makoka - uct presentation 23june2015 .pptx (read-only) · lilongwe,+malawi.+ uct...

TRANSCRIPT

Supply-‐side Issues in Tobacco Control

Donald Makoka. Centre for Agricultural Research and Development

Lilongwe University of Agriculture and Natural Resources (LUANAR)

Lilongwe, Malawi.

UCT Wednesday, 24 June 2015

2

Introduction • The supply-‐side impact of tobacco-‐control policies, speci8ically the macro-‐economic, employment, and agricultural issues.

• Supply-‐side stakeholders, mainly farmers and manufacturers of tobacco products, tend to form a political and emotional lobby to resist control policies that jeopardize their interests.

• Policy-‐makers often balance the public health imperative of reducing smoking against the economic interests of their tobacco-‐producing or tobacco-‐manufacturing constituents.

3

Introduction • Should policy-‐makers encourage substitution from tobacco to alternative crops, or even buy-‐out tobacco producers altogether?

• Tobacco Industry Myth: • There are currently no economically sustainable alternatives to tobacco farming for small-‐scale farmers, particularly in low-‐ and middle-‐income countries.

4

Introduction • ARTICLE 17 , FTCT: Provision of Support for Economically Viable Alternative Activities.

Parties shall, in cooperation with each other

and with competent international and regional intergovernmental organizations, promote, as appropriate, economically viable alternatives for tobacco workers, growers and, as the case

may be, individual sellers.

5

Supply Side Issues – Malawi as a Case Study.

6

Introduction to Malawi • Malawi’ economy is heavily dependent on the agricultural sector § 39% of GDP comes from agriculture § 83% of foreign exchange earnings

• The main export crop is tobacco, which accounts for around 52.1% of all export earnings

• Malawi is the world’s most tobacco-‐dependent economy (Otanez et al. 2009)

• Tobacco control is challenging to advance because of the role that tobacco plays in the economy.

• Malawi is not a member to the FCTC.

7

Introduction • Top Ten Tobacco Producing Countries in the World in 2012, (MT)

8

Malawi Main Export Commodities in 2012

9

Tobacco Leaf Trade and the FCTC -‐ Malawi • The debate around the FCTC continues to take centre-‐stage

• Tobacco leaf growing continues to shape the politics of tobacco control in Malawi.

• Policy makers often weigh the health bene8its of tobacco control against the potential economic losses that may be brought about by tobacco control

• The central question we ask?

• Is there a difference in the pattern of Malawi’s unmanufactured tobacco external trade during pre-‐FCTC period (2000-‐2005) and after the FCTC was introduced in February 2005?

10

Methodology and Data • The study uses time series data from the International Trade Centre (ITC)’s Trade Map. • The Trade Map provides trade statistics for international business development.

• Trends in unmanufactured tobacco imports and exports were analyzed using trade statistics covering the period 2000 and 2013.

• The data were classi8ied into two groups:

• The pre-‐FCTC period covering the period 2000 to 2005; • The FCTC period covering the period 2006 to 2013.

11

Result 1: RISING EXPORT VALUES • Value of Malawi’s Tobacco Exports (US$, 000), 2001-‐2012

12

Results: RISING EXPORT VALUES • Growth in Malawi’s Tobacco Values (%), 2001/2-‐2012/13

• Tobacco exports have grown by an average of 12.6% between 2005/06 and 2012/13

• For the pre-‐FCTC the annual growth was 1.7%

-‐11.4

6

-‐16.8

29.2

54.7

3.3

39.6

28.7

-‐23

-‐2.4

16

-‐16

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13

13

Result 2: Steady Imports from Neighbouring Countries • Sources of Malawi’s Imported Tobacco Leaf in 2013

• Total imported leaf was valued at US$89.912 million; 88% was imported from Zambia.

14

Result 2: Steady Imports from Neighbouring Countries • Share of Zambia’s Unmanufactured Tobacco Export Volumes by Destination, 2001-‐2013.

15

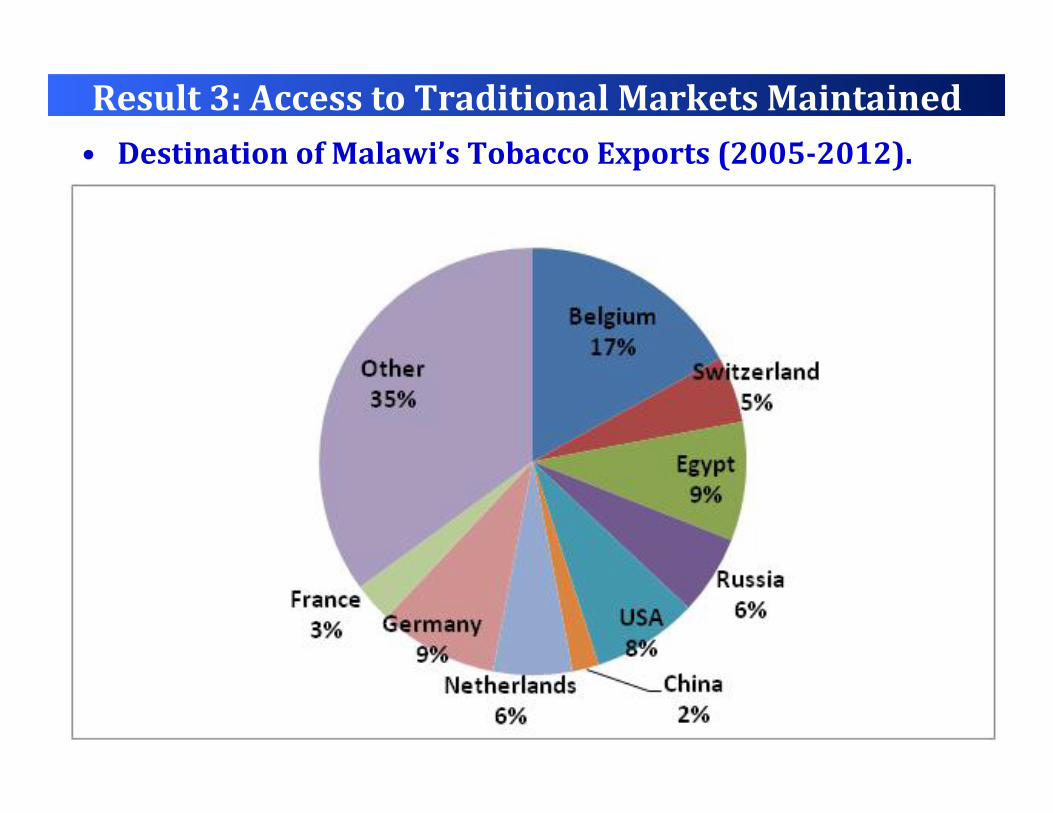

Result 3: Access to Traditional Markets Maintained • Destination of Malawi’s Tobacco Exports (2005-‐2012).

16

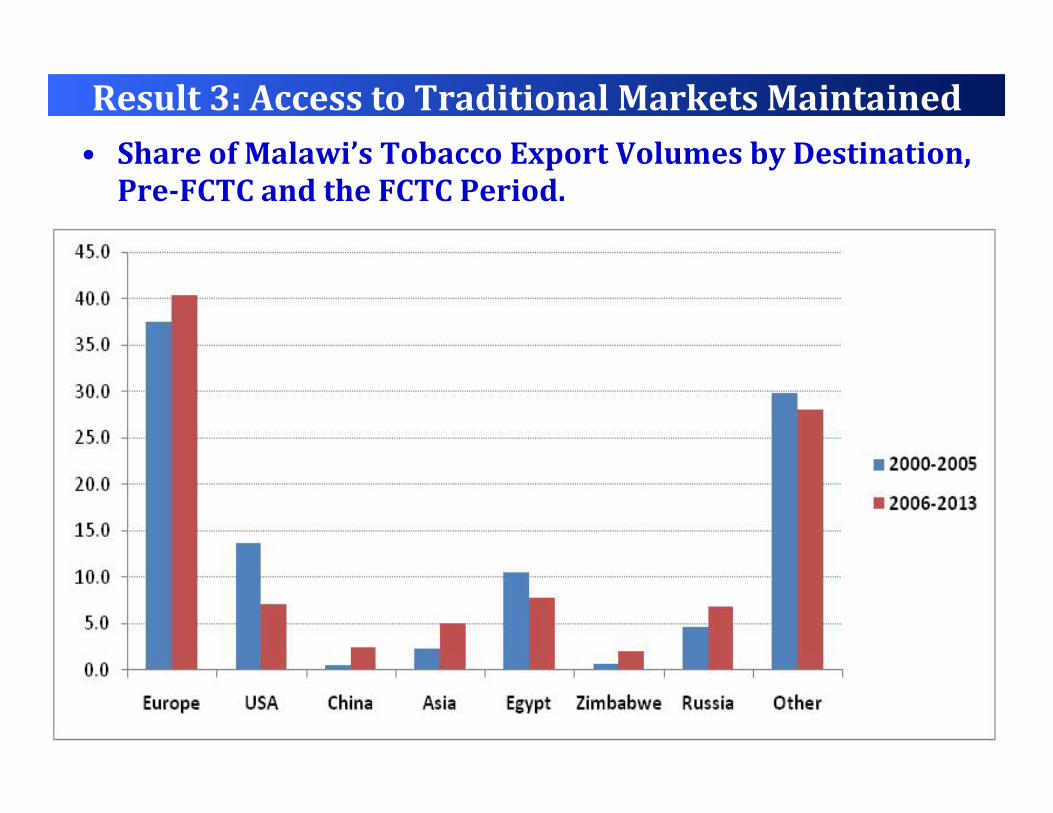

Result 3: Access to Traditional Markets Maintained • Share of Malawi’s Tobacco Export Volumes by Destination, Pre-‐FCTC and the FCTC Period.

17

Key Findings • Up until now the threat of the FCTC on Malawi’s access to European markets has not been signi8icantly felt.

• The data do not also agree with the assertion that Malawi is now looking to China and other Asian markets for its tobacco exports, as the proportion of Malawi’s tobacco that is exported to China has remained below 4% between 2005 and 2012.

• Similarly, its share of tobacco exports to other Asian countries (Republic of Korea and the Philippines) has not gone beyond 7% per year.

• At least in the short term, Malawi will continue to rely on the European market for its exports.

• The 8low of unmanufactured tobacco between Zambia and Malawi has continued unabated even after the signing of the FCTC in Zambia in 2008.

18

Summary and Conclusions • In the short term, the large United States based tobacco leaf-‐buying companies (Universal Corporation and Alliance One International), through their Malawian subsidiary companies – Limbe Leaf Tobacco Company and Alliance One Tobacco Company-‐ will continue to advise Malawi on tobacco-‐related trade policies that attempt to undermine the global tobacco control agenda (Otanez et al, 2009; Otanez et al, 2007).

• Up until now, however, the Malawian policymakers may not yet be losing their sleep over the FCTC.

19

Summary and Conclusions

20

What is the economic situation of tobacco farmers in Malawi?

21

Smallholder Tobacco Production in Malawi • Traditionally tobacco marketing has been through auctioning

22

Smallholder Tobacco Production in Malawi • The Integrated Production System (contract)

• Established in 2012/13 season. • A minimum of 10 individual farmers set up a club

• Each farmer should have at least 1 Ha • The contracts are between the leaf company and the club.

• To facilitate extension services • Trainings • Access to loans • Packaging, baling etc.

• Farmers are still responsible for transporting the tobacco

23

IPS Package

Tobacco Seed is provided as a loan to the IPS farmers

24

IPS Package

Pesticides are also part of the package

25

IPS Package

26

IPS Package

Each farmer is given 2X50 Kg of inorganic fertilizer for maize. They are also given maize seed.

27

IPS Package Farmers are also given seedlings on loan to address the p r o b l e m o f d e f o r e s t a t i o n associated with tobacco farming.

28

IPS Package

P r o t e c t i v e g e a r f o r farmers is also par t o f the package from 2 0 1 4 / 1 5 season. This is also provided on loan. The farmers do not know how much it costs.

29

Smallholder Tobacco Production in Malawi • Input Costs – Individual vs IPS Farmers

Input in 2013/14 season

Individual Farmer

Contract Farmers

Tobacco Fertilizer (50 Kg bag)

$42.86 $47.62

Maize fertilizer (50 Kg bag)

$35.70 $39.47

Maize seed (10 Kg)

$11.90 S14.29

30

Smallholder Tobacco Production in Malawi • The contract farmers are not aware of the cost of the inputs • The cost of inputs under IPS is quoted in US$ • Around January, farmers are given a loan of around US$50.

• Reduce the risk of farmers selling tobacco to intermediate buyers.

• If one individual within the club is unable to repay the loan, the leaf company deducts from the proceeds of the remaining 9 farmers.

• If the whole club has not been able to repay the loan, the farmers are given a new loan to enable the leaf company to recover its money. In the end the farmers are trapped.

• ALLIANCE ONE ((Dimon [USA] and Standard Commercial [USA]) • “Maize yields have increased 10 times “ • “IPS increases tobacco yield by 3 times (600kg/ha to 1,800kg/ha)”

31

• The Malawian tobacco farmer faces the following levies: • TAMA Classi8ication levy (1%) • Association Fee (0.85%) • TCC Levy (0.13%) • ARET Levy (1%) • Hessian Levy (Packaging) (US$0.92/bale)

Smallholder Tobacco Production in Malawi

32

• The interest was to understand the production-‐related (costs, revenues, pro8itability, etc) between contract and individual farmers.

Smallholder Tobacco Production in Malawi

33

Dowa 14.3%

Kasungu 21.8%

Lilongwe 17.5%

Mchinji 16.4%

Ntchisi 14.2%

Rumphi 15.9%

Data • 685 smallholder tobacco farmers -‐307 contract farmers -‐378 individual farmers

34

Data • 685 smallholder tobacco farmers -‐ Proportion of female farmers – 9.9% (National -‐59.5%) -‐ Average age – 40.6 years -‐ Total household size -‐ 6.6 (national 4.4) -‐ Average years of schooling – 7 years

-‐ Total land size – 7.7 Acres (National – 4 Acres) -‐ Proportion of land allocated to tobacco – 40%

35

Data

• Estimating the Cost of Household Labour Supplied to Tobacco Farms

36

Tobacco Nursery

37

Tobacco Drying and Grading

38

Labour

• Tobacco production is highly labour intensive. • The majority of the farmers do not include the cost of household labour when making their decisions to produce.

• So, we attempted the quantify the cost of household labour for each activity.

• For each activity, (e.g. Nursery preparation; nursery watering; planting; fertilizer application, etc), we asked about how many individuals were involved, how many days they worked and how many hours they worked each day.

• Then we calculated the total man-‐hours taken for each activity, and used the government-‐set minimum wage rate for the rural areas to calculate the cost of household labour.

39

Results: Production Costs • Production Costs (US$/Acre)

• Malawian farmers do not include labour costs: • Labour costs -‐ 60.5% (individual farmers); 51.7% (contract farmers)

40

Results: Prices -‐ Average Price (US$/Kg) -‐ Contract Farmers – US$2.43/Kg -‐ Individual Farmers – US$1.78/Kg

• Prices offered to contract farmers is higher to attract farmers to join the contract arrangement (IPS)

• Currently, 80% of total tobacco produced is under contract.

• Industry’s objective is to get rid of auctioning of tobacco

41

Result: Progitability of Leaf Production • Progits/Acre (US$)

• The individual farmers think they are making pro8its; • Contract farmers’ pro8its are actually making only 36% of what they think

they are making.

42

• How does this compare with other crops?

43

Result 2: Future of Tobacco Production

Mzimba

Kasungu

Lilongwe

Mangochi

Chitipa

Rumphi

Dedza

Dowa

Chikwawa

Ntcheu

Mchinji

Zomba

Machinga

Karonga

Nkhotakota

Nkhata Bay

Salima

Balaka

Ntchisi

Mwanza

Nsanje

MulanjeThyolo

Blantyre PhalombeChiradzulu

Likoma

CENTRAL

SOUTHERN

NORTHERN

MOZAMBIQUE

ZAMBIA

TANZANIA

0 50 100

Kilometers

Soybean Study – 2013 -‐ 185 farmers

Paprika and Birds’ Eye Chillies – 2011 -‐ 118 paprika farmers -‐ 91 birds’ eye chillies farmers

44

Progitability of Various Products

US$/Acre Soybean Paprika Birds’ Eye Chillies

Tobacco (Contract)

Tobacco (Individual)

Labour ($/Kg)

96.0 61.84 64.86 405.8 454.3

Price ($/Kg)

0.74 1.03 2.48 2.43 1.78

Profit ($/Acre)

123.00 30.57 209.19 224.30 -‐37.30

N 185 118 91 307 378

45

Perceptions of Tobacco Farmers on the Future of Tobacco Production.

46

Future of Tobacco Production

• Mixture of both qualitative and quantitative methodologies

• Focus group discussions and key informant interviews • Tobacco farmers • Extension workers of leaf companies

• Household survey – 685 farmers.

47

Reasons for Growing Tobacco

• Farmers are growing tobacco mainly because they lack alternatives.

48

Result 2: Future of Tobacco Production

• 41.3% of the farmers have ever considered switching • Poor market prices – 68.5% • Labour intensity – 29.1% • High input (non-‐labour) requirements – 26.3%

• 42.2% do not see themselves still growing tobacco in the next 8ive years.

• Farmers are growing tobacco mainly because they lack alternatives.

49

Future of Tobacco Production • What will make farmers switch from tobacco? • Stable and reliable markets for alternatives – 65.5% • Higher prices for alternative crops – 32.5%

• Alternative crops need to be identi8ied and their supply chains well developed to attract farmers to switch from tobacco.

50

Best Performer – 2014 –Limbe Leaf

A farmer displaying his reward from Limbe Leaf Company for being the best IPS farmer in 2013/14 season.

51

AREAS FOR FURTHER RESEARCH • What is the economics of tobacco growing in the leading African countries (e.g. what are the socio-‐economic conditions of tobacco growers? Are the socio-‐economic conditions tied to the industry-‐grower contracts?)

• What are the trade-‐related alternatives (i.e. value-‐added commodities)

Impact on employment Enablers and barriers in the context of trade agreements (Multilateral, Regional, Bilateral) – tariff dynamics

Sanitary standards across the different agreements for raw food crops (extra-‐ and intra-‐regional standards)

Identi8ication of alternative crops

52

AREAS FOR FURTHER RESEARCH

• What is the political economy of domestic tobacco leaf cultivation and sale (NOTE: conservation of resources theory – psychology)?

• Multilevel approach to analysis – individual farmer perceptions, local and regional environmental conditions, commercial contracts with growers, political interests/incentives at each level, national policy, international arrangements, FCTC provisions and integration into domestic legislation (Articles 17 and 18).

53

AREAS FOR FURTHER RESEARCH

What are the health effects of tobacco production in countries like Malawi?

54

END OF PRESENTATION

THANK YOU SO MUCH