moving to museum trusts - egeria

TRANSCRIPT

Moving to Museum Trusts: Learning from Experience

Advice to Museums in England & Wales

Part 1: Strategic Overview Adrian Babbidge, Egeria with Rosemary Ewles, Egeria Julian Smith, Farrer & Co

Museums, Libraries and Archives Council Victoria House Southampton Row London WC1B 4EA © MLA 2006 ‘Historical Background’ and ‘The First Devolutions’ in Chapter 1.2 and the Annex to this report includes material previously published as Charitable Status for Museums © 1998 Adrian Babbidge The rights of Adrian Babbidge. Rosemary Ewles and Julian Smith to be identified as the authors of this work have been asserted by them in accordance with the Copyright, Designs and Patents Act 1985 MLA is the national development agency for museums, archives and libraries, advising the government on policy and priorities for the sector. Our mission is to enable the collections and services of museums, archives and libraries to touch the lives of everyone. MLA is a Non-Departmental Public Body sponsored by the Department for Culture, Media and Sport. A CIP catalogue record of this publication is available from the British Library ISBN 1-903743-93-1 MLA is not responsible for views expressed by consultants or those cited from other sources. This report is intended for guidance only and is not a substitute for professional advice. No responsibility for loss occasioned as a result of any person acting for failing to act can be accepted by MLA or the authors. It does not fully include any changes in the law after 1 January 2006.

CONTENTS

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview ii

Executive Summary 1 Summary of Recommendations 6 1 Introduction 10 Background to the Study 100 Scope & Definition 11 Organisation of the Report 12 Methodology 13 Acknowledgments 13 2 Context & Trends 15 Organisational Basis 15 Historical Background 15 The First Devolutions 18 Public Managerialism & Museum Trusts 21 New Labour & Best Value 22 Local Government in 2006 25 The Future 26 Museums Trusts in Other Countries 27 3 Options for Service Delivery 29 Options Adopted 30 Change Outcomes other than Devolution 32 o Joint Arrangements 32 o Contracting-out 33 o Outsourcing to a Non-Profit-Distributing Organisation 34 o Outsourcing to an Independent Museum 35 Museum Development Trusts and Friends Organisations 35 Transfers from Charities to Local Authority Museums 36 University Museums 38 4 The Devolved Museums 39 Allerdale Borough Council: The Helena Thompson Museum 41 Bexley London Borough: Bexley Museum Trust 43 Birmingham City Council: Thinktank 46 Bolton Metropolitan Borough Council: Smithills Hall 48 Braintree District Council: Braintree District Museum 49 Cheltenham Borough Council: Holst Birthplace Trust 51 Chichester District Council: Pallant House Gallery 53 Coventry City Council: Coventry Transport Museum 56 Dacorum Borough Council: Dacorum Heritage Trust 58 Denbighshire County Council: Bodelwyddan Castle 59 Dudley Metropolitan Borough Council: Black Country Museum 63 Durham County Council: The Bowes Museum 66 Harrow London Borough: Headstone Manor Museum 70 Inner London Education Authority: Geffrye & Horniman Museums 71 Kent County Council: Museum of Kent Life 72 Sheffield City Council: Sheffield Industrial Museums Trust and 74

Sheffield Galleries & Museum Trust o Sheffield Industrial Museums Trust 75 o Sheffield Galleries & Museum Trust 78 o Sheffield Outcomes 81 Southwark London Borough: South London Gallery 82 St Helens Metropolitan Borough Council: The World of Glass 84 Torfaen County Borough Council: Torfaen Museum Trust 85 Waverley Borough Council: Godalming Museum 87 West Dorset District Council: Bridport Museum 91 York City Council: York Museums Trust 92 5 Lessons Learnt & Issues Raised 98 General Characteristics 98 The Review Process 99 Culture/Leisure Trusts 99 Legalities of Transfer 100 The Voluntary Sector Compact 102 Partial Transfers & Hybrids 103 Funding Agreements & Timeliness 103 The Change Process 104 Boards & Trustees 108 o The Chair 108 o Board Size & Committees 109 o Board Recruitment 111 o Board Remuneration 111 Recruitment of Directors/Chief Executives 112 Relationships with Core Funders 112 Annual Reports 114 Publication of Information 115 Pensions 116 Networking 117 Partnerships & Synergies 118 ‘Stabilisation’ 119 When Things Go Wrong: Case Study 120 Museum Trusts: A Successful Approach ? 122 Annex: Constitutional Forms of Outsourced Organisations 126 o The Industrial & Provident Societies 126 o The Charitable Trust 126 o The Charitable Company Limited by Guarantee 126 o The Non-Charitable Company Limited by Guarantee 128 o The Company Limited by Shares 128 o The Community Interest Company 129 o The Charitable Incorporated Organisation 129 Bibliography 130 Appendix A: Membership of Steering Group 135 Appendix B: List of Consultees 135

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview iii

EXECUTIVE SUMMARY 1. This report focuses on museums that have been ‘devolved’ by local authorities.

They are distinguished by the following characteristics:

a) they are charitable bodies (‘museum trusts’) specially created to deliver a local authority’s museums services, with the intention of a long-term relationship between the council and the museum trust;

b) all the council’s museum responsibilities (including strategic planning)

are transferred, not only day-to-day management responsibilities; and

c) there is a sharing of risk between the council and the museum trust.

2 Although the period since 1975 has seen substantial discussion about the benefits and disadvantages of devolving public authority museums, the number of occasions when this has taken place is few. However, the idea has recently acquired a new impetus - of the 23 devolutions in England and Wales, more than half have taken place during the past ten years, and others are in train. In only one case has the position been reversed. Devolutions have taken place in museums of all sizes and scales, with eleven having incomes of under £1 million, and six over £2 million.

3 All these devolutions are from local authorities. Universities – which like local

authorities are conglomerate organisations – have found them irrelevant, as universities already benefit from the fiscal benefits that come to charities, and devolution would risk divorcing them from the Arts and Humanities Research Council, their main funding stream. In organisational terms, university museums often have their own committees or influential supporters who act as their advocates both in the university and without. The reality is that in many cases the museum is already at arm’s length from its sponsoring university - the challenge is to reduce the risk of drifting apart from the main funder, an issue also for museums that have been devolved for some time.

4 Museum trusts have not been the only destinations for museums that have

moved out of local authorities. Others have been:

National museums (Merseyside County Museums became what is now National Museums Liverpool);

Joint Committees (such as those for Tyne and Wear Museums, the North

of England Open Air Museum at Beamish, and for a number of the museums operated by the Hampshire County Museums Service);

the private sector (eg at Weymouth and Walsall); and

outsourcing to an existing independent museum/heritage organisation (eg

West Park Museum at Macclesfield to Macclesfield Museum Trust and

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 1

Baysgarth House Museum in North Lincolnshire to Barton on Humber Community Heritage Arts and Media Partnership).

5 Only rarely do the reasons for devolutions appear to have derived from a wish

to improve service to the public, or a museum’s efficiency and effectiveness. Usually the causes given were:

a) to develop a newly-established museum service or capital project (while

common in the 1970s and 1980s, this is becoming increasingly infrequent);

b) as a response to funding difficulties (an increasingly frequent

circumstance);

c) as a consequence of pressure from the Arts Council and its Stabilisation Scheme;

d) as an outcome of a Best Value review; or

e) as a consequence of moves to rationalise a service’s branch museums.

6 The general advantages experienced by the devolved museum trusts are

reported to be:

a) a sense of direction, freed from the wider corporate issues of local authorities and the ability to focus on their core business;

b) flexibilities and freedoms to establish plans and policies appropriate to the need of current and potential audiences and users as well as stakeholders;

c) management structures that enable timely decisions at the most appropriate operational level;

d) a sustainable framework, based on funding arrangements that create a stable basis for business planning and development;

e) the opportunity for cultural change in the museum organisation;

f) opportunities to benefit from the fiscal advantages of charitable status and to increase income through commercial activity and sponsorship;

g) opportunities to make new connections and develop new partnerships

(both in the museum sector and outside) relevant to the museum’s core purpose; and

h) a greater attractiveness to donors or persons considering long-term loans

of collections.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 2

7 The contrast between the reasons for change and the advantages cited as a consequence suggests that many organisations began the process with very little idea of the positive outcomes that might emerge. On the one hand this may represent museums wearied by a process of continuous internal restructurings and reorganisations; or, on the other, it may represent a lack of ambition for improvement in local authorities and/or their museum services.

8 Where, following review, devolutions did not take place, the reasons normally

given are:

a) Strategic

1) it was believed that other means (such as a major Lottery project) would transform the museum;

2) the museum was perceived to be ‘working well’, so there was no

reason to change;

b) Political

1) there was principled political hostility to ‘hiving off’ services;

2) stakeholders (especially trades unions) were opposed to what was regarded as ‘privatisation’;

c) Emotional

1) devolution being perceived as ‘selling the family silver’.

d) Practical

1) there was no substantial and immediate financial incentive to devolve;

2) previous devolutions had led to financial or organisational difficulties for the council;

3) the council’s internal advice had presented legal obstacles;

4) there was no political or management impetus from within the council;

5) change in key personnel (whether political leadership or senior

management) stifled the process of change;

6) the council/museum claimed insufficient capacity or resources, whether to undertake a comprehensive review or manage the devolution process; and

7) the vested interests of museum staff (especially heads of service) who

feared loss of job or working arrangements) or council corporate or

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 3

back-office functions who feared the impact of change on their operations and cost-base.

9 In most cases there was no single reason for lack of change. In some cases there was a difference between ‘official’ and ‘real’ reasons. Where devolutions did occur, key factors appear to have been:

a) champions within the council at Elected Member, Corporate Director or

Head of Museum Service level (experience suggests change requires champions at two of these three levels as a minimum);

b) an external stimulus – though not essential, strong advocacy for the

museum from the local community facilitates the process; and c) self-confidence within both council and museum that the result would lead

to a substantial improvement.

10 Where devolutions did occur, they were of the following types:

a) full – where the museum/service is transferred as a going concern, with all its assets, to a museum trust; or

b) hybrid – where responsibility is devolved to a museum trust, as are some

assets, but others are retained by the Council (eg staff remaining part of the council and seconded to the museum trust).

11 Some museums have been transferred (or are in the process of transferring)

to ‘culture/leisure trusts’ which embrace a wider range of cultural activities, and this route is also being considered for others. While the benefits of a strategic approach to cultural policy is self-evident, whether there is advantage in translating this into operational arrangements is open to doubt. Generally, the relatively small scale of museum operations within the culture/leisure trust’s operations transplant the difficulties they face within local authorities, while making advocacy to the funding body more difficult.

12 Local authorities are unlikely to make any immediate and substantial financial

benefits from devolution. In terms of Gershon, the process generates ‘non-cashable’ efficiencies. Given that few museum services are generously funded, they are (at least initially) unlikely to require less funding under devolved arrangements than when they were delivered directly; indeed, there may be an immediate need for some additional investment to compensate for deferred building maintenance. In the longer term, reduction of local authority funding may compromise the museum trust’s financial viability. Rather than immediate financial savings, key objectives for devolution should be the intention to:

a) develop the museum service and continuously improve its quality, in line

with the philosophy of Best Value ;

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 4

b) undertake significant investment in the museums service and access additional funding;

c) promote and market the museum service to an expanded market;

d) provide accountability to the community on whose behalf the museum

holds the collections, responding to user needs;

e) provide an economically-viable future for the museum, based on robust business planning; and

f) widen the financial support for the museum within the community.

13 Devolved museums have usually been incorporated as charitable companies limited by guarantee, governed by boards of between five and fifteen members, of which up to 20% are nominated by the core-funding local authority. There is some evidence that the size and composition of boards is leading to two tiers of trustees – those that are members of an executive committee who participate in the museum’s governance, and a larger group who meet less frequently and who discharge what is a scrutiny rather than a governance role.

14 Having a ‘two tier’ board of trustees can be undesirable and smaller boards

might well represent a better way of working. If a need is felt for greater contact with stakeholders, or for a larger forum for consultation and discussion, then it is always open to create an ‘advisory council’ which can provide an opportunity for debate, discussion and consultation, without the need to compromise the effectiveness and efficiency of the museum’s board. Whatever structure is preferred, it is essential that corporate governance arrangements are defined and formally agreed by the trustees, and supported by appropriate systems and processes.

15 Lacking any generally-accepted consensus of what constitutes ‘a successful

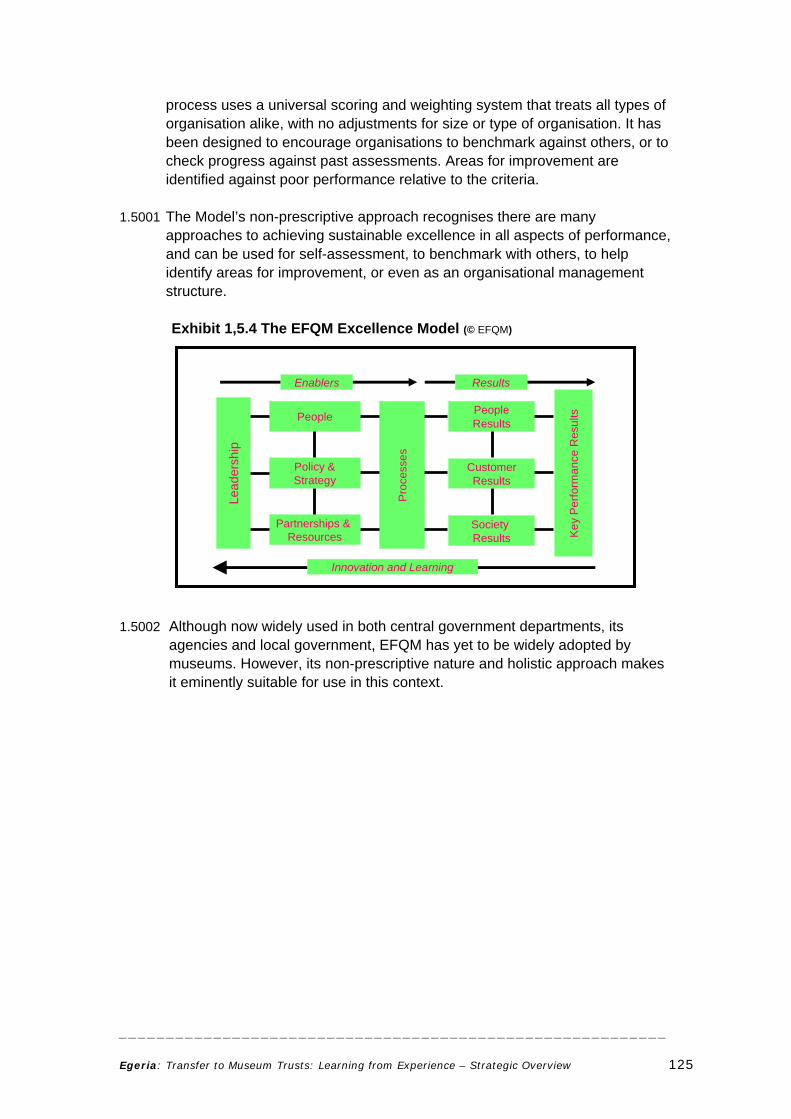

museum’, it is difficult to say with confidence that devolved museums are any more successful than those that have remained within local authorities. Devolution in itself is no guarantee of better governance or management. The museum sector lacks easily-verified and reported measures that connect with museums’ missions and core values, and incorporate reliable indicators of long-term organisational and financial health. Very few museums have made use of holistic models, such as the European Foundation for Quality Management (EFQM) Model.

16 Additionally, the following general points can be made:

a) There is no single, shared Business/Operating Model common to all devolved museums, the balance between earning income from visitors, winning grant funding, and commercial development differs from museum to museum.

b) Devolved museums have performed well in attracting additional funding,

though most of this comes from public funding sources available to other __________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 5

museums, and it appears that relatively little effort has been put into cultivating potential private donors, which has a longer lead-time and where benefits are less immediate.

c) They are generally responsive and entrepreneurial, though many have

created new bureaucracies to replace those of their local authority predecessors. Their external funding bodies have their own reporting requirements which can prove onerous.

17 The risks faced by the devolved museums are:

a) the risk of over-rapid growth that takes the museum beyond the levels where it can be sustained by its Business/Operating Model;

b) stagnation of core funding increasing the income required from other

sources beyond realistically-achievable levels; c) over-reliance on external project funding which places areas of activity at

risk when that funding dries up; d) a change of political philosophy within the local authority that requires an

end of devolved arrangements and return of services to direct delivery; e) changes in taxation (and especially in VAT) which inadvertently place

pressure on free-admission museums; f) increasing pension liabilities compromising the museum’s core budget; g) the inability of the museum to recruit high-calibre trustees to replace the

founding board or senior management; and h) poor quality internal audit, regulatory and reporting structures.

Summary of Recommendations 18 The following recommendations are made as a result of this study: Reviews

a) While good governance requires that regular structural reviews be undertaken to ensure that local authority museum services are delivered in the most effective and efficient manner, this needs to be balanced with the impact of conducting such reviews on operations and opportunities. It is RECOMMENDED that :

(1) there should be five clear years between the end of one review

and the start of the next, and that reviews should be conducted in a timely way that places the minimum disruption on services; and

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 6

(2) reviews should be thorough, strategic assessments with terms of reference that take into account all those factors associated with best value and improving customer service, not merely financial savings, identifying both cashable and non-cashable efficiencies; and

(3) the results of reviews should be published, and the reasons for the

option selected, and the evidence that led to that conclusion, clearly stated.

b) Reviews should give thorough consideration to the range of options for

delivering museum services, which will sometimes include a single not-for-profit organisation that will incorporate all an authority’s cultural services. It is RECOMMENDED that, in considering outsourcing to culture/leisure trusts, the proposed arrangements should provide both local authorities and their museums with an equivalent, or greater, advantage than would come from devolving their museum services on a separate basis.

The Process of Devolution c) While recognising that local circumstances differ, it is RECOMMENDED

that: the relationship between councils and devolved museums should be encapsulated in a formal legal document that:

(1) has a defined term of not less than three years; (2) indicates the funding that the council will make available

throughout that period, and when and how it will be paid; (3) defines the services the museum trust will provide in return for the

grant, and how this is to be reported to the council; (4) specifies any obligations on the council (eg building maintenance

and meeting insurance costs); (5) defines in precise terms the defaults on both sides that would lead

to termination before the end of the agreement, indicating where liabilities would lie; and

(6) agrees the process at the end of the agreement, whether a timely

negotiated renewal procedure or a reversion to the council at its cost.

d) It is RECOMMENDED that partial transfers should only be considered in

exceptional circumstances where some irresistible factor precludes full devolution.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 7

e) It is RECOMMENDED that all relationships between councils and museum trusts comply with The Compact on Relations between the Government and the Voluntary and Community Sectors, and its counterpart Local Compacts.

f) It is RECOMMENDED that, where local authorities agree to devolve their

museum services, sufficient resources should be made available to ensure that the Shadow Board of the newly-formed museum trust is able to access its own advice and support, and the council should indemnify the Shadow Board so that no liabilities fall on its members in the event of the devolution not taking place.

g) The legal costs of drafting appropriate legal documentation is substantial,

and if this process is gone through in every case there is a substantial duplication of expenditure from public funds. It is RECOMMENDED that MLA commission model documentation (including governing instruments, funding, transfer and collections agreements). So to do would relieve the costs on public funds, facilitate the process of implementation, and embed good practice.

Corporate Governance h) It is RECOMMENDED that local authority nominees to boards of trustees,

or chairs of museum trusts who are local authority nominees, should not be replaced on a change of political control in the council, and should serve the remainder of their full term of office. Accountability should be exercised by other means, such as Funding Agreements.

i) While there is a need for a small Shadow Board during the

implementation process, this group should not thereafter become embedded as an executive committee. It is RECOMMENDED that the governance of museum boards should rest, in practice as well as constitutionally, in the hands of boards as a whole, and that board composition and membership should be designed to enable this to happen. It is further RECOMMENDED that all museum trusts should have audit committees to scrutinise both audit arrangements and financial processes/systems within the museum trust, the membership of which should not include office-holders.

j) Charity annual reports and financial information are now more widely

available than ever before. The Charities SORP 2005 requires a common standard of reporting from all charities. It is RECOMMENDED that all museum trusts, in meeting those requirements, provide key performance information in absolute terms, and indicate trends over recent years. It is further RECOMMENDED that DCMS and MLA produce guidance on the reporting and accounting requirements related to the SORP, with the intention of providing common practice within the museum sector that enables greater comparability between accounts.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 8

k) It is RECOMMENDED that all museum trusts should have formal schemes for reporting their work to their sponsoring council, and that responsibility for discharging this role should fall on the chair and board (with the chief executive in support) rather than on the chief executive and senior management acting on behalf of the board;

l) It is RECOMMENDED that all museums trusts should encourage a culture

of openness and follow good practice in providing public access about the relationship with their sponsoring local authority, their governance and performance, using their website and through other means to disseminate such information.

Management m) In view of increasing difficulties in recruiting candidates of calibre to head

museum trusts, it is RECOMMENDED that MLA should investigate whether the nature of entry-level job descriptions and specifications discourage the recruitment and retention of people with the aptitude, skills, temperament and acumen necessary to manage museums on a business-like basis.

n) The national difficulties over pension provision affect museum trusts as

much as any other part of society. It is particularly important that museum trusts should be seen to have fair personnel practices. It is RECOMMENDED that:

(1) all museum trusts that adopt pension schemes other than the

Local Government Pension Scheme should provide details of that scheme with the details sent to all potential job applicants, indicating how it differs from the LGPS; and

(2) the Museums Association and Association of Independent

Museums investigate the viability of a multi-employer pension scheme, whether operated by the Pensions Trust or a commercial provider.

o) It is RECOMMENDED that the Museums Association and/or the

Association of Independent Museums should consider providing network events for informal exchange of experience and information specific to devolved museums.

Funding

p) While museum trusts have been successful in bids for public funding,

efforts to attract private and philanthropic giving have been more modest. It is RECOMMENDED that museum trusts develop long-term strategies to cultivate private and commercial donors to supplement funding from public sources.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 9

CHAPTER 1.1 – INTRODUCTION Background to the Study 1.101 In the summer of 2003, the (then) Chief Secretary to the Treasury, Paul

Boateng MP, invited Sir Nicholas Goodison, ‘to review the effectiveness and efficiency of support to regional and national museums and galleries to help them acquire works of art and culture of distinction that might otherwise be sold abroad, and to make those items accessible to the public.’ His report (Goodison, 2004, 18) stated:

‘Some museums financed by local authorities have set themselves up

as charitable trusts or companies limited by guarantee. There are three advantages, it seems to me, of doing this. First, it can transform the leadership of a museum because experienced and well-connected trustees can extend the museum’s contacts, bring management and strategic skills, and give guidance and advice to the director and staff. Second, it can release energy and enthusiasm, because the director and staff are no longer part of the local authority’s hierarchy but answerable to the trustees. Third, it can improve money-raising prospects, because it is more likely that private and charitable donors will give to a charitable trust than to a local authority. I hope that other local authorities and museums, including university museums, will be inclined to study the examples set by Sheffield, York and the Bowes Museum and consider whether it could be advantageous for them to follow suit.’

1.102 These observations led to Sir Nicholas recommending that the Museums,

Libraries and Archives Council (MLA) should make available to other local authorities and museums a summary of the means by which museum trusts were set up, their reasons for doing it, their agreements for continued local authority or other public funding, and their experience as independent entities since they were set up.

1.103 MLA and its regional agencies were already receiving frequent requests for

advice from local authorities reviewing future arrangements for governing and managing their museums, and in particular trust status. We have therefore been commissioned to undertake a study that provides both a strategic assessment of the issue, and practical advice for those local authorities that are considering this option.

1.104 We have also been asked to make recommendations based on identification

of the strengths and weaknesses of trust governance in relation to other options, giving special attention to practical issues connected with funding, trustee recruitment and longer-term sustainability, and to identify any further work that may be necessary or desirable.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 10

Scope & Definitions

1.105 The study focuses on museums that have been ‘devolved’ by local authorities to organisations that have been specially created by the council for that purpose. This is in distinction to arrangements under which museums have been outsourced to an existing body which takes on that role in addition to other activities. Other forms of arm’s length delivery – joint arrangements with other local authorities, or outsourcing to commercial or community companies – are touched on solely for comparative purposes, though some issues dealt with will also be relevant to these other types of arrangement.

1.106 As defined in this study, devolved local authority museums are distinguished

by the following characteristics:

a) there is an intention of a long-term relationship between the council and the museum trust;

b) all the council’s museum responsibilities (including strategic planning) is

transferred, not only day-to-day management responsibilities; and

c) there is a sharing of risk between the council and the museum trust - the trust takes the financial risks associated with its freedom of action, its trustees the reputational risks that would come with financial difficulties, and the council faces the financial and political risks that would arise should the trust fail and transfer back become necessary.

1.107 The geographic remit of our Report is limited to England and Wales. Since

Devolution in 1998 the Welsh Assembly Government has been the competent authority for local government in Wales. Where the position in Wales differs to that in England appropriate references are provided. Though many of the issues in the Report are applicable in Scotland and Northern Ireland, they fall under different legal arrangements. Some of the key issues relevant to the Scottish legal position have been dealt with elsewhere.1

1.108 The following conventions have been adopted throughout the Report:

The term ‘museum’ is taken to mean all those institutions (including art galleries) that meet the Museums Association’s definition of a museum, which is:

Museums enable people to explore collections for inspiration, learning and enjoyment. They are institutions that collect, safeguard and make accessible artefacts and specimens, which they hold in trust for society.

The term ‘museum trust’ is used in a loose sense to include any museum operated by an organisation whose primary purpose is the operation of a museum, and has been registered as a charity

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 11

1 Scottish Museums Council Local Authorities and Charitable Trusts (1997)

with the Charity Commission or with HM Revenue & Customs, rather than in the narrow sense of a charity created by Trust Deed. Its charitable status is implicit, in view of its role as a ‘trustee for society’, in the Museums Association’s definition.

‘Trustee’ is a member of the governing body of a museum trust,

whether or not titled as such. Organisation of the Report 1.109 The report is in two parts. Part I takes a strategic overview by:

reviewing the factors that have led to a change of status, whether from direct provision to trust, or from trust to direct provision, or to a decision to retain the status quo, in the context of government and other policy;

evaluating the experience of those former local authority museums that

have adopted the charitable trust style of governance;

assessing the overall impact of trust status, both financial and practical, on institutions where change has taken place; and

considering a methodology for the assessment of the effectiveness and

efficiency of such bodies in relation to other means of governance, in relation to what constitutes ‘a successful museum’.

1.110 It includes the following elements:

Chapter 2 describes the context and trends that have led to the devolution of local authority museums to charitable bodies, and why some authorities have not chosen to pursue this option;

Chapter 3 describes the options for service delivery by local authorities;

Chapter 4 provides case studies for museums that have moved to trust

status, comparing their fortunes with local authority and National museums, and includes a cautionary case study of how things can go wrong; and

Chapter 5 considers whether or not, or in what way, these devolutions

have been successful, including some consideration of what constitutes a successful museum.

1.111 Part 2 deals with the process of devolution, and is intended to provide

practical help and guidance for those considering transferring a museum from a local authority to a specially-created museum trust. It includes chapters that:

provide background information on charities, their application to museums

and the benefits of charitable status;

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 12

describe organisational issues concerning the process of transfer; and

explain the legal and practical issues relating to the process of transfer. Methodology 1.112 This report has been prepared using the following sources:

annual reports and financial statements of the devolved museums, whether at Companies House or the Central Register of Charities;

reports and committee papers of local authorities that have considered or

adopted the museum trust option;

Museum Registration returns held by MLA;

publications listed in the Bibliography; and

interviews, either in person or by telephone, or through discussion groups, with a sample of people who have gone through either service reviews or the devolution process, either recently or in the more distant past (these consultees are listed in Appendix B).

Acknowledgements 1.113 The report has been prepared and written by Adrian Babbidge, assisted by

Rosemary Ewles, and advised by Julian Smith of Farrer and Company who reviewed the legal content. He is grateful to:

the members of the study’s Steering Group, whose membership is listed

at Appendix A., and especially to David Uffindell, Export Licensing Manager at MLA, who managed for the project for MLA;

Emmeline Leary and Alex Roberts of MLA for making available Museum

Registration records since 1989, which provided a key information source;

Sir Nicholas Goodison, whose review initiated this study and who provided valuable comments on the draft report;

Janet Dawson, Fellow of the Institute of Pensions Management who

provided advice on pensions issues; and

the large number of people who have responded to requests for information and provided their experience and advice.

1.114 However, some institutions and individuals were not able to provide or (for

reasons of confidentiality or to protect their intellectual property) felt unable to share certain types of information. Normally we have been able to overcome

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 13

this difficulty by accessing that information through other public sources though, as a consequence, there may be some gaps.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 14

CHAPTER 1.2: CONTEXT & TRENDS

Organisational Basis

1.201 While the organisational structures of UK museums are far from

homogeneous, they invariably fall into one or other of the following two categories:

where the function of operating a museum is the primary purpose of the

parent organisation; or

where the museum’s operation sits alongside other functions within a larger conglomerate organisation that has broader aims and purposes.

1.202 The primary source of funding is not a determinant of organisational type.

Thus, in the UK, single purpose organisations embrace both large National museums core-funded by the State and small, volunteer-run, self-funding local museums. Conglomerate arrangements include museums run by local authorities, universities and charities, whether or not any form of subsidy from the parent body is required (though normally it is).

1.203 Yet, traditionally, UK museums have been classified on the basis of their

primary source of funding rather than by their organisational form. Until the 1970s museums other than those funded by the state, local government or universities were termed ‘private’, irrespective as to whether they were run for personal profit or were operated by charities. Yet charity is a term of art which indicates that the organisation’s activities are exclusively for the public benefit, and as a consequence are subject to regulation by the State. Museums have moved between the constituent parts of this broad definition of ‘public sector’ throughout their history.

Historical Background

1.204 While during the 17th and 18th centuries the first museums in the UK that were

open to the public were owned by either universities or private individuals, from the turn of the 18th and 19th centuries their development was heavily influenced by learned societies dedicated to the pursuit of knowledge. Many of these – such as the Royal Institution of Cornwall, the Yorkshire Philosophical Society and the Society of Antiquaries of Newcastle upon Tyne - established museums to house and display collections that were brought together by their members.

1.205 In the cities and towns – and especially in those that grew as a consequence

of the Industrial Revolution – museums were also a key element in the social movement for education, instruction and self-improvement. The Museums Act 1845 authorised the levying of rates to provide museums in places with a population of more than 10,000. This and subsequent enabling legislation

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 15

throughout the 19th century enabled a growth in municipal museums,2 based on an assertion of civic pride. However, even in some cities and large towns it was the founding learned society that funded and operated the local museum, an arrangement which in some cases lasted until the end of the 19th century, when their resources became insufficient to maintain the collections and buildings, and local authorities stepped in to sustain their achievements. As has been shown for Yorkshire3, while the need of the learned societies to divest themselves of what had become liabilities was common, the motivations of the civic authorities that accepted them varied according to local circumstances.

1.206 The passage of museums into local authority control characterised the cities

and larger towns rather than more rural areas where, until the County Councils’ legislation of the 1880s, local government lacked a comparable scale of resources. Thus, in these areas, learned societies continued to be the main providers of museums well into the twentieth century – a role that continues in counties such as Wiltshire, Dorset and Cornwall. However, for the first half of the twentieth century, the trend was for museums operated by learned societies and charities to move to local authority control.

1.207 While in some cases acquisition by the local authority led to the museums and

their collections becoming the council’s corporate property, this was not invariably the case. Occasionally (as is the case in of the Buckinghamshire County Museum at Aylesbury) the collections and the museum building that housed them were leased from the county society to the Council. Elsewhere (eg the Royal Scientific Institution at Bath, the Hertfordshire County Museum at St Albans (now the Museum of St Albans), and Newarke Houses Museum (at Leicester), the council became sole trustee of a charitable trust that either constituted the whole museum or collection or building within which the collections were housed.

1.208 In other cases a similar mechanism was adopted by benefactors wishing to

‘ring-fence’ their gift from the general assets of a local authority - for example the Russell Cotes Museum at Bournemouth and the Mappin Art Gallery at Sheffield. In the 1950s, the Army Museums Ogilby Trust (AMOT) encouraged the relocation of regimental museums to civilian (local authority) museums, with a purpose-designed Trust Deed providing oversight by the regiment and the means of ring-fencing its collections within the museum’s wider holdings.

1.209 However, this separate charitable status was rarely recognised by the outside

world (and sometimes not even by the local authority). Such museums were generally regarded as being operated by the local council, and local authority regimes came to characterise governance arrangements for local museums in England and Wales.

1.210 The framework for local government in England and Wales was laid by the

Municipal Corporations Act 1835, the Local Government Acts of 1888 and

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 16

2 For a general history of museums in the UK see Lewis (1984) 3 Davies (1989), 31 - 42

1894, and the London Council Act of 1899. The structure adopted by those Acts lasted until the Local Government Act 1972, which introduced a new system. Throughout this period, local authority museums (whether or not they were solely discharging charitable trusts) were generally constituted as council departments, with their directors/curators reporting to ‘museum committees’. The museum was in fact, a discrete local institution.

1.211 This changed following the 1972 Act, with the new councils heavily influenced

by the Bains Report.4 Rather than the professional units that typified the old local authorities, Bains advocated the role of chief executive as a leader supported by a senior management team, the need for a vision defining the purposes and policies of a council, the adoption of corporate management to secure integration between departments, and the creation of conglomerate departments that incorporated a range of linked activities.

1.212 Following the models illustrated in the report, museum committees ceased to

exist in favour of ‘recreation and leisure’ committees, museum heads lost their direct access to committees and found themselves (perhaps at second or third tier within the department) subordinate to Leisure Directors who only rarely came from a background that had given any experience of museums. While this gave some museums the opportunity to thrive through a more joined-up approach to cultural provision, and to benefit from synergies with other services (notably libraries and tourism), this was by no means the universal experience.

1.213 Meanwhile, the 1960s and 1970s saw a new generation of museums being

created, frequently in response to the rapid disappearance of some aspect of the nation’s industrial history. While many were supported by local authorities, they were largely driven by enthusiasts or community groups. With the Ironbridge Gorge Museum Trust as their prototype, they were invariably constituted as charities, and usually as companies limited by guarantee. Over time they became known as ‘independent museums’. All were reliant on plural funding. European structural funds and tourist board grants were major sources of capital finance; revenue costs were met by admission charges and trading income. The availability of labour through government job creation schemes provided opportunities for both operations and development. Voluntary workers also made a substantial contribution.

1.214 However, notwithstanding the success of these museums in raising funds

from a variety of sources, most relied on the support of public bodies (such as local authorities or new town development corporations), whether in cash or kind, to maintain their viability. Only a handful of public museums have ever been profitable in a strictly-commercial sense, and independent museums have generally depended on some sort of subsidy from public funds.

1.215 This new breed of Independent museums transformed the British museums

scene. With their customer focus, marketing skills and business flexibility – and the need to generate revenue to pay their way – they were in sharp

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 17

4 Bains (1972)

contrast to most local authority museums, which had seen little change - or investment - for decades. Local authority museum workers looked on the independent sector with a mixture of suspicion (believing that their commercial imperative was inconsistent with the public service ethos of museums) and envy (especially of the flexibility and public profile they enjoyed).

The First Devolutions

1.216 In 1976 (Sir) Neil Cossons, then Director of the Ironbridge Gorge Museum,

spoke at the Museums Association Conference in Bristol5. Having analysed what he regarded as the governance and management shortcomings of local authority museums, he suggested that they should be ‘hived off’ as charitable museums on the Ironbridge model. He suggested that the advantages of this for the museum would be:

a) a wholehearted belief in, and in working for, the museum’s best interests,

untrammeled by the larger corporate issues of the local authority;

b) freedom from local politics, but having the capability of political clout as an independent local institution;

c) a focus on the need for high-quality, well-motivated staff;

d) academic and entrepreneurial freedom for staff to perform creatively and

effectively;

e) the flexibility to respond to changing circumstances so that the museum could adapt and evolve.

1.217 This proposition coincided with the new councils created by the 1974 re-organisation of local government being confronted by the first of what came to be successive, substantial reductions in their central government funding. Some of these authorities had been seeking to develop new museum projects, often as part of economic regeneration programmes, or strategies to provide comprehensive leisure provision for their districts.

1.218 Realising that these ambitions could never be met within the lower level of internal resources, a few councils adopted the Ironbridge model to develop such schemes. Dudley Borough Council had already agreed to develop its social and industrial history collections in this way, and the Black Country Museum Trust was incorporated in October 1975. In 1977 the Torfaen Museum Trust was established to take over Torfaen Borough Council’s museum service, and progress a project that had come in the train of local government reorganisation in 1974, but which had stalled as a consequence of the financial pressures on the Council.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 18

5 Cossons (1976)

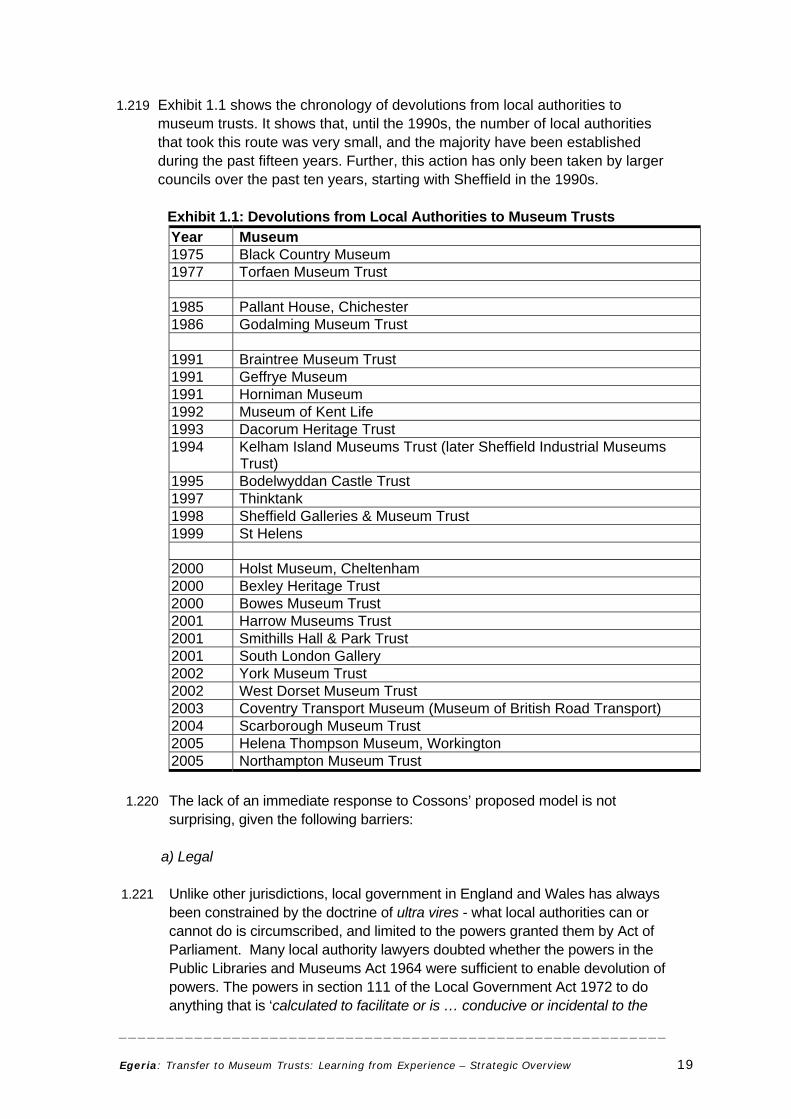

1.219 Exhibit 1.1 shows the chronology of devolutions from local authorities to museum trusts. It shows that, until the 1990s, the number of local authorities that took this route was very small, and the majority have been established during the past fifteen years. Further, this action has only been taken by larger councils over the past ten years, starting with Sheffield in the 1990s.

Exhibit 1.1: Devolutions from Local Authorities to Museum Trusts Year Museum 1975 Black Country Museum 1977 Torfaen Museum Trust 1985 Pallant House, Chichester 1986 Godalming Museum Trust 1991 Braintree Museum Trust 1991 Geffrye Museum 1991 Horniman Museum 1992 Museum of Kent Life 1993 Dacorum Heritage Trust 1994 Kelham Island Museums Trust (later Sheffield Industrial Museums

Trust) 1995 Bodelwyddan Castle Trust 1997 Thinktank 1998 Sheffield Galleries & Museum Trust 1999 St Helens 2000 Holst Museum, Cheltenham 2000 Bexley Heritage Trust 2000 Bowes Museum Trust 2001 Harrow Museums Trust 2001 Smithills Hall & Park Trust 2001 South London Gallery 2002 York Museum Trust 2002 West Dorset Museum Trust 2003 Coventry Transport Museum (Museum of British Road Transport) 2004 Scarborough Museum Trust 2005 Helena Thompson Museum, Workington 2005 Northampton Museum Trust

1.220 The lack of an immediate response to Cossons’ proposed model is not

surprising, given the following barriers:

a) Legal

1.221 Unlike other jurisdictions, local government in England and Wales has always been constrained by the doctrine of ultra vires - what local authorities can or cannot do is circumscribed, and limited to the powers granted them by Act of Parliament. Many local authority lawyers doubted whether the powers in the Public Libraries and Museums Act 1964 were sufficient to enable devolution of powers. The powers in section 111 of the Local Government Act 1972 to do anything that is ‘calculated to facilitate or is … conducive or incidental to the

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 19

discharge of any of their functions’ also appeared to be doubtful 6. While Part III of the Local Government & Housing Act 19897 appeared to provide powers to support the creation of ventures that would increase employment, the influential view of the Solicitor to the Audit Commission was that these powers were, in themselves, not sufficient to empower councils to devolve services.

b) Political

1.222 While the earliest devolutions took place under the Labour governments of the

1970s, the election of a Conservative administration under Margaret Thatcher in the general election of 1979 led to reforms that changed the political environment within which such changes might take place. 8 These included:

narrowing the autonomy of local councils by the imposition of fiscal

restraints by central government;

a re-definition of the role of local government from service provider to enabler, encouraging the delivery of services by the private sector or not-for-profit organisations,9 with the introduction of a competitive tendering regime for some local authority services;

encouragement to relinquish direct control over council housing stock to

non-profit housing corporations, and, under the Education Reform Act 1988, to transfer responsibility for polytechnics to central government and schools to local management; and

the establishment of quasi-autonomous non-governmental

organisations (quangos), with members appointed by central government and dominated by business people, to discharge responsibilities that had previously been exercised by municipal authorities.

1.223 Unsurprisingly, such changes were resisted by local authorities reluctant to

relinquish power and authority. Any such move – however well-intentioned or beneficial it might appear – was likely to be opposed, and externalising services was widely seen to be the same as privatisation, even when, as in the case of transfer to a charity, it was rather a move to another part of the public domain. Government’s habit of referring to museums other than those directly controlled by public authorities as ‘private’ did not help in this, Nor did the ambivalent tone of the Museums & Galleries Commission’s 1991 Report on Local Authorities and Museums, 10 which consistently used the term ‘privatisation’ to describe the museum trust option, while making the superfluous recommendation that transfer should only be considered ‘for positive reasons’.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 20

6 which proved to be the correct view as judged by the Court of Appeal in Credit Suisse v The

Borough Council of Allerdale QB 306; [1996] 4 All ER 129; {1996] 3 WLR 894,CA 7 ss 33 – 35 8 Stewart & Stoker (1999) 9 Goodwin (1992), 118 - 120 10 MGC (1991), 26 - 27

1.224 The idea that quangos were an appropriate form of government was not only resisted by local politicians. Commentators suggested that ‘government is being handed back to the ‘new magistracy’ from which it was removed in the counties more than a hundred years ago. Elected representatives are being replaced by a burgeoning army of the selected – the unknown government of our society’.11

1.225 These factors would inevitably be taken into account by museum workers,

especially given that many were left-of-centre in their politics. The sparsity of successful precedents discouraged others from following the same route, especially given the embattled nature of many museums. Central government budget cuts reduced funding for local government (whose expenditure, as a proportion of total government spending, decreased substantially in the 1980s and 1990s) and created very real difficulties.

c) Professional

1.226 Museum staff, besides having natural concerns about their own job security and

terms and conditions of employment, subscribed to codes of professional conduct that emphasised that museums discharged a ‘trustee’ role in safeguarding collections for future generations. Irrespective as to how far this was true in a strictly legal sense (most local authority museum collections were the corporate property of the council, to do with as it wished12) the duty to safeguard this inheritance was strongly-felt. Any risk to the legacy was to be avoided, and what were generally termed ‘private’ museums were, by definition, to be regarded with suspicion.

Public Managerialism & Museum Trusts

1.227 The 1980s and 1990s saw a number of new local authority-funded museums

(such as at Manchester Museum of Science and Industry, Richmond on Thames Museums, and the New Forest Museum at Lymington in Hampshire) being established using the independent museum model, but there was no major movement to devolve local authority museums to such trusts. While the 1980s saw much debate about the principle of such transfers, it had very little practical impact. When metropolitan county councils were extinguished by the Local Government Act 1985, the structures set up to replace their museum services led to the incorporation of the former Merseyside museums as a National institution,13 and created a local authority joint committee for Tyne & Wear Museums. In London, The Iveagh Bequest at Kenwood passed to English Heritage, and the Geffrye and Horniman Museums to the Inner London Education Authority (ILEA).

1.228 However when, five years later, ILEA’s abolition necessitated new governance

for the Horniman and Geffrye Museums, the selected option was the museum

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 21

11 Jones & Stewart (1992) 12 Babbidge (1991), 259 - 60 13 The Merseyside Museums and Galleries Order 1986 (SI 1986 No 226) under s 46 of the

Local Government Act 1985

trust (rather than the alternative of absorption by an existing National museum) though with government funding and a board nominated by Ministers, that took over ILEA’s responsibilities.

1.229 The transformation at those two museums was generally regarded as dramatic.

Both had strong reputations for pioneering educational activities and temporary exhibitions, but in other respects they had stood still for decades. Yet at the Horniman, described by its then Director as ’a time capsule in terms of museum development’, the change enabled a major refurbishment of the museum building, as well as the implementation of the donor’s original intent for the Museum and its adjacent gardens to be managed and developed together (rather than being operated separately, which had been the position in the previous local authority regime). The assessment was that ‘more has been achieved in the past two years than in the entire preceding decade’.14

1.230 This, and the achievements of other governance models at Liverpool and Tyne

and Wear, helped break down the view that this was the only possible model to deliver a successful museum service. That most independent museums appeared to thrive, and that the constituency maintained a high profile throughout the 1980s also helped. A speech by the Minister for the Arts at the Museums Association conference at Newcastle upon Tyne in 1992 advocated devolution, and local authorities were encouraged to consider this option by Treasures in Trust, the government’s review of museum policy15 published in 1996.

1.231 Treasures in Trust maintained the view that the operation of museum services

should be a matter of local discretion. However, it suggested that the museum trust should be considered, not only for its perceived advantages in terms of plural funding, but also for management benefits. The review maintained the view that mirrored arrangements at a national level – that museums should hold collections under the control of a dedicated board with no responsibilities other than those for the museum and its direction. Its director or curator should be directly responsible for the collection and accountable to the museum’s board.

1.232 This policy development coincided with the growth of ‘agency theory’ (the

study of relationships between principals and agents) and market economics. Trends in business management, and the ideas of management gurus such as Michael Porter, honed on experiences in the world of commerce, exerted a major influence on the public sector. This ‘public managerialism’ is typified by:

accountability, the monitoring of performance and incentives for good

performance;

separation of strategy from delivery, and a focus on management rather than policy;

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 22

14 Boston (1992) 15 DNH (1995), 18 - 19

an inclination to introduce market mechanisms for delivery, including competition and contracting-out;

responsiveness to customer preferences; and

disaggregation of large bureaucratic structures, with autonomy having to

be earned within a framework of strong central control. 1.233 The same period saw local authorities experience a substantial reduction in

their expenditure, and greater central government intervention in what they did receive. Between 1990 and 2004, the proportion of locally-raised taxation fell from 58% to 28%16. This was principally due to the abolition of locally-determined business rates and the introduction of standard national non-domestic property rates. Previously, regional and sub-regional centres and market towns had been able to justify funding the provision of facilities of more than local significance by the commercial benefit that accrued to local businesses from people coming to use them. The introduction of a common national rate removed this justification.

New Labour & Best Value 1.234 The Labour Party in opposition had espoused the benefits of applying private-

sector management techniques to the public sector. Tony Blair, speaking as Leader of the Opposition to the shadow assembly of the Local Government Association in July 1996, made it clear that the emphasis should be on ‘the best possible outcome in service delivery regardless of who actually delivers the service’ and ‘it would make no sense to suggest that a local service should be kept in-house for ideological reasons if it would be more efficient and would serve the public interest better to deliver it in another way.’17

1.235 Within a month of the election of the New Labour government in May 1997 the Local Government Minister announced to Parliament that the government was pressing forward with its manifesto commitments to modernise local government. In July 1998 it set out its framework for the modernisation of local government in the White Paper, Modern Local Government: In Touch with the People, which described local government as a partner of central government in meeting local needs as well as national aims, and particularly the four public service priorities of education, health, crime and transport. Councils were seen as having a significant role in making sure that priorities were reflected locally, with central government checking delivery through performance measures. Those that performed well would be awarded greater freedoms and flexibilities than those that did not.

1.236 A series of Acts of Parliament reformed both the structure of local government (by replacing the traditional committee structure with executive Cabinets and, where the local population requisitioned it, elected Mayors) and how it operated (including the introduction of external performance

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 23

16 ODPM (2004),12 17 Local Government Chronicle 26 July 1996

inspections). The relationship between central and local government was crystallised.

1.237 The consequences of these changes for local authority museums can be

characterised as follows:

they have tended to be amalgamated with other services as part of larger operating units, which are themselves elements within large directorates/departments, placing them at the margins of the council and distant from decision-making18;

they have created an imperative need (not always encouraged by the

council’s corporate management) to cultivate the Council’s political leadership (whether an elected Mayor, Leader or relevant Cabinet portfolio holder) and key top managers, without whose support museums cannot achieve profile and whose support is essential if their funding is not to be vulnerable;

they have had to respond to the growth of performance indicators, first

recommended in 199119 and now refined in nationally-published performance indicators for number of museum visits, number of museum uses, and number of visits by schoolchildren in organised groups;

there has been a need to reconcile the council’s corporate priorities,

which are largely influenced by central government, with the needs of the Museum and its audiences, which may differ – the art of ‘managing paradoxes’;20

changing patterns of employment, with short-term contracts (often

externally-funded) becoming more commonplace; and

the requirement to meet corporate strategies in all areas, and to develop bids for external funding, has stretched museums’ capacity.

1.238 Many of these issues are encapsulated in the Best Value and (in England) Comprehensive Performance Assessment (CPA) regimes. Best Value is a duty21 on councils: to make arrangements to secure continuous improvement in the way they exercise their functions, having regard to a combination of economy, efficiency and effectiveness. Originally planned as a review of all the services provided by each local authority during a five-year cycle, the scale and resources they absorbed soon led to a greater emphasis on cross-cutting generic evaluations. Now local authorities have a deal of freedom in

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 24

18 Kawashima (1997), 20 19 Audit Commission (1991) 20 Kawashima (1997), 153 21 Local Government Act 1999 Part I

deciding the scope and timing of Best Value reviews, which are published in their annual Best Value Performance Plans. 22

1.239 CPA, introduced in 2002, is an annual external inspection aimed at providing a rounded picture of a council’s performance. It has taken over from Best Value as the primary performance assessment and improvement mechanism for local authorities. From 2002 to 2004 councils were rated as ‘excellent’, ‘good’, ‘fair’, ‘weak’ or ‘poor’, but from 2005 these categories were replaced by star ratings ranging from four star (highest) to 0 star (lowest). Councils are also now rated on their progress towards improvement, and are scored as 'improving strongly', 'improving well', 'improving adequately' or 'not improving'. These terms are known as 'direction of travel'. The more challenging CPA framework introduced on 2005 places greater emphasis on councils' role as community leader, giving recognition to the way in which they are increasingly using partnership working to deliver local services. Underpinning the new framework is a measurement of councils' ability to fulfill their responsibilities in a way that is the most cost-effective.

Local Government in 2006 1.240 Local government is fundamentally different in 2006 to what it was fifteen

years earlier, both in governance and management. While national regulation through the national performance framework, represented by Best Value and CPA, has clearly been highly influential in stimulating change, it is not alone, and a series of other initiatives have positively encouraged local councils to become more outward looking. These include:

Local Strategic Partnerships (LSPs) - a top level partnership bringing

together organisations from the public, private, community and voluntary sector within a local authority area, with the objective of improving people's quality of life;

Local Area Agreements (LAAs), designed to improve co-ordination

between central government and local authorities and their partners, working through the Local Strategic Partnership;

Local Public Service Agreements (PSAs), which identify specific targets

and rewards for defined performance improvement by local authorities, and are specifically aimed at improving performance in relation to areas of public service delivery.

Local Compacts, based on the national guidance,23 to promote

understanding of how the relationships between central and local government and the voluntary sector can be developed for mutual

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 25

22 Following the creation of the Welsh Assembly Government in 1999 the requirement on local

authorities in Wales to follow Best Value has been modified, and new Wales Programme for Improvement introduced. Though the framework remains similar to that in England, it is claimed to be more flexible, and less bureaucratic, than the Best Value regime.

23 The Compact on Relations between Government and the Voluntary and Community Sector in England (Home Office 1989)

advantage, and reflect central government’s policy of engagement with the voluntary sector. 24

1.241 Increasingly, the degree to which a local authority is engaging with its

stakeholders is being seen as a touchstone for its general effectiveness.25

1.242 Responding to these national initiatives, local government in England has

adopted a positive response to plural working. Independence, Opportunity, Trust – A manifesto for local communities26 recognises the benefits in empowering local community organisations to manage assets and provide services. Understanding the Future: Museums and 21st Century Life, DCMS’s consultation paper on future museums policy, considered alternative structural issues to be fruitful areas for future debate.27 Of the 75 responses to this important document only a handful took up the invitation to express feelings about museum trusts, and all bar two were non-commital. While this could suggest that devolution has ceased to be the controversial issue it was in the 1990s, perhaps a more probable explanation is that museums are disinclined to engage with such issues.

1.243 It should be noted that the foregoing reflects government policy in England. The Welsh Assembly Government takes a different approach. Its policy is that where executive Assembly-sponsored public bodies undertake functions that are governmental either on policy or delivery, they should be brought in-house, on the basis that Ministers are responsible for allocation of public money, and the Assembly for scrutinising the arrangements made by Ministers.28 While the functions of the National Museums and Galleries of Wales were deemed to be essentially non-governmental, and its current governance arrangements will remain, the Welsh Assembly Government’s overall approach reflects the reluctance of government in Wales – whether national or local – to adopt the active encouragement of service devolution that has been taking place in England.

The Future 1.244 The CPA regime on local authorities in England will continue into the

foreseeable future. Like all public sector initiatives, it is informed by the definitions of efficiencies in the Gershon Report:29

reduced number of inputs (eg people or assets whilst maintaining the

same level of service provision;

lower prices for the resources needed to provide public services;

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 26

24 eg in HM Treasury (2003) 25 DETR (1998), 23 26 Local Government Association (September 2004) 27 DCMS (2005),30 28 Official Record of the Welsh Assembly 30 November 2004: Statement by the First Minister 29 Gershon (2004), 6 - 7

additional outputs, such as enhanced quality or quantity of service for the same level of inputs;

improved ratios of output per unit cost of input; and

changing the balance between different outputs aimed at delivering a

similar overall objective in a way which achieves a greater overall output for the same inputs.

1.245 These efficiencies can be regarded as ‘cashable’ – they release savings for

recycling and use for another purpose – or ‘non-cashable’ – higher quality goods or services have been purchased for the same price.

1.246 For the future, the underlying tenets of CPA and Gershon are likely to

continue to encourage English local authorities to consider outsourcing service provision, and in the case of museums to consider devolution to trusts.

Museum Trusts in Other Countries

1.247 It is not only in England that new business approaches to managing public

institutions have had an impact. Decentralisation has been a key feature of many countries that were formerly typified by the ‘unitary state’, especially in Eastern Europe, where the pace of change has been quick, in response to a rapidly evolving political agenda. Both decision-making and the day-to-day management of key resources have been delegated away from central ministries and municipal governments

1.248 In most cases these delegations have been to new autonomous public bodies, such as the conversion of leading museums into établissements

publiques in France or the conversion of leading Netherlands museums into independent Foundations, run by supervisory boards of trustees. There are similar moves in Italy and Spain, though in many cases the absence of a tradition of non-governmental (charitable) organisation blurs the edges between devolution and privatisation. In these countries statutory safeguards usually regulate the public interest in those museums and their collections.

1.249 Such legislation is usually absent in countries (including the United States of

America) that have ‘common law’ legal systems, which usually have a ‘third sector’ based on the English experience of charity law. The museum trust approach is at its most developed in New Zealand, where the major regional museums at Auckland (the Auckland War Memorial Museum), Christchurch (the Canterbury Museum) and Otago (the Otago Museum) are incorporated as museum trusts by Local Act of Parliament, with their revenue budgets funded by a precept on the local authorities in their locality.

1.250 Though the trend to devolve continues to increase throughout the world, in

absolute terms the number of museums that have moved in this direction are small. Even in the United States, where there is a more substantial

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 27

independent sector than in the UK, relatively few of the local councils that operate museums (and faced by similar financial pressures as those experienced by their UK counterparts), have devolved museums, and where this has happened the results have not always been the happiest. 30

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 28

30 see para 1.578 and following

CHAPTER 1.3 – OPTIONS FOR SERVICE DELIVERY

1.301 In England, the impact of both Best Value and CPA, and the government’s

encouragement of partnership working with the private and voluntary sectors, has been to stimulate local authorities to give serious consideration to whether there are alternative means of service delivery, Most local authorities have dropped any principled opposition to such arrangements. Both commercial enterprises and the third sector of non-governmental organisations now undertake work that complements – and in some areas substitutes for – tasks formerly undertaken by local government.

1.302 Besides devolution to museum trusts, the following options are available to

deliver museum services:

a) Direct delivery, where the Council organises and manages the service from within its own organisation, which represents the status quo in most authorities;

b) Joint arrangements with other local authorities, whether by amalgamating

their museums into a single service under a joint committee of the participating councils (as is the case at Tyne & Wear), or as a commercial arrangement with another local authority providing museum services (though there are as yet no examples of this in England or Wales);

c) Outsourcing, whether:

1) by contracting-out, for a specified term on the basis of a specification and contract procured under European Union procurement regulations (eg Walsall Museums Service (which does not include the New Art Gallery) is among the twenty council functions that have been managed from September 2005 by Fujitsu Services, an international service provider company);

2) to a culture/leisure non-profit-distributing organisation (NPDO) either

on the same basis as to a commercial contractor or through a special purpose vehicle created by the Council for that purpose (such as CiP at Hounslow); or

3) to an existing independent museum (eg the West Park Museum at

Macclesfield is managed for the Council by the Macclesfield Museum Trust, and the Margate Museum by the East Kent Maritime Museum);

1.303 The various constitutional forms adopted in the case of (2) and (3) above are

described in the Annex to this Part of the study.

__________________________________________________________ Egeria: Transfer to Museum Trusts: Learning from Experience – Strategic Overview 29

Options Adopted 1.304 There are 410 principal local authorities (ie excluding town, parish and

community councils) in England and Wales. Of these, in September 2005,

142 councils (35%) made no direct museum provision; and

of the 268 that did: o 204 (76%) delivered some or all of those services directly; o 40 councils (15%) did this through joint arrangements with other

local authorities, including joint committees; o 23 councils (8%) have devolved, or are in the process of devolving,

their museum operations, in whole or part, to museum trusts; o three councils have outsourced their operations to culture/leisure

trusts; and o two have contracted-out their operations to a commercial operator.

1.305 A survey for the Group of Museum Directors in 2000 suggested that at that

time 60% of museum services were considering or had considered museum trust status, mostly in advance of Best Value. Though only five had decided to further pursue the matter, 75% anticipated some other form of reorganisation or restructuring during the coming two years. 31

1.306 The scope and scale of these reviews are highly variable. While a few are in-

depth, thorough and externally moderated, many are internal, some are superficial, and a few ill-informed. It is not surprising, therefore, that in most cases the chosen option appears to be ‘no change’, though in a handful of cases it has led to modifications to enable a greater contribution to the museum’s governance from outside the council.32

1.307 A number of reasons have been given for no change:

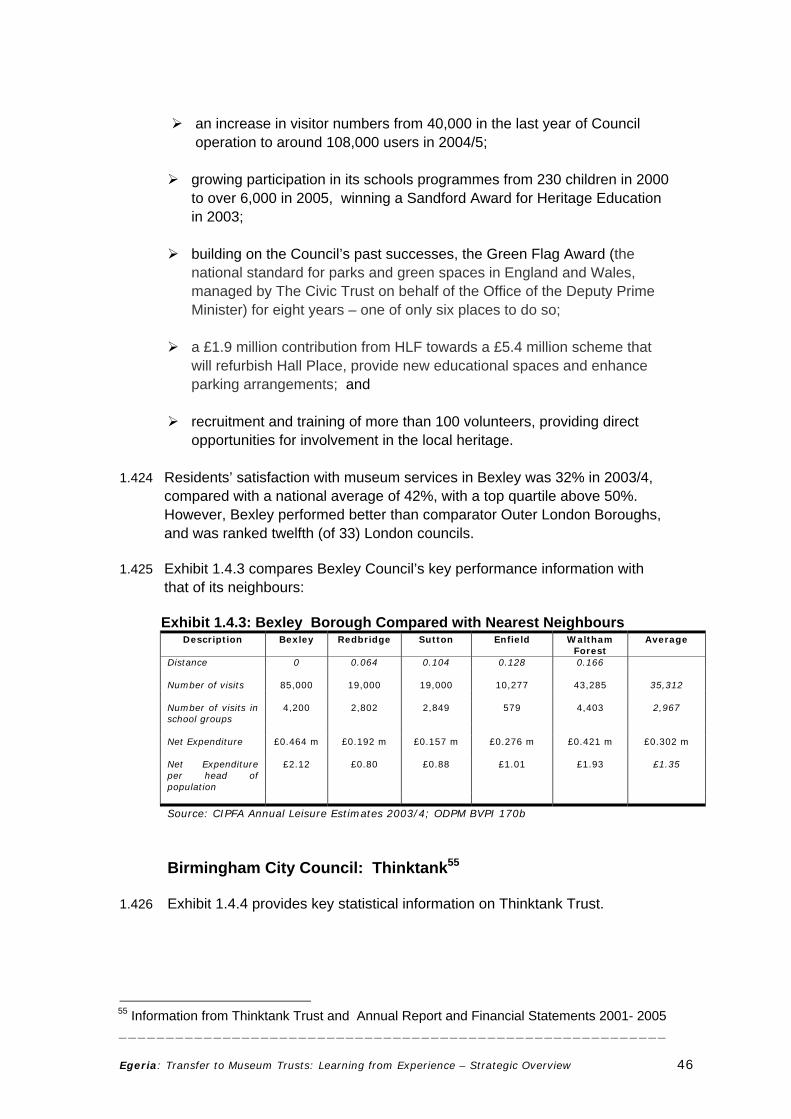

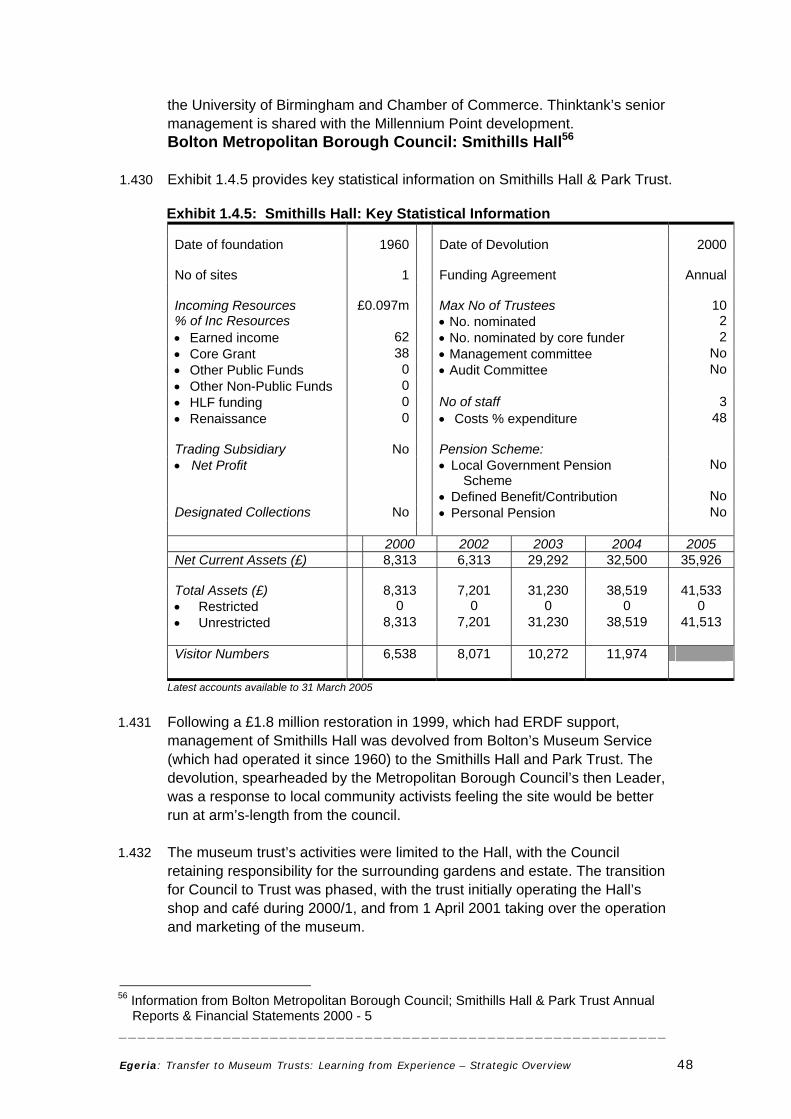

a) Financial – devolution would: