india infrastructure development opportunities and …presentations\88\mr. parvez... · railways...

TRANSCRIPT

India Infrastructure DevelopmentOpportunities and Challenges

A presentation by

66,666Railways120,000Energy11,111Ports17,778Irrigation8,889Airports

336,664Total

76,666Others-Telecom, Tourism, SEZs, Townships, Supporting Urban Infra, Water & Sanitation, State & rural roads, Logistics etc.

48,888National Highways

Infrastructure Investments

MN US$

Sectors

FINANCING REQUIREMENTS

Funding requirements during the Eleventh Five Year Plan 2007-12

60 %Urban Infrastructure

55 %Tourism100 %Roads42 %Railways30 %Nuclear Power

70 %Hydro

20%Thermal

-Power50%Ports80%Irrigation42%Airports

Construction component

Sectors

Source- CRISINFAC

Contracting Opportunity

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATER

CENTRECENTRE

STATESTATE

CENTRECENTRE-- MAJORMAJOR

STATESTATE-- MINORMINOR

CENTRECENTRE-- AAIAAI

CENTRECENTRE

STATESTATE

CENTRECENTRE

STATESTATE

STATESTATE

CITYCITY

Responsibility

Opportunities….

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATEROpportunities….

Fact fileIndia has a dense road network which covers 3.3 million kms and includes 0.2 million kms of highways.

India’s road network carries close to 70% of the country’s freight traffic and 85% of its passenger traffic

National Highways account for only 2% of the total network but accounts for 40% of the total traffic.

Of the total 65,000 kms of national highways, only 9% are four-lane, 56% are two-lane, and 35% are single-lane.

Traffic on roads growing at 7-10% per annum

ROADS

Of TotalKMType

33,15,23126,50,0004,67,7631,31,899

65,569

100%79.9%14.1%

4%2%

Village & Other RoadsTotal Length

Major District RoadsState HighwaysNational Highways

Source- National Highways Authority of India

NHAI was constituted in 1995 for implementation of Road Projects.

NHAI is a AAA rated Entity in the Debt Markets

Modes of Road sector development by NHAI

Through construction contracts- Govt. Funded

Through Annuity based projects on PPP Model

Through Toll based BOT projects on PPP Model

ROADS

ROADS

GQ – 5846 Kms

NSEW – 7300 Kms

1000

5800

500

10,000

7300

5846

LengthKm

PPP- 100%

PPP- 100%

Govt. funded- 100%PPP- 100%

Govt. funded- 50-70%PPP- 30-50%

Govt. funded- 90%PPP- 10%

Mode

Expressways 8 Corridors

Phase VI

Phase I revisited (FROM 4 laning – 6 laning of GQ)

Phase V

Port Connectivity Phase IV

Interconnection of Phase I & Phase IIPhase III

North – South & East – West Corridors Phase II

Connecting 4 Metros referred to as GQ. (2 lane – 4 lane)

Phase I

Description Stage

NHAI Roadmap Since 1997

ROADS

• All projects on BOT basis.• Total length of around 5800 Km.• Total number of projects – 44 valued at US $ 10 Bn.• 8 Projects at prequalification stage, valued at US $ 1.8 Bn • Projects cleared by the centre

- overall grant +10 %• Most projects expected on concession premium i.e. on revenue

sharing basis• Concession Period –20 years (including construction phase)

Characteristics of Phase V (carried forward from Phase I)

ROADS

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATEROpportunities….

PORTS

Fact file

India has 13 major and 185 minor and intermediate ports, along 7,000 kms of coastline.

Seaports handle 95% of India’s foreign trade in volume terms and70% in value terms.

Major ports accounted for 75% of the total cargo traffic of 345 million tons in F2004.

During F1996-F2006, average cargo traffic growth was 20% and 7% at small ports and major ports, respectively.

Low productivity at Indian ports primarily due to operational & labour inefficiencies, high tariff rates & poor hinterland connectivity and lack of capital investments

Source- Ministry of Shipping, Road Transport & Highways

Asia's share of world trade more than doubledduring 1970-2005

0.05.0

10.015.020.025.030.0

1970 1975 1980 1985 1990 1995 2000 2005

Asia's share of world trade (%)

• Momentum of growth in Developing Asia has shown an uptrendwith Indian economy at No. 2 position after China

Asia Rising

PORTS

Share of World trade defined as(total exports + total imports)/(world exports + world imports)

423.41 To

834.00

281.13 To

423.41

152.85To

281.13

20.01To

152.85

Major Ports

(MN T)

145.53 To

391.00

87.37To

145.53

12.78To

87.37

2.50To

12.78

Non- Major Ports

(MN T)

Total(MN T)

11.47568.94 To

1225.0

2005-06To

2013-2014

Projected Traffic

8.54368.50To

568.94

2000-01To

2005-06

Post- Private Sector Participation

6.28165.63To

368.50

1990-91To

2000-01

Pre-Private Sector Participation

5.2022.51 To

165.63

1950-51To

1990-91

Pre-Liberalisation

CAGR (%)PeriodERA

Trend of Traffic - INDIA

PORTS

423.41383.69344.80313.55287.59All Major Ports

96.27

37.73

22.52

26.43

22.93

17.51

12.06

13.02

36.12

3.40

44.34

21.13

30.40

2001-02

105.41

40.63

26.84

26.80

23.65

21.43

13.02

13.30

33.69

8.49

46.01

23.90

35.80

2002-03

137.83

41.54

32.81

35.19

30.66

33.90

14.09

15.81

43.81

9.48

50.15

30.10

46.16

2004-05

145.59

45.91

37.75

44.19

31.69

34.45

13.94

17.14

47.25

9.17

55.80

33.10

53.02

2005-06

120.84Non Major Ports

41.53Kandla

31.18JNPT

30.00Mumbai

27.87Mormugao

26.67New Mangalore

13.57Cochin

13.68Tuticorin

36.71Chennai

9.28Ennore

47.74Visakhapatnam

25.31Paradip

41.26Kolkata & Haldia

2003-04PORT

All India Traffic in last 5 Years (Million Tons)

PORTS

Traffic includes all cargo including bulk and containers; 1 Container (TEU) is taken as 15 Tons

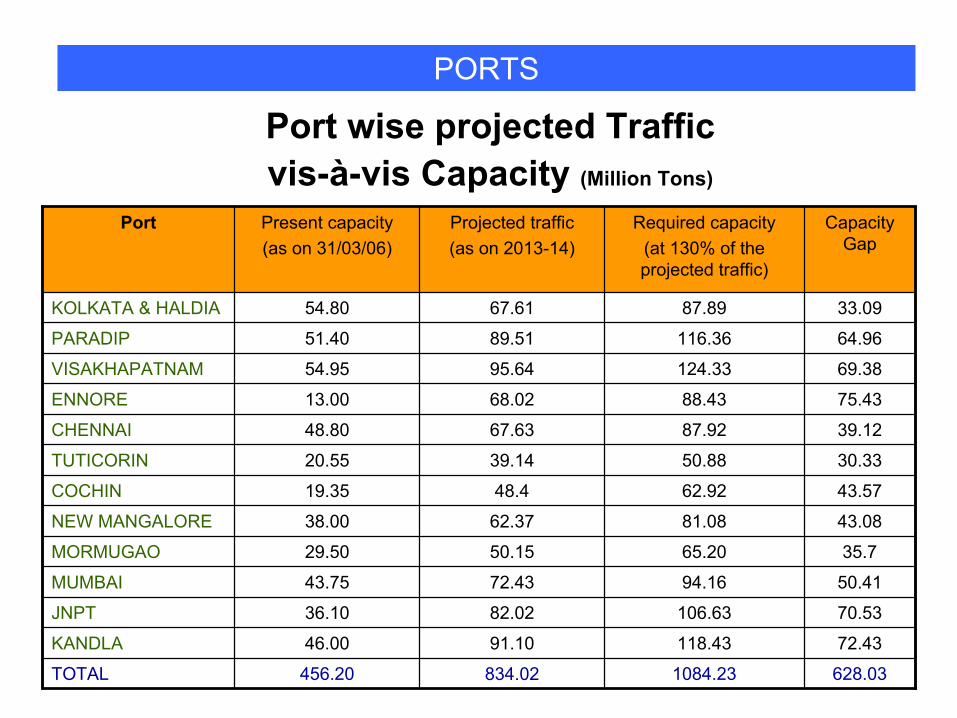

Port wise projected Traffic vis-à-vis Capacity (Million Tons)

1084.23

118.43

106.63

94.16

65.20

81.08

62.92

50.88

87.92

88.43

124.33

116.36

87.89

Required capacity (at 130% of the projected traffic)

834.02

91.10

82.02

72.43

50.15

62.37

48.4

39.14

67.63

68.02

95.64

89.51

67.61

Projected traffic(as on 2013-14)

628.03

72.43

70.53

50.41

35.7

43.08

43.57

30.33

39.12

75.43

69.38

64.96

33.09

Capacity Gap

456.20

46.00

36.10

43.75

29.50

38.00

19.35

20.55

48.80

13.00

54.95

51.40

54.80

Present capacity(as on 31/03/06)

ENNORE

TOTAL

KANDLA

JNPT

MUMBAI

MORMUGAO

NEW MANGALORE

COCHIN

TUTICORIN

CHENNAI

VISAKHAPATNAM

PARADIP

KOLKATA & HALDIA

Port

PORTS

Container Traffic (Million TEUs)

PORTS

Year (Mn TEUs)1993-94 1.05 1994-95 1.26 1995-96 1.45 1996-97 1.70 1997-98 1.89 1998-99 1.93 1999-00 2.19 2000-01 2.44 2001-02 2.88 2002-03 3.37 2003-04 3.90 2004-05 4.23 2005-06 4.61 2006-07 5.44

60% of the Container Traffic is handled at JNPT port- Mumbai Port

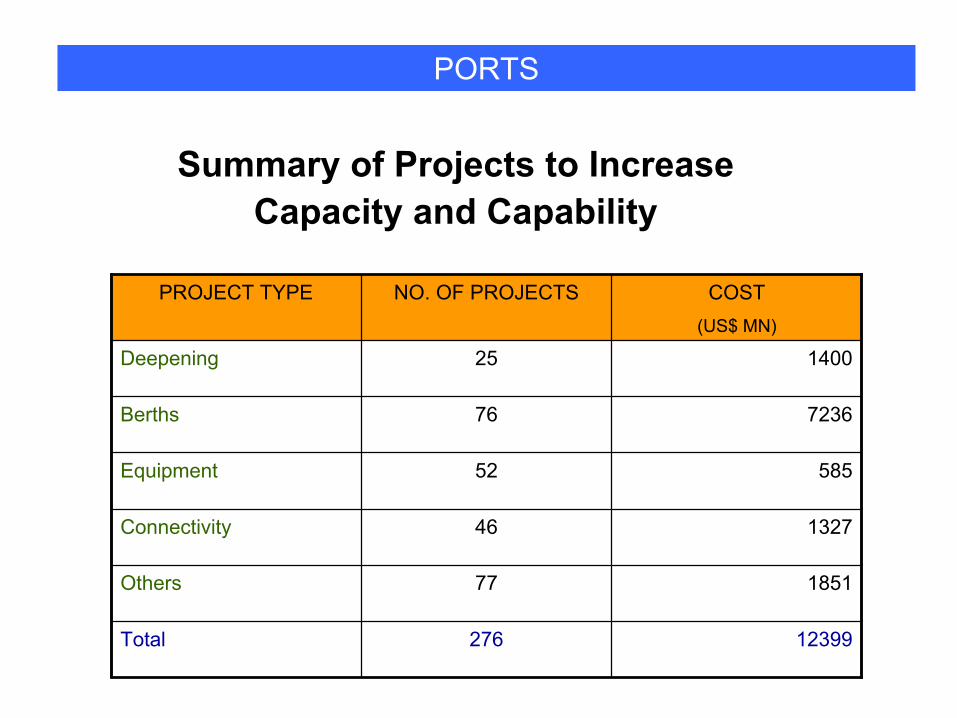

Summary of Projects to Increase Capacity and Capability

12399276Total

185177Others

132746Connectivity

58552Equipment

723676Berths

140025Deepening

COST(US$ MN)

NO. OF PROJECTSPROJECT TYPE

PORTS

Proposed Funding Pattern For Port Infrastructure Projects

55803391734505137713609276Total

8346565162290422578Others

59563634-22329045Rail and Road connectivity works

263213010751427-52Procurement of Equipments, etc.

325635028083386756376Construction/ re-construction of berths/ jetties, etc.

6304481853340273125Deepening of channels/ berths, etc.

TotalOthersPrivateInvest-ment

InternalResources

BudgetarySupport

No. of Projects

Project Head

PORTS

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATEROpportunities….

Fact fileMajor four airports at Mumbai, Delhi, Kolkatta & Chennai account for 63% of India’s passenger traffic & 78% of its freight traffic.

AAI has started the modernization process of airports with Mumbai, Delhi, Bangalore & Hyderabad airports

With a 24.3% growth in passenger traffic & 9.6% growth in cargo handled (Source: AAI) over the previous period (FY05), India is amongst the fastest growing aviation markets.

Category FY06 FY05 % Y/YAircraft Movements (in '000)International 191 162 17.8%Domestic 647 557 16.2%Total 838 719 16.6%Passengers (in Million)International 22 19 17.7%Domestic 51 40 27.4%Total 73 59 24.3%Cargo (in '000 tons)International 920 822 11.9%Domestic 484 459 5.4%Total 1404 1281 9.6%

AIRPORTS

Source: Airports Authority of India

Source: CRISIL (S&P’s Indian arm)

AIRPORTS

1.908.6016.79.7023.702005-06

1.7311.8120.6519.8021.502004-05

0.8112.7610.359.1011.602003-04

1.597.5412.014.609.402002-03

Multiple (Traffic

Growth over GDP)

GDP Growth %, yoy

Traffic Growth%

Cargo Traffic Growth %,

yoy

PassangerTraffic

Growth %, yoy

Year

GDP v/s Total Traffic

AIRPORTS

International benchmark for Traffic Growth is 0.8-1 times GDP growth

Airport Growth Story – 2005-06

Airport Development Fund Requirements – USD 8.85 bn

AIRPORTS

AIRPORTS

AIRPORTS

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

Opportunities….

METRO RAILS IN INDIA

Government FundedKolkata Metro Rail (One of the oldest running Metro rail systems in India)

Mumbai Metropolitan Rail system (existing)

Delhi Metro Rail

Bangalore Metro Rail

On PPP FormatHyderabad Metro Rail (Line I, II & III)

Kochi Metro Rail

Mumbai Metro Rail (Phase I, II & III)

Delhi Airport Metro Rail Link

Chandigarh monorail (planned)

Chennai monorail (planned)

METRO RAILS IN INDIA

The Bangalore Metro is the proposed mass-transit rail system for the city of Bangalore. The agency responsible for its implementation is Bangalore Mass Rapid Transit Ltd (BMRTL). The Delhi Metro Rail Corporation] (DMRC) are the general consultants for the project.

A project report envisages a 33km elevated and underground rail network with 32 stations for Phase I of the project. The proposed gauge is standard gaugeunlike the broad gauge on the Delhi Metro network.

On 25 April 2006 the Indian cabinet approved the project, which is now budgeted at more than 54.5 billion rupees (about US$1.2 billion). The work is scheduled to be completed by 2011.

The EPC Contracts and E&M Contracts are at the Bid stage

Bangalore Metro Rail

Source- BMRTL

METRO RAILS IN INDIA

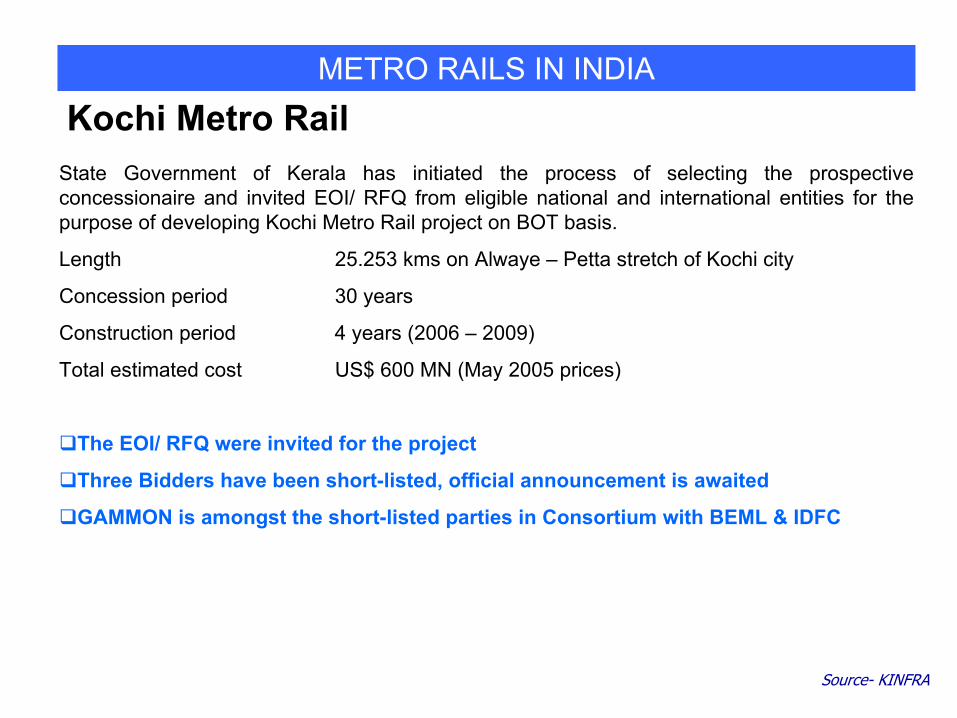

State Government of Kerala has initiated the process of selecting the prospective concessionaire and invited EOI/ RFQ from eligible national and international entities for the purpose of developing Kochi Metro Rail project on BOT basis.

Length 25.253 kms on Alwaye – Petta stretch of Kochi city

Concession period 30 years

Construction period 4 years (2006 – 2009)

Total estimated cost US$ 600 MN (May 2005 prices)

The EOI/ RFQ were invited for the project

Three Bidders have been short-listed, official announcement is awaited

GAMMON is amongst the short-listed parties in Consortium with BEML & IDFC

Kochi Metro Rail

Source- KINFRA

METRO RAILS IN INDIA

–Project Features:Concession of 35 years including 5 years of construction period.Bid Parameter: Min. Viability Gap Funding

3 corridors totaling 66.39 km: –Line 1:Miyapuri to Chaitanyapuri /L.B Nagar- 29.87 km–Line 2:Jubilee Bus Station to Falaknuma- 14.78 km–Line 3:Habsiguda/ Tarnaka to Hitec City-21.74 km

One combined bid for all three packages

Hyderabad Metro Rail

Source- KINFRALine 1,2 & 3Package III

Line 2Package II

Line 1 & 3Package I

CorridorPackage

METRO RAILS IN INDIA

62.68 KmTotal

13.37 KmBandra - Kurla – Mankhurd- LINE 3

38.24 KmColaba - Bandra – Charkop- LINE 2

11.07 KmVersova - Andheri – Ghatkopar (under implementation)- LINE 1

LengthPhase I year (2006 – 2011)

Mumbai Metro Rail

Source- MMRDA

Master Plan is to develop the Metro in 3 Phases

Total Length as per Master Plan – 146.5 Km

Total Cost as per Master Plan –4.35 bn $

METRO RAILS IN INDIA

3.5 KmSewri – Prabhadevi

21.8 KmHutatma Chowk – Ghatkopar

18.0 KmAndheri(E) - Dahisar(E)

19.5 KmBKC - Kanjur Marg via Airport

LengthPhase III ( 2016 – 2021)

12.4 KmGhatkopar – Mulund

7.5 KmCharkop - Dahisar

LengthPhase II (2011 – 2016)

Mumbai Metro Rail

Source- MMRDA

METRO RAILS IN INDIA

Airport Link Mass Rapid Transit Systems

Delhi International Airport Link

Bangalore International Airport Link

Hyderabad International Airport Link

Cochin International Airport Link

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATEROpportunities….

POWER

Fact file

India has a power shortage of 12% at peak level.

Govt. of India has set up a target of 100,000 MW capacity addition over 2002-2012 to contain power shortage.

Ongoing huge Investments in Transmission & Distribution required to augment the planned generation capacity and overhauling the outdated & inefficient infrastructure

Hydro power opportunity being given renewed thrust. More than 35% of the planned capacity addition during the tenth plan is inhydro power.

Source- Ministry of Power

Source- Ministry of Power, Planning Commission

Power capacity creation

37%60,89622,420Eleventh plan (2008-12) target34%31,90010,800Likely addition in tenth plan35%41,10014,393Tenth plan (2003-07) target25%105,04626,269Capacity in March 2002

% of total

TotalHydroYear to 31 March

Hydro Power capacity creation

66,98560,8852007-2012Eleventh Plan period (E)

35,00041,1002002-2007Tenth Plan period (E)

19,16540,2451997-2002Ninth Plan period

16,42230,5381992-1997Eighth Plan period

Actual / implied requirement

TargetPeriod

66,98560,8852007-2012Eleventh Plan period (E)

35,00041,1002002-2007Tenth Plan period (E)

19,16540,2451997-2002Ninth Plan period

16,42230,5381992-1997Eighth Plan period

Actual / implied requirement

TargetPeriod

POWER

Source- Ministry of Power, Planning Commission

Sector MW %age

State Sector 71,250 55.4

Central Sector 43,231 33.7

Private Sector 13,951 10.9

Total 1,28,432

Total installed capacity

POWER

Source- Ministry of Power, Planning Commission

Fuel MW %age

Total ThermalCoal

84,40069,616

65.654.1

Gas 13,582 10.6

Oil 1,202 0.9

Hydro 33,942 26.5

Nuclear 3,900 3.0

Renewable 6,191 4.8

Total 1,28,432

POWER

Source- Ministry of Power, Planning Commission

Capacity MVA Circuit KM

765/800 KV -- 2,037

400 KV 91,052 73,753

220 KV 1,52,967 112,901

HVDC 3,000 5,872

High Voltage Transmission Capacity

POWER

ROADSROADS

PORTSPORTS

AIRPORTSAIRPORTS

POWERPOWER

METRO RAILSMETRO RAILS

INFRASTRUCTUREINFRASTRUCTURE

WATERWATEROpportunities….

WATERUrban WSS Investment required for meeting the MDG

•Financial Closure•Environmental issues•Engineering challenges•Mechanisation•Operational efficiency•Revenue collection

Post Bid/ Award

•Project feasibility•PPP structure offered•Willingness to pay•License Agreement•Credibility of Client

Pre Bid/ Award

Challenges in Challenges in Privatisation Privatisation ProjectsProjects

Challenges….

THANK YOU