lorenzo pupillio presentation

DESCRIPTION

Lorenzo Pupillio PresentationTRANSCRIPT

The State of Telecom 2012 September 24, 2012 – Columbia University – New York

Lorenzo Maria Pupillo Gianfranco Ciccarella Telecom Italia Group

Financial implications in the OTTs-Telcos relation A win-win perspective

State of Telecom 2012

2

* It includes the cost for the LTE spectrum

Fonti: TI’s elaboration based on Forecasts of Investment Banks (Morgan Stanley, Hsbc, Citi, Credit Suisse, JP Morgan, Bernstein, Nomura, Barclays, Deutsche Bank) – Mar/Apr 2012.

Sustainability issue

State of Telecom 2012

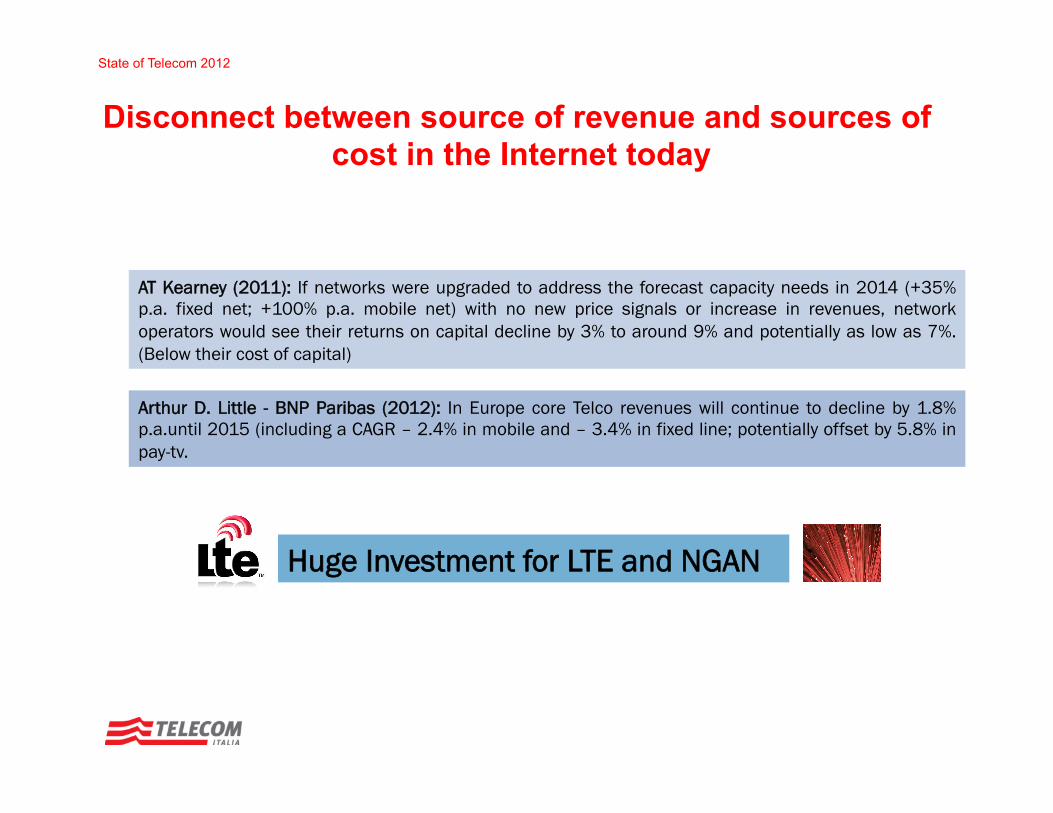

Disconnect between source of revenue and sources of cost in the Internet today

3

Huge Investment for LTE and NGAN

AT Kearney (2011): If networks were upgraded to address the forecast capacity needs in 2014 (+35% p.a. fixed net; +100% p.a. mobile net) with no new price signals or increase in revenues, network operators would see their returns on capital decline by 3% to around 9% and potentially as low as 7%. (Below their cost of capital)

Arthur D. Little - BNP Paribas (2012): In Europe core Telco revenues will continue to decline by 1.8% p.a.until 2015 (including a CAGR – 2.4% in mobile and – 3.4% in fixed line; potentially offset by 5.8% in pay-tv.

State of Telecom 2012

IP Interconnection: peering & transit (1/3)

4

Concentration of Host/ Content in some Carriers who become Tier1 and sell IP Transit

1995: NSFNet closes down and gives ISP Tier1 a clear run Global Internet Traffic: 0,18 PB/month

Telco C

Telco E

Telco B

Telco A

Telco D

peering

transit

transit peering

Host/ Content

Host/ Content Tier1

Tier1 Host/Content

Host/Content

transit

€

€

€

Typical delivery is based on Best Effort

State of Telecom 2012

IP Interconnection: peering & transit (2/3)

5

Telco/ Carrier

Telco/ Carrier

Telco B

Telco A

Telco D

peering

transit

transit peering

Host/ Content

Host/ Content

Host/Content

Host/Content

transit

Free riding !

2004: Google is listed in the S.E. Global Internet Traffic: 1477 PB/month

Growing importance of contents and Carriers/ Aggregators

Arrival of OTT/CP with steady concentration in big players (Google, Yahoo,...)

OTT

OTT

Best Effort - Big volume growth Performance improvement for selected traffic

Concentration of Host/ Content in some Carriers who become Tier1 and sell IP Transit

1995: NSFNet closes down and gives ISP Tier1 a clear run Global Internet Traffic: 0,18 PB/month

State of Telecom 2012

IP Interconnection: peering & transit (3/3)

6

Growth of CDN Providers for content global quality delivery (buffering, caching, web acceleration), and "Carriers" who deliver IP Transit (Level3, Global Crossing, Sparkle)

2010: Akamai’s revenues exceed 1B$ Global Internet Traffic: 20197 PB/m

Telco/ Carrier

Telco/ Carrier

Telco B

Telco A

Telco D

peering

transit

transit peering

Host/ Content

Host/ Content

Host/Content

Host/Content

transit

OTT

OTT CDN Node

CDN Node

CDN Node

Best Effort - Continuous volume growth CDN to improve delivery performance

Concentration of Host/ Content in some Carriers who become Tier1 and sell IP Transit

Growing importance of contents and Carriers/ Aggregators Arrival of OTT/CP with steady concentration in big players (Google, Yahoo,...)

1995: NSFNet closes down and gives ISP Tier1 a clear run Global Internet Traffic: 0,18 PB/month

2004: Google is listed in the S.E. Global Internet Traffic: 1477 PB/month

State of Telecom 2012

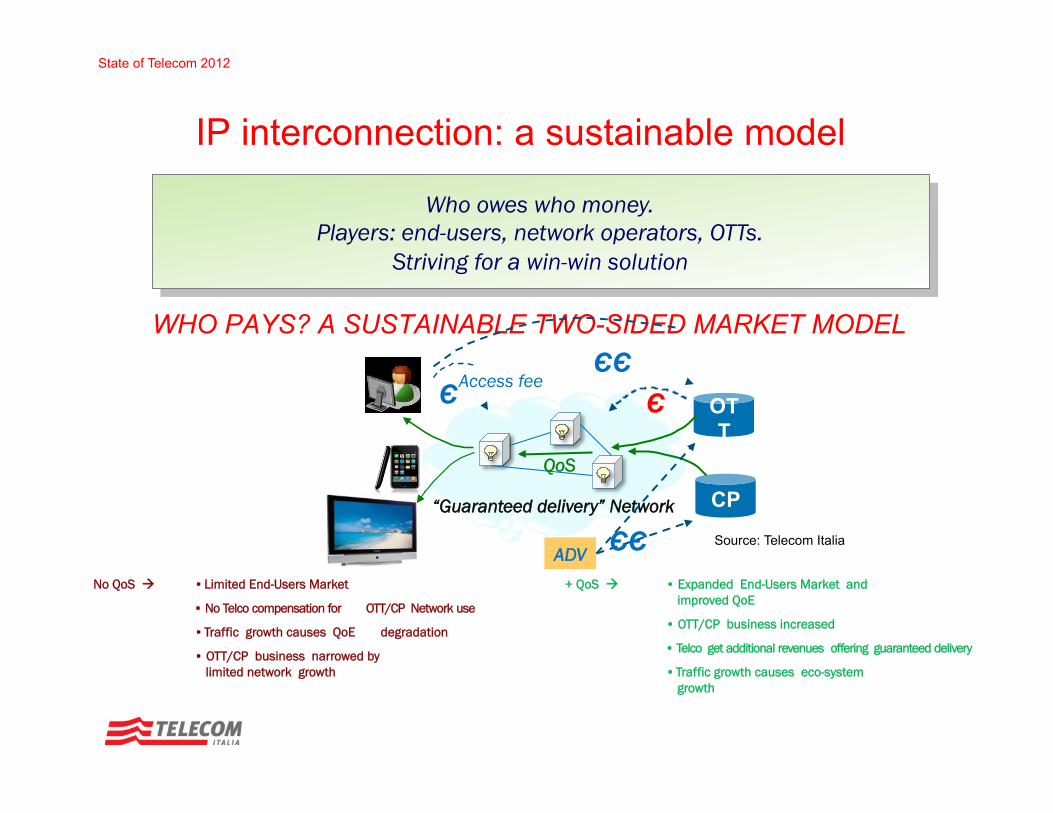

IP interconnection: a sustainable model

WHO PAYS? A SUSTAINABLE TWO-SIDED MARKET MODEL

“Guaranteed delivery” Network

OTT

CP

ЄЄ Є

ADV ЄЄ

Access fee

QoS

Є

Source: Telecom Italia

Who owes who money. Players: end-users, network operators, OTTs.

Striving for a win-win solution

+ QoS à ▪ Expanded End-Users Market and improved QoE

▪ OTT/CP business increased

▪ Telco get additional revenues offering guaranteed delivery

▪ Traffic growth causes eco-system growth

No QoS à ▪ Limited End-Users Market

▪ No Telco compensation for OTT/CP Network use

▪ Traffic growth causes QoE degradation

▪ OTT/CP business narrowed by limited network growth

State of Telecom 2012

The value of QoS…

(*) conversion rate: ratio of visitors who convert casual content views or website visits into desired actions (e.g. product sale, info or SW download, surfing on a specific page…)

* seconds of delay

milliseconds of delay

Reduction in revenue per client

Less search on their web

8 (#) DSA: Dynamic Site Accelerator

Akamai 2010 Investor Summit

Improvement of performances with

Akamai’s DSA#

State of Telecom 2012

Sizing the QoS market

9

Source: TI’s Elaboration based on Forecasts from Cisco VNI 2011-2016 (worldwide)

Revenues are mainly from Advertising and Video on Demand

One can estimate that more than half of the overall traffic

can benefit from a Quality of Service Delivery (this percentage could grow)

Source: Ti’s Elaboration based on Forecasts from Cisco VNI 2011-2016 (worldwide)

In a differentiated delivery scenario, we think that Telcos could address 10-15% of the OTT turnover

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

PB/M

onth

Voice over IP (VoIP)

Online gaming

Web, email, and data

Internet video

File sharing

CAGR 29%

10%

60%

10% 10%

5% 4% 1%

2012

Short form

Long form

Internet video to TV

State of Telecom 2012

Today’s demand for QoS

Licensed Caching & Fully

Licensed CDN

Only interconnection

10 Source: Akamai 2012

State of Telecom 2012

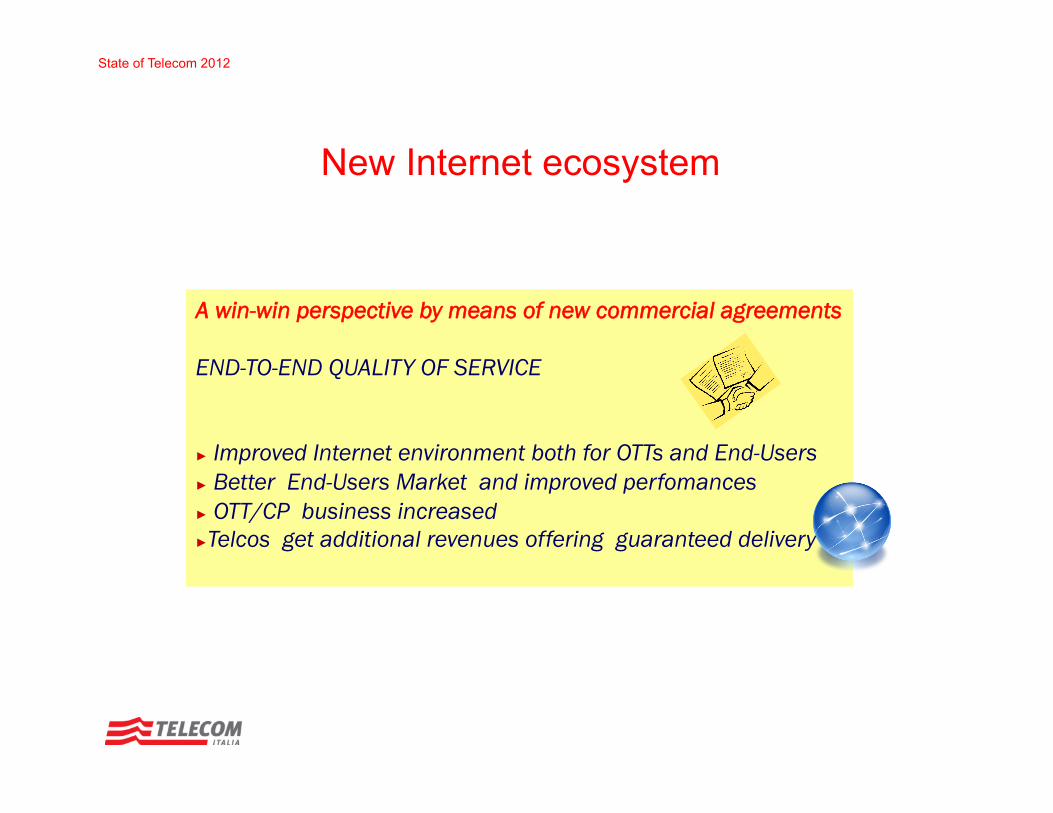

New Internet ecosystem

A win-win perspective by means of new commercial agreements END-TO-END QUALITY OF SERVICE ► Improved Internet environment both for OTTs and End-Users ► Better End-Users Market and improved perfomances ► OTT/CP business increased ► Telcos get additional revenues offering guaranteed delivery