. Vendor!Donor

v. Location(Pin Code)vi Unique identificationnumbervii. Custodianviii. Relevant Unit of Measurementix, Useful Life of Assetx. OpeningBalance as onOl.04 ..xi. Additions (amount paid during the year)xii. Cost of asset disposed!de-recognisedxiii. .Closing.Balance as on313 ..•.

xiv. Ullpaid aIllount1:1s011 313...xv. Amount under CWIPxvi. Remarks, ifany

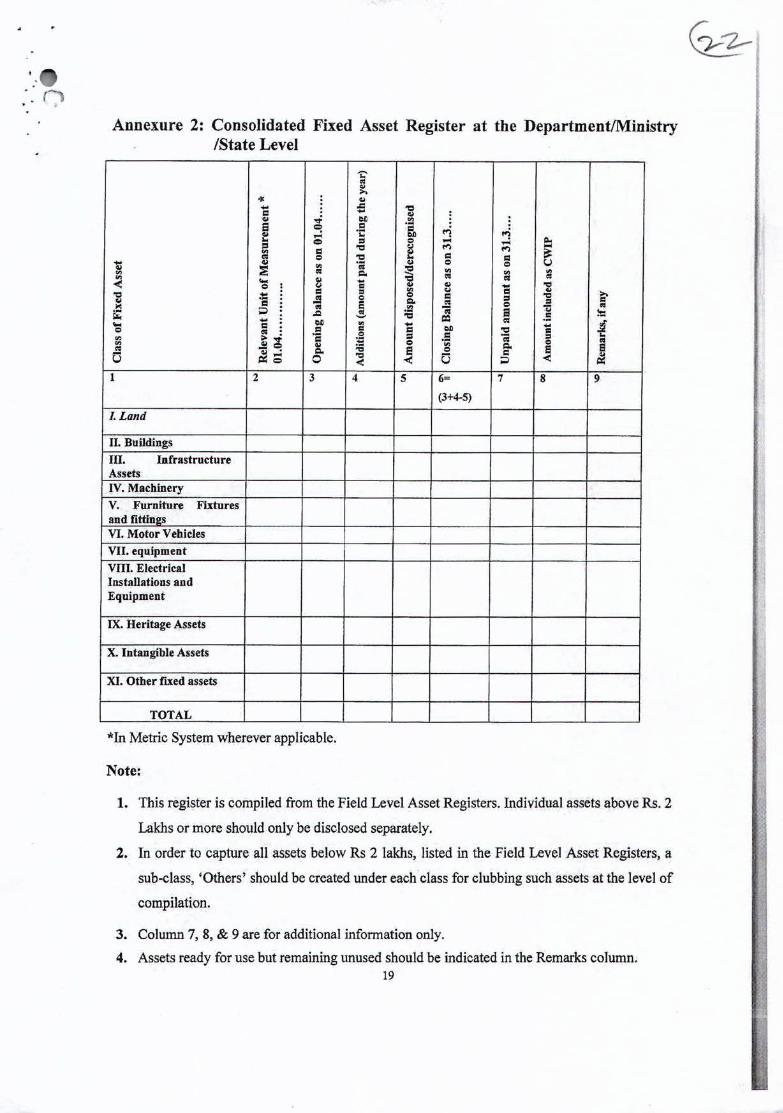

11.2. The Consolidated Fixed Asset Register should be composed of the followingminimum.information:'

i. Class of Fixed Assetii. Relevant Unit ofMeasurementlll. OpeningBalance as on 01.04 .iv. Additions (amount paid during the year)

v. COstof asset disposed!de-recognisedvi. Closing Balance as on 31.3 .

vii. Unpaid amount as on 31.3 ..viii. Amount under CWIPix, Remarks, ifany

The threshold limit to capture assets in the Consolidated FIxed Asset Register at the

MinistryiDepartment level should be Rs. 2 lakhs. All assets beiow Rs. 2 lakhs listed in the

Consolidated Fixed Asset Register should be clubbed under the sub-head 'Others' under each

class offixed asset.

11.3. The Statement on Capital Expenditure for Acquisition 'Of Fixed Assets (forinclusion in the annual FinanceAccounts) shouldpresent the followinginformation:

i. Capital ExpenditureHead as per the extantPUA (Object Heads)ii, Openingbalance I:IS on 01 .04.....

iii. Additions.Dll:ringthe.year12

.r'• ~ 1

iv. Closing balance at 31.03 .

11.4. The entity should also disclose the following in the Remarks column of'Annexures1,2 &3:

i. Transfers to or from other entities, which may be additions or deletions;

n, The existence and amount of restrictions on fixed assets including on title;

iii. Fixed assets given as securities for liabilities;

iv. Encroachment On land/building;

v. In case of land, the existing circle rate from the land revenue department;

VI. Cost of rehabilitation and resettlement in case of land acquired and ip.terest paid on

loans, that are capitalized as part of the cost of asset; and

11.5. The fact that certain existing fixed assets have been included in the Fixed Asset

Registers at nominalamount of Re 1/- and not drawn from the accounts should be disclosedby way pi afCl91Jiote;

lZ, Eff~ctive Date

This Guidance Note will be effective from the date notified by the Government of

India ..

~3. Way Forward

13.1. the Guidance Note envisages a robust IT system for capturing of complete

information I'lt the time of preparation of accounts with least manual interface. It is

sug~ested that the linkages with the accounting procedure be built-in, in the system so

that the information on assets flows from the point of acquisition ill. respect of

procurement of an asset.

13.2. Extatlt rules peed to be revisited to facilitate the disclosures e.g . .including the

process of de-recognition and deletion of obsolete assets to arrive at a listing (prQgr¢ssive

capital expendittll"<,l)of only the existing assets in the books of account, Thus, post

notification of this Guidance Note, the corresponding rules should be amended by

Government, wherever required.

13

----- _.

I;)

APPENDIX ~1

1. ACCOUNTING OF CAPITAL ExpENDiTURE INCURRED FOR ACQUISITIONOF FIXED ASSETS AND FIXED ASSET REGISTERS ...

1.1. Preparation of Fixed Asset Registers (Annexures 1& 2)

The }"ixedAsset Registers should be prepared at two levels,.the FieldUnit Level and theConsolidated Register at the Departmental Level. The compilation of completeinformation on the fixed assets owned/controlled by the government entities following

present systemof cash basis of acceunting should be implementedill two phases for whichtwo Separatefixed assets registers should be maintained Initially»

1~1.1 for .1lJe assets identified through physical verification which were acquired inthe past. The cost of these assets should be duly assigned from aVailablerecords/ vouchersor measured at nominalvalue of'Re 1; and

1.1.2 for the fixedassets acquired after notificationof the GuidanceNote. 'l1lisAssetRegister should be without an OpeningBalance in the first year;

On completion of physical verificatiori of existing assets (acquired beforenotification) as per 1.1.1 above, the valuesobtained Mainst each class of assets inthe Asset Registers should form the opening balan~e for the Asset Registersprepared post-notification leading to amalgamationof the two asset registers.The above two.phases are further elaboratedas follows:

A) The tr~n~itiOIl.phasewhere.the existing fixed assets owned and Mquir¢dinlhepast that are expected to have future economic benefits or service, potentialshould be identified through physical 'verification, These should be identifiedand listed under the given classes as pet paragraph 7 (in accordance with thePUA). The primary requirement of the ~overnment is to obtain complete

information on the listing of the assets. The value should be assigned at thehistorical cost from the existing records. Where records are not available, thefixed assets should be measured-atnominal value of'Re.l. Existing fixed assetsbooked under R~venueExpenditure like Furniture, Fixtures&Fittings, HeritageaSsets, Qffice-equipment, Computers dat~.processing Qnits lie. Ptiilpherals andElectrical Installations& Equipment above the threshold limit, should be listedafterverification.The existing fixed assetsshould be reflected in the Fixed Asset

Registers (Annexures 1 & 2) at the amounts as aforesaid. Preparation of the

list of the assets at the field level after due physical verification should be

a. joint exercise of the Executive Authority and Accounting Authorities.

This information should be consolidated in a generic way at the higher

levels as per paragraph 704. This phase should entail the following

processes;

i, Identification of Assets

Ii, Listing of all fixed assets that have been identified.iii. Dla"ssificationof allassets as per paragraph 7.

iv. Measurement of all fixed assets at paid cost or nominal value of Re.I as

per the principles laid down in this GuidanceNote.

v, Fixed Asset Registers should be prepared at two levels, viz; Field and

Consolidated levels. At the Fie14 level, the item-wise fi?ced Asset

Registers should be maintajneg by tJ;teCustodian in the entity as per

Annexure 1. Thereafter,·consolidation of assets should 'be- dcine at theDepartment level, in the format given at Annexure- .:2, ()f ·!heQt#da*eNot~. The Fixed Asset Register should be prepared by the Custodian, ThegetaiJed proforma ip. Annexure-I should be submitted to the Executive

Authority on a periodical basis for monitoring and reporting purposes.At

the Department level, Consolidated Fixed Assets Register should be

prepared in Annexure-Z.While consolidating the details in Annex1ll'e~2,

the individual items of value above Rs. 2 lakhs of eat:h class of assets

~p9wdbe.disclosed anp an the residual items upto Rs2 lakh~ should be

clubbed and amount should be gepicted under 'Others' below each classof asset.

B) Ppst Notiticatiop/ Implementation phase: Both the Pield and Cop.solidated

ASset Registers should capture the information on flX~d assets

acquired/constructed/purchased from the accounts, in accordance with the

principles laid doW11in this Guidance Note. ThUS,the Fixed A~§et~~gis~ersneed to be transaction based and linked with vouchers. The fOrplat of vOtlcherswould need modification to clearly specify whetherthe expt:m:dif!,lf¢is towards

Capital Works-in-Progress or completed fixed assets. This phase should erit?ilthe followlng processes:

(i) Classificationof all assets.15

16

(ii) Measurement of all fixed assets at the paid cost or nOI11iJ),a:Ivalue

of Re.1 as pet the principles.laid down in this Guidance Note.

(iii) Preparation of Fixed Asset Registers.

Further, the entity should physically verify all fixed assets over a period of not morethan 3 years .and diserepancy.rif any, be recorded, For the purpose of: deleting the

amount under CWIP, there should be an annual physical verification of aU CWIP

projects, jointlyby the Administrative and Accounting Authority of the entity. At

the time of-transfer of the Custodian, there should be a formal handover of the

assets.

t2. Prepar~ti0l1:.of '.~-,State1!Ieot on.Capital Expenditur¢ for Acquisition of FixedASsets (forJnclusion io thy annual .Finance.AcCOiJnts-fi.itoe~ure '3)

The Fm~nce Ac.coupts presents lnformafion on capital expenditure of the Union, States

and limon Territories with Legislature. The existing statements inthe Finance Accounts

include the current and oumulatlve-capitalexperrditute on :both financial and physical

assets of the Governments 'up to the Minor Head/Sub-Head. Thi~re is no aggregation of this

expenditure at the PUA {natut¢ of exp¥nditilre) level.

The Statement oft Capital Expenditure on Acquisition of Fixed Assets as recommended inthis Guidance Note proposes to capture expenditure directly from the extant PUA to

clearly disclose the nature and class ofasset hying acquired. For tile purpose of drawing a

concordance between the Statement and the Fixed Asset Registers, some ofthe principles

of recognition of capital expenditure cannot be applied as extant rules need modification.

For instance, rules will requite modification to address tnefolIQwing cases:

i. ·to bring in.the concept of'recegnitiori ofCWW and fixed assets, rather than merely

capturing capital expenditure;

Ii. .capital expenditure should include items of expenditure above the thresholdvalue of

Rs. 5,000/- (Rupees five thousand) and assets with life 'of more than a period. of

twelve months only. The items below this amount and consumable within a year

should.be-treated as revenue expenditure;

iii. to recognise and measure assets.acquired-wlthoutincurring expenditure; e.g. for land

received free as gift, it will b~enecessaryto-creete a 'capitalreserV'~ head' and depict

the assetata rtowinal value ofRe 11;

iv. assets hitherto being recognized as revenue expenditure e.g., furniture & fixtures

and computers, to be recognized as capital expenditure;

v. the classification depicted in paragraph 7 for the Fixed Asset Register should be in

accordance with the extant PUA in this Statement. It is recommended that as far as

possible the PUA should match the classification of assets suggested in paragraph

7;

vi. to bring in the principle of de-recognitionto the government accounts;

vii. to require Disclosures as specified in paragraph 11above in the Statement.

17

Annexure 1: Fixed Assets Register in the Field Unit

~ i: 0o 0<Il o..::Z.",

~ :~~'!:l

-~~ 0o'l:!IJ4 -< c:""' ~090en ~ ~'" ..80 Q (/ls

0._

~IO'... ,.,. t fa 'ok .~0§ "g ..0 ~ ~

.~ ~ § ]. ., -cq o.~,S c: fA "'"'sO I:: 8 0 ..;.

0 e:,. 6 ..2 qsll -e '.gj

~ § '-a .;.:3 0;§".~ ,0 ~.~

c:OJ:! 0.=:~ ,..J os '..:: ..... 0

'~1s g~

0 '" ~.

8'- ,..J 'a ;:J .8<~ 4> ;:J 166- ....'08 a ca~

..0

i ~ t>I)...,.'Ejz ~ 0)0.0

3 4 5 6 7 8 9 101 2 11

..,M .~ ~0) ~ta . .~ o

'~ "! m ~~

...... c:§ M 0, "0s ~ .,8';' "0

.-8 ~ § ~ ~

1., ,5~.

0.~. §

0. ca "0 ],~ p:l '0;"0 t>I) §'.., oS0) ;:;~ s

..... [i0......,0u12 13"'(10 14 15 16

+11-12)

I. Land

II. Bllildings

JII. InfrastructureAssetsIV. Machinery

V. FurnitureFixtures and fittings

VI. Ml)tor Vehicles

VII. Equipment......

VIII. ElectricalI~$taUations andEquipmentIX; Heritage Assets

X. Intangible Assets

XI. Other fixedassets'

*InMetric Systemwherever applicable.Notes:1. The format is indicative only, shOWingthe minimum requirements. Thus, sub-classesmay be added under

tbe above classes e.g. under :SuUdings.sub-classes of 'Residential' and 'Non-residential' can be disclosedas per the requirements of the entity. The entities also retain the fleXibilityof adding columns as per tbeirrequirement.

2, All assets of strategic nature should.be di$ciosedas per the ex-tantgovernment policy.3. The Object Heads in the extant DFPR should have a, direct concordance with the classes offixed assets as

far as possible.4. Assets ready for use but remllinmg·unllsedmay be ~dic(lted in the remarks column.5. Extent of completion 'Ofverification of assets should be certified in the fixed assets register annually.6. Derecognition of assets during the year shotdd be depicted in the relevant column along with sanction

number.7. Column numbers 14, 15& 16 are for additional infonnation only.

18

Annexure 2: Consolidated Fixed Asset Register at the Department/Ministry/State Level

'i:'..~

i!< ~.... .= "0= .... ,Q,)Q,) i c:I) .~a c ~ tf) tf)...; ....Q,) ...... e = e ... ,..; Q.o:I "1:1 (J 'tt"I tt"I ...... :I f :::::,(II = "0 C =.... Q,)

<II .; ~ = e uQ,) ~ ~.... ,(11 Q;. .... <II ~'" .... G.l (II ell< ...e (J 1:1 G.l Go>

-="0'.... C :I rn U .. .>."0 .:s s c:> = = "0

',Q,) -= Q;. 'ell :I =.)'o! ell 1:1 .~ "; c:> ] ,101~'

;:i;) ,.Q .s a ....."0 = ........ CIl ,., ell f.... 1:1 ... ....= eoI 1::1 = = 011 "0 =,II> ;.. ..f ·s 0 = .S -; :I

.", ,.!j e Q,) ~ c:> II) Q;. 0 e'" ',~ ... Q;. e e :I E0 "0 0 ~<:> 0 -< < j;) -<1 2 3 4 5 6"" 7 8 9

(3+4-5)

I.. Land

II.Buildi~gsIII. .InfrastructureAssets:

Yo .···li"urI!.itur~Fixturesand fiffiu2$VI. MQtor VehiclesVII, equipm~ntVIII. ElectricalInstallati6ilS andEquiPDterit

IX. Heritage ,.\ssets

X. IIt'taJigibleAssets

XI,'Other f'lXed assets

TOTAL

*In Metric System wherever applicabl~.

No~e:

1. This register is compiled from the Field Level Asset Registers. Il1dividuala'ssetsabove,Rs. 2Lakhs 0t111.0reshould. only be disclosed separately.

Z. In prder to capture all assets below Rs 2 lakhs~ listed in the Fiel,d Level As~et Registers, asllP-class, 'Others'. shqutd be created under each' class for clubbing such assets at the level ofcOlIlpilation.

3. Column 1, 8~&9 are for additional information only_4. Assets ready for uSebuttemaining unused shotUdbe indicated in the Remarks column;

19

....Annexure 3: Statement on Capital Expenditure for Acquisition of Fixed Assets

(for inclusion in the annualFinance Accounts)

Capital Opening balance as Additions during the year Closing balance atExpenditure on 01.04...... 31.03.•.Head as per theextant PUA(Object Heads)

1 2 3= (1+2)

TOTAL

20