may 12 1130 auditing and monitoring your compliance program

TRANSCRIPT

v

Presented By:

vv

vPresented By:

v

Presented By:

vv

vPresented By:

v

Presented By:

May 12, 2015Ethics & Compliance:

Auditing and Monitoring Your Compliance Program

11:30 am – 12:45 pm

v

Presented By:

• KATHLEEN EDMOND, Partner, Robins Kaplan LLP

• ANDY HINTON, Vice President, Global Ethics and Compliance, Google Inc.

• LISA BETH LENTINI, Vice President, Global Compliance, Carlson Wagonlit Travel

• CRAIG VAN DEVENTER, Vice President, Compliance, Wyndham

v

Presented By:

v

Presented By:

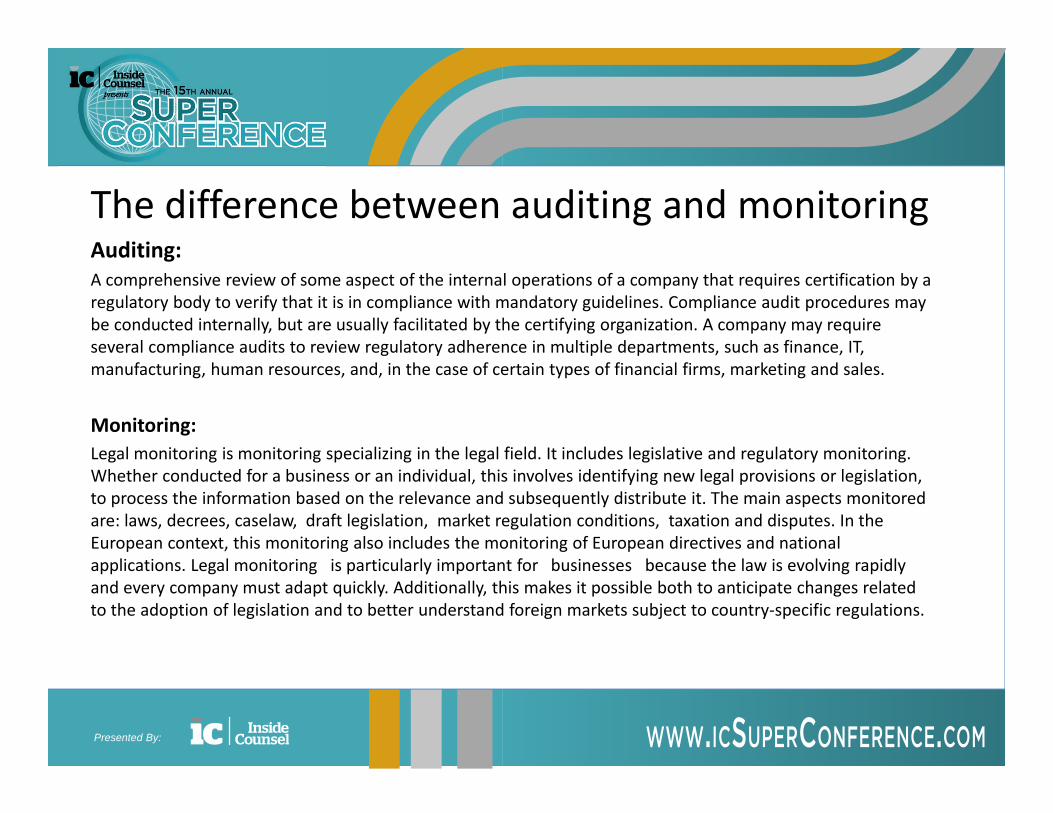

The difference between auditing and monitoringAuditing:A comprehensive review of some aspect of the internal operations of a company that requires certification by a regulatory body to verify that it is in compliance with mandatory guidelines. Compliance audit procedures may be conducted internally, but are usually facilitated by the certifying organization. A company may require several compliance audits to review regulatory adherence in multiple departments, such as finance, IT, manufacturing, human resources, and, in the case of certain types of financial firms, marketing and sales.

Monitoring:Legal monitoring is monitoring specializing in the legal field. It includes legislative and regulatory monitoring. Whether conducted for a business or an individual, this involves identifying new legal provisions or legislation, to process the information based on the relevance and subsequently distribute it. The main aspects monitored are: laws, decrees, caselaw, draft legislation, market regulation conditions, taxation and disputes. In the European context, this monitoring also includes the monitoring of European directives and national applications. Legal monitoring is particularly important for businesses because the law is evolving rapidly and every company must adapt quickly. Additionally, this makes it possible both to anticipate changes related to the adoption of legislation and to better understand foreign markets subject to country‐specific regulations.

v

Presented By:

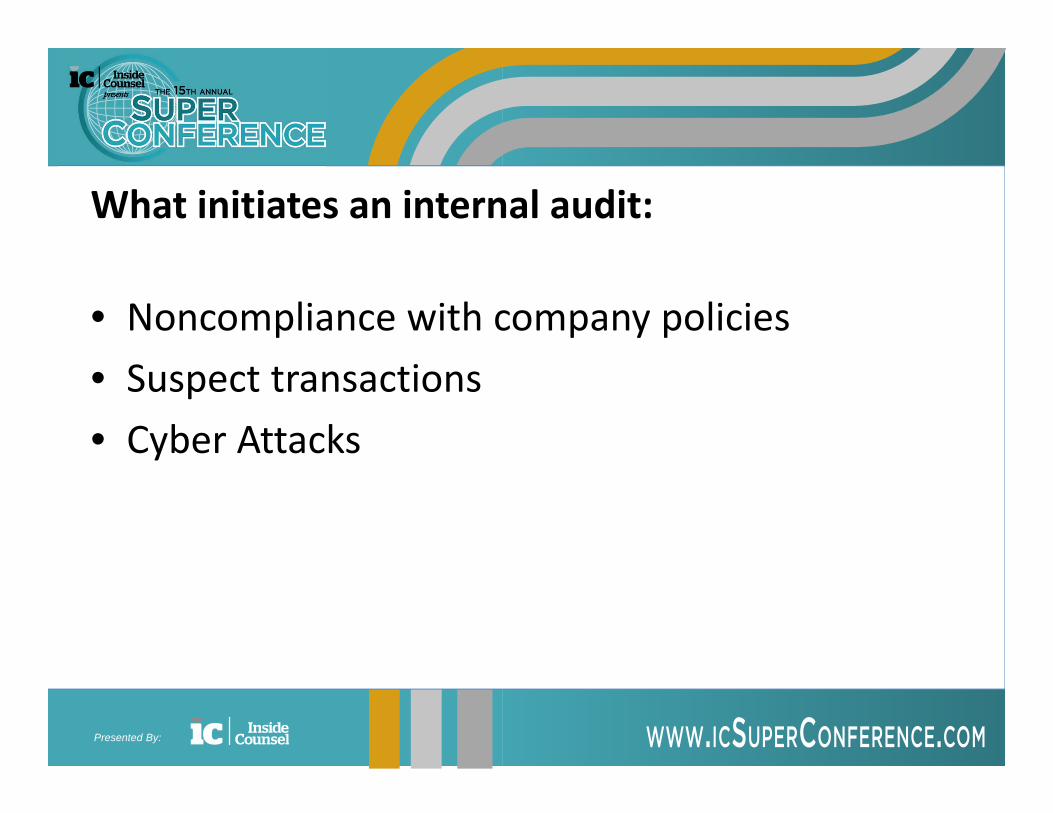

What initiates an internal audit:

• Noncompliance with company policies • Suspect transactions• Cyber Attacks

v

Presented By:

Benefits of an audit:• How to make sure the audit strengthens the compliance

program?– Provides validity– Discovers errors– Limits legal and tax issues– Educate Business Owner

v

Presented By:

Checklist of what you need to do:

• Establish and communicate the scope and objectives for the audit to appropriate management.• Develop an understanding of the business area under review. This includes objectives, measurements, and

key transaction types. This involves review of documents and interviews. Flowcharts and narratives may be created if necessary.

• Describe the key risks facing the business activities within the scope of the audit.• Identify management practices in the five components of control used to ensure each key risk is properly

controlled and monitored. Internal Audit Checklist can be a helpful tool to identify common risks and desired controls in the specific process or industry being audited.

• Develop and execute a risk‐based sampling and testing approach to determine whether the most important management controls are operating as intended.

• Report issues and challenges identified and negotiate action plans with management to address the problems.

• Follow‐up on reported findings at appropriate intervals. Internal audit departments maintain a follow‐up database for this purpose.

v

Presented By:

Who is responsible for audit findings:

Publicly‐traded United States corporations typically have an internal auditing department, led by a Chief Audit Executive ("CAE") who generally reports to the Audit Committee of the Board of Directors, with administrative reporting to the Chief Executive Officer.

v

Presented By:

Monitoring and Reviewing

This includes the continual measurement and monitoring of the risk environment and the performance of the risk management strategies.

– Set written policies. – Inform your workforce.– Use technology tools– Manage and get the most out of their internal and external legal

resource.

v

Presented By:

Any questions?