kempen european property seminar 30 may 2012 in amsterdam · 5/30/2012 · kempen european...

TRANSCRIPT

Kempen European Property Seminar

30 May 2012 in Amsterdam

Profile

Top 3 listed Dutch mixed real estate fund

Dutch REIT / Listed on Amsterdam Euronext (Midkap AMx)

Portfolio: €2.29bn

TRI: €203m

Outstanding shares: 63,381,376

Mixed fund

2 home markets (NL, B)

Exit strategy for Switzerland

High yield fund (8,9% GIY)

Focus on retail and offices (50/50 on average)

NL: retail and offices

B: offices and warehouses

Focus on small and medium sized companies

Financial highlights

Quarterly dividend, 30-50% Stock

LTV target 50%, Fixed interest > 80%

80% free float, main shareholder 20%

Dutch Office

portfolio:

39%

Financial ratios Consolidated

x €1,000 Q1 2012 Q4 2011 Q1 2011

Investments 2,294,260 2,321,813 1,357,829

Shareholders’ equity 895,404 909,620 600,105

Shareholders’ equity NSI 763,647 781,218 600,105

Debts to credit institutions

(excluding derivatives)

1,315,693 1,329,166 737,412

Q1 2012 Q4 2011 Q1 2011

Loan to value (%) 57.3 57.2 54.4

Average interest rate (%) 4.3 4.2 4.3

Average maturity loans (years) 2.3 2.1 2.1

Fixed interest loans (%) 91.6 91.3 91.3

Interest coverage ratio 2.5 2.4 2.7

NAV 12.86 12.96 13.86

EPRA NAV 13.83 14.02 14.27

Steady Result & Loan To Value

1.36 1.36 1.36 1.34 1.40 1.34 1.26 1.19

0.26

45,327 46,635 48,510 47,810 50,037 51,627 52,398

56,030

16,181

2004 2005 2006 2007 2008 2009 2010 2011 Q1 2012

Dividend Direct result

Direct result and Dividend

52,2 50 49,7

46,9

57,2 54,9 54,8

57,2 57,3

40

45

50

55

60

2004 2005 2006 2007 2008 2009 2010 2011 Q1 2012

LTV

Business Highlights

Merger with VastNed

Offices/Industrials

• €1.0 bn portfolio

• €68m (35%) book profit on

acquisition

• Strong focus on Randstad

• Integration completed

Record of renewals and new leases

in 2011

10,000 m² letting for the Red

Elephant The Hague

Introduction in the Euronext

Amsterdam Midcap Index (AMx)

0

20

40

60

80

100

120

Amste

rdam

regio

n

Rotterd

am re

gion

Utrech

t region

The Hague re

gion

Eindhoven re

gion

Breda

Tilburg

m² Rationale Progress Capitalizing upon NSI’s

strengths:

• NSI’s tenant focus

• Skills & funds to innovate and

invest

• In house letting teams,

development & property

management

Occupancy top priority:

• Proactive approach expiration

calendar VNOI accelerated

• VNOI data integrated into

CRM system

• Letting ‘De Rode Olifant’

shows approach is paying off

• 15% lower refurbishment

costs Rode Olifant

Increased opportunities of

scale

• Reducing operational costs

• Reducing overhead

• Leveraging operational

synergies

• Increased opportunities tenant

retention

Synergies gradually kicking

in:

• Cost synergies to amount to

approx. € 2.0 FY ‘12

• Full benefits from operational

synergies expected to

materialize as of Q4 2012

• First successes

Increased access to financial

markets

• Increased visibility for both

equity and debt capital markets

• NSI is included in MidCap

• €25 million equity issue

• 60% stock dividend 2011 final

dividend

• Syndicated loan extended

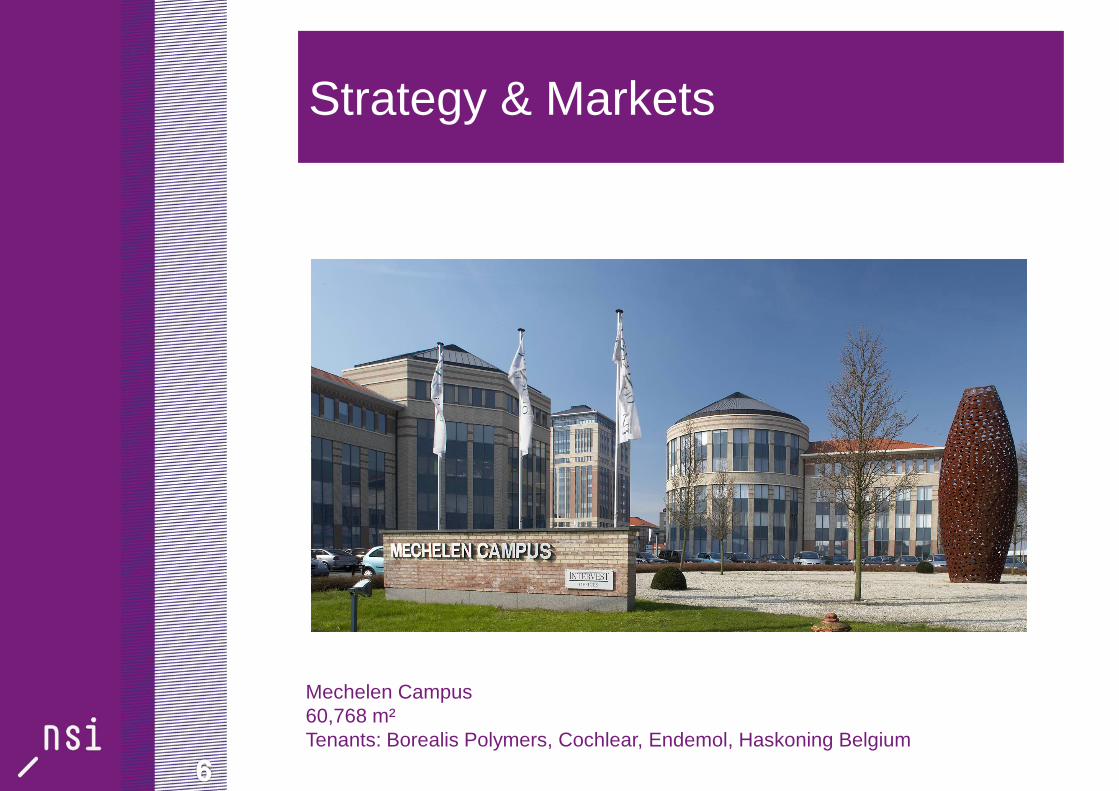

Strategy & Markets

Mechelen Campus

60,768 m²

Tenants: Borealis Polymers, Cochlear, Endemol, Haskoning Belgium

Portfolio & Market Focus

Switzerland The Netherlands

* 232 properties; €1.6 billion

* Retail and Offices

* Retail: day to day shopping

10,000 m²

Yield: 7.4% (GIY)

*Offices

Focus on Randstad

Multi tenant

Approx. 5,000 m²

Yield: 9.7% (GIY)

* 4 properties: €119m

* GIY: 6.7%

* Exit strategy in progress

Belgium

* 40 properties; €590m

* Offices and Warehouses (GIY 8.9%)

* Offices: multi tenant

* Warehouse on logistic

axes (North/South and East /West

Direct Investment Result Consolidated

Q1 2012

x €1,000

per avg

share

x €1

∆ in €

2012 vs.

2011

Q1 2011

x €1,000

per avg

share

x €1

Gross rental income 41.499 0.69 15,628 25.871 0.60

Service costs not recharged - 1.482 - 0.03 - 1,075 - 407 - 0.01

Operating costs - 4.938 - 0.08 - 1,389 - 3.549 - 0.08

Net rental income 35.079 0.58 13,164 21.915 0.51

Financing income 28 - 15 13 -

Financing expenses - 14.007 - 0.23 - 5,923 - 8.084 - 0.19

Administrative costs - 1.816 - 0.03 - 817 - 999 - 0.02

Direct investment result before

tax

19.284 0.32 6,439 12.845 0.30

Corporate income tax - 80 - - 61 - 19 -

Direct investment result after

tax

19.204 0.32 6,378 12.826 0.30

Direct result attritutable to

minority interests

- 3.023 - 0.05 - 3,023 - -

Direct investment result 16.181 0.27 3,355 12.826 0.30

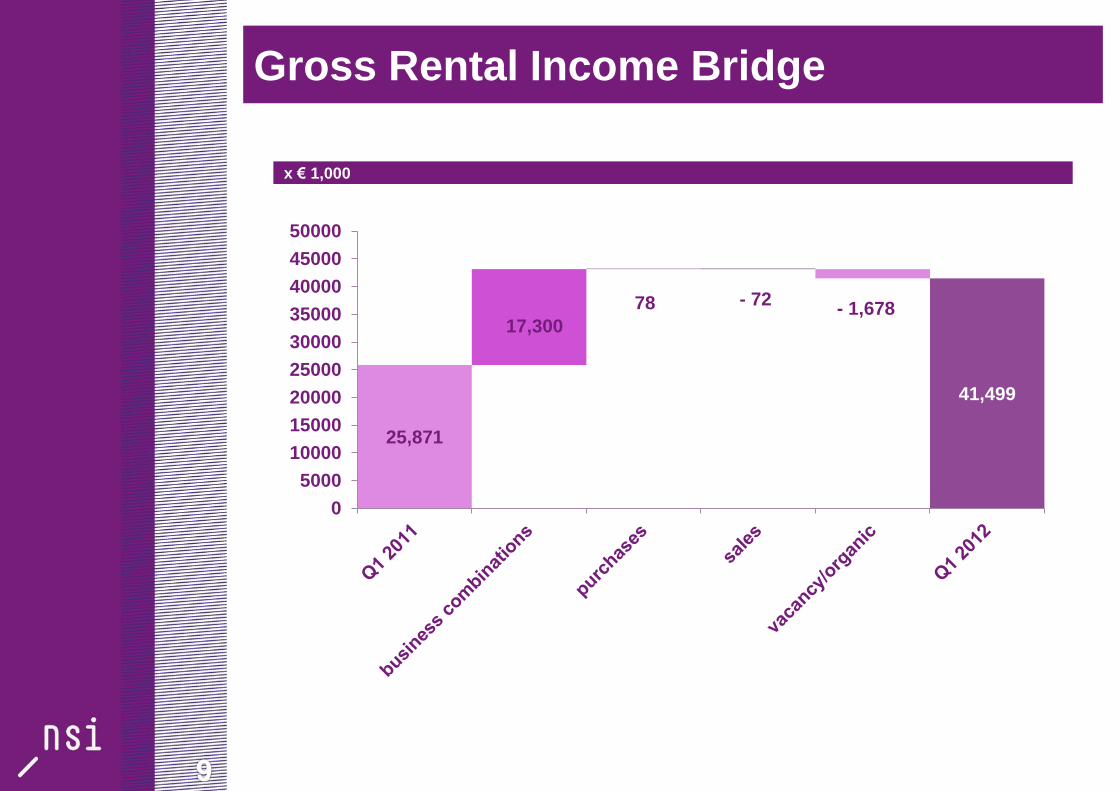

Gross Rental Income Bridge

25,871

17,300

78 - 72 - 1,678

41,499

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

x € 1,000

Portfolio Rent Development

Average effective contractual rent/m² (NL)

110,00

140,00

170,00

200,00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Q12012

Offices

Retail

Offices quarterly

Vacancy In Portfolio (%)

3,0 3,1 2,9 3,4

3,5

4,7

4,6 4,9 4,3 4,8 4,7 5,1

4,9

11,9

12,8 13,1 13,0

13,7

14,7 14,1

16,0

13,7

14,8

16,1

21,1

24,0

6,6 6,5 6,0

10,5 10,1

10,3

14,8 14,5

13,0

15,3

13,6

10,6

12,0

7,9 8,7 8,7 9,1 9,5

10,4 10,2 11,2

9,9 10,5

11,0

15,9

17,8

0,0

5,0

10,0

15,0

20,0

25,0

30,0

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Retail

Offices

Industrials

Total

• Healthy occupancy Retail at friction levels

• In Offices focus is on actively managing expiration calendar

• Redevelopment of properties to new concepts impact vacancy until completion

Property values

• Full quarterly revaluation, 25%

external

• Since peak 2007 approx. 25% re-

valuation in offices

• Valuation offices and industrial

Belgium increased

• Valuation per m2 below replacement

costs per m2 indicates general low

level of valuations

• Increased deal activity in the market;

investors returning to the market

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

2012 2013 2014 2015 2016 2017e.v.

retail

offices

industrials

14%

32%

16%

18% 17%

12%

14%

23%

4%

36%

4%

22%

Expiration of Leases

31 March 2012 (NL)

rental income x €1,000

4%

21%

15%

13%

21% 14%

Lease Strategy – Client Focus

Multi tenant over single tenant:

– Spread the risk

– Accelerate occupancy rate improvement

– Aiming at smaller and medium sized business

Improving of lettability by increasing quality and sustainability

Client focus:

- Retail specialist and local managers

- CRM and vacancy management (offices)

- In-house technical management

Flexible leasing schemes at certain dedicated locations

Huur

Service Kosten

Parkeren

Traditioneel vastgoed

Huur

Service kosten

Operator inkomsten

meetingrooms

parkeren

memberships

Horeca / IT partner

inkomsten

HNKR concept

HNKR Business model

diensten

HNK

Amsterdam

HNK

Rotterdam

Vasteland Scheepvaartkwartier

Kop van Zuid

3.0 Antwoord

HNK

Rotterdam

HNKR Clubroom

Fixed Float Total Hedge

d

% Fixed Maturity Interest

%

# banks

NL 128.1 765.2 893.2 746.6 97.9% 1.7 4.4% 10

CHF 80.9 - 80.9 - 100.0% 1.4 3.3% 1

BE 74.3 211.3 285.7 120,0 68.0% 3.2 3.9% 5

Total 283.3 976.5 1,259.8 866.6 91.3% 2.1 4.2% 14

Loan book & Hedging per country

Hedge portfolio of swaps: No overhedged positions, no margin calls

Debt maturity in the Netherlands to be further extended

• NSI is financed by well

capitalized financial

partners

• NSI is committed to active

relationship management

with its core financiers

• Novelty of insurance

company in syndicate

Loan Duration

x € 1,000

Refinancing 2012 2/3rds covered

BE: €130 mln refinanced in 2012, first expiry (€ 10 mln) end of 2013

€225mln NSI syndicated loan extended to 2015; €50m syndicated to insurance company

VNOI syndicate (amounts are exposure):

• RCF A (€ 30.4 mln) and Term A (€ 121 mio) to expire 30/6/2013

• RCF B (€ 9.2 mln) to expire 20/11/2013

• Term B (€ 99 mln) and Ancillary Fac. € 25 mln) to expire 30/6/2014

Outlook 2012

Managing the balance sheet

• Disposal program smaller assets mainly offices NL

• Swiss properties

Fully using synergies

• Improving former VNOI portfolio (client focus occupancy)

• 2.0 – 2.5m cost synergies

Branding NSI’s office portfolio

• Alliances with operators

(Re)development of properties

• Shopping centre Keizerslanden, Deventer

• Extension of several smaller shopping centres

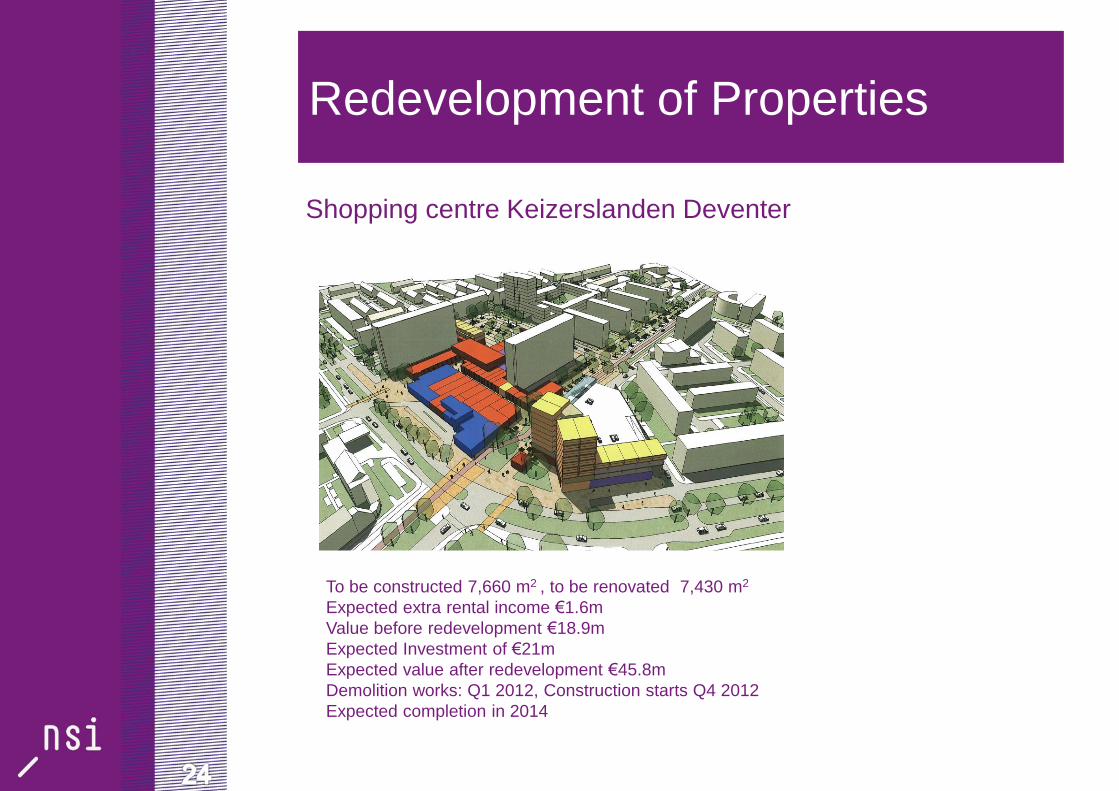

Redevelopment of Properties

Shopping centre Keizerslanden Deventer

To be constructed 7,660 m2 , to be renovated 7,430 m2

Expected extra rental income €1.6m

Value before redevelopment €18.9m

Expected Investment of €21m

Expected value after redevelopment €45.8m

Demolition works: Q1 2012, Construction starts Q4 2012

Expected completion in 2014

25

Impression

Financials

Archimedesweg Leiden

2,500 m²

Tenants: Proxy, Xendo

Balance Sheet Consolidated

x €1,000 31-03-2012 31-12-2011 31-03-2011

Total non-current assets 2,186,735 2,334,212 1,372,734

Total current assets 143,908 18,356 17,764

Total assets 2,330,643 2,352,598 1,390,498

Total shareholders equity 895,404 909,620 600,105

Interest bearing loans 999,822 1,122,648 592,758

Financial derivatives 67,192 62,297 19,239

Deferred tax liabilities 1,886 1,678 973

Redemption requirement long-term liabilities 226,439 137,189 115,313

Financial derivatives - 96 460

Debts to credit institutions 94,529 73,727 42,696

Other accounts payable and deferred income 45,371 256,325 177,423

Total shareholders’ equity and liabilities 2,330,643 2,352,568 1,390,498

* including minority share

Indirect Investment Result Consolidated

x €1,000 Q1 2012 Q4 2011 Q1 2011

Revaluation of investments - 26,581 - 18,879 - 5,097

Elimination of rental incentives - 293 - -

Result from other investments - 170 - 254

Net result on sales of investments - 127 -

Movements in market value of financial

derivatives

- 4,799 - 5,926 11,564

Exchange-rate differences - 523 - 14 275

Allocated management costs - 581 - 573 - 340

Merger costs - - 6,557 - 217

Result from bargain purchase - 68,161 -

Indirect investment result before tax - 32,777 36,509 5,931

Corporate income tax - 193 - 114 - 80

Indirect investment result after tax - 32,970 36,395 5,851

Indirect result attributable to minority

interests

- 332 2,034 -

Indirect investment result - 33,302 38,429 5,851

Portfolio Bridge

2,321,813

1,899 - 4,005

- 23,839

- 4,293

1,551

1,134

2,294,260

2.000.000

2.250.000

2.500.000

x € 1,000

Direct Investment Result Consolidated

x €1,000 Q1 2012 Q4 2011 Q1 2011

Gross rental income 41,499 42,575 25,871

Service costs not recharged - 1,482 - 1,469 - 407

Operating costs - 4,938 - 4,902 - 3,549

Net rental income 35,079 36,204 21,915

Financing income - 28 46 13

Financing costs - 14,007 - 14,822 - 8,084

Administrative costs - 1,816 - 1,819 - 999

Direct investment result before tax 19,284 19,609 12,845

Corporate income tax - 80 - 113 - 19

Direct investment result after tax 19,204 19,496 12,826

Direct result attributable to minority

interests

- 3,023 - 2.608 -

Direct investment result 16,181 16,88 12,826