individual and organizational ethics: challenges and opportunities beach... · ·...

TRANSCRIPT

Individual and Organizational Ethics: Challenges and Opportunities

Lawrence Kalbers, Ph.D., CPA R. Chad Dreier Chair in Accounting Ethics

Chair, Department of Accounting Director, Center for Accounting Ethics, Governance, and the Public Interest

Loyola Marymount University [email protected]

March 16, 2017

Overview

• Ethics • Using an ethical decision making model • Ethical culture and management • Aligning ethics, values, and governance • Why is it so hard to be ethical? • IIA Ethics • AICPA revised Code of Professional Conduct • Consequences of unethical behavior • Improving individual and organizational ethics and

decisions

Ethics

• Personal (Individual) • Professional (AICPA, IFAC, etc.)

(Individual and Professional Organizations)

• Organizational (mission, values, codes)

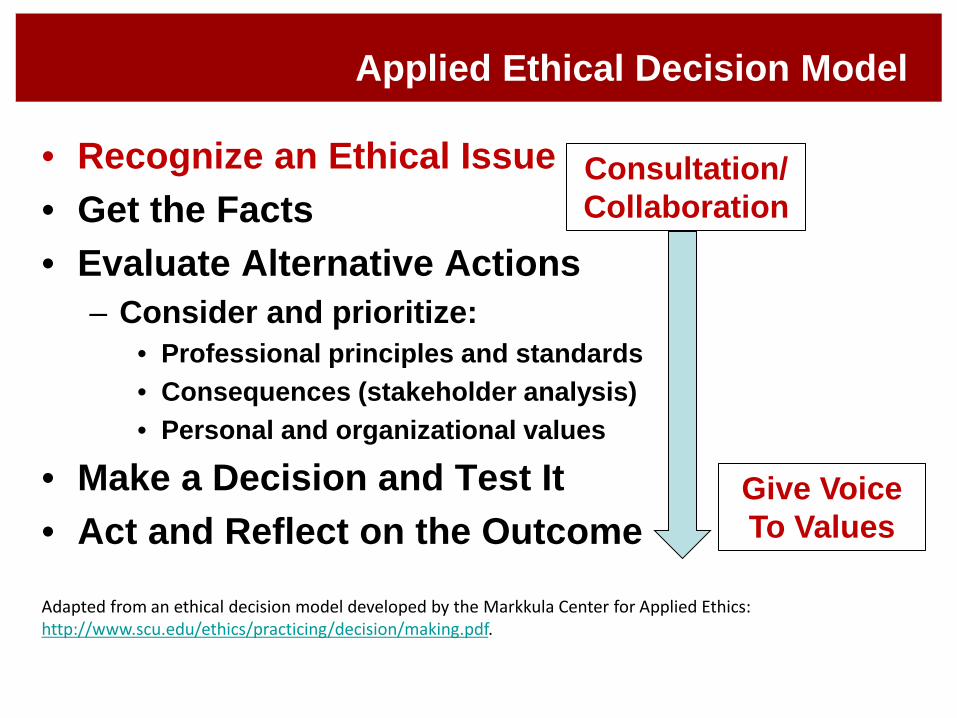

Applied Ethical Decision Model

• Recognize an Ethical Issue • Get the Facts • Evaluate Alternative Actions

– Consider and prioritize: • Professional principles and standards • Consequences (stakeholder analysis) • Personal and organizational values

• Make a Decision and Test It • Act and Reflect on the Outcome

Adapted from an ethical decision model developed by the Markkula Center for Applied Ethics: http://www.scu.edu/ethics/practicing/decision/making.pdf.

Consultation/ Collaboration

Give Voice To Values

Corporate Culture

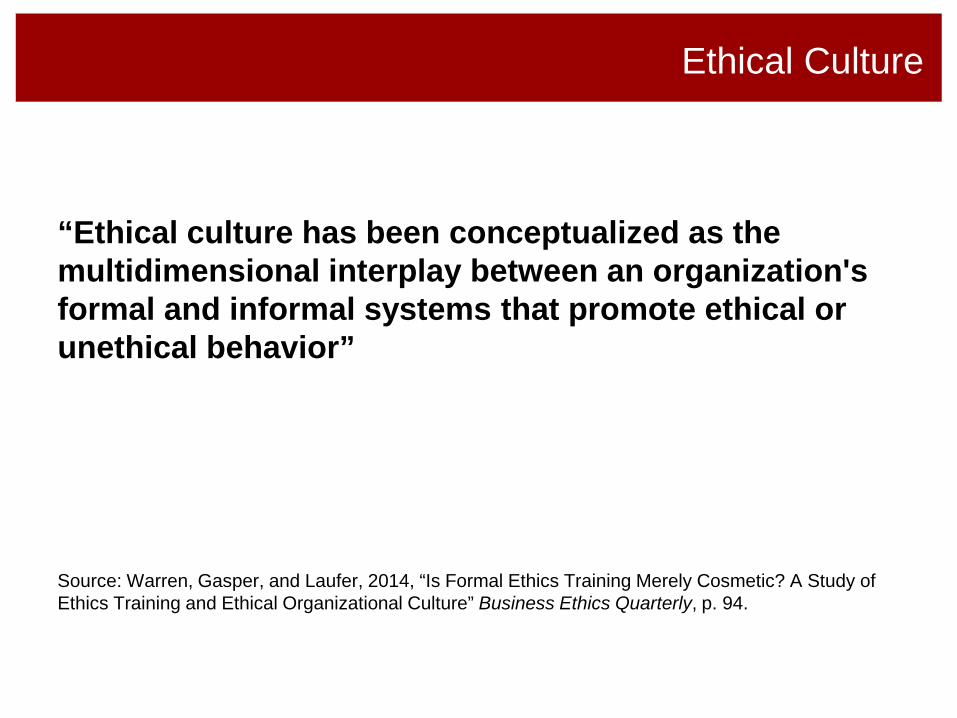

Ethical Culture

“Ethical culture has been conceptualized as the multidimensional interplay between an organization's formal and informal systems that promote ethical or unethical behavior”

Source: Warren, Gasper, and Laufer, 2014, “Is Formal Ethics Training Merely Cosmetic? A Study of Ethics Training and Ethical Organizational Culture” Business Ethics Quarterly, p. 94.

Corporate Culture

Think of an organization that might fit the descriptions below for “corporate culture.” • The Good • The Bad • The Ugly

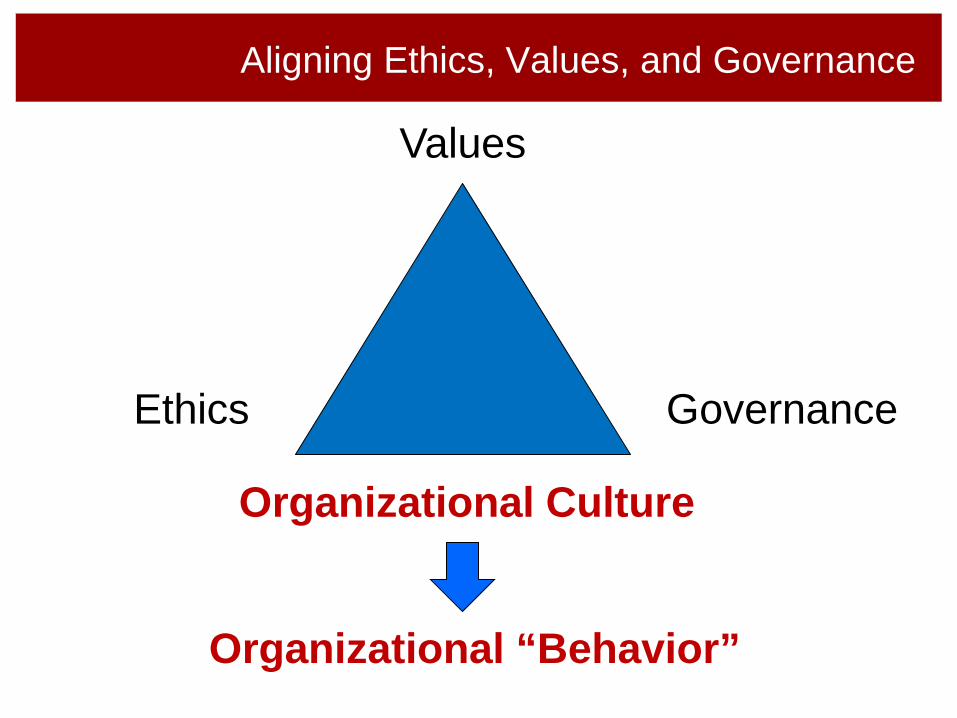

Aligning Ethics, Values, and Governance

Organizational Culture

Ethics

Values

Governance

Organizational “Behavior”

Negative Causes and Consequences of Organizational Culture

• Product safety and recalls • Poor governance

Recent product recall example 1

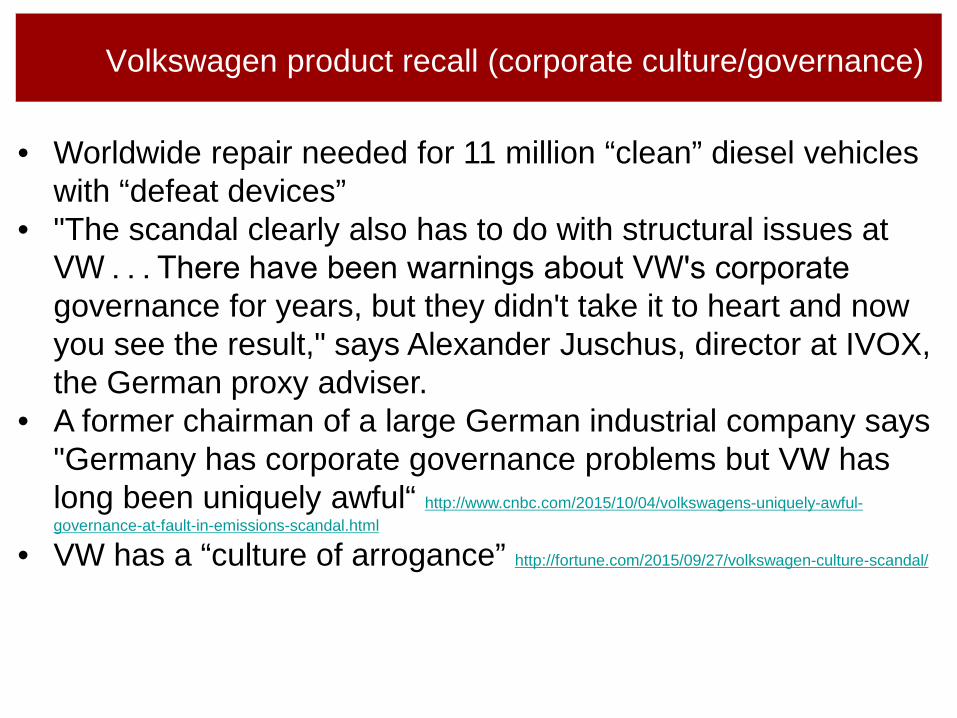

Volkswagen product recall (corporate culture/governance)

• Worldwide repair needed for 11 million “clean” diesel vehicles with “defeat devices”

• "The scandal clearly also has to do with structural issues at VW . . . There have been warnings about VW's corporate governance for years, but they didn't take it to heart and now you see the result," says Alexander Juschus, director at IVOX, the German proxy adviser.

• A former chairman of a large German industrial company says "Germany has corporate governance problems but VW has long been uniquely awful“ http://www.cnbc.com/2015/10/04/volkswagens-uniquely-awful-governance-at-fault-in-emissions-scandal.html

• VW has a “culture of arrogance” http://fortune.com/2015/09/27/volkswagen-culture-scandal/

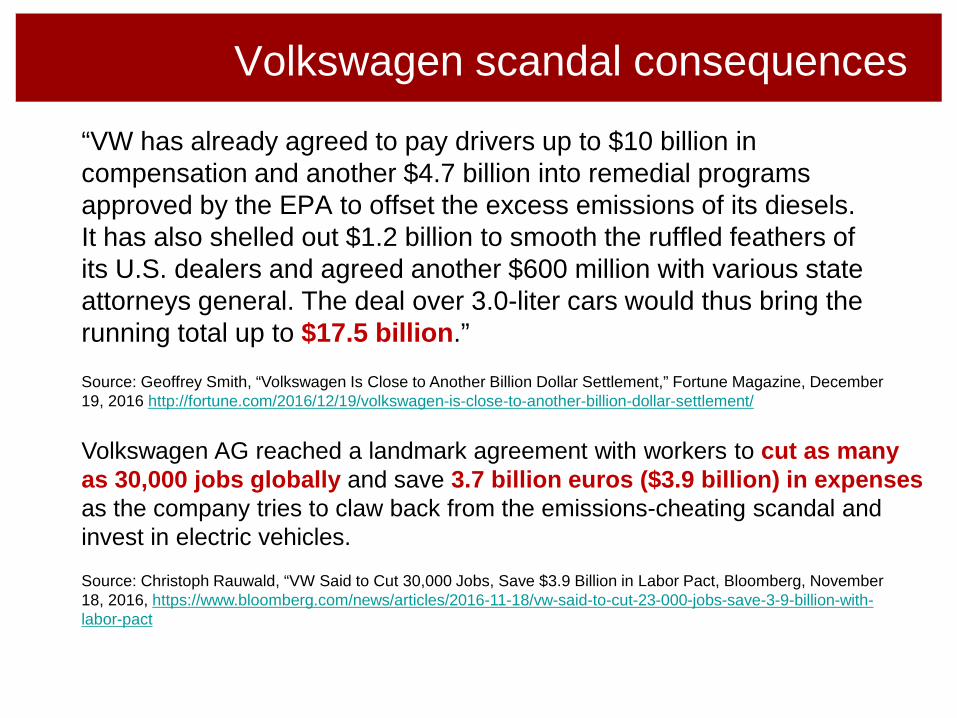

Volkswagen scandal consequences

“VW has already agreed to pay drivers up to $10 billion in compensation and another $4.7 billion into remedial programs approved by the EPA to offset the excess emissions of its diesels. It has also shelled out $1.2 billion to smooth the ruffled feathers of its U.S. dealers and agreed another $600 million with various state attorneys general. The deal over 3.0-liter cars would thus bring the running total up to $17.5 billion.”

Source: Geoffrey Smith, “Volkswagen Is Close to Another Billion Dollar Settlement,” Fortune Magazine, December 19, 2016 http://fortune.com/2016/12/19/volkswagen-is-close-to-another-billion-dollar-settlement/

Volkswagen AG reached a landmark agreement with workers to cut as many as 30,000 jobs globally and save 3.7 billion euros ($3.9 billion) in expenses as the company tries to claw back from the emissions-cheating scandal and invest in electric vehicles.

Source: Christoph Rauwald, “VW Said to Cut 30,000 Jobs, Save $3.9 Billion in Labor Pact, Bloomberg, November 18, 2016, https://www.bloomberg.com/news/articles/2016-11-18/vw-said-to-cut-23-000-jobs-save-3-9-billion-with-labor-pact

VW Consequences (continued)

Volkswagen's diesel emissions scandal to cause more than a thousand premature deaths, MIT study finds

Of the premature deaths, 500 will likely occur in Germany, according to MIT, with most of the others happening in Poland, France and the Czech Republic

Source: http://www.independent.co.uk/news/business/news/volkswagens-diesel-emissions-scandal-premature-deaths-car-vw-mit-study-thousands-killed-a7609061.html

VW Consequences (continued)

BUSINESS NEWS | Fri Mar 10, 2017 | 11:15am EST

Volkswagen pleads guilty in U.S. court in diesel emissions scandal Volkswagen AG (VOWG_p.DE) pleaded guilty on Friday to three felony counts as part of a $4.3 billion settlement reached with the Justice Department in January over the automaker's massive diesel emissions scandal. Source: http://www.reuters.com/article/us-volkswagen-emissions-idUSKBN16H1W4

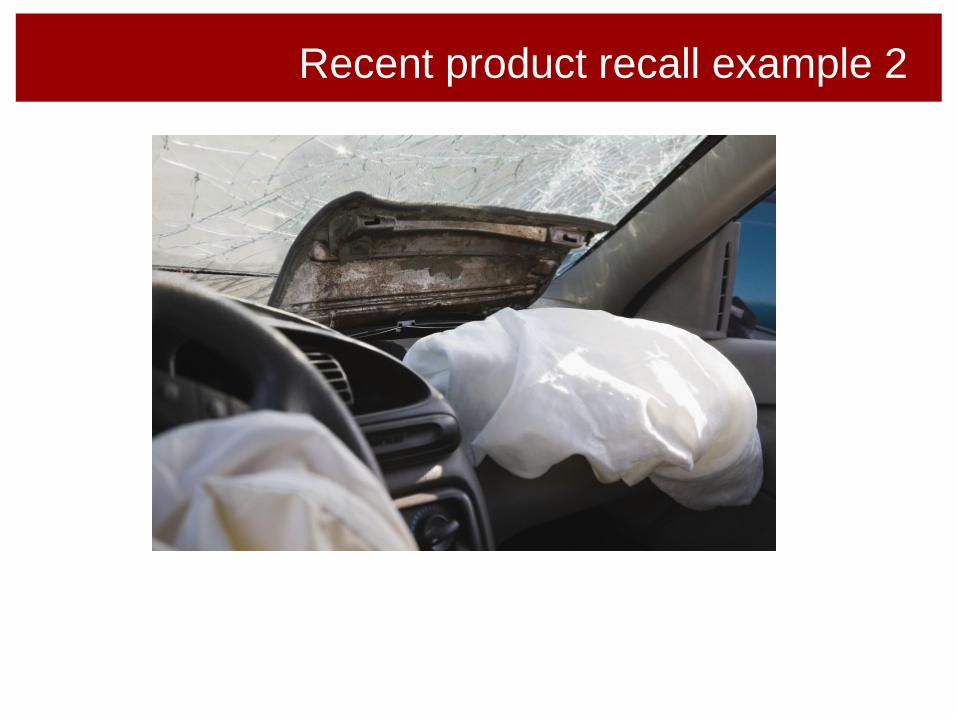

Recent product recall example 2

Takata (the continuing story)

Honda Adds 772,000 Vehicles to Takata Airbag Recalls JANUARY 11, 2017 AT 3:07 PM BY CLIFFORD ATIYEH

UPDATE 2/27/2017, 6:30 p.m.: Takata has officially pleaded guilty to criminal wire fraud for covering up the engineering defects that have led to at least 17 deaths and the biggest recall in automotive history. The guilty plea comes six weeks after a Justice Department announcement that Takata had agreed to a $1 billion settlement, including $850 million to compensate automakers for repairs, $125 million for a victim settlement fund, and a $25 million criminal fine. Three Takata executives also have been charged with fraud.

Recent Corporate Culture/Governance Case

http://www.commondreams.org/news/2016/10/13/wells-fargo-ceo-steps-down-warren-its-not-real-accountability

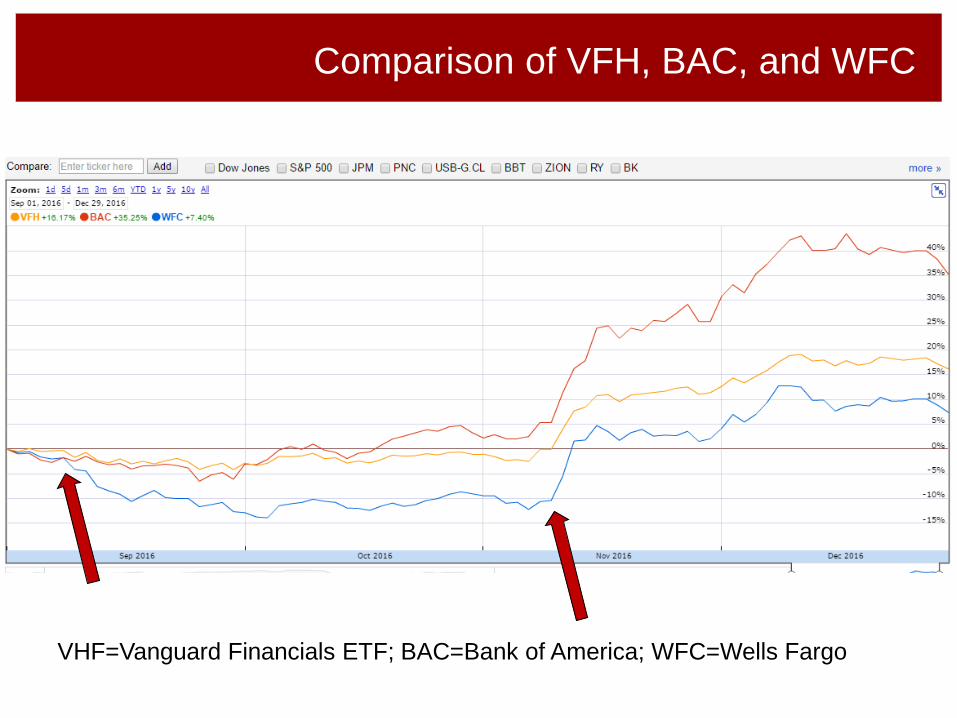

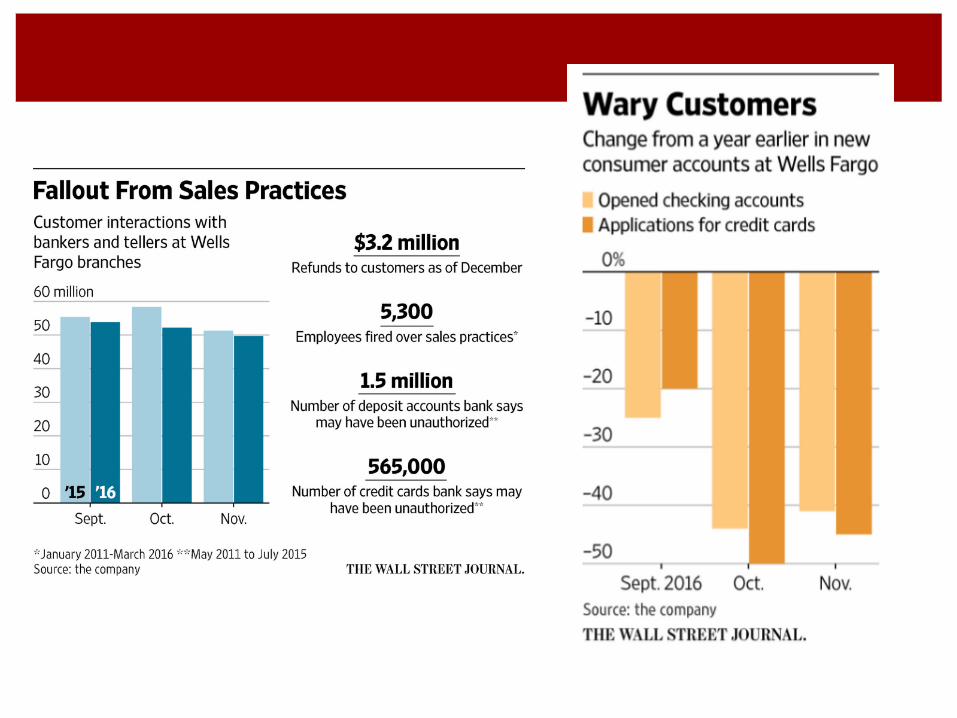

The Case of Wells Fargo

November 9: “Wells Fargo Leads Banks Up as Trump Win Seen Curbing Warren”

(Bloomberg Headline)

September 8: CFPB, Los Angeles City County Attorney, and OCC announce $185 million fine.

Comparison of VFH, BAC, and WFC

VHF=Vanguard Financials ETF; BAC=Bank of America; WFC=Wells Fargo

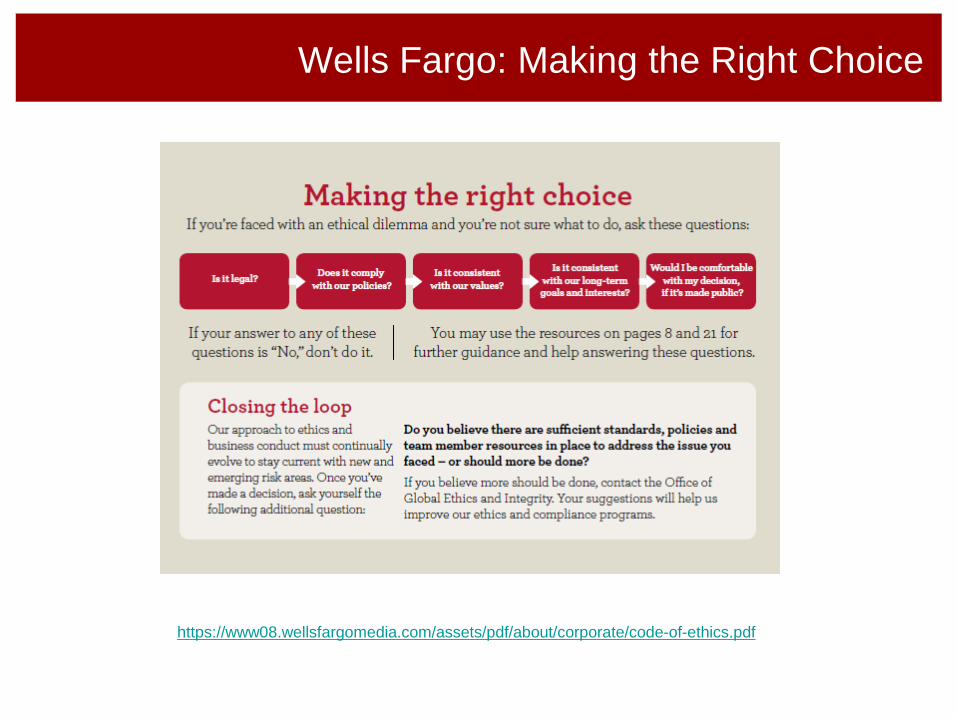

Wells Fargo: Vision and Values

https://www08.wellsfargomedia.com/assets/pdf/about/corporate/code-of-ethics.pdf

https://www08.wellsfargomedia.com/assets/pdf/about/corporate/code-of-ethics.pdf

Wells Fargo: Making the Right Choice

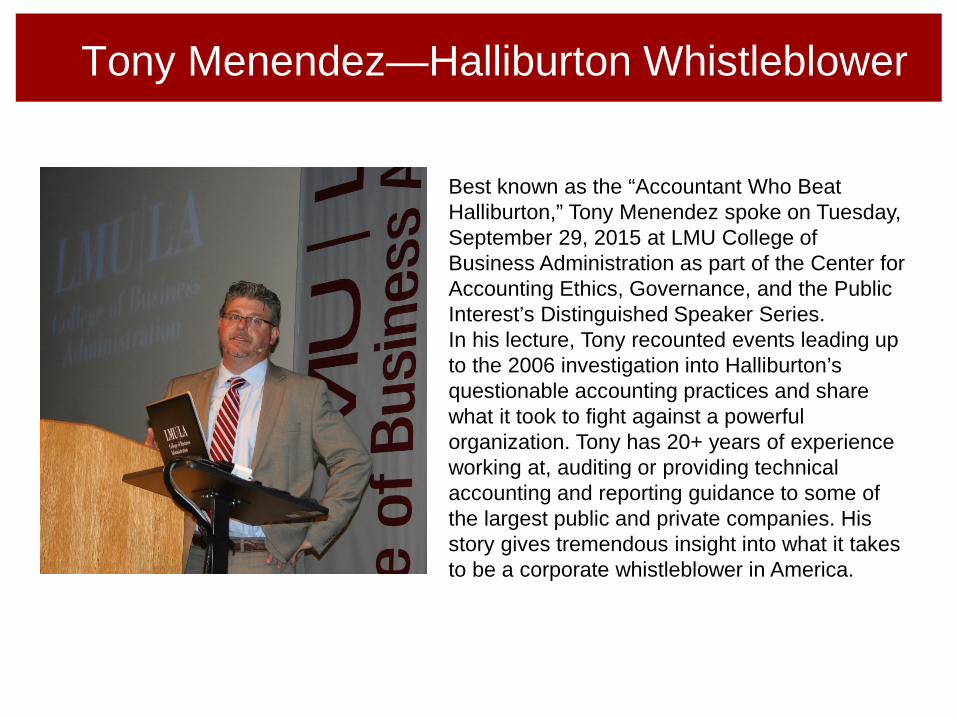

Tony Menendez—Halliburton Whistleblower

Best known as the “Accountant Who Beat Halliburton,” Tony Menendez spoke on Tuesday, September 29, 2015 at LMU College of Business Administration as part of the Center for Accounting Ethics, Governance, and the Public Interest’s Distinguished Speaker Series. In his lecture, Tony recounted events leading up to the 2006 investigation into Halliburton’s questionable accounting practices and share what it took to fight against a powerful organization. Tony has 20+ years of experience working at, auditing or providing technical accounting and reporting guidance to some of the largest public and private companies. His story gives tremendous insight into what it takes to be a corporate whistleblower in America.

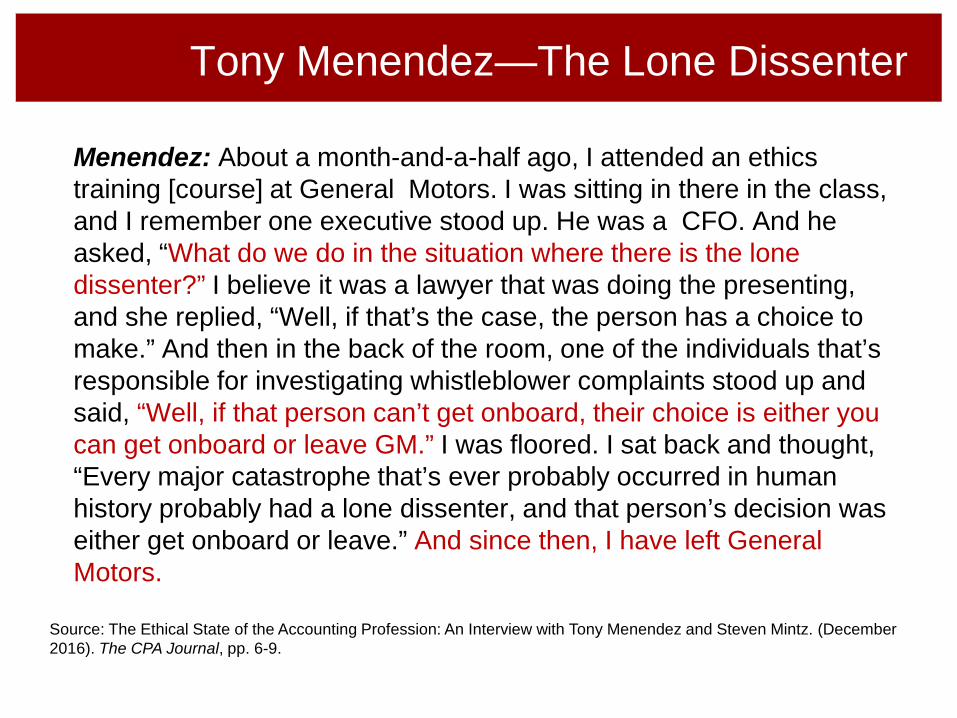

Tony Menendez—The Lone Dissenter

Menendez: About a month-and-a-half ago, I attended an ethics training [course] at General Motors. I was sitting in there in the class, and I remember one executive stood up. He was a CFO. And he asked, “What do we do in the situation where there is the lone dissenter?” I believe it was a lawyer that was doing the presenting, and she replied, “Well, if that’s the case, the person has a choice to make.” And then in the back of the room, one of the individuals that’s responsible for investigating whistleblower complaints stood up and said, “Well, if that person can’t get onboard, their choice is either you can get onboard or leave GM.” I was floored. I sat back and thought, “Every major catastrophe that’s ever probably occurred in human history probably had a lone dissenter, and that person’s decision was either get onboard or leave.” And since then, I have left General Motors.

Source: The Ethical State of the Accounting Profession: An Interview with Tony Menendez and Steven Mintz. (December 2016). The CPA Journal, pp. 6-9.

Why is it so hard to be ethical?

• Professional responsibilities • The fraud triangle • Conflicts of interest and cognitive biases

The Accountant’s Professional Role

Consulting Auditing Tax

Advocacy Professional Skepticism

Integrity

Objectivity

Client The Public Duty

Ethics

Internal Auditor?

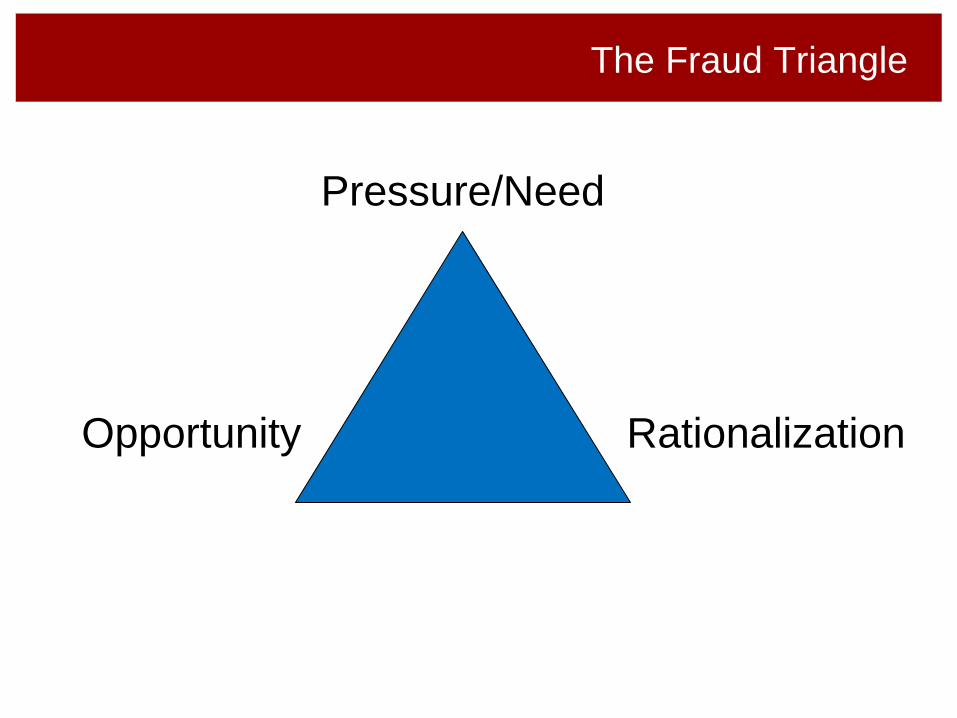

The Fraud Triangle

Pressure/Need

Opportunity Rationalization

Rationalization Tactics

• Legality* • Denial of responsibility* • Denial of injury* • Denial of victim* • Social weighting*

*Source: Blake Ashforth and Vikas Anand, “The Normalization of Corruption in Organizations,” Research in Organizational Behavior, 2003, Vol. 25: 1-52.

**Source: Joseph Heath, “Business Ethics and Moral Motivation: A Criminological Perspective,” Journal of Business Ethics, 2008, Vol. 83: 595-614.

• Appeal to higher loyalties* • Balancing the ledger* • Everyone else is doing it** • Entitlement**

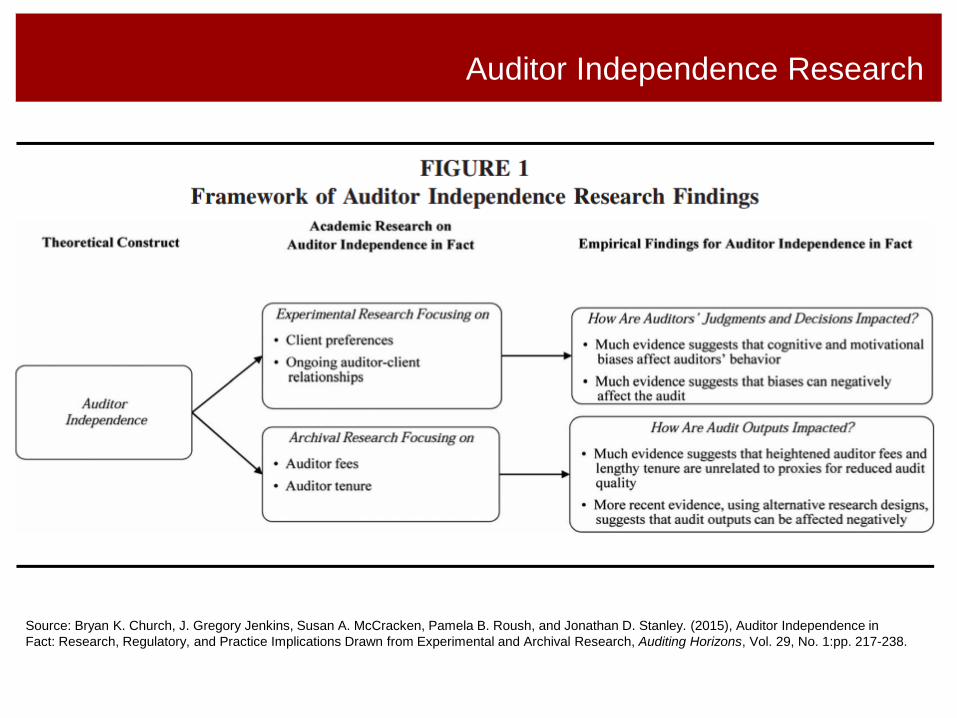

Auditor Independence Research

Source: Bryan K. Church, J. Gregory Jenkins, Susan A. McCracken, Pamela B. Roush, and Jonathan D. Stanley. (2015), Auditor Independence in Fact: Research, Regulatory, and Practice Implications Drawn from Experimental and Archival Research, Auditing Horizons, Vol. 29, No. 1:pp. 217-238.

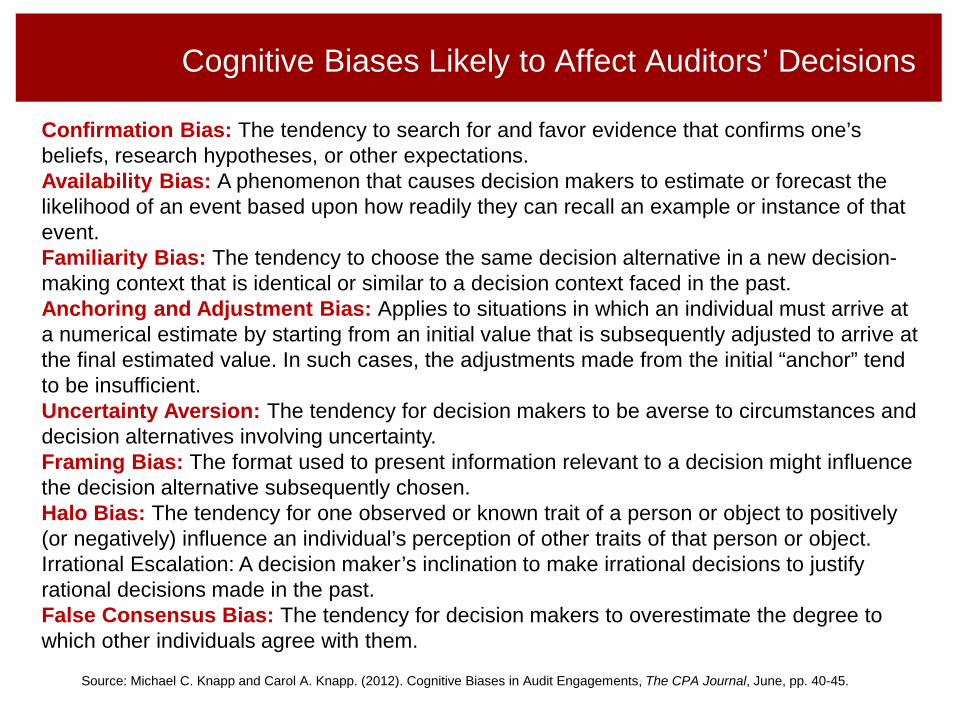

Cognitive Biases Likely to Affect Auditors’ Decisions

Confirmation Bias: The tendency to search for and favor evidence that confirms one’s beliefs, research hypotheses, or other expectations. Availability Bias: A phenomenon that causes decision makers to estimate or forecast the likelihood of an event based upon how readily they can recall an example or instance of that event. Familiarity Bias: The tendency to choose the same decision alternative in a new decision-making context that is identical or similar to a decision context faced in the past. Anchoring and Adjustment Bias: Applies to situations in which an individual must arrive at a numerical estimate by starting from an initial value that is subsequently adjusted to arrive at the final estimated value. In such cases, the adjustments made from the initial “anchor” tend to be insufficient. Uncertainty Aversion: The tendency for decision makers to be averse to circumstances and decision alternatives involving uncertainty. Framing Bias: The format used to present information relevant to a decision might influence the decision alternative subsequently chosen. Halo Bias: The tendency for one observed or known trait of a person or object to positively (or negatively) influence an individual’s perception of other traits of that person or object. Irrational Escalation: A decision maker’s inclination to make irrational decisions to justify rational decisions made in the past. False Consensus Bias: The tendency for decision makers to overestimate the degree to which other individuals agree with them.

Source: Michael C. Knapp and Carol A. Knapp. (2012). Cognitive Biases in Audit Engagements, The CPA Journal, June, pp. 40-45.

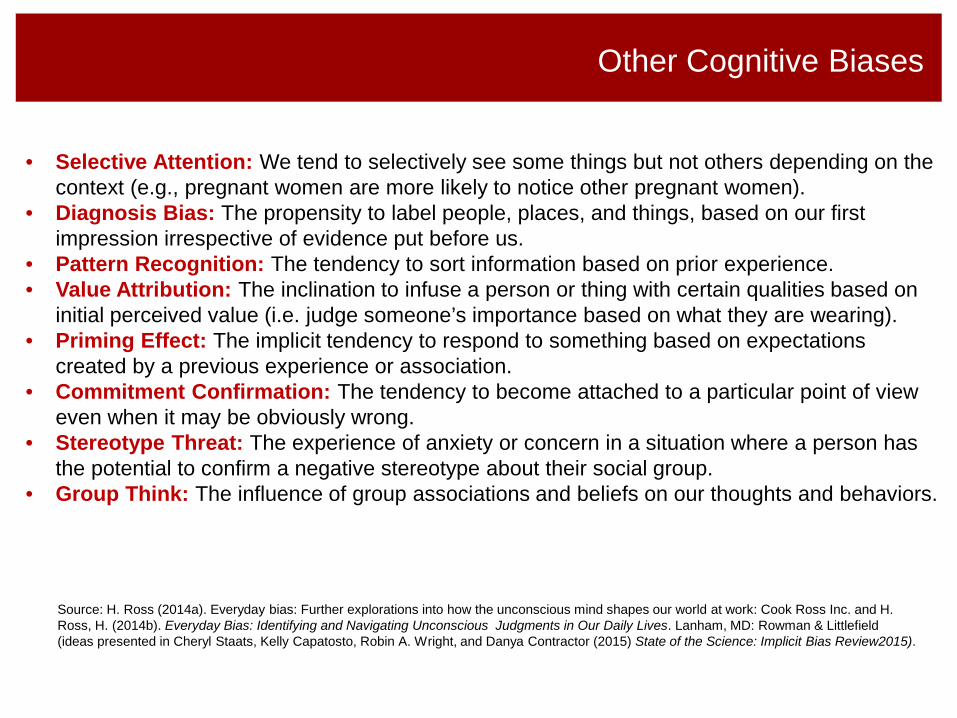

Other Cognitive Biases

• Selective Attention: We tend to selectively see some things but not others depending on the context (e.g., pregnant women are more likely to notice other pregnant women).

• Diagnosis Bias: The propensity to label people, places, and things, based on our first impression irrespective of evidence put before us.

• Pattern Recognition: The tendency to sort information based on prior experience. • Value Attribution: The inclination to infuse a person or thing with certain qualities based on

initial perceived value (i.e. judge someone’s importance based on what they are wearing). • Priming Effect: The implicit tendency to respond to something based on expectations

created by a previous experience or association. • Commitment Confirmation: The tendency to become attached to a particular point of view

even when it may be obviously wrong. • Stereotype Threat: The experience of anxiety or concern in a situation where a person has

the potential to confirm a negative stereotype about their social group. • Group Think: The influence of group associations and beliefs on our thoughts and behaviors.

Source: H. Ross (2014a). Everyday bias: Further explorations into how the unconscious mind shapes our world at work: Cook Ross Inc. and H. Ross, H. (2014b). Everyday Bias: Identifying and Navigating Unconscious Judgments in Our Daily Lives. Lanham, MD: Rowman & Littlefield (ideas presented in Cheryl Staats, Kelly Capatosto, Robin A. Wright, and Danya Contractor (2015) State of the Science: Implicit Bias Review2015).

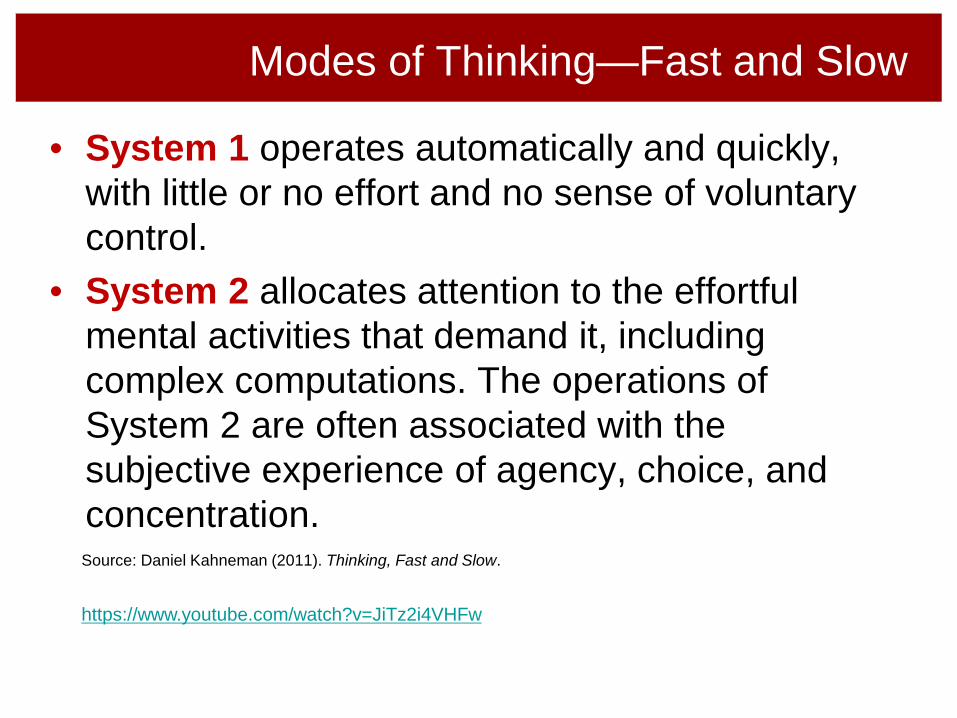

Modes of Thinking—Fast and Slow

• System 1 operates automatically and quickly, with little or no effort and no sense of voluntary control.

• System 2 allocates attention to the effortful mental activities that demand it, including complex computations. The operations of System 2 are often associated with the subjective experience of agency, choice, and concentration. Source: Daniel Kahneman (2011). Thinking, Fast and Slow.

https://www.youtube.com/watch?v=JiTz2i4VHFw

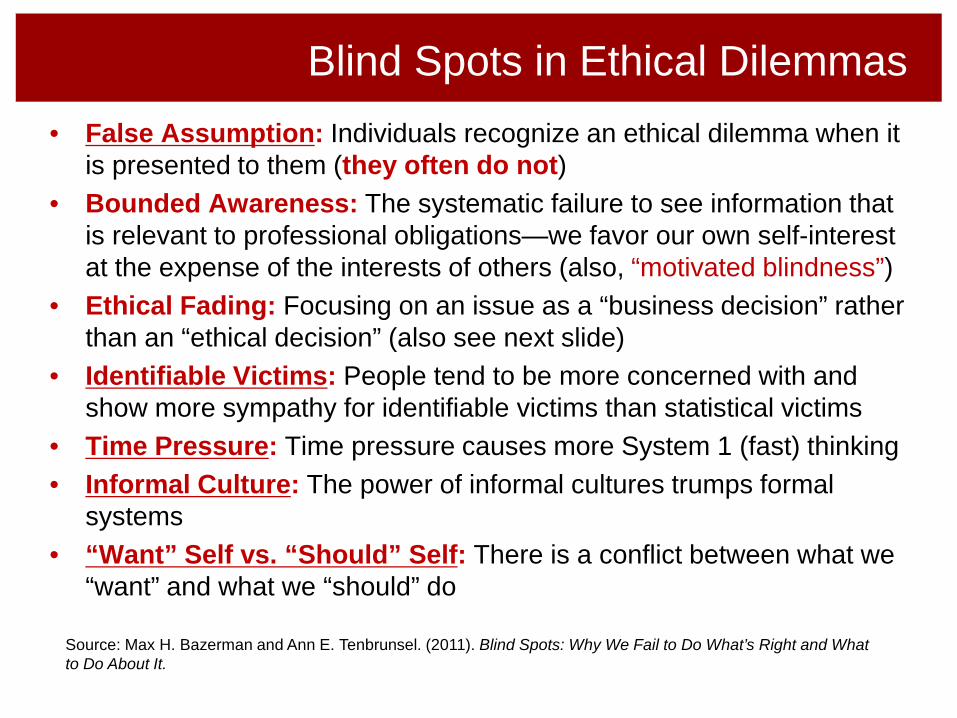

Blind Spots in Ethical Dilemmas • False Assumption: Individuals recognize an ethical dilemma when it

is presented to them (they often do not) • Bounded Awareness: The systematic failure to see information that

is relevant to professional obligations—we favor our own self-interest at the expense of the interests of others (also, “motivated blindness”)

• Ethical Fading: Focusing on an issue as a “business decision” rather than an “ethical decision” (also see next slide)

• Identifiable Victims: People tend to be more concerned with and show more sympathy for identifiable victims than statistical victims

• Time Pressure: Time pressure causes more System 1 (fast) thinking • Informal Culture: The power of informal cultures trumps formal

systems • “Want” Self vs. “Should” Self: There is a conflict between what we

“want” and what we “should” do

Source: Max H. Bazerman and Ann E. Tenbrunsel. (2011). Blind Spots: Why We Fail to Do What’s Right and What to Do About It.

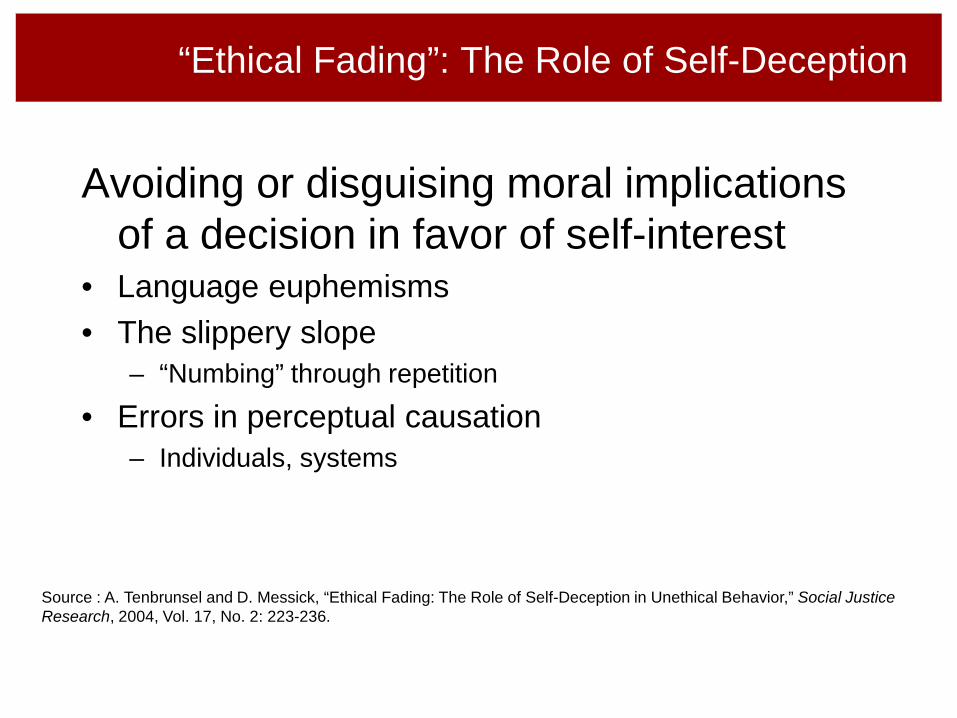

“Ethical Fading”: The Role of Self-Deception

Avoiding or disguising moral implications of a decision in favor of self-interest

• Language euphemisms • The slippery slope

– “Numbing” through repetition

• Errors in perceptual causation – Individuals, systems

Source : A. Tenbrunsel and D. Messick, “Ethical Fading: The Role of Self-Deception in Unethical Behavior,” Social Justice Research, 2004, Vol. 17, No. 2: 223-236.

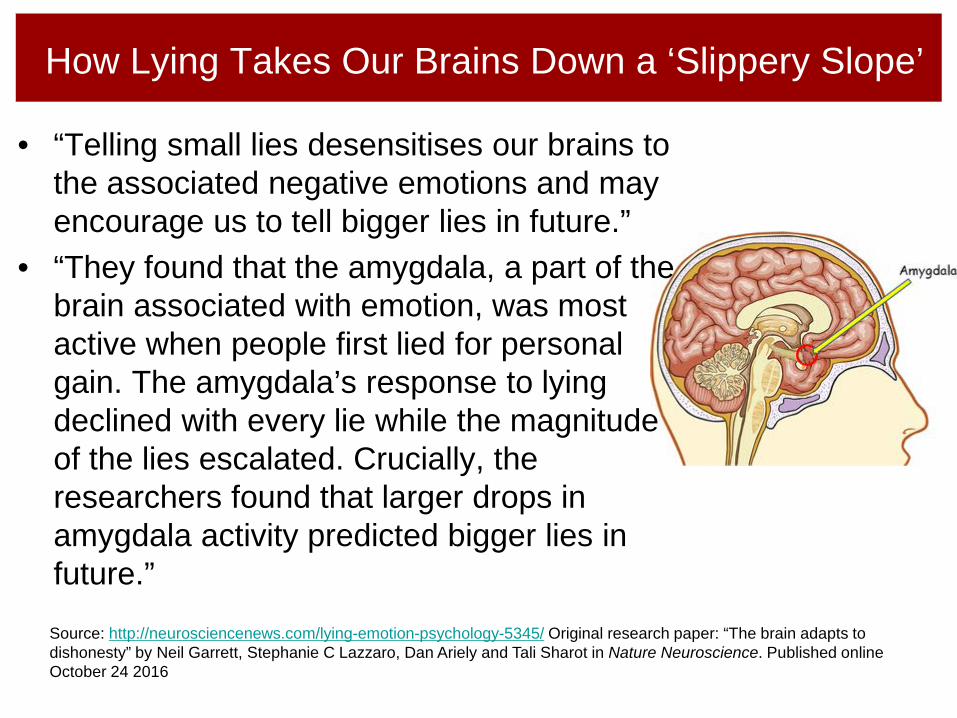

How Lying Takes Our Brains Down a ‘Slippery Slope’

• “Telling small lies desensitises our brains to the associated negative emotions and may encourage us to tell bigger lies in future.”

• “They found that the amygdala, a part of the brain associated with emotion, was most active when people first lied for personal gain. The amygdala’s response to lying declined with every lie while the magnitude of the lies escalated. Crucially, the researchers found that larger drops in amygdala activity predicted bigger lies in future.”

Source: http://neurosciencenews.com/lying-emotion-psychology-5345/ Original research paper: “The brain adapts to dishonesty” by Neil Garrett, Stephanie C Lazzaro, Dan Ariely and Tali Sharot in Nature Neuroscience. Published online October 24 2016

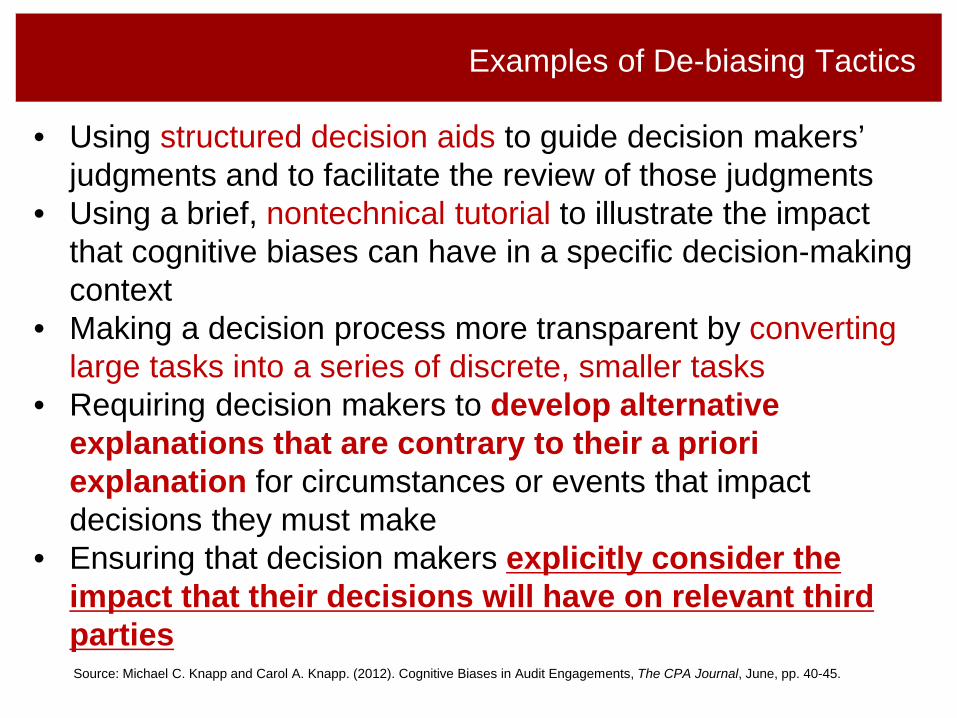

Examples of De-biasing Tactics

• Using structured decision aids to guide decision makers’ judgments and to facilitate the review of those judgments

• Using a brief, nontechnical tutorial to illustrate the impact that cognitive biases can have in a specific decision-making context

• Making a decision process more transparent by converting large tasks into a series of discrete, smaller tasks

• Requiring decision makers to develop alternative explanations that are contrary to their a priori explanation for circumstances or events that impact decisions they must make

• Ensuring that decision makers explicitly consider the impact that their decisions will have on relevant third parties Source: Michael C. Knapp and Carol A. Knapp. (2012). Cognitive Biases in Audit Engagements, The CPA Journal, June, pp. 40-45.

IPPF IIA Code of Ethics

• Principles and Rules – Integrity – Objectivity – Confidentiality – Competency

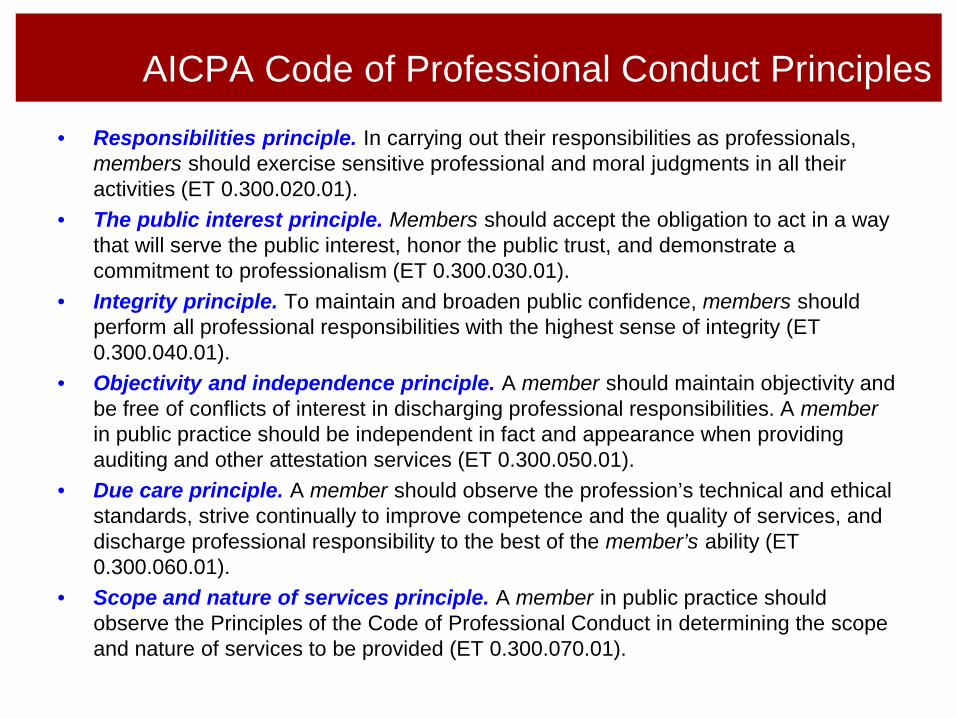

AICPA Code of Professional Conduct Principles

• Responsibilities principle. In carrying out their responsibilities as professionals, members should exercise sensitive professional and moral judgments in all their activities (ET 0.300.020.01).

• The public interest principle. Members should accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate a commitment to professionalism (ET 0.300.030.01).

• Integrity principle. To maintain and broaden public confidence, members should perform all professional responsibilities with the highest sense of integrity (ET 0.300.040.01).

• Objectivity and independence principle. A member should maintain objectivity and be free of conflicts of interest in discharging professional responsibilities. A member in public practice should be independent in fact and appearance when providing auditing and other attestation services (ET 0.300.050.01).

• Due care principle. A member should observe the profession’s technical and ethical standards, strive continually to improve competence and the quality of services, and discharge professional responsibility to the best of the member’s ability (ET 0.300.060.01).

• Scope and nature of services principle. A member in public practice should observe the Principles of the Code of Professional Conduct in determining the scope and nature of services to be provided (ET 0.300.070.01).

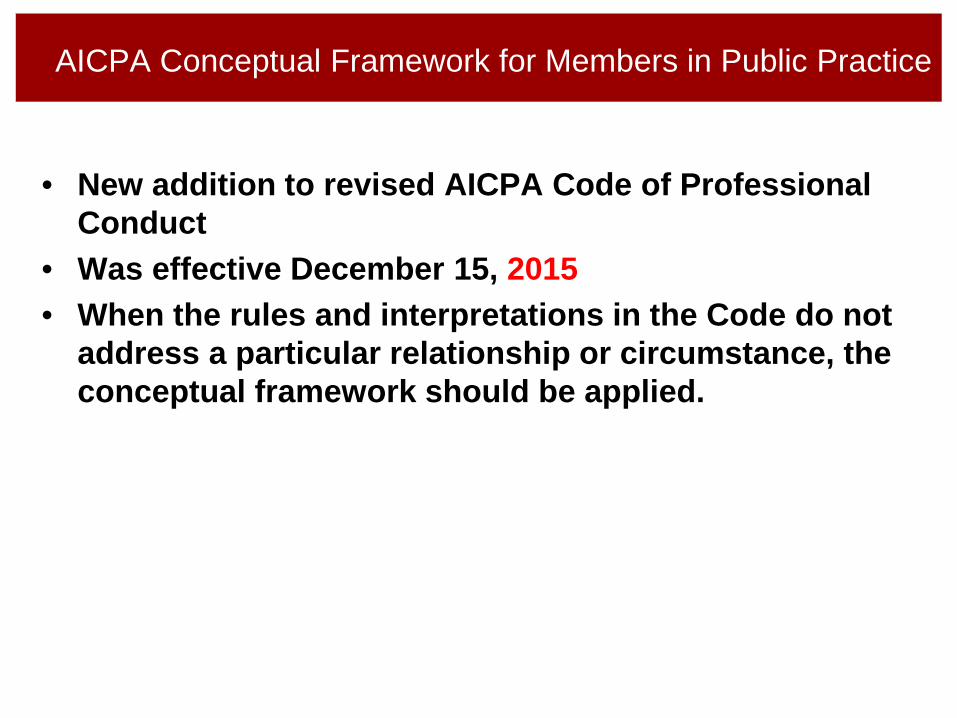

AICPA Conceptual Framework for Members in Public Practice

• New addition to revised AICPA Code of Professional Conduct

• Was effective December 15, 2015 • When the rules and interpretations in the Code do not

address a particular relationship or circumstance, the conceptual framework should be applied.

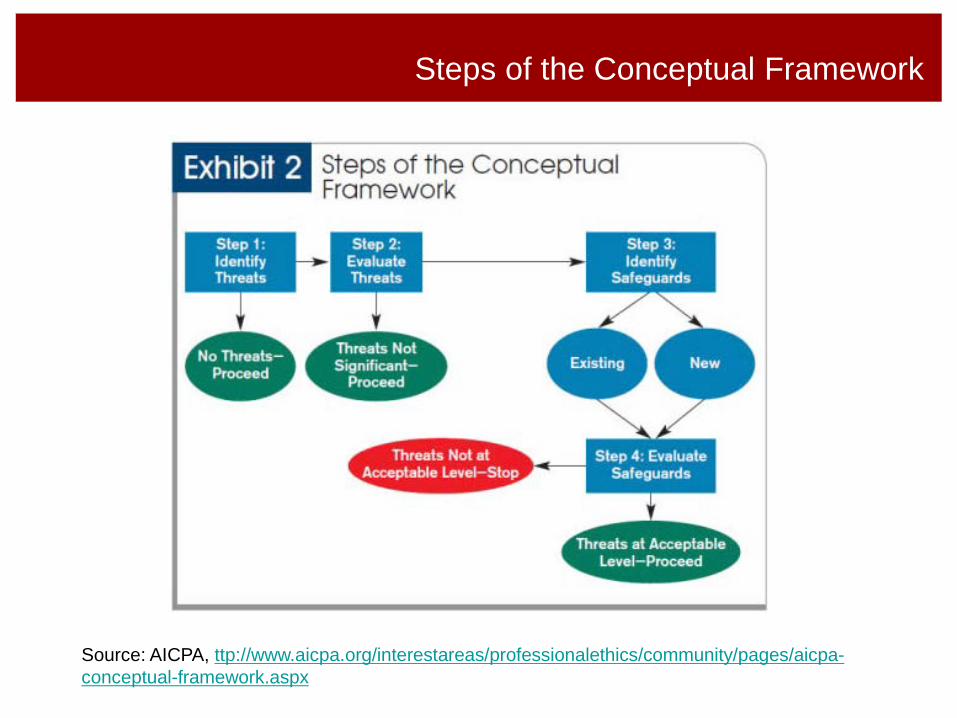

Steps of the Conceptual Framework

Source: AICPA, ttp://www.aicpa.org/interestareas/professionalethics/community/pages/aicpa-conceptual-framework.aspx

AICPA Conceptual Framework for Members in Public Practice

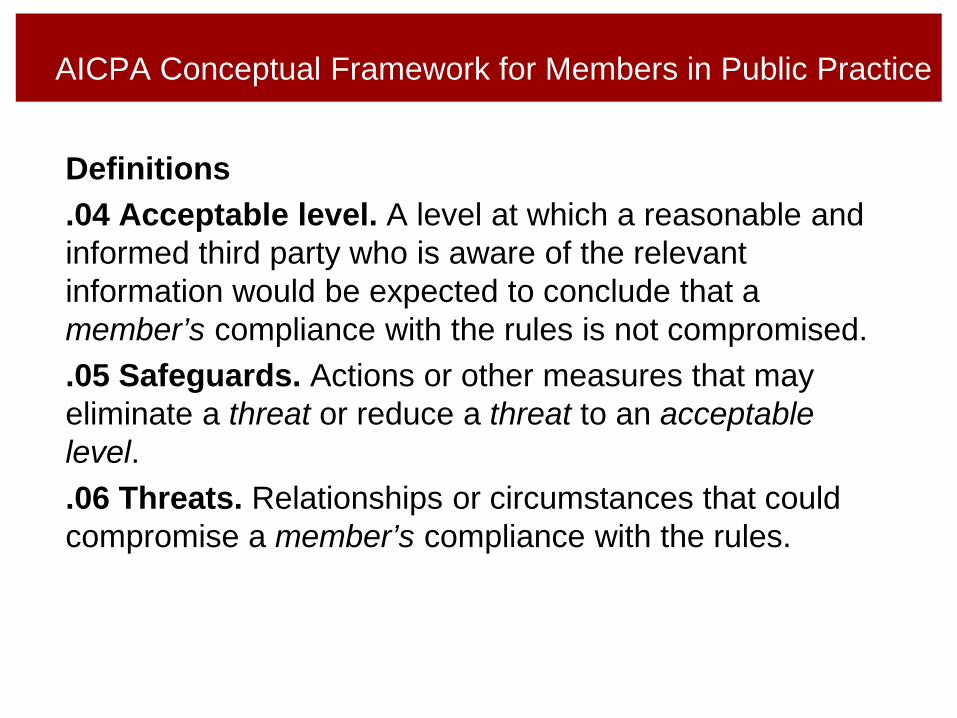

Definitions .04 Acceptable level. A level at which a reasonable and informed third party who is aware of the relevant information would be expected to conclude that a member’s compliance with the rules is not compromised. .05 Safeguards. Actions or other measures that may eliminate a threat or reduce a threat to an acceptable level. .06 Threats. Relationships or circumstances that could compromise a member’s compliance with the rules.

.10 Adverse interest threat. The threat that a member will not act with objectivity because the member’s interests are opposed to the client’s interests. .11 Advocacy threat. The threat that a member will promote a client’s interests or position to the point that his or her objectivity or independence is compromised. .12 Familiarity threat. The threat that, due to a long or close relationship with a client, a member will become too sympathetic to the client’s interests or too accepting of the client’s work or product. .13 Management participation threat. The threat that a member will take on the role of client management or otherwise assume management responsibilities, such may occur during an engagement to provide nonattest services.

AICPA Conceptual Framework for Members in Public Practice

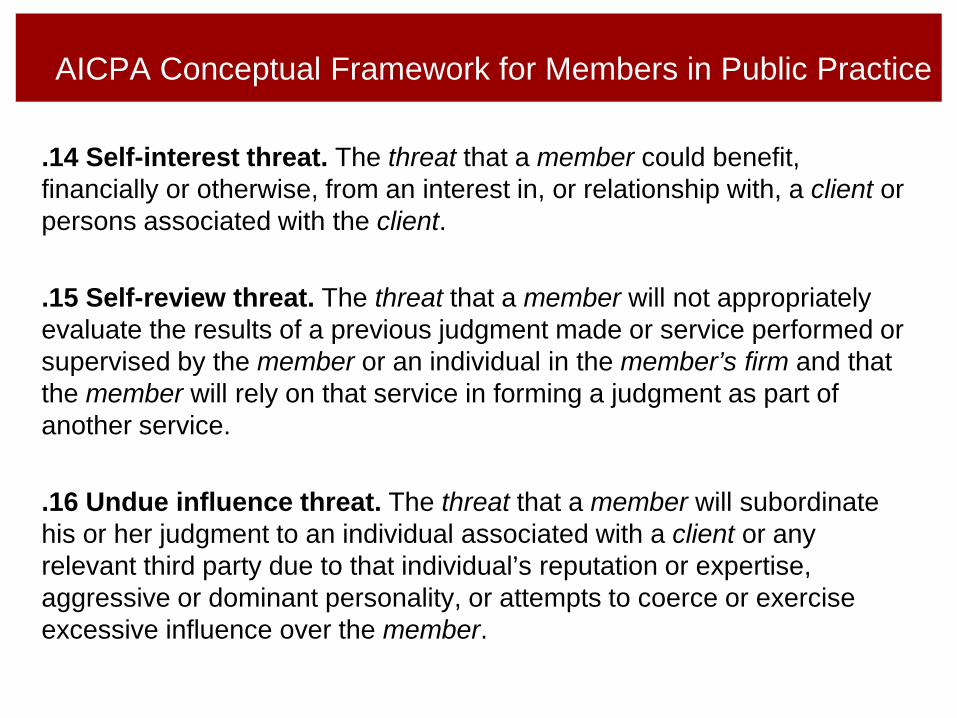

.14 Self-interest threat. The threat that a member could benefit, financially or otherwise, from an interest in, or relationship with, a client or persons associated with the client. .15 Self-review threat. The threat that a member will not appropriately evaluate the results of a previous judgment made or service performed or supervised by the member or an individual in the member’s firm and that the member will rely on that service in forming a judgment as part of another service. .16 Undue influence threat. The threat that a member will subordinate his or her judgment to an individual associated with a client or any relevant third party due to that individual’s reputation or expertise, aggressive or dominant personality, or attempts to coerce or exercise excessive influence over the member.

AICPA Conceptual Framework for Members in Public Practice

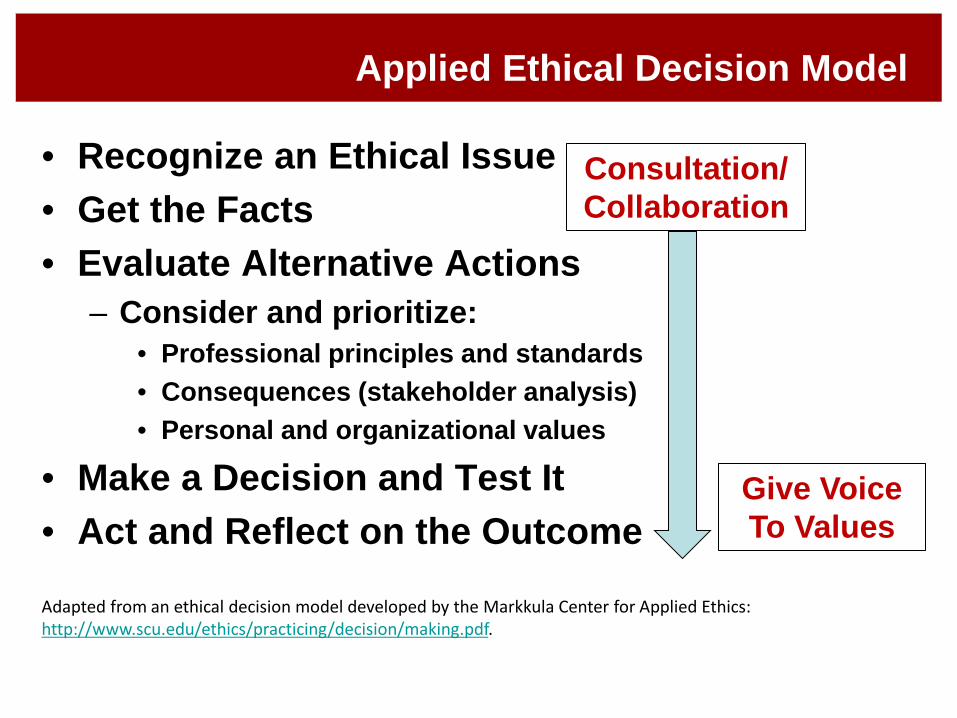

Applied Ethical Decision Model

• Recognize an Ethical Issue • Get the Facts • Evaluate Alternative Actions

– Consider and prioritize: • Professional principles and standards • Consequences (stakeholder analysis) • Personal and organizational values

• Make a Decision and Test It • Act and Reflect on the Outcome

Adapted from an ethical decision model developed by the Markkula Center for Applied Ethics: http://www.scu.edu/ethics/practicing/decision/making.pdf.

Consultation/ Collaboration

Give Voice To Values

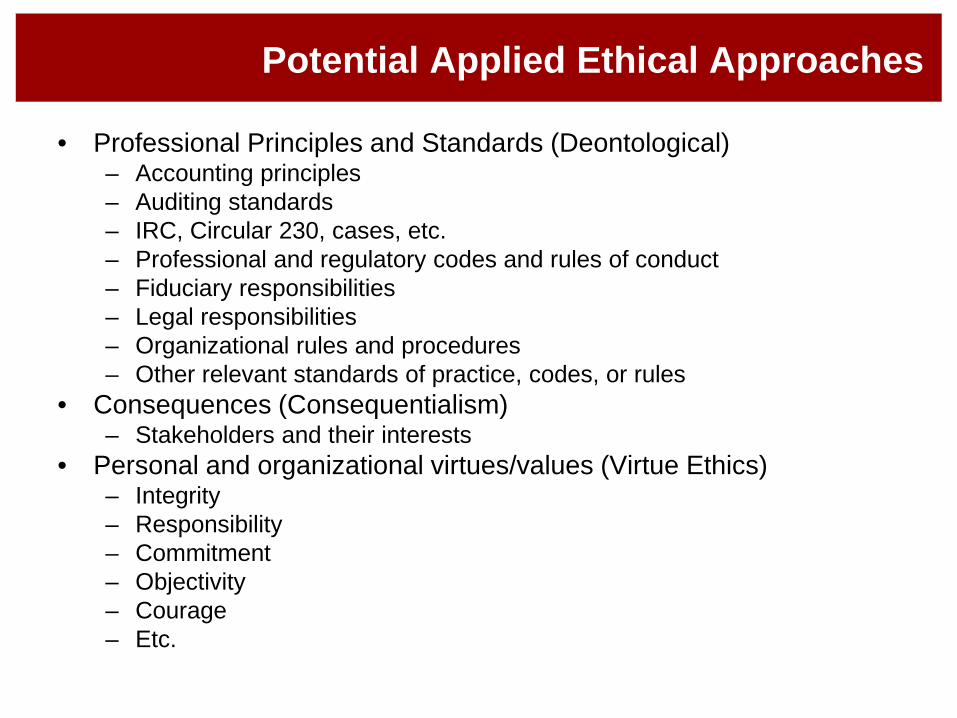

Potential Applied Ethical Approaches

• Professional Principles and Standards (Deontological) – Accounting principles – Auditing standards – IRC, Circular 230, cases, etc. – Professional and regulatory codes and rules of conduct – Fiduciary responsibilities – Legal responsibilities – Organizational rules and procedures – Other relevant standards of practice, codes, or rules

• Consequences (Consequentialism) – Stakeholders and their interests

• Personal and organizational virtues/values (Virtue Ethics) – Integrity – Responsibility – Commitment – Objectivity – Courage – Etc.

Negative Consequences of Unethical Behavior

• Self (reputation, job, license, family) • Firm • Clients • Profession

Consultation/Collaboration

• In applying the ethical decision model, DON’T GO IT ALONE!

• Find others to get their feedback (consultation) • Work with others toward a solution (collaboration)

Giving Voice to Values (GVV)

• Seven Pillars of GVV Curriculum – Acknowledging shared values – Choosing to act – Normalizing values conflicts – Defining professional purpose – Understanding the self – Using one’s voice – Preparing responses (“scripts”)

Source: Mary C. Gentile, Voicing Values, Finding Answers, BizEd, July/August 2008, pp. 40-45.

Stakeholder Analysis

Stakeholders: Now you are at a stage to identify the interested parties (i.e., stakeholders) based on the compiled facts and alternatives. • Who is affected by our decision or any of the alternatives? • What are their relationships, their priorities to me, and what is their

power over my decision? • Who has a stake in the outcome? • Do not limit your inquiry only to those stakeholders to whom you

believe you owe a duty; sometimes a duty arises as a result of the impact. For instance, you might not necessarily first consider your competitors as stakeholders; however, once you understand the impact of your decision on those competitors, an ethical duty may arise.

Source: Laura P. Hartman, Perspectives in Business Ethics, Third Edition, McGraw-Hill Irwin, New York, 2005.

Improving Organizational Ethics and Decisions

• Mission • Tone at the top • Leadership (at all levels) • Culture, shared values, shared responsibilities • Appreciation of cultural differences • Policies and procedures, including zero tolerance of

unethical behavior • Ethical decision models, including consultation/

collaboration • The power of stories • Proper reward structure • Training and reinforcement • Hiring and retention practices

Questions?