managed care: present and future robert (james) walling, mrh&t james b. connor, pricewaterhouse...

Post on 19-Dec-2015

217 views

TRANSCRIPT

Managed Care: Present and Future

Robert (James) Walling, MRH&T

James B. Connor, Pricewaterhouse Coopers

James W Macdonald, Reliance Reinsurance Corp.

Managed Care: A Brief Look at the Past

Robert J. Walling, Consulting Actuary

Miller, Rapp, Herbers, & Terry, Inc.

Why look at “Ancient History”

Those who cannot remember the past are condemned to repeat it.

—George Santayana

That men do not learn very much from the lessons of history is the most important of all the lessons of history.

—Aldous Huxley

Ancient History 1

1910– First prepaid group practice (50¢ /member/mo)– First group health policy issued to Montgomery

Ward

1917– Early medical society opposition to managed care

begins as Pierce County Service Bureau is formed to limit competition from prepaid plans.

1929: Depression & Managed Care

Decreased philanthropic support of hospitals Substantial medical inflation Decreased hospital occupancy First prepaid hospital (Dallas Schools &

Baylor University Hospital) The Ross-Loos service clinic establishes

prepaid clinic in L.A. for Power and Water Departments

Backlash

1931 - Ross & Loos expelled from L.A.

County Medical Society

1932 - AMA Publishes a strong statement

opposing prepaid medical.

1932 - Blue Cross developed (medical

community responded more favorably to

health insurance than prepaid medical)

Development Despite Opposition

1937 - First Urban HMO established (Group Health Associates in D.C.)

1937 - Henry Kaiser begins Permanente Plans as prepaid medical plan for workers on Grand Coulee Dam construction site.

Judicial Developments

1941 - U.S. Supreme Court finds D.C. Medical Society guilty of Restraint of Trade against Group Health Associates

Several court successes for HMOs follow. (Shadid v. Oklahoma Medical Society)

Over the next 10 years, 100 rural group health plans, 20 HMOs, and prepaid group health plans for several local unions (Teamsters, UAW, UMW) develop.

Social/Political Changes

1965 - Social Security expanded to include medical insurance for the elderly (Medicare) and poor (Medicaid)

1970 - Nixon responds to $85B in US Health expenditures by endorsing HMOs as new national health strategy

1973 - HMO Act signed by Nixon. Provides for “assistance and encouragement for the establishment and expansion of HMOs”

Economic Changes

1975-84 - Hospital charges inflated at average of 9.3%

1970-90 US Health expenditures rise from $85B to $647B

1990 - Health Expenditures 12% of GDP.

Economic Changes (cont.)

Dramatic increase in medical malpractice costs

Dramatic advances in medical technology (CAT scans, MRI, Organ transplants, etc.) revolutionize medical care but at a substantial cost

A number of social factors (aging population, more doctors, new techniques, relatively low employee costs) increase utilization.

Number of HMOs

1950 - 20 1970 - 37 in 14 states 1975 - 183 in 32 states (297 more in

planning) 1980 - 236 HMOs serving 9.1 million

members 1985 - 393 HMOs 1987 - 662 HMOs

Early Cost Containment Efforts

Controlling Utilization– Utilization Review– Weekend Admissions– Maternity Length of Stay– Preadmission review– Second Surgical Opinion– Case Management– Appropriate Level of Care– Pre-admission Review

Early Cost Containment Efforts

Employee Contributions Reducing Plan Benefits

– Deductibles

– Copayments

– Maximums (Mental Health, Private Rooms, Chemical Dependency, DME, Physical Therapy)

– Outpatient Incentives

Provider Network Discounts

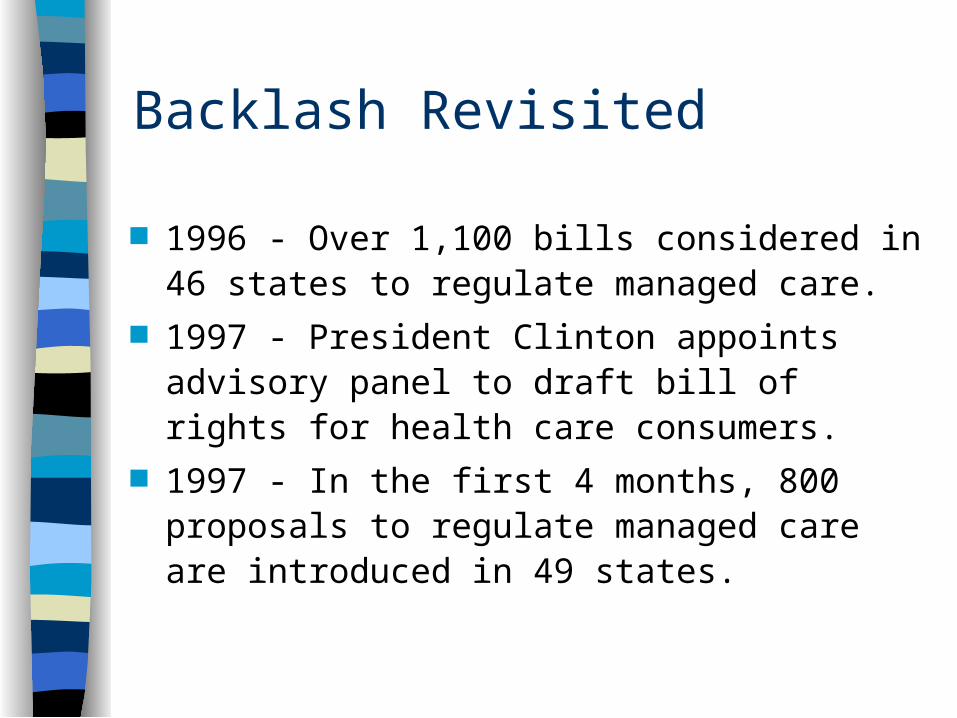

Backlash Revisited

1996 - Over 1,100 bills considered in 46 states to regulate managed care.

1997 - President Clinton appoints advisory panel to draft bill of rights for health care consumers.

1997 - In the first 4 months, 800 proposals to regulate managed care are introduced in 49 states.

Managed Care: Present & Future

Jim Conner

Pricewaterhouse Coopers

Managed Care - Overview Current Environment

– Trend Issues– Overview

Growth Prices Medical Care Costs Margins Mergers Quality of Care Member Satisfaction Government Programs Computer Systems Regulatory

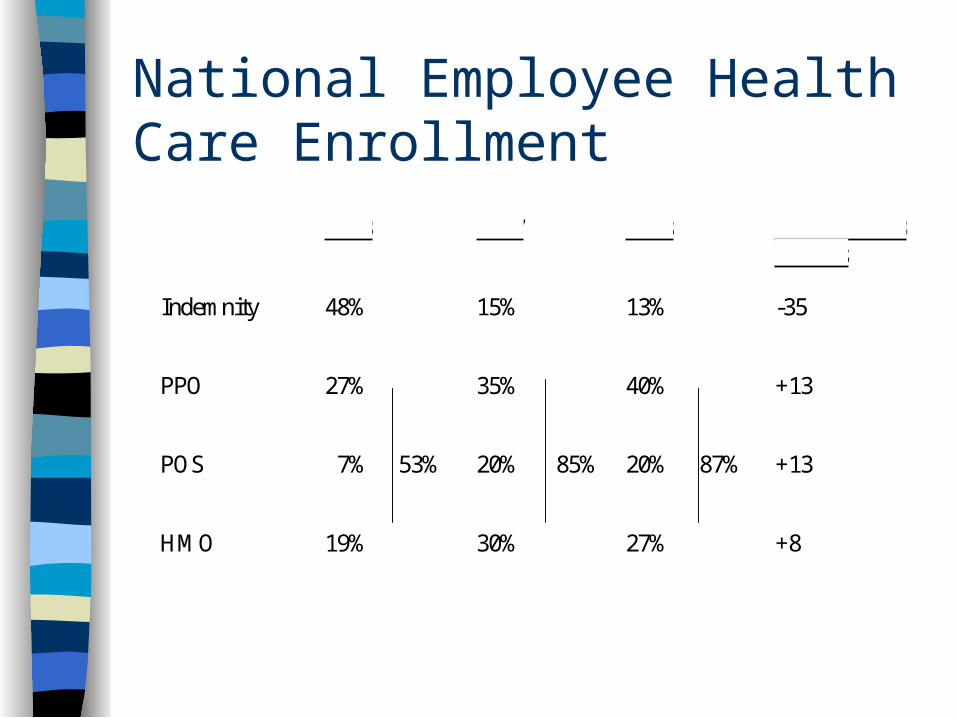

National Employee Health Care Enrollment

1993 1997 1998 Change 1993 to 1998

Indemnity 48% 15% 13% -35

PPO 27% 35% 40% +13

POS 7% 53% 20% 85% 20% 87% +13

HMO 19% 30% 27% +8

Overview - HMO Results

1990 1994 1996 1997

# Members 36.5 mil 51.1 mil 64 Mil 64 mil

Growth Rate 5% 13% 19% 0%

Penetration 15% 20% 24% 24%

Margin 4.6% 4.7% 2.0% -0.5%

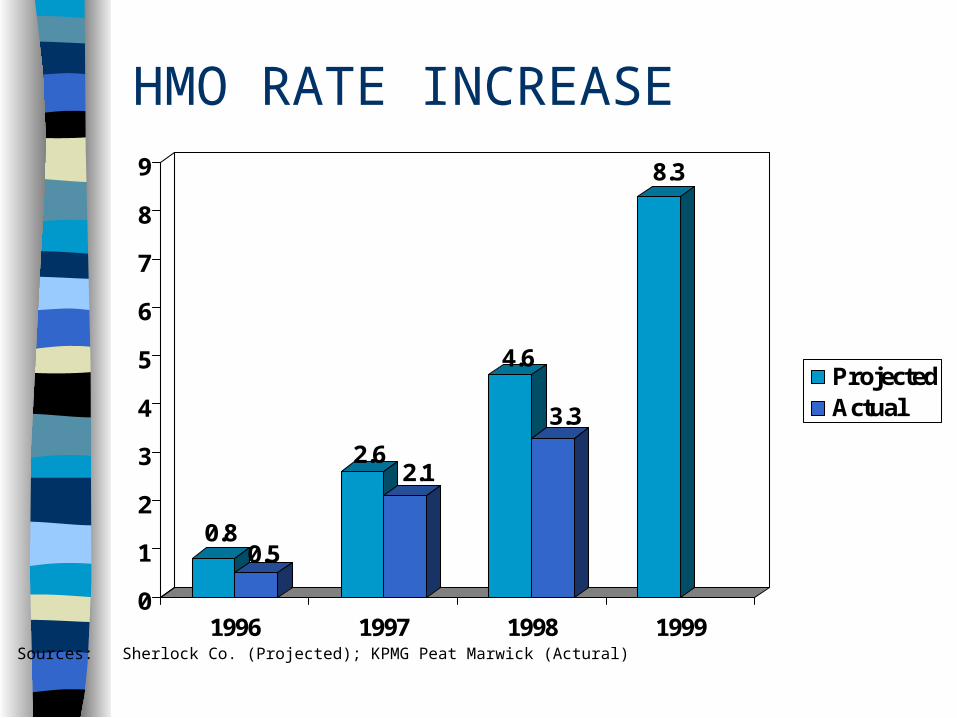

HMO RATE INCREASE

0.80.5

2.62.1

4.6

3.3

8.3

0

1

2

3

4

5

6

7

8

9

1996 1997 1998 1999

ProjectedActual

Sources: Sherlock Co. (Projected); KPMG Peat Marwick (Actural)

Managed Care - Growth

Penetration/Growth Rate

Control Risk

Underwriting Risk

Provider Contracting Leverage

Managed Care - Prices

Price Changes

Market Share Driven

Employer Leveraged

Expectations of Managed Care

Purchasing Coalitions

Underwriting Cycle

Managed Care - Medical Care Costs

Utilization vs. Inflation

Aging Population

Disease Management

Capitation/Risk Sharing

Pharmacy Costs

Complementary & Alternative Medicine (CAM)

Managed Care - Margins

Digesting Acquisitions

Computer Capacity

Rising Medical Costs

Building Market Share

Managed Care - Quality of Care

Clinical vs. Administrative

Accreditation (NCQA)

HEDIS Reporting

Quality vs. Cost

Managed Care - Member Satisfaction

Choice of Provider

Point of Service/Open Access Products

Availability of Provider

Managed Care - Government Programs

Medicare Risk

Medicare + Choice

Medicaid

Managed Care - Computer Systems

Information Driven Business

Capacity

Medical Management

Integrated Healthcare Systems

Dynamic Industry

Managed Care -Pricing Components

Pricing Grid

Medical Service Categories 20 - 30

Diagnostic Related Groups (DRG)495

Procedure Codes (CPT) 1,000+

Diagnostic Codes (ICD9) 1,000+

Managed Care -Regulatory Consumer Protection Legislation

– Emergency Care– External Appeals– Access to Specialists– Continuity of Care– Right to Sue Health Plan

Medicare Reform– Medicare & Choice– Outpatient Drugs

Medical Record Privacy– Consent Issue– Genetic Data

Uninsured (45 Million)

MANAGED CARE MANAGED HEALTH

Future of Managed Care: The Only Certainty is (Much) More Change

James W Macdonald, Senior Vice President

Reliance Reinsurance Corp.

Important recent developments most likely to define the future

of Managed Care

Consumer Choice is returning rapidly

500

550

600

650

700

750

800

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Number of Operating HMOs - Dramatic Growth Since 1993

Source: Hoechst Marion Roussel Managed Care Digest 1998; SMG Marketing Group

25

35

45

55

65

75

85

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

Total Enrollment Approached 84 Million In 1997

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Staff 4.3 4.2 3

Group 16.2 19.5 19.8

Network 8.9 8.4 14.2

IPA 38 45.2 46.7

1995 1996 1997

Decentralized Models are #1: Over 70% of 1997 HMO Enrollees were in Network or

IPA model plans

35.00%

45.00%

55.00%

65.00%

75.00%

1996 49.00%

1997 73.90%

IPA HMOs

IPA Model HMOs Not Penalizing Physicians for Certain Practices Increased From 49% in 1996 to

74.1% in 1997

38.0%

39.0%

40.0%

41.0%

42.0%

43.0%

44.0%

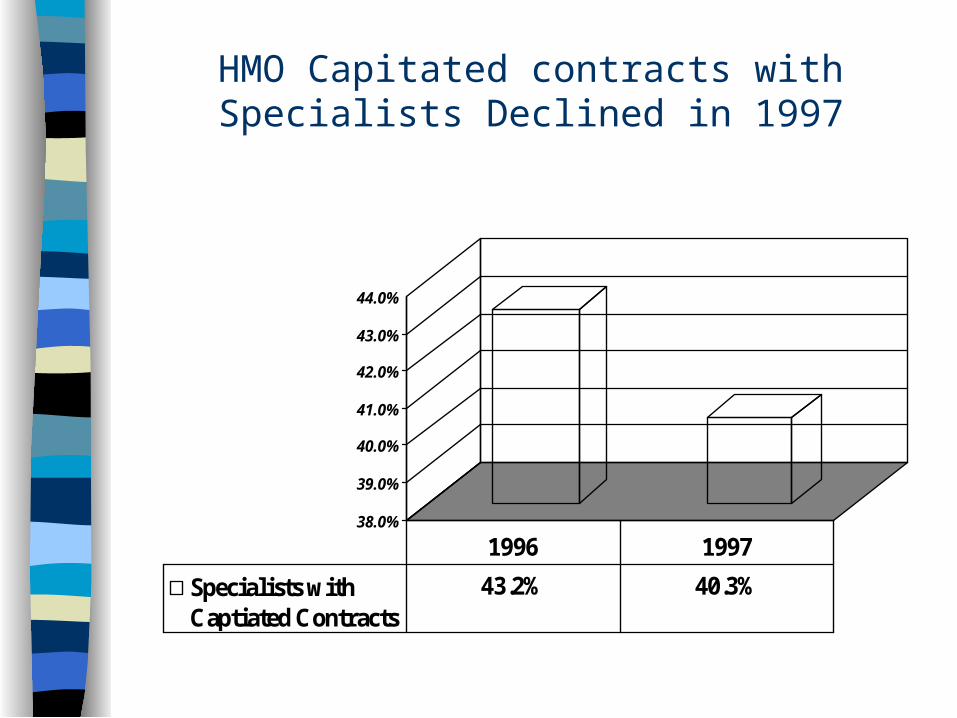

Specialists withCaptiated Contracts

43.2% 40.3%

1996 1997

HMO Capitated contracts with Specialists Declined in 1997

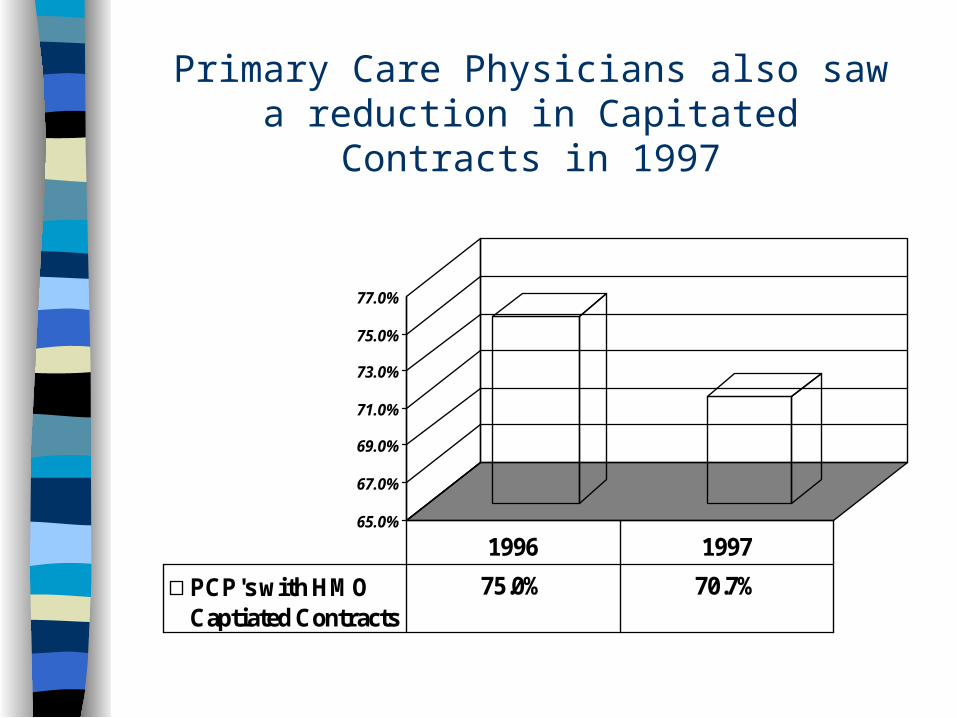

65.0%

67.0%

69.0%

71.0%

73.0%

75.0%

77.0%

PCP's with HMOCaptiated Contracts

75.0% 70.7%

1996 1997

Primary Care Physicians also saw a reduction in Capitated Contracts in 1997

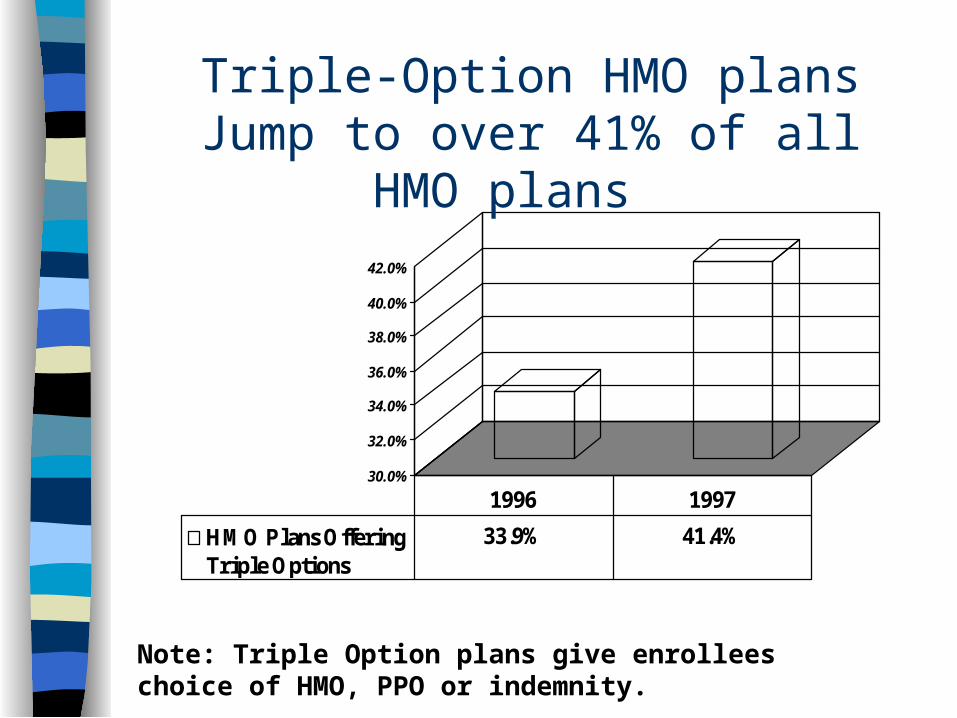

30.0%

32.0%

34.0%

36.0%

38.0%

40.0%

42.0%

HMO Plans OfferingTriple Options

33.9% 41.4%

1996 1997

Triple-Option HMO plans Jump to over 41% of all HMO plans

Note: Triple Option plans give enrollees choice of HMO, PPO or indemnity.

Important recent developments most likely to define the future

of Managed Care

Consumer Choice is returning rapidly The Cost of Health Care will Re-Accelerate

Health Care Expenditures as a Percent of GDP - New Growth Expected

(Selected Years to 2007)

5

7

9

11

13

15

17

19

1970 1980 1990 1993 1996 1998e 2001e 2007e

Sources: HCFA, Office of the Actuary; US Department of Commerce, Bureau of Economic Analysis

Private Sector Expected to assume Burden of Increased Expenditures ($B)...

200

300

400

500

600

700

800

900

1000

1100

1200

Public Sector 284.4 389 483.1 540.4 637.4 987.4

Private Sector 415.1 505.9 552 606.4 746.6 1145.9

1990 1993 1996 1998e 2001e 2007e

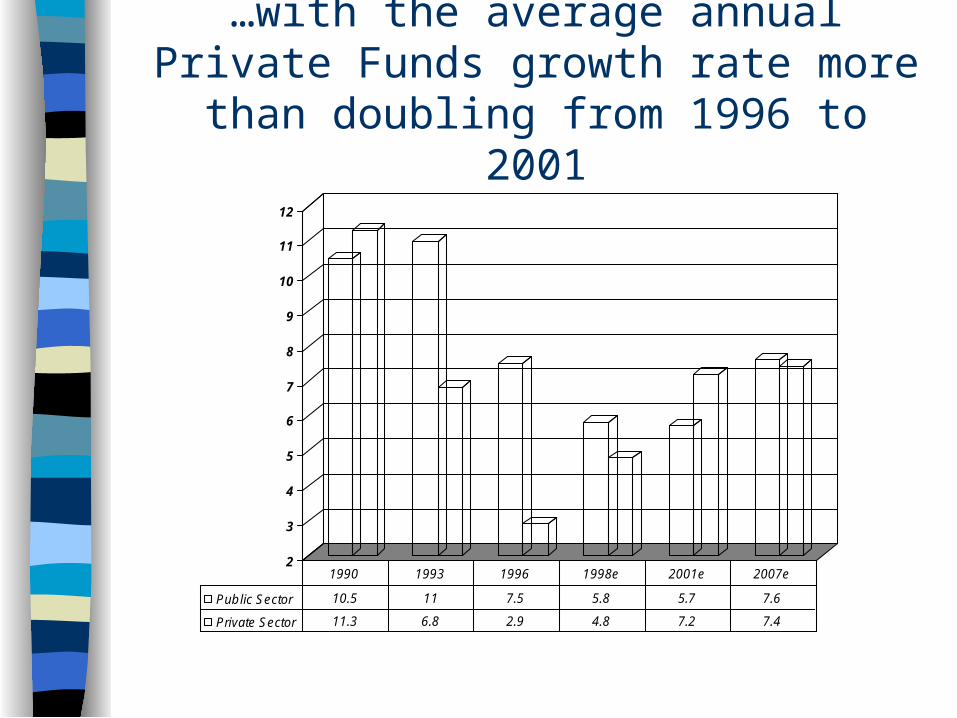

…with the average annual Private Funds growth rate more than doubling from 1996 to

2001

2

3

4

5

6

7

8

9

10

11

12

Public Sector 10.5 11 7.5 5.8 5.7 7.6

Private Sector 11.3 6.8 2.9 4.8 7.2 7.4

1990 1993 1996 1998e 2001e 2007e

…But widespread double-digit growth rates are not expected to return

(Average Annual Growth Rate From Prior Year Shown)...

0

5

10

15

20

25

30

National Health Expend. 12.9 5 7.5

Hospital care 13.9 4.9 6.6

Physician services 12.8 3.5 7.8

Other professional 16.3 7.8 8.1

Home health care 26.9 9.7 8

Prescription Drugs 8.2 7.6 9.8

1970-1980 1993-1996 2001-2007

Two assumptions critical to these projections ...

Cost savings produced by Managed Care are “primarily one-time” and are not sustainable.

Only a small long term growth rate reduction will result from the impact of managed care on the use of higher cost medical technology.

Important recent developments most likely to define the future

of Managed Care

Consumer Choice is returning rapidly The Cost of Health Care will Re-

Accelerate Vertical Integration will become as

much a change driver as Horizontal Integration

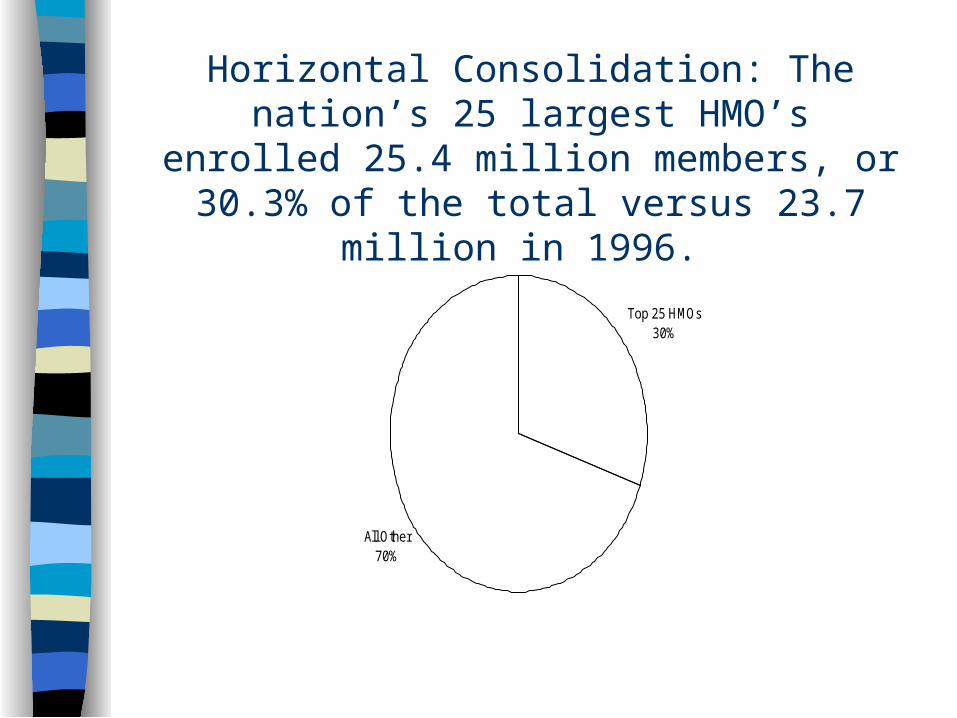

Horizontal Consolidation: The nation’s 25 largest HMO’s enrolled 25.4 million members, or 30.3%

of the total versus 23.7 million in 1996.

Top 25 HMOs30%

All Other70%

40

45

50

55

60

65

Hospital-OwnedHMOs

46 58 61

1995 1996 1997

Vertical Consolidation: Hospitals are forming and taking increased equity stakes in HMOs

Source: SMG Marketing Group

2200

2700

3200

3700

4200

Hospital-OwnedHMO Emrollment(000s)

2,448 2959.8 4082.1

1995 1996 1997

Vertical Consolidation: Hospital-Owned Enrollment Growth Possible Key Indicator to

Future of Managed Care

Source: SMG Marketing Group

30%

40%

50%

60%

70%

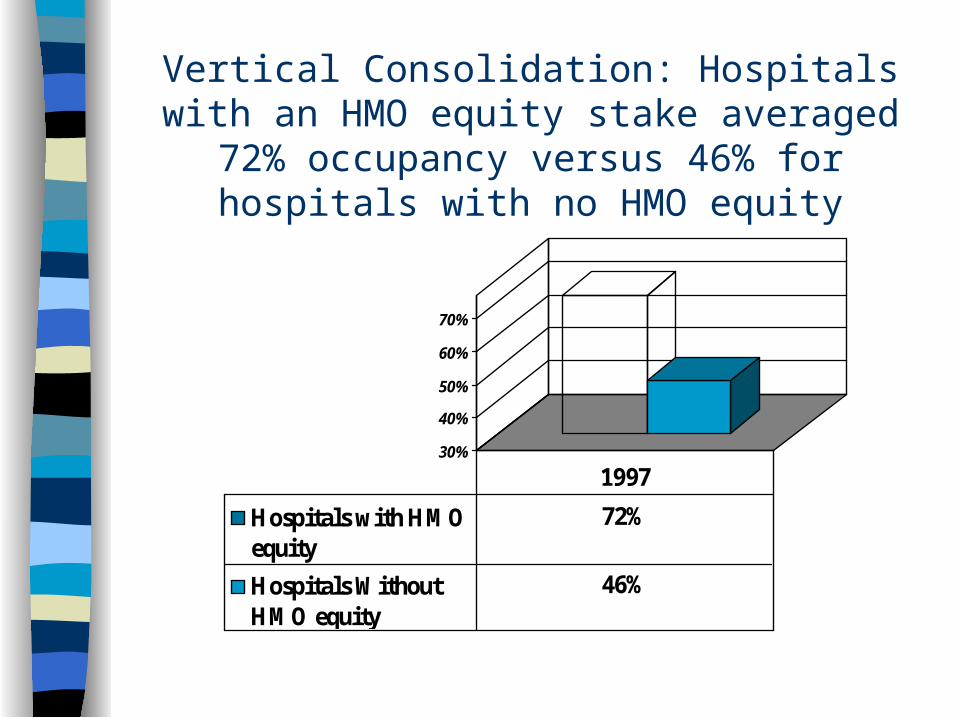

Hospitals with HMOequity

72%

Hospitals WithoutHMO equity

46%

1997

Vertical Consolidation: Hospitals with an HMO equity stake averaged 72% occupancy versus 46%

for hospitals with no HMO equity

Vertical Consolidation: Pharmaceutical Segment

Top Down: Merck / Medco Bottom Up: Rite Aid / PCS Mixed Segments: McKesson / HBOC

Important recent developments most likely to define the future

of Managed Care

Consumer Choice is returning rapidly The Cost of Health Care will Re-

Accelerate Vertical Integration will become as much

a change driver as Horizontal Integration Future of Managed Care / Health Care

Phase 1:

National expansion & share consolidation

Free Market Ideal: Three Phases to Market Evolution

Source: Andersen Consulting

S eg m en t1 S eg m en t 2 S eg m en t 3

H M OC u s tom ers

Phase 2:

Market Segmentation

Phase: 3

Outcomes Based Product & Service Differentiation

Three Phases to Market Evolution:

Source: Andersen Consulting

“...universally accepted quality standards and measurement capabilities…”

Conclusion: Past Key Health Care Issues Remain Unresolved ...

Aging Baby Boomers (should drive medicare Managed Care Growth)

Uninsured & Underinsured Americans Solvency of Medicare / Medicaid Highest Health Care % of GDP High Cost of New Technology Need for highly informed patient / consumer

(“Demand Management”)

… while several tough issues have emerged today...

Demonization of Managed Care Probable loss of ERISA protection Patient Distrust of For-Profit Providers Failure of PPMC model: Physicians in

disarray New and tougher regulatory

environment

… and new important challenges appear to be on the

horizon. End of low cost malpractice and E&O

Insurance? Payer Dis-intermediation: Large

Employer Direct Contracting (e.g. John Deere)?

Impact of BBA of 1997 prospective payment system

Conclusion: Follow the MoneyTwo Possible Long Term Scenarios

Decentralized, regional payer and provider system– Can consumer bear increased cost?– Can investors achieve adequate ROI?

If not, probable alternative: centralized, single or limited payer system– Strictly tiered, government controlled– Similar to British or Canadian systems

Conclusion: Most Likely Scenario“Tiers - R - Us”

Safety Net

SecureMiddle Market

Elite

1980 1990

Safety Net

UpscaleManaged

CareVulnerable

Middle Market

Elite Elite

Low-End Managed Care

Safety Net

2000+

Q&A