lee county business climate survey report executive business climate survey report, 2016 q2...

TRANSCRIPT

LEE COUNTY BUSINESS

CLIMATE SURVEY REPORT Second Quarter, 2016

Prepared in partnership with:

and

The Regional Economic Research Institute • Florida Gulf Coast University

Project Staff

Dr. Christopher Westley, Director

John Shannon, Economist

Nicholas Holst, Lead Student Researcher

Monique Carlone, Student Researcher

Alesa Whitehead, Student Researcher

Report Information

This report is conducted quarterly by the Horizon Council of Lee County, Florida, and

Florida Gulf Coast University’s Regional Economic Research Institute. This work would not

be possible without considerable cooperation from the Horizon Council’s Chairs, the RERI’s

student researchers, and the Lee County Economic Development Council.

The Regional Economic Research Institute studies, analyzes are reports on the regional

economy encompassing Collier, Lee, Charlotte, Hendry, and Glades counties. Established

in 2005, it serves as a public service and economic development unit of the Lutgert College

of Business’ Dean’s Office and strives to connect Southwest Florida to the resources of

Florida Gulf Coast University.

The Institute’s Business Climate Survey group specializes in sampling design and analysis,

including program evaluation, policy research, and needs assessment. The Business

Climate Survey group involves FGCU students in every stage of survey development,

allowing them to develop professional skills and networks that add value to their degrees

and, by extension, to their future employers.

Regional Economic Research Institute

Lutgert College of Business

Florida Gulf Coast University

10501 FGCU Blvd, S.

Fort Myers, FL 33965-6565

(239) 590-1000

http://www.fgcu.edu/cob/reri/

Photo Credits: Shutterstock, Lee County Economic Development Office

1 Regional Economic Research Institute

TABLE OF CONTENTS

INTRODUCTION ............................................................................................................................................................. 2

EXECUTIVE SUMMARY .................................................................................................................................................. 3

I. RECURRING QUESTIONS ............................................................................................................................................. 4

II. THE EXECUTIVE BUSINESS CLIMATE INDEX ................................................................................................................ 6

III. SPECIAL TOPICS ........................................................................................................................................................ 7

IV. COMMENTS, SUGGESTIONS, AND RECOMMENDATIONS ........................................................................................ 9

V. COMPANY CHARACTERISTICS ................................................................................................................................. 10

APPENDIX A. HISTORICAL TRENDS OF RECURRING QUESTIONS .................................................................................. 11

APPENDIX B. FULL COMMENTS, SUGGESTIONS, AND RECOMMENDATIONS .............................................................. 12

APPENDIX C. FULL COMMENTS ON TOP FIVE CHALLENGES FOR COMPANIES ............................................................. 13

2 Executive Business Climate Survey Report, 2016 Q2

INTRODUCTION

The Lee County Business Climate Survey Report, published in partnership

between the Horizon Council and Florida Gulf Coast University, provides primary

research to the business community, elected officials, and other concerned

citizens in an effort to gauge the state of Lee County’s economy over time as well

as impressions and concerns about it in the future.

Since the beginning of this partnership, the BCS has been comprised of three

areas of focus. The first area—encompassed in the first seven questions of the

survey—focuses on Lee County business executives’ impressions of economic conditions and trends with respect to hiring and

investment. The second area has been the calculation of an Executive Business Climate Index. This EBCI provides a summary number

which will allow one to quickly gauge whether the business climate in Lee County is improving or declining. Finally, the third area has

been various questions that change from survey to survey. In the past, these “Special Topics” have focused on areas such as business

executives’ concerns about interest rates and access to capital, firms’ demand for critical occupations and their ability to find workers

within those occupations, the cost of doing business in Lee County, and even concern for employee wellness and wellness programs.

The BCS also allows respondents to voice concerns, kudos, and criticisms of Lee County’s economic environment. Every effort is made

to include these comments in each survey.

The Horizon Council FGCU Business Climate Survey is administered, written, and published by the staff and students working with the

Regional Economic Research Institute in the Lutgert College of Business. We very much welcome your comments and suggestions

regarding the report, including suggestions for Special Topics questions for future editions.

This survey would not have been possible without the many busy business owners and executives who took the time to respond to it.

I also thank John Boland, Glen Salyer, and their colleagues at the Lee County Economic Development Office; Robert Beatty, Dean of

Lutgert College of Business at FGCU; Russell Schropp, Chair of the Horizon Council’s Business Issues Taskforce; and Michael Quaintance

of Keiser University. CareerSource Southwest Florida’s James Wall and Peg Elmore provided valuable input and advice.

Christopher Westley Dr. Christopher Westley Director, Regional Economic Research Institute Lutgert College of Business Florida Gulf Coast University Fort Myers, Florida 33965-6565

3 Regional Economic Research Institute

EXECUTIVE SUMMARY

The Executive Business Climate Survey provides a view of the local economy that is based on responses from senior executives from

a range of industries across the county. An invitation to complete the internet survey was sent to 565 executives and business owners

in Lee County. Eighty-eight executives completed the survey from April 18, 2016, through May 2, 2016. Four reminders were sent

during the survey period.

This survey provides a key economic indicator for Lee County, the Executive Business Climate Index. This index value is computed each

quarter and released to the public as a way to provide an established economic indicator on the state of the local economy. The index

is computed using the two questions concerning the current and future economic conditions and a third question concerning the

expected industry economic conditions. The index is an average of the responses, with substantially better equal to 100, moderately

better equal to 75, same equal to 50, moderately worse equal to 25 and substantially worse equal to zero. The index value can range

from 0 to 100.

The results from the second quarter survey reflect a five-point decline from the first quarter 2016 measure, with the index falling from

68 to 63. This marks the lowest EBCI since the second quarter 2012, when the EBCI was calculated at 62.

The current survey’s Special Topics section focuses on the cost of doing business, prices, the state of the economy, and primary

business challenges for business in Lee County. Other findings of the Business Climate Survey for the second quarter of 2016 include:

59 percent of executives stated that the current economic conditions have improved over last year, while 33 percent stated

that they were the same;

50 percent of the executives expect the economy to improve over the next year;

50 percent of the executives stated that the current economic conditions for their industry have improved over last year, but

32 percent stated that economic conditions remained approximately the same, and 18 percent indicated they are moderately

worse;

49 percent of executives expect economic conditions for their industry to improve over the next year;

58 percent of companies expect to increase investment next year while 2 percent expect to reduce investment levels;

50 percent of executives had increased employment over the last year, while 2 percent had reduced employment;

44 percent of executives expect to increase employment at their companies during the next year, while 56 percent of

executives plan to remain at the same level;

79 percent of executives indicate that the cost of doing business has increased by no more than 5 percent over the past year;

12 percent of executives believe that the cost of doing business will increase by at least 5 percent over the next year;

41 percent of executives indicate that they have increased prices by at least 2 percent over the past year;

87 percent of executives stated they are optimistic about the Southwest Florida economy over the next year;

88 percent of executives indicate that they are optimistic about the state of Florida economy over the next year;

58 percent of executives stated that they are optimistic about the United States economy over the next year, while 42 percent

are pessimistic about the United States economy over the next year; and

63 percent of executives believe that finding qualified employees will be a top 5 challenge over the next year.

4 Executive Business Climate Survey Report, 2016 Q2

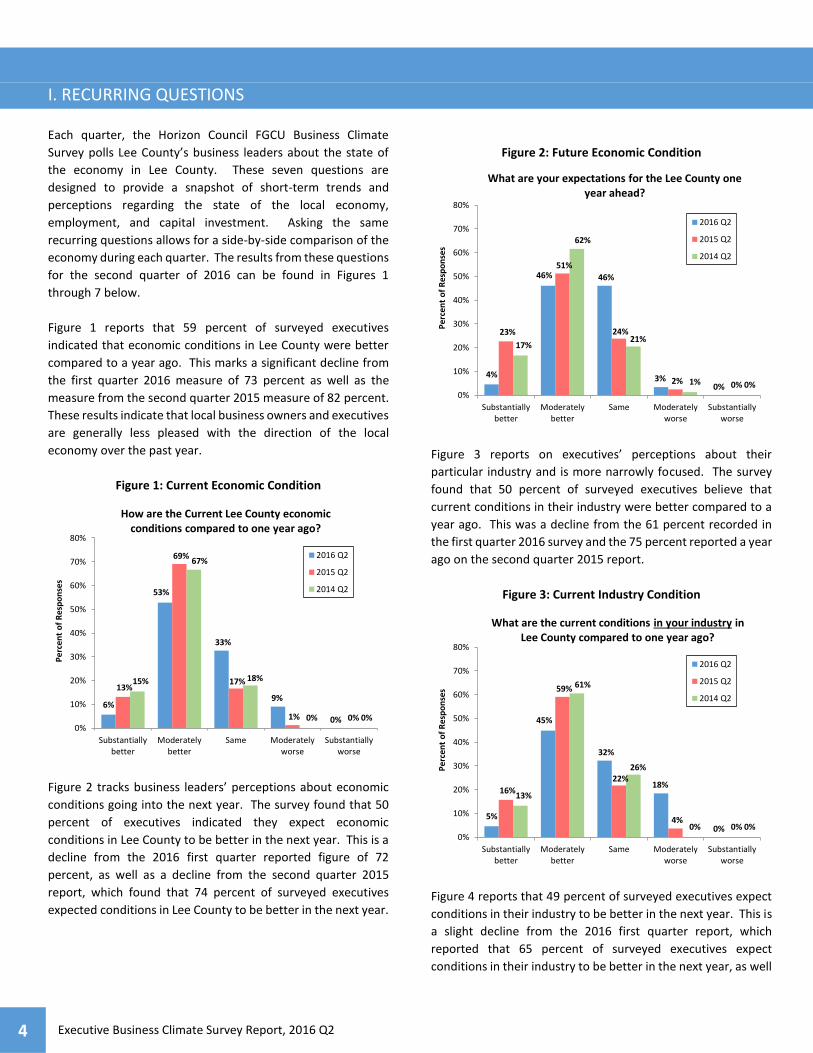

I. RECURRING QUESTIONS

Each quarter, the Horizon Council FGCU Business Climate

Survey polls Lee County’s business leaders about the state of

the economy in Lee County. These seven questions are

designed to provide a snapshot of short-term trends and

perceptions regarding the state of the local economy,

employment, and capital investment. Asking the same

recurring questions allows for a side-by-side comparison of the

economy during each quarter. The results from these questions

for the second quarter of 2016 can be found in Figures 1

through 7 below.

Figure 1 reports that 59 percent of surveyed executives

indicated that economic conditions in Lee County were better

compared to a year ago. This marks a significant decline from

the first quarter 2016 measure of 73 percent as well as the

measure from the second quarter 2015 measure of 82 percent.

These results indicate that local business owners and executives

are generally less pleased with the direction of the local

economy over the past year.

Figure 1: Current Economic Condition

Figure 2 tracks business leaders’ perceptions about economic

conditions going into the next year. The survey found that 50

percent of executives indicated they expect economic

conditions in Lee County to be better in the next year. This is a

decline from the 2016 first quarter reported figure of 72

percent, as well as a decline from the second quarter 2015

report, which found that 74 percent of surveyed executives

expected conditions in Lee County to be better in the next year.

Figure 2: Future Economic Condition

Figure 3 reports on executives’ perceptions about their

particular industry and is more narrowly focused. The survey

found that 50 percent of surveyed executives believe that

current conditions in their industry were better compared to a

year ago. This was a decline from the 61 percent recorded in

the first quarter 2016 survey and the 75 percent reported a year

ago on the second quarter 2015 report.

Figure 3: Current Industry Condition

Figure 4 reports that 49 percent of surveyed executives expect

conditions in their industry to be better in the next year. This is

a slight decline from the 2016 first quarter report, which

reported that 65 percent of surveyed executives expect

conditions in their industry to be better in the next year, as well

6%

53%

33%

9%

0%

13%

69%

17%

1% 0%

15%

67%

18%

0% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallybetter

Moderatelybetter

Same Moderatelyworse

Substantiallyworse

Pe

rcen

t o

f R

esp

on

ses

How are the Current Lee County economic conditions compared to one year ago?

2016 Q2

2015 Q2

2014 Q2

4%

46% 46%

3%0%

23%

51%

24%

2% 0%

17%

62%

21%

1% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallybetter

Moderatelybetter

Same Moderatelyworse

Substantiallyworse

Pe

rcen

t o

f R

esp

on

ses

What are your expectations for the Lee County one year ahead?

2016 Q2

2015 Q2

2014 Q2

5%

45%

32%

18%

0%

16%

59%

22%

4%0%

13%

61%

26%

0% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallybetter

Moderatelybetter

Same Moderatelyworse

Substantiallyworse

Pe

rce

nt

of

Res

po

nse

s

What are the current conditions in your industry in Lee County compared to one year ago?

2016 Q2

2015 Q2

2014 Q2

5 Regional Economic Research Institute

as a decline from the 2015 second quarter report, which

reported that 72 percent of surveyed executives expect

conditions in their industry to be better in the next year.

Figure 4: Future Industry Condition

Figures 5 and 6 focus on employment. Figure 5 reports that 50

percent of executives have increased employment over the last

year. This is an increase from the 2016 first quarter report,

which reported that 49 percent of surveyed executives have

increased employment over the past year, however this was a

decline from the 2015 second quarter report, which reported

that 55 percent of surveyed executives have increased

employment over the past year.

Figure 5: Current Hiring Trend

Figure 6 reports that 44 percent of surveyed executives expect

to increase employment over the next year. This is a decline

from the 2016 first quarter report, which reported that 48

percent of surveyed executives expect to increase employment

over the next year, and a decline from the 2015 second quarter

report, which reported that 60 percent of surveyed executives

expect to increase employment over the next year.

Figure 6: Future Hiring Trend

Finally, Figure 7 focuses on capital investment. It reports that

58 percent of surveyed executives expect to increase

investment over the next year. There was a decrease from the

2016 first quarter report, which reported that 60 percent of

surveyed executives expect to increase investment over the

next year, and a decline from the second quarter report from

2015, which reported that 62 percent of surveyed executives

expect to increase investment over the next year.

Figure 7: Future Investment Trend

Results from previous quarters’ surveys going back to 2012 can

be found on FGCU’s Regional Economic Research Institute’s

web site, at fgcu.edu/cob/reri. For charts depicting historical

trends for recurring questions, see Appendix A below.

7%

42%46%

4%1%

18%

54%

24%

5%0%

19%

54%

27%

0% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallybetter

Moderatelybetter

Same Moderatelyworse

Substantiallyworse

Pe

rcen

t o

f R

esp

on

ses

What are your expectations for your own industryin Lee County one year ahead?

2016 Q2

2015 Q2

2014 Q2

10%

40%44%

6%

0%

5%

50%

42%

4%0%

9%

54%

33%

4%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallyincreased

employment

Moderatelyincreased

employment

Little or nochange In

employment

Moderatelyreduced

employment

SubstantiallyReduced

Employment

Pe

rcen

t o

f R

esp

on

ses

What has been your hiring trend over the last year?

2016 Q2

2015 Q2

2014 Q2

6%

38%

56%

0% 0%

7%

53%

39%

1% 0%0%

54%

44%

1% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallyincrease

employment

Moderatelyincrease

employment

Same or flatemployment

Moderatelyreduce

employment

SubstantiallyReduce

Employment

Pe

rcen

t o

f R

esp

on

ses

What hiring trends do you see for your business over the next year?

2016 Q2

2015 Q2

2014 Q2

7%

51%

40%

2%0%

11%

51%

33%

5%0%

13%

49%

33%

4%1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Substantiallyincrease

investment

Moderatelyincrease

investment

Keepinvestment the

same or flat

Moderatelyreduce

investment

SubstantiallyReduce

investment

Pe

rce

nt

of

Re

spo

nse

s

Do you plan to increase investment in your business during the next year?

2016 Q2

2015 Q2

2014 Q2

6 Executive Business Climate Survey Report, 2016 Q2

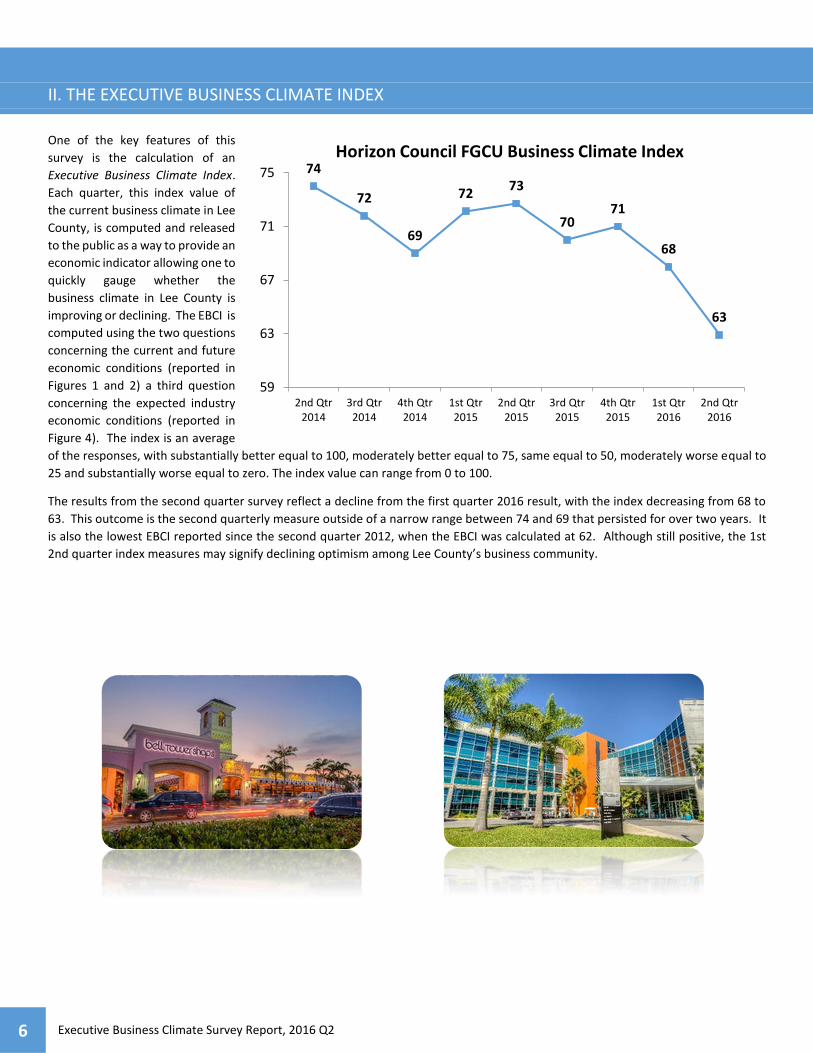

II. THE EXECUTIVE BUSINESS CLIMATE INDEX

One of the key features of this

survey is the calculation of an

Executive Business Climate Index.

Each quarter, this index value of

the current business climate in Lee

County, is computed and released

to the public as a way to provide an

economic indicator allowing one to

quickly gauge whether the

business climate in Lee County is

improving or declining. The EBCI is

computed using the two questions

concerning the current and future

economic conditions (reported in

Figures 1 and 2) a third question

concerning the expected industry

economic conditions (reported in

Figure 4). The index is an average

of the responses, with substantially better equal to 100, moderately better equal to 75, same equal to 50, moderately worse equal to

25 and substantially worse equal to zero. The index value can range from 0 to 100.

The results from the second quarter survey reflect a decline from the first quarter 2016 result, with the index decreasing from 68 to

63. This outcome is the second quarterly measure outside of a narrow range between 74 and 69 that persisted for over two years. It

is also the lowest EBCI reported since the second quarter 2012, when the EBCI was calculated at 62. Although still positive, the 1st

2nd quarter index measures may signify declining optimism among Lee County’s business community.

74

72

69

7273

7071

68

63

59

63

67

71

75

2nd Qtr2014

3rd Qtr2014

4th Qtr2014

1st Qtr2015

2nd Qtr2015

3rd Qtr2015

4th Qtr2015

1st Qtr2016

2nd Qtr2016

Horizon Council FGCU Business Climate Index

7 Regional Economic Research Institute

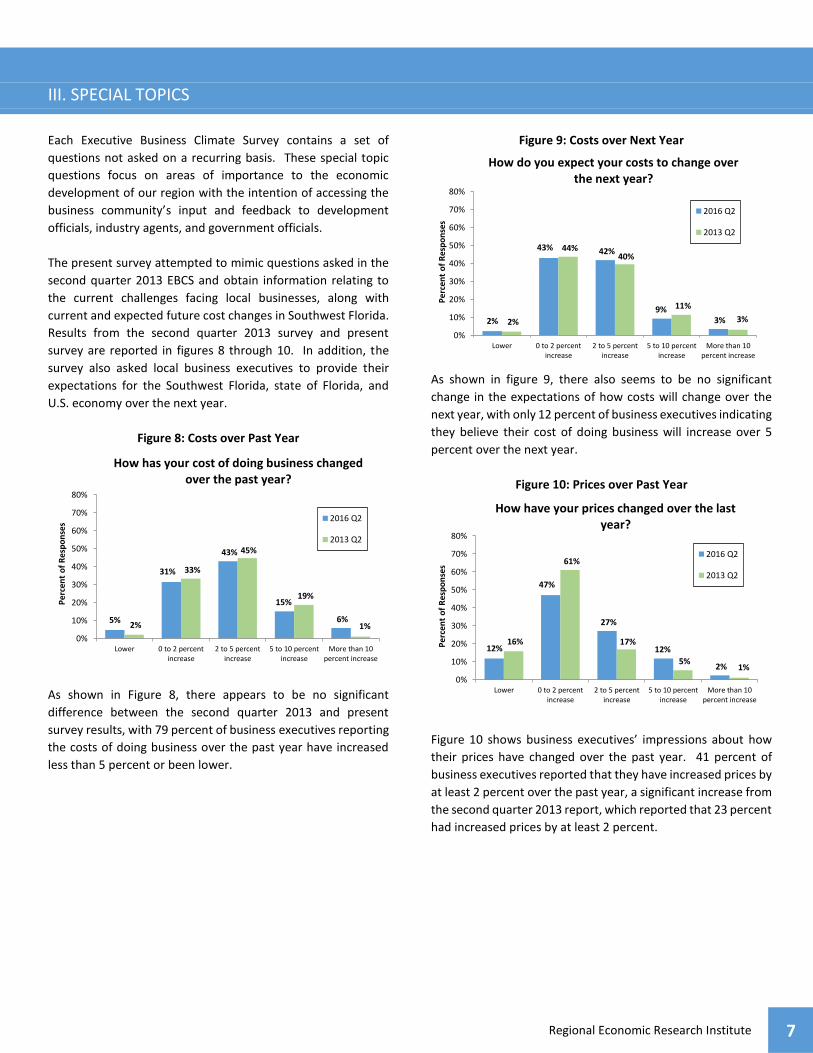

III. SPECIAL TOPICS

Each Executive Business Climate Survey contains a set of

questions not asked on a recurring basis. These special topic

questions focus on areas of importance to the economic

development of our region with the intention of accessing the

business community’s input and feedback to development

officials, industry agents, and government officials.

The present survey attempted to mimic questions asked in the

second quarter 2013 EBCS and obtain information relating to

the current challenges facing local businesses, along with

current and expected future cost changes in Southwest Florida.

Results from the second quarter 2013 survey and present

survey are reported in figures 8 through 10. In addition, the

survey also asked local business executives to provide their

expectations for the Southwest Florida, state of Florida, and

U.S. economy over the next year.

Figure 8: Costs over Past Year

As shown in Figure 8, there appears to be no significant

difference between the second quarter 2013 and present

survey results, with 79 percent of business executives reporting

the costs of doing business over the past year have increased

less than 5 percent or been lower.

Figure 9: Costs over Next Year

As shown in figure 9, there also seems to be no significant

change in the expectations of how costs will change over the

next year, with only 12 percent of business executives indicating

they believe their cost of doing business will increase over 5

percent over the next year.

Figure 10: Prices over Past Year

Figure 10 shows business executives’ impressions about how

their prices have changed over the past year. 41 percent of

business executives reported that they have increased prices by

at least 2 percent over the past year, a significant increase from

the second quarter 2013 report, which reported that 23 percent

had increased prices by at least 2 percent.

5%

31%

43%

15%

6%2%

33%

45%

19%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Lower 0 to 2 percentincrease

2 to 5 percentincrease

5 to 10 percentincrease

More than 10percent increase

Pe

rcen

t o

f R

esp

on

ses

How has your cost of doing business changed over the past year?

2016 Q2

2013 Q2

2%

43% 42%

9%3%2%

44%40%

11%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Lower 0 to 2 percentincrease

2 to 5 percentincrease

5 to 10 percentincrease

More than 10percent increase

Pe

rcen

t o

f R

esp

on

ses

How do you expect your costs to change over the next year?

2016 Q2

2013 Q2

12%

47%

27%

12%

2%

16%

61%

17%

5%1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Lower 0 to 2 percentincrease

2 to 5 percentincrease

5 to 10 percentincrease

More than 10percent increase

Pe

rcen

t o

f R

esp

on

ses

How have your prices changed over the last year?

2016 Q2

2013 Q2

8 Executive Business Climate Survey Report, 2016 Q2

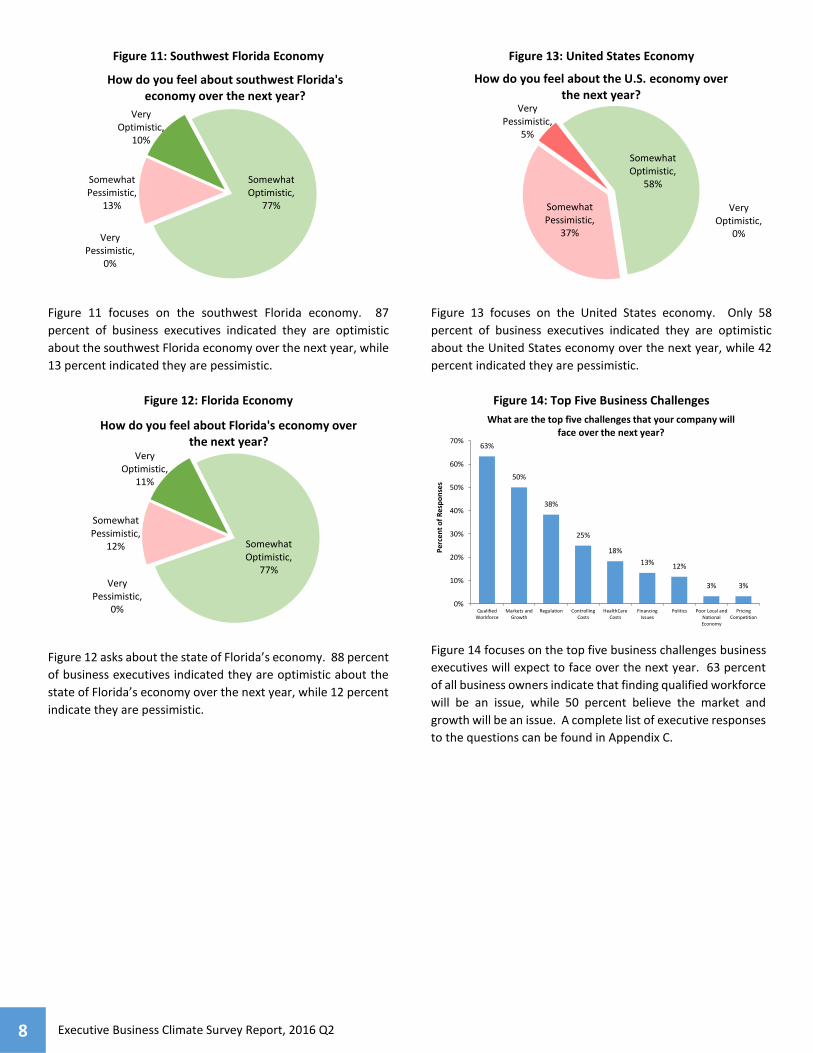

Figure 11: Southwest Florida Economy

Figure 11 focuses on the southwest Florida economy. 87

percent of business executives indicated they are optimistic

about the southwest Florida economy over the next year, while

13 percent indicated they are pessimistic.

Figure 12: Florida Economy

Figure 12 asks about the state of Florida’s economy. 88 percent

of business executives indicated they are optimistic about the

state of Florida’s economy over the next year, while 12 percent

indicate they are pessimistic.

Figure 13: United States Economy

Figure 13 focuses on the United States economy. Only 58

percent of business executives indicated they are optimistic

about the United States economy over the next year, while 42

percent indicated they are pessimistic.

Figure 14: Top Five Business Challenges

Figure 14 focuses on the top five business challenges business

executives will expect to face over the next year. 63 percent

of all business owners indicate that finding qualified workforce

will be an issue, while 50 percent believe the market and

growth will be an issue. A complete list of executive responses

to the questions can be found in Appendix C.

Very Optimistic,

10%

Somewhat Optimistic,

77%

Somewhat Pessimistic,

13%

Very Pessimistic,

0%

How do you feel about southwest Florida's economy over the next year?

Very Optimistic,

11%

Somewhat Optimistic,

77%

Somewhat Pessimistic,

12%

Very Pessimistic,

0%

How do you feel about Florida's economy over the next year?

Very Optimistic,

0%

Somewhat Optimistic,

58%

Somewhat Pessimistic,

37%

Very Pessimistic,

5%

How do you feel about the U.S. economy over the next year?

63%

50%

38%

25%

18%

13% 12%

3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

QualifiedWorkforce

Markets andGrowth

Regulation ControllingCosts

HealthCareCosts

FinancingIssues

Politics Poor Local andNationalEconomy

PricingCompetition

Per

cen

t o

f R

esp

on

ses

What are the top five challenges that your company will face over the next year?

9 Regional Economic Research Institute

IV. COMMENTS, SUGGESTIONS, AND RECOMMENDATIONS

The comments indicated that executives were concerned with the national and international economy as it relates to local activity, as

well as some general comments of the workforce. There are concerns and comments about:

Public Infrastructure

Proper training

Governmental regulation

Increasing costs

Wage rates

Executive responses to this question are found in Appendix B.

10 Executive Business Climate Survey Report, 2016 Q2

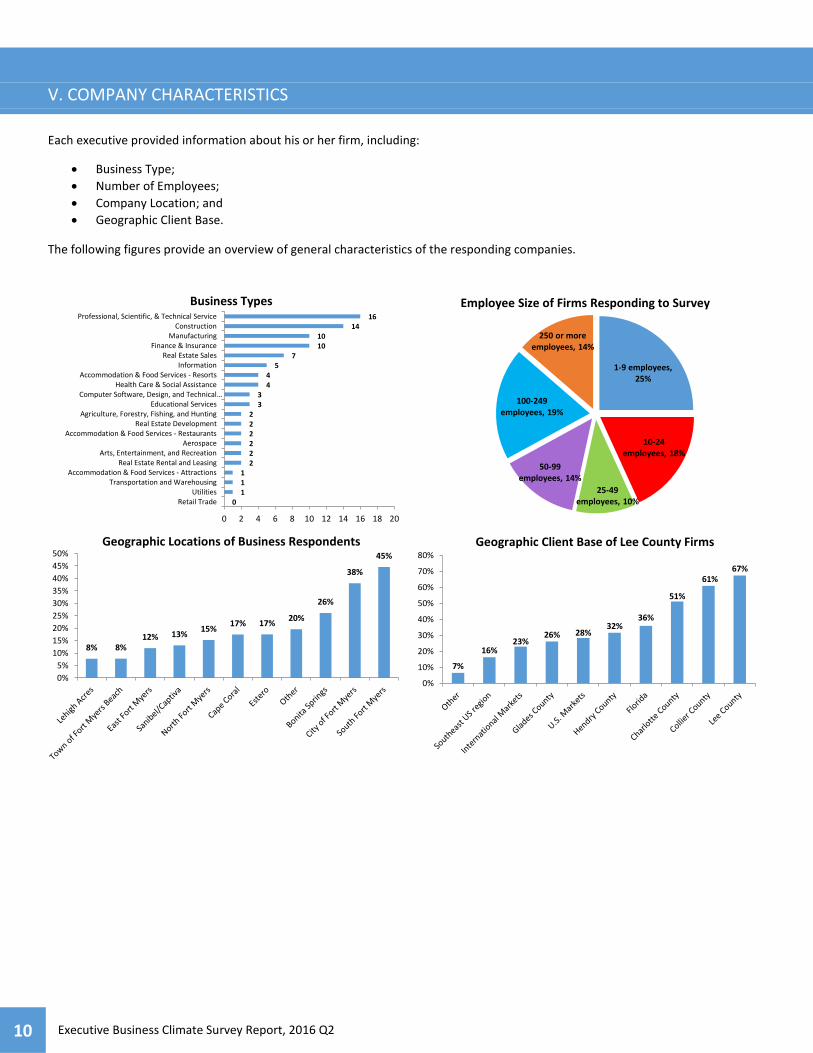

V. COMPANY CHARACTERISTICS

Each executive provided information about his or her firm, including:

Business Type;

Number of Employees;

Company Location; and

Geographic Client Base.

The following figures provide an overview of general characteristics of the responding companies.

0111

222222

33

44

57

1010

1416

0 2 4 6 8 10 12 14 16 18 20

Retail TradeUtilities

Transportation and WarehousingAccommodation & Food Services - Attractions

Real Estate Rental and LeasingArts, Entertainment, and Recreation

AerospaceAccommodation & Food Services - Restaurants

Real Estate DevelopmentAgriculture, Forestry, Fishing, and Hunting

Educational ServicesComputer Software, Design, and Technical…

Health Care & Social AssistanceAccommodation & Food Services - Resorts

InformationReal Estate Sales

Finance & InsuranceManufacturing

ConstructionProfessional, Scientific, & Technical Service

Business Types

1-9 employees, 25%

10-24 employees, 18%

25-49 employees, 10%

50-99 employees, 14%

100-249 employees, 19%

250 or more employees, 14%

Employee Size of Firms Responding to Survey

8% 8%12% 13%

15%17% 17%

20%

26%

38%

45%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%Geographic Locations of Business Respondents

7%

16%23%

26% 28%32%

36%

51%

61%67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Geographic Client Base of Lee County Firms

11 Regional Economic Research Institute

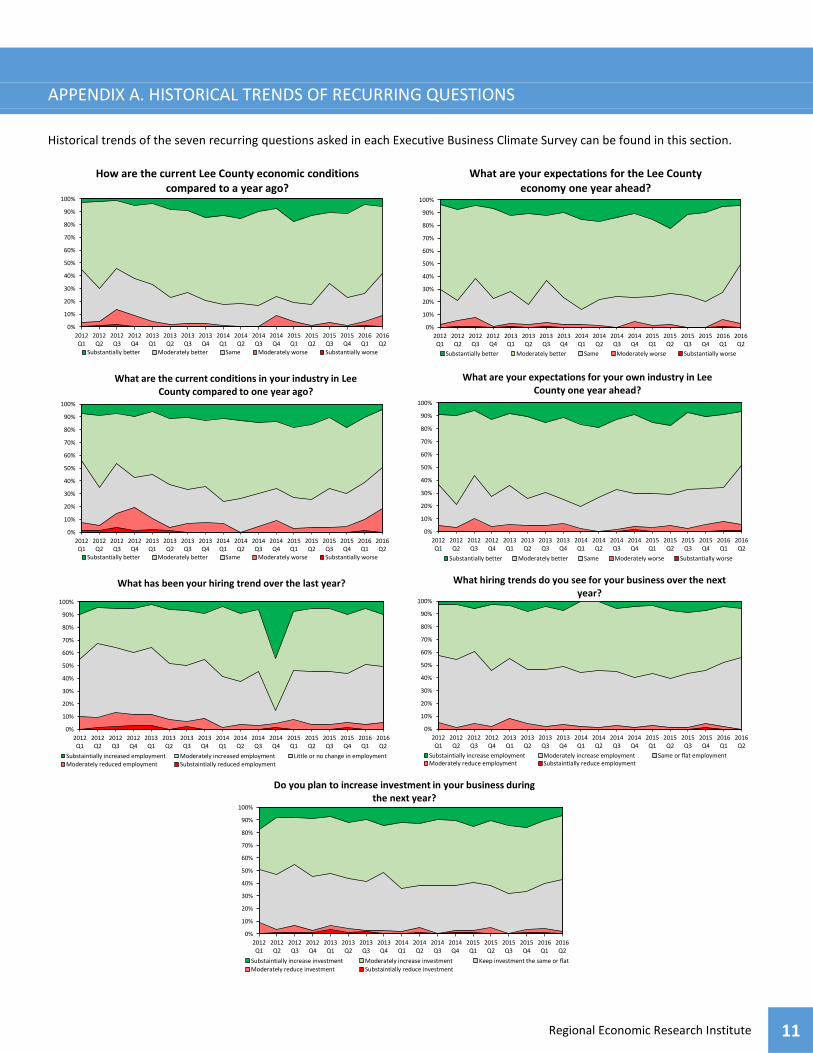

APPENDIX A. HISTORICAL TRENDS OF RECURRING QUESTIONS

Historical trends of the seven recurring questions asked in each Executive Business Climate Survey can be found in this section.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

How are the current Lee County economic conditions compared to a year ago?

Substantially better Moderately better Same Moderately worse Substantially worse

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

What are your expectations for the Lee County economy one year ahead?

Substantially better Moderately better Same Moderately worse Substantially worse

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

What are the current conditions in your industry in Lee County compared to one year ago?

Substantially better Moderately better Same Moderately worse Substantially worse

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

What are your expectations for your own industry in Lee County one year ahead?

Substantially better Moderately better Same Moderately worse Substantially worse

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

What has been your hiring trend over the last year?

Substaintially increased employment Moderately increased employment Little or no change in employmentModerately reduced employment Substaintially reduced employment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

What hiring trends do you see for your business over the next year?

Substaintially increase employment Moderately increase employment Same or flat employmentModerately reduce employment Substaintially reduce employment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

Do you plan to increase investment in your business during the next year?

Substaintially increase investment Moderately increase investment Keep investment the same or flat

Moderately reduce investment Substaintially reduce investment

12 Executive Business Climate Survey Report, 2016 Q2

APPENDIX B. FULL COMMENTS, SUGGESTIONS, AND RECOMMENDATIONS

This list includes specific responses from the executives for the following question:

Please indicate any other comments, suggestions, or recommendations you would like to make regarding the regional economy or your

business.

1. Again, more skilled workers needed.

2. Lee County needs to improve its roadways and infrastructure before development happens - not in response to it after it

happens. Collier County does a good job of putting in roadways and infrastructure knowing where development will be

expanding in future years. Lee County continues to wait and be reactive. This is not a good strategy. This could be a result

of Lee County's reduced impact fees limiting the funding needed.

3. Focus on more technology based businesses and industries, and promote or incentivize local colleges to increase pool of

qualified employees with math and computer technology skills.

4. We must stop the dumping of freshwater from Lake Okeechobee, this is killing local business. We must encourage Southwest

Florida to invest in bringing more industry to the area. This area is entirely service based and cannot support the salaries

required to keep educated, quality people in the area.

5. There is increasing pressure in Southwest Florida and particular in Lee County to push away all "dirty" business, as in heavy

industrial and manufacturing business. These types of businesses provide for well-rounded regional economy and often,

allow for the "pretty" businesses to function. It is wonderful for the residents of southern Lee County to want to push out

"that dirty old railroad", or the trucks and warehouses. But they forget how all the materials arrived to build their homes,

how the food they eat ended up on the grocery shelves, or how all of the recyclable materials they "throw-away" leave the

area. We need to stop beating up on heavy industry and transportation, and build a better Southwest Florida for today and

tomorrow.

6. The density of areas needs to be increased to reduce suburban sprawl which is what creates massive traffic. We need an

improved metro system, and connection to a high speed rail nationwide system that also intersects with Tampa, Orlando,

Miami and Jacksonville. Without changes the future will be traffic gridlock.

7. We need to look carefully at limiting growth. We cannot maintain the current pace and have any quality of life. Also, limit

the contact between elected officials and developers.

8. I still believe that diversification is important for a robust regional economy. I see some diversification, but we are still very

service and tourism focused. Our demographic is heavily skewed toward seniors. This will impede efforts to diversify the

economy.

9. Costs for doing business varies by county/region. For instance, the cost of doing business in Cape Coral is about 20% more

than in Fort Myers, and they are in the same county.

10. Regional approach to attracting new and coming business. Stream-lining processes for permitting, zoning, land entitlement,

(area standardization) Redundancy elimination.

11. Increase plumbing salaries.

13 Regional Economic Research Institute

APPENDIX C. FULL COMMENTS ON TOP FIVE CHALLENGES FOR COMPANIES

This list includes specific responses from the executives for the following questions:

What are the top five challenges that your company will face over the next year?

Qualified Workforce

1. Training and recruiting young workforce

2. Hiring technological competent workers

3. Hiring employees for traditional manual labor

4. Finding qualified employees

5. Hiring experienced colleagues

6. Retaining qualified employees

7. Access to skilled labor

8. Hiring well quailed tradesmen and technicians

9. Hiring class A CDL drivers

10. Finding educated and qualified help to perform administrative duties

11. Attracting talent

HealthCare Costs

1. Increase in healthcare and overall benefits costs.

2. Health insurance

3. Increased cost of healthcare for employees

Controlling Costs

1. Increase pressure to raise wages

2. Increased difficulty managing costs through operations improvements

3. Material prices continue to increase

4. Holding fees close to the CPI

5. Costs to do business continue to rise

Markets and Growth

1. Demand is not increase at the same rate as inflation

2. Difficulty staying up to date with technological changes

3. Increased difficulty maintaining market share

4. Difficulty attracting and maintaining clients

5. Lack of other businesses investing in technology

6. Technology will continue to fragment media consumption thereby reducing my company’s penetration…thereby lowering

my ability to hold advertising rates

7. Financial sector profits are nil, good for clients bad for us. We are doing the same work for half the revenue.

8. Commodity inflation/deflation

9. Expanding our market

10. Need to increase international exposure in Europe

11. Keeping up with false demands in housing

14 Executive Business Climate Survey Report, 2016 Q2

12. Slowdown of home sales

13. Excessive hotel rates and rental housing become issues for consumer spending and hiring of personnel. Disposable income

for tourism is limited to hotel stays and bare essentials, when the average cost of a hotel in Southwest Florida is in excess of

$250 per night. Also, lack of affordable housing and limited rental housing makes it difficult to recruit talented personnel to

the SWFL region. We have experienced several staff members resign and return "home" to other areas due to the housing

crisis. Our employment cost has gone up as a result.

Regulation

1. Increased federal and state requirements not related to delivery of service

2. Increase in regulations from the EPA

3. Increase in government bureaucracy is slowing down permit processes

4. Dealing with governmental regulations

5. Swings in direction of local governing body

6. Ever changing HR laws

7. Dealing with financial and administrative headaches of increase federal regulation

Financing Issues

1. Holding onto cash and freezing new projects

2. Devaluation of foreign currency

3. Lack of funding and access to capital

Poor Local and National Economy

1. Economic conditions of the country

2. Potential second housing bubble

3. Fed interest rate policy

4. Low interest rate environment

5. Broad economic growth

6. Material shortages

Pricing Competition

1. Competing with lower cost imports

2. Increased pressure to lower prices

3. Competition willing to “lower the bar” by inadequate fees and free labor

4. Heavy international competitive pressure

5. Increase competition

Politics

1. Concerned that we are going towards a socialist government

2. Concerned about political and taxation activism

3. Uncertainty of upcoming election