india market strategy 2-

TRANSCRIPT

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

18 May 2017 Asia Pacific/India Equity Research

Strategy

India Market Strategy Research Analysts

Neelkanth Mishra

91 22 6777 3716

Prateek Singh

91 22 6777 3894

Ravi Shankar

91 22 6777 3869

STRATEGY

Can companies grow fast without innovation?

Figure 1: Tough to beat GDP growth even in under-penetrated sectors

Source: Euromonitor, CSO, Company Data, Credit Suisse estimates

■ The difference between economy and markets. Tempting as it is to link

them, the relationship between the economy and markets is tenuous at best, in

our view. Not only are market returns more P/E than EPS driven, markets and

economy also have different structures. To study this, we categorised BSE500

stocks into: Global, Macro, Penetration and Market Share (as key revenue

driver). 64 of the 97 stocks that grew sales at more than 25% CAGR over ten

years improved penetration, and 15 (mostly private banks) gained share. We,

therefore, analyse the drivers of penetration.

■ Growing revenues faster than GDP is tough. The 2002-16 growth for even

under-penetrated categories is not too different from the growth in nominal

GDP. For a category to grow meaningfully faster, one needs one or more of:

(1) Innovations that bring down price points to a level where price elasticity of

demand is high (e.g., sachets, mortgages); (2) Improvement in enablers (e.g.,

electricity for appliances); (3) Improved distribution; and (4) Demographics. In

India, only items with very low price points have high penetration (telecom

penetration is 90% only as it is profitable at Rs80 ARPU). For under-penetrated

categories to grow fast, they must innovate and cut costs sharply so they can

stay profitable even at low price points.

■ Market pricing in a tide; there may be none. Even as revenue growth has

slowed in the recent years, P/E multiples have risen (24% of stocks trade at

30x P/E or more, vs 6% five years back). This is partly due to global drivers,

but also implies a broad-based growth faster than GDP. This is unlikely. We

believe sharp penetration improvement would be selective—in NBFCs

(Overweight on Chola Finance), banking, consumer appliances (HAVL,

Crompton Consumer), select Staples (Godrej Consumer, ITC), telecom towers

(Bharti Infratel) and QSR (Jubilant). Expectations (high P/E) appear excessive

in NEST, COLG and TVSM (Underweight).

-2% 0% 2% 4% 6% 8% 10%12%14%16%

Shampoo

Detergents

Bar Soap

Carbonated Drinks

Cigarettes

Tooth Paste

Tea

Alcohol

Biscuits

2W

Paints

4W

Volume Price

Expenditure G

rowth

Revenue Growth 2002-16

Shampoo

Detergents

Bar Soap

Carbonated Drinks

Cigarettes

Tooth Paste

Tea

AlcoholBiscuits

2W

Paints

4W

0%

2%

4%

6%

8%

10%

12%

-5% 0% 5% 10% 15%

Volume Growth CAGR

Pric

e G

row

th C

AG

R (

2002

-16)

Drivers of 2002-16 revenue growth

18 May 2017

India Market Strategy 2

Focus charts

Figure 2: Nifty returns dominated by P/E changes Figure 3: India GDP growth vs Nifty EPS growth

Source: The BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates Source: CSO, The BLOOMBERG PROFESSIONAL™ service, RAVE, Credit Suisse

estimates

Figure 4: Market cap for each sector split into the four categories, by key driver of revenue growth

Source: The BLOOMBERG PROFESSIONAL™ service, RAVE, Credit Suisse estimates

Figure 5: 64 of 97 fast growing names in Penetration Figure 6: Growth though has slowed sharply of late

Source: Capitaline, Credit Suisse estimates Source: Capitaline, Credit Suisse estimates

Figure 7: Penetration/Market share at a premium Figure 8: P/E Multiples have risen across the board

Source: RAVE, Credit Suisse estimates Source: RAVE, Credit Suisse estimates

-40%

-20%

0%

20%

40%

60%

80%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12MF EPS Change 12MF P/E Change Index Change

1Y Change

-5%

0%

5%

10%

15%

20%

-10%

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Nifty EPS Growth Nominal GDP Growth (RHS)

0%

20%

40%

60%

80%

100%

IT

Ene

rgy

Priv

ate

Ban

k

Sta

ples

PS

U B

ank

NB

FC

Aut

os

Hea

lth

Indu

stria

ls

Tel

ecom

Util

ities

Met

als

Cem

ent

Dis

cret

ion

ary

Che

mic

als

Rea

lE

stat

e

Tot

al

Penetration

Market Share

Macro

Global

0%

20%

40%

60%

80%

100%

Decline 0-15% 15-25% 25%+ Total

Penetration Macro Global Market Share

# Cos 8 172 164 97 441

0%

20%

40%

60%

80%

100%

10Y 5Y 3Y 1Y

Decline 0-15% 15-25% 25%+

5

10

15

20

25

30

Jan-11 Sep-11 May-12 Jan-13 Sep-13 May-14 Jan-15 Sep-15 May-16 Jan-17

Penetration Market Share Macro

Global Total

12MF PE 0%

20%

40%

60%

80%

100%

5Y 3Y 1Y Now

< 10 10-15 15-20 20-25 25-30 > 30

18 May 2017

India Market Strategy 3

Can companies grow fast without innovation? The difference between economy and markets

Intuitive as it may seem to link macroeconomic trends to market performance, such a relationship is at best tenuous, in our view. Not only are market returns more P/E than EPS driven, the markets and the economy also have different structures. The economy has a very large informal component, large parts of the formal economy are not listed, and a large part of the market is driven by global factors, or is growing penetration and share.

To study these dynamics better, we divided the BSE500 stocks into four categories: Global, Macro, Penetration and Market Share. 25% of the BSE500 market cap is almost completely driven by global factors, 22% by local macro, 11% by market share (private sector banks and telecom) and 42% by penetration driven stories.

Expectedly, penetration and market share driven stories have seen much stronger organic revenue growth over the last ten years — together they are 79 of the 97 companies in the BSE500 (22% of total) that grew revenues at 25% CAGR. They have also outperformed the index over the past three and five years, with P/E multiples expanding sharply. In this note we focus primarily on the concept of Penetration and potential for growth.

Growing revenues faster than GDP is tough

We find that the 2002-16 growth in market-size for even under-penetrated categories is not too different from the growth in nominal GDP. For a category to grow meaningfully faster than nominal GDP at least one of the following must happen: (1) Innovations that bring down price points to a level where price elasticity of demand is high (e.g., sachets, mortgages); (2) Improvement in enablers (e.g., electricity for appliances, doctors to write prescriptions); (3) Improvement in distribution (local presence and brand awareness); and (4) Demographics. The first two can drive short-lived bursts of very strong growth and the latter two provide a smaller boost but over longer periods.

Whether the Indian middle class has 300 mn or 100 mn people is an important debate as only items that have very low price points have high penetration. Telecom penetration for example would not have been 90% if companies were not profitable at Rs80 ARPU. Intuitive as this is, it throws a challenge to enterprises in under-penetrated categories to innovate and cut costs to a level where one can stay profitable even at low price points.

We believe some NBFCs and banks are benefiting from a sharp fall in operating costs, enabled by improving technology and telecom penetration. A sharp improvement in electrification could be an enabler for appliance companies, and lower interest costs and more tax filings (that act as income proof) could enable better mortgage penetration. There are very few other examples that come to mind. We continue to believe that factors of production—capital, labour and land, are likely to get cheaper in India, but their impact on production costs would be slow, even though steady.

Market pricing in a tide: There may be none

Growth rates have slowed steadily in recent years—only 12% of BSE500 companies saw revenues grow faster than 25% CAGR in the last five years. During the same period P/E multiples have increased across the board—while 6% of BSE500 (232 stocks for which forward EPS is available) traded above 30x P/E five years back, now 24% do.

While this re-rating has much to do with a global increase in P/E multiples, a popular justification is a future acceleration in India's economic growth that would drive super-normal growth for companies. Our framework suggests that such acceleration would be contingent on sector and stock specific factors, and it is prudent to be selective.

Key overweights: GCPL, Havells, Crompton, BHRI, CHLF, Jubilant and ITC. Key Underweights: Nestle, Colgate, TVS Motors. We provide the rationale in Figure 9.

The relationship between the economy

and markets is tenuous at best, in our view

Stories driven by penetration (42% of

BSE500 market cap) and market share (11%)

have seen stronger organic revenue growth and also outperformed

the index over years

The growth in market size over 2002-16 is not

too different from the nominal GDP growth

and growing faster than that is tough, unless

there are a few specific drivers in place

In India, only items with

low price points have seen high penetration

The factors of production are likely to

get cheaper but their impact on production costs would be slow

Even as revenue growth has slowed

over years, P/E multiples have

expanded

18 M

ay 2

017

Ind

ia M

ark

et S

trate

gy

4

Financial Summary

Figure 9: Stock ideas

Company RIC Rating Mkt Cap

($ bn)

Comments

Recommended Overweight stocks

ITC Ltd ITC.BO OUTPERFORM 53 1. Government moving to a rational tax regime, three consecutive declines in excise hikes on cigarettes, FY18 saw just a 6% hike.

2. This should give ITC more flexibility in the volume vs. price balance, and retain bigger share of market (earlier government took much of the increase).

3. We expect ITC to return to ~15% earnings growth with a ~5% volume growth in cigarettes in in FY18. It is also the cheapest consumer staples name in our coverage.

Bharti Infratel Ltd BHRI.BO OUTPERFORM 11 1. As data prices drop sharply, volumes are likely to surge driving an increased need for towers along with incremental business from Jio.

2. Downside from Idea-Vodafone merger would at most be loss of half a year’s growth. Long term tenancy growth story is beginning to look better with a

higher benchmark being set by the Idea+Vodafone in terms of network size.

3. Path to ‘independent’ ownership is now visible.

Godrej Consumer

Products Ltd

GOCP.BO OUTPERFORM 9 1. Product innovation pace has accelerated over the last five years especially in home insecticides, e.g. the Re1 mosquito repellant and cheap air fresheners.

2. India business saw a very strong recovery in 4Q post demonetisation. Margins went up without cutting ad spends. Has high pricing power in its portfolio except soaps.

3. Worst of the currency headwinds in the international business seem behind. Company also increased div. payout to 45% from 20%.

Cholamandalam Finance CHLA.BO OUTPERFORM 3 1. Using technology creatively to not just improve operating efficiency but also to increase credit quality.

2. We see room for NIM expansion with delayed funding cost benefit and operating leverage as growth comes back in Vehicle finance.

3. It has maintained portfolio quality in its vehicle finance book albeit incurring higher operating cost. This could drive ROE expansion. At current valuations,

Chola trades at 2.6XFY19E P/B and 12.8XFY19E P/E.

Crompton Greaves

Consumer Electrical Ltd

CROP.BO OUTPERFORM 2 1. Key beneficiary of rising electrification and improving power availability through its appliances business. Making a big push in premium fans (40-50%

growth) and revamping distribution to become FMCG like.

2. Has historically been a strong franchise but now getting requisite investments. The new management at the help has rich consumer experience (P&G, Pidilite).

3. We think margins will gradually move up due to premiumisation and cost savings, results already evident.

Jubilant Foodworks JUBI.BO OUTPERFORM 1 1. Company reviving price competitiveness: lower priced items have been introduced and price hikes have ben near zero since Dec 2015. Important for volume growth.

2. Business has a very high operating leverage and thus earnings can accelerate with steady SSSG improvement.

3. Separately, they have taken several strategic decisions recently to focus on improving profitability of existing stores and moderating expansion plans.

Havells India Ltd HVEL.BO NEUTRAL 5 1. Key beneficiary of rising electrification and improving power availability through its appliances business. Also a direct play on overall economic growth

(switch gears and cable business).

2. Havells management has built strong brand equity over the years with consistent marketing spends and has the strongest pan India in domestic electricals.

3. Management is seeing some greenshoots in its core switchgear and expects double digit growth in FY18.

Recommended Underweight stocks

Nestle India NEST.BO UNDERPERFORM 10 1. The focus on margins in the last few years has meant very poor quality growth. Recent pickup in investment behind ad spends may show up with a lag.

2. Nestle has been able to get back only a 60% market share for Maggi versus the 70% before the ban.

3. P/E multiples are too high versus what we think are achievable growth rates in the coming years.

TVS Motors TVSM.BO UNDERPERFORM 4 1. As our analysis shows, supernormal growth in 2W industry revenues could be challenging.

2. TVS intends to expand market share and also expand margins through cost optimization and better product mix but we foresee challenges as competitive

intensity in 2W industry remain high.

3. Valuations are expensive even after building reasonable growth in volumes and expansion in operating margins.

Colgate-Palmolive India COLG.BO NEUTRAL 4 1. Toothpastes are a well penetrated category, and growth can only now come through premiumisation.

2. But Colgate is losing share of premium products to Patanjali and Dabur’s herbal variants. It lost an alarming 200bps worth of market share in CY16.

3. For effectively a single product company, this is a big risk. P/E multiples are too high versus what we think are achievable growth rates in the coming years.

Source: Company data, Credit Suisse estimates

18 May 2017

India Market Strategy 5

The difference between economy & markets

Markets and the local economy not always in sync

Intuitive as it may seem to link macroeconomic trends to market performance, such a

relationship is at best tenuous, in our view. Looking at GDP growth versus Nifty returns

(Figure 10), and also at the deviation of GDP growth from trend versus Nifty returns

(Figure 11), we find the relationship is weak and far from predictive. That is, one cannot

predict the performance of markets only on the basis of a strong/weak economy.

Figure 10: India GDP growth vs Nifty performance Figure 11: Deviation from GDP trend vs Nifty returns

Source: CSO, Bloomberg, Credit Suisse estimates Source: CSO, Bloomberg, Credit Suisse estimates

There are many well discussed reasons for this, including timing, that is, when the market

prices in future earnings are variable, as reflected in a volatile P/E ratio. Market returns are

as often P/E driven as they are EPS driven (Figure 12). While one can assume over time,

as the P/E remains in a range, on a long enough time horizon it should be earnings that

drive market returns, and should therefore, be linked to the economy. Interestingly,

however, even Nifty EPS growth has a weak link to GDP growth (Figure 13).

Figure 12: Split of Nifty change into P/E & EPS Figure 13: India GDP growth vs Nifty EPS growth

Source: The BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates Source: CSO, The BLOOMBERG PROFESSIONAL™ service, CS estimates

-40%

-20%

0%

20%

40%

60%

80%

100%

0%

2%

4%

6%

8%

10%

12%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Real GDP Growth Nifty Performance YoY

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

GDP: Deviation from Trend Nifty Performance YoY

-40%

-20%

0%

20%

40%

60%

80%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

12MF EPS Change 12MF P/E Change Index Change

1Y Change

-5%

0%

5%

10%

15%

20%

-10%

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Nifty EPS Growth Nominal GDP Growth (RHS)

18 May 2017

India Market Strategy 6

There are multiple reasons for this—the constitution of the markets and the economy is

different. Not only does the economy have a very large informal component, large parts of

the formal economy are also not listed (e.g., LIC, most real-estate developers, nearly 40%

of the car market, consumer appliance and cellphone producers, cola companies). In

important sectors like banks, the share of market capitalisation of PSU Banks is very

different from their share of deposits or credit (Figure 14). Further, a large part of the

market is driven by global factors (e.g., IT, Pharmaceutical exporters, Tata Motors). Lastly,

many listed companies are likely to be increasing penetration (e.g., Microfinance, cars), or

beneficiaries of large market share shifts (e.g., private sector banks).

Figure 14: PSU Banks' share of market cap is low Figure 15: Unlisted names dominate some markets

Source: Company Data, RBI, The BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

Source: Company Data, Credit Suisse estimates

Classifying stocks by their key drivers

To study these dynamics better, we divided the BSE500 stocks into four categories:

Global, Macro, Penetration, and Market Share; Figure 16 shows how these are defined.

Figure 16: Category definitions

Category Stock fundamentals primarily driven by

Global Global factors.

Macro Indian macroeconomic factors, like GDP growth, interest rates, inflation, investments, etc.

Penetration Stock/sector-specific issues, related to greater penetration, improved distribution, etc.

Market Share The sector may not be expanding meaningfully, but there are big market share shifts happening.

Source: Credit Suisse Research

■ Global: 14% by number (Figure 17) and 25% by market cap (Figure 18) is almost

completely driven by global factors: mainly IT, Metals, Energy and some Auto names.

We do not include Pharmaceuticals here (ANDA filings and India business are drivers).

■ Macro: 26% by number and 22% by market cap, the companies are driven by

domestic macroeconomic catalysts. These include Industrials, PSU Banks, Cement,

Utilities, some Energy and NBFC names and Real estate.

■ Market Share: This has only 17 names (3%)—private sector banks and telecom

companies. However, these form 11% of BSE500 market cap.

■ Penetration: The largest category both in terms of number of companies (57%), as

well as market cap (42%). This is likely the primary reason that aggregate market

revenues and profits can potentially grow faster than the nominal economic growth.

32%

74% 76%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mcap Loans Deposits

Share of PSU Banks among all banks

0%

10%

20%

30%

40%

50%

60%

70%

80%

Dairy Jewellery 2W Biscuits 4W AC LifeInsurance

Share of unlisted formal companies in overall market

18 May 2017

India Market Strategy 7

Figure 17: Split of BSE500 by Number of Companies Figure 18: Split of BSE500 by Market Cap

Source: Credit Suisse Source: RAVE, Credit Suisse estimates

Sector-wise classification into the four categories

The split for each sector is available in Figure 19. Sectors like IT, Energy and Metals are

almost entirely classified as global. Private Banks and Telecom are classified as market

share because their growth is less dependent on the growth in the sector, but more by

their ability to take share from government companies (in the case of banks), or to protect

share from new entrants (in the case of telecom). Healthcare is classified as penetration

as there is a significant growth potential in the domestic market, and most listed

companies also have large pending pipelines in the large US market. NBFCs,

Discretionary, Autos and Chemicals are classified primarily as Penetration.

Figure 19: Market cap for each sector split into the four categories, by key driver of revenue growth

Source: RAVE, Credit Suisse estimates

Penetration57%

Market Share3%

Macro26%

Global14%

Penetration42%

Market Share11%

Macro22%

Global25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

IT

Ene

rgy

Priv

ate

Ban

k

Sta

ples

PS

U B

ank

NB

FC

Aut

os

Hea

lth

Indu

stria

ls

Tel

ecom

Util

ities

Met

als

Cem

ent

Dis

cret

iona

ry

Che

mic

als

Rea

l Est

ate

Tot

al

Penetration Market Share Macro Global

18 May 2017

India Market Strategy 8

Why we classified Staples under Penetration and not Macro

We debated whether Staples should be classified as Macro or Penetration, and chose the

latter. Many if not most of these categories are well penetrated, and growth at the sector

level seems to be rarely higher than the nominal GDP growth, as we see in the next

section. But the listed companies in this space are still expanding in new product

categories and geographies. Even the largest of these firms still does not have direct

distribution or advertising reach in large swathes of India, can be called underpenetrated.

Penetration-driven stories dominate the market

Stocks in the penetration and market share categories have significantly outperformed the

market and the Global and Macro categories over three and five years (Figure 20).

Penetration showed a 25% CAGR rise over five years, versus 16% CAGR for the market.

Figure 20: Performance by Type (CAGR) Figure 21: P/E for each category over time

Source: RAVE, Credit Suisse estimates Source: RAVE, Credit Suisse estimates

However, over the past year, their performance has been in line with the overall market, as

Macro (i.e., Industrials, PSU Banks) has outperformed meaningfully. One reason for this

performance could be the sharp increase in P/E ratios for this set of stocks (Figure 21).

Figure 22: Split by 10-year growth for each category Figure 23: Category-wise split by ten-year growth

Source: Capitaline, Credit Suisse estimates Source: Capitaline, Credit Suisse estimates

28%27%

25%

28%

20% 20%

36%

15%

10%

21%

10%12%

28%

18%16%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1Y 3Y 5Y

Penetration Market Share Macro Global Total

Annualized Returns

-10% 0% 10% 20% 30% 40% 50% 60% 70%

Global

Penetration

Market Share

Macro

5Y 3Y 1Y CYTD

Change in 12M Forward PE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Penetration Macro Global Market Share Total

Decline 0-15% 15-25% 25%+

# Cos 244 119 63 15 441

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Decline 0-15% 15-25% 25%+ Total

Penetration Macro Global Market Share

# Cos 8 172 164 97 441

18 May 2017

India Market Strategy 9

22% of companies grew revenues >25% for ten years

While historical growth rates may not help predict future trends, they provide useful insights into what can drive revenue growth meaningfully higher than India's nominal GDP growth. We find that 39% of the companies in the BSE500 (441 for which ten-year records are available) failed to beat 15% growth (nominal GDP growth was 12-14%), another 37% grew between 1x and 2x nominal GDP, and 22% grew more than 25% CAGR (Figure 22). Two-thirds of companies growing this fast were in the Penetration category (Figure 23).

Figure 24: Market-cap wise split by ten-year growth Figure 25: % of companies split by ten-year growth

Source: Capitaline, Credit Suisse estimates Source: Capitaline, Credit Suisse estimates

23% of BSE500 market capitalisation grew revenues at 25% CAGR, 39% showed 15-25% growth, and as much as 36% grew less than the nominal GDP growth (Figure 24). The share by number of companies was similar (Figure 25) indicating average sizes to be similar, though these averages hide sharp sector-level disparity.

Figure 26: Sector-wise split of 25%+ growth (no.) Figure 27: Sector-wise split of 25%+ growth (Mcap)

Source: Capitaline, Credit Suisse estimates Source: Capitaline, Credit Suisse estimates

The sectoral split of companies with more than 25% ten-year revenue CAGR reveals that NBFCs and discretionary dominate in number of companies (Figure 26). However, 75% of the market capitalisation is in Private sector banks, NBFCs and companies that have made large global acquisitions, like Tata Motors, Motherson Sumi, and Vedanta (Figure 27). Discretionary companies on the other hand are relatively small—they are 20% of the companies, but add up to only 5% of the market capitalisation.

Decline2%

0-15%36%

15-25%39%

25%+23%

Split of market cap by 10Y revenue CAGR

Decline2%

0-15%39%

15-25%37%

25%+22%

Split of companies by 10Y CAGR

NBFC26%

Discretionary20%

Industrials12%

Health9%

IT7%

Pvt. Bank6%

Chemicals5%

Staples4%

Autos3%

Real Estate3%

Others5%

Split of companies with 10Y CAGR >25%

Pvt. Bank.35%

NBFC27%

Health9%

Autos8%

Industrials5%

Discretionary5%

IT3%

Metals3%

Telecom1%

Real Estate1%

Chemicals1%

Others2%

Split of Market Cap with 10Y CAGR >25%

18 May 2017

India Market Strategy 10

Growing revenues faster than GDP is tough

Most categories grow at the pace of per capita GDP

India has a low per capita GDP, and therefore, a greater potential for growth is now well

known—at least among EMs, since 1980, long-term growth rates have been inversely

proportional to the starting GDP (Figure 36). In India, growth in the nominal per capita

GDP as well as consumption per capita has averaged about 12% in the last decade

(Figure 29). A growth of 10-12% going forward is a reasonable assumption.

Figure 28: Per capita GDP PPP adjusted is low Figure 29: Per capita GDP & spending growth

Source: IMF, Credit Suisse estimates Source: CSO, Credit Suisse estimates

Intuitively, growth experienced by a category can be faster than this pace, if penetration

(defined as the number of households per 100 that use the product in a month) improves

as well. Even where penetration is high, like in detergents, (Figure 30) growth need not be

zero, as significant upgradation potential exists, like moving from low-end Rs40/kg

powders to higher-end Rs140/kg low-foam powders for front-loading washing machines.

Figure 30: Change in penetration over more than a decade (2000 to 2012)

Source: NSSO, SIAM, Credit Suisse estimates

China

India

Thailand

Indonesia

Malaysia

Turkey

Mexico

BrazilS. Africa

0%

2%

4%

6%

8%

10%

12%

0 1,000 2,000 3,000 4,000 5,000 6,000

Per Capita GDP (PPP Adjusted, US$, 1980)

CA

GR

in p

er C

ap. G

DP

(198

0-20

17)

-10%

-5%

0%

5%

10%

15%

20%

1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012 2017

GDP PFCENominal Per Capita Growth

1%4%

35%

56%

35%

42%

65%

97% 95% 96%

3%

22%

46%

52%

68% 69%

89%

97% 98% 99%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

4W 2W Bicycle Tobacco Skin Care Biscuits Toothpaste Edible Oil Soap Detergents

2000 2012

18 May 2017

India Market Strategy 11

We find that medium-term growth in market-size for a category is not too different from the

growth in nominal GDP (Figure 31). Enterprises operating in these categories can choose

to increase penetration by keeping prices subdued and growing volumes, or, like in

cigarettes, take price hikes while keeping volume growth subdued.

Figure 31: Growth in market 2002-2016 (CY) Figure 32: Price and volume are inversely related

Source: Euromonitor, Credit Suisse estimates Source: Euromonitor, Credit Suisse estimates

This is because price and volume have an inverse relationship (Figure 32). As they

should—only when a product/service becomes affordable to more people that penetration

can increase (Figure 33), which implies a reduction in real prices.

Figure 33: Companies can choose to grow volumes or price; latter is harder

Source: Credit Suisse Research

For example, an important driver of the increase in penetration of four-wheelers and two-

wheelers is the decline in real prices. Over and above the 33% decline in inflation adjusted

realisations of both two-wheelers (Figure 34) and four-wheelers (Figure 35) since 2002,

excise duties have also come down by 10-12% since 2000 (from 24% to 12.5% for two-

wheelers as well as small cars), bringing down retail prices in real terms by nearly 40%.

This is after feature upgrades and increase in sizes of both categories. In well penetrated

categories like toilet soaps, this plays out as premium products at similar real prices.

-2% 0% 2% 4% 6% 8% 10% 12% 14% 16%

Shampoo

Detergents

Bar Soap

Carbonated Drinks

Cigarettes

Tooth Paste

Tea

Alcohol

Biscuits

2W

Paints

4W

Volume Price

Expenditure G

rowth

Revenue Growth 2002-16

Shampoo

Detergents

Bar Soap

Carbonated Drinks

Cigarettes

Tooth Paste

Tea

AlcoholBiscuits

2W

Paints

4W

0%

2%

4%

6%

8%

10%

12%

-2% 0% 2% 4% 6% 8% 10% 12%

Volume Growth CAGR (2002-16)P

rice

Gro

wth

CA

GR

(20

02-1

6)

Drivers of 2002-16 revenue growth

18 May 2017

India Market Strategy 12

Figure 34: Real 2W realisations down 33% 2003-17 Figure 35: Real 4W realisations down 33% 2003-17

Source: Company Data, CMIE, Credit Suisse estimates Source: Company Data, CMIE, Credit Suisse estimates

Drivers of category penetration/market growth

For a category to grow meaningfully faster than the per capita consumption growth, at

least one of the following must happen. Of these the first two can cause sharp acceleration

for a few years, and the last two a moderate pick-up in growth over a longer period:

1. Innovations that bring down price points meaningfully: The income pyramid is not

smooth with a price elasticity of -1, i.e., the improvement in volumes need not be the

same as the decline in prices. At certain inflection points, price elasticity of demand

can be high and volume growth can offset price declines, growing the market strongly

in value terms, e.g., cellphones/smartphones, computers and banking.

These need not only be technological innovations—economic ones like shampoo

sachets (rural penetration improved from 13% in 2000 to 32% by 2005, and currently

90%), or buying consumer appliances on EMI (brings down the price point at which a

product becomes affordable) can be very potent too. If affordable housing can work,

say by using cheap land made available by government departments or public sector

units, together with subsidised mortgages, that would also be an economic innovation.

2. Improvement in Infrastructure/Enablers: There are several examples here:

− Consumer appliances are useless without availability of electricity, even if the

products are affordable. Improvement in the quality and quantity of power supply is

necessary to help the category grow.

− Availability of good roads is necessary for vehicle ownership.

− Improvement in doctor availability improves demand for pharmaceuticals

− Growth in tax filers/salaried employees helps mortgage demand as this helps

provide a proof of income needed for disciplined mortgage lending.

3. Improvement in distribution: Some goods and services require local presence,

lending and banking being the most obvious examples. Due to elevated operating

costs some businesses may not be able to expand their distribution. However, through

efficient processes and automation, companies can expand their geographical

footprint while bringing down their costs of operation. HDFC's mortgages are a good

example—it has grown its branch strength manifold (Figure 36) in an under-

penetrated market, helped by a falling cost-to-income ratio (Figure 37).

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2003 2005 2007 2009 2011 2013 2015 2017

Avg. realization 2W (Rs/vehicle) Real Terms

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Avg. realization 4W (Rs/vehicle) Real Terms

18 May 2017

India Market Strategy 13

Even for companies operating in well-penetrated categories, distribution reach is still

limited. We, therefore, classify Staples companies as penetration-driven despite their

categories being mature. This also explains the relatively strong reported growth of

categories like edible oils—demand for fats is rising faster than the average food

demand, but only by a few percentage points. The main reason for the growth is the

transition from loose, unbranded oils to branded packaged edible oil.

Figure 36: HDFC's branch network Figure 37: HDFC's cost-to-income ratio 1998-2017

Source: Company Data, Credit Suisse estimates Source: Company Data, Credit Suisse estimates

4. Demographics: Demographic trends also support greater penetration of some

categories, like the use of pre-prepared foods and packaged masalas can be linked to

more women joining the workforce (at the high-end this also explains the demand for

studded jewelry). While these trends are very powerful, their impact is rarely sudden.

The price point is critical: It is all about unit costs

Figure 38: Household penetration of various categories

Source: NSSO, Credit Suisse estimates

Whether the Indian middle class has 300 mn or 100 mn people is an important debate—

only the cheaper items (Figure 38), i.e., those that have very low price points, have high

penetration. Intuitive as this is, it throws a challenge to enterprises in under-penetrated

0

50

100

150

200

250

300

350

400

450

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

No. of HDFC Outlets

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

HDFC Ltd. Cost to Income Ratio

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mic

row

ave

Mal

ted

Foo

ds

Car

bona

ted

Drin

ks

4W

Cig

aret

tes

Com

pute

r

Was

hing

Mac

hine

Alc

ohol

MF

Fol

ios

Ref

riger

ator

2W

Sal

ty S

nack

s

TV

Ski

n ca

re

Bis

cuits

Cho

cola

tes

Tea

Mob

ile P

hone

Too

thpa

ste

Hai

r oi

l

Sha

mpo

o

Edi

ble

Oil

Soa

p

Det

erge

nts

Ban

k A

ccou

nt

Household Penetration of Various goods and services

18 May 2017

India Market Strategy 14

categories for bringing operating costs to a level where even at rock bottom revenues one

can stay profitable. For example, telecom penetration would not have reached 90% if the

telecom sector was not profitable at Rs100 ARPU (Figure 39). Similarly, while TV

penetration in India is not universal, nearly every TV-owning household has

cable/satellite—the highest such ratio in the world, primarily as subscription costs are the

lowest globally.

Figure 39: Telecom ARPUs vs penetration Figure 40: % of households with bank accounts

Source: Company Data, Trai, Credit Suisse estimates Source: PMJDY, Census 2011, Credit Suisse estimates

Banking penetration increase driven by falling transaction costs

In our view, banking penetration would not have grown (Figure 40) without a sharp decline

in operating costs, which brought down the minimum balance at which an account

becomes viable for a bank. Transaction cost for an ATM cash withdrawal is nearly a third

of a withdrawal from a bank branch, and mobile banking transfers are nearly zero-cost in

comparison; further, Aadhaar as KYC (Know Your Client) is faster and much cheaper than

paper KYC. A meaningful part of this improvement has come from technology and

widespread availability of cheap telecom services.

Figure 41: Number of MFI accounts Figure 42: NBFC operating ratio

Source: MFIN, Credit Suisse estimates Source: Company Data, Credit Suisse estimates

0%

25%

50%

75%

100%

0

100

200

300

400

Mar-05 Jun-06 Sep-07 Dec-08 Mar-10 Jun-11 Sep-12 Dec-13 Mar-15 Jun-16

Industry ARPU (Rs/sub/month) Mobile Telecom Penetration (RHS)

Removal of inactive subscribers from records

Sharp jump as RJio brought down ARPUs

Strong penetration growth as ARPUs fell by three-fourths

0%

20%

40%

60%

80%

100%

Mar-01 Mar-11 Nov-14 Jan-15

% Households having banking facilities

PMJDY launched

-20%

-10%

0%

10%

20%

30%

40%

50%

0

5

10

15

20

25

30

35

40

45

2012 2013 2014 2015 2016 2017

MFI Accounts (mn) YoY (RHS)

0.60%

0.70%

0.80%

0.90%

1.00%

1.10%

1.20%

1.30%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Employee Cost Other Opex

As % of AUM (Shriram Transport)

18 May 2017

India Market Strategy 15

NBFCs benefit from banking penetration, databases and innovation

The rapid scale up in retail lending and microfinance (Figure 41) has benefited from similar

trends—online transfers to bank accounts are significantly less expensive than cash

collection and disbursements, making it easier for NBFCs to operate. A drop in operating

costs allows the NBFC to expand its geographical footprint, and therefore, its customer

base. We show Shriram Transport (Figure 42) as an example; as we earlier saw HDFC's

operating costs have come down sharply too (Figure 36).

A sharp drop in credit assessment costs has helped too—earlier manual evaluations of

creditworthiness that could cost several hundred rupees would have been 1 pp or more of

the loan issued (say a consumer durable loan of Rs25,000); but loan viability assessment

through databases like CIBIL or MFIN brings costs down to a fraction, and smaller ticket-

size loans can be disbursed as well.

Figure 43: NBFC AUMs growth stays steady Figure 44: Growth in durables has been steady

Source: Company Data, Credit Suisse estimates Source: Company Data, Credit Suisse estimates

While the ability to break a large purchase into smaller monthly payments may have

improved the affordability of durables, such a trend is not yet visible (Figure 44)—the

growth in durables has been steady even as the share of sales financed by Bajaj Finance

(which dominates the durables financing market) has risen sharply.

Cheaper factors of production to help, but slowly

All three factors of production, i.e. land, labour and capital have historically been very

costly in India. A fourth, enterprise formation, has been impeded by excessive regulation.

Not only has this hurt India's export competitiveness, necessitating several government

interventions (like allowing global financing for export oriented units to bring down cost of

capital); it has slowed improvements in production efficiency that could have brought down

costs, and hence, improved penetration of various products and also substituted imports.

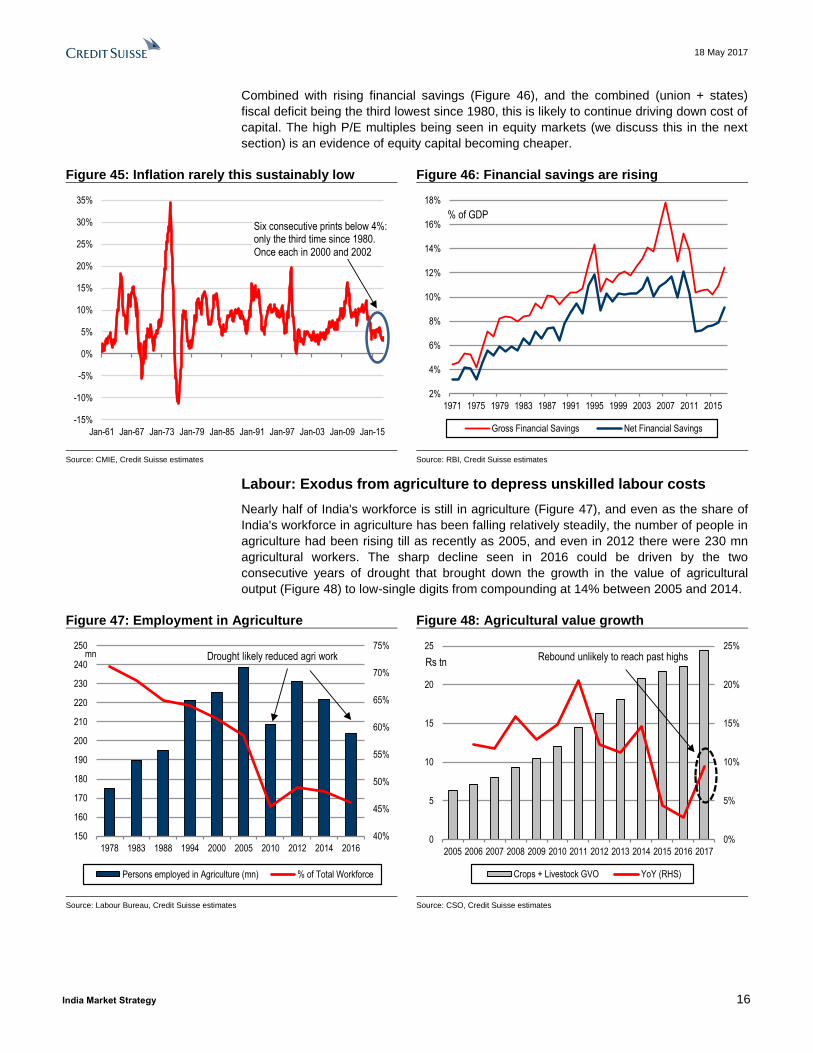

Capital: Falling inflation, rising financial savings, falling repression

However, changes are afoot—with inflation below 3% in April 2017, we have now had six

consecutive months of sub-4% inflation; the last time this happened was in 2002 (Figure

45), and only the third time since 1980. Unlike the episodes before 1980, this appears

sustainable. While the RBI has been reluctant to project the current low inflation levels

going forward, apprehending price increases driven by GST and the pay commission's

recommendations, sustenance of such trends would mean lower interest rates.

0%

5%

10%

15%

20%

25%

2012 2013 2014 2015 2016 2017

NBFC AUM Growth YoY0%

10%

20%

30%

40%

50%

60%

CY13 CY14 CY15 CY16

Indian cons. durables sales growth

Bajaj cons. durables segmentgrowth

18 May 2017

India Market Strategy 16

Combined with rising financial savings (Figure 46), and the combined (union + states)

fiscal deficit being the third lowest since 1980, this is likely to continue driving down cost of

capital. The high P/E multiples being seen in equity markets (we discuss this in the next

section) is an evidence of equity capital becoming cheaper.

Figure 45: Inflation rarely this sustainably low Figure 46: Financial savings are rising

Source: CMIE, Credit Suisse estimates Source: RBI, Credit Suisse estimates

Labour: Exodus from agriculture to depress unskilled labour costs

Nearly half of India's workforce is still in agriculture (Figure 47), and even as the share of

India's workforce in agriculture has been falling relatively steadily, the number of people in

agriculture had been rising till as recently as 2005, and even in 2012 there were 230 mn

agricultural workers. The sharp decline seen in 2016 could be driven by the two

consecutive years of drought that brought down the growth in the value of agricultural

output (Figure 48) to low-single digits from compounding at 14% between 2005 and 2014.

Figure 47: Employment in Agriculture Figure 48: Agricultural value growth

Source: Labour Bureau, Credit Suisse estimates Source: CSO, Credit Suisse estimates

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Jan-61 Jan-67 Jan-73 Jan-79 Jan-85 Jan-91 Jan-97 Jan-03 Jan-09 Jan-15

Six consecutive prints below 4%: only the third time since 1980. Once each in 2000 and 2002

2%

4%

6%

8%

10%

12%

14%

16%

18%

1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2015

Gross Financial Savings Net Financial Savings

% of GDP

40%

45%

50%

55%

60%

65%

70%

75%

150

160

170

180

190

200

210

220

230

240

250

1978 1983 1988 1994 2000 2005 2010 2012 2014 2016

Persons employed in Agriculture (mn) % of Total Workforce

Drought likely reduced agri workmn

0%

5%

10%

15%

20%

25%

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Crops + Livestock GVO YoY (RHS)

Rs tnRebound unlikely to reach past highs

18 May 2017

India Market Strategy 17

Normal rainfall last year increased the sown area, and likely created more agricultural

jobs. However, as growing output met slowing demand (please refer to our reports

Agriculture: The Problem is Plenty, and "Interest"ing Times for details on this theme),

prices declined. This has been the root cause of slowing inflation, and has also resulted in

continuing agricultural distress despite the good monsoons. With monsoons now projected

to be normal in 2017 as well, this trend may persist. Thus, the minor pick-up in rural wage

growth that we have seen over the past few months (Figure 49) may not sustain, as

farmers adjust their costs of production to the changing realities of agriculture. This may

benefit construction companies who keep their costs low.

Figure 49: Rural wage growth Figure 50: India has very low rental yields

Source: Labour Bureau, Credit Suisse estimates Source: Global Property Guide, Credit Suisse estimates

Land: Weaker agri income, black money clampdown to make it cheaper

High land costs inflate project expenses—in real-estate, they show up in the lowest rental

yields in the world despite a high-interest environment (Figure 50). As most farmers

deployed their excess savings in hard assets (silver, gold, land), slowing agricultural

income growth brings down demand for land. The clampdown on black money is likely to

further hurt land demand as it was one of the preferred mechanisms to hide black money.

While all these factors becoming cheaper is very positive over the medium term, all of this

is great over the medium term, but will take time.

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Jan-03 Aug-04 Mar-06 Oct-07 May-09 Dec-10 Jul-12 Feb-14 Sep-15

Nominal Wage Growth Real Wage Growth

Rural Agri Wage Growth

0% 2% 4% 6% 8% 10%

India

China

UK

Russia

Germany

Japan

South Africa

USA

Australia

Malaysia

Brazil

Mexico

Philippines

Indonesia

Gross Rental Yields

18 May 2017

India Market Strategy 18

Enablers improve; distribution growth may continue

Figure 51: Electrification of households improving Figure 52: Power availability/quality improving too

Source: Census 2011, Credit Suisse estimates Source: Prayas, Credit Suisse estimates

As we have been highlighting over the past five years, there has been a substantial

improvement in household electrification in the recent years (Figure 51), and this trend

continues. As political priorities shift, the quality of electricity available has improved as

well (Figure 52). Night-time satellite pictures of India published by NASA show a

substantial improvement in the last five years (Figure 53).

Figure 53: Evidence of a substantial improvement in electrification and availability—night-time pictures

Source: NASA, ESRI, Credit Suisse

44%55%

75%

88%93%

99%

56%67%

83%

0%

20%

40%

60%

80%

100%

2001 2011 2017

Rural Urban India

% Households Electrified

0

2

4

6

AP BI GA KN MH MP UP HR

State Capital District HeadquartersOther Municipal Area Gram Panchayat(hrs)

Availability of power supply in 6 hours

18 May 2017

India Market Strategy 19

In addition to the impact on GDP and productivity, this creates opportunity to sell

consumer appliances. Further, the improvement in TV and cable/DTH penetration (Figure

54) that this engenders help brands reach new areas. Improving rural road connectivity

(Figure 55) helps extend supply chains. Thus, distribution should continue to improve.

These trends, however, are only slightly more rapid than the demographic changes.

Figure 54: TV/DTH allow for brand-building Figure 55: Rural roads penetration up sharply

Source: Company Data, Credit Suisse estimates Source: PMGSY, Credit Suisse estimates

25%

30%

35%

40%

45%

50%

55%

60%

65%

100

110

120

130

140

150

160

170

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total no. of TV households (mn) C&S penetration (%, RHS)

0

25

50

75

100

125

150

0

100

200

300

400

500

600

700

Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14 Mar-16 Mar-18

Roads Completed, Cum. ('000 km) Habitations, Cum ('000, RHS)

18 May 2017

India Market Strategy 20

Market pricing in a tide: There may be none

Growth has slowed sharply in the last few years

As discussed in the first section, 22-23% of companies in the BSE500 have managed to

grow faster than 2x nominal GDP in the last ten years. This mostly has private sector

banks and some NBFCs among the larger market capitalisation set (Figure 26). In recent

years, however, growth has slowed meaningfully, with only 9% of the companies (Figure

56), adding up to 7% of market capitalisation (Figure 57) showing 25% growth in FY16.

Figure 56: BSE500 split by revenue growth (No.) Figure 57: BSE500 split by revenue growth (MCap)

Source: Capitaline, Credit Suisse estimates Source: Capitaline, Credit Suisse estimates

When P/E multiples have risen across the board

On the other hand, all this while P/E multiples have been going up (Figure 58).

Figure 58: BSE500 P/E has risen sharply Figure 59: P/E multiples have risen across the board

Source: Bloomberg, Credit Suisse estimates Source: Capitaline, RAVE, Credit Suisse estimates

Whereas five years back only 6% of companies (232 of the BSE500 that have forward

earnings available) had P/E greater than 30x, now nearly a fourth of companies fall in that

bracket (Figure 59), and 44% of them have P/E greater than 20x.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

10Y 5Y 3Y 1Y

Decline 0-15% 15-25% 25%+

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

10Y 5Y 3Y 1Y

Decline 0-15% 15-25% 25%+

7x

12x

17x

22x

27x

Jul-05 Oct-06 Jan-08 Apr-09 Jul-10 Oct-11 Jan-13 Apr-14 Jul-15 Oct-16

Trailing 12 Months P/E 12 Month Forward P/E

BSE500 P/E

42%33%

25%15%

25%

23%

23%

22%

14%

19%

18%

19%

8%11%

14%

12%

5%4%

4%

8%

6% 10%16%

24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

5Y 3Y 1Y Now

< 10 10-15 15-20 20-25 25-30 > 30

18 May 2017

India Market Strategy 21

Re-rating strongest in Market-share and Macro

As one would expect, the Penetration and Market Share categories have the highest P/E

(Figure 60), and have re-rated sharply since 2012. Global P/E has seen the least

movement. Till last year the P/E for Macro was lower than in 2011, but since then has

rallied sharply, partly due to a rebound in PSU Banks, but also as government ordering

has boosted construction order books, and reduction in interest rates has helped earnings.

Figure 60: Over five years all of Penetration, Market Share and Macro have seen P/E re-rating

Source: RAVE, Credit Suisse estimates

The P/E premium of Penetration category continues to be elevated, but is meaningfully

lower than in 2013 (Figure 61). However, that of Market Share and Macro is now

approaching its peak. The discount for Global continues to increase, as the category does

not seem to be participating in the broader market rally.

Figure 61: P/E premium to overall market by category

Source: RAVE, Credit Suisse estimates

5

10

15

20

25

30

1-Jan-11 1-Jun-11 1-Nov-11 1-Apr-12 1-Sep-12 1-Feb-13 1-Jul-13 1-Dec-13 1-May-14 1-Oct-14 1-Mar-15 1-Aug-15 1-Jan-16 1-Jun-16 1-Nov-16 1-Apr-17

Penetration Market Share Macro Global Total12MF PE

-60%

-40%

-20%

0%

20%

40%

60%

80%

1-Jan-11 1-Jun-11 1-Nov-11 1-Apr-12 1-Sep-12 1-Feb-13 1-Jul-13 1-Dec-13 1-May-14 1-Oct-14 1-Mar-15 1-Aug-15 1-Jan-16 1-Jun-16 1-Nov-16 1-Apr-17

Penetration Market Share Macro Global12MF PE

18 May 2017

India Market Strategy 22

Global factors have also contributed to re-rating

Much of the increase in P/E multiples in India appears to be driven by global factors

(Figure 62), with premiums of most sector indices of MSCI India over those of MSCI World

remaining broadly unchanged over the past five years. The increase in Telecom is likely

driven by the sharp earnings cuts and the drop in the Indian IT premium (to a discount

now) is due to market concerns with medium-term growth and the US trade restrictions (a

view we disagree with). The growth in P/E multiples and the continuing premium for most

sectors also presumes a growth acceleration in the coming years.

Figure 62: Sector-wise P/E premium of MSCI India sector indices to MSCI World indices

Source: Bloomberg, Credit Suisse estimates

In the last two decades India has indeed seen a proliferation of companies with US$1 bn

or more in sales (Figure 63), with 184 companies reporting sales higher than that

threshold in FY16. The number of companies with US$1 bn or more in market

capitalisation has also continued to rise, with the number now at 282 (Figure 64).

Figure 63: # of listed companies with US$1 bn sales Figure 64: # of companies with US$1 bn MCap

Source: The BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates Source: The BLOOMBERG PROFESSIONAL™ service, Credit Suisse estimates

-60%

-40%

-20%

0%

20%

40%

60%

80%

Total Discretionary Staples Energy Financials Healthcare Industrials IT Materials Telecom Utilities

5Y 3Y 1Y Now

MSCI India's Premium to MSCI World 304%

0 0

37

122

180 184

0

50

100

150

200

250

300

1995 2000 2005 2010 2015 Now

No. of companies with >=$1bn Sales

1526

91

210223

282

0

50

100

150

200

250

300

1995 2000 2005 2010 2015 Now

No. of companies with >=$1bn Market Cap.

18 May 2017

India Market Strategy 23

Extraordinary growth only in a few sectors

While the increase in P/E multiples, and therefore, implied growth expectations has been

broad-based within the Penetration category (Figure 65), growth going forward may not be

as indiscriminate. As discussed in the previous section, improving penetration

meaningfully in a short period of time requires innovation or a substantial improvement in

the enabling environment.

We believe that these are only available in banking, some NBFCs, and in consumer

appliances, driven by the rapid improvement in electrification and quality of electricity. For

most of Staples, that forms the largest component of the Penetration category (Figure 66),

such growth is unlikely, except in pockets (e.g., sachets even for premium shampoos, or

the innovations in insecticides and room fresheners introduced by Godrej Consumer). We

believe that the government slowing down on increasing taxes for cigarettes can drive

more balanced volume vs price growth for ITC.

Figure 65: P/E by sector for Penetration category Figure 66: Split of Penetration category by sector

Source: RAVE, Credit Suisse estimates Source: RAVE, Credit Suisse estimates

Recommended Trades

In the Penetration category, we suggest ten trade ideas based on our analysis and the

theme developed in this report (Figure 67).

Recommended Overweight: ITC, Jubilant, Chola Finance, GCPL, Havells, Crompton,

Bharti Infratel

Recommended Underweight: Nestle, Colgate, TVS Motors.

0x 5x 10x 15x 20x 25x 30x 35x

Utilities

Real Estate

IT

Pharma

Industrials

Autos

NBFC

Chemicals

Cons. Disc.

Staples

Now 3Y

12MF P/E for Penetration category

Staples21%

NBFC20%

Autos17%

Health15%

Discretionary15%

Chemicals5%

Utilities2%

IT2%

Industrials1%

Telecom2%

18 M

ay 2

017

Ind

ia M

ark

et S

trate

gy

2

4

Financial Summary

Figure 67: Stock ideas

Company RIC Rating Mkt Cap

($ bn)

Comments

Recommended Overweight stocks

ITC Ltd ITC.BO OUTPERFORM 53 1. Government moving to a rational tax regime, three consecutive declines in excise hikes on cigarettes, FY18 saw just a 6% hike.

2. This should give ITC more flexibility in the volume vs. price balance, and retain bigger share of market (earlier government took much of the increase).

3. We expect ITC to return to ~15% earnings growth with a ~5% volume growth in cigarettes in in FY18. It is also the cheapest consumer staples name in our coverage.

Bharti Infratel Ltd BHRI.BO OUTPERFORM 11 1. As data prices drop sharply, volumes are likely to surge driving an increased need for towers along with incremental business from Jio.

2. Downside from Idea-Vodafone merger would at most be loss of half a year’s growth. Long term tenancy growth story is beginning to look better with a

higher benchmark being set by the Idea+Vodafone in terms of network size.

3. Path to ‘independent’ ownership is now visible.

Godrej Consumer

Products Ltd

GOCP.BO OUTPERFORM 9 1. Product innovation pace has accelerated over the last five years especially in home insecticides, e.g. the Re1 mosquito repellant and cheap air fresheners.

2. India business saw a very strong recovery in 4Q post demonetisation. Margins went up without cutting ad spends. Has high pricing power in its portfolio except soaps.

3. Worst of the currency headwinds in the international business seem behind. Company also increased div. payout to 45% from 20%.

Cholamandalam Finance CHLA.BO OUTPERFORM 3 1. Using technology creatively to not just improve operating efficiency but also to increase credit quality.

2. We see room for NIM expansion with delayed funding cost benefit and operating leverage as growth comes back in Vehicle finance.

3. It has maintained portfolio quality in its vehicle finance book albeit incurring higher operating cost. This could drive ROE expansion. At current valuations,

Chola trades at 2.6XFY19E P/B and 12.8XFY19E P/E.

Crompton Greaves

Consumer Electrical Ltd

CROP.BO OUTPERFORM 2 1. Key beneficiary of rising electrification and improving power availability through its appliances business. Making a big push in premium fans (40-50%

growth) and revamping distribution to become FMCG like.

2. Has historically been a strong franchise but now getting requisite investments. The new management at the help has rich consumer experience (P&G, Pidilite).

3. We think margins will gradually move up due to premiumisation and cost savings, results already evident.

Jubilant Foodworks JUBI.BO OUTPERFORM 1 1. Company reviving price competitiveness: lower priced items have been introduced and price hikes have ben near zero since Dec 2015. Important for volume growth.

2. Business has a very high operating leverage and thus earnings can accelerate with steady SSSG improvement.

3. Separately, they have taken several strategic decisions recently to focus on improving profitability of existing stores and moderating expansion plans.

Havells India Ltd HVEL.BO NEUTRAL 5 1. Key beneficiary of rising electrification and improving power availability through its appliances business. Also a direct play on overall economic growth

(switch gears and cable business).

2. Havells management has built strong brand equity over the years with consistent marketing spends and has the strongest pan India in domestic electricals.

3. Management is seeing some greenshoots in its core switchgear and expects double digit growth in FY18.

Recommended Underweight stocks

Nestle India NEST.BO UNDERPERFORM 10 1. The focus on margins in the last few years has meant very poor quality growth. Recent pickup in investment behind ad spends may show up with a lag.

2. Nestle has been able to get back only a 60% market share for Maggi versus the 70% before the ban.

3. P/E multiples are too high versus what we think are achievable growth rates in the coming years.

TVS Motors TVSM.BO UNDERPERFORM 4 1. As our analysis shows, supernormal growth in 2W industry revenues could be challenging.

2. TVS intends to expand market share and also expand margins through cost optimization and better product mix but we foresee challenges as competitive

intensity in 2W industry remain high.

3. Valuations are expensive even after building reasonable growth in volumes and expansion in operating margins.

Colgate-Palmolive India COLG.BO NEUTRAL 4 1. Toothpastes are a well penetrated category, and growth can only now come through premiumization.

2. But Colgate is losing share of premium products to Patanjali and Dabur’s herbal variants. It lost an alarming 200bps worth of market share in CY16.

3. For effectively a single product company, this is a big risk. P/E multiples are too high versus what we think are achievable growth rates in the coming years.

Source: Company data, Credit Suisse estimates

18 May 2017

India Market Strategy 25

Companies Mentioned (Price as of 18-May-2017) Bajaj Finance Ltd (BJFN.BO, Rs1322.8) Bharti Infratel Ltd (BHRI.BO, Rs390.2) Cholamandalam Finance (CHLA.BO, Rs1042.05) Colgate-Palmolive India (COLG.BO, Rs977.3) Crompton Greaves Consumer Electrical Limited (CROP.BO, Rs241.65) Godrej Consumer Products Ltd (GOCP.BO, Rs1857.95) Havells India Ltd (HVEL.BO, Rs508.8) Housing Development Finance Corp (HDFC.BO, Rs1552.65) ITC Ltd (ITC.BO, Rs281.85) Jubilant Foodworks (JUBI.BO, Rs1049.45) Nestle India (NEST.BO, Rs6554.65) TVS Motors (TVSM.BO, Rs532.75)

Disclosure Appendix

Analyst Certification Neelkanth Mishra, Prateek Singh and Ravi Shankar each certify, with respect to the companies or securities that the individual analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows: Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months. Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months. Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months. *Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiv eness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap wi th Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011. Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the company at this time. Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation: Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months. Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months. Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months. *An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Credit Suisse's distribution of stock ratings (and banking clients) is:

Global Ratings Distribution

Rating Versus universe (%) Of which banking clients (%) Outperform/Buy* 44% (64% banking clients) Neutral/Hold* 39% (61% banking clients) Underperform/Sell* 14% (54% banking clients) Restricted 2% *For purposes of the NYSE and FINRA ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, and Un derperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdin gs, and other individual factors.

Important Global Disclosures Credit Suisse’s research reports are made available to clients through our proprietary research portal on CS PLUS. Credit Suisse research products may also be made available through third-party vendors or alternate electronic means as a convenience. Certain research products are only made available through CS PLUS. The services provided by Credit Suisse’s analysts to clients may depend on a specific client’s preferences regarding the

18 May 2017

India Market Strategy 26

frequency and manner of receiving communications, the client’s risk profile and investment, the size and scope of the overall client relationship with the Firm, as well as legal and regulatory constraints. To access all of Credit Suisse’s research that you are entitled to receive in the most timely manner, please contact your sales representative or go to https://plus.credit-suisse.com . Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein. Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: https://www.credit-suisse.com/sites/disclaimers-ib/en/managing-conflicts.html . Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties. This material is intended for your use only and not for general distribution. This material is not intended to promote or procure a particular outcome in the UK General Election (the "Election"). Credit Suisse does not promote or endorse any party in the Election. This material does not constitute, and should not be interpreted as, a recommendation by Credit Suisse as to the merits of a particular outcome of the Election. See the Companies Mentioned section for full company names The subject company (JUBI.BO, ITC.BO, CROP.BO, BHRI.BO, NEST.BO, BJFN.BO, HDFC.BO) currently is, or was during the 12-month period preceding the date of distribution of this report, a client of Credit Suisse. Credit Suisse provided investment banking services to the subject company (JUBI.BO, CROP.BO, NEST.BO, HDFC.BO) within the past 12 months. Credit Suisse provided non-investment banking services to the subject company (JUBI.BO, ITC.BO, NEST.BO, BJFN.BO, HDFC.BO) within the past 12 months Credit Suisse has managed or co-managed a public offering of securities for the subject company (NEST.BO, HDFC.BO) within the past 12 months. Credit Suisse has received investment banking related compensation from the subject company (JUBI.BO, CROP.BO, NEST.BO, HDFC.BO) within the past 12 months Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (CHLA.BO, JUBI.BO, CROP.BO, BHRI.BO, NEST.BO, COLG.BO, BJFN.BO, HDFC.BO) within the next 3 months. Credit Suisse has received compensation for products and services other than investment banking services from the subject company (JUBI.BO, ITC.BO, NEST.BO, BJFN.BO, HDFC.BO) within the past 12 months A member of the Credit Suisse Group is party to an agreement with, or may have provided services set out in sections A and B of Annex I of Directive 2014/65/EU of the European Parliament and Council ("MiFID Services") to, the subject issuer (HVEL.BO, JUBI.BO, GOCP.BO, CROP.BO, BHRI.BO, TVSM.BO, NEST.BO, COLG.BO, BJFN.BO, HDFC.BO) within the past 12 months. Please visit https://credit-suisse.com/in/researchdisclosure for additional disclosures mandated vide Securities And Exchange Board of India (Research Analysts) Regulations, 2014 Credit Suisse may have interest in (HVEL.BO, CHLA.BO, JUBI.BO, GOCP.BO, ITC.BO, CROP.BO, BHRI.BO, TVSM.BO, NEST.BO, COLG.BO, BJFN.BO, HDFC.BO) As of the end of the preceding month, Credit Suisse beneficially own 1% or more of a class of common equity securities of (JUBI.BO). Credit Suisse beneficially holds >0.5% long position of the total issued share capital of the subject company (JUBI.BO).

For other important disclosures concerning companies featured in this report, including price charts, please visit the website at https://rave.credit-suisse.com/disclosures or call +1 (877) 291-2683. For date and time of production, dissemination and history of recommendation for the subject company(ies) featured in this report, disseminated within the past 12 months, please refer to the link: https://rave.credit-suisse.com/disclosures/view/report?i=301798&v=-qaxnpgu4s8mvt2ln18cwmgkh .