igate investors analysts day

TRANSCRIPT

May 4, 2012 Proprietary and Confidential 0

iGATE Corporation 2012 Investor/Analyst Day

May 4, 2012 Proprietary and Confidential 1

Agenda

Time

2:00-2:05 Introduction

2:05-2:45 Phaneesh Murthy, CEO

2:45-3:05 David Kruzner, EVP and Co-Head of Consulting & Solutions

3:05-3:25 Sean Narayanan, EVP and Chief Delivery Officer

3:25-3:35 Break

3:35-3:55 Satish Joshi, EVP and Head of Product and Engineering Solutions

3:55-4:15 Srinivas Kandula, EVP and Head of Human Resources

4:15-4:35 Sujit Sircar, EVP and Chief Financial Officer

4:35-4:40 CEO Summary

4:40-4:55 Break

4:55-5:50 Q&A Session

5:50 - 7:00 Management Mixer

May 4, 2012 Proprietary and Confidential 2

Safe Harbor Statement

• The following presentations will contain forward-looking statements that reflect management’s current view, projections and estimates regarding, but not limited to, our financial and growth projections as well as statements concerning our plans, strategies, intentions and beliefs relating to our business and the markets in which we operate. These statements are based on information currently available to us, and we assume no obligation to update these statements as circumstances change.

• There are a number of risks and uncertainties that could cause actual events to differ materially from these forward-looking statements. These risks include, but are not limited to, general economic conditions, the level of market demand for our services, the highly-competitive market for the types of services that we offer, market conditions that could cause our customers to reduce their spending for our services, our ability to create, acquire and build new businesses and to grow our existing businesses, our ability to attract and retain qualified personnel, currency fluctuations and market conditions in India and elsewhere around the world, and other risks not specifically mentioned herein but those that are common to industry.

• The following presentation contains non-GAAP financial measures as defined by the Securities and Exchange Commission. Reconciliations of these non-GAAP measures to their comparable GAAP measures are available on the company’s website at www.igate.com. These non-GAAP measures should only be used to evaluate iGATE's results of operations in conjunction with the corresponding GAAP measures, and should be considered supplemental in nature, and not as a substitute for or superior to GAAP results.

May 4, 2012 Proprietary and Confidential 3

PHANEESH MURTHY Chief Executive Officer

iGATE Corporation Value creation through differentiated business model

May 4, 2012 Proprietary and Confidential 4

Agenda

Outsourcing Industry Overview

iGATE Overview

Acquisition of Patni and Successful Integration

Growth Strategy - Investing in Our Future

Summary

May 4, 2012 Proprietary and Confidential 5

Global Trends Details

Macro economic and demographic trends

World GDP growth for 2011 and 2012 estimated at 2.7 percent and 2.5 percent

Shifting centres of economic activity – GDP of Asia and Europe will converge

Working age population shrinking is key

Social and environmental trends

Increased internet and mobile connectivity transforming the way people live and interact

Increasing consumption and associated supply gap in key natural resources (e.g. oil, water) creating need for resource efficient and climate change solutions

Business and technology trends

Buyers are moving towards integrated technology and operations outsourcing

Shift in industry structures and higher regulatory control

Corporate boundaries being redefined (e.g. open innovation, extended supply chain)

Technology radically transforming the way traditional corporations and governments function

Opportunities Developed markets are still attractive from

cost rationalization perspective Rise of largely untapped market segments Geographies: India and China, US is still

huge market Verticals: Public sector, Healthcare Customer Segments: Second wave of

outsourcing

Risks

Shift in existing market segments driven by Cannibalisation of existing services (e.g.

SaaS replacing production support) Spend consolidation Automation

Regulatory control in source markets, hence slowdown in adoption

Prevailing global megatrends present new opportunities and risks for the industry

Outsourcing Industry Overview

May 4, 2012 Proprietary and Confidential 6

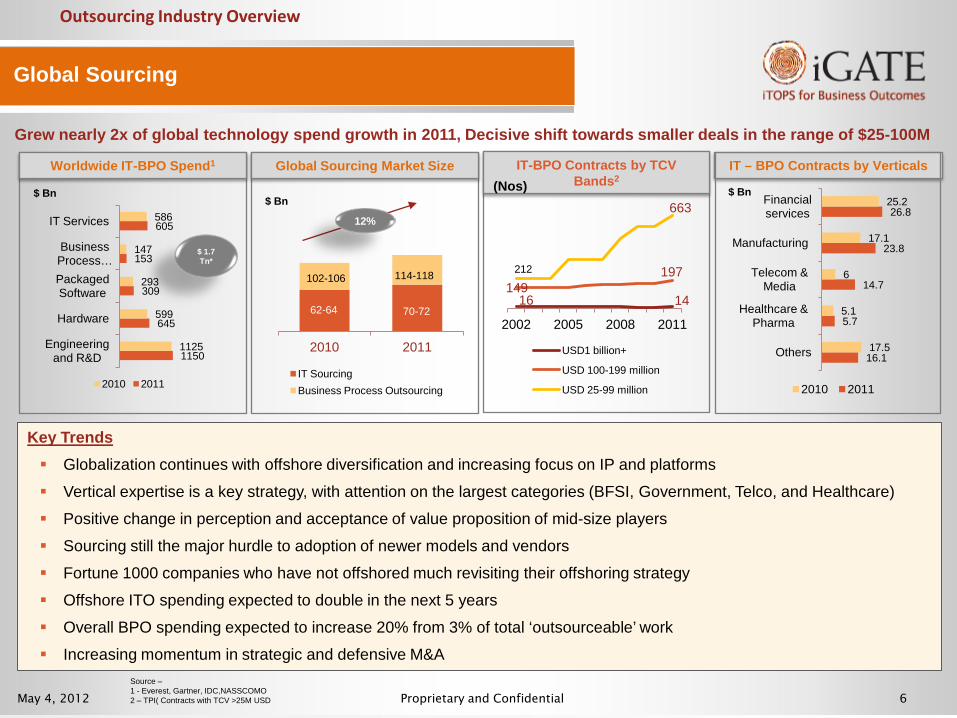

1150

645

309

153

605

1125

599

293

147

586

Engineering and R&D

Hardware

Packaged Software

Business Process …

IT Services

2010 2011

$ 1.7 Tn*

Worldwide IT-BPO Spend1

$ Bn

Global Sourcing Market Size

$ Bn

62-64 70-72

2010 2011

IT Sourcing Business Process Outsourcing

102-106 114-118

12%

IT-BPO Contracts by TCV Bands2

16 14 149

197 212

663

2002 2005 2008 2011

USD1 billion+

USD 100-199 million

USD 25-99 million

(Nos)

16.1

5.7

14.7

23.8

26.8

17.5

5.1

6

17.1

25.2

Others

Healthcare & Pharma

Telecom & Media

Manufacturing

Financial services

2010 2011

IT – BPO Contracts by Verticals

$ Bn

Grew nearly 2x of global technology spend growth in 2011, Decisive shift towards smaller deals in the range of $25-100M

Key Trends Globalization continues with offshore diversification and increasing focus on IP and platforms

Vertical expertise is a key strategy, with attention on the largest categories (BFSI, Government, Telco, and Healthcare)

Positive change in perception and acceptance of value proposition of mid-size players

Sourcing still the major hurdle to adoption of newer models and vendors

Fortune 1000 companies who have not offshored much revisiting their offshoring strategy

Offshore ITO spending expected to double in the next 5 years

Overall BPO spending expected to increase 20% from 3% of total ‘outsourceable’ work

Increasing momentum in strategic and defensive M&A

Global Sourcing

Source – 1 - Everest, Gartner, IDC,NASSCOMO 2 – TPI( Contracts with TCV >25M USD

Outsourcing Industry Overview

May 10, 2012 Proprietary and Confidential 7

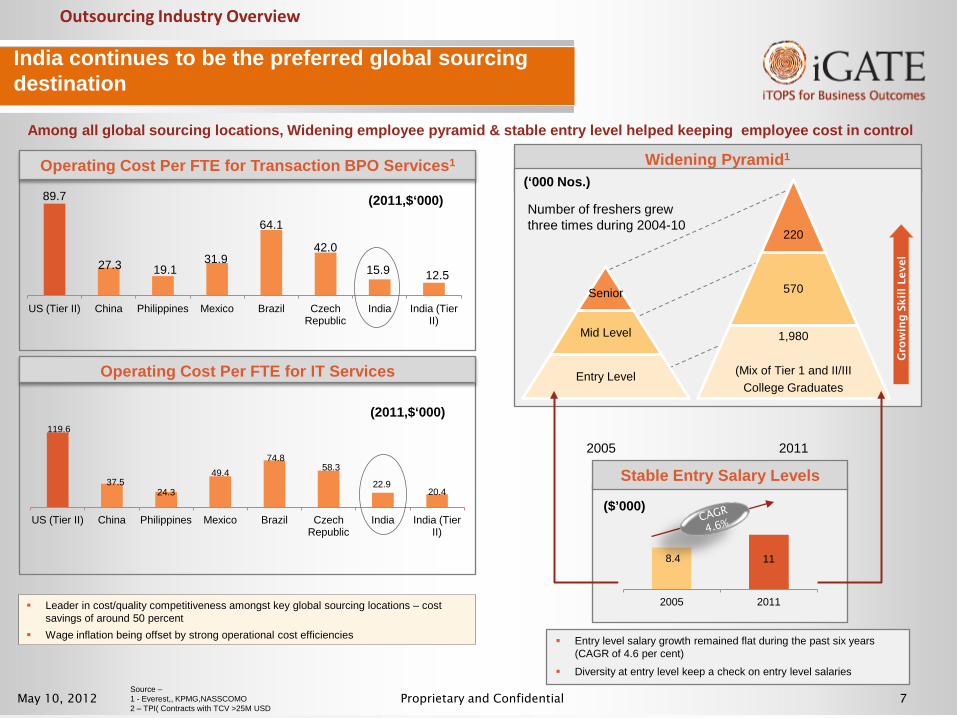

89.7

27.3 19.1 31.9

64.1

42.0

15.9 12.5

US (Tier II) China Philippines Mexico Brazil Czech Republic

India India (Tier II)

Operating Cost Per FTE for Transaction BPO Services1

(2011,$‘000)

119.6

37.5 24.3

49.4 74.8

58.3

22.9 20.4

US (Tier II) China Philippines Mexico Brazil Czech Republic

India India (Tier II)

Operating Cost Per FTE for IT Services

(2011,$‘000)

Leader in cost/quality competitiveness amongst key global sourcing locations – cost savings of around 50 percent

Wage inflation being offset by strong operational cost efficiencies

Widening Pyramid1

8.4 11

2005 2011

($’000)

Stable Entry Salary Levels

Number of freshers grew three times during 2004-10

Senior

Mid Level

Entry Level

220

570

1,980

(Mix of Tier 1 and II/III College Graduates

(‘000 Nos.)

2005 2011

Gro

win

g S

kil

l Level

Among all global sourcing locations, Widening employee pyramid & stable entry level helped keeping employee cost in control

India continues to be the preferred global sourcing destination

Entry level salary growth remained flat during the past six years (CAGR of 4.6 per cent)

Diversity at entry level keep a check on entry level salaries Source – 1 - Everest,, KPMG,NASSCOMO 2 – TPI( Contracts with TCV >25M USD

Outsourcing Industry Overview

May 4, 2012 Proprietary and Confidential 8

Maturity

Shared, Managed Services

Business Tech. Mgmt.

Monetisation of Assets/Platforms

SaaS

Cloud, Mobility Social

Agile Methodology

Verticalised CoEs

Pay-per-use, Risk and Reward Models

Verticalisation Innovation Transformation

Shared, Managed Services

SLA-Driven

Agile Methodology

Cloud, Platform Solutions

Test Labs, CoEs

Pay-per-use

Differentiation

Asset-Lite

Shared, Services

Resources Sharing

Test Labs

Emergence of Managed Services

Process Excellence

Asset-Heavy

Dedicated/ Captive Model

Time and Material

Staff Augmentation

Labour Arbitrage

Shift to Managed Services Model

Shift to “Pay per use” Model

<2004 2004-2007 2007-2009 2009-2012

Companies are moving towards business outcomes

Valu

e

Business Outcome pricing is rare today but is increasingly the model of choice. In Forrester’s Enterprise IT Services Survey, approximately 25% of firms stated moving to output-based pricing models as a critical or high priority –

Forrrester in Business Outcomes based pricing models drive results in Packaged application Implementations- April 2010

Outsourcing Industry Overview

May 4, 2012 Proprietary and Confidential 9

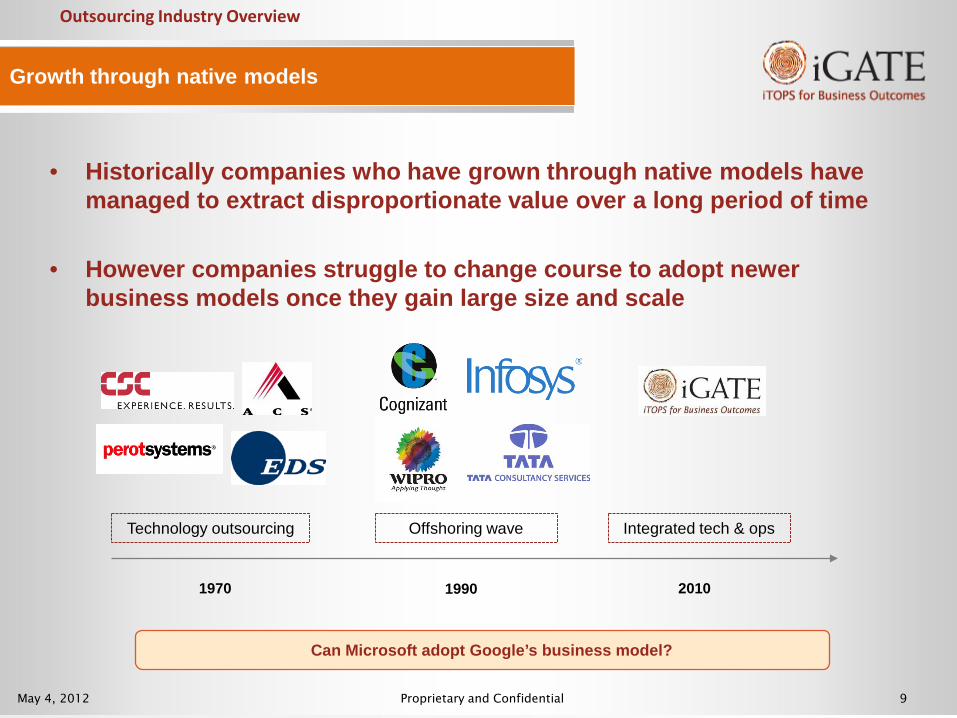

Growth through native models

• Historically companies who have grown through native models have managed to extract disproportionate value over a long period of time

• However companies struggle to change course to adopt newer business models once they gain large size and scale

1990 1970 2010

Can Microsoft adopt Google’s business model?

Offshoring wave Integrated tech & ops Technology outsourcing

Outsourcing Industry Overview

May 4, 2012 Proprietary and Confidential 10

Agenda

Outsourcing Industry Overview

iGATE Overview

Acquisition of Patni and Successful Integration

Growth Strategy - Investing in Our Future

Summary

May 4, 2012 Proprietary and Confidential 11

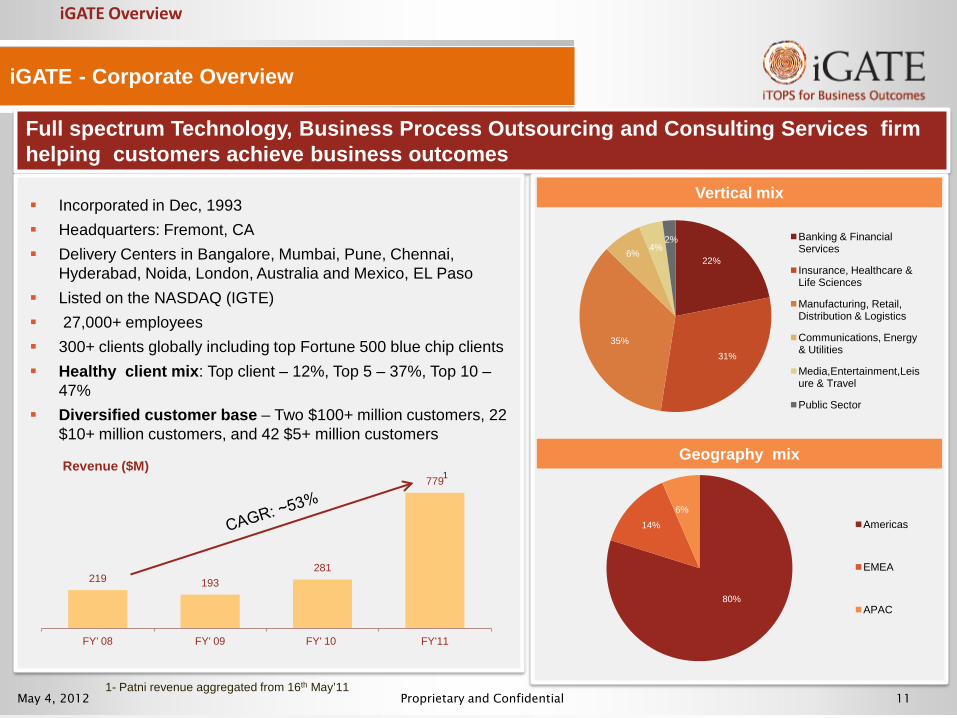

iGATE - Corporate Overview

Full spectrum Technology, Business Process Outsourcing and Consulting Services firm helping customers achieve business outcomes

Vertical mix

Geography mix

22%

31% 35%

6% 4% 2% Banking & Financial

Services

Insurance, Healthcare & Life Sciences

Manufacturing, Retail, Distribution & Logistics

Communications, Energy & Utilities

Media,Entertainment,Leisure & Travel

Public Sector

80%

14%

6% Americas

EMEA

APAC

Incorporated in Dec, 1993 Headquarters: Fremont, CA Delivery Centers in Bangalore, Mumbai, Pune, Chennai,

Hyderabad, Noida, London, Australia and Mexico, EL Paso Listed on the NASDAQ (IGTE) 27,000+ employees 300+ clients globally including top Fortune 500 blue chip clients Healthy client mix: Top client – 12%, Top 5 – 37%, Top 10 –

47% Diversified customer base – Two $100+ million customers, 22

$10+ million customers, and 42 $5+ million customers

219 193 281

779

FY' 08 FY' 09 FY' 10 FY'11

Revenue ($M)

iGATE Overview

1- Patni revenue aggregated from 16th May’11

1

May 4, 2012 Proprietary and Confidential 12

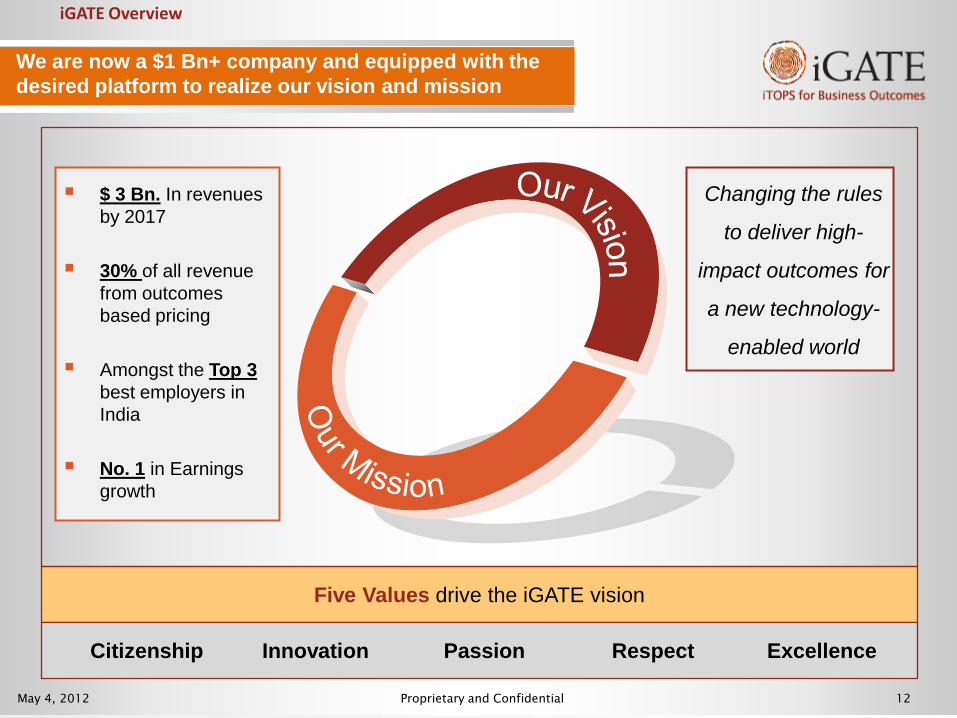

We are now a $1 Bn+ company and equipped with the desired platform to realize our vision and mission

Five Values drive the iGATE vision

Citizenship Innovation Passion Respect Excellence

Changing the rules

to deliver high-

impact outcomes for

a new technology-

enabled world

$ 3 Bn. In revenues by 2017

30% of all revenue from outcomes based pricing

Amongst the Top 3 best employers in India

No. 1 in Earnings growth

iGATE Overview

May 4, 2012 Proprietary and Confidential 13

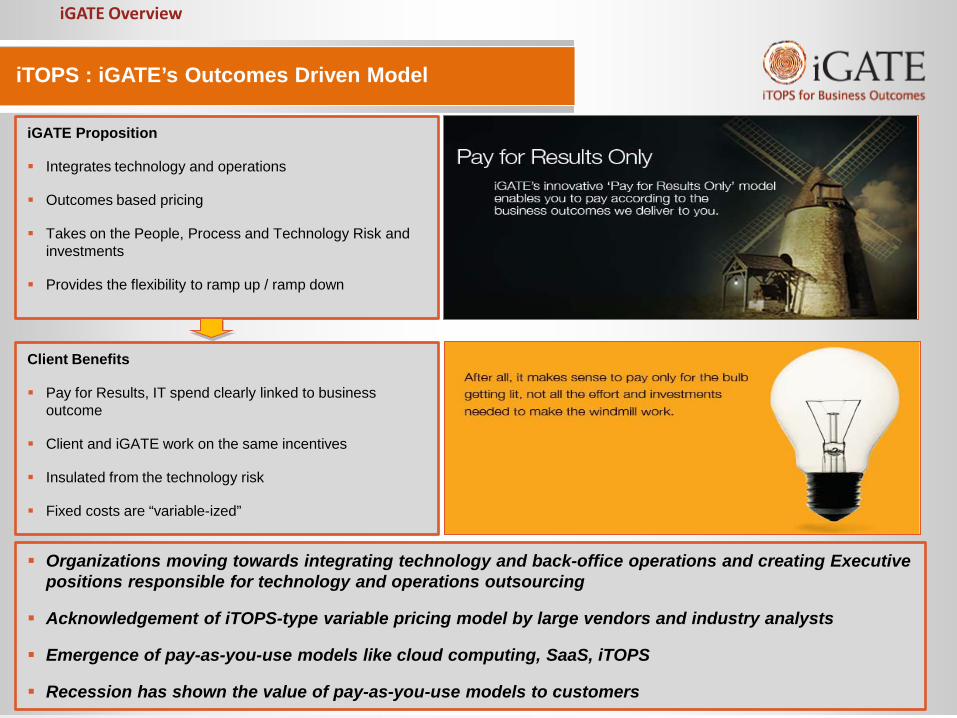

iTOPS : iGATE’s Outcomes Driven Model

iGATE Proposition

Integrates technology and operations

Outcomes based pricing

Takes on the People, Process and Technology Risk and investments

Provides the flexibility to ramp up / ramp down

Client Benefits

Pay for Results, IT spend clearly linked to business outcome

Client and iGATE work on the same incentives

Insulated from the technology risk

Fixed costs are “variable-ized”

Organizations moving towards integrating technology and back-office operations and creating Executive positions responsible for technology and operations outsourcing

Acknowledgement of iTOPS-type variable pricing model by large vendors and industry analysts

Emergence of pay-as-you-use models like cloud computing, SaaS, iTOPS

Recession has shown the value of pay-as-you-use models to customers

iGATE Overview

May 4, 2012 Proprietary and Confidential 14

Shared Services Operating Model Value Proposition

Repeatable iTOPS Solutions across multiple clients

Thought Leadership

Over-the-horizon

Intellectual Property (IP) Integrated

technology platform Next-Gen process

re-invention/Lean Six Sigma Deep domain and

process expertise

Transformational Impact

Repeatable output Predictable unit cost Shared Operational risk

management Shared business risk

through partnership Low switching cost

On-Demand Platforms

Scalable talent &

capabilities in an on-demand solutions Embedded agility Plug-and-play

simplicity Engaged talent for

continuous improvement Transparent cost

structure

Outcomes-based Engagements

Outcomes-based

pricing Billed on realized

outcomes Lower transaction

costs via the ‘Cloud’ Reduced Capex with

dynamic capacity allocation

Committed to deliver the highest order of value

iGATE Overview

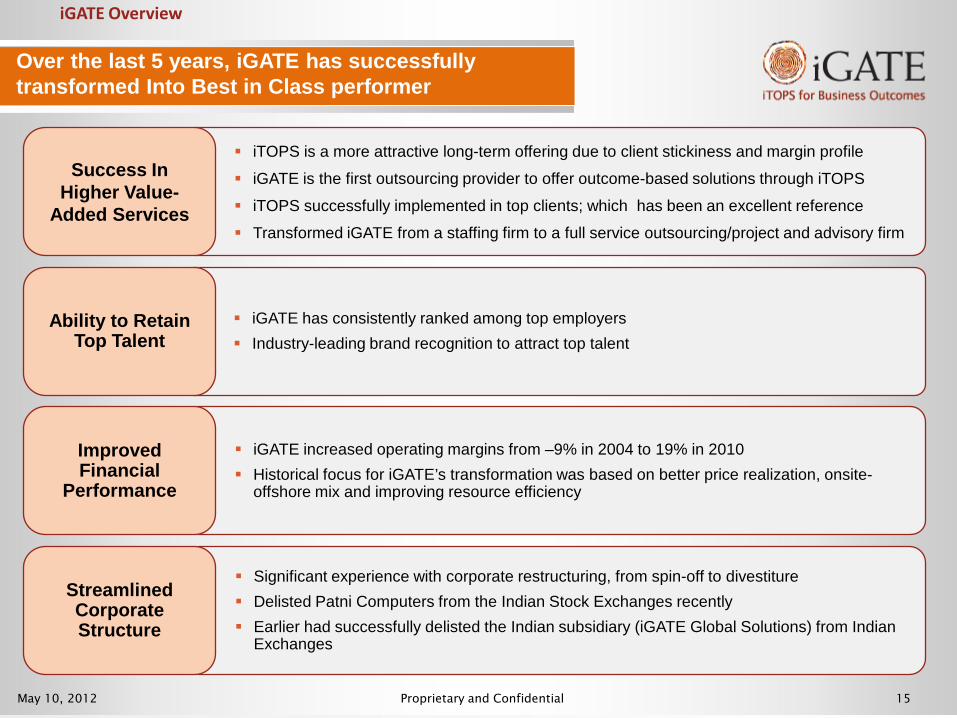

May 10, 2012 Proprietary and Confidential 15

Over the last 5 years, iGATE has successfully transformed Into Best in Class performer

iTOPS is a more attractive long-term offering due to client stickiness and margin profile

iGATE is the first outsourcing provider to offer outcome-based solutions through iTOPS

iTOPS successfully implemented in top clients; which has been an excellent reference

Transformed iGATE from a staffing firm to a full service outsourcing/project and advisory firm

Success In Higher Value-

Added Services

iGATE has consistently ranked among top employers Industry-leading brand recognition to attract top talent

Ability to Retain Top Talent

iGATE increased operating margins from –9% in 2004 to 19% in 2010 Historical focus for iGATE’s transformation was based on better price realization, onsite-

offshore mix and improving resource efficiency

Improved Financial

Performance

Significant experience with corporate restructuring, from spin-off to divestiture Delisted Patni Computers from the Indian Stock Exchanges recently Earlier had successfully delisted the Indian subsidiary (iGATE Global Solutions) from Indian

Exchanges

Streamlined Corporate Structure

iGATE Overview

May 4, 2012 Proprietary and Confidential 16

Agenda

Outsourcing Industry Overview

iGATE Overview

Acquisition of Patni and Successful Integration

Growth Strategy - Investing in Our Future

Summary

May 4, 2012 Proprietary and Confidential 17

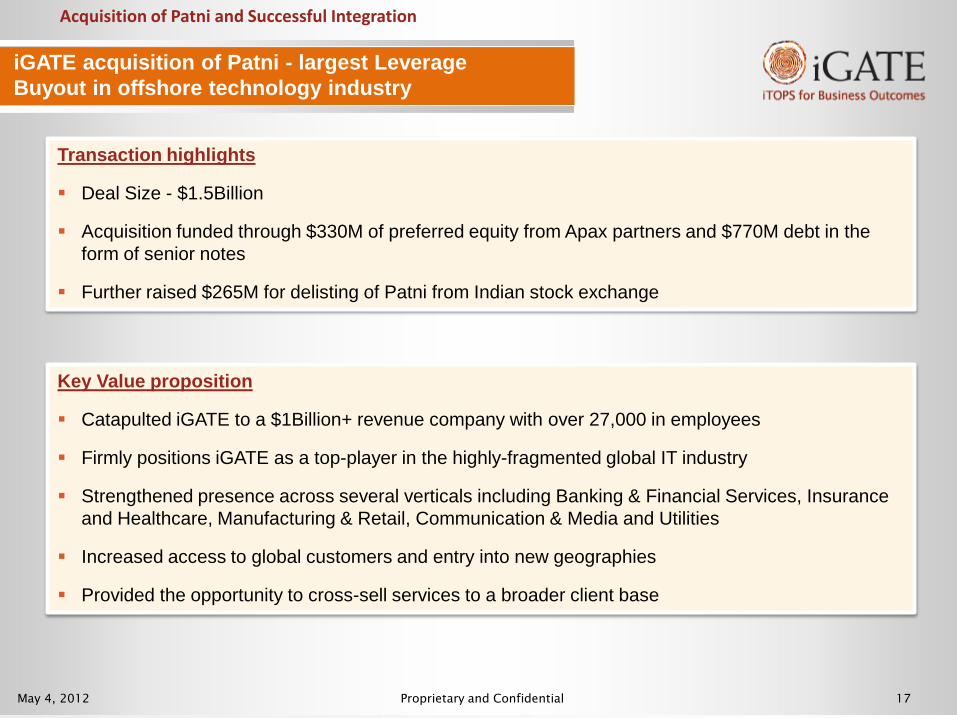

iGATE acquisition of Patni - largest Leverage Buyout in offshore technology industry

Transaction highlights

Deal Size - $1.5Billion

Acquisition funded through $330M of preferred equity from Apax partners and $770M debt in the form of senior notes

Further raised $265M for delisting of Patni from Indian stock exchange

Key Value proposition

Catapulted iGATE to a $1Billion+ revenue company with over 27,000 in employees

Firmly positions iGATE as a top-player in the highly-fragmented global IT industry

Strengthened presence across several verticals including Banking & Financial Services, Insurance and Healthcare, Manufacturing & Retail, Communication & Media and Utilities

Increased access to global customers and entry into new geographies

Provided the opportunity to cross-sell services to a broader client base

Acquisition of Patni and Successful Integration

May 4, 2012 Proprietary and Confidential 18

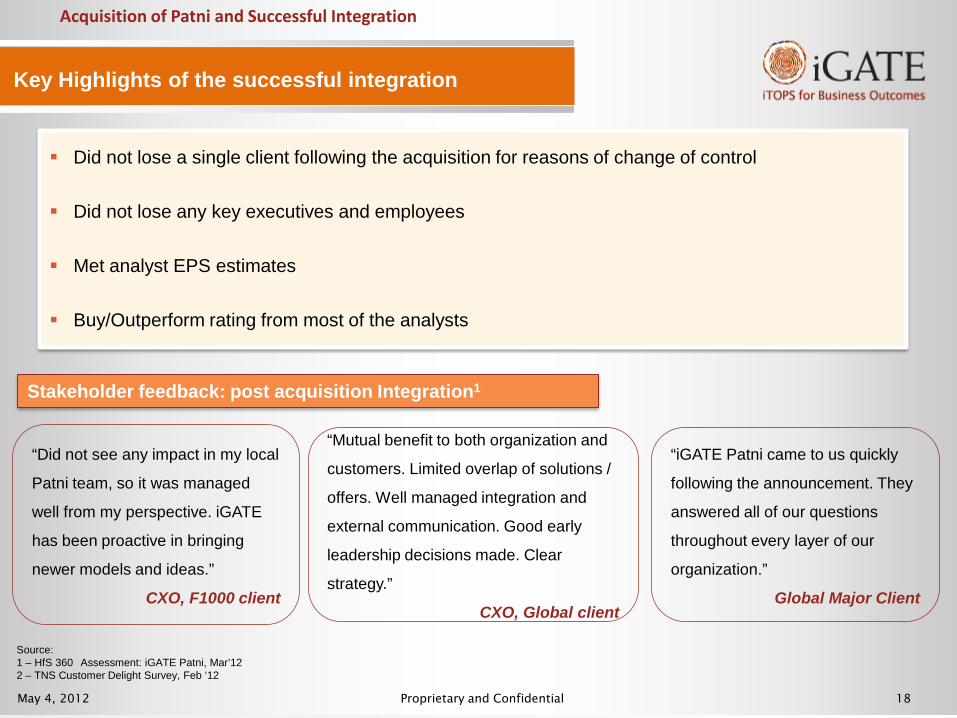

Key Highlights of the successful integration

Did not lose a single client following the acquisition for reasons of change of control

Did not lose any key executives and employees

Met analyst EPS estimates

Buy/Outperform rating from most of the analysts

Stakeholder feedback: post acquisition Integration1

“Did not see any impact in my local

Patni team, so it was managed

well from my perspective. iGATE

has been proactive in bringing

newer models and ideas.”

CXO, F1000 client

“Mutual benefit to both organization and

customers. Limited overlap of solutions /

offers. Well managed integration and

external communication. Good early

leadership decisions made. Clear

strategy.”

CXO, Global client

“iGATE Patni came to us quickly

following the announcement. They

answered all of our questions

throughout every layer of our

organization.”

Global Major Client

Source: 1 – HfS 360 Assessment: iGATE Patni, Mar’12 2 – TNS Customer Delight Survey, Feb ‘12

Acquisition of Patni and Successful Integration

May 4, 2012 Proprietary and Confidential 19

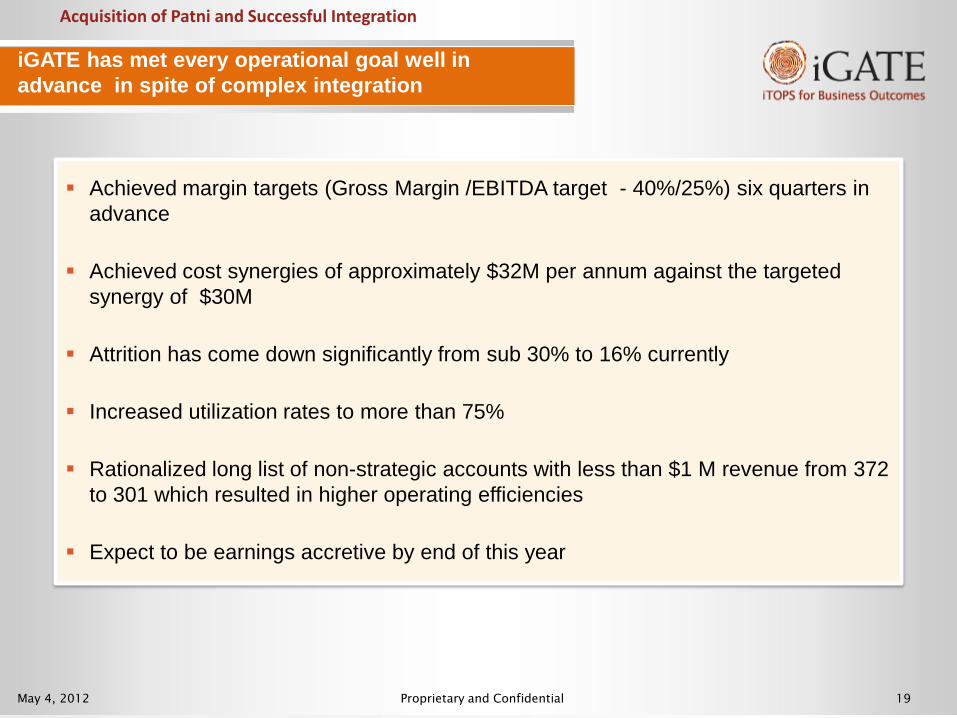

iGATE has met every operational goal well in advance in spite of complex integration

Achieved margin targets (Gross Margin /EBITDA target - 40%/25%) six quarters in advance

Achieved cost synergies of approximately $32M per annum against the targeted synergy of $30M

Attrition has come down significantly from sub 30% to 16% currently

Increased utilization rates to more than 75%

Rationalized long list of non-strategic accounts with less than $1 M revenue from 372 to 301 which resulted in higher operating efficiencies

Expect to be earnings accretive by end of this year

Acquisition of Patni and Successful Integration

May 4, 2012 Proprietary and Confidential 20

Agenda

Outsourcing Industry Overview

iGATE Overview

Acquisition of Patni and Successful Integration

Growth Strategy - Investing in Our Future

Summary

May 4, 2012 Proprietary and Confidential 21

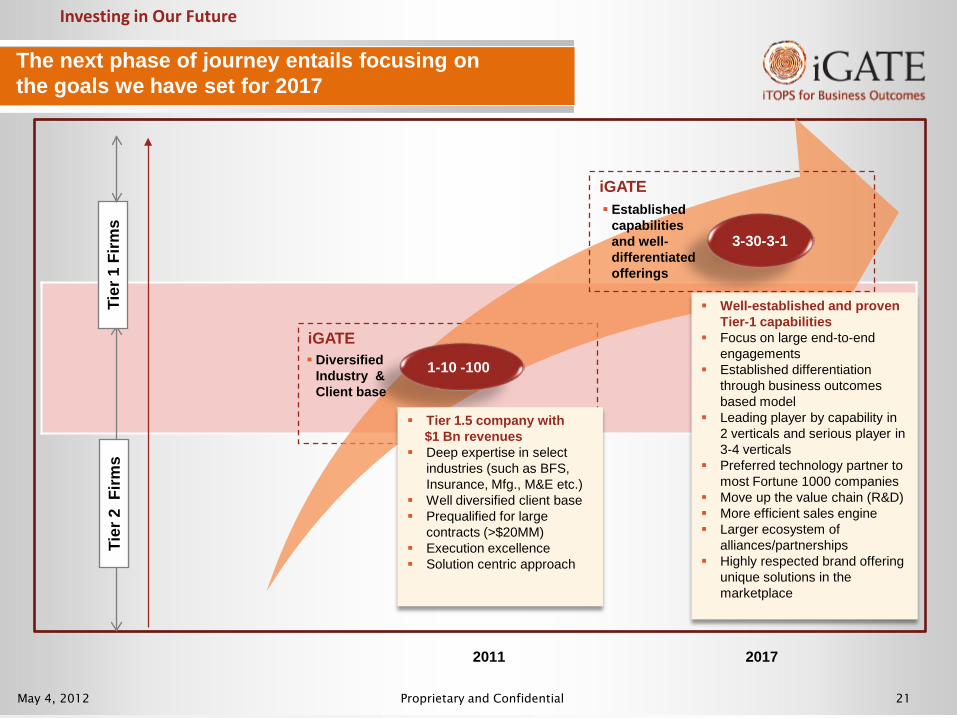

iGATE

The next phase of journey entails focusing on the goals we have set for 2017

Tier

1 F

irms

Tier

2 F

irms

2017 2011

1-10 -100

Tier 1.5 company with $1 Bn revenues

Deep expertise in select industries (such as BFS, Insurance, Mfg., M&E etc.)

Well diversified client base Prequalified for large

contracts (>$20MM) Execution excellence Solution centric approach

3-30-3-1

Well-established and proven Tier-1 capabilities

Focus on large end-to-end engagements

Established differentiation through business outcomes based model

Leading player by capability in 2 verticals and serious player in 3-4 verticals

Preferred technology partner to most Fortune 1000 companies

Move up the value chain (R&D) More efficient sales engine Larger ecosystem of

alliances/partnerships Highly respected brand offering

unique solutions in the marketplace

Diversified Industry & Client base

Established capabilities and well-differentiated offerings

Investing in Our Future

iGATE

May 4, 2012 Proprietary and Confidential 22

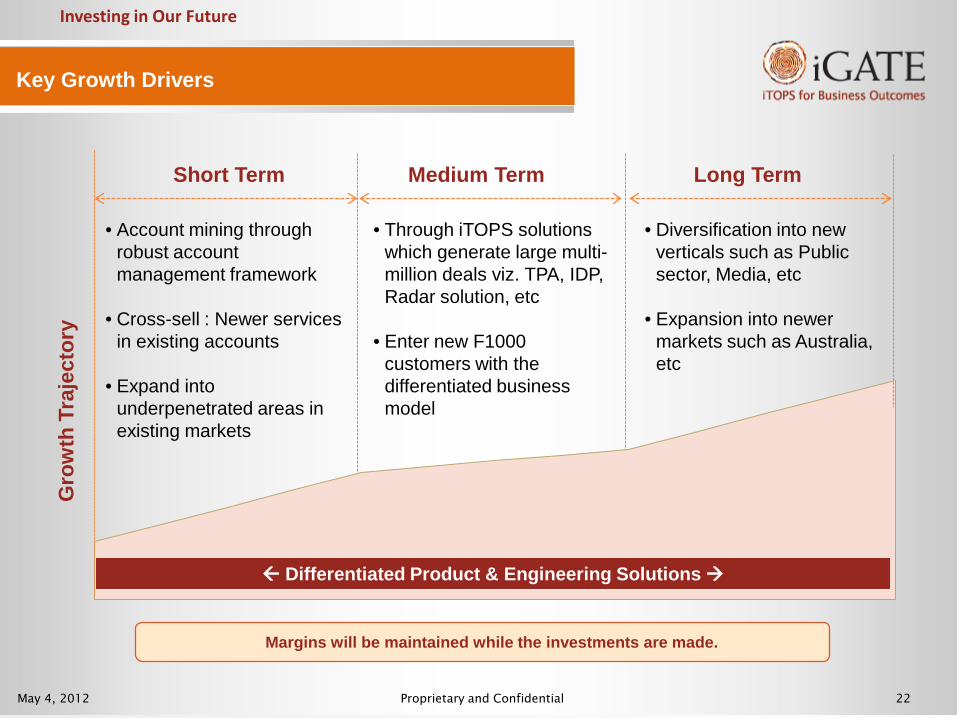

Key Growth Drivers

Investing in Our Future

• Account mining through robust account management framework

• Cross-sell : Newer services in existing accounts

• Expand into underpenetrated areas in existing markets

• Through iTOPS solutions which generate large multi-million deals viz. TPA, IDP, Radar solution, etc

• Enter new F1000 customers with the differentiated business model

Differentiated Product & Engineering Solutions

• Diversification into new verticals such as Public sector, Media, etc

• Expansion into newer markets such as Australia, etc

Short Term Medium Term Long Term

Gro

wth

Tra

ject

ory

Margins will be maintained while the investments are made.

May 4, 2012 Proprietary and Confidential 23

Agenda

Outsourcing Industry Overview

iGATE Overview

Acquisition of Patni and Successful Integration

Growth Strategy - Investing in Our Future

Summary

May 4, 2012 Proprietary and Confidential 24

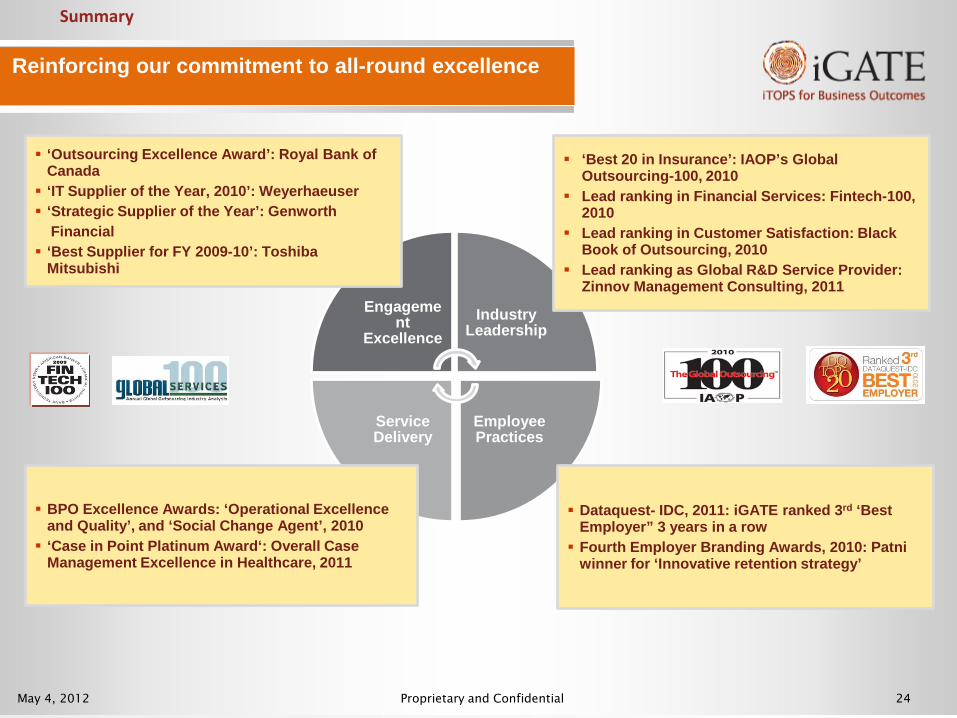

Engagement

Excellence Industry

Leadership

Employee Practices

Service Delivery

‘Outsourcing Excellence Award’: Royal Bank of Canada ‘IT Supplier of the Year, 2010’: Weyerhaeuser ‘Strategic Supplier of the Year’: Genworth Financial ‘Best Supplier for FY 2009-10’: Toshiba

Mitsubishi

‘Best 20 in Insurance’: IAOP’s Global Outsourcing-100, 2010

Lead ranking in Financial Services: Fintech-100, 2010

Lead ranking in Customer Satisfaction: Black Book of Outsourcing, 2010

Lead ranking as Global R&D Service Provider: Zinnov Management Consulting, 2011

BPO Excellence Awards: ‘Operational Excellence and Quality’, and ‘Social Change Agent’, 2010 ‘Case in Point Platinum Award‘: Overall Case

Management Excellence in Healthcare, 2011

Dataquest- IDC, 2011: iGATE ranked 3rd ‘Best Employer” 3 years in a row Fourth Employer Branding Awards, 2010: Patni

winner for ‘Innovative retention strategy’

Reinforcing our commitment to all-round excellence

Summary

May 4, 2012 Proprietary and Confidential 25

Thank You

May 4, 2012 Proprietary and Confidential 26

David Kruzner EVP and Co-Head of Consulting & Solutions

iGATE Corporation Solution & Consulting

May 10, 2012 Proprietary and Confidential 27

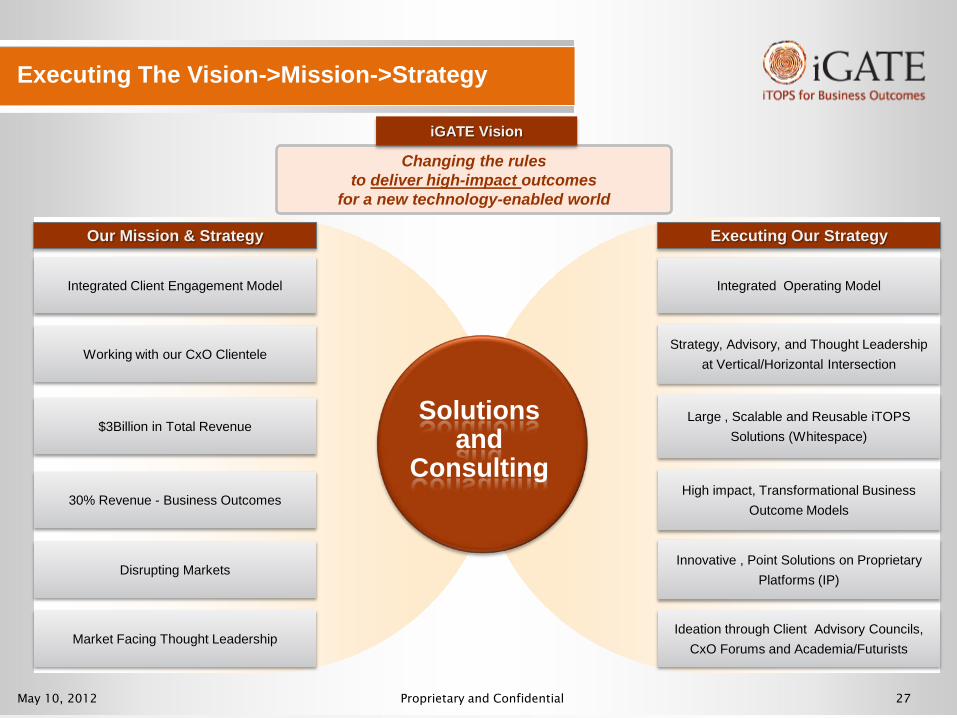

Changing the rules to deliver high-impact outcomes

for a new technology-enabled world

Executing The Vision->Mission->Strategy

iGATE Vision

Working with our CxO Clientele

$3Billion in Total Revenue

30% Revenue - Business Outcomes

Disrupting Markets

Integrated Client Engagement Model

Our Mission & Strategy

Market Facing Thought Leadership

Integrated Operating Model

Strategy, Advisory, and Thought Leadership at Vertical/Horizontal Intersection

Large , Scalable and Reusable iTOPS Solutions (Whitespace)

Innovative , Point Solutions on Proprietary Platforms (IP)

High impact, Transformational Business Outcome Models

Executing Our Strategy

Ideation through Client Advisory Councils, CxO Forums and Academia/Futurists

Solutions and

Consulting

May 10, 2012 Proprietary and Confidential 28

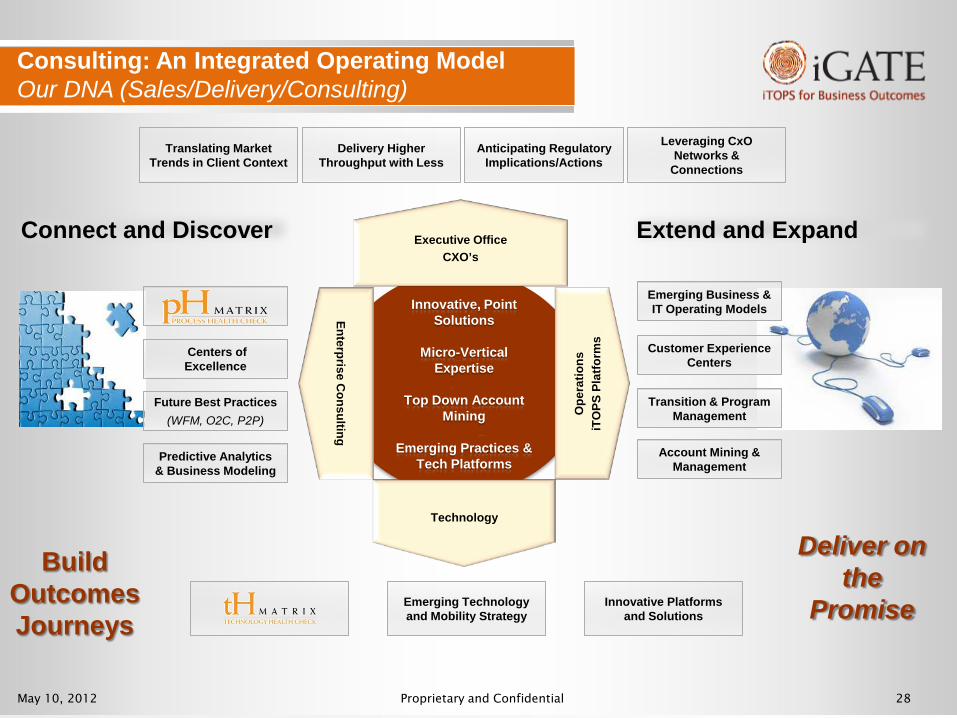

Consulting: An Integrated Operating Model Our DNA (Sales/Delivery/Consulting)

Executive Office CXO’s

Enterprise Consulting

Innovative, Point Solutions

Micro-Vertical Expertise

Top Down Account Mining

Emerging Practices & Tech Platforms

Ope

ratio

ns

iTO

PS P

latfo

rms

Technology

Centers of Excellence

Future Best Practices (WFM, O2C, P2P)

Connect and Discover Extend and Expand

Transition & Program Management

Emerging Technology and Mobility Strategy

Emerging Business & IT Operating Models

Customer Experience Centers

Predictive Analytics & Business Modeling

Account Mining & Management

Deliver on the

Promise

Build Outcomes Journeys

Delivery Higher Throughput with Less

Innovative Platforms and Solutions

Anticipating Regulatory Implications/Actions

Translating Market Trends in Client Context

Leveraging CxO Networks &

Connections

May 10, 2012 Proprietary and Confidential 29

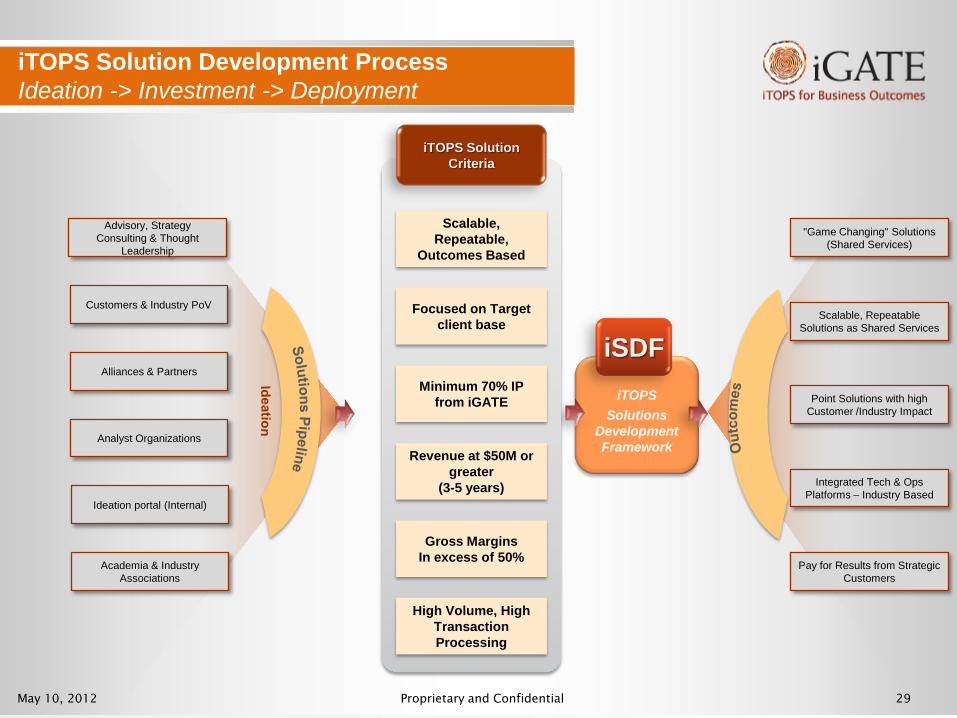

iTOPS Solution Development Process Ideation -> Investment -> Deployment

Customers & Industry PoV

Alliances & Partners

Advisory, Strategy Consulting & Thought

Leadership

Analyst Organizations

Ideation portal (Internal)

iTOPS

Solutions Development Framework

iSDF

Scalable, Repeatable,

Outcomes Based

Minimum 70% IP from iGATE

Revenue at $50M or greater

(3-5 years)

Gross Margins In excess of 50%

High Volume, High Transaction Processing

iTOPS Solution Criteria

Point Solutions with high Customer /Industry Impact

Scalable, Repeatable Solutions as Shared Services

"Game Changing" Solutions (Shared Services)

Pay for Results from Strategic Customers

Integrated Tech & Ops Platforms – Industry Based

Focused on Target client base

Academia & Industry Associations

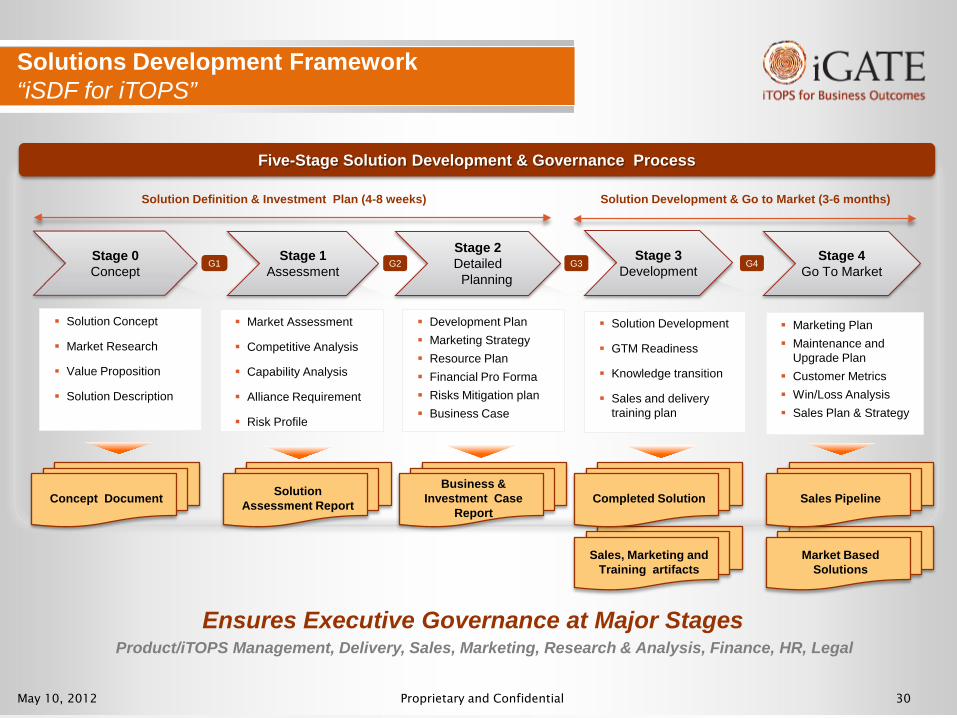

May 10, 2012 Proprietary and Confidential 30

Solution Concept

Market Research

Value Proposition

Solution Description

Market Assessment

Competitive Analysis

Capability Analysis

Alliance Requirement

Risk Profile

Development Plan Marketing Strategy Resource Plan Financial Pro Forma Risks Mitigation plan Business Case

Solution Development

GTM Readiness

Knowledge transition

Sales and delivery training plan

Marketing Plan Maintenance and

Upgrade Plan Customer Metrics Win/Loss Analysis Sales Plan & Strategy

Solutions Development Framework “iSDF for iTOPS”

Solution Definition & Investment Plan (4-8 weeks) Solution Development & Go to Market (3-6 months)

Stage 0 Concept

Stage 1 Assessment

Stage 2 Detailed

Planning

Stage 3 Development

Stage 4 Go To Market

G1 G2 G3 G4

Five-Stage Solution Development & Governance Process

Ensures Executive Governance at Major Stages Product/iTOPS Management, Delivery, Sales, Marketing, Research & Analysis, Finance, HR, Legal

Concept Document Solution Assessment Report

Business & Investment Case

Report

Sales, Marketing and Training artifacts

Market Based Solutions

Sales Pipeline Completed Solution

May 10, 2012 Proprietary and Confidential 31

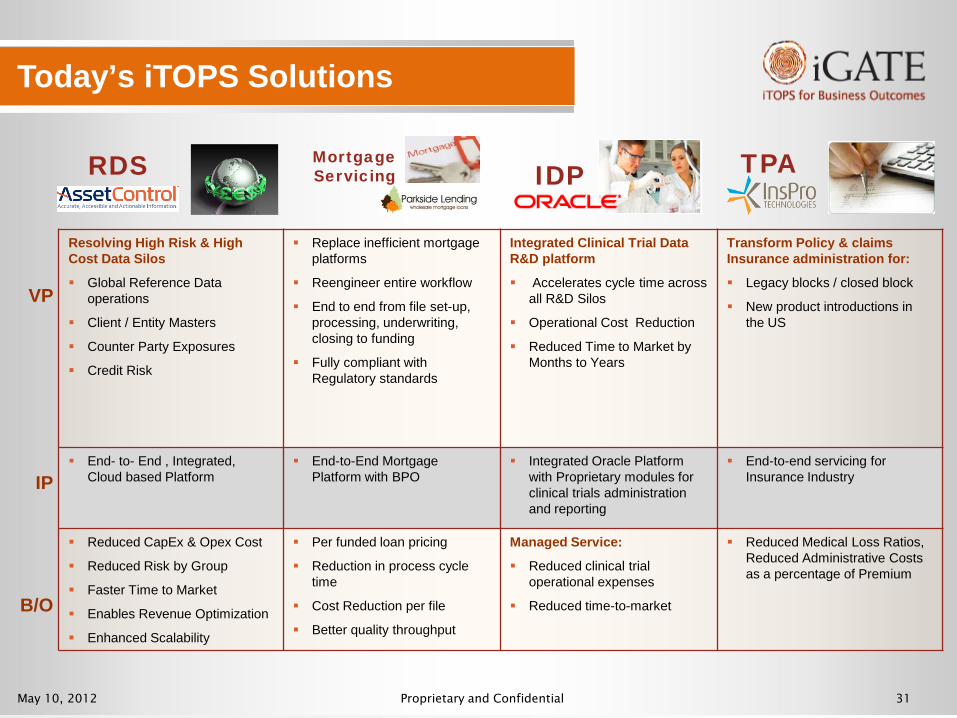

Resolving High Risk & High Cost Data Silos

Global Reference Data operations

Client / Entity Masters

Counter Party Exposures

Credit Risk

Replace inefficient mortgage platforms

Reengineer entire workflow

End to end from file set-up, processing, underwriting, closing to funding

Fully compliant with Regulatory standards

Integrated Clinical Trial Data R&D platform

Accelerates cycle time across all R&D Silos

Operational Cost Reduction

Reduced Time to Market by Months to Years

Transform Policy & claims Insurance administration for:

Legacy blocks / closed block

New product introductions in the US

End- to- End , Integrated, Cloud based Platform

End-to-End Mortgage Platform with BPO

Integrated Oracle Platform with Proprietary modules for clinical trials administration and reporting

End-to-end servicing for Insurance Industry

Reduced CapEx & Opex Cost

Reduced Risk by Group

Faster Time to Market

Enables Revenue Optimization

Enhanced Scalability

Per funded loan pricing

Reduction in process cycle time

Cost Reduction per file

Better quality throughput

Managed Service:

Reduced clinical trial operational expenses

Reduced time-to-market

Reduced Medical Loss Ratios, Reduced Administrative Costs as a percentage of Premium

Today’s iTOPS Solutions

IDP TPA RDS Mortgage Servicing

VP

IP

B/O

May 4, 2012 Proprietary and Confidential 32

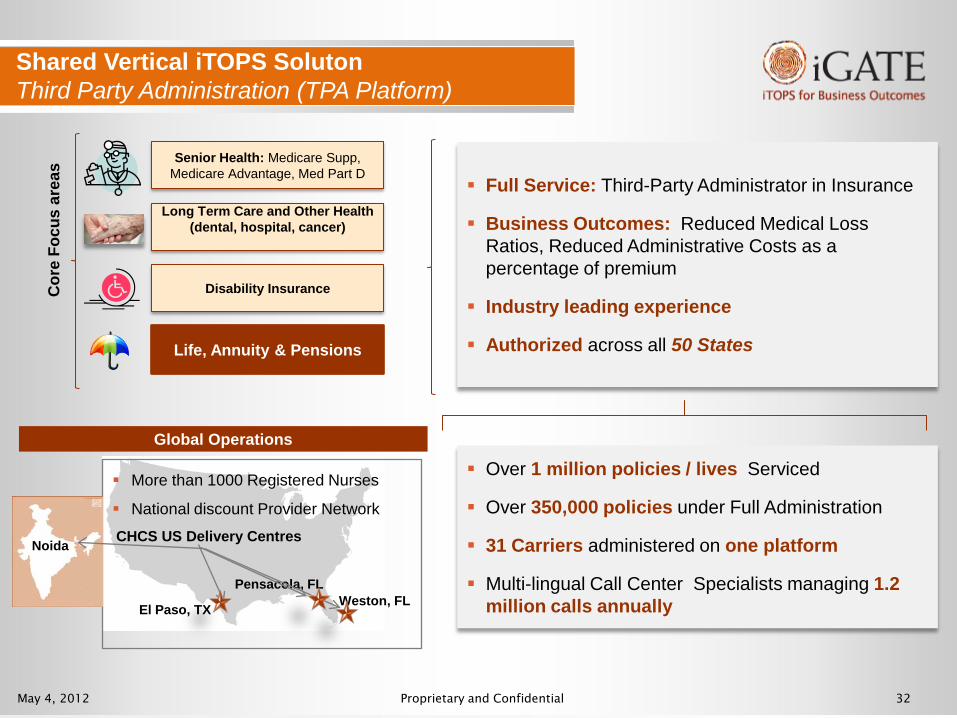

Shared Vertical iTOPS Soluton Third Party Administration (TPA Platform)

Senior Health: Medicare Supp, Medicare Advantage, Med Part D

Life, Annuity & Pensions

Disability Insurance

Long Term Care and Other Health (dental, hospital, cancer)

Cor

e Fo

cus

area

s

More than 1000 Registered Nurses

National discount Provider Network

El Paso, TX

Pensacola, FL Weston, FL

CHCS US Delivery Centres

Global Operations

Full Service: Third-Party Administrator in Insurance

Business Outcomes: Reduced Medical Loss Ratios, Reduced Administrative Costs as a percentage of premium

Industry leading experience

Authorized across all 50 States

Over 1 million policies / lives Serviced

Over 350,000 policies under Full Administration

31 Carriers administered on one platform

Multi-lingual Call Center Specialists managing 1.2 million calls annually

Noida

May 4, 2012 Proprietary and Confidential 33

Growing Existing Accounts through cross-industry thought leadership and Advisory Services to embark on client’s Outcomes journey.

Growing New Business in new accounts through trusted CXO relationships

Creating New Avenues of growth through unique, Point Solutions from our iSDF process addressing key pain points in both new and existing markets.

Innovating and Building Shared Services platforms for the future.

Key TakeAways Creating The Future…..2014 and Beyond

Solutions & Consulting is about:

2012 Market Creators

2014unique and Market Leaders

2016 Market Innovators

May 4, 2012 Proprietary and Confidential 34

Thank You

May 4, 2012 Proprietary and Confidential 35

SEAN NARAYANAN

Chief Delivery Officer

iGATE Corporation Delivering Business Outcomes

May 4, 2012 Proprietary and Confidential 36 Proprietary and Confidential 36 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 37

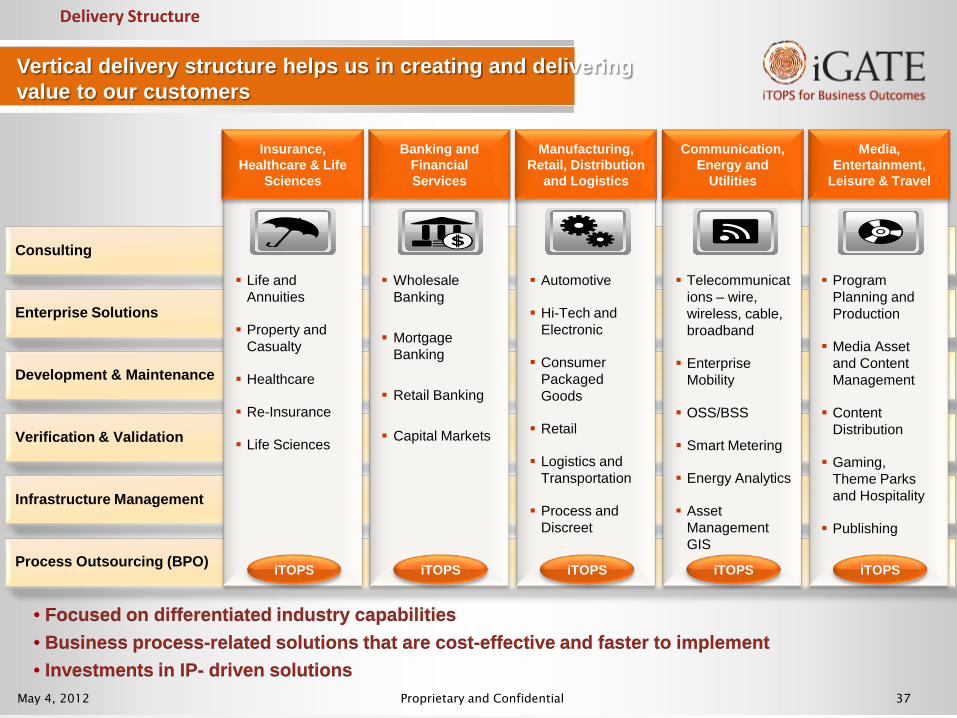

Vertical delivery structure helps us in creating and delivering value to our customers

Delivery Structure

Process Outsourcing (BPO)

Consulting

Enterprise Solutions

Development & Maintenance

Verification & Validation

Infrastructure Management

Insurance, Healthcare & Life

Sciences

Banking and Financial Services

Manufacturing, Retail, Distribution

and Logistics

Communication, Energy and

Utilities

Media, Entertainment,

Leisure & Travel

• Focused on differentiated industry capabilities • Business process-related solutions that are cost-effective and faster to implement • Investments in IP- driven solutions

Life and Annuities

Property and Casualty

Healthcare

Re-Insurance

Life Sciences

Automotive

Hi-Tech and Electronic

Consumer Packaged Goods

Retail

Logistics and Transportation

Process and Discreet

Telecommunications – wire, wireless, cable, broadband

Enterprise Mobility

OSS/BSS

Smart Metering

Energy Analytics

Asset Management GIS

Program Planning and Production

Media Asset and Content Management

Content Distribution

Gaming, Theme Parks and Hospitality

Publishing

Wholesale Banking

Mortgage Banking

Retail Banking

Capital Markets

iTOPS iTOPS iTOPS iTOPS iTOPS

May 4, 2012 Proprietary and Confidential 38

We bring our organizational capabilities together through an integrated core team for strategic customers

Delivery Structure

iTOPS

Integrated Technology & Operations –

iTOPS Manager

Research & Innovation

•Centers of Excellence •Tech. Consulting

•Research and thought leadership

Client Services •Client-centricity and

building deeper relationships

•Subject and thought leadership

Quality Process Consulting

•CMM 5, ISO 9001, Six Sigma, ITIL, Kaizen,

COPC •Independent audits

Resource Management &

Training •Cross trained multi skill

talent availability •Customized training to

meet business needs Domain Group

•Vertical specific domain Business Analysts

•Translate domain needs into Technology

Solution Design Group

•Customer centric solutions and value

proposition •Org-wide best practices

and competencies

ENTER

PRISE SYSTEM

IN

TEGR

ATION

APP

LIC

ATIO

N

DEV

ELO

PMEN

T A

ND

M

AIN

TEN

AN

CE

BUSINESS PROCESS OUTSOURCING

CONSULTING

May 4, 2012 Proprietary and Confidential 39 Proprietary and Confidential 39 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 40

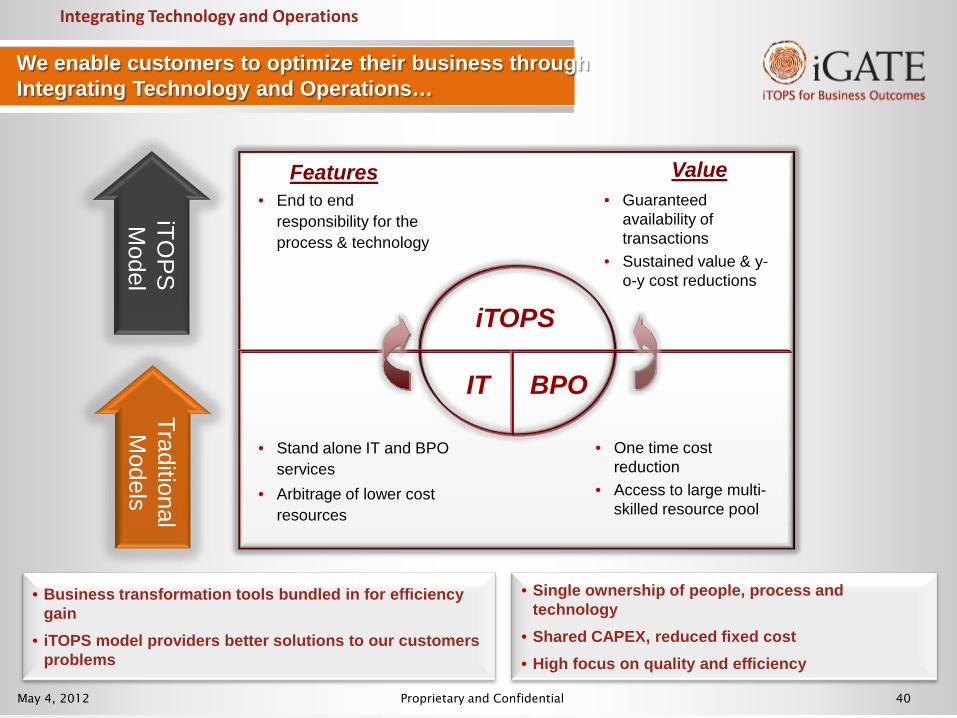

We enable customers to optimize their business through Integrating Technology and Operations…

Integrating Technology and Operations

iTOPS

Features Value • End to end

responsibility for the process & technology

• Guaranteed availability of transactions

• Sustained value & y-o-y cost reductions

IT BPO

• Stand alone IT and BPO services

• Arbitrage of lower cost resources

• One time cost reduction

• Access to large multi-skilled resource pool

iTOP

S

Model

• Business transformation tools bundled in for efficiency gain

• iTOPS model providers better solutions to our customers problems

• Single ownership of people, process and technology

• Shared CAPEX, reduced fixed cost • High focus on quality and efficiency

Traditional M

odels

May 4, 2012 Proprietary and Confidential 41

… and aligning our solutions to their business outcomes

Del

iver

y E

nabl

ers

• Development / Implementation, Reengineering / Upgrade, Testing

• Maintenance

• Process Definition and Set-up; Improvements

• Implementation/Refresh and Hosting

• Monitoring/Management

Per Invoice processed, L/C processed, Funded loan, etc.

Per Application, Report, Test Script, etc.

Per Device - Service Catalog

SaaS

Shared Risk/Reward

Business Benefits based SLA

Implement Best-in-breed Solutions – Oracle Advanced Collections, Trade Finance, Mortgage, Insurance

Increased Automation iGATE Solutions – OCR, Workflow, Document Mgmt, ePartner, Web Portal

Process Re-engineering

Delivery team rationalization - COSM Shared Services – F&A, Reporting Factory, Remote Monitoring

Business Transform

ation

Processes/Ops: F&A, Procurement, Sales Order Mgmt, Trade Finance, etc.

Business Layer

Applications Layer Custom / Packages

Infrastructure Layer

Outcome based Models

Efficiency & Integration

Business Outcome Alignment

Cocoon Model - Accelerators, Training, Quality & Resource Management

Governance Goals alignment

Talent Pool & Management iTOPS skills, High Avg. Experience, Flexible

Resourcing

Info Security ISO 27001

Project Mgmt & Control Automation, Real time tracking

Continual Improvement Six Sigma, Kaizen

Business / Technology Alliances Automation, Industry Solutions

Integrating Technology and Operations

May 4, 2012 Proprietary and Confidential 42 Proprietary and Confidential 42 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 43

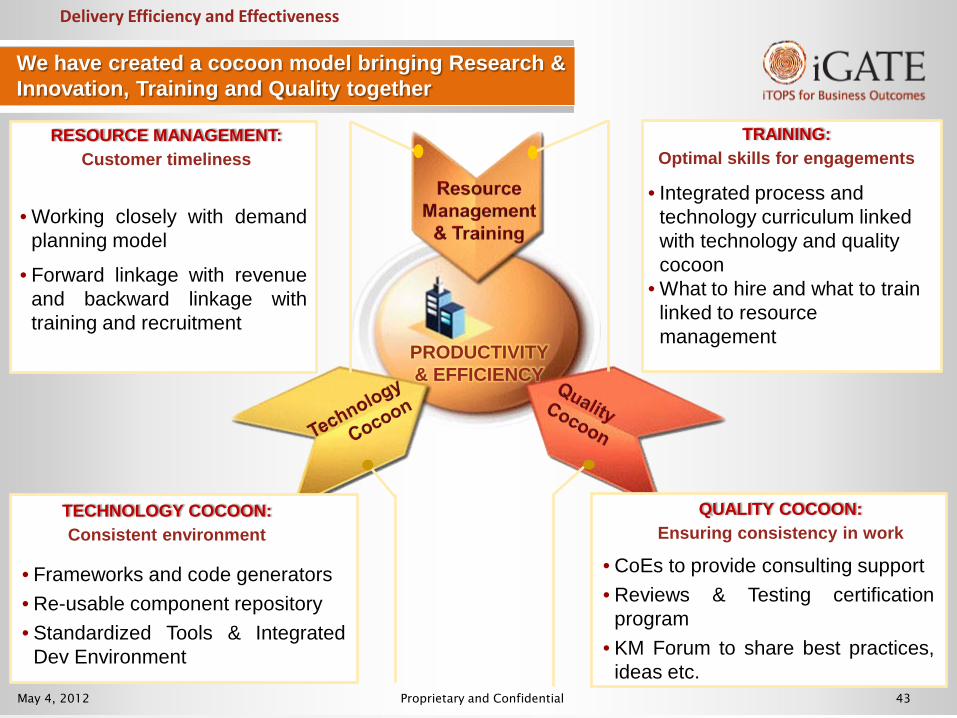

We have created a cocoon model bringing Research & Innovation, Training and Quality together

Delivery Efficiency and Effectiveness

PRODUCTIVITY & EFFICIENCY

• Integrated process and technology curriculum linked with technology and quality cocoon

• What to hire and what to train linked to resource management

• Frameworks and code generators • Re-usable component repository • Standardized Tools & Integrated

Dev Environment

• Working closely with demand planning model

• Forward linkage with revenue and backward linkage with training and recruitment

RESOURCE MANAGEMENT: Customer timeliness

TRAINING: Optimal skills for engagements

TECHNOLOGY COCOON: Consistent environment

QUALITY COCOON: Ensuring consistency in work

• CoEs to provide consulting support • Reviews & Testing certification

program • KM Forum to share best practices,

ideas etc.

May 4, 2012 Proprietary and Confidential 44

PRODUCTIVITY & EFFICIENCY

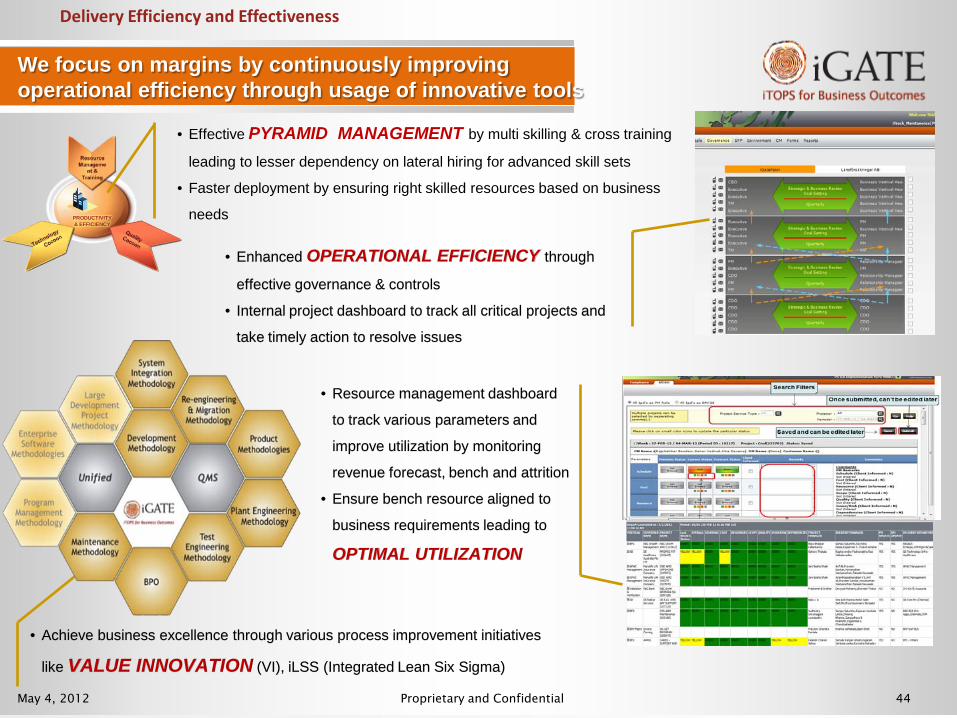

We focus on margins by continuously improving operational efficiency through usage of innovative tools

• Effective PYRAMID MANAGEMENT by multi skilling & cross training

leading to lesser dependency on lateral hiring for advanced skill sets

• Faster deployment by ensuring right skilled resources based on business

needs

• Enhanced OPERATIONAL EFFICIENCY through

effective governance & controls

• Internal project dashboard to track all critical projects and

take timely action to resolve issues

• Resource management dashboard

to track various parameters and

improve utilization by monitoring

revenue forecast, bench and attrition

• Ensure bench resource aligned to

business requirements leading to

OPTIMAL UTILIZATION

• Achieve business excellence through various process improvement initiatives

like VALUE INNOVATION (VI), iLSS (Integrated Lean Six Sigma)

Delivery Efficiency and Effectiveness

May 4, 2012 Proprietary and Confidential 45 Proprietary and Confidential 45 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 46

A host of trends imply the industry is moving towards a utility model

Market Research Led Innovation

Trend Opportunity

Emerging Trends

• Cloud Based Outsourcing

• Enterprise Mobility

• Big Data & Extreme Information

• Reduced dependence on labor by 10%-25% in the next 3-5 yrs

• Growth in Transformation and System Integration opportunities

• Mobility and Big Data to offset shrinkage in traditional ADM revenue

Enterprise Resource Planning • Resurgence in demand; shift in revenue from maintenance / upgrade to solutions / configuration / integration

BPO

• Greater adoption processes on standard platforms (like SAP/Oracle) supplemented by point solutions (where ERPs do not exist)

• Next wave of outcome based delivery

Infrastructure Management

• Services like RIM to continue to grow; significant shift likely due to

change from asset ownership to Infra as a service

Alternate ‘Offshore’ for Service Delivery

• India continues to be the hub for North Americas

• Eastern Europe as a hub for Continental Europe

• China as the hub for Japan and China

May 4, 2012 Proprietary and Confidential 47

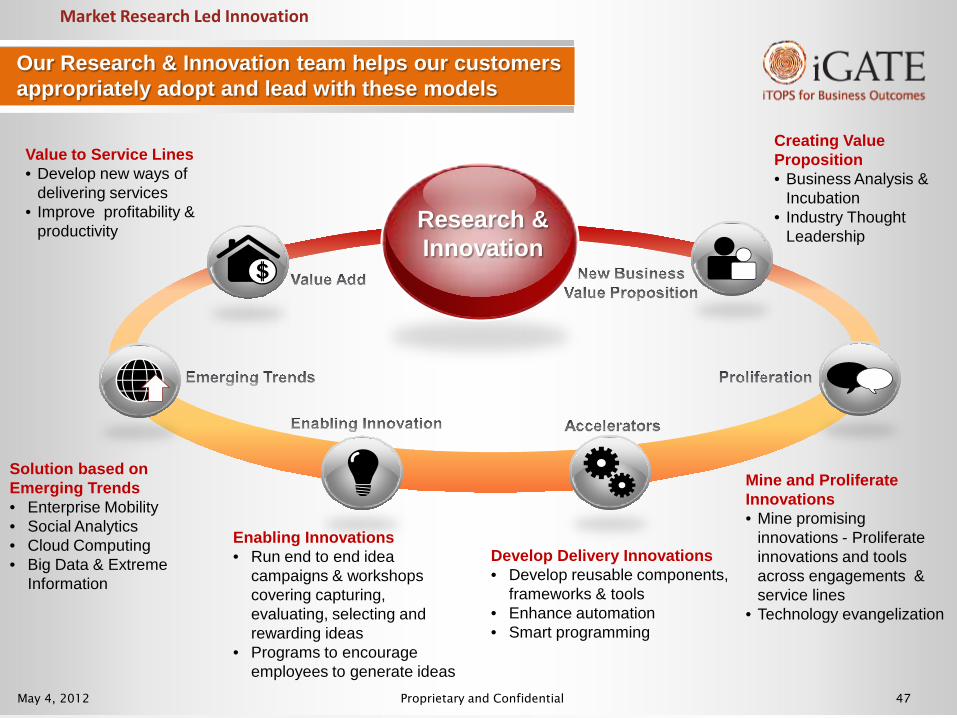

Our Research & Innovation team helps our customers appropriately adopt and lead with these models

Solution based on Emerging Trends • Enterprise Mobility • Social Analytics • Cloud Computing • Big Data & Extreme

Information

Enabling Innovations • Run end to end idea

campaigns & workshops covering capturing, evaluating, selecting and rewarding ideas

• Programs to encourage employees to generate ideas

Develop Delivery Innovations • Develop reusable components,

frameworks & tools • Enhance automation • Smart programming

Mine and Proliferate Innovations • Mine promising

innovations - Proliferate innovations and tools across engagements & service lines

• Technology evangelization

Creating Value Proposition • Business Analysis &

Incubation • Industry Thought

Leadership Research & Innovation

Value to Service Lines • Develop new ways of

delivering services • Improve profitability &

productivity

Market Research Led Innovation

May 4, 2012 Proprietary and Confidential 48 Proprietary and Confidential 48 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 49

Our services are also aligned to Business Outcomes

Customer Outcomes

Successful execution of automated test scripts

Reducing testing cycle time

Successful month/year close within defined

period

Data consolidation, reduction in latency, and

single version of the truth

Product Engineering

Services

Application Development

& Maintenance

Verification & Validation

(V&V)

Enterprise Solutions

Infrastructure Management

Services

Meeting business SLA’s for key business applications

Implementation / Refresh and Hosting - Per device maintained

Monitoring / Management - Service Catalog based;

Successfully resolved trouble call

Maintenance - Per Application

Maintained

Development, Implementation,

Reengineering, Upgrade - Per

Report

Pre defined outage limits; zero

downtimes during critical

business cycles

Business Process

Outsourcing

F&A - Per Invoice processed

Mortgage Fulfillment - Per

Funded loan

Loan servicing - Per Loan

Serviced

Closed Block - Policy

Administered

Value engineering to guarantee compliance with

environmental standards

Reduction in regression testing time

Enhancement in product performance

May 4, 2012 Proprietary and Confidential 50

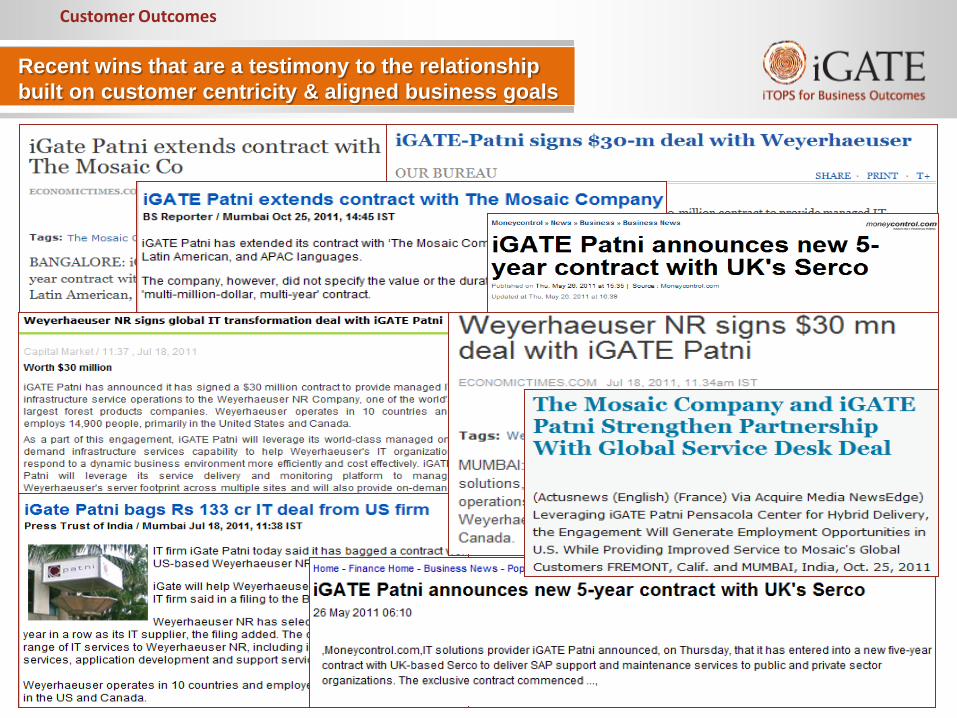

Recent wins that are a testimony to the relationship built on customer centricity & aligned business goals

Customer Outcomes

May 4, 2012 Proprietary and Confidential 51 Proprietary and Confidential 51 May 10, 2012

Agenda

Delivery Structure

Integrating Technology and Operations

Delivery Efficiency and Effectiveness

Market Research Led Innovation

Customer Outcomes

Key Takeaways

May 4, 2012 Proprietary and Confidential 52

• An integrated delivery model that enables convergence of technology and operations

• Our traditional services are aligned to customer business outcomes

• Consistency in delivery through creation of a cocoon model

• Non-headcount based delivery through iTOPS shared services platforms

• Focus on margins through operational efficiency and innovative tools

Key Takeaways

Key Takeaways

May 4, 2012 Proprietary and Confidential 53

Thank You

May 4, 2012 Proprietary and Confidential 54

iGATE Corporation Product and Engineering Solutions

Satish Joshi EVP and Head of Product and Engineering Solutions

May 4, 2012 Proprietary and Confidential 55

Product and Engineering Solutions (It’s Engineering! not IT)

Services

End to end product development and product life cycle management

Research & Evaluation

System Development and

Integration

Verification & Validation

Sustenance & Maintenance

Engineering Design

Electronic Design

May 4, 2012 Proprietary and Confidential 56

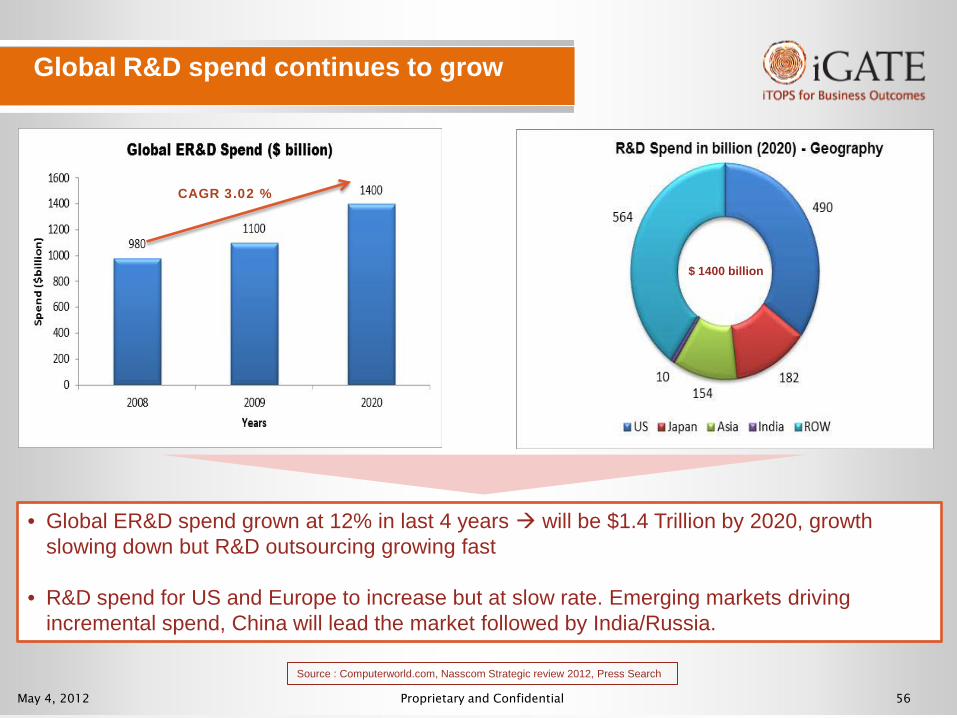

Global R&D spend continues to grow

CAGR 3.02 %

• Global ER&D spend grown at 12% in last 4 years will be $1.4 Trillion by 2020, growth slowing down but R&D outsourcing growing fast

• R&D spend for US and Europe to increase but at slow rate. Emerging markets driving incremental spend, China will lead the market followed by India/Russia.

$ 1400 billion

Source : Computerworld.com, Nasscom Strategic review 2012, Press Search

May 4, 2012 Proprietary and Confidential 57

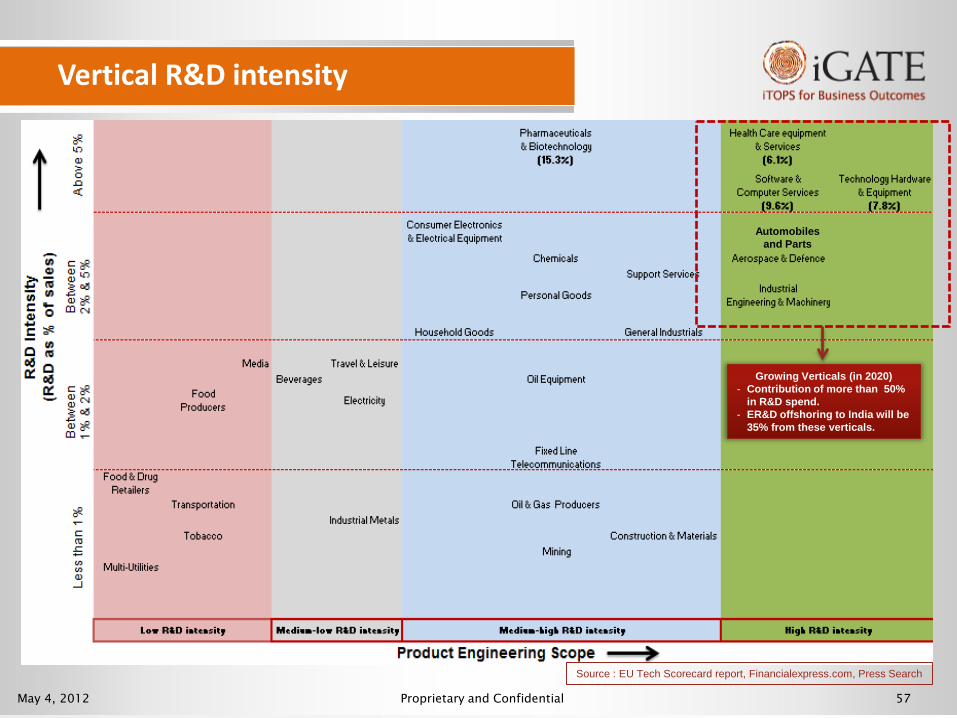

Vertical R&D intensity

Growing Verticals (in 2020) - Contribution of more than 50% in R&D spend. - ER&D offshoring to India will be 35% from these verticals.

Automobiles and Parts

Source : EU Tech Scorecard report, Financialexpress.com, Press Search

May 4, 2012 Proprietary and Confidential 58

Product and Engineering Solutions (It’s Engineering! not IT)

Research & Evaluation

System Development

Verification & Validation

Sustenance & Maintenance

Electronic Design

Engineering Design

Services

End to end product development and product life cycle management

Automotive Electronics

Medical Electronics

Industrial Automation

Storage Networks & Computing

Consumer Electronics & Communication Protocol Stacks - H.323, IP Phone, Streaming, QoS Audio/Video/Imaging Mobile & Wireless, Handset platforms Digital Camera, DTV, Set Top boxes Office equipment – Printers, Scanners Business Equipment – POS terminals, Bar code

readers/printers, Sales automation devices etc

Under the hood – ECUs, Vehicle Sub-Systems Body Electronics Onboard Network – LIN, CAN, MOST, 802.11 Telematics and Navigation systems In-Car Audio/Video Systems

• Network/Resource management, Access Management • Storage Components – SCSI, RAID, FC, IP, SNMP • File Systems & OS - CIFS, NFS, SAMBA, IPC • Hardware Platforms, Boards, HBAs, Controllers, Drives • Network Appliances, Routers, Switches

• Field Devices, Instruments • Intelligent Components – PLCs, RTUS, Controllers • SCADA, HMI, DCS • Building Automation, Plant Automation • Railway Electronics

Monitoring Equipment Diagnostic Equipment Therapeutic Equipment

Enterprise Platform Software • Shrink-wrapped, Platform/OS, CASE tools, Testing Tools • System s/w, Application F/W & Enterprise s/w • PLM/PDM & CAD/CAM/CAE s/w • Banking & Financial Services, Insurance, Telecom • Hospitality, Energy & Utilities, Manufacturing and Healthcare

May 10, 2012 Proprietary and Confidential 59

iGATE Patni : A leading R&D Service Provider

Overview

iGATE Patni ranks among Top 3 Service Providers in Global R&D Service Providers’ Rating, a comprehensive rating and analysis for the top R&D Service Providers in India, China, Russia and Eastern Europe conducted by Zinnov Management Consulting

May 4, 2012 Proprietary and Confidential 60

Partnering for Innovation

The Rio Tinto India Innovation Center

Scope: Development of Technologies for the “Mines-of-the-Future” • Remote Minining operations • Safety • Logistics • Yield Optimization • Cross-Domain lateral innovation (useability, imaging, Safety, Data mining

and analytics, Wireless technolgies etc) Scale : 0 350 people center in the first year

potentially 60-80 Million revenue over 5 years for iGatepatni

May 10, 2012 Proprietary and Confidential 61

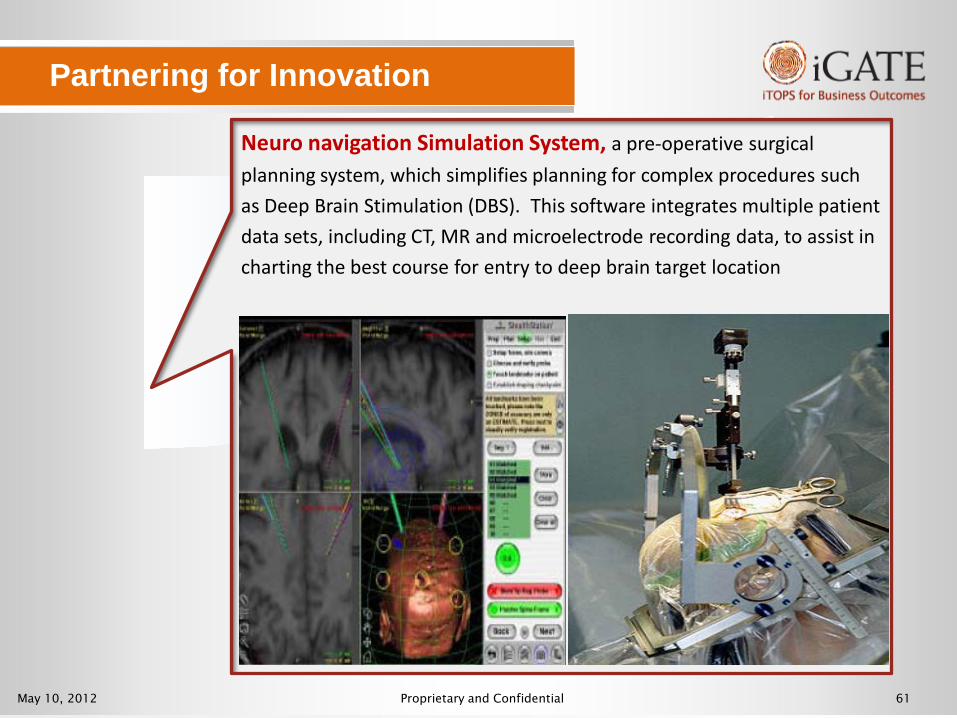

Neuro navigation Simulation System, a pre-operative surgical

planning system, which simplifies planning for complex procedures such

as Deep Brain Stimulation (DBS). This software integrates multiple patient

data sets, including CT, MR and microelectrode recording data, to assist in

charting the best course for entry to deep brain target location

Partnering for Innovation

May 10, 2012 Proprietary and Confidential 62

Partnering in development of an Electronic Train Management

System that integrates new technology with existing train control and

operating systems to enhance train operation safety. It helps prevent track

authority violations, speed limit violations and unauthorized entry into

work zones – all of which reduce the potential for train accidents.

Partnering for Innovation

May 10, 2012 Proprietary and Confidential 63

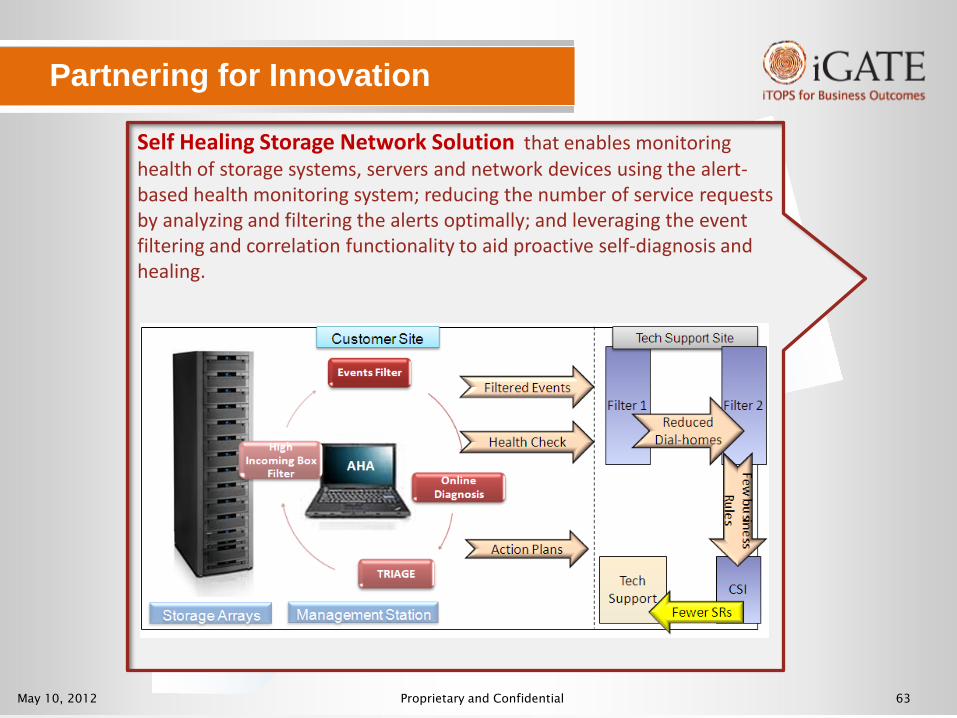

Self Healing Storage Network Solution that enables monitoring health of storage systems, servers and network devices using the alert-based health monitoring system; reducing the number of service requests by analyzing and filtering the alerts optimally; and leveraging the event filtering and correlation functionality to aid proactive self-diagnosis and healing.

Partnering for Innovation

May 4, 2012 Proprietary and Confidential 64

Winds of Change –2011 : Customer-speak!

• Industrial Machinery Manufacturer – Redesign for Indian markets

• Medical Imaging Systems Manufacturer – Cloud Solution to be hosted and run jointly to provide Imaging as a

service

• A Mining Company – Innovation Center to leverage cross industry knowledge to create

technology for the Mines of the Future (Saftey, Useability, Automation, Analytics)

• Plant Automation Systems and Equipment manufacturer – Real-time analytics and reporting of shop-floor data for intelligent

plant monitoring

“Cross-domain” knowledge integration

May 4, 2012 Proprietary and Confidential 65

• Expansion of Geographic Footprint – Europe:

• Automotive, Industrial Automation, Medical , Specifically in Scandinavia: Plant Engineering, Marine, Heavy Machinery

– Japan • Automotive, Industrial Automation, Medical, Consumer Electronics

Drivers for Growth

• Expansion of Market Scope: New Branded Services/Solutions – Value Engineering & Obsolescence Proofing : Especially in the Industrial

Automation and Medical Devices Market – Reengineering for emerging markets – Automotive Functional Safety & ISO 26262 Compliance – Packaged/Stadardized Sustenance services with “skin-in-the-game” outcome

based models in the Storage/ISV markets

• Cross Sale Opportunities within Existing Client Base Manufacturing (Esp. High-Tec) customers:

• Through Engineering, New technology and Product Development solutions • Partnering/Joint product re-engineering/Product support opportunities • Jointly addressing opportunities in Product Lifecycle Management and

Manufacturing Execution Systems Management

May 4, 2012 Proprietary and Confidential 66

Summary

• iGate an acknowledged leader in several sectors of the R&D and Engineering solutions market

• Investments in Industrial Automation & Heavy Engineering, Medical Technologies, Automotive, Computing technologies etc continue to grow

• Product and Technology adoption for emerging markets an important investment focus for our customers and prospects

• Large relatively untapped potential in Europe and Japan

• Synergies for cross-sale into other dominant verticals in iGate’s Enterprise IT portfolio

May 4, 2012 Proprietary and Confidential 67

Thank You

May 4, 2012 Proprietary and Confidential 68

iGATE Corporation Outcome-based & iTOPS-focused Human Resource Management Model

Srinivas Kandula EVP and Head of Human Resources

May 4, 2012 Proprietary and Confidential 69

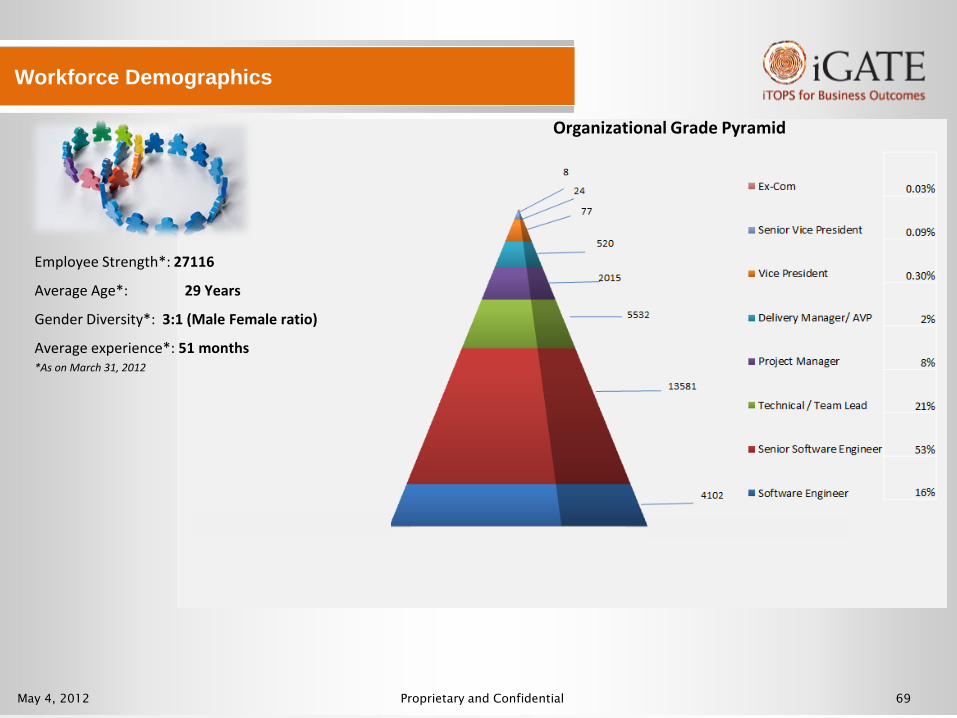

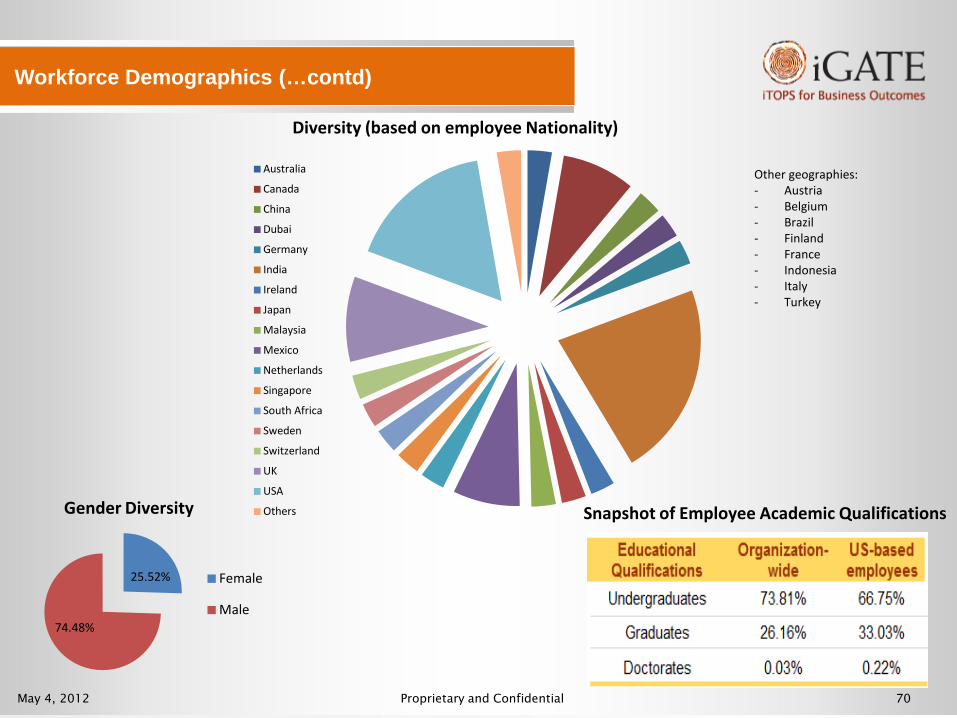

Organizational Grade Pyramid

Workforce Demographics

Employee Strength*: 27116

Average Age*: 29 Years

Gender Diversity*: 3:1 (Male Female ratio)

Average experience*: 51 months *As on March 31, 2012

May 4, 2012 Proprietary and Confidential 70

Workforce Demographics (…contd)

25.52%

74.48%

Female

Male

Gender Diversity Snapshot of Employee Academic Qualifications

Diversity (based on employee Nationality)

Other geographies: - Austria - Belgium - Brazil - Finland - France - Indonesia - Italy - Turkey

Australia

Canada

China

Dubai

Germany

India

Ireland

Japan

Malaysia

Mexico

Netherlands

Singapore

South Africa

Sweden

Switzerland

UK

USA

Others

May 4, 2012 Proprietary and Confidential 71

iGATE- Outcome-based 5C Model of HR

May 4, 2012 Proprietary and Confidential 72

iGATE- Outcome-based 5C Model of HR

Our Compensation model follows a 3-fold holistic approach

May 4, 2012 Proprietary and Confidential 73

iGATE- Outcome-based 5C Model of HR

GREEN BUILDING AWARD

May 4, 2012 Proprietary and Confidential 74

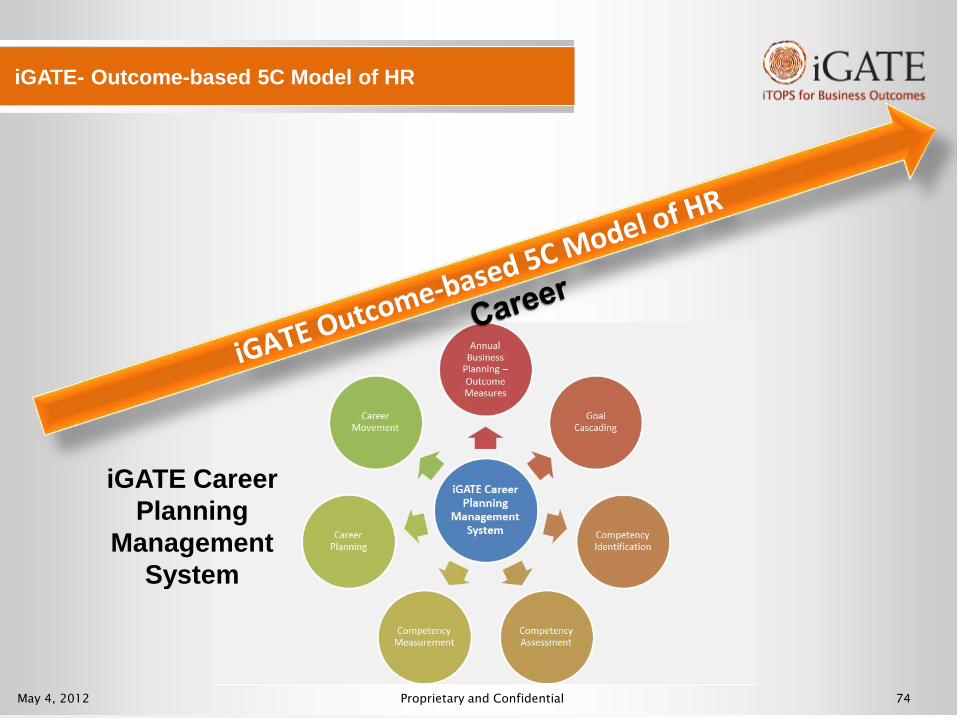

iGATE- Outcome-based 5C Model of HR

iGATE Career Planning

Management System

May 4, 2012 Proprietary and Confidential 75

iGATE- Outcome-based 5C Model of HR

Code of Business Conduct & Ethics

May 4, 2012 Proprietary and Confidential 76

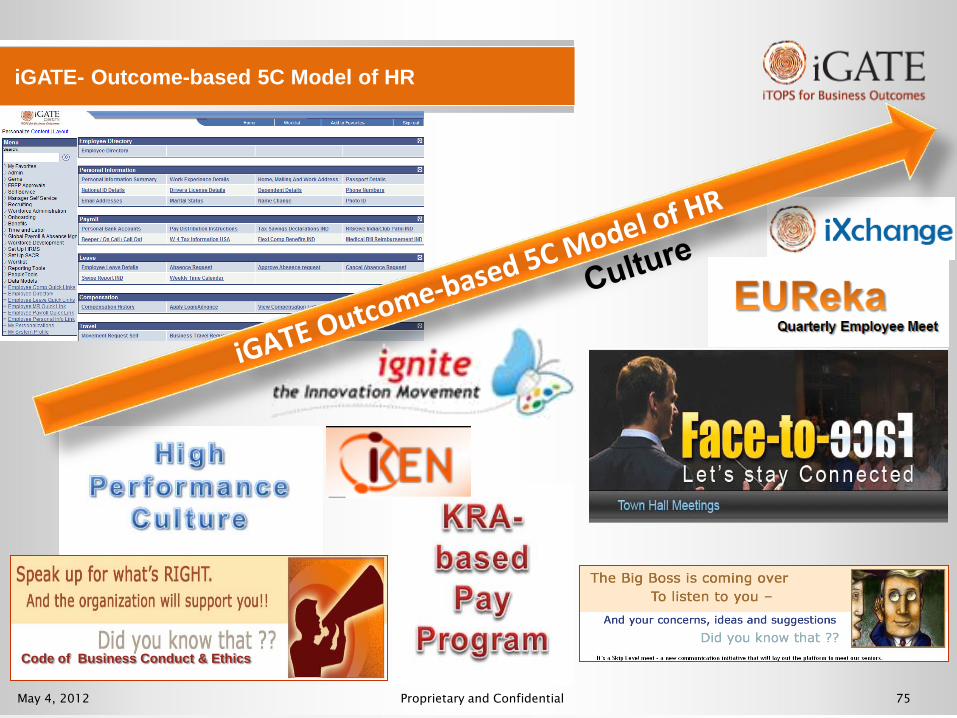

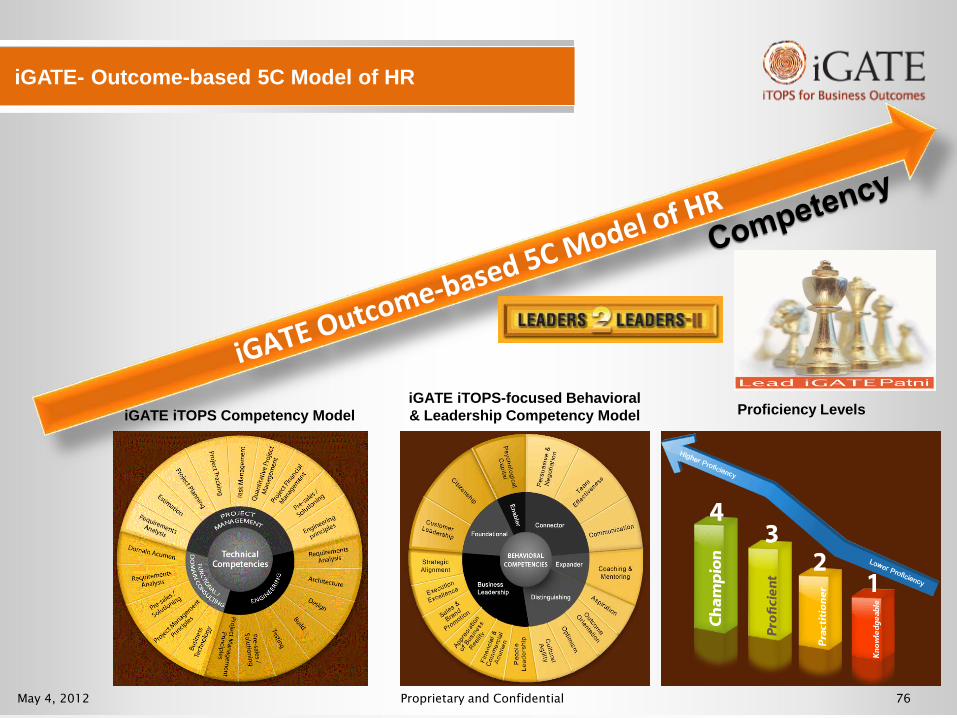

iGATE- Outcome-based 5C Model of HR

iGATE iTOPS Competency Model iGATE iTOPS-focused Behavioral & Leadership Competency Model Proficiency Levels

May 4, 2012 Proprietary and Confidential 77

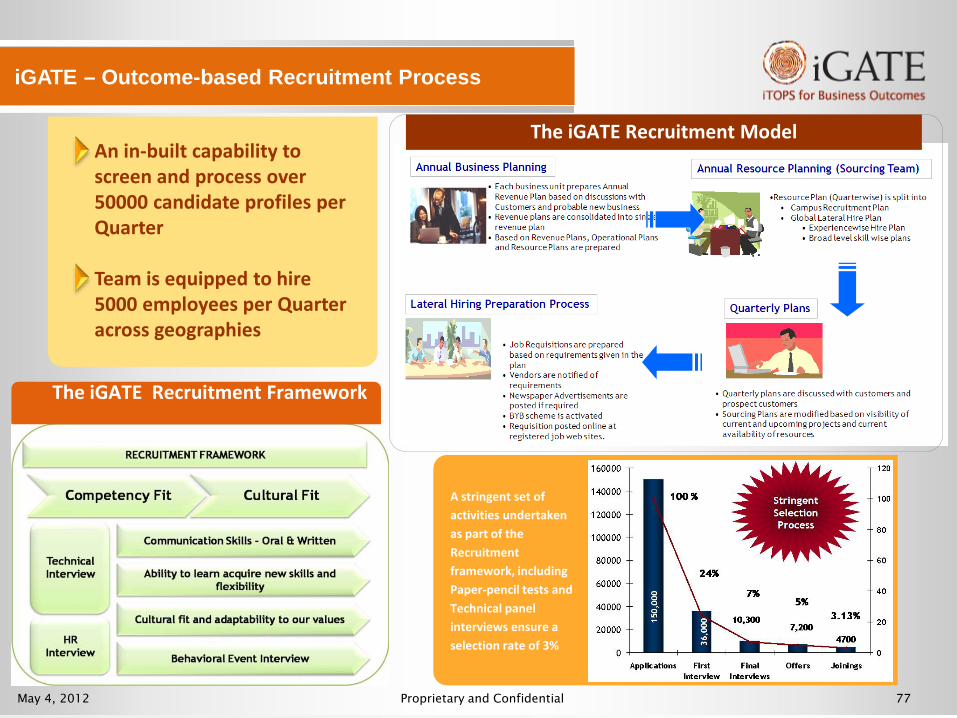

iGATE – Outcome-based Recruitment Process

A stringent set of activities undertaken as part of the Recruitment framework, including Paper-pencil tests and Technical panel interviews ensure a selection rate of 3%

The iGATE Recruitment Model • An in-built capability to

screen and process over 50000 candidate profiles per Quarter

• Team is equipped to hire 5000 employees per Quarter across geographies

The iGATE Recruitment Framework

May 4, 2012 Proprietary and Confidential 78

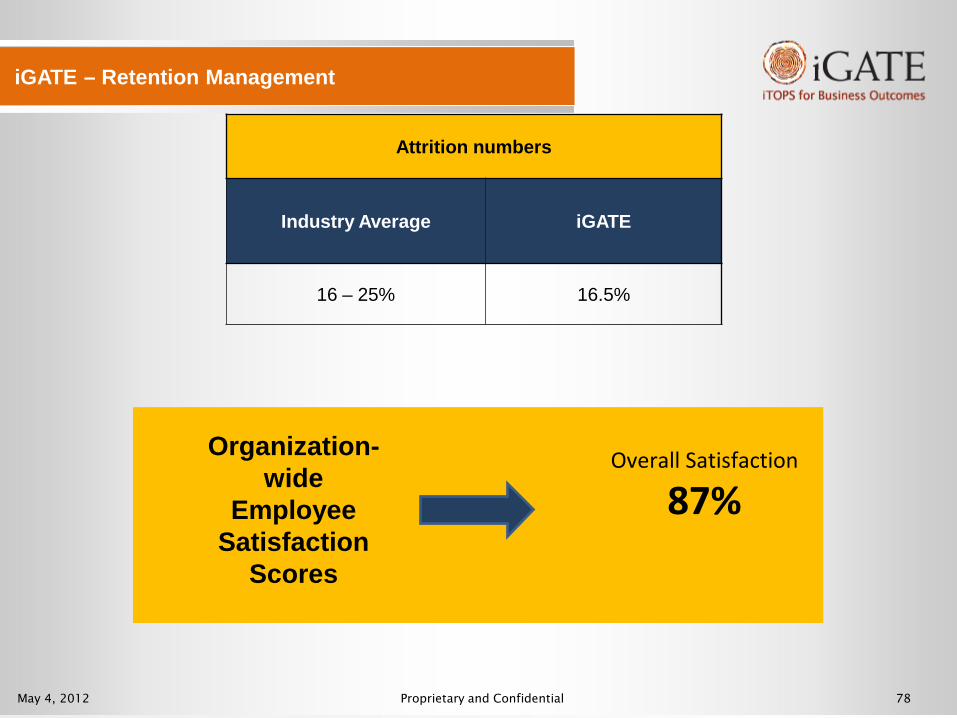

iGATE – Retention Management

Attrition numbers

Industry Average iGATE

16 – 25% 16.5%

Organization-wide

Employee Satisfaction

Scores

Overall Satisfaction

87%

May 4, 2012 Proprietary and Confidential 79

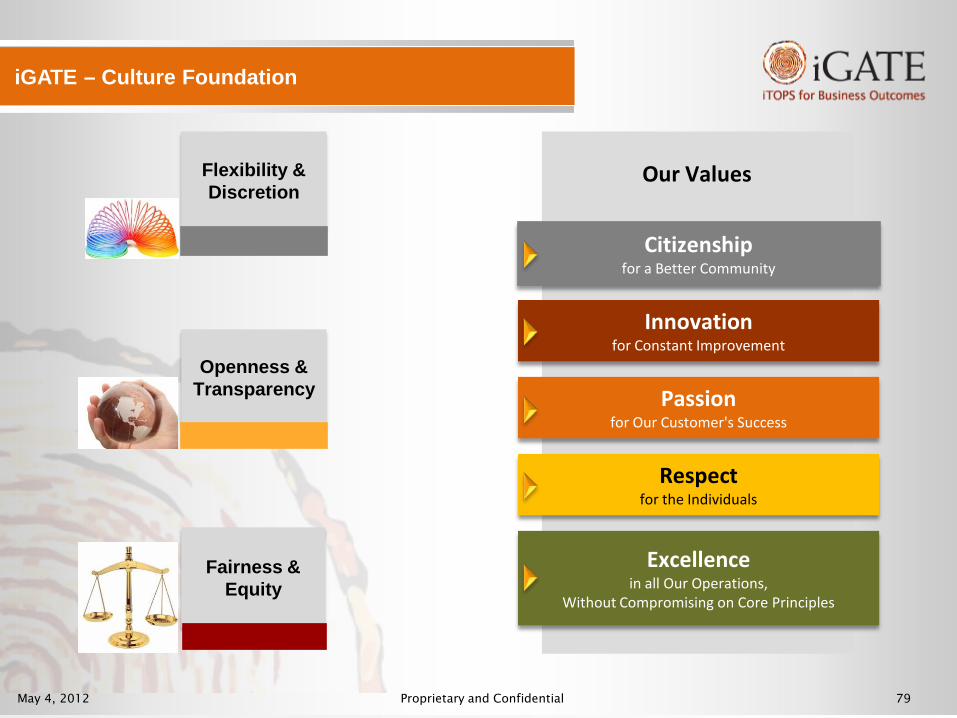

iGATE – Culture Foundation

Our Values Flexibility & Discretion

Openness & Transparency

Fairness & Equity

Citizenship for a Better Community

Innovation for Constant Improvement

Passion for Our Customer's Success

Respect for the Individuals

Excellence in all Our Operations,

Without Compromising on Core Principles

May 4, 2012 Proprietary and Confidential 80

HIGHLIGHTS • Outcome based and iTOPS Enabled- 5C HR Model

to significantly contribute to achieve 3-30-3-1 mission

• More focus on performance and competency

enhancement through iGATE’s specific people development practices

• Creation of iTOPS workforce

• To be the Best Employer in all major Geographies

May 4, 2012 Proprietary and Confidential 81

iGATE - Rewards & Accolades for HR Practices

SMART WORKPLACE AWARDS

May 4, 2012 Proprietary and Confidential 82

Thank You

May 4, 2012 Proprietary and Confidential 83

Sujit Sircar Chief Financial Officer

iGATE Corporation Enhancing Shareholder Value

May 4, 2012 Proprietary and Confidential 84

Agenda

Significant Milestones

Way Forward

Financial & Operational Challenges

May 4, 2012 Proprietary and Confidential 85

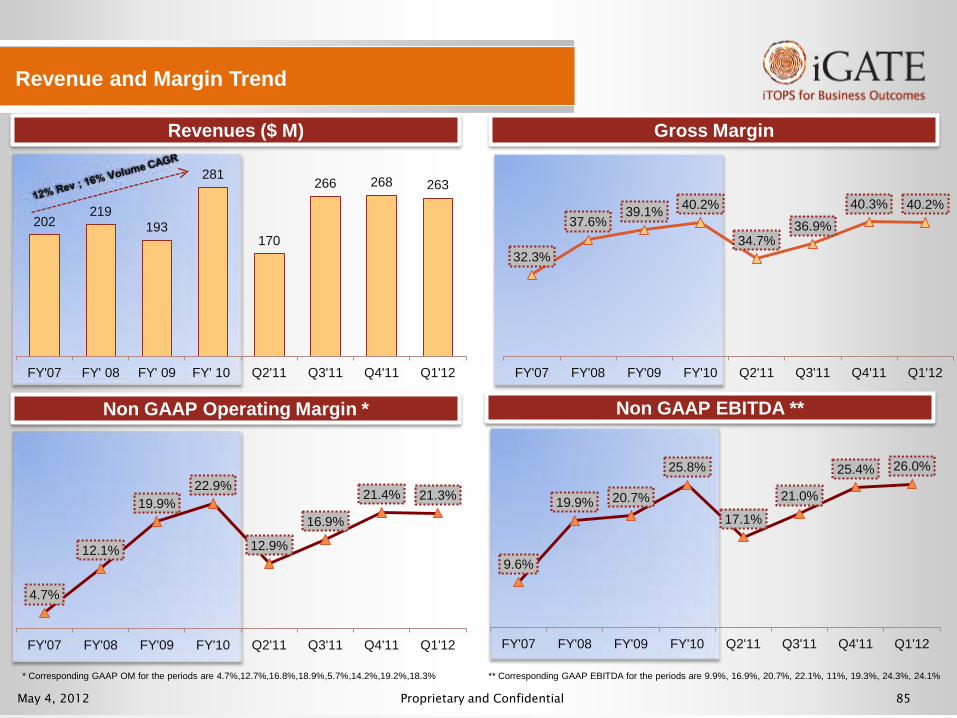

9.6%

19.9% 20.7%

25.8%

17.1%

21.0%

25.4% 26.0%

FY'07 FY'08 FY'09 FY'10 Q2'11 Q3'11 Q4'11 Q1'12

32.3%

37.6% 39.1% 40.2%

34.7% 36.9%

40.3% 40.2%

FY'07 FY'08 FY'09 FY'10 Q2'11 Q3'11 Q4'11 Q1'12

4.7%

12.1%

19.9% 22.9%

12.9%

16.9%

21.4% 21.3%

FY'07 FY'08 FY'09 FY'10 Q2'11 Q3'11 Q4'11 Q1'12

202 219

193

281

170

266 268 263

FY'07 FY' 08 FY' 09 FY' 10 Q2'11 Q3'11 Q4'11 Q1'12

Revenue and Margin Trend

** Corresponding GAAP EBITDA for the periods are 9.9%, 16.9%, 20.7%, 22.1%, 11%, 19.3%, 24.3%, 24.1%

Revenues ($ M) Gross Margin

Non GAAP Operating Margin * Non GAAP EBITDA **

* Corresponding GAAP OM for the periods are 4.7%,12.7%,16.8%,18.9%,5.7%,14.2%,19.2%,18.3%

May 4, 2012 Proprietary and Confidential 86

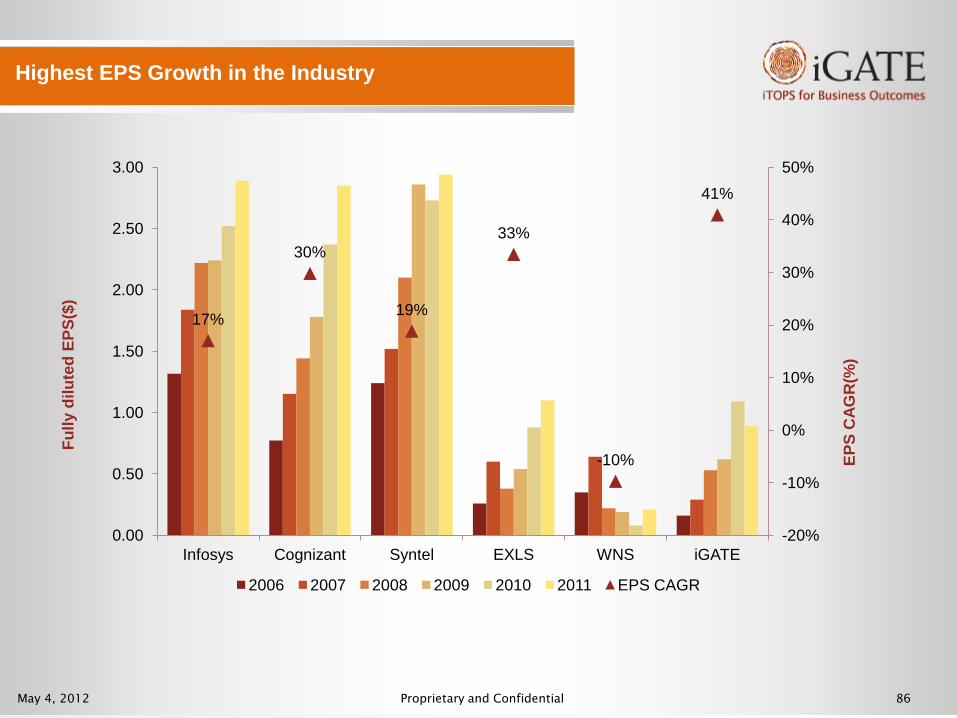

Highest EPS Growth in the Industry

17%

30%

19%

33%

-10%

41%

-20%

-10%

0%

10%

20%

30%

40%

50%

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Infosys Cognizant Syntel EXLS WNS iGATE

2006 2007 2008 2009 2010 2011 EPS CAGR

Fully

dilu

ted

EPS(

$)

EPS

CAG

R(%

)

May 4, 2012 Proprietary and Confidential 87

Agenda

Significant Milestones

Way Forward

Financial & Operational Challenges

May 4, 2012 Proprietary and Confidential 88

71.6%

54.3% 55.3% 55.7% 58.1%

28%

46% 45% 44% 42%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12

FP T&M

Margin expansion through operating levers like utilization, SG&A leverage and expansion of employee pyramid

23.8% 21.1% 20.7%

18.3% 16.7% 17.1%

2006 2007 2008 2009 2010 2011

SG&A Cost 1 (%)

Offshore Leverage & Utilization (IT services) Contract Type (IT Services)

5.2 4.8 4.5 4.3 4.3 5.1

2006 2007 2008 2009 2010 2011

Average experience (in years)

48% 49% 48% 46% 48%

80% 77% 77% 78% 79%

80.0% 79.1% 80.9% 77.4% 75.4%

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12

Off Revenue % Leverage Utilization

1- SG&A % is excluding D&A, Acquisition and severance cost)

May 4, 2012 Proprietary and Confidential 89

Agenda

Significant Milestones

Way Forward

Financial & Operational Challenges

May 4, 2012 Proprietary and Confidential 90

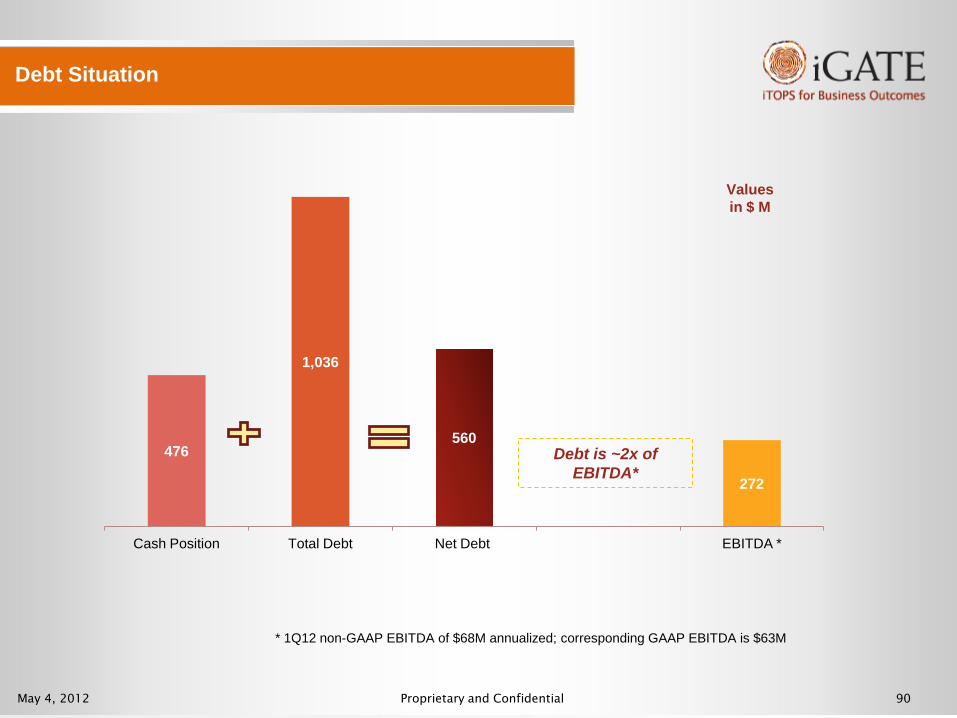

Debt Situation

476

1,036

560

272

Cash Position Total Debt Net Debt EBITDA *

Debt is ~2x of EBITDA*

* 1Q12 non-GAAP EBITDA of $68M annualized; corresponding GAAP EBITDA is $63M

Values in $ M

May 4, 2012 Proprietary and Confidential 91

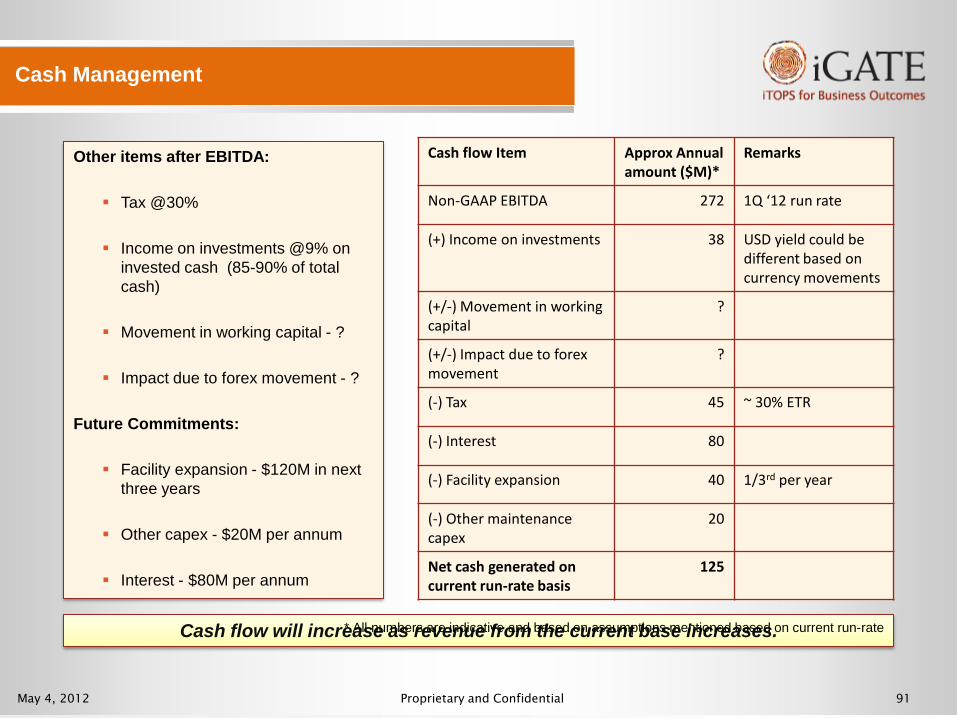

Cash Management

Other items after EBITDA:

Tax @30%

Income on investments @9% on invested cash (85-90% of total cash)

Movement in working capital - ?

Impact due to forex movement - ?

Future Commitments:

Facility expansion - $120M in next three years

Other capex - $20M per annum

Interest - $80M per annum

Cash flow will increase as revenue from the current base increases.

Cash flow Item Approx Annual amount ($M)*

Remarks

Non-GAAP EBITDA 272 1Q ‘12 run rate

(+) Income on investments 38 USD yield could be different based on currency movements

(+/-) Movement in working capital

?

(+/-) Impact due to forex movement

?

(-) Tax 45 ~ 30% ETR

(-) Interest 80

(-) Facility expansion 40 1/3rd per year

(-) Other maintenance capex

20

Net cash generated on current run-rate basis

125

* All numbers are indicative and based on assumptions mentioned based on current run-rate

May 4, 2012 Proprietary and Confidential 92

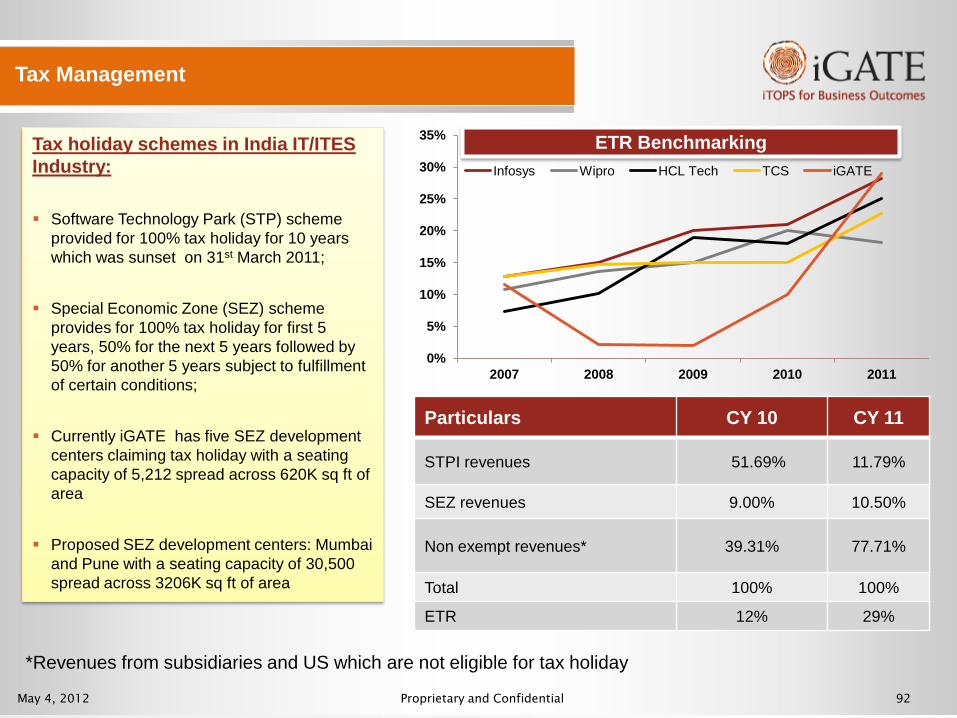

Tax Management

Tax holiday schemes in India IT/ITES Industry:

Software Technology Park (STP) scheme provided for 100% tax holiday for 10 years which was sunset on 31st March 2011;

Special Economic Zone (SEZ) scheme provides for 100% tax holiday for first 5 years, 50% for the next 5 years followed by 50% for another 5 years subject to fulfillment of certain conditions;

Currently iGATE has five SEZ development centers claiming tax holiday with a seating capacity of 5,212 spread across 620K sq ft of area

Proposed SEZ development centers: Mumbai and Pune with a seating capacity of 30,500 spread across 3206K sq ft of area

Particulars CY 10 CY 11

STPI revenues 51.69% 11.79%

SEZ revenues 9.00% 10.50%

Non exempt revenues* 39.31% 77.71%

Total 100% 100%

ETR 12% 29%

*Revenues from subsidiaries and US which are not eligible for tax holiday

0%

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011

Infosys Wipro HCL Tech TCS iGATE

ETR Benchmarking

May 4, 2012 Proprietary and Confidential 93

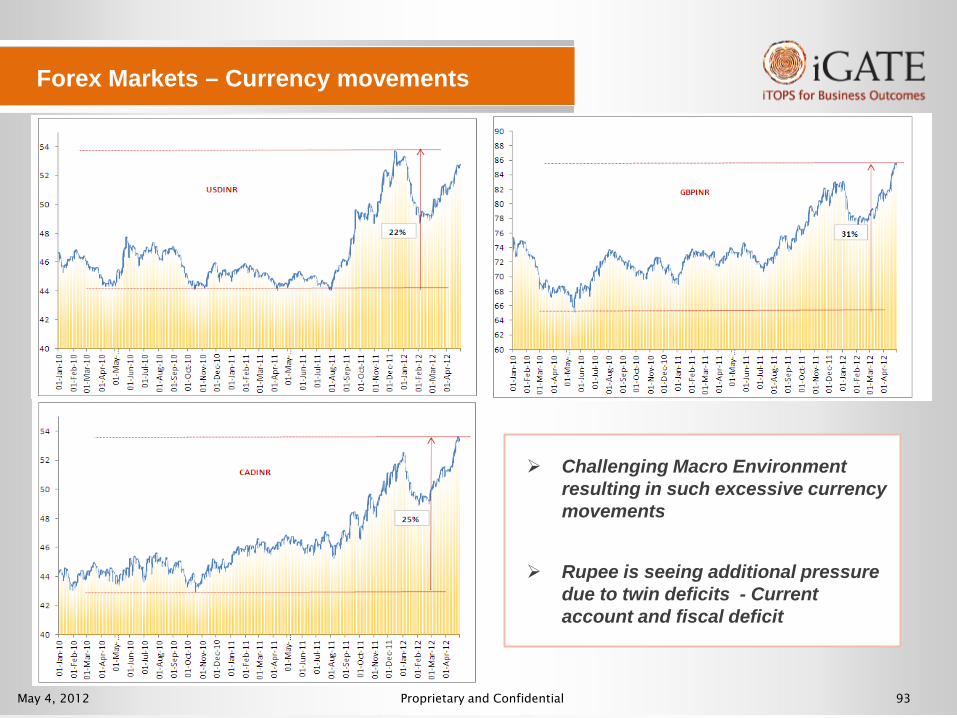

Forex Markets – Currency movements

Challenging Macro Environment resulting in such excessive currency movements

Rupee is seeing additional pressure due to twin deficits - Current account and fiscal deficit

May 4, 2012 Proprietary and Confidential 94

Forex Management

We manage our exposure on rolling 12 month basis

Our policy is to hedge on the basis of net exposure and through simple instruments

Protect our benchmark rate through ‘Value-at-Risk framework” Successful in protecting benchmark rate through

various cycles of currency movements

No exponential impact due to hedging – generally a trade off between operational gains & hedging gain/loss on account of currency movements

Business performance is significantly impacted by forex volatility;

Every 1% change in USD-INR rate impacts Operating margins by 25 - 30 bps

Dealing with basket of currencies due to global footprint; revenue split by billing currencies:

USD – 75%; CAD – 10%; GBP – 7%, EUR, AUD, JPY - ~2% each

Main operating Items impacting Fx Gain Loss:

Exchange rate prevailing at the time of billing

Receivables & Payables revaluation

Revaluation of cash balances in currencies other than base currency

Other Liability items which are revalued: Term Loan – $ loan but usage in INR, INR

amount in Escrow account

PCFC – to be settled with USD inflows, in the interim, revaluation results in gain loss

Some other non-cash liabilities

Our Hedging Policy

Excessive currency volatility has increased the business risk Substantially

Various Elements impacting Forex Gain Loss in P& L Statement

Mar-12 Dec-11 Sep-11 Jun-11

367 M 406 M 486 M 374 M

Hedge book position in last 4 quarter( USD Eq.)

May 4, 2012 Proprietary and Confidential 95

Summary

Highest EPS growth in the industry in last five years

Still possess lot of operational levers to enhance margins

Net debt position comfortable at ~2X EBITDA

Simplified capital structure post delisting of Patni

Tax and Forex challenges could pose headwinds to earnings

May 4, 2012 Proprietary and Confidential 96

Thank You

May 4, 2012 Proprietary and Confidential 97

Emerged as a key player in the industry with the acquisition of Patni Created discontinuity in the market with its innovative business outcomes model Delivery and cost transformation through leveraging greater scale efficiencies in operations and

shared services Enhance large deal sourcing and conversion by building differentiated capabilities Growing Existing Accounts through cross-industry thought leadership and Advisory Services to

embark on client’s Outcomes journey. Growing New Business in new accounts through trusted CXO relationships Creating New Avenues of growth through unique, Point Solutions from our iSDF process

addressing key pain points in both new and existing markets. Innovating and Building Shared Services platforms for the future. An integrated delivery model that enables convergence of technology and operations Our traditional services are aligned to customer business outcomes Consistency in delivery through creation of a cocoon model Non-headcount based delivery through iTOPS shared services platforms Focus on margins through operational efficiency and innovative tools

Key Takeaways

Summary

May 4, 2012 Proprietary and Confidential 98

Growing Existing Accounts through cross-industry thought leadership and Advisory Services to embark on client’s Outcomes journey.

Growing New Business in new accounts through trusted CXO relationships

Creating New Avenues of growth through unique, Point Solutions from our iSDF process addressing key pain points in both new and existing markets.

Innovating and Building Shared Services platforms for the future.

Key TakeAways Creating The Future…..2014 and Beyond

Solutions & Consulting is about:

2012 Market Creators

2014unique and Market Leaders

2016 Market Innovators

May 4, 2012 Proprietary and Confidential 99

iGate an acknowledged leader in several sectors of the R&D and Engineering solutions market Investments in Industrial Automation & Heavy Engineering, Medical Technologies, Automotive,

Computing technologies etc continue to grow Product and technology adoption for emerging markets an important investment focus for our

customers and prospects Large relatively untapped potential in Europe and Japan Synergies for cross-sale of P&ES into other dominant verticals in iGate’s Enterprise IT portfolio Outcome based and iTOPS Enabled - 5C HR Model More focus on performance and competency enhancement through iGATE’s specific people

development practices Creation of iTOPS workforce To be the Best Employer in all major Geographies Highest EPS growth in the industry in last five years Still possess lot of operational levers to enhance margins Net debt position comfortable at ~2X EBITDA Simplified capital structure post delisting of Patni Tax and Forex challenges could pose headwinds to earnings Lower equity base through leverage gives significant upside to equity holders over long term as

the company continue to de-leverage

Key Takeaways

Summary

May 4, 2012 Proprietary and Confidential 100

Thank You