liquids rich montney - blackswanenergy.com · 4. financial performance • demonstrated material...

TRANSCRIPT

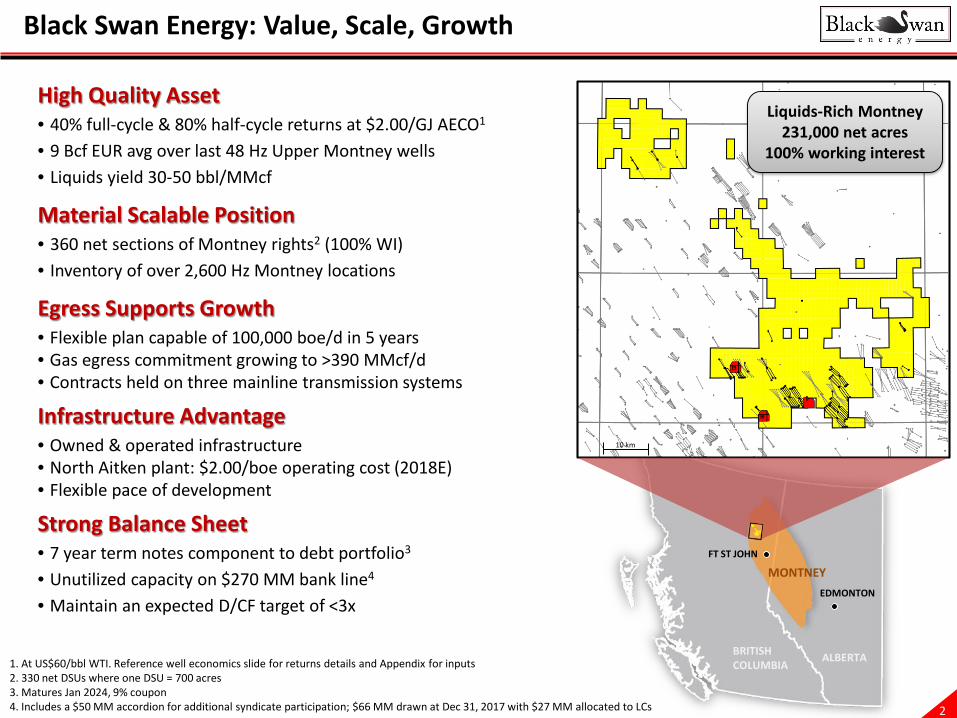

Liquids Rich Montney Value | Scale | Growth

March 2018

2

FT ST JOHN

EDMONTON

MONTNEY

BRITISH COLUMBIA

ALBERTA

10 km

Liquids-Rich Montney 231,000 net acres

100% working interest

Black Swan Energy: Value, Scale, Growth

High Quality Asset• 40% full-cycle & 80% half-cycle returns at $2.00/GJ AECO1

• 9 Bcf EUR avg over last 48 Hz Upper Montney wells • Liquids yield 30-50 bbl/MMcf

Material Scalable Position• 360 net sections of Montney rights2 (100% WI)• Inventory of over 2,600 Hz Montney locations

Egress Supports Growth• Flexible plan capable of 100,000 boe/d in 5 years• Gas egress commitment growing to >390 MMcf/d• Contracts held on three mainline transmission systems

Infrastructure Advantage• Owned & operated infrastructure• North Aitken plant: $2.00/boe operating cost (2018E)• Flexible pace of development

Strong Balance Sheet• 7 year term notes component to debt portfolio3

• Unutilized capacity on $270 MM bank line4

• Maintain an expected D/CF target of <3x

1. At US$60/bbl WTI. Reference well economics slide for returns details and Appendix for inputs2. 330 net DSUs where one DSU = 700 acres 3. Matures Jan 2024, 9% coupon4. Includes a $50 MM accordion for additional syndicate participation; $66 MM drawn at Dec 31, 2017 with $27 MM allocated to LCs

3

-

4,000

8,000

12,000

16,000

20,000

24,000

28,000

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2013 2014 2015 2016 2017 2018E

Avg.

Dai

ly P

rodu

ctio

n (b

oe/d

)Building Momentum Exiting 2017

1. Based on field estimates2. Evaluated by GLJ Petroleum Consultants3. Capital costs include the cost of the North Aitken Creek Gas Plant & land &

changes in Future Development Capital (FDC)

Production Growth

Delineation

- 50

100 150 200 250 300 350 400 450 500

2012 2013 2014 2015 2016

Rese

rves

(MM

boe)

PDP PDNP + PUD Probable

Reserve Growth

Development

Corporate Production• Dec 2016: 16,650 boe/d (16% liquids)• Dec 2017: 27,000 boe/d (20% liquids)1

Reserves Growth2

• 2016 YE: 2P 478 MMboe; 1P 171 MMboe• 2016 FD&A (incl. FDC)3:

• PDP $5.86 | 1P $7.63 | 2P $5.78

78% CAGR Q4 2014-2017(achieved with less than one rig annually)

Significant reserves based on large delineated area of development

4

Financial Performance

• Demonstrated material cost savings per unit with execution of growth plan

• Transportation costs increase reflects increased Alliance capacity

Reducing Cash Costs

• Q4/17 delivered record cash flow of $27 MM and net earnings of $8.1 MM1

• Asset performance delivering production growth

• Cash flow margins protected by:• Infrastructure ownership strategy• Disciplined spending and cost controls

• Significant liquids contribution to revenues

Growing Cash Flow

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017

$/bo

e

Controllable Cash Costs (corporate)

Opex Transportation G&A Financing

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$0

$5

$10

$15

$20

$25

$30

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017

AECO

(C$/

GJ)

Cash

Flo

w

Cash Flow vs. Commodity Prices

Cash Flow ($MM) Cash Flow Netback ($/boe) AECO Natural Gas (C$/GJ)

1. Excludes unrealized hedging gains of $7.9MM

5

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

$1.00/GJ Stn 2$55/bbl WTI

$1.50/GJ Stn 2$60/bbl WTI

$2.00/GJ Stn 2$65/bbl WTI

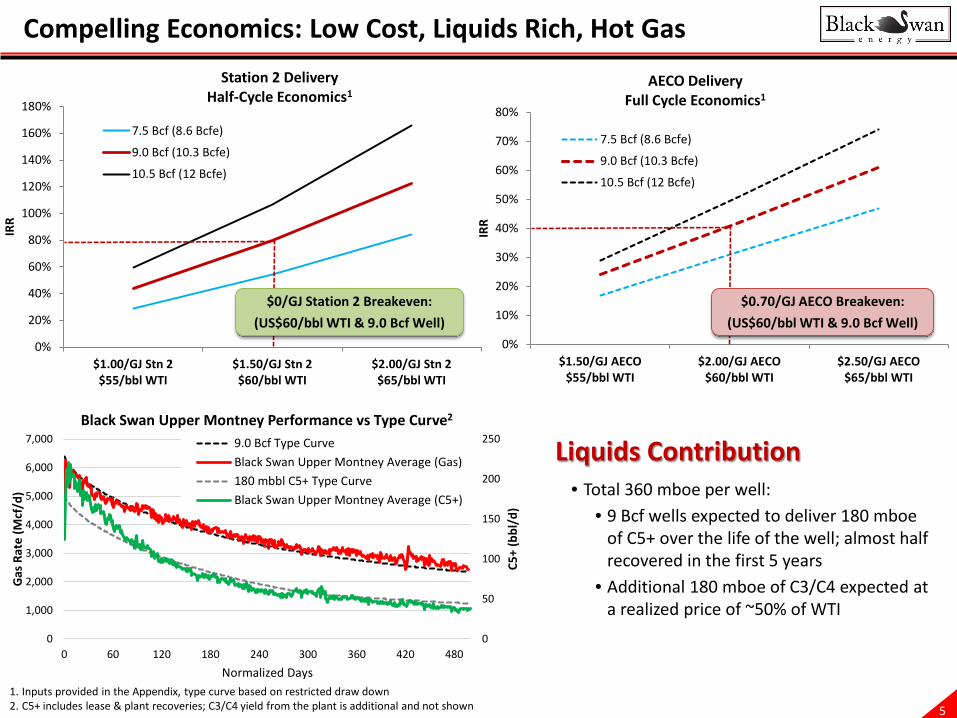

IRR

Station 2 DeliveryHalf-Cycle Economics1

7.5 Bcf (8.6 Bcfe)

9.0 Bcf (10.3 Bcfe)

10.5 Bcf (12 Bcfe)

0

50

100

150

200

250

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0 60 120 180 240 300 360 420 480

C5+

(bbl

/d)

Gas

Rat

e (M

cf/d

)

Normalized Days

Black Swan Upper Montney Performance vs Type Curve2

9.0 Bcf Type CurveBlack Swan Upper Montney Average (Gas)180 mbbl C5+ Type CurveBlack Swan Upper Montney Average (C5+)

Compelling Economics: Low Cost, Liquids Rich, Hot Gas

1. Inputs provided in the Appendix, type curve based on restricted draw down2. C5+ includes lease & plant recoveries; C3/C4 yield from the plant is additional and not shown

Liquids Contribution• Total 360 mboe per well:

• 9 Bcf wells expected to deliver 180 mboe of C5+ over the life of the well; almost half recovered in the first 5 years

• Additional 180 mboe of C3/C4 expected at a realized price of ~50% of WTI

0%

10%

20%

30%

40%

50%

60%

70%

80%

$1.50/GJ AECO$55/bbl WTI

$2.00/GJ AECO$60/bbl WTI

$2.50/GJ AECO$65/bbl WTI

IRR

AECO DeliveryFull Cycle Economics1

7.5 Bcf (8.6 Bcfe)

9.0 Bcf (10.3 Bcfe)

10.5 Bcf (12 Bcfe)

$0/GJ Station 2 Breakeven:(US$60/bbl WTI & 9.0 Bcf Well)

$0.70/GJ AECO Breakeven:(US$60/bbl WTI & 9.0 Bcf Well)

6

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

2014 2015 2016 2017 2018E

D&C

Cost

s ($M

M/w

ell)

Drilling Cost Completion Cost Design Evolution

Repeatable Well Deliverability at Low Cost

Decreasing Costs on Multi-well Pads

$4.5 MM2

$6.4 MM

$4.6 MM

$3.8 MM

0.0

2.0

4.0

6.0

8.0

10.0

12.0

EUR

(Bcf

/wel

l)

Upper Montney Wells (by completion date)

EUR (on-stream) Average EUR

2012/13 2014 2015 2016 2017

Evolving Wellbore Design• 2017: tested increased well length, proppant

loading, stage count and inter-well spacing• 2018 wellbore design range3:

• Base design (pads): $4.0MM and 9 Bcf• Aggressive design: up to $4.8MM and

>9 Bcf (pending evaluation of ‘17 program)

1. Well results are not normalized for completions2. Includes $0.4 MM for cost of testing design changes3. Base design includes 1,800 m lateral, 30 stages, 60 T/ frac. Average well

cost excludes land retention wells

Ongoing Operational Success• Avg EUR: 9.0 Bcf since 2012 (48 wells)1

• Repeatable and predictable outcomes

Driving Lower Costs• Continuous rig program• Ongoing optimization• Pad drilling• Frac water infrastructure • Timing of completions

$4.0-$4.8 MM3

7

Owned & Operated Infrastructure: Flexible Pace of Growth

North Aitken CreekGas Plant

110 MMcf/d capacity

10” sales gas line; connects to Enbridge T-North system

50 MMcf/d compression & dehy, volumes

flow to McMahon for processing

6”6”

6”

10”

10”

Gathering trunk-lines built H1/16

10”

8”

10 km

Existing gathering trunk-lines

110 MMcf/d North Aitken Creek (Plant 1)

Future site for 198 MMcf/d facility (Plant 2)

• 41 km raw gas gathering lines to North Aitken plant & Black Swan compressors

• 22 km sour gas lines to 3rd party facilities

• 14 km sweet sales gas lines (Enbridge T-North & Alliance)

1. Full capacity reached Nov 20172. Pending FID on Plant 2

Plant 1: 110 MMcf/d •50 MMcf/d (Q1 2016) + 60 MMcf/d (Q2 2017)1

•Liquids recoveries capable of ~40 bbl/MMcf (>50% C5+)

Plant 2: 198 MMcf/d •Engineering in progress with long lead equipment

included in ‘17 budget•Phase A on-stream timing to match pipeline expansions

Infrastructure Investment At 2017 YE: $312 MM

2018 Budget: $90 MM2

8

0

5

10

15

20

25

30

35

40

45

50

Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18

Liqu

ids Y

ield

(bbl

/MM

cf R

aw)

C5 Yield (bbl/MMcf Raw) C3/C4 Yield (bbl/MMcf Raw)

0

20

40

60

80

100

120

Jan/16 May/16 Sep/16 Jan/17 May/17 Sep/17 Jan/18

Gas

Pro

duct

ion

(MM

cf/d

)

Inlet Gas (MMcf/d) Inlet Capacity (MMcf/d)

Expanded Capacity

Owned & Operated Infrastructure: Lower Costs & Higher Netbacks

Final compressor commissionedPlant at capacity of 110 MMcf/d

Stable Liquids: ~45 bbl/MMcf

$10.03

$7.33

$2.31

$2.10

$3.00 $0.89

$0.00$2.00$4.00$6.00$8.00

$10.00$12.00$14.00$16.00$18.00$20.00

Costs Revenues

$/bo

e

RoyaltyTransportationOperating CostC3/C4 RevenueC5+ RevenueGas Revenue

Higher Revenues & Lower Costs

2017 Field Netback1

$13.86/boe

Top Tier 2018E Operating Costs

1. Unaudited: Average price of $2.04/GJ, -$0.56/GJ Station 2 to AECO differential, US$50.93/bbl WTI and $1.30 C$/US$, excludes hedging gains/(losses)

Source: National Bank Financial and Black Swan

98.6% run time prior to turnaround for expansion

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

Peer

1

Peer

2

BSE

Plan

t

BSE

Peer

3

Peer

4

Peer

5

Peer

6

Peer

7

Peer

8

Peer

9

Peer

10

$/bo

e

9

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17 Jan-18 Apr-18 Jul-18 Oct-18

Daily

Pro

duct

ion

(boe

/d)

Black Swan Production

Actuals (Gas) Actuals (Liquids) Base Decline Completed Awaiting Capacity 2018 Completions

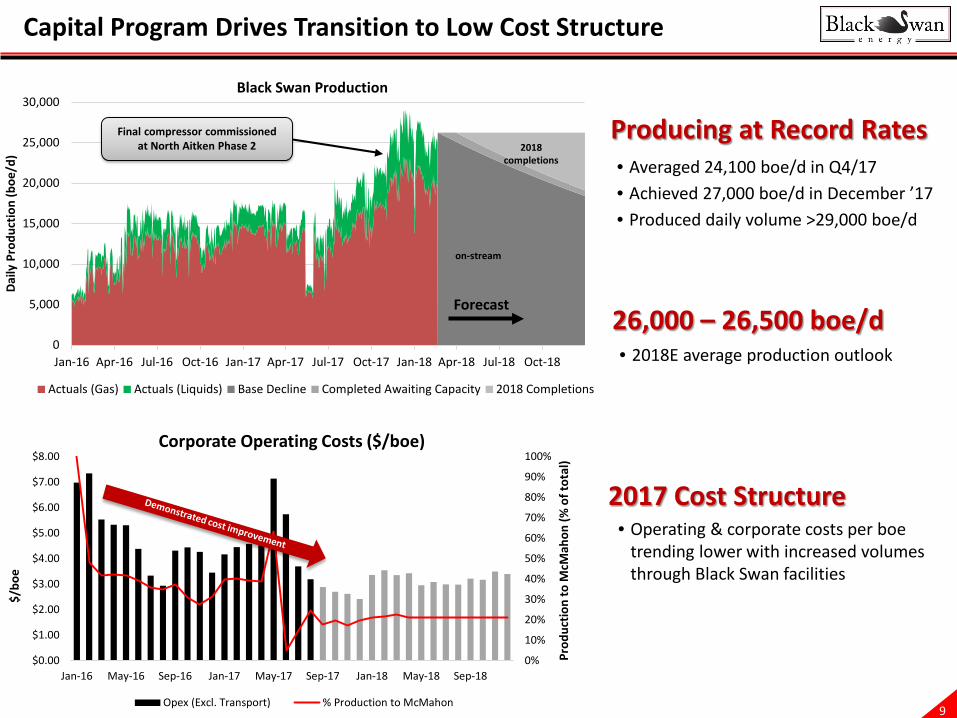

Capital Program Drives Transition to Low Cost Structure

26,000 – 26,500 boe/d• 2018E average production outlook

Producing at Record Rates• Averaged 24,100 boe/d in Q4/17• Achieved 27,000 boe/d in December ’17• Produced daily volume >29,000 boe/d

2017 Cost Structure• Operating & corporate costs per boe

trending lower with increased volumes through Black Swan facilities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

Jan-16 May-16 Sep-16 Jan-17 May-17 Sep-17 Jan-18 May-18 Sep-18

Prod

uctio

n to

McM

ahon

(% o

f tot

al)

$/bo

e

Corporate Operating Costs ($/boe)

Opex (Excl. Transport) % Production to McMahon

on-stream

Final compressor commissioned at North Aitken Phase 2 2018

completions

Forecast

10

$10.37

$6.82

$1.80 $0.16 $2.79

$3.73 $3.00 $1.44 $0.89 $2.02

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

Costs Revenues

2017E

$/bo

e

2017E Revenues vs. Costs

Interest

Royalty

G&A

Transportation

Operating Cost

Hedging

Processing Income

C3/C4 Revenue

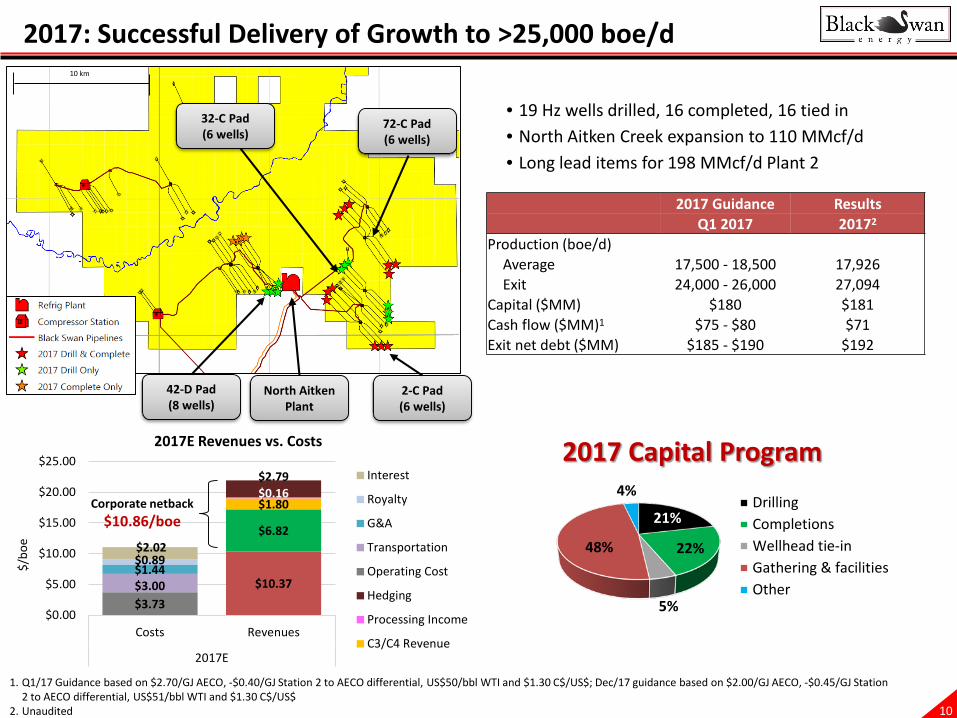

2017: Successful Delivery of Growth to >25,000 boe/d

42-D Pad(8 wells)

2-C Pad(6 wells)

72-C Pad(6 wells)

North Aitken Plant

10 km

21%

22%

5%

48%

4%

2017 Capital Program

DrillingCompletionsWellhead tie-inGathering & facilitiesOther

• 19 Hz wells drilled, 16 completed, 16 tied in• North Aitken Creek expansion to 110 MMcf/d• Long lead items for 198 MMcf/d Plant 2

1. Q1/17 Guidance based on $2.70/GJ AECO, -$0.40/GJ Station 2 to AECO differential, US$50/bbl WTI and $1.30 C$/US$; Dec/17 guidance based on $2.00/GJ AECO, -$0.45/GJ Station 2 to AECO differential, US$51/bbl WTI and $1.30 C$/US$

2. Unaudited

32-C Pad(6 wells)

Corporate netback $10.86/boe

2017 Guidance ResultsQ1 2017 20172

Production (boe/d)Average 17,500 - 18,500 17,926Exit 24,000 - 26,000 27,094

Capital ($MM) $180 $181Cash flow ($MM)1 $75 - $80 $71Exit net debt ($MM) $185 - $190 $192

11

Stable Base Production: Minimal Maintenance Capital Required

1. Notes:• Assumes 35% base decline; $6,000/boe/d rig efficiency, $5MM/year miscellaneous field capital• Prior to hedging gains/losses; Assumes $0.50/GJ Station 2 Differential • The ratio between maintenance capital and free cash flow will remain the same as productions grows

2. At $2.00/GJ AECO & $60/bbl WTI and $1.30 C$/US$ FX

<60% of Cash FlowRequired to maintain production2

Free cash flow positive & able to maintain production at low prices

Strong Asset Base Fundamentals:<$3/boe F&D cost

<$6,000/boe/d capital efficiency

Avg 9 Bcf over last 48 Upper Montney wells drilled

$0

$20

$40

$60

$80

$100

$120

$140

$160

$1.5/GJ AECO $2/GJ AECO $2.5/GJ AECO

US $55/bbl WTI US $60/bbl WTI US $65/bbl WTI

$MM

Free Cash Flow Generation at 26,000 boe/d1

Maintenance Capital Free Cash Flow Total Cash Flow

12

Connected to Multiple Markets

McMahon Gas Plant

Sunset

T-South to Huntington/Sumas

Station 2

Aitken Creek Gas Storage

NGTL to AECO

North Aitken Gas Plant

BRIT

ISH

COLU

MBI

AAL

BERT

A

25 km

1. NGTL is part of the TransCanada pipeline system2. North Montney Mainline subject to regulatory approval

• Egress on all three Canadian gas transmission systems2

• Connection to different markets enables netback optimization

• Option to accelerate production growth based on market conditions

Egress Via 3 Major Gas PipelinesLong term >2/3 of egress on TCPL with access to

AECO and beyond

13

0

50

100

150

200

250

300

350

400

450

Jan

Mar

May Ju

l

Sep

Nov Ja

n

Mar

May Ju

l

Sep

Nov Ja

n

Mar

May Ju

l

Sep

Nov Ja

n

Mar

May Ju

l

Sep

Nov

2018E 2019E 2020E 2021E

Gas

(MM

cf/d

)

Planned Plant Capacity vs. Egress Commitments

Egress Commitments Provide Transformational Growth

1. Unutilized tolls: $0.8 MM/month post Plant 2A; $0.4MM/month post Plant 2B; $1.8 MM/month with no new processing capacity

Existing Processing

Plant 2A

Plant 2B

Alliance Capacity

Enbridge Capacity

TransCanada Expansion

Option to accelerate1

Owned & operated

• New processing units built in 100 MMcf/d (19,000 boe/d) increments

• Plant construction timed to align with pipeline expansion

Egress grows to >390 MMcf/d

• Option to flow up to 100% on TCPL by 2019• Long term >2/3 of egress on TCPL with

access to AECO and beyond• Connection to different markets enables

netback optimization• Option to accelerate production growth

based on market conditions

Market & Growth Optionality

Enbridge Expansion

Spruce Ridge ProjectBlack Swan:60 MMcf/dEst. Q3/19

North Montney MainlineBlack Swan:229 MMcf/dEst. Q2/19

Existing Pipelines

14

$10.58

$6.26

$1.72 $0.10 $1.43

$3.24 $2.25 $1.11 $0.97 $1.59

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

Costs Revenues

2018E

$/bo

e

2018E Revenues vs. CostsInterest

Royalty

G&A

Transportation

Operating Cost

Hedging

Processing Income

C3/C4 Revenue

C5+ Revenue

Gas Revenue

2018: Maintaining Low Cost Production Ahead of 2019 Ramp Up

• Maintenance capital: • Wells: $56MM (5 Hz drills, 15 completions, 15 tied-in)• Gathering & Misc: $6MM

• Growth capital: • Land retention wells: $7MM (2 Hz, 1 Vt; drill only)• Plant 2 long lead: $33MM• Wells: $36MM (18 Hz drills)1

• Plant 2 construction: $49MM1

1. Pending FID on Plant 22. Based on annual pricing of $1.80/GJ AECO, -$0.40/GJ Station 2 to AECO differential, US$55/bbl WTI and $1.27 C$/US$

Netback$9.85/boe

2018 Guidance2

Production (boe/d)Average 26,000 – 26,500Exit 26,000 – 26,500

Capital ($MM) $190Cash flow ($MM)1 $90 - $95Exit Net Debt ($MM) $290 - $295

32-C Pad Complete

19-EDrill & Complete

42-D Pad Complete

Ramp Up Ahead of North Plant 2

Production Maintenance Activity

88-C PadDrill

Plant 2c-46-C

52-C Pad Drill

56-C Pad Drill

5 km

Scalable 2018 Capital Program44-C Pad Drill & Complete

15

Aitken Area Capable of Delivering & Sustaining >100,000 boe/d

10 km

Aitken Core Development Area

Development Plan1 Uses <20% of Inventory• Upper Montney delineated across the Aitken core

development area; 430 Hz locations remaining

• Remaining acreage & landing zones have potential to• Increase peak production, or• Extend production plateau

Aitken core development delineated; upside on

northern acreage

1. Drilling plans are subject to annual review and may be modified based on factors including: commodity prices, facility access and regulatory constraints

2. Assumes min 25 wells/rig/year; based on IP 365 of 765 boe/d (half-cycle 9.0 Bcf EUR type curve, $4.5 MM DCET)

92-C/72-C padEUR = 9 Bcf

54-D/42-D padAvg EUR = 9 Bcf

22-C/2-C padAvg EUR = 11 Bcf

19-E padAvg. EUR = 9 Bcf

7-H padAvg EUR = 7 Bcf

45-D wellEUR = 11 Bcf

Capital Efficient Asset Provides Robust Growth• Single continuous one rig program drills ~25 wells per

year• Add 19,000 boe/d/rig annually2

• F&D cost<$3.00/boe• Capital efficiency <$6,000/boe/d• Delivers 100,000 boe/d in 5 yrs with 2 rigs

16

Source Water Secured for Long-Term Development Plan

• Underpins growth to 100,000 boe/d • Permanent intake and storage in place• Water license for up to 100+ Hz wells per year

through Dec. 31, 20211

Water pump station1. With renewal provisions

Black Swan has re-used 100% of produced water since June 2014

Water License Intake 1

10 km

Water Pump Station

b-54-D65,800 m³

c-7-H60,300 m³

b-11-A44,900 m³

d-42-D65,000 m³

a-72-C68,000 m³

c-38-C56,000 m³

Responsible management & recycling • >2.2 MMbbl of fresh water storage capacity

constructed• Produced water is recovered & recycled• Temporary handling infrastructure allows

flexibility of operation + optimization of capital

Water License

17

0

500

1,000

1,500

2,000

2,500

2018 2019

Hedg

ed V

olum

es (b

bl/d

)

C4 & C5+ Avg. Contract Pricing

Swaps (C$ WTI) Collars (C$ WTI)

Puts (C$ WTI)

Risk Management: Ability to Hedge up to 3 Years Out

Note: Gas pricing portfolio percentages include physical contracts. Put prices are shown net of premiums and Chicago prices are shown prior to transportation costs on Alliance; 2018 NYMEX puts & 2019 NYMEX collars are matched with C$-2.15/MMBtu and C$-1.82/MMBtu AECO basis swaps respectively

0

20,000

40,000

60,000

80,000

100,000

2018 2019

Hedg

ed V

olum

es (G

J/d)

Natural Gas Avg. Contract Pricing

Station 2 Diff ($/GJ) AECO Swaps ($/GJ)AECO Puts ($/GJ) Chicago Swaps (C$/MMBtu)NYMEX Puts (C$/MMBtu) NYMEX Collars (C$/MMBtu)

0

100

200

300

400

500

600

700

2018 2019

Hedg

ed V

olum

es (b

bl/d

)

Propane Avg. Contract Pricing

Swaps (C$ Conway)

Gas Pricing Portfolio C4 & C5+ Hedging$2

.34

-$0.

49

$1.7

9 -$0.

39$1

.84

$55.

00 x

$67

.25

Propane Hedging

$55.

00 x

$68

.00

$68.

30

$4.6

2 $3.2

6

$69.

83

$39.

26

$34.

37

$66.

50

$3.3

3 x

$3.6

3

$66.

35

63%

19%

4%

30%

14%

3%

67%

0%

20%

40%

60%

80%

100%

2018 2019% o

f Net

Cor

pora

te P

rodu

ctio

n

Hedged Floating ChicagoFloating AECO Floating Station 2

82%

42%

18%

58%

0%

20%

40%

60%

80%

100%

2018 2019% o

f Net

Cor

pora

te P

rodu

ctio

nHedged Unhedged

76%

37%

24%

63%

0%

20%

40%

60%

80%

100%

2018 2019

% o

f Net

Cor

pora

te P

rodu

ctio

n

Hedged Unhedged

18

0%10%20%30%40%50%60%70%80%90%

100%

$0

$2

$4

$6

$8

$10

$12

$14

$0

$2

$4

$6

$8

$10

$12

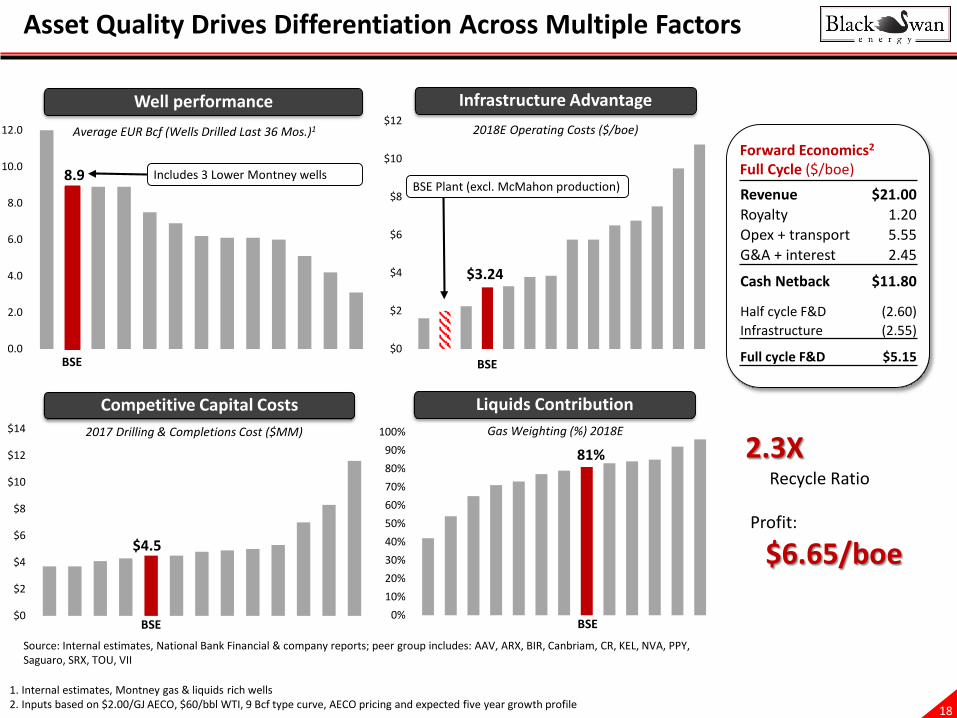

Asset Quality Drives Differentiation Across Multiple Factors

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Well performance

Revenue $21.00Royalty 1.20Opex + transport 5.55G&A + interest 2.45

Cash Netback $11.80

Half cycle F&D (2.60)Infrastructure (2.55)

Full cycle F&D $5.15

1. Internal estimates, Montney gas & liquids rich wells 2. Inputs based on $2.00/GJ AECO, $60/bbl WTI, 9 Bcf type curve, AECO pricing and expected five year growth profile

8.9

$4.5

$3.24

81%

Source: Internal estimates, National Bank Financial & company reports; peer group includes: AAV, ARX, BIR, Canbriam, CR, KEL, NVA, PPY, Saguaro, SRX, TOU, VII

Includes 3 Lower Montney wellsBSE Plant (excl. McMahon production)

Average EUR Bcf (Wells Drilled Last 36 Mos.)1

Infrastructure Advantage2018E Operating Costs ($/boe)

2017 Drilling & Completions Cost ($MM)

Competitive Capital Costs Liquids ContributionGas Weighting (%) 2018E

Forward Economics2

Full Cycle ($/boe)

$6.65/boeProfit:

2.3XRecycle Ratio

BSE BSE

BSE BSE

19

Appendix

Liquids Rich Montney Value | Scale | Growth

20

Black Swan Energy Executive Team

David Maddison, P.Eng.David is President, CEO and founder of Black Swan Energy. He has over 37 years of industry experience focused on conventional and resource plays in Western Canada. Prior to Black Swan, he was with Talisman Energy where he managed multi-disciplinary teams in the WCSB, with production of 100,000 boe/d and annual capital budgets of $1 billion.

Marc Mereau, P.Eng.Marc is Chief Operating Officer and a co-founder of Black Swan Energy. He has over 36 years of experience in the oil and gas industry, both domestically and internationally. Prior to Black Swan, Marc worked at Talisman Energy, where he held progressively larger roles including Senior Vice President of Western Operations for North America.

Michael Wilhelm, B.Comm., CPA, CGAMike is Vice President, Finance and CFO and a co-founder of Black Swan Energy. He has over 30 years experience in the oil and gas industry, with an extensive background in both private and public financings in Canadian and U.S. markets. Mike was involved as a founder and in the ongoing funding of Equatorial Energy and Espoir Exploration. He was also involved with the IPO of Resolute Energy Inc. through the RTO of Equatorial Energy Inc.

Bruce Thornhill, P.GeoBruce is Vice President, Exploration of Black Swan Energy. He has over 35 years of experience in the energy industry focused on conventional and resource play exploration and development throughout Western Canada, primarily in Deep Basin areas. Prior to joining Black Swan, he was a member of the senior management team at TAQA North, first as VP of Exploration and later as VP of the North Asset managing an annual capital budget of $200MM.

Bryan Lang, P.Eng.Bryan is Vice President, Operations of Black Swan Energy. He has over 27 years of experience in the energy industry focused on Western Canadian operations. He started his career at Chevron Canada and at growth oriented operators Northrock Resources and Peyto Exploration. He played a lead role in the development of horizontal multistage resource plays, and has assembled highly efficient teams focused on safe, low cost operations.

Leanne Juneau, B.Comm.Leanne is Vice President, Land and co-founder of Black Swan Energy. She has over 20 years experience negotiating and executing exploration and development agreements and strategic corporate and asset acquisitions and dispositions within Western Canada totaling over $500 million. She has previously held positions at Redcliffe Exploration, Talisman Energy and Northrock Resources.

Diane Shirra, B.Eng., MBA, P.Eng.Diane is Vice President, Business Development of Black Swan Energy. She has over 33 years of experience in the energy industry focused on exploitation and development of both conventional and resource plays throughout Western Canada. Most recently she was VP Montney Gas Development and VP Reserves and Strategic Projects at Pengrowth Energy Corporation.

Christine Ezinga, B.Comm., CFAChristine is Vice President of Strategy & Planning at Black Swan Energy. She has over 16 years of diverse capital markets experience in finance, investor relations and corporate development with direct involvement in over $9 billion of executed M&A deals. Prior to joining Black Swan, she was Team Lead – Finance, Business Development at Sinopec Canada, following the successful sale of Daylight Energy to Sinopec. Christine currently serves on the Board of the Petroleum Acquisition and Divestiture Association.

21

Black Swan Energy Board of Directors

David Maddison, P.Eng.David is President, CEO and founder of Black Swan Energy. He has over 37 years of industry experience focused on conventional and resource plays in Western Canada. Prior to Black Swan, he was with Talisman Energy where he managed multi-disciplinary teams in the WCSB, with production of 100,000 boe/d and annual capital budgets of $1 billion.

Jackie Sheppard, Lead DirectorJackie was the Executive Vice-President, Corporate and Legal and Corporate Secretary for Talisman Energy Inc. She served as Secretary to the Board responsible for Corporate Projects and Acquisitions, Communications and Investor Relations. She currently serves on the Boards of Cairn Energy, Emera Inc. and Seven Generations.

Dr. James BuckeeIn September 1991 Jim was appointed President and Chief Operating Officer for BP Canada Inc. and in May 1993 he was appointed President and Chief Executive Officer of Talisman Energy Inc. (formerly BP Canada). When Jim retired, in October 2007, Talisman was producing over 500,000 boe/d. He also serves on the boards of Magma Global and M-Flow and sits on the advisory Board of Azimuth Capital Management. Jim holds a BSc Honours in Physics from the University of Western Australia and in 1970 he received his PhD in Astrophysics at Oxford University.

Evan Hazell, P. Eng. MBA Evan has been involved in the global oil and gas industry for over 30 years, both as a petroleum engineer and as an investment banker. At present, he serves as a Director of non-profit and community organizations Opera America, Calgary Municipal Land Corporation and Calgary YMCA. From 1998 to 2011, Mr. Hazell acted as a managing director at several financial institutions including HSBC Global Investment Bank and RBC Capital Markets. Mr. Hazell holds a Bachelor of Applied Science degree from Queen's University, a Master of Engineering degree from the University of Calgary, and an MBA degree from the University of Michigan.

Robert MellemaRobert has been with the Canada Pension Plan Investment Board (CPPIB) since 2008 and focuses on Natural Resources investments. Prior to joining CPPIB, Mr. Mellema worked at UBS on the Canadian M & A team. Mr. Mellema serves as a Director on the boards of Livingston International Inc. and Wolf Midstream and has previously been involved in CPPIB’s investments in Teine Energy and Seven Generations Energy. Mr. Mellema holds a MBA from the Wharton School at the University of Pennsylvania and a Bachelor of Commerce degree from Queen’s University.

David B. Krieger, MBA David is a member of the Warburg Pincus Executive Management team, having joined Warburg in 2000, and focuses on energy investments. Previously, he worked at McKinsey & Company. Mr. Krieger is a Director of Kosmos Energy, MainSail Energy, MEG Energy, Osum Oil Sands, Rubicon Oilfield International, Sheridan Production, Trident Energy and Velvet Energy. Mr. Krieger received a B.S. in economics summa cum laude from the Wharton, an M.S. with high honors from the Georgia Institute of Technology and an MBA with distinction from Harvard Business School.

Roy Ben-Dor, MBARoy joined Warburg Pincus in 2011 and previously worked at McKinsey & Company in New York. He is also a director of MainSail Energy and Zenith Energy and works with MEG Energy, Navitas Midstream and Osum Oil Sands. He received his BA cum laude in psychology and economics with Distinction from Duke University, a J.D. magna cum laude from Harvard Law School and a MBA with high distinction from Harvard Business School.

Dave PearceDave is Deputy Managing Partner with Azimuth Capital Management. During his 36 years in the energy sector, Mr. Pearce has worked in a variety of technical and executive roles in Exploration, Production and Corporate Development as well as an Independent Director in Canada and internationally. Mr. Pearce was President and CEO of Northrock Resources, an intermediate Canadian E&P company. Currently, Mr. Pearce is also a Director of TimberRock Energy, Altex Energy Ltd., Kaisen Energy, Kaden Energy, Entrada Resources and Raging River Exploration.

Jim NieuwenburgJim is an Operating Partner at Azimuth Capital Management. He has over 35 years of experience in the energy sector and over 20 years of executive management and corporate governance experience. Previously, he has held positions at Petromet Resources (CEO), Norcen Energy (Vice President) and Amoco Canada. Jim also serves as a Director on the boards of Corex Resources, Monolith Materials, Recovery Energy Services and Rifco Inc.

22

Historical Financial Summary

1. Unaudited, subject to Board approval2. NOI as presented does not include realized hedging gains/(losses)

20171 2017 2016 2016 2015 2015Full Year Q41 Q3 Q2 Q1 Full Year Q4 Q3 Q2 Q1 Full Year Q4 Q3 Q2 Q1

ProductionOil (bbl/d) - - - - - 16 - - - 65 79 54 64 82 116Gas (mcf/d) 88,559 116,138 85,769 66,194 85,832 67,151 74,626 75,484 71,376 46,944 23,538 26,513 24,318 19,431 23,853NGL (bbl/d) 3,166 4,838 3,501 1,868 2,427 2,099 2,254 2,506 2,399 1,232 614 875 539 519 521Total (boe/d) 17,926 24,194 17,796 12,900 16,732 13,307 14,692 15,087 14,295 9,121 4,616 5,348 4,656 3,840 4,612

Financial ($ 000)Net Operating Income2 74,435 23,425 14,130 14,241 22,639 50,484 20,154 16,506 10,188 3,636 13,098 3,082 3,272 3,945 2,799 EBITDA 84,282 30,855 19,631 13,074 20,722 47,513 15,529 16,104 11,452 4,428 6,819 1,571 1,559 2,558 1,131 Cash Flow 71,025 27,132 16,347 9,705 17,841 43,225 14,503 15,138 9,518 4,066 4,881 1,103 1,176 1,598 1,004 Capex (incl. A&D) 180,623 25,735 50,972 54,539 49,377 84,453 28,432 23,499 (2,209) 34,731 402,684 58,667 79,415 222,931 41,671

Capital Structure ($ 000)

Working Capital Deficit (Surplus) 4,688 4,688 23,176 23,916 (8,140) 11,507 11,255 5,875 612 16,981 46,854 46,854 41,707 (7,196) 32,116 Bank Debt 66,147 66,147 48,759 13,091 - 76,555 76,555 68,258 65,180 60,538 - - 555 50,000 25,000 Term Notes 121,322 132,275 121,078 125,645 128,867 - - - - - - - - - -Total Net Debt 192,157 203,110 193,013 162,916 120,727 88,062 87,810 74,133 65,792 77,519 46,854 46,854 41,262 42,804 57,116 Total Credit Facility 270,000 270,000 250,000 200,000 200,000 200,000 200,000 140,000 140,000 130,000 130,000 130,000 80,000 70,000 70,000

Netback Summary ($/boe)Net Revenue 18.99 17.13 15.49 22.13 23.07 17.97 22.65 18.83 14.97 13.60 18.82 16.26 18.19 21.77 20.02 Hedging Gain (Loss) 2.79 5.20 4.06 0.27 (0.20) 0.87 (1.28) 0.44 2.46 2.60 0.33 0.60 (0.04) 0.60 0.15 Royalties (0.89) (0.72) (0.65) (1.02) (1.26) (0.94) (1.44) (1.13) (0.46) (0.57) (0.99) (0.73) (0.76) (0.95) (1.57)Opex (3.73) (2.56) (3.25) (5.74) (4.39) (4.56) (4.01) (3.53) (4.49) (6.34) (9.07) (7.49) (9.24) (8.80) (10.99)Transportation (3.00) (3.32) (2.96) (3.23) (2.34) (2.10) (2.29) (2.28) (2.19) (2.31) (0.98) (1.77) (0.55) (0.73) (0.72)Operating Netback 14.16 15.73 12.69 12.40 14.83 11.24 13.63 12.34 10.29 6.98 8.11 6.87 7.60 11.89 6.89 General & Administrative (1.44) (2.00) (0.83) (1.45) (1.27) (1.76) (2.33) (1.12) (1.68) (2.01) (4.52) (5.28) (3.95) (4.57) (4.17)Processing Income 0.16 0.13 0.14 0.19 0.20 0.27 0.19 0.38 0.19 0.37 0.47 1.61 - - -Interest/Other Expense (2.02) (1.68) (2.02) (2.87) (1.91) (0.87) (0.74) (0.70) (1.48) (0.44) (1.16) (0.96) (0.90) (2.75) (0.30)

Cash Flow From Operations 10.86 12.18 9.98 8.27 11.85 8.88 10.73 10.91 7.32 4.90 2.90 2.24 2.75 4.57 2.42

23

Type Curve Assumptions

1. Station 2 Delivery: Economics assume volumes flow through existing Black Swan owned infrastructure (reflects half cycle) with tolls to Station 2 and a price differential of -$0.50/GJ relative to AECO

2. AECO Delivery: Economics assume volumes flow through new Black Swan owned infrastructure (reflects full cycle) with tolls to AECO on the NGTL system and gas realizations priced equal to AECO

3. FX rate of C$1.25/US$ applied to US$WTI prices4. Economics include equip & tie-in costs of $0.5 MM/well for total well costs of $4.5 MM5. Black Swan pays BC Crown royalties calculated on a sliding scale for gas based on price and production rate & fixed percentage of

revenue for liquids 6. Pricing relative to C$WTI: C5+: 91%, C4: 47%, C3: 33% at US$60/bbl oil (realizations include price offsets; trucking of $4.00/bbl included

in opex & transportation)7. Opex & transportation represent the average cost during the first 12-months

AssumptionsStation 2 Delivery

(reflects existing plant)AECO Delivery

(reflects new plant)D&C Cost ($MM, excl. $0.5 MM tie-in) $4.0 $4.0EUR (Bcf) 9.0 9.0

IP30 - Total (boe/d) 1,160 1,160Heat Content (MMBtu/mcf) 1,150 1,150Liquids Yield (bbl/MMcf) 40 40Price Differential to AECO ($/GJ) -$0.50 -Royalty Drilling Credit ($ MM) $1.05 $1.05 Opex & Transportation ($/boe) $3.95 $4.60 Full Cycle – Infrastructure ($/boe) - $1.34Full Cycle – G&A ($/boe) $0.90 $0.90

B-tax NPV ($MM) $7.0 $5.7B-tax IRR 79% 42%F&D ($/boe) $2.60 $3.95Payout (months) 14 24

24

Completions: Optimization of Design

4,600

5,600

6,600

7,600

2012 2013 2014 2015 2016 20171,400

1,600

1,800

2,000

2,200

2,400

2,600

feet

met

res

Completed Well Length

330

430

530

630

730

830

930

2012 2013 2014 2015 2016 20170.5

0.7

0.9

1.1

1.3

1.5

lbs/

ft

tonn

e/m

Proppant Concentration

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016 20170

20406080

100120140160180200220

feet

met

res

Stage Spacing

2017 Completion Design

Open hole ball drop• 2,200 m lateral, 34 stages, single port entry• 65 m port spacing• Proppant: 90 tonne/stage, 3,000 tonne/well, 1.33 tonne/m loading• 13,000 m3 recycled slickwater blend

Pad design modifications provide• Optimized landing interval for frac initiation, geometric completion design• Multiple wells with modified zipper frac• Complementary inter-well stage overlap with maximum interference between

wells/stages to enhance stimulated reservoir volume

Early move to short stages, optimizing well length and sand loading in development• 2012/13 – Perf-plug, long stage length, 8 stages x3 perfs/stage, 0.7 t/m• 2014/15 – Open hole, short stage length, 20 stages, 1.0 t/m• 2016/17 – Reduced stage length, increased lateral length, 33 stages,

1.33 t/m• From early development to current design, +33% increase in length, 70%

reduction in stage spacing and 80% increase in sand loading resulting in increasing EUR per well and high recovery factor

Completion Design Evolution

Optimizing Recovery Per DSU• Extended reach wells to reduce capital• Tighter stage spacing (65m vs 90m)• Increased sand intensity with wider inter-well spacing• Fluid additive technology, diversion techniques• Unlimited stage fracturing systems

25

Upper Montney Multi-Well Pad Production Summary

• Black Swan utilizes downhole chokes on all Hz wells for operational purposes

• Data presented is based on actual daily production which has been normalized to adjust for downtime

• Details collapsed for pads where all wells have >365 days of production history, averages represent the average of all Upper Montney wells on the pad

Note: Gas rates shown are raw

Internal UWI Completion Montney IP30 / well IP90 / well IP365 / wellCum to Dec/17 EUR

Reference (Year) Target (mcf/d) (mcf/d) (mcf/d) (Bcf) (Bcf)9 Bcf Type Curve (restricted) 5,900 5,300 3,900 9.072-C Well Pad (6 wells) 2017 Upper 6,438 NA NA 1.6 9.5a-72-C 200/b-059-B 094-H-04/00 2017 Upper 6,545 NA NA 0.3 10.0a-A72-C 200/a-060-B 094-H-04/00 2017 Upper 6,744 NA NA 0.3 10.5a-B72-C 200/d-050-B 094-H-04/00 2017 Upper 6,696 NA NA 0.3 10.0a-C72-C 200/c-093-C 094-H-04/00 2017 Upper 5,321 NA NA 0.2 8.5a-D72-C 200/a-094-C 094-H-04/00 2017 Upper 5,827 NA NA 0.2 8.0a-E72-C 200/c-084-C 094-H-04/00 2017 Upper 7,494 NA NA 0.4 10.042-D Well Pad (8 wells) 2017 Upper 5,373 5,018 NA 1.3 8.0d-42-D 200/a-073-D 094-H-04/00 2017 Upper 5,400 5,018 NA 0.5 8.0d-A42-D 200/b-073-D 094-H-04/00 2017 Upper 5,710 NA NA 0.2 8.0d-B42-D 200/c-063-D 094-H-04/00 2017 Upper 5,480 NA NA 0.4 8.0d-C42-D 200/d-064-D 094-H-04/00 2017 Upper 4,904 NA NA 0.3 8.0d-D42-D 200/d-040-C 094-H-04/02 2018 Upper NA NA NA NA NAd-E42-D 200/a-040-C 094-H-04/02 2018 Upper NA NA NA NA NAd-F42-D 200/b-040-C 094-H-04/02 2018 Upper NA NA NA NA NAd-G42-D 204/d-042-D 094-H-04/00 2018 Upper NA NA NA NA NA2-C Well Pad (6 wells) 2017 Upper 5,997 5,231 NA 4.6 9.4c-E2-C 200/a-091-K 094-A-13/00 2017 Upper 6,641 5,732 NA 0.9 9.5c-D2-C 200/b-100-J 094-A-13/00 2017 Upper 5,815 5,179 NA 0.9 9.0c-C2-C 200/a-100-J 094-A-13/00 2017 Upper 6,076 5,009 NA 0.5 9.0c-B2-C 200/c-025-C 094-H-04/00 2017 Upper 5,463 4,887 NA 0.6 9.5c-A2-C 200/b-035-C 094-H-04/00 2017 Upper 5,178 4,716 NA 0.8 9.5c-2-C 200/a-035-C 094-H-04/00 2017 Upper 6,810 5,862 NA 0.9 10.019-E Well Pad (3 wells) 2016 Upper 4,647 4,674 NA 4.9 9.2b-B19-E 200/b-097-D 094-H-04/00 2016 Upper 3,240 4,444 NA 1.0 9.0a-20-E 200/c-088-D 094-H-04/00 2016 Upper 5,000 4,448 NA 1.2 8.0b-19-E 200/b-098-D 094-H-04/02 2015 Upper 5,701 5,129 4,617 2.7 10.592-C Well Pad (6 wells) 2016 Upper 5,231 4,881 3,892 7.2 8.6a-B92-C 200/c-004-F 094-H-04/00 2016 Upper 5,917 5,577 NA 1.4 11.0a-A92-C 200/a-014-F 094-H-04/00 2016 Upper 6,126 5,614 NA 1.3 11.5a-E92-C 200/b-080-B 094-H-04/00 2016 Upper 4,847 4,309 NA 0.8 6.5a-D92-C 200/a-080-B 094-H-04/00 2016 Upper 4,833 4,317 3,184 1.2 6.5a-C92-C 200/d-080-B 094-H-04/00 2016 Upper 3,774 3,519 NA 0.8 6.0a-92-C 200/d-004-F 094-H-04/02 2013 Upper 5,886 5,951 4,599 1.7 10.022-C Well Pad (6 wells) 2015 Upper 6,786 6,327 4,857 13.2 10.154-D Well Pad (8 wells) 2015 Upper 5,016 4,770 3,766 15.4 8.67-H Well Pad (5 wells) 2014 Upper 6,850 4,645 3,372 8.8 7.3

26

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0 60 120 180 240 300 360 420 480 540 600

Pad Operations: Core Area Delineated with High Rate Pads

Upper Montney Pad Performance Tracking Type Curves

2-C

92-C

7-H

19-E

22-C54-D

10 km

Upper Montney Pad Wells

Aitken Core AreaPlot

Legend PadYear

CompletedWells/

Pad

AvgD&C

($MM)

Avg EUR(Bcf)

72-C 2017 6 4.7 10.3

42-D 2017 4 3.9 8.0

2-C 2017 6 4.9 9.4

19-E 2015/16 3 3.72 9.2

92-C 2016 6 3.9 8.6

22-C 2015 7 4.1 11.41

54-D 2015 8 4.6 8.6

7-H 2014 5 6.4 7.31

10.5 Bcf9.0 Bcf7.5 Bcf

Type Curves

Black Swan’s type curves reflect a restricted draw down

42-D

72-C

Normalized Days

Mcf/d

27

Key Western Canadian Pipelines & Market Hubs

NGTL

ENBRIDGE

ALLIANCE

NORTHERNBORDER

TCPL MAINLINE

GREAT LAKESIROQUOIS

VIKING

ROVER

NEXUS

FOOTHILLS

GTN

VECTOR

CHICAGO

DAWN

AECO

MALIN

SKAB

BC

MB

ONQC

WADDINGTONEMERSONSUMAS

STN 2

HENRY HUB

ROCKIES EXPRESS

NIAGRA

OPAL

RUBY

2

3

4

6

5

1

7

8

Infrastructure connects Black Swan to diverse existing and new markets• NEBC Montney is one of the most active natural gas development area

in western Canada • Western Canadian base production declines and new demand will be

predominantly supplied by the Montney• Existing infrastructure capable of delivering ~12 Bcf/d of gas beyond

western Canadian markets (to the US and eastern Canada)

Canadian LNG projects - potential access to offshore markets• Multiple export licenses issued by Canadian government• PETRONAS: PNW cancelled, reviewing other west coast LNG options• LNG Canada (Shell): FID delayed, owners remain supportive• Woodfibre LNG announced approval for funding to proceed Nov 4, 2016

Market2017 FutureBcf/d Bcf/d

1 Westcoast LNG 0 4.0+2 T-South 1.6 1.83 NGTL West Gate 2.1 2.84 Oil Sands 2.6 3.15 Alliance 1.6 2.16 Intra AB Market 3 3.47 Empress/McNeil 4.6 4.6+

28

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Eagl

e Fo

rd O

il - E

ast (

Top

Qua

rtile

)Bo

ne S

prin

g (T

op Q

uart

ile)

Wol

fcam

p/Sp

rabe

rry

N. M

idla

nd (T

op Q

uart

ile)

Wol

fcam

p - D

elaw

are

(Top

Qua

rtile

)N

orth

Dak

ota

Bakk

en (T

op Q

uart

ile)

Mon

tney

at K

akw

aN

orth

Dak

ota

Thre

e Fo

rks (

Top

Qua

rtile

)SK

Miss

issip

pian

Hz.

Mon

tney

at K

arr

Wol

fcam

p/Sp

rabe

rry

S. M

idla

nd (T

op Q

uart

ile)

Viki

ng H

z. D

odsla

ndCh

arlie

Lak

eM

ontn

ey a

t Ing

a/Fi

rew

eed

Eagl

e Fo

rd O

il - W

est (

Top

Qua

rtile

)Sh

auna

von

Hz.

Kayb

ob D

uver

nay

Top

30 W

ells

Bakk

en H

z. (<

1700

m)

Mon

tney

at B

eg -

Blac

k Sw

anCa

rdiu

m P

embi

na W

est

Mon

tney

at E

lmw

orth

/Wap

itiN

orth

Dak

ota

Bakk

enN

E M

arce

llus D

ryCa

rdiu

m W

illes

den

Gree

nVi

king

Hz.

Alb

erta

Mon

tney

at D

awso

n/Pa

rkla

ndBo

ne S

prin

gW

olfc

amp

- Del

awar

eST

ACK

Mer

amec

Eagl

e Fo

rd O

il - E

ast

Lloy

dmin

ster

Hz.

Wol

fcam

p/Sp

rabe

rry

N. M

idla

ndSW

Mar

cellu

s Liq

uids

Ric

hHa

ynes

ville

Sha

le -

LAEa

gle

Ford

Sha

le -

Gas-

Con

dens

ate

Mon

tney

at B

egM

ontn

ey a

t Gre

ater

Um

bach

STAC

K W

oodf

ord

Nor

th D

akot

a Th

ree

Fork

sM

ontn

ey A

nte

Cree

k Hz

.M

ontn

ey a

t Big

ston

eM

ontn

ey a

t Gla

cier

Glau

coni

te a

t Hoa

dley

Mon

tney

at P

ouce

Cou

peM

ontn

ey a

t Alta

res (

Liqu

ids R

ich)

Wilr

ich

at E

dson

Mon

tney

Tow

erSW

Mar

cellu

s Dry

Wol

fcam

p/Sp

rabe

rry

S. M

idla

ndHa

ynes

ville

Sha

le -

TXTo

rqua

y Fl

at L

ake

Wilr

ich

at R

esth

aven

/Kak

wa

Not

ikew

in S

unda

nce

Eagl

e Fo

rd O

il - W

est

Upp

er M

annv

ille

- Bra

zeau

Mon

tney

at G

roun

dbirc

hKa

ybob

Duv

erna

y Li

quid

s Ric

hM

ontn

ey a

t Tow

n (D

ry)

Eagl

e Fo

rd S

hale

- Dr

y G

as

Year

s

North American Oil and Natural Gas PlaysHalf-Cycle Payout Period

Benchmarking: Ranking Across Commodity

Source: Peters & Co. Limited February 2018, estimates based on US$60/bbl WTI and US$3.00/Mcf NYMEX (C$2.25/Mcf AECO) prices

Median Gas Plays 3.5 Years

Median Oil Plays 2.3 Years

29

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00M

ontn

ey -

Pou

ce C

oupe

Mon

tney

- T

ower

Mon

tney

- N

est

2M

ontn

ey -

Att

achi

eEa

gle

Ford

Wet

Tie

r 1

Mon

tney

- D

oeM

ontn

ey -

Ait

ken

Mon

tney

- D

awso

nM

ontn

ey -

Gun

dyN

E M

arce

llus

Dry

Tie

r 1

Mon

tney

- B

ilbo

Mon

tney

- S

unri

seAl

pine

Hig

hM

ontn

ey -

Sun

dow

nM

ontn

ey -

Gro

undb

irch

Mon

tney

- E

lmw

orth

SCO

OP

Woo

dfor

d W

et G

as /

Con

dyM

ontn

ey -

Gor

dond

ale

Mon

tney

- G

laci

erM

ontn

ey -

Tow

nsen

dM

ontn

ey -

Nes

t 1

Mon

tney

- B

lair

Mon

tney

- P

ouce

Cou

peSW

Mar

cellu

s D

ry T

ier

1Te

rryv

ille

/ N

LA

Mon

tney

- W

est

Sept

imus

Eagl

e Fo

rd D

ry G

as T

ier

1M

ontn

ey -

Par

klan

dN

E M

arce

llus

Dry

Tie

r 2

OH

Uti

ca D

ryH

ayne

svill

ePA

Uti

ca D

rySW

Mar

cellu

s D

ry T

ier

2M

arce

llus

Wet

Mon

tney

- G

old

Cree

k ga

sEa

gle

Ford

Wet

Tie

r 2

Mon

tney

- S

epti

mus

Barn

ett

Rich

Uti

ca W

etM

eram

ec W

et G

asPi

neda

leFa

yett

evill

e Co

re /

Moo

refi

eld

Pice

ance

Cana

Wet

Gas

Cana

Lea

n G

asSC

OO

P Sy

cam

ore

Wet

Gas

Uti

ca C

onde

nsat

e

Brea

keve

n H

Hub

Pri

ce (

$/m

cfe)

@ 3

0%

Montney GasMontney OilUS Play

Benchmarking - Key North American Plays

Source: TPH Research, February 2018Assumes: US$50/bbl WTI, US$ -0.95/MMBtu AECO basis, $0.79 USD/CAD for 30% Atax IRR

Relative North American Supply Costs

BSE

30

Substantial Resource to Unlock

Capable of sustaining 2 Bcf/d for 10 years• Gas-in-place supports long-term growth

• Average 250 Bcf/DSU OGIP• 83 Tcf of gas-in-place

• Over 2,600 Hz well inventory and 15 Tcfe of recoverable resource (two horizons only)

• Potential for development of four horizons

Aitken

Laprise/Sojer

Jedney

1. 4.5 wells/DSU/layer (300 m spacing), two layers developed, ranging from 5.0-9.0 Bcf/well, 90% land utilization2. 4.5 wells/DSU/layer (300 m spacing), four layers developed, ranging from 7.0-11.0 Bcf/well, 90% land utilization

Note: Based on management estimates, liquids converted at 1 bbl: 6 Mcf for gas equivalency, 40 bbl/MMcf liquids and 8% shrinkage

DSUs Base Case1 Upside Estimate2

#Hz Locations

#

Recoverable Resource

Tcfe

Hz Locations

#

Recoverable Resource

TcfeAitken 152 1,225 8.3 2,449 19.0

Laprise/Sojer 114 919 4.6 1,837 12.9

Jedney 64 516 2.6 1,031 7.2

Total 330 2,659 15.4 5,318 39

19% Recovery Factor 47% Recovery Factor

Internal Estimate of Resource

10 km

Legend

1

2

3

4

31

Growth Plan Supported by Low Cost Reserves

16%

25%

44%

2%

1%

12%

2016 Reserves: Value1

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

PPY AAV ARX BSE BIR CR PEY BNP TOU SRX NVA KEL VII

$/bo

e

Peer Comparison: 3 Year 2P FD&A (incl. FDC)

1. GLJ January 1, 2017 price forecast, includes 1P FDC $0.9 B and 2P FDC $2.4 B2. Natural gas volumes converted to barrels of oil equivalent at 6,000 cubic feet per barrel (6 mcf = 1 boe)

2016 PDP adds replaced 196% of annual production

Avg: $6.43/boe

2016 Company Interest ReservesNet Present

Value1 Before Tax ($MM)

Gas (MMcf)

NGLs (mbbl)

Total (mboe)2 0% 10%

PDP 190,215 6,344 38,046 649 366Total proved 850,804 29,010 170,811 2442 898Proved + probable 2,366,565 83,095 477,522 8,583 2,125

8%

28%

64%

2016 Total Reserves

PDPProved Non-ProducingProbable

32

95

12311

44

104

2016 Reserves: Locations

32

Superior recoveries realized through Black Swan’s North Aitken plant

• Until August 2017 North Aitken was operated to minimize C3 recovery and maximize gas heat content to optimize netbacks (~10 bbl/MMcf C3/C4 vs. design of 20 bbl/MMcf)

• Average McMahon recoveries:• 19 bbl/MMcf (73% C5+); 11% liquids

• Corporate liquids ratio will increase as Black Swan expands its owned and operated processing capacity and McMahon volumes are a smaller percentage

• Long term expected liquids recovery: 30-50 bbl/MMcf (varying based on propane prices)

Black Swan Liquids Yields

0%

10%

20%

30%

40%

50%

60%

70%

80%

Jan

Feb

Mar Ap

rM

ay Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

cJa

nFe

bM

ar Apr

May Jun Jul

Aug

Sep

Oct

Nov De

c

2014 2015 2016 2017

Liquids Revenue as % of Total Revenue

% Liquids Revenue (excl. hedging) % Liquids Revenue (incl. hedging)

North Aitken plant online

Strong gas prices

Weak gas prices

Liquid RecoveriesQ4 2017

bbl/MMcf Corporate North AitkenC5+ 22 24C3/C4 16 21Total 38 45

0

10

20

30

40

50

60

70

80

90

100

Jan/16 Apr/16 Jul/16 Oct/16 Jan/17 Apr/17 Jul/17 Oct/17 Jan/18

Liqu

ids Y

ield

(bbl

/MM

cf)

Black Swan Corporate Liquid Yield

Black Swan Plant McMahon Black Swan Corporate

Black Swan’s plant provides superior liquids yield vs. McMahon

33

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan-

14

Apr-

14

Jul-1

4

Oct

-14

Jan-

15

Apr-

15

Jul-1

5

Oct

-15

Jan-

16

Apr-

16

Jul-1

6

Oct

-16

Jan-

17

Apr-

17

Jul-1

7

Oct

-17

Avg

Cale

ndar

Day

Gas

(MM

cf/d

)

Production Month

North Montney Production1

ARC

Chinook

CNRL

Conoco

Polar Star

Kelt

Todd

Tourmaline

Saguaro

Storm

BSE

Canbriam

Painted Pony

Progress

NEBC Growth Driven by Junior/Intermediate Producers

1. Historical Tourmaline production represents Shell prior to the Gundy acquisition; UGR combined with historical Painted Pony production; Suncor combined with historical Canbriam

Industry investment• Rig activity: 6 rigs operating Feb 2018 vs. 12 in Feb 2017• North Montney production peak at 1.6 Bcf/d in Dec 2017• Juniors and Intermediates represent ~55% of total North

Montney production, up from ~30% three years ago

June 2015 & 2017 volumes impacted by Enbridge

McMahon turnarounds

Note: Competitor land positions based on public reports and geoSCOUT

20 km

34

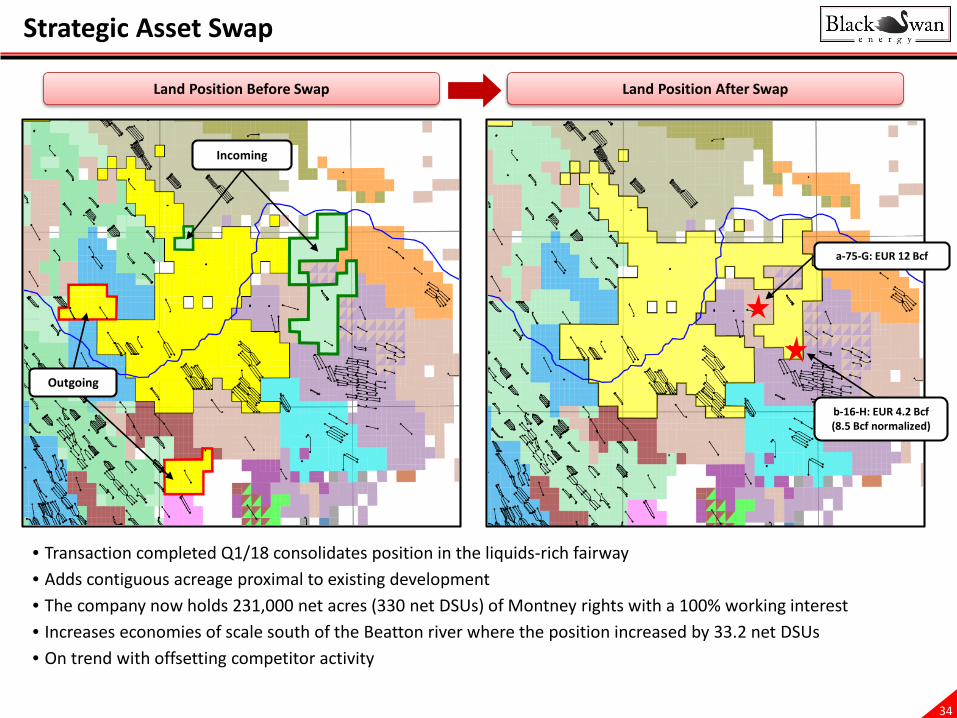

Strategic Asset Swap

• Transaction completed Q1/18 consolidates position in the liquids-rich fairway • Adds contiguous acreage proximal to existing development• The company now holds 231,000 net acres (330 net DSUs) of Montney rights with a 100% working interest• Increases economies of scale south of the Beatton river where the position increased by 33.2 net DSUs• On trend with offsetting competitor activity

Incoming

Outgoing

Land Position Before Swap Land Position After Swap

a-75-G: EUR 12 Bcf

b-16-H: EUR 4.2 Bcf (8.5 Bcf normalized)

35

0

100

200

300

400

500

600

700

800

Blac

k Sw

anPr

ogre

ssCN

QSa

guar

oTO

UCa

nbria

mPo

lar S

tar

CR ARX

ECA

PPY

SRX

CKE

Wom

aRD

SLX

ETO

DD/P

OU

Adur

oCO

PM

UR

KEL

PGF

Prim

aver

a

NET

DSU

s

Repeatable deliverability• Highly over-pressured reservoir 13-16 kPa/m

Liquids-rich• Total liquids of 30-50 bbl/MMcf1 (>50% C5+)

Low capital cost • Shallow target, surface access and drilling characteristics

Low operating costs• Owned & operated infrastructure

Scalable• Large contiguous position

Delivering on a Long-Term Strategy

Upper Montney Oil Window

Normally Pressured

Upper Montney Dry Gas

Alberta

B.C.

Caribou

Umbach

Town

Altares Septimus

Groundbirch

Swan

Parkland

Aitken

Beg

Jedney Laprise

Montney Hz post 2013

Legend

Montney Hz

Black Swan land

Liquids-rich gas window

Dry gas window

Oil window (>75 bbl/MMcf)

Montney TVD contour1600m

25 km

Upper Montney Over-Pressured

Liquids-Rich Fairway

Liquids-rich gas

Largest Holder of Liquids-Rich Montney Rights

Dry gas Oil

36

Corporate Information

Executive Independent Reserve EvaluatorDavid Maddison President & Chief Executive Officer GLJ Petroleum ConsultantsMarc Mereau Chief Operating OfficerBruce Thornhill VP Exploration AuditorsMichael Wilhelm VP Finance & Chief Financial Officer KPMG LLPChristine Ezinga VP Strategy & PlanningLeanne Juneau VP Land Legal CounselBryan Lang VP Operations Norton Rose Canada LLPDiane Shirra VP Business Development

BankersCanadian Imperial Bank of Commerce

Directors Toronto-Dominion BankJackie Sheppard Lead Director Business Development Bank of CanadaDavid Maddison President & Chief Executive Officer Royal Bank of CanadaJim Buckee Independent Director National Bank of CanadaEvan Hazell Independent DirectorJim Nieuwenburg Azimuth Capital Management Head OfficeDavid Pearce Azimuth Capital Management 2700, Bow Valley Square IVRobert Mellema Canada Pension Plan Investment Board 250 6th Avenue SWRoy Ben-Dor Warburg Pincus LLC Calgary, AlbertaDavid Krieger Warburg Pincus LLC T2P 3H7

website: www.blackswanenergy.comPhone: (403) 930-4400

Investor Information Contact

Christine Ezinga (403) 930-4440VP Strategy & Planning [email protected]