ipst members meeting combined heat & power: a generator …

TRANSCRIPT

April 11, 2012

Paul Baer, Marilyn Brown,

and Gyungwon Kim

Combined Heat & Power: A Generator of Green Energy and Green Jobs

IPST Members Meeting

Presentation Overview

• Study background

• Methods

• CHP Policies

• Construction Bill of Goods

• Results

• Discussion

Study Background

• High salience of “green jobs”

• Politicized studies by different analysts

• Interest in developing robust methodology

• CHP selected as case study

Numerous Market Failures and Barriers Inhibit the Growth of Industrial CHP

• Regulatory barriers

– Input-based emissions standards

– The Sarbanes-Oxley Act of 2002

– Utility monopoly power & grid access difficulties

• Financial barriers

– Access to credit and project competition within firm

– Purchase power agreements

• Information and workforce barriers

– Workforce engineering know-how

CHP

Power Plant

Boiler

ELECTRICITY

HEAT

Traditional System

CHP System

45- 49%

75- 80%

Efficiency Efficiency

Policy options are available to tackle these barriers.

Regional Distribution of Industrial CHP Facilities in Pulp and Paper Plants

(Data source: Combined Heat and Power Installation Database, 1900-2010)

Capacity of CHP Facilities

Legend

Capacity of CHP in pulp and paper industry Capacity of CHP in other industries

We Have Shown that Two CHP Policy Options Could Have Numerous Benefits

http://www.ornl.gov /sci/eere/publications.shtml

Output-Based Emissions Standards (OBES):

This policy would provide financial incentives and technical assistance to states to spur adoption of OBES – as authorized by the EPA – to reduce energy consumption, emissions of criteria air pollutants and GHG, and regulatory burdens.

A Federal Energy Portfolio Standard (EPS)with CHP and a 30% Investment Tax Credit:

This policy would mandate electric distributors to meet an EPS with CHP as an eligible resource and to extend and expand the current investment tax credits for CHP. This policy would concurrently establish measurement and verification methods for qualifying CHP resources.

The Two CHP Policies Appear to be Highly Cost-Effective

Box and Whisker Plot from Monte Carlo Simulation of Net Private Benefit (7% discount rate)

• Spurring the adoption of output-based emissions standards is particularly cost-effective, but so is the energy portfolio standard

• They are cost-effective under a range of assumptions

0

50

100

150

200

250

Net

Pri

vate

Be

nef

it (

Bill

ion

$2

00

9)

OBES

EPS

OBES = Output Based Emissions Standards EPS = Energy Portfolio Standards with an ITC for CHP

How would more widespread use of CHP impact employment?

Methodology for Addressing This Question:

Hybrid NEMS-Input/Output Model • Goal: Examine expected employment impacts from clean

energy investments

• Clean energy policies and investments are first modeled in Georgia Tech’s National Energy Modeling System (GT-NEMS)

• Using NEMS 2011, we compare two scenarios:

1) The reference case with CHP assumptions of 2010 NEMS

2) Case of higher efficiency and lower installation costs, per 2011 NEMS.

• NEMS outputs (capacity changes, supply changes, energy bill changes) then drive input-output multipliers to estimate employment impacts

Input-output Model: Circular Flow Of The Economy

Households

$ consumption spending

Manufacturers and Businesses

Businesses

$ wages & salaries

Goods & Services

Labor

$ wages & salaries

First Order Impacts

• Direct, indirect and induced jobs from

– Construction of new CHP facilities

– Operation of CHP facilities

– Purchase of fuel for CHP facilities

– Decrease in purchase of electricity

• Requires

– Cost and bill of goods for construction and operation

– Quantity and price for change in fuel and electricity purchase

Second Order Impacts

• Changes in energy supply and demand lead to additional savings or costs

• CHP operators have new (lower) cost structure – Energy savings (and grid sales) are recycled through

lowered prices, increased profits/dividends

• Other sectors are impacted by price changes – Electricity prices fall

– Natural gas prices rise

– Demand changes with price changes

– Savings (or increased costs) are recycled

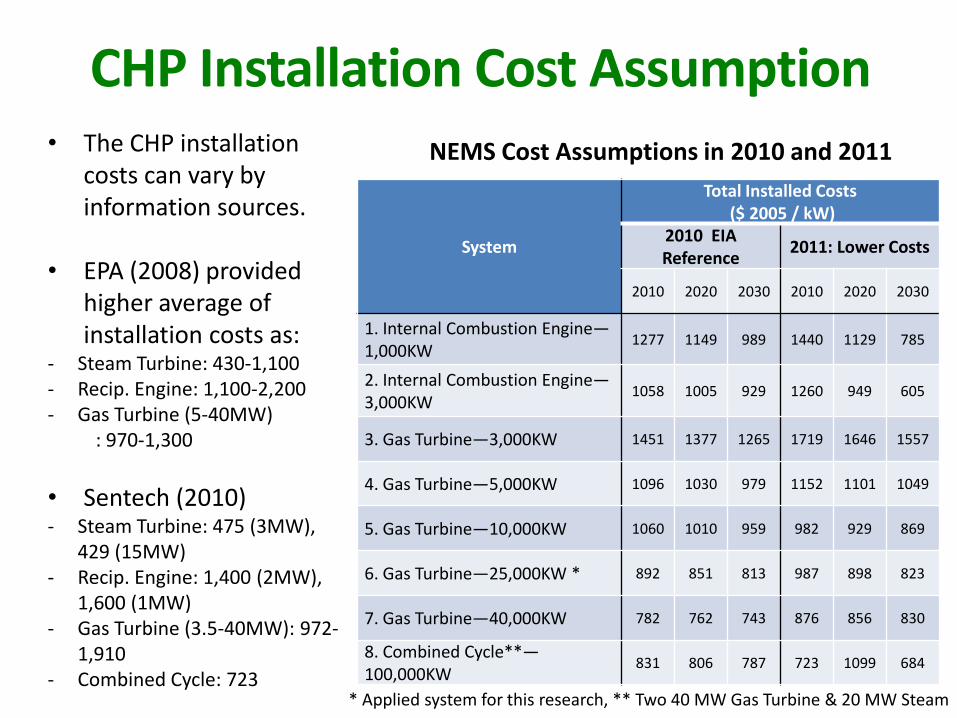

CHP Installation Cost Assumption

System

Total Installed Costs ($ 2005 / kW)

2010 EIA Reference

2011: Lower Costs

2010 2020 2030 2010 2020 2030

1. Internal Combustion Engine—1,000KW

1277 1149 989 1440 1129 785

2. Internal Combustion Engine—3,000KW

1058 1005 929 1260 949 605

3. Gas Turbine—3,000KW 1451 1377 1265 1719 1646 1557

4. Gas Turbine—5,000KW 1096 1030 979 1152 1101 1049

5. Gas Turbine—10,000KW 1060 1010 959 982 929 869

6. Gas Turbine—25,000KW * 892 851 813 987 898 823

7. Gas Turbine—40,000KW 782 762 743 876 856 830

8. Combined Cycle**—100,000KW

831 806 787 723 1099 684

* Applied system for this research, ** Two 40 MW Gas Turbine & 20 MW Steam

• The CHP installation costs can vary by information sources.

• EPA (2008) provided higher average of installation costs as:

- Steam Turbine: 430-1,100 - Recip. Engine: 1,100-2,200 - Gas Turbine (5-40MW)

: 970-1,300

• Sentech (2010) - Steam Turbine: 475 (3MW),

429 (15MW) - Recip. Engine: 1,400 (2MW),

1,600 (1MW) - Gas Turbine (3.5-40MW): 972-

1,910 - Combined Cycle: 723

NEMS Cost Assumptions in 2010 and 2011

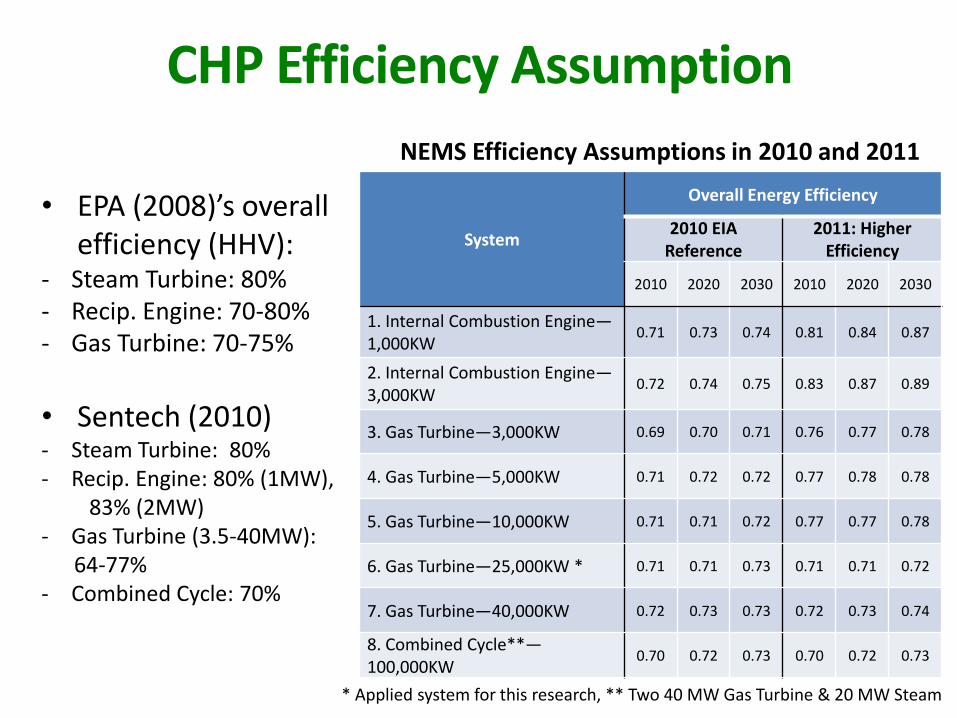

CHP Efficiency Assumption

System

Overall Energy Efficiency

2010 EIA Reference

2011: Higher Efficiency

2010 2020 2030 2010 2020 2030

1. Internal Combustion Engine—1,000KW

0.71 0.73 0.74 0.81 0.84 0.87

2. Internal Combustion Engine—3,000KW

0.72 0.74 0.75 0.83 0.87 0.89

3. Gas Turbine—3,000KW 0.69 0.70 0.71 0.76 0.77 0.78

4. Gas Turbine—5,000KW 0.71 0.72 0.72 0.77 0.78 0.78

5. Gas Turbine—10,000KW 0.71 0.71 0.72 0.77 0.77 0.78

6. Gas Turbine—25,000KW * 0.71 0.71 0.73 0.71 0.71 0.72

7. Gas Turbine—40,000KW 0.72 0.73 0.73 0.72 0.73 0.74

8. Combined Cycle**—100,000KW

0.70 0.72 0.73 0.70 0.72 0.73

* Applied system for this research, ** Two 40 MW Gas Turbine & 20 MW Steam

• EPA (2008)’s overall efficiency (HHV):

- Steam Turbine: 80% - Recip. Engine: 70-80% - Gas Turbine: 70-75%

• Sentech (2010) - Steam Turbine: 80% - Recip. Engine: 80% (1MW),

83% (2MW) - Gas Turbine (3.5-40MW): 64-77% - Combined Cycle: 70%

NEMS Efficiency Assumptions in 2010 and 2011

Induced Impact

Categories of “Accounts”

• 1. CHP Installation

– Productive investment from private sectors

– Program and administration costs

– Public financial incentives to stimulate overall productive investment

• 2. Operation and Management: Non-fuel

• 3. Operation and Management: Fuel

– Change in natural gas demand

– Change in coal and petroleum demand

• 4. Changes in Electricity demand and supply

– Change in industrial electricity demand purchased from utility

– Sales to the grid

• 5. Induced impacts from changed energy bills (passed to households)

– Change in energy bill in residential and commercial sectors

– Changes in industrial energy bills (increased gas purchases, reduced electricity bills and increased grid sales)

Installation

Operation

Energy Production

• Methodology – Based on the literature, we preliminarily estimated the division of

construction costs between different sectors (matching IMPLAN’s sectors)

– Sectoral detail was combined into ten categories

– Experts survey is used to confirm the bill of goods by asking the fraction of expenses for installing a CHP system (focusing on a medium sized (10MW) gas turbine fueled by biomass in pulp and paper industry)

Construction Bill of Goods

CATEGORY

Respondents Results from

Experts

Elicitation

Our Estimates International Paper (NG-based)

RED (NG-based)

AMEC (biomass-based)

GE Energy (biomass-based)

Primary Generation (Turbine and Power Boiler) 56% 39% 37% 36% 39% 25%

Construction 11% 20% 22% 25% 20% 20%

Electrical Equipment 11% 6% 4% 6% 7% 10%

Machinery and Fabricated Metal 6% 5% 11% 7% 9% 15%

Electronic Components (Controls) 3% 1% 3% 3% 4% 10%

Environmental Equipment 3% 10% 5% 5% 6% 7%

Other Materials 0% 2% 8% 3% 3% 3%

Scientific and Technical Services 11% 9% 7% 7% 8% 5%

Finance and Insurance 0% 8% 2% 8% 4% 5%

Other 0% 0% 1% 0% 0% 0% Total 100% 100% 100% 100% 100% 100%

Bills of Goods for CHP • When constructing a CHP

system, how are financial resources spent?

Answer = 14.5 jobs per $1 million investment.

IMPLAN Code and Industrial Sector weights (

%)

Jobs per

Million

dollars

(2010

IMPLAN)

Installation 100% 14.48

1. Primary generation 39.0% 12.58

222 Turbine and turbine generator set units manufacturing 11.34

188 Power boiler and heat exchanger manufacturing 13.42

2. Construction 20.0% 18.04

35 Construction of new nonresidential manufacturing structures 18.04

3. Electrical Equipment 7.0% 11.56

266 Power, distribution, and specialty transformer manufacturing 11.23

267 Motor and generator manufacturing 11.23

268 Switchgear and switchboard apparatus manufacturing 10.76

269 Relay and industrial control manufacturing 11.50

272 Communication and energy wire and cable manufacturing 10.02

275 All other miscellaneous electrical equipment and component manufacturing 14.62

4. Machinery and Fabricated Metal 9.0% 13.74

171 Steel product manufacturing from purchased steel 12.74

174 Aluminum product manufacturing from purchased aluminum 10.37

186 Plate work and fabricated structural product manufacturing 14.98

193 Hardware manufacturing 13.34

194 Spring and wire product manufacturing 14.19

195 Machine shops 18.94

196 Turned product and screw, nut, and bolt manufacturing 15.09

198 Valve and fittings other than plumbing 12.52

201 Fabricated pipe and pipe fitting manufacturing 13.71

202 Other fabricated metal manufacturing 14.79

207 Other industrial machinery manufacturing 15.82

226 Pump and pumping equipment manufacturing 12.71

5. Electronic Components 4.0% 11.09

234 Electronic computer manufacturing 8.57

235 Computer storage device manufacturing 11.26

236 Computer terminals and other computer peripheral equipment manufacturing 13.37

244 Electronic capacitor, resistor, coil, transformer, and other inductor manufacturing 16.39

6. Environmental Equipment 6.0% 13.05

214 Air purification and ventilation equipment manufacturing 14.68

216 Air conditioning, refrigeration, and warm air heating equipment manufacturing 12.45

250 Automatic environmental control manufacturing 14.57

7. Other Materials 3.0% 11.27

127 Plastics material and resin manufacturing 9.59

136 Paint and coating manufacturing 11.44

144 Plastics pipe and pipe fitting manufacturing 11.40

151 Rubber and plastics hoses and belting manufacturing 13.36

160 Cement manufacturing 11.78

8. Scientific and Technical Services 8.0% 22.08

369 Architectural, engineering, and related services 22.17

374 Management, scientific, and technical consulting services 20.75

375 Environmental and other technical consulting services 23.15

9. Financial and Insurance Service 4.0% 14.80

357 Insurance carriers 11.33

358 Insurance agencies, brokerages, and related activities 20.31

359 Funds, trusts, and other financial vehicles 15.50

CHP Plant Natural Gas

IMPLAN (Input-Output) Jobs Coefficients

14.5

19.8

5.7 6.6

7.4

17.4

-

5.0

10.0

15.0

20.0

25.0

Construction and Equipment

Operation & Maintenance-Non

Fuel

Electricity Natural Gas Coal & Petroleum Other - Energy Bill Savings, res and

com

Induced Impact

Installation

Operation

Energy Production

• CHP operations and maintenance are also labor-intensive, as are the goods and services purchased by the energy bill savings.

• Compare these coefficients with those for energy production.

800

850

900

950

1000

1050

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

Pu

rch

ase

d E

lec.

Co

nsu

mp

tio

n (

Bill

kW

h)

20

30

40

50

60

70

80

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

CH

P C

apac

ity

(GW

)

2010 Reference

2011 High Efficiency/Lower Costs

First-Order Impacts

Industrial Purchased Electricity Consumption

Industrial Natural Gas Consumption Total Industrial CHP Capacity

15% 8%

5%

0

20

40

60

80

100

120

140

160

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

Sale

s to

th

e G

rid

(B

ill k

Wh

)

Industrial Sales to the Grid

12%

1200

1300

1400

1500

1600

1700

1800

1900

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

NG

Co

nsu

mp

tio

n (

Bill

kW

h)

$4,660 million (in 2009$) Savings $840 million (in 2009$) gains

Capacity: 64.7->74.2 GW Elec. Price: 7.23->7.10 cents/kWh

Capacity: 39.7->43.3 GW Elec. Price: 6.290 ->6.287cents/kWh

9%

2%

9%

3%

$3,198 million (in 2009$) costs

20

30

40

50

60

70

80

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

CH

P C

apac

ity

(GW

)

2010 Reference

2011 High Efficiency/Lower Costs

CHP Capacity by Industry (NEMS) Pulp and Paper CHP Capacity

Bulk Chemicals CHP Generation Food Industry CHP Generation

6

7

8

9

10

11

12

13

20

08

2

00

9

20

10

2

01

1

20

12

2

01

3

20

14

2

01

5

20

16

2

01

7

20

18

2

01

9

20

20

2

02

1

20

22

2

02

3

20

24

2

02

5

20

26

2

02

7

20

28

2

02

9

20

30

2

03

1

20

32

2

03

3

20

34

2

03

5

Tota

l CH

P C

apac

ity

(GW

)

8

9

10

11

12

13

14

15

16

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

Tota

l CH

P C

apac

ity

(GW

)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

Tota

l CH

P C

apac

ity

(GW

)

Total Industrial CHP Capacity

15%

5%

53% 18%

26

27

28

29

30

31

32

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

09

$/m

ill B

tu

Second-Order Impacts

Residential Electricity Prices Commercial Electricity Prices

2%

- $2.4 billion Energy Bill Savings

30

31

32

33

34

35

36

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

09

$/m

ill B

tu

2010 Reference

2011 Higher Efficiency/Lower Costs 1%

- $1.6 billion Energy Bill Savings

Estimated Employment Impacts

8,800 1,400

19,900

37,000

62,200

-40000

-20000

0

20000

40000

60000

80000

100000

2015 2020 2025 2030 2035

Nu

mb

er

of

Job

s

Construction and CHP Equipment Operation & Maintenance -Non Fuel

Electricity purchases Natural Gas

Coal & Petroleum Other- Program expenses

Other- Energy Bill Savings, Res and Com Other - reduced Industry costs/increased profits

Aggregating All Jobs: The Bottom Line

Combining one time construction/installation jobs and the “annual” jobs from operation, utility-purchase changes and energy savings, yields total job-years/GW that rise from ~70,000 to ~130,000 between 2010 and 2035. Therefore, about 100,000 job-years per installed GW over 20 years or 5,000 equivalent full time jobs in a year.

0

20

40

60

80

100

120

140

160

2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029 2031 2033 2035

Job

s/G

W (

tho

u)

Total job-years over 20 years, by year of installation

Total annual non-construction job-years over 20-year life

One-time CHP construction jobs per GW

The case of a typical 25 MW CHP plant (based on a natural gas-fired turbine)

For a plant installed in 2020

Expected full-time-equivalent jobs, economy-wide

125

CHP Installation capital cost

$22.45M @ $898/kW

Value of electricity produced annually (.80 capacity factor)

$11 million @ 6.3 cents/kWh

Value of electricity used on site

$8.7 million

Annual electricity sales to the grid

$2.2 million

Annual additional natural gas costs*

$4.3 million @ $5.1/MMBtu

* Natural gas price from the EIA projection, which is more than double the current market price

• Policies and technology improvements can expand the role of

CHP in the U.S. energy economy.

• Employment is generated by plant construction, O&M, and

the expenditures from energy savings.

• Second-order job impacts far exceed construction

employment impacts.

• Lean manufacturing with CHP has triple dividends for jobs:

– maintaining domestic manufacturing = retained jobs

– direct, indirect, and induced jobs from CHP investments

– more competitive manufacturing of green products.

24

Conclusions

Contact Information ***************************************** Dr. Paul Baer Assistant Professor, School of Public Policy Email: [email protected] Dr. Marilyn A. Brown Professor, School of Public Policy Email: [email protected] Gyungwon Kim Ph.D. Student, School of Public Policy Email: [email protected] www.cepl.gatech.edu *****************************************