monthly report october 2016 - manufacturingchampions.in · monthly report –october 2016...

TRANSCRIPT

1

Summary growth trends for the month of October 2016

Overall, October registered a growth of ~5% for the Indian industry, slowing in pace post its

high growth months of August and September

All regions witnessed a sluggish growth: North saw the slowest growth at only 4% and

South saw a sharp difference in volume and value growth at 5% and 8% respectively. East

and West grew at the same pace of 5% through October

Inflation for Oct 2016 (difference between value and volume growth) seemed marginal across

geographies

Consumer durables (~17%), commercial vehicles (~12%), textile and apparels (10%) emerged

as winners in October; Two wheelers (9%), engineering products (7%) and passenger

vehicles (~5%) showed moderate growth, while auto components (~1%) and building

materials (~1%) witnessed relatively weak growth

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Inflation reported above is the value over volume growth based on the survey results.Source: CII BCG Growth Index Survey; Industry association data on automotive sales

2

Survey Results

3

Survey results: October 2016 performance

VolumeValue

0

4

8

12

Oct’16

5%5%

Sep ’16

8%8%

Aug ’16

8%9%

Jul’16

4%6%

YoY growth %

Jun’16

8%9%

May’16

6%7%

Summary – all respondents Regional growth – All respondents1

Industry growth comparison

Value growth (%)

Peer growth comparison

-20

-15

-10

-50

5

10

15

20

20151050-5-10-15-20

Volume growth (%)

Value growth (%)

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

0-2-4-6 18161412108642

Two WheelersEngineering

ProductsBuilding

Products

Auto components

All industry average All industry average

West:

5% (6%)

South:

8%

(5%)

North:

4% (3%)

East:

5% (5%)

Volume growth (%)

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basisNote: Building materials (BM) industry refers to cement, cementitious products, paints, tiles, roofing, scaffolding. Industry average is displayed only when there are 3+ responses per industry. Other industries where responses were received include: consumer durables, Steel, chemicals, plastics, logistics, packaging, Consulting services, Financial services. Regional averages may not fully align with national average because of different regional exposures of respondent industries. All averages are 'simple averages' (i.e. not weighted by size of company). CV – Commercial vehicles, PV –Passenger vehicles, Auto Comp – Auto Components, Engg prod & services – Engineering products and services, Build. mater. – Building Materials, MHE – Material Handling EquipmentSource: CII BCG Growth Index Survey; Industry association data on automotive sales

Value

growth yoy

Volume

growth yoy

Region

xx:

xx% (yy%)

4

Building materials witnessed sharp fall in overall

growth, deepest in North and West

Peer growth comparison

Value growth (%)All industry average

-16

-12

-8

-4

0

4

8

12

16

20

-16 -12 -8 -4 0 4 8 12 16 20

Volume growth (%)

• Building materials witnessed a de-growth in North and growth in

West fell to 2%. Overall, the industry grew <1% in revenue

• South re-gained it's position as the leading market for building

growth, maintaining a steady rate of 9%

• Sentiments from survey respondents:

<500 cr

Regional growth – All respondents1

West:

2% (5%)

South:

9%

(7%)

North:

-0.5% (-0.5%)

East:

3% (5%)

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Building materials include cement, cementitious products, paints, tiles, roofing, scaffolding , and glass. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. Source: CII BCG Growth Index Survey, CMIE, Projectstoday

Value

growth yoy

Volume

growth yoy

Region

xx:

xx% (yy%)"Markets and demand seem to be on the upswing post a good

monsoon. There was a dip in sales on account of Dussera and

Diwali holiday's. Across various part of the country there were

nearly 7-8 holidays, despite which there was growth."

- Mr. Rahul Chopra, Sr. VP and Head Roofing, Everest

Industries Ltd.

5

Material Handling Equipment witnessed growth at

6% across India with strongest growth in East

Regional growth – All respondents1

West:

3% (6%)

South:

4%

(0%)

North:

3% (-4%)

East:

10% (9%)

Peer growth comparison

Value growth (%)

-16

-12

-8

-4

0

4

8

12

16

-4 0 4 8 12 16 20

Volume growth (%)

• Material handling witnessed revenue growth of 6% and

volume growth of 4%

• With the demonetization of notes industries like

infrastructure, consumer durable, auto and real estate is

likely to feel the most heat. This might be layered with the

fresh uncertainty once there is more clarity on GST

• Sentiment of respondents:

< 500 cr

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. 2. Capacity addition and distribution lines data is for Jul 2016. 3. Export rise is on YoY for Apr –Aug period. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. The growth numbers reported are on an year-on-year basis. MHE – Material handling equipments. Source: CII BCG Growth Index Survey

Value

growth yoy

Volume

growth yoy

Region

xx:

xx% (yy%)

All industry average

"Though there are project enquiries being released,

movement is slow" – Mr. Pramod M. Pophale, GM Sales,

Josts Engineering Company Limited

6

Engineering products registered healthy growth at

7%, with strongest growth in South

Regional growth – All respondents1

West:

6% (8%)

South:

9%

(5%)

North:

5% (4%)

East:

8% (5%)

Peer growth comparison

Value growth (%)

-16

-12

-8

-4

0

4

8

12

16

20

-4 0 4 8 12 16 20

Volume growth (%)

• Sector slowed slightly over October with growth at 7% as

compared to 10% in September and August

• External trade data for October shows exports rise

almost 10% and imports increase 8%; gold imports up

108%, YoY

• Sentiments of survey respondents:

< 500 cr

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. MHE – Material handling equipments. Source: CII BCG Growth Index Survey

Value

growth yoy

Volume

growth yoy

Region

xx:

xx% (yy%)

All industry average

"Positive sentiment but still missing GCF growth esp

Private capex . Rural consumption (is) seeing slow pickup

but still not strong .Govt capex and consumption in urban

(areas is) currently driving growth. Manufacturing growth is

still visible enough to confirm growth is back" – Mr.

Ravichandran, President, Danfoss

7

Automotive components witnessed wide variance in

growth across companies and across regions

Regional growth – All respondents1

West:

-2.5% (2%)

South:

1%

(2%)

North:

0% (2%)

East:

-3.5% (3%)

Value growth (%)All industry average

-8

-4

0

4

8

12

16

-16 -12 -8 -4 0 4 8 12 16

Volume growth (%) < 500 cr

Peer growth comparison

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. No. of "visible" data points on the graph is less than the number of respondents due to overlaps. Source: CII BCG Growth Index Survey

Value

growth yoy

Volume

growth yoy

Region

xx:

xx% (yy%)

• Highest growth in revenue witness at ~7.5% while the

slowest growth at -12.5%. Volume growth ranged

between -7.5% to 12.5%.

• 2 Wheelers cashed in on the festive seasons as Royal

Enfield has registered a sales growth of 32% while India

Yamaha Motor has announced 22% rise in sales

• Sales of PV varied by manufacturer as TATA motors

(32%), Maruti Suzuki (2.2%) and Hyundai (6.4%) saw a

growth in sales, Honda (-23%), Toyota Kirloskar (-6%)

and Ford (-25%) saw a sharp dip in sales through

October 2016

8

Industry Deep Dives

9

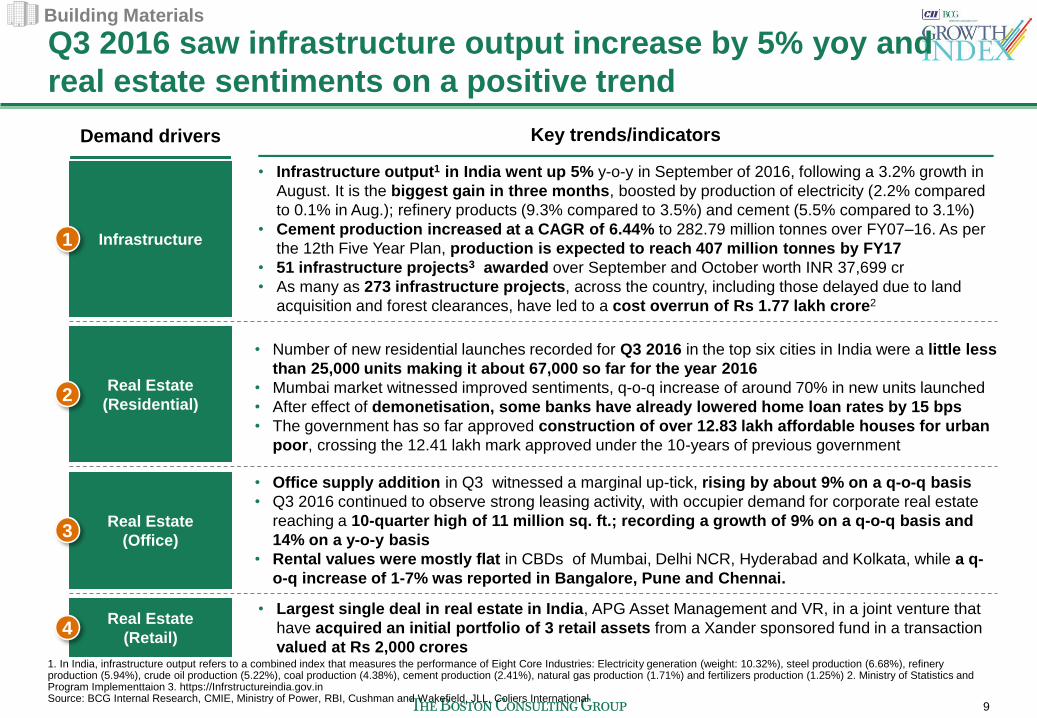

Q3 2016 saw infrastructure output increase by 5% yoy and

real estate sentiments on a positive trend

Demand drivers Key trends/indicators

Infrastructure

• Infrastructure output1 in India went up 5% y-o-y in September of 2016, following a 3.2% growth in

August. It is the biggest gain in three months, boosted by production of electricity (2.2% compared

to 0.1% in Aug.); refinery products (9.3% compared to 3.5%) and cement (5.5% compared to 3.1%)

• Cement production increased at a CAGR of 6.44% to 282.79 million tonnes over FY07–16. As per

the 12th Five Year Plan, production is expected to reach 407 million tonnes by FY17

• 51 infrastructure projects3 awarded over September and October worth INR 37,699 cr

• As many as 273 infrastructure projects, across the country, including those delayed due to land

acquisition and forest clearances, have led to a cost overrun of Rs 1.77 lakh crore2

Real Estate

(Residential)

• Number of new residential launches recorded for Q3 2016 in the top six cities in India were a little less

than 25,000 units making it about 67,000 so far for the year 2016

• Mumbai market witnessed improved sentiments, q-o-q increase of around 70% in new units launched

• After effect of demonetisation, some banks have already lowered home loan rates by 15 bps

• The government has so far approved construction of over 12.83 lakh affordable houses for urban

poor, crossing the 12.41 lakh mark approved under the 10-years of previous government

Real Estate

(Office)

• Office supply addition in Q3 witnessed a marginal up-tick, rising by about 9% on a q-o-q basis

• Q3 2016 continued to observe strong leasing activity, with occupier demand for corporate real estate

reaching a 10-quarter high of 11 million sq. ft.; recording a growth of 9% on a q-o-q basis and

14% on a y-o-y basis

• Rental values were mostly flat in CBDs of Mumbai, Delhi NCR, Hyderabad and Kolkata, while a q-

o-q increase of 1-7% was reported in Bangalore, Pune and Chennai.

1

2

3

Real Estate

(Retail)

• Largest single deal in real estate in India, APG Asset Management and VR, in a joint venture that

have acquired an initial portfolio of 3 retail assets from a Xander sponsored fund in a transaction

valued at Rs 2,000 crores4

1. In India, infrastructure output refers to a combined index that measures the performance of Eight Core Industries: Electricity generation (weight: 10.32%), steel production (6.68%), refinery production (5.94%), crude oil production (5.22%), coal production (4.38%), cement production (2.41%), natural gas production (1.71%) and fertilizers production (1.25%) 2. Ministry of Statistics and Program Implementtaion 3. https://Infrstructureindia.gov.inSource: BCG Internal Research, CMIE, Ministry of Power, RBI, Cushman and Wakefield, JLL, Coliers International

Building Materials

10

Construction sector going through a lull phase, though

projected to catch speed in next 4-6 quarters

0

1,000

2,000

3,000

0

2

4

6

8

10

INR Billion Percentage of Total Value Added

Q2’

17E

Q1

’17

Q4

’16

Q3

’16

Q2

’16

Q1

’16

Q4

’15

Q3

’15

Q2

’15

Q1

’15

Q4

’14

Q3

’14

Q2

’14

Q1

’14

+12%+5%

+6% +2%

Q4’

18E

Q3’

18E

Q2’

18E

Q1’

18E

Q4’

17E

Q3’

17E

Note: Data for Q2'17 onwards is projections based on growth rate for "Construction, Value-added output, real LCU" estimated by Oxford EconomicsSource: RBI, Oxford Economics, CMIE

Share in total value added has been decreasing since

Q2'15 while GFCF is consecutively fell for three quarters

Construction GDP showed flat growth Capital formation growth is

-5

0

5

10

15

Jan-16Jan-15Jan-14Jan-13Jan-12

GFCF Growth (YoY)

Building Materials

Projections

11

Credit deployment in infrastructure and construction

sector remains flat

5,992 6,045 5,799 5,382 5,386 5,288 5,245 5,217 5,178

1,789 1,7941,775

1,756 1,827 1,840 1,835 1,603 1,640

1,165 1,1661,161

1,112 1,109 1,102 1,1381,038 1,044

937 939913

941 951 910 883840 851

739 746745

787 766 755 758719 725

0

3,000

6,000

9,000

12,000

Apr-16Mar-16Feb-16

INR Bn

Jul-16May-16 Aug-16Jan-16 Jun-16

-16%

Sep-16

TelecomConstruction Other Infrastructure PowerRoads

Note: Includes repayments as wellSource: RBI

Infrastructure

Other

Construction

Building Materials

12

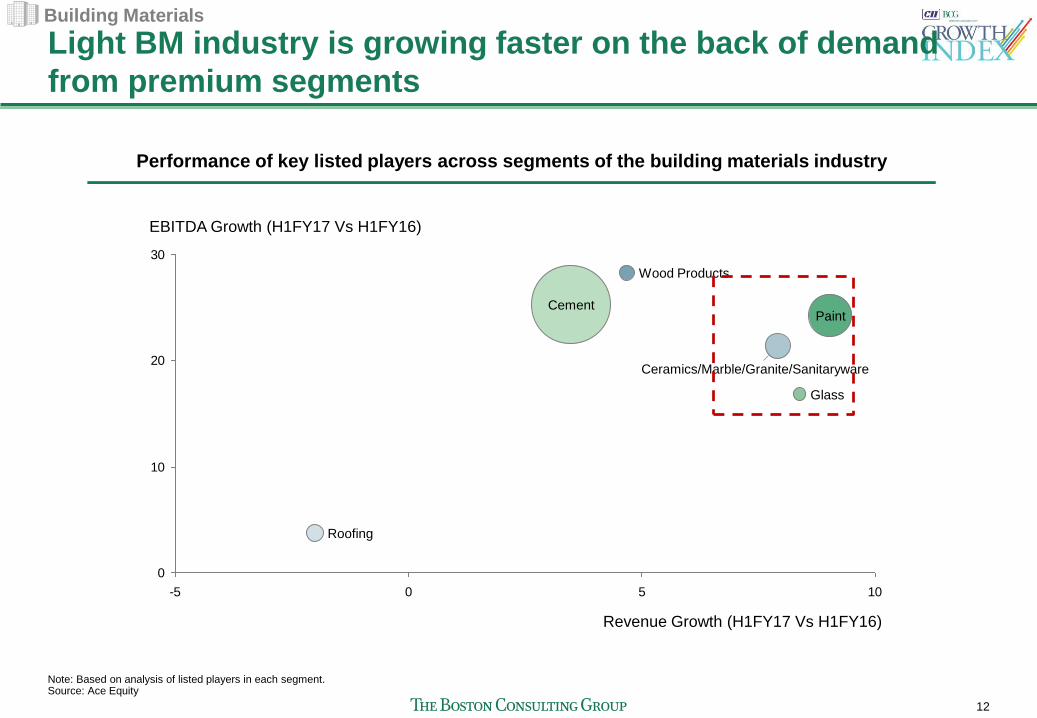

Light BM industry is growing faster on the back of demand

from premium segments

0

10

20

30

-5 0 5 10

Paint

Wood Products

Cement

Glass

EBITDA Growth (H1FY17 Vs H1FY16)

Roofing

Revenue Growth (H1FY17 Vs H1FY16)

Ceramics/Marble/Granite/Sanitaryware

Note: Based on analysis of listed players in each segment.Source: Ace Equity

Building Materials

Performance of key listed players across segments of the building materials industry

13

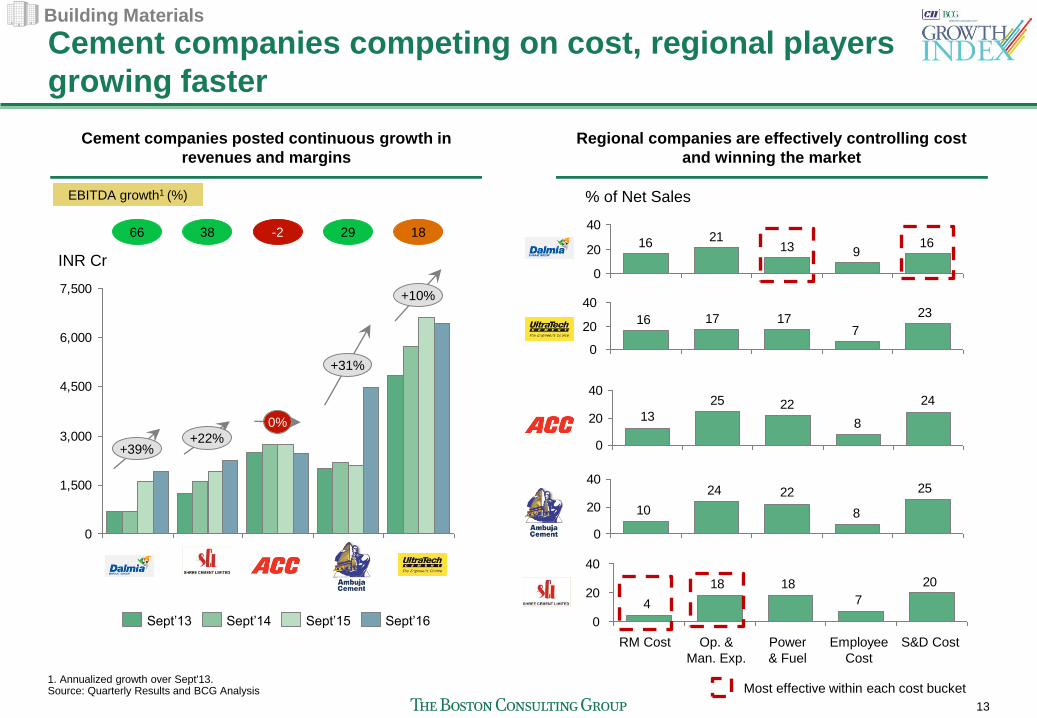

Cement companies competing on cost, regional players

growing faster

0

1,500

3,000

4,500

6,000

7,500

INR Cr

+39%+22%

+31%

+10%

0%

Sept’13 Sept’14 Sept’16Sept’15

1. Annualized growth over Sept'13. Source: Quarterly Results and BCG Analysis

Cement companies posted continuous growth in

revenues and margins

66 38 -2 1829

Regional companies are effectively controlling cost

and winning the market

16913

2116

0

20

40

% of Net Sales

23

7171716

0

20

40

24

8

2225

13

0

20

40

25

8

2224

10

0

20

40

20

7

1818

4

0

20

40

RM Cost Employee

Cost

S&D CostOp. &

Man. Exp.

Power

& Fuel

EBITDA growth1 (%)

Building Materials

Most effective within each cost bucket

14

Paint companies generated high EBITDA but sales

remained under pressure

4,000

3,500

1,000

500

0

INR Cr

+6%

+6%+9%

+6%

-5%

Sept’16Sept’15Sept’14Sept’13

1. Annualized growth over Sept'13.Source: Quarterly Results and BCG Analysis

Paint companies have shown subdued sales growth

but higher EBITDA

EBITDA growth1 (%)

13 21 1235

Cost structure is almost same for all leading players,

Nerolac effectively controls non-RM cost

818

56

0

50

100

% of Net Sales

722

56

0

50

100

518

57

0

50

100

1026

56

0

50

100

-8

816

57

0

50

100

Employee CostOp. & Man. Exp.RM Cost

Building Materials

Most effective within each cost bucket

15

Roofing companies benefitted by higher demand and

increased focus on cost control

0

100

200

300

+3%-3%

INR Cr

+27% +24%

-21%

Sept’16Sept’15Sept’14Sept’13

Note: Sept'16 data is not available for Ramco Ind, hence, taken June'161. Annualized growth over Sept'13.Source: Quarterly Results and BCG Analysis

De-growth for some over H1 FY 17 while 2 of the top 5

firms witnessed >20% growth in the same period

-12 48 24 6516

Cost control is key in a hyper competitive market, RM

costs almost 50% of total cost base for most

1538

51

0

50

100

% of Net Sales

142651

0

50

100

824

60

0

25

50

75

720

54

0

20

40

60

9

3444

0

20

40

60

Employee CostOp. & Man. Exp.RM Cost

EBITDA growth1 (%)

Building Materials

Most effective within each cost bucket

16

Automotive industry continued to grow on the account

of new models and festive season

• PV industry grew by ~4.5% with auto

makers resorting to inventory

correction after pushing stocks in the

previous month ahead of festive

season

• Maruti's UV segment witnessed a

growth of 90.9% YoY (down 2.3%

MoM), supported by newly launched

Brezza, S-Cross and Ertiga upgrade

• Tata's volumes grew on back of

robust performance by Tiago

• CV segment touched double digit

growth (11.9% YoY)

• Tata's domestic M&HCV sales

Domestic volumes ended the four-

month losing streak, growing 9%

YoY in October

• Ashok Leyland has posted 36%

growth YoY in MHC&V segment on

a lower base of Oct-15 due to pre-

buying in Aug/Sep-15 (driven by

change in emission norms from Oct-

15)

Value growth (%)All industry average

-40

-20

0

20

40

60

80

-40 -20 0 20 40 60 80

Volume growth (%)

Value growth (%)All industry average

-10

0

10

20

30

40

200 4-4 128 16 24 28 32 36

Volume growth (%)

Value growth (%)All industry average

-75

-50

-25

0

25

50

75

100

125

0-75 -50 -25 25 50 75 100 125

Volume growth (%)

• Festive season fuelled the growth of

2 wheeler segment – grew by 9%

• Piaggio's sales doubled on YoY

basis on a lower base of 2,800 units

in Oct-15

• Royal Enfield continued to grow at

the rate of 30%+ on YoY basis

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Revenue size of the companies not represented in the graph Source: CII BCG Growth Index Survey, Industry association data on automotive sales

Passenger vehicle (PV) Commercial vehicle (CV) 2-wheelers

Automobile and Auto Components

17

Premium and Mini passenger vehicle segments drive

growth in the sector

SegmentSegment Size &

Growth (FY 2017)Key Players and Market shares Key trends

Mini

Domestic Sales

Growth

338K

14%

Maruti

Hyundai

Renault

71%

9%

19%

• Maruti lost 14% market share; Alto and Wagon R sales down by 9.8%

• Renault gained 17% market share with its new entrant Kwid

Compact

Domestic Sales

Growth

732K

5%

Maruti

Hyundai

Tata Motors

Honda

45%

27%

10%

5%

• Sales across manufacturers remain consistent since FY 16

• Honda's market share dropped by 4% as its new hatchbacks, Jazz, Brio

and Amaze failed to impress the markets

Mid-size

Domestic Sales

Growth

96K

-10%

Maruti

Hyundai

Renault

Honda

40%

11%

5%

35%

• Maruti gained 12% market shared since FY 16

• Hyundai and Toyota maintained their market share with only marginal

movement

• Honda's share reduced by 8% from 43% to 35% in FY 17

Executive

Domestic Sales

Growth

7.8K

-21%

Toyota

Hyundai

GM

Volkswagen

Skoda

41%

15%

7%

10%

19%

• Toyota Corolla leads the market with 41% steady market share since FY 16

• Hyundai's Elantra maintains its market share at 15%

• GM sees 3% gain in market share through its Optra and Cruz models

• Volkswagen's Jetta loses 4% market share over the recent controversies

• Skoda's Laura and Octavia help gain 2% market share in FY 17

PremiumDomestic Sales

Growth

2.2K

58%

Skoda

Toyota

57%

39%

• Skoda gained 13% market share as sales for Superb doubles since FY 16

• Toyota lost 17% market share primarily due to drop in Camry sales

Note: YOY Growth is over FY 16Source: CRISIL Reports, SIAM, BCG analysis

Automobile and Auto Components

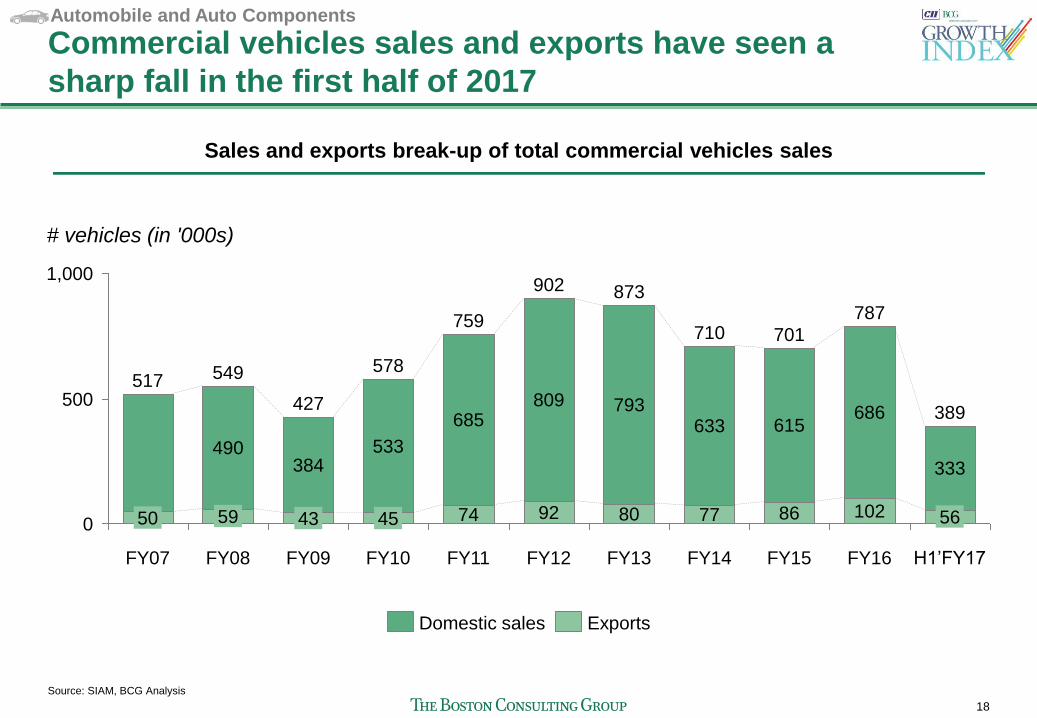

18

Commercial vehicles sales and exports have seen a

sharp fall in the first half of 2017

0

1,000

500

# vehicles (in '000s)

56

FY16

787

102

686

FY15

701

86

615

FY14

710

77

633

FY13

873

80

793

FY12

902

92

809

FY11

759

74

685

FY10

578

45

533

FY09

427

43

384

FY08

549

59

490

FY07

517

50

333

H1’FY17

389

ExportsDomestic sales

Sales and exports break-up of total commercial vehicles sales

Source: SIAM, BCG Analysis

Automobile and Auto Components

19

Commercial vehicle sales

Overall economic indicators: October 2016 review

Passenger vehicle sales

20

40

0

80

60

'000

Oct-

16

66

+21%

Sep-1

6

62

Aug-1

6

53

Jul-16

52

Jun-1

6

56

May-

16

Jan-1

6

62

Dec-1

5

57

Nov-1

5

59

Oct-

15

59

Sep-1

5

Mar-

16

Aug-1

5

52

Jul-15

52

54

80

Apr-

16

57

+6%

Feb-1

6

62

63

0

200

50

100

150

250

300

260

Jun-1

6

223

May-

16

232

Apr-

16

242

Mar-

16

281

Feb-1

6

234

Jan-1

6

232

Dec-1

5

231

Nov-1

5

252

Oct-

15

269

Sep-1

5

232

Aug-1

5

'000

Jul-15

222

Oct-

16

+17%

Sep-1

6

257 278

Aug-1

6

+1%

259

Jul-16

222

Latest

month

Previous

month

Growth Indices

IIP (%)7

(y-o-y)

Steel production (Mn Tn)1

CV Auto vol growth8 (%)

(y-o-y)

Cement production (Mn Tn)1

Energy req growth1 (%)

(y-o-y)

PV Auto vol growth8 (%)

(y-o-y)

0.7

22.6

4.0

11.9

7.8

4.5

(0.7)

22.3

1.0

1.5

8.6

16.3

Select industry metrics

Economy statistics

FII flows (US$ Mn)3

FDI flows (US$ Mn)4

Latest

month

Previous

month

NRI deposits (US$ Bn)2

Forex reserves (US$ Bn)3

Currency competitiveness6

Balance of payment measures

(644)

4,743

130

367

66.6

China GDP growth est. (%)5 6.7 6.7Oil imports growth3 (%)1

(y-o-y) (8.5)3.9

Inflation – WPI (%)1 3.39 3.57Non-oil imports growth3 (%)1

(y-o-y) (14.9)(5.3)

1,567

4,338

129

370

66.7

BSE Sensex6 27,930 27,866 Trade deficit (US$ Bn) 3 (7.7)(8.3)

India GDP growth est. (%)5 7.1 7.9Exports growth3 (%)1

(y-o-y)1.24.7

Capital account

Current account

*Not comparable as one of the data 1. As of Sept and Aug 2. Total outstanding values as of Sept and Aug 3. For Aug and July. Includes only equity flows. 4. As of end Aug and Jul 5. Average of GDP estimates for FY16-17 for China and India made by leading international financial institutions in Sep & Aug 6.As in Sep & Aug 7. As of Sept and Aug 8. As of Oct and Sept Note: PV and CV refer to passenger and commercial vehicles resp. Source: RBI, Thomson One, Ministry of Finance monthly Report, Capitaline, EIS, BCG analysis, Press Search.

Thank you

bcg.com | bcgperspectives.com