multivariate garch models -...

TRANSCRIPT

Multivariate GARCH Models

Eduardo Rossi

University of Pavia

Introduction

Economics and financial economics present problems whose solutions

need the specification and estimation of a multivariate distribution.

• the standard portfolio allocation problem

• the risk management of a portfolio of assets

• pricing of derivative contracts based on a more than one

underlying asset (e.g., Quanto options)

• Financial contagion (shocks transmission volatility and returns)

Eduardo Rossi c© - Econometria finanziaria 2010 2

Introduction

Stylized facts:

• Volatility clustering

• Time-varying dynamic covariances and dynamic correlations

Financial variables have time-dependent second order moments.

Parametric models:

1. Multivariate GARCH models

2. Multivariate Stochastic volatility models

3. Multifactor models

4. Multifactor realized volatility models

Eduardo Rossi c© - Econometria finanziaria 2010 3

Multivariate Volatility Models

Vector of returns:

yt = (y1t, . . . , yNt)′ (N × 1)

yt − µt = ǫt = H−1/2t zt

Let {zt} be a sequence of (N × 1) i.i.d. random vector with the

following characteristics:

E [zt] = 0

E [ztz′

t] = IN

zt ∼ G (0, IN )

with G continuous density function.

Eduardo Rossi c© - Econometria finanziaria 2010 4

Multivariate Volatility Models

Et−1 (ǫt) = 0

Et−1 (ǫtǫ′

t) = Ht

E (ǫtǫ′

t) = Σ

Et−1[·] = E[·|Φt−1]

Φt−1 is the σ-field generated by past values of observable variables.

where Ht is a matrix (N ×N) positive definite and measurable with

respect to the information set Φt−1, that is the σ-field generated by

the past observations: {ǫt−1, ǫt−2, . . .}.The correlation matrix:

Corrt−1(ǫt) = Rt = D−1/2t HtD

−1/2t

Dt = diag(h11,t, . . . , hNN,t)

Eduardo Rossi c© - Econometria finanziaria 2010 5

Multivariate Volatility Models

MVMs provide a parametric structure for the dynamic evolution of

Ht. MVMs must satisfy:

1. Diagonal elements of Ht must be strictly positive;

2. Positive definiteness of Ht;

3. Stationarity: E[Ht] exists, finite and constant w.r.t. t.

Eduardo Rossi c© - Econometria finanziaria 2010 6

Multivariate Volatility Models

Ideal characteristics of a MVM:

1. Estimation should be flexible for increasing N

2. It should allow for covariance spillovers and feedbacks;

3. Coefficients should have an economic or financial interpretation

Eduardo Rossi c© - Econometria finanziaria 2010 7

MGARCH

The extension from a univariate GARCH model to an N -variate

model requires allowing the conditional variance-covariance matrix of

the N -dimensional zero mean random variables ǫt depend on the

elements of the information set.

Eduardo Rossi c© - Econometria finanziaria 2010 8

Covariance targeting

Caporin and McAleer (2009). Covariance targeting if the conditions

are met:

• The model intercept is an explicit function of the model long-run

covariance (or correlation) The long-run covariance (or

correlation) solution is given by the E[Ht] or E[Rt].

• The long-run solution is replaced by a consistent estimator.

Eduardo Rossi c© - Econometria finanziaria 2010 9

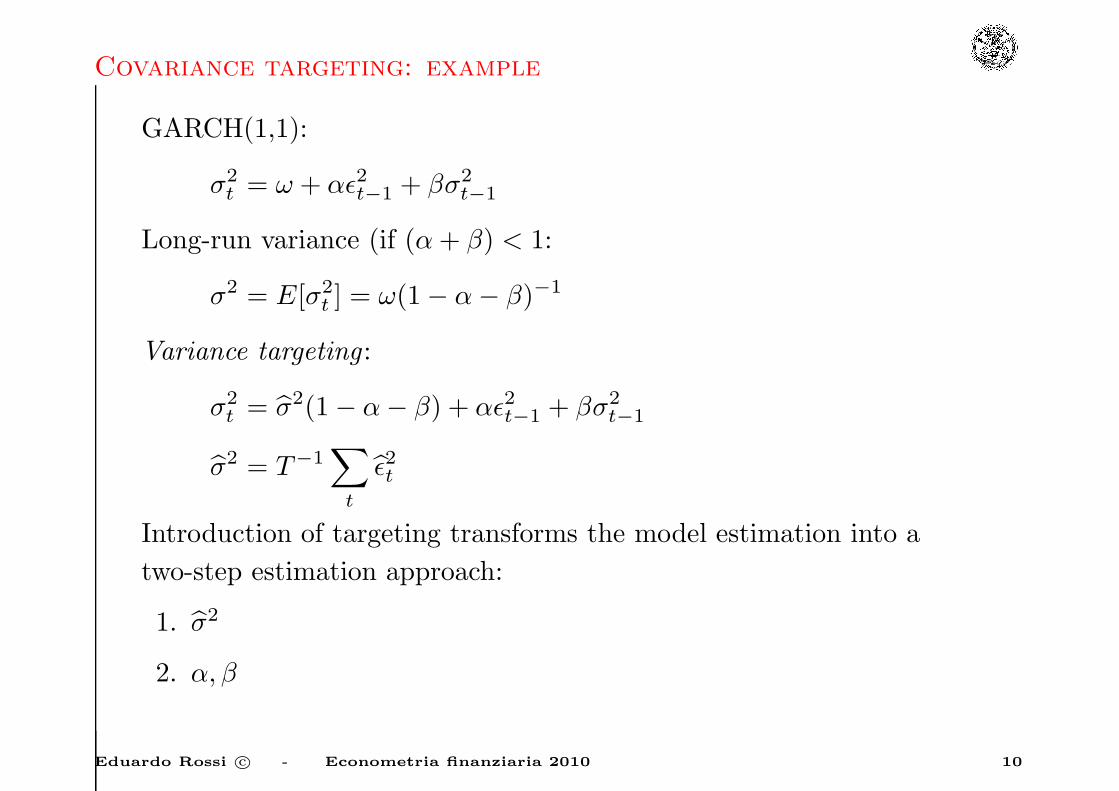

Covariance targeting: example

GARCH(1,1):

σ2t = ω + αǫ2t−1 + βσ2

t−1

Long-run variance (if (α+ β) < 1:

σ2 = E[σ2t ] = ω(1− α− β)−1

Variance targeting :

σ2t = σ2(1− α− β) + αǫ2t−1 + βσ2

t−1

σ2 = T−1∑

t

ǫ2t

Introduction of targeting transforms the model estimation into a

two-step estimation approach:

1. σ2

2. α, β

Eduardo Rossi c© - Econometria finanziaria 2010 10

Covariance targeting: example

N assets: N variances + 12N(N − 1) covariances = N

2 (N + 1).

Two alternative approaches:

• Models of Ht

• Models of Dt and Rt

The parametrization of Ht as a multivariate GARCH, which means

as a function of the information set Φt−1, allows each element of Ht

to depend on q lagged of the squares and cross-products of ǫt, as well

as p lagged values of the elements of Ht. So the elements of the

covariance matrix follow a vector of ARMA process in squares and

cross-products of the disturbances.

Eduardo Rossi c© - Econometria finanziaria 2010 11

MGARCH-Vech representation

Let vech denote the vector-half operator, which stacks the lower

triangular elements of an N ×N matrix as an [N (N + 1) /2]× 1

vector.

Let A be (2× 2), then vech(A)

vech(A) =

a11

a21

a22

Since the conditional covariance matrix Ht is symmetric,

vech (Ht) , (N(N + 1)/2× 1) contains all the unique elements in Ht.

Eduardo Rossi c© - Econometria finanziaria 2010 12

MGARCH-Vech representation

A natural multivariate extension of the univariate GARCH(p,q)

model is

vech (Ht) = W +

q∑

i=1

A∗

i vech(ǫt−iǫ

′

t−i

)+

p∑

j=1

B∗

jvech (Ht−j)

= W +A∗ (L) vech (ǫtǫ′

t) +B∗ (L) vech (Ht)

A∗ (L) = A∗

1L+ . . .+A∗

qLq

B∗ (L) = B∗

1L+ . . .+B∗

qLp

Eduardo Rossi c© - Econometria finanziaria 2010 13

MGARCH-Vech representation

N∗ ≡ N(N + 1)

2

W : [N (N + 1) /2]× 1

A∗

i , B∗

j : [N∗ ×N∗]

N = 2, Vech-GARCH(1,1):

h11,t

h21,t

h22,t

=

w∗1

w∗2

w∗3

+

a∗11

a∗12

a∗13

a∗21

a∗22

a∗23

a∗31

a∗32

a∗33

ǫ21,t−1

ǫ1,t−1ǫ2,t−1

ǫ22,t−1

+

b∗11

b∗12

b∗13

b∗21

b∗22

b∗23

b∗31

b∗32

b∗33

h11,t−1

h21,t−1

h2,t−1

Eduardo Rossi c© - Econometria finanziaria 2010 14

MGARCH-Vech representation

• This general formulation is termed vec representation by Engle

and Kroner (1995).

• The number of parameters is[1 + (p+ q) [N (N + 1) /2]2

].

• Even for low dimensions of N and small values of p and q the

number of parameters is very large; for N = 5 and p = q = 1 the

unrestricted version of (1) contains 465 parameters.

• The number of parameters is of order O(N4): the curse of

dimensionality.

For any parametrization to be sensible, we require that Ht be

positive definite for all values of ǫt in the sample space in the vech

representation this restriction can be difficult to check, let alone

impose during estimation.

Eduardo Rossi c© - Econometria finanziaria 2010 15

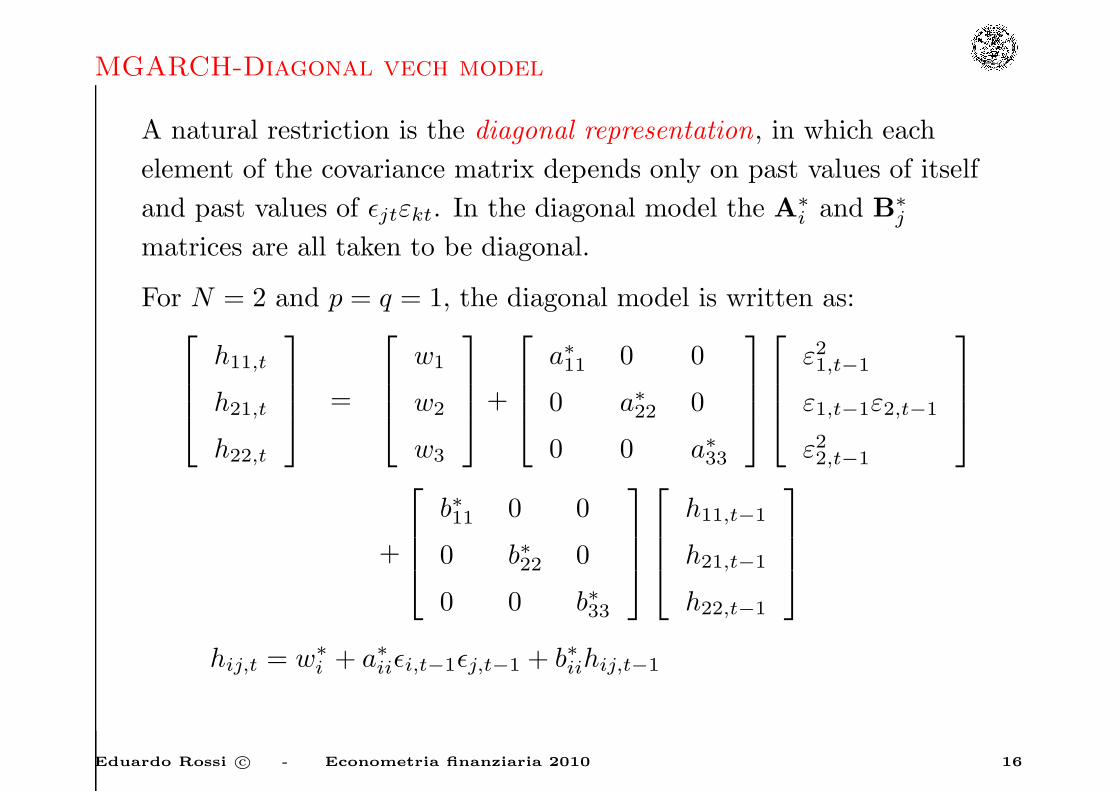

MGARCH-Diagonal vech model

A natural restriction is the diagonal representation, in which each

element of the covariance matrix depends only on past values of itself

and past values of ǫjtεkt. In the diagonal model the A∗

i and B∗

j

matrices are all taken to be diagonal.

For N = 2 and p = q = 1, the diagonal model is written as:

h11,t

h21,t

h22,t

=

w1

w2

w3

+

a∗11 0 0

0 a∗22 0

0 0 a∗33

ε21,t−1

ε1,t−1ε2,t−1

ε22,t−1

+

b∗11 0 0

0 b∗22 0

0 0 b∗33

h11,t−1

h21,t−1

h22,t−1

hij,t = w∗

i + a∗iiǫi,t−1ǫj,t−1 + b∗iihij,t−1

Eduardo Rossi c© - Econometria finanziaria 2010 16

MGARCH-Diagonal vech model

Thus the (i, j) th element in Ht depends on the corresponding (i, j) th

element in εt−1ε′

t−1 and Ht−1. This restriction reduces the number of

parameters to [N (N + 1) /2] (1 + p+ q). This model does not allow

for causality in variance, co-persistence in variance and asymmetries.

The number of parameters is of order O(N2).

The diagonal vech is equivalent to:

Ht = W +A⊙ ǫt−1ǫ′

t−1 +B⊙Ht−1

where A and B are symmetric matrices. ⊙ is the Hadamard product.

Eduardo Rossi c© - Econometria finanziaria 2010 17

MGARCH(1,1)-vech-Unconditional Covariance Matrix

Given that

ǫtǫ′

t = Ht +Vt

with Et−1 (Vt) = 0.

vech (ǫtǫ′

t) = vech (Ht) + vech (Vt)

vech (Vt) vector m.d.s.

with E (vech (Vt)) = vech(E (Vt)) = 0.

Eduardo Rossi c© - Econometria finanziaria 2010 18

MGARCH(1,1)-vech-Unconditional Covariance Matrix

For a GARCH(1,1), the unconditional covariance matrix, when it

exists, is given by

vech (ǫtǫ′

t) = W +A∗

1vech(ǫt−1ǫ

′

t−1

)

+B∗

1

[vech

(ǫt−1ǫ

′

t−1

)− vech (Vt−1)

]+ vech (Vt)

E (ǫtǫ′

t) = Σ

vech (E (ǫtǫ′

t)) = W + (A∗

1 +B∗

1)[vech

(E(ǫt−1ǫ

′

t−1

))]

vech (Σ) = [IN∗ −A∗

1 −B∗

1]−1

W.

For a GARCH(p,q) model

vech (Σ) = [IN∗ −A∗ (1)−B∗ (1)]−1

W

Eduardo Rossi c© - Econometria finanziaria 2010 19

MGARCH-vech representation

Targeting cannot easily introduced in the model.

MGARCH(1,1)-vech, unconditional var-cov matrix

[IN∗ −A∗

1 −B∗

1]vech(Σ)

Σ = T−1∑

t

ǫtǫ′

t

Targeting allows reducing by N∗ the parameters to be estimated.

The total number of parameters is still O(N4).

vech (Ht) = vech(Σ)+A∗

1vech[ǫt−1ǫ

′

t−1 − vech(Σ)]

+B∗

1

[vech (Ht−1)− vech

(Σ)]

Eduardo Rossi c© - Econometria finanziaria 2010 20

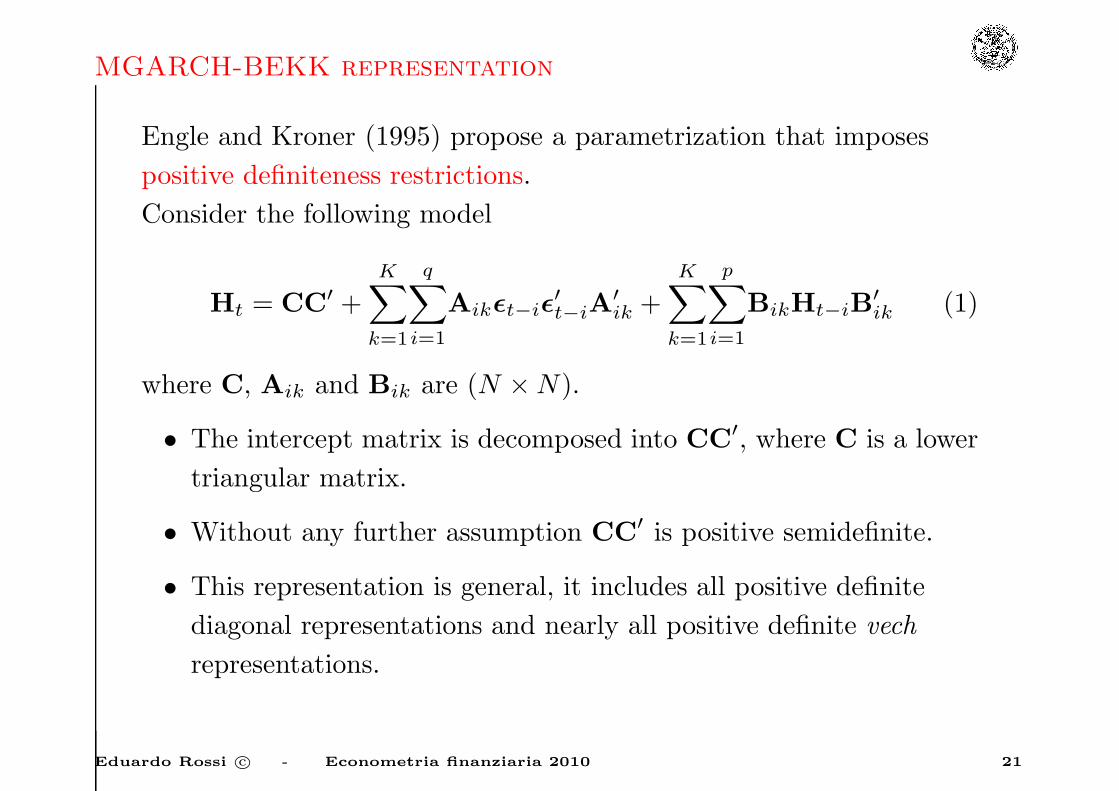

MGARCH-BEKK representation

Engle and Kroner (1995) propose a parametrization that imposes

positive definiteness restrictions.

Consider the following model

Ht = CC′ +K∑

k=1

q∑

i=1

Aikǫt−iǫ′

t−iA′

ik +K∑

k=1

p∑

i=1

BikHt−iB′

ik (1)

where C, Aik and Bik are (N ×N).

• The intercept matrix is decomposed into CC′, where C is a lower

triangular matrix.

• Without any further assumption CC′ is positive semidefinite.

• This representation is general, it includes all positive definite

diagonal representations and nearly all positive definite vech

representations.

Eduardo Rossi c© - Econometria finanziaria 2010 21

MGARCH-BEKK representation

For exposition simplicity we will assume that K = 1:

Ht = CC′ +

q∑

i=1

Aiǫt−iǫ′

t−iA′

i +

p∑

i=1

BiHt−iB′

i

Consider the simple GARCH(1,1) model:

Ht = CC′ +A1ǫt−1ǫ′

t−1A′

1 +B1Ht−1B′

1 (2)

Proposition 1. (Engle and Kroner (1995)) Suppose that the

diagonal elements in C are restricted to be positive and that a11 and

b11 are also restricted to be positive. Then if K = 1 there exists no

other C, A1, B1 in the model (2) that will give an equivalent

representation.

Eduardo Rossi c© - Econometria finanziaria 2010 22

MGARCH-BEKK representation

The purpose of the restrictions is to eliminate all other

observationally equivalent structures.

For example, as relates to the term A1ǫt−1ǫ′

t−1A′

1 the only other

observationally equivalent structure is obtained by replacing A1 by

−A1. The restriction that a11 (b11) be positive could be replaced

with the condition that aij (bij) be positive for a given i and j, as

this condition is also sufficient to eliminate −A1 from the set of

admissible structures.

Eduardo Rossi c© - Econometria finanziaria 2010 23

MGARCH-BEKK representation

MGARCH(1,1)-BEKK, N = 2:

Ht = CC′ +

a11 a12

a21 a22

ε21t−1 ε1t−1ε2t−1

ε2t−1ε1t−1 ε22t−1

a11 a12

a21 a22

′

+

b11 b12

b21 b22

h11t−1 h12t−1

h21t−1 h22t−1

b11 b12

b21 b22

′

Eduardo Rossi c© - Econometria finanziaria 2010 24

MGARCH-BEKK representation

Sufficient condition for positive definiteness of Ht in

BEKK-GARCH(p,q) model.

Proposition 2. (Engle and Kroner (1995)) (Sufficient condition)

If H0, H−1, . . . ,H−p+1 are all positive definite, then the BEKK

parametrization (with K = 1) yields a positive definite Ht for all

possible values of εt if C is a full rank matrix or if any Bi

i = 1, . . . , p is a full rank matrix.

Eduardo Rossi c© - Econometria finanziaria 2010 25

MGARCH-BEKK representation

For simplicity consider the GARCH(1,1) model. The BEKK

parameterization is

Ht = CC′ ++A1ǫt−1ǫ′

t−1A′

1 +B1Ht−1B′

1

The proof proceeds by induction.

First Ht is p.d. for t = 1: The term A1ǫ0ǫ′

0A′

1 is positive

semidefinite because ǫ0ǫ′

0 is positive semidefinite. Also if the null

spaces of the matrices of C and B1 intersect only at the origin, that

is at least one of two is full rank then

CC′ +B1H0B′

1

is positive definite. This is true if C or B1 has full rank.

Eduardo Rossi c© - Econometria finanziaria 2010 26

MGARCH-BEKK representation

To show that the null space condition is sufficient CC′ +B1H0B′

1 is

p.d. if and only if

x′ (CC′ +B1H0B′

1)x > 0 ∀x 6= 0

or

(C′x)′

(C′x) +(H

1/20 B′

1x)′(H

1/20 B′

1x)> 0 ∀x 6= 0 (3)

where H0 = H1/2′0 H

1/20 and H

1/20 is full rank.

Eduardo Rossi c© - Econometria finanziaria 2010 27

MGARCH-BEKK representation

Defining N (P ) to be the null space of the matrix P , (3) is true if and

only if

N (C′) ∩N(H

1/20 B′

1

)= ∅.

N(H

1/20 B′

1

)= N (B′

1) because H1/20 is full rank. This implies that

CC′ +B1H0B′

1 is positive definite if and only if

N (C′) ∩N(H

1/20 B′

1

)= ∅. Now suppose that Ht is positive definite

for t = τ .

Then,

Hτ+1 = CC′ +A1ǫτǫ′

τA′

1 +B1HτB′

1

is positive definite if and only if, given that A1ǫτǫ′

τA′

1 is positive

semidefinite, the null space condition holds, because Hτ is positive

definite by the induction assumption.

Eduardo Rossi c© - Econometria finanziaria 2010 28

Diagonal BEKK

Consider MGARCH(1,1)-BEKK, N = 2 with

A1 = diag(a11, a22) B1 = diag(b11, b22)

the model reduces to

Ht = CC′ +

a11 0

0 a22

ε21t−1 ε1t−1ε2t−1

ε2t−1ε1t−1 ε22t−1

a11 0

0 a22

′

+

b11 0

0 b22

h11t−1 h12t−1

h21t−1 h22t−1

b11 0

0 b22

′

h11,t = c211 + a211ǫ21t−1 + b211h11t−1

h12,t = c21c11 + a11a22ǫ1t−1ǫ2t−1 + b11b22h12t−1

h22,t = c21c11 + c222 + a222ǫ21t−1 + b222h11t−1

Eduardo Rossi c© - Econometria finanziaria 2010 29

Diagonal BEKK

This model is equivalent to the Hadamard BEKK:

Ht = CC′ + aa′ ⊙ ǫt−1ǫ′

t−1 + bb′ ⊙Ht−1

positive definiteness is not guaranteed. Positive semidefiniteness is

obtained by imposing p.s.d. of all terms.

Eduardo Rossi c© - Econometria finanziaria 2010 30

Scalar BEKK

MGARCH(1,1) - Scalar BEKK

A1 = αIN , B1 = βIN

Ht = CC′ + α2(ǫt−1ǫ′

t−1) + β2Ht−1

Eduardo Rossi c© - Econometria finanziaria 2010 31

MGARCH(1,1)- BEKK - Covariance targeting

1. BEKK

Ht = Σ+A1

(ǫt−1ǫ

′

t−1 −Σ)A′

1 +B1 (Ht−1 −Σ)B1

or

Ht = (Σ−A1ΣA1 −B1ΣB′

1)+A1

(ǫt−1ǫ

′

t−1

)A′

1+B1Ht−1B′

1

To have p.d-ness of Ht, (Σ−A1ΣA1 −B1ΣB′

1) must be p.d..

2. Hadamard BEKK

Ht = Σ+A1 ⊙(ǫt−1ǫ

′

t−1 −Σ)+B1 ⊙ (Ht−1 −Σ)

(ǫt−1ǫ

′

t−1 −Σ)must be p.s.d., while (Ht−1 −Σ) must be p.s.d.

3. Scalar BEKK

Ht = Σ+ α2(ǫt−1ǫ

′

t−1 −Σ)+ β2 (Ht−1 −Σ)

for α+ β < 1.

Eduardo Rossi c© - Econometria finanziaria 2010 32

BEKK and vec representations

We now examine the relationship between the BEKK and vech

parameterizations. The mathematical relationship between the

parameters of the two models can be found simply vectorizing the

BEKK equation:

vec(Ht) = vec(CC′)+

q∑

i=1

vec(Aiǫt−iǫ′

t−iA′

i)+

p∑

i=1

vec(BiHt−iB′

i)

where vec () is an operator such that given a matrix A (n× n),

vec(A) is a(n2 × 1

)vector. The vec () satisfies

vec (ABC) = (C′ ⊗A) vec (B)

Eduardo Rossi c© - Econometria finanziaria 2010 33

BEKK and vec representations

For a symmetric A, (n× n):

• vech (A) contains precisely the n (n+ 1) /2 distinct elements of

A;

• the elements of vec (A) are those of vech (A) with some

repetitions;

• There exists a unique n2 × n (n+ 1) /2 which transforms, for

symmetric A, vech (A) into vec (A). This matrix is called the

duplication matrix and is denoted Dn:

vec (A) = Dnvech (A)

where Dn is the duplication matrix.

Eduardo Rossi c© - Econometria finanziaria 2010 34

BEKK and vec representations

Then

vec(Ht) = vec(CC′) +

q∑

i=1

(Ai ⊗Ai) vec(εt−iǫ′

t−i)

+

p∑

i=1

(Bi ⊗Bi) vec(Ht−i)

DNvech (Ht) = DNvech(CC′) +

q∑

i=1

(Ai ⊗Ai)DNvech(ǫt−iǫ′

t−i)

+

p∑

i=1

(Bi ⊗Bi)DNvech(Ht−i)

Eduardo Rossi c© - Econometria finanziaria 2010 35

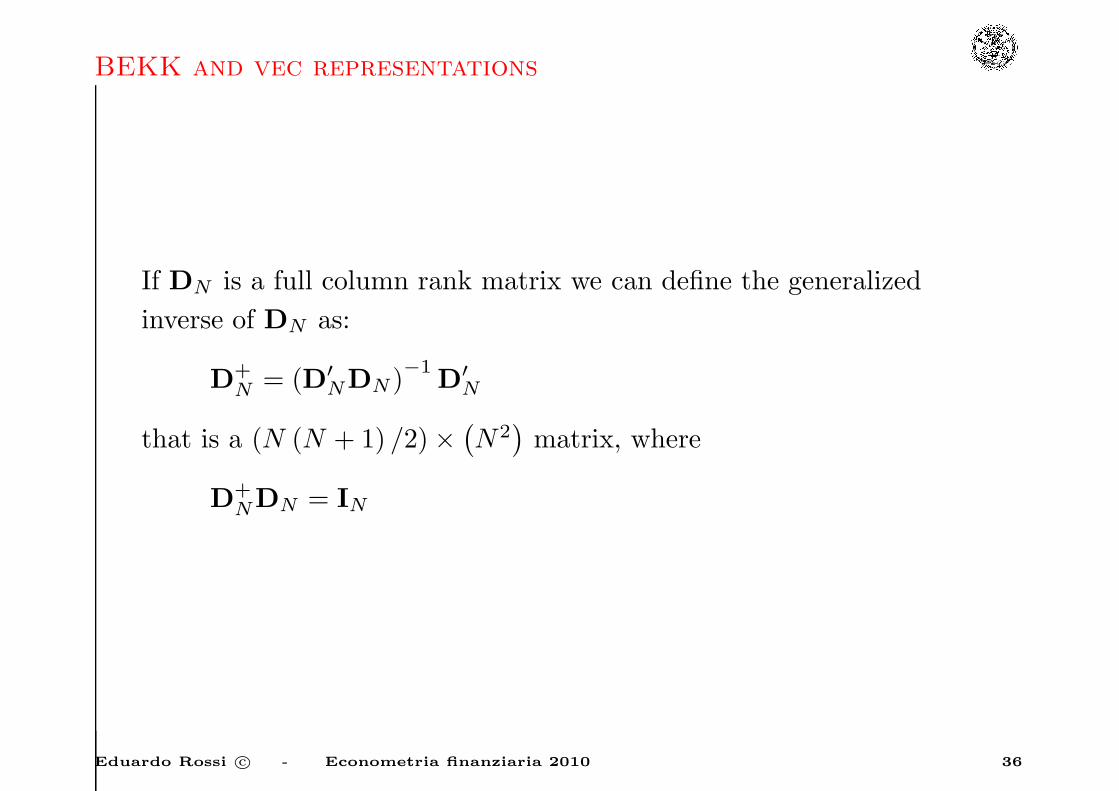

BEKK and vec representations

If DN is a full column rank matrix we can define the generalized

inverse of DN as:

D+N = (D′

NDN )−1

D′

N

that is a (N (N + 1) /2)×(N2)matrix, where

D+NDN = IN

Eduardo Rossi c© - Econometria finanziaria 2010 36

BEKK and vec representations

This implies that premultiplying by D+N

vech (Ht) = vech(CC′) +D+N

(q∑

i=1

(Ai ⊗Ai)

)DNvech(ǫt−iǫ

′

t−i)

+D+N

(p∑

i=1

(Bi ⊗Bi)

)DNvech(Ht−i)

• The vech model implied by any given BEKK model is unique,

while the converse is not true.

• The transformation from a vech model to a BEKK model (when

it exists) is not unique, because for a given A∗

1 the choice of A1

is not unique.

Eduardo Rossi c© - Econometria finanziaria 2010 37

BEKK and vec representations

• This can be seen recognizing that (Ai ⊗Ai) = (−Ai ⊗−Ai) so

while A∗

i = D+N (Ai ⊗Ai)DN is unique, the choice of Ai is not

unique. It can also be shown that all positive definite diagonal

vech models can be written in the BEKK framework.

Given Ai diagonal matrix, then D+N (Ai ⊗Ai)DN is also diagonal,

with diagonal elements given by aiiajj (1 ≤ j ≤ i ≤ N) (See Magnus).

Eduardo Rossi c© - Econometria finanziaria 2010 38

MGARCH-Covariance Stationarity

Given the vech model

vech (Ht) = W +A∗ (L) vech (εtε′

t) +B∗ (L) vech (Ht)

the necessary and sufficient condition for covariance stationary of

{εt} is that all the eigenvalues of A∗ (1) +B∗ (1) are less than one in

modulus. But defining

A∗ (1) = D+N

(q∑

i=1

(Ai ⊗Ai)

)DN

B∗ (1) = D+N

(q∑

i=1

(Bi ⊗Bi)

)DN

Eduardo Rossi c© - Econometria finanziaria 2010 39

MGARCH-Covariance Stationarity

This implies also that in the BEKK model, {ǫt} is covariance

stationary if and only if all the eigenvalues of

D+N

(q∑

i=1

(Ai ⊗Ai)

)DN +D+

N

(p∑

i=1

(Bi ⊗Bi)

)DN

are less than one in modulus.

Let λ1, . . . , λN be the eigenvalues of Ai, the eigenvalues of

D+N

(q∑

i=1

(Ai ⊗Ai)

)DN

are λiλj (1 ≤ j ≤ i ≤ N) (Magnus).

Eduardo Rossi c© - Econometria finanziaria 2010 40

MGARCH(1,1)-BEKK Unconditional Covariance Matrix

BEKK model

vec (ǫtǫ′

t) = vec (CC′) + (A1 ⊗A1) vec(ǫt−1ǫ

′

t−1

)

+(B1 ⊗B1)[vec(ǫt−1ǫ

′

t−1

)− vec (Vt−1)

]+ vec (Vt)

E [vec (ǫtǫ′

t)] = vec (CC′)+[(A1 ⊗A1) + (B1 ⊗B1)]E[vec(ǫt−1ǫ

′

t−1

)]

vec (Σ) = [IN2 − (A1 ⊗A1)− (B1 ⊗B1)]−1 vec (CC′)

or in vech representation as

DNvech (E (ǫtǫ′

t)) = DNvech (CC′) + (A1 ⊗A1)DNvech(E(ǫt−1ǫ

′

t−1

))

+(B1 ⊗B1)DNvech(E(ǫt−1ǫ

′

t−1

))

vech (Σ) =[IN∗ −D+

N (A1 ⊗A1)DN −D+N (B1 ⊗B1)DN

]−1

vech (CC′)

N∗ = N (N + 1) /2.

Eduardo Rossi c© - Econometria finanziaria 2010 41

MGARCH(1,1)-Diagonal models - Covariance stationarity

• The diagonal vech model is stationary if and only if the sum

a∗ii + b∗ii < 1 for all i.

• In the diagonal BEKK model the covariance stationary condition

is that a2ii + b2ii < 1.

Only in the case of diagonal models the stationarity properties are

determined solely by the diagonal elements of the Ai and Bi

matrices.

Eduardo Rossi c© - Econometria finanziaria 2010 42

Asymmetric MGARCH-in-mean model

A general multivariate model can be written as:

yt = µ+Π (L)yt−1 +Ψxt−1 +Λvech (Ht) + ǫt (4)

yt : (N × 1)

Π (L) = Π1 +Π2L+ · · ·+ΠkLk−1 (N ×N)

Ψ : (N × L)

Λ : (N ×N (N + 1) /2)

xt : (L× 1)

Eduardo Rossi c© - Econometria finanziaria 2010 43

Asymmetric MGARCH-in-mean model

xt−1 contains predetermined variables. ǫt is the vector of innovation

with respect to the information set formed exclusively of past

realizations of yt.

Ht = Et−1 (ǫtǫ′

t)

Ht = CC′ +

q∑

i=1

Ai (ǫt−i + γ) (ǫt−i + γ)′

A′

i +

p∑

j=1

BjHt−jB′

j (5)

Eduardo Rossi c© - Econometria finanziaria 2010 44

Asymmetric MGARCH-in-mean model

We can consider a multivariate generalization of the size effect and

sign effect:

Ht = CC′+A1ǫt−1ǫ′

t−1A′

1+B1Ht−1B′

1+Dvt−1v′

t−1D′+Gǫt−1ǫ

′

t−1G′

where vt = |zt| − E |zt|, with zit = εit/√hii,t and

G =

I (ε1t−1 < 0) g11 0 . . . 0

0. . .

......

. . . 0

0 . . . 0 I (εNt−1 < 0) gNN

Eduardo Rossi c© - Econometria finanziaria 2010 45

Asymmetric MGARCH-in-mean model

When N = 2

vt−1v′

t−1 =

∣

∣

∣ε1t−1/

√

h11,t−1

∣

∣

∣− E

∣

∣

∣ε1t−1/

√

h11,t−1

∣

∣

∣

∣

∣

∣ε2t−1/

√

h22,t−1

∣

∣

∣− E

∣

∣

∣ε2t−1/

√

h22,t−1

∣

∣

∣

×

∣

∣

∣ε1t−1/

√

h11,t−1

∣

∣

∣− E

∣

∣

∣ε1t−1/

√

h11,t−1

∣

∣

∣

∣

∣

∣ε2t−1/

√

h22,t−1

∣

∣

∣− E

∣

∣

∣ε2t−1/

√

h22,t−1

∣

∣

∣

′

=

(|z1t| − E |z1t|)2 (|z1t| − E |z1t|) (|z2t| − E |z2t|)

(|z2t| − E |z2t|) (|z1t| − E |z1t|) (|z2t| − E |z2t|)2

Eduardo Rossi c© - Econometria finanziaria 2010 46

Asymmetric MGARCH-in-mean model

Gǫt−1ǫ′

t−1G′ =

g∗211ε

21t−1 g∗11g

∗

22ε1t−1ε2t−1

g∗11g∗

22ε1t−1ε2t−1 g∗222ε22t−1

=

I (ε1t−1 < 0) g211ε

21t−1 δ12g11g22ε1t−1ε2t−1

δ12g11g22ε1t−1ε2t−1 I (ε2t−1 < 0) g222ε22t−1

δ12 = I (ε1t−1 < 0) I (ε2t−1 < 0)

Eduardo Rossi c© - Econometria finanziaria 2010 47

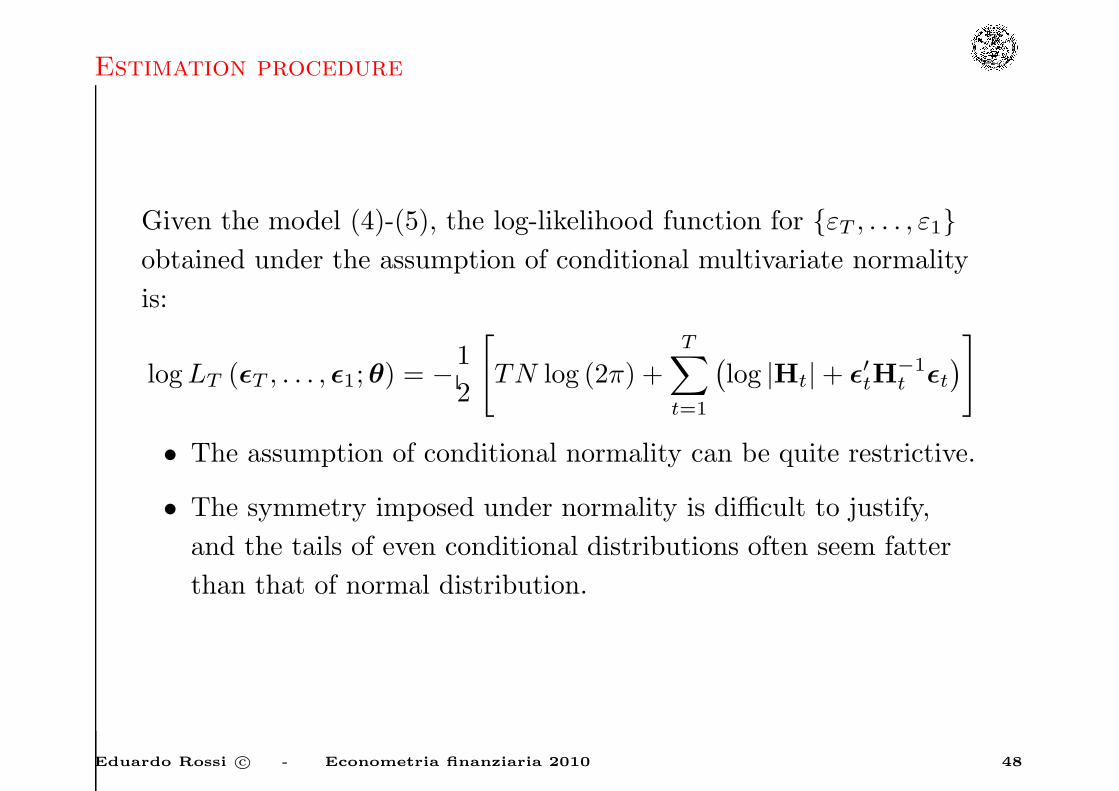

Estimation procedure

Given the model (4)-(5), the log-likelihood function for {εT , . . . , ε1}obtained under the assumption of conditional multivariate normality

is:

logLT (ǫT , . . . , ǫ1; θ) = −1

2

[TN log (2π) +

T∑

t=1

(log |Ht|+ ǫ′tH

−1t ǫt

)]

• The assumption of conditional normality can be quite restrictive.

• The symmetry imposed under normality is difficult to justify,

and the tails of even conditional distributions often seem fatter

than that of normal distribution.

Eduardo Rossi c© - Econometria finanziaria 2010 48

Estimation procedure

Let {(yt,xt) : t = 1, 2, . . .} be a sequence of observable random

vectors with yt (N × 1) and xt (L× 1).

The vector yt contains the ”endogenous” variables and xt contains

contemporaneous ”exogenous” variables.

wt = (xt,yt−1,xt−1, . . . , y1,x1) .

The conditional mean and variance functions are jointly

parameterized by a finite dimensional vector θ:

{µt (wt, θ) , θ ∈ Θ}

{Ht (wt, θ) , θ ∈ Θ}where Θ ⊂ R

P and µt and Ht are known functions of wt and θ.

Eduardo Rossi c© - Econometria finanziaria 2010 49

Estimation procedure

The validity of most of the inference procedures is proven under the

null hypothesis that the first two conditional moments are correctly

specified, for some θ0 ∈ Θ,

E (yt |wt ) = µt (wt, θ0)

V ar (yt |wt ) = Ht (wt, θ0) t = 1, 2, . . .

The procedure most often used to estimate θ0 is the maximization of

a likelihood function that is constructed under the assumption that

yt |wt ∼ N (µt,Ht).

The approach taken here is the same, but the subsequent analysis

does not assume that yt has a conditional normal distribution.

Eduardo Rossi c© - Econometria finanziaria 2010 50

Estimation procedure

For observation t the quasi-conditional log-likelihood is

lt (θ;yt, wt) = −N2ln (2π)− 1

2ln |Ht (wt, θ)|

−1

2(yt − µt (wt, θ))

′

H−1t (wt, θ) (yt − µt (wt, θ))

Letting

ǫt (yt, wt, θ0) ≡ yt − µt (wt, θ) : (N × 1)

denote the residual function

lt (θ) = −N2log (2π)− 1

2log |Ht (θ)| −

1

2ǫ′t (θ)H

−1t (θ) ǫt (θ)

logLT (θ) =

T∑

t=1

lt (θ)

Eduardo Rossi c© - Econometria finanziaria 2010 51

Estimation procedure

If µt (wt, θ) and Ht (wt, θ) are differentiable on Θ for all relevant wt,

and if Ht (wt, θ) is nonsingular with probability one for all θ ∈ Θ,

then the differentiation of the loglik yields the (1× P ) score function

st (θ):

st (θ)′

= ∇θlt (θ)′ −∇θµt (θ)

′

H−1t (θ) ǫt (θ) +

1

2∇θHt (θ)

′[H−1

t (θ)⊗H−1t (θ)

]vec

[ǫt (θ) ǫt (θ)

′ −Ht (θ)]

where

∇θµt (θ) : (N × P )

∇θHt (θ) :(N2 × P

)

Eduardo Rossi c© - Econometria finanziaria 2010 52

Estimation procedure

If the first conditional two moments are correctly specified, the true

error vector is defined as

ǫ0t ≡ ǫt (θ0) = yt − µt (wt, θ0)

and E(ǫ0t |wt

)= 0,

E(ǫ0t ǫ

0′t |wt

)= Ht (wt, θ0)

It follows that under correct specification of the first two conditional

moments of yt given wt:

E [st (θ0) |wt ] = 0

The score evaluated at the true parameter is a vector of martingale

difference with respect to the σ − fields {σ (yt, wt) : t = 1, 2, . . .}.This result can be used to establish weak consistency of the

quasi-maximum likelihood estimator (QMLE).

Eduardo Rossi c© - Econometria finanziaria 2010 53

Estimation procedure

For robust inference we also need an expression for the hessian

ht (θ) of lt (θ). Define the positive semidefinite matrix

at (θ0) = −E [∇θst (θ0) |wt ] = E [−ht (θ0) |wt ] : (P × P )

at (θ0) = ∇θµt (θ0)′

H−1t (θ0)∇θµt (θ0)

+1

2∇θHt (θ)

′[H−1

t (θ)⊗H−1t (θ)

]∇θHt (θ)

When the normality assumption holds the matrix at (θ0) is the

conditional information matrix. However, if yt does not have a

conditional normal distribution then

V ar [st (θ0) |wt ] 6= at (θ0)

and the information matrix equality is violated.

Eduardo Rossi c© - Econometria finanziaria 2010 54

Estimation procedure

The QMLE has the following properties:

[A0−1

T B0TA

0−1T

]−1/2√T(θT − θ0

)d→ N (0, IP )

where

A0T ≡ − 1

T

T∑

t=1

E [ht (θ0)] =1

T

T∑

t=1

E [at (θ0)]

and

B0T ≡ V ar

[T−1/2ST (θ0)

]=

1

T

T∑

t=1

E[st (θ0)

′ st (θ0)]

in addition

AT −A0T

p→ 0

BT −B0T

p→ 0

Eduardo Rossi c© - Econometria finanziaria 2010 55

Estimation procedure

The matrix A−1T BT A

−1T is a consistent estimator od the robust

asymptotic covariance matrix of√T(θT − θ0

).

In practice,

θT ≈ N(θ, A−1

T BT A−1T /T

)

Under normality, the variance estimator can be replaced by A−1T /T

(Hessian form) or B−1T /T (outer product of the gradient form).

Eduardo Rossi c© - Econometria finanziaria 2010 56

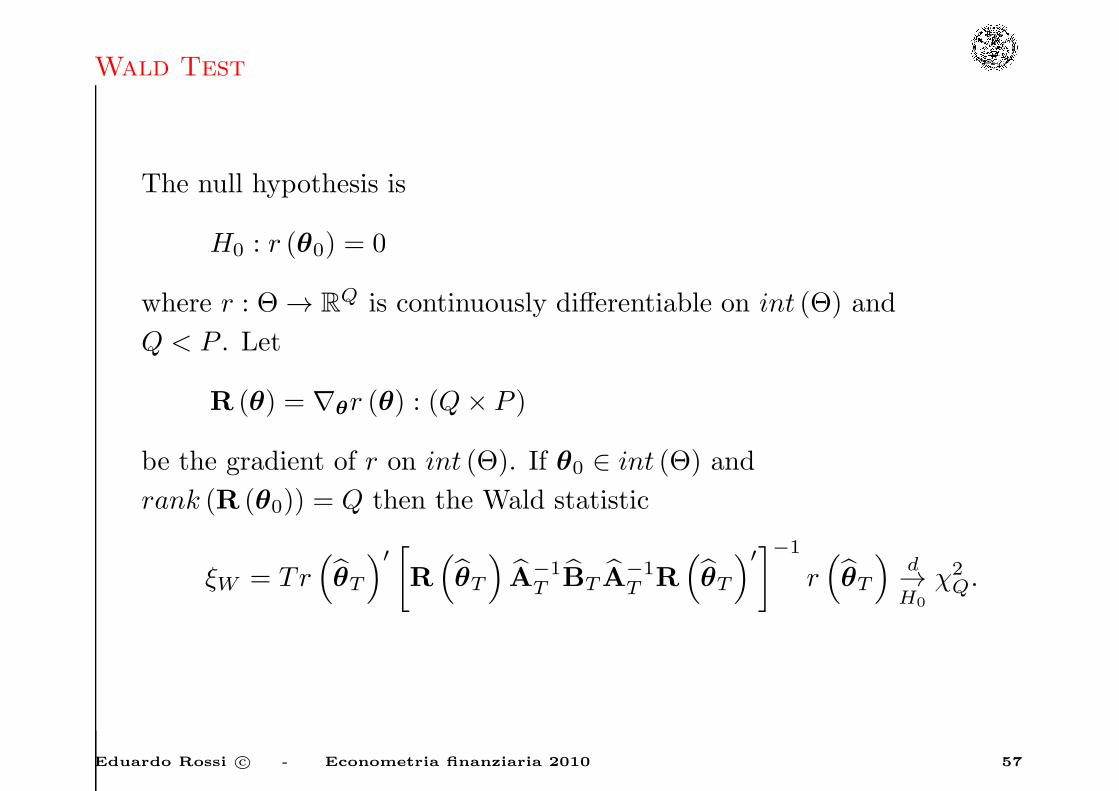

Wald Test

The null hypothesis is

H0 : r (θ0) = 0

where r : Θ → RQ is continuously differentiable on int (Θ) and

Q < P . Let

R (θ) = ∇θr (θ) : (Q× P )

be the gradient of r on int (Θ). If θ0 ∈ int (Θ) and

rank (R (θ0)) = Q then the Wald statistic

ξW = Tr(θT

)′

[R(θT

)A−1

T BT A−1T R

(θT

)′

]−1

r(θT

)d→H0

χ2Q.

Eduardo Rossi c© - Econometria finanziaria 2010 57

Factor-GARCH

The Factor GARCH model, introduced by Engle et al. (1990), can be

thought of as an alternative simple parametrization of the BEKK

model. Suppose that the (N × 1) yt has a factor structure with K

factors given by the K × 1 vector ft and a time invariant factor

loadings given by the N ×K matrix B:

yt = Bft + ǫt

Eduardo Rossi c© - Econometria finanziaria 2010 58

Factor-GARCH

Assume that the idiosyncratic shocks ǫt have conditional covariance

matrix Ψ which is constant in time and positive semidefinite, and

that the common factors are characterized by

Et−1 (ft) = 0

Et−1 (ftf′

t) = Λt

Λt = diag (λ1, . . . , λK) and positive definite. The conditioning set is

{yt−1, ft−1, . . . ,y1, f1}. Also suppose that E (ftǫ′

t) = 0. The

conditional covariance matrix of yt equals

Et−1 (yty′

t) = Ht = Ψ+BΛtB′ = Ψ+

K∑

k=1

βkβ′

kλkt

where βk denotes the kth column in B. Thus, there are K statistics

which determine the full covariance matrix.

Eduardo Rossi c© - Econometria finanziaria 2010 59

Factor-GARCH

Forecasts of the variances and covariances or of any portfolio of

assets, will be based only on the forecasts of these K statistics.

There exists factor-representing portfolios with portfolio weights that

are orthogonal to all but one set of factor loadings:

rkt = φ′

kyt

φ′

kβj =

1 k = j

0 otherwise

the vector of factor-representing portfolios is

rt = Φ′yt

where the columns of matrix Φ are the φk vectors.

Eduardo Rossi c© - Econometria finanziaria 2010 60

Factor-GARCH

The conditional variance of rkt is given by

Vart−1 (rkt) = φ′

kEt−1 (yty′

t)φk = φ′

kHtφk

= φ′

k (Ψ +BΛtB′)φk

= ψk + λkt

where ψk = φ′

kΨφk. The portfolio has the exact time variation as the

factors, which is why they are called factor-representing portfolios. In

order to estimate this model, the dependence of the λkt’s upon the

past information set must also be parameterized:

θkt ≡ φ′

kHtφk = V art−1 (rkt) = ψk + λkt

So we get that

K∑

k=1

βkβ′

kθkt =K∑

k=1

βkβ′

kψk +K∑

k=1

βkβ′

kλkt

Eduardo Rossi c© - Econometria finanziaria 2010 61

Factor-GARCH

K∑

k=1

βkβ′

kλkt =K∑

k=1

βkβ′

kθkt −K∑

k=1

βkβ′

kψk

Ht = Ψ+K∑

k=1

βkβ′

kλkt = Ψ+K∑

k=1

βkβ′

kθkt −K∑

k=1

βkβ′

kψk

= Ψ∗ +

K∑

k=1

βkβ′

kθkt

where Ψ∗ =

(Ψ−

K∑k=1

βkβ′

kψk

).

Eduardo Rossi c© - Econometria finanziaria 2010 62

Factor-GARCH

The simplest assumption is that there is a set of factor-representing

portfolios with univariate GARCH(1,1) representations. The

conditional variance θkt follows a GARCH(1,1) process

θkt = ωk + αk

(φ′

kǫt−1

)2+ γkEt−2

(r2kt−1

)

θkt = ωk + αkφ′

k

(ǫt−1ǫ

′

t−1

)φk + γkEt−2

[(φ′

kyt) (

φ′

kyt)]

θkt = ωk + αkφ′

k

(ǫt−1ǫ

′

t−1

)φk + γk

[φ′

kEt−2 (yty′

t)φk

]

θkt = ωk + αkφ′

k

(ǫt−1ǫ

′

t−1

)φk + γk

[φ′

kHt−1φk

]

Eduardo Rossi c© - Econometria finanziaria 2010 63

Factor-GARCH

The conditional variance-covariance matrix of yt can be written as

Ht = Ψ∗ +K∑

k=1

βkβ′

kθkt

= Ψ∗ +K∑

k=1

βkβ′

k

{ωk + αk

[φ′

k

(ǫt−1ǫ

′

t−1

)φk

]+ γk

[φ′

kHt−1φk

]}

=

(Ψ∗ +

K∑

k=1

βkβ′

kωk

)+

K∑

k=1

βkβ′

k

{αk

[φ′

k

(ǫt−1ǫ

′

t−1

)φk

]+ γk

[φ′

kHt−1φk

Ht = Γ +K∑

k=1

βkβ′

kθkt

Eduardo Rossi c© - Econometria finanziaria 2010 64

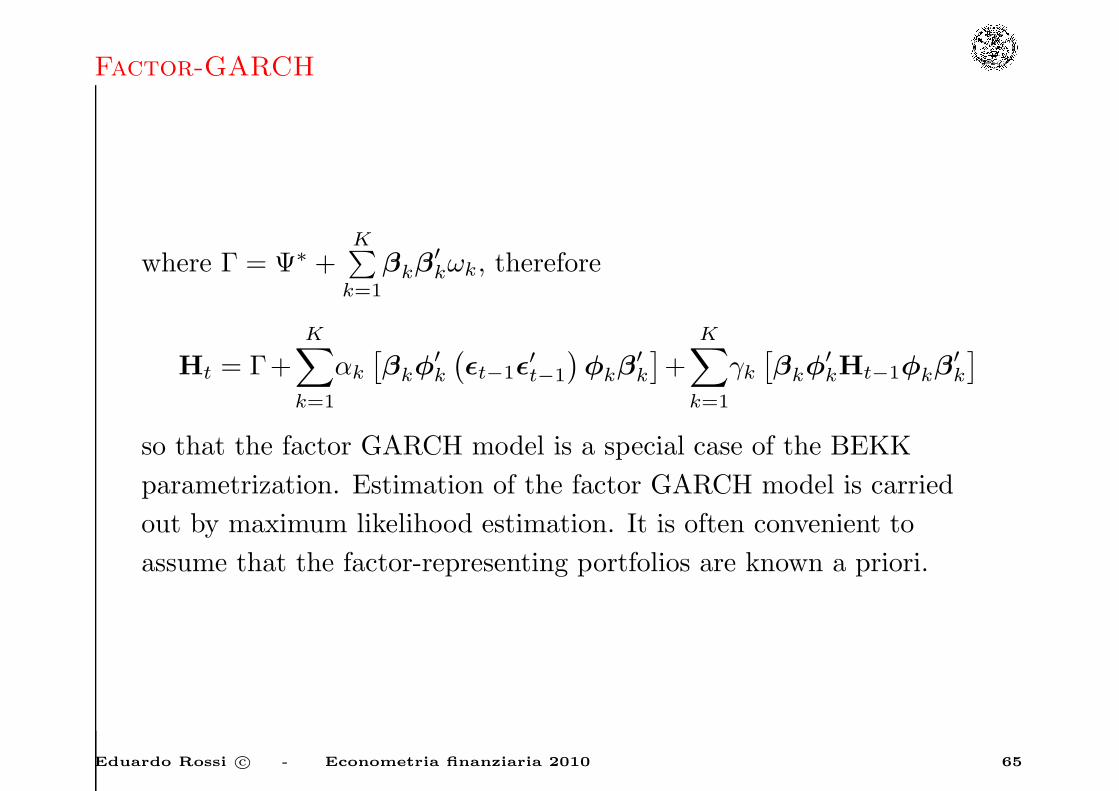

Factor-GARCH

where Γ = Ψ∗ +K∑

k=1

βkβ′

kωk, therefore

Ht = Γ+K∑

k=1

αk

[βkφ

′

k

(ǫt−1ǫ

′

t−1

)φkβ

′

k

]+

K∑

k=1

γk[βkφ

′

kHt−1φkβ′

k

]

so that the factor GARCH model is a special case of the BEKK

parametrization. Estimation of the factor GARCH model is carried

out by maximum likelihood estimation. It is often convenient to

assume that the factor-representing portfolios are known a priori.

Eduardo Rossi c© - Econometria finanziaria 2010 65

Orthogonal-GARCH model

The orthogonal models are particular factor models. They are based

on the assumption that the observed data can be obtained by a linear

transformation of a set of uncorrelated components.

The components are the principal components of the data, or a

subset of them.

The diagonal matrix V contains the empirical variances of yt:

V = diag{s21, . . . , s2N}

the standardized returns are

ut = V−1/2yt

E[ut] = 0 E[utu′

t] = R

Eduardo Rossi c© - Econometria finanziaria 2010 66

Orthogonal-GARCH model

The sample correlation matrix can be decomposed as:

R = PΛP′

P is the orthonormal eigenvectors matrix, Λ is the diagonal matrix of

the eigenvalues:

Λ = diag{λ1, . . . , λN}

ranked in descending order.

Eduardo Rossi c© - Econometria finanziaria 2010 67

Orthogonal-GARCH model

P satisfies:

P′ = P−1 P′P = IN PP′ = IN

It follows that

R = PΛ1/2Λ1/2P′ = LL′

L = PΛ1/2

Principal components

ft = L−1ut

E[ftf′

t ] = L−1E[utu′

t]L−1′ = L−1RL−1′

= L−1LL′L′−1 = IN

Eduardo Rossi c© - Econometria finanziaria 2010 68

Orthogonal-GARCH model

Assuming

Et−1[ftf′

t ] = Qt = diag(σ2f1,t , . . . , σ

2fN,t

)

Qt is a diagonal matrix.

σ2fi,t ∼ GARCH(p,q) i = 1, 2, . . . , N

Et−1[utu′

t] = Et−1[Lftf′

tL′] = LQtL

′

Et−1[yty′

t] = Et−1[V1/2utu

′

tV1/2] = V1/2LQtL

′V1/2

Eduardo Rossi c© - Econometria finanziaria 2010 69

Orthogonal-GARCH model

We can work with a reduced number m < N of principal components

(eigenvalues), those which explain most of the variation in the data.

L−1 is replaced by a matrix (m×N):

Λ−1/2m P′

m

Pm is a matrix (N ×m) containing the m eigenvectors of P

corresponding to the m largest eigenvalues.

fmt = Λ−1/2m P′

mut

where fmt = [f1t, . . . , fmt]

Et−1[fmt ] = 0

Et−1[fmt fm

′

t ] = Qt = diag(σ2f1,t , . . . , σ

2fm,t

)

Eduardo Rossi c© - Econometria finanziaria 2010 70

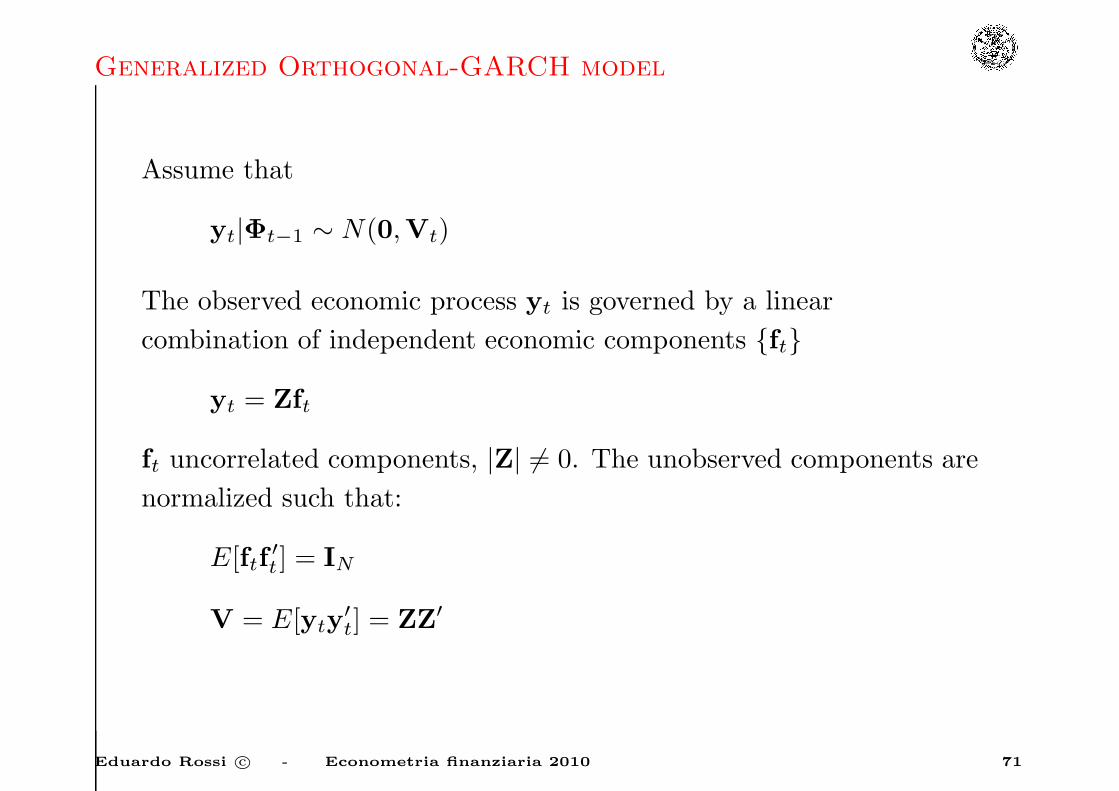

Generalized Orthogonal-GARCH model

Assume that

yt|Φt−1 ∼ N(0,Vt)

The observed economic process yt is governed by a linear

combination of independent economic components {ft}

yt = Zft

ft uncorrelated components, |Z| 6= 0. The unobserved components are

normalized such that:

E[ftf′

t ] = IN

V = E[yty′

t] = ZZ′

Eduardo Rossi c© - Econometria finanziaria 2010 71

Generalized Orthogonal-GARCH model

Vt = Et−1[yty′

t] = ZEt−1[ftf′

t]Z′ = ZHtZ

′

Ht = diag{h1,t, . . . , hN,t}

hi,t = (1− α1 − βi) + αiy2i,t−i + βihi,t−1 i = 1, . . . , N

V = E[Vt] = ZHZ′

H diagonal. The diagonal decomposition of the unconditional

covariance matrix:

V = PΛP′

P: orthogonal matrix, O-GARCH estimator for Z, is only guaranteed

to coincide with Z, when the diagonal elements of H are all distinct.

Eduardo Rossi c© - Econometria finanziaria 2010 72

Generalized Orthogonal-GARCH model

Suppose that H = I

V = E[Vt] = ZIZ′ = ZZ′

The matrix Z is no longer identified by the eigenvector matrix of V

as for every orthogonal matrix Q we have

(ZQ)(ZQ)′ = I

The matrix Z is well identified when conditional information is taken

into account. Based on singular value decomposition:

PΛ1/2U0 = Z

Let the estimator of U0 be U. We restrict

|U| = 1.

Eduardo Rossi c© - Econometria finanziaria 2010 73

Generalized Orthogonal-GARCH model

The matrices P and Λ have N(N−1)2 and N parameters, so we have

N2 parameters for the invertible matrix Z.

The matrices P and Λ will be estimated by means of unconditional

information, as they will extracted from the sample covariance

matrix V (N(N+1)2 parameters). Conditional information is required

to estimate U0 (N(N−1)2 free parameters).

The orthogonal U0 is parameterized by means of rotation matrices.

Eduardo Rossi c© - Econometria finanziaria 2010 74

Generalized Orthogonal-GARCH model

Rotation matrix: Grs, (N ×N), r, s ∈ N, r < s ≤ N :

Grs = {gij}grr = gss = cos(θ)

gii = 1 i = 1, . . . , N i 6= r, s

gsr = − sin(θ)

grs = sin(θ)

and all other elements are zero. N = 3:

G12 =

cos(θ) sin(θ) 0

− sin(θ) cos(θ) 0

0 0 1

Eduardo Rossi c© - Econometria finanziaria 2010 75

Generalized Orthogonal-GARCH model

Every N-dimensional orthogonal matrix U with det(U) = 1 can be

represented as a product of N(N−1)2 rotation matrices:

U =∏

i<j

Gij(θij) − π ≤ θij ≤ π

Gij(θij) performs a rotation in the plane spanned by the i-th and the

j-th vectors of the canonical basis of RN over an angle δij .

N = 3:

U = G12G13G23

Eduardo Rossi c© - Econometria finanziaria 2010 76

Generalized Orthogonal-GARCH model

Time-varying conditional correlations:

Rt = D−1t VtD

−1t

Dt = (Vt ⊙ Im)1/2

N = 2

Z =

1 0

cos θ sin θ

θ measures the extent to which the uncorrelated components are

mapped in the same direction. For θ = 0 the mapping in not

invertible, yielding perfect correlation between the observed variables,

whereas θ = π2 , Z = I so that observed variables are completely

uncorrelated.

Eduardo Rossi c© - Econometria finanziaria 2010 77

Generalized Orthogonal-GARCH model

ρt =Covt−1(y1t, y2t)√

V art−1(y1t)√V art−1(y2t)

In this example the conditional correlation is:

ρt =h1t cos (θ)

√h1t

√h1t cos2 (θ) + h2t sin

2 (θ)

=cos (θ)√

cos2 (θ) + h1t

h2tsin2 (θ)

=1√

1 + zt tan2 (θ)

where zt =h1t

h2t.

Note that a constant linkage Zθ gives rise to time-varying correlations

between the observed variables. These correlations rise on average

when the components are mapped more in the same direction.

Eduardo Rossi c© - Econometria finanziaria 2010 78

Generalized Orthogonal-GARCH model

Suppose GO-GARCH(1,1) parameters to be estimated by means of

the conditional information are (α′,β′, θ′)′

α = (α1, . . . , αN ) β = (β1, . . . , βN )

θ = (θ1, . . . , θm) m =N(N − 1)

2The log-likelihood can be expressed:

lt = −1

2

(N log(2π) + log |Vt|+ y′

tV−1t yt

)

= −1

2

(N log(2π) + log |ZθHtZ

′

θ|+ f ′tZ′

θ(ZθHtZ′

θ)−1Zθft

)

= −1

2

(N log(2π) + log |ZθZ

′

θ|+ log |Ht|+ f ′tZ′

θ(ZθHtZ′

θ)−1Zθft

)

= −1

2

(N log(2π) + log |ZθZ

′

θ|+ log |Ht|+ f ′tH−1t ft

)

logLT =∑

t

lt

Eduardo Rossi c© - Econometria finanziaria 2010 79

Generalized Orthogonal-GARCH model

Two-step estimation

1. Zθ = PΛ1/2U0 where P and Λ from the sample covariance

matrix:

V = PΛP′

Zθ = PΛ1/2U

where

U =∏

i<j

Gij(θij) − π ≤ θij ≤ π

2. Estimate (α′,β′, θ′)′ by maximizing the logLT .

Eduardo Rossi c© - Econometria finanziaria 2010 80

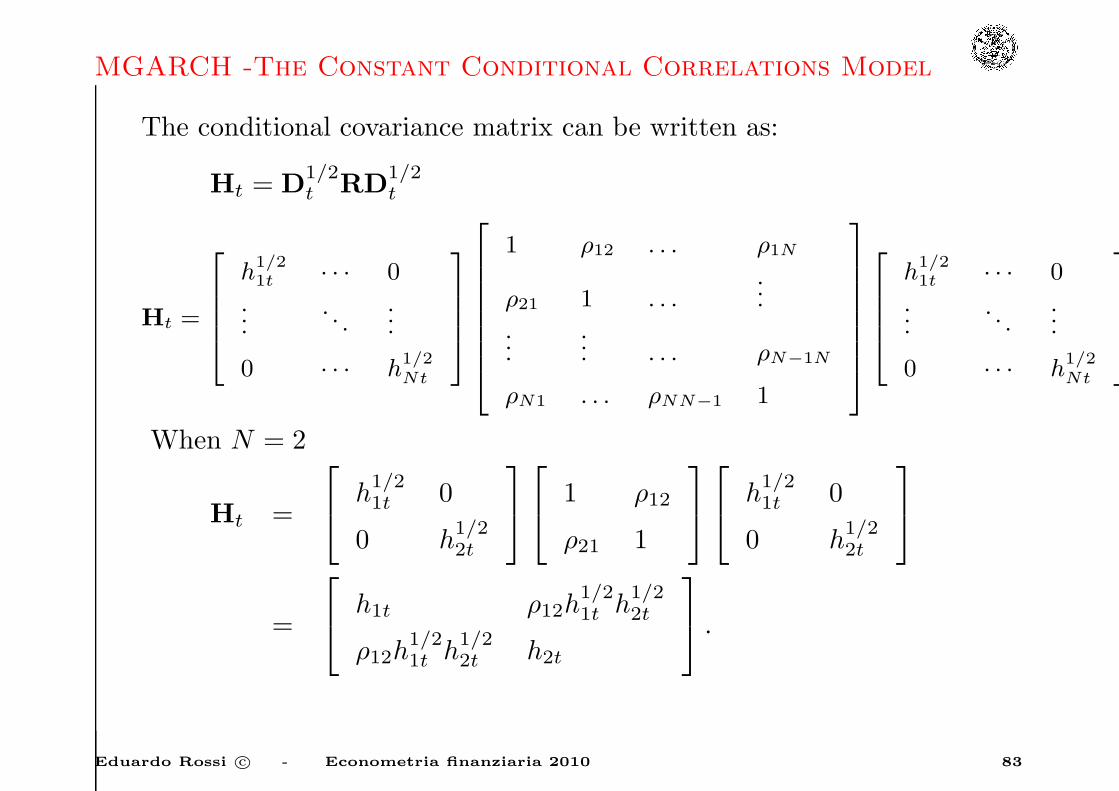

MGARCH -The Constant Conditional Correlations Model

• These models are based on a decomposition of the Ht.

• The conditional var-cov matrix is expressed as

Ht = DtRtDt

where Rt is possibly time-varying.

• Conditional correlations and variances are separately modeled.

Eduardo Rossi c© - Econometria finanziaria 2010 81

MGARCH -The Constant Conditional Correlations Model

Bollerslev (1990) Constant Conditional Correlations model:

The time-varying conditional covariances are parameterized to be

proportional to the product of the corresponding conditional

standard deviations. The model assumptions are:

Et−1 [ǫtǫ′

t] = Ht

{Ht}ii = hit i = 1, . . . , N

{Ht}ij = hijt = ρijh1/2it h

1/2jt i 6= j i, j = 1, . . . , N

Dt = diag {h1t, . . . , hNt}

Eduardo Rossi c© - Econometria finanziaria 2010 82

MGARCH -The Constant Conditional Correlations Model

The conditional covariance matrix can be written as:

Ht = D1/2t RD

1/2t

Ht =

h1/21t · · · 0

.... . .

...

0 · · · h1/2Nt

1 ρ12 . . . ρ1N

ρ21 1 . . ....

...... . . . ρN−1N

ρN1 . . . ρNN−1 1

h1/21t · · · 0

.... . .

...

0 · · · h1/2Nt

When N = 2

Ht =

h

1/21t 0

0 h1/22t

1 ρ12

ρ21 1

h

1/21t 0

0 h1/22t

=

h1t ρ12h

1/21t h

1/22t

ρ12h1/21t h

1/22t h2t

.

Eduardo Rossi c© - Econometria finanziaria 2010 83

MGARCH -The Constant Conditional Correlations Model

• The sequence of conditional covariance matrices {Ht} is

guaranteed to be positive definite a.s. for all t, If the conditional

variances along the diagonal in the Dt matrices are all positive,

and the conditional correlation matrix R is positive definite

• Furthermore the inverse of Ht is given by

H−1t = D

−1/2t R−1D

−1/2t .

When calculating the log-likelihood function only one matrix

inversion is required for each evaluation.

• CCC is generally estimated in two steps:

1. conditional variances are estimated employing the marginal

likelihoods

2. R is estimated using the sample estimator of standardized

residuals D−1t yt (assuming µt = 0).

Eduardo Rossi c© - Econometria finanziaria 2010 84

MGARCH -The Constant Conditional Correlations Model

• The CCC solves the curse of dimensionality problem of

MGARCH models

• The number of parameters is O(N2) but these are not jointly

estimated. The two-step estimation procedure impacts on the

computational issues.

• Asymptotic properties of QMLE estimators verified in McAleer

and Ling (2003).

Eduardo Rossi c© - Econometria finanziaria 2010 85

The Dynamic Conditional Correlation GARCH Model

The CCC has two main limitations:

1. No spillover neither feedback effects across conditional variances

2. Correlations are static

The evolution of CCC is the Dynamic Conditional Correlation

(DCC) Model of Engle (2002). The DCC is an extension of the

Bollerslev’s CCC Model.

Eduardo Rossi c© - Econometria finanziaria 2010 86

The Dynamic Conditional Correlation GARCH Model

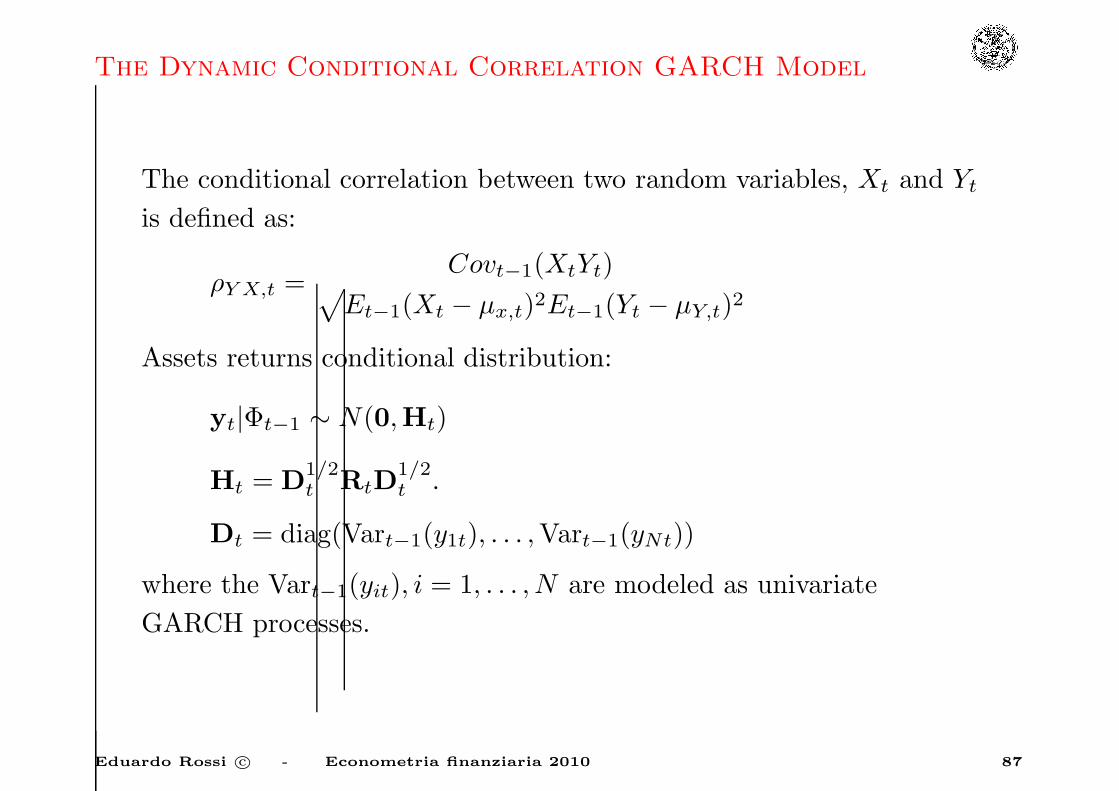

The conditional correlation between two random variables, Xt and Yt

is defined as:

ρY X,t =Covt−1(XtYt)√

Et−1(Xt − µx,t)2Et−1(Yt − µY,t)2

Assets returns conditional distribution:

yt|Φt−1 ∼ N(0,Ht)

Ht = D1/2t RtD

1/2t .

Dt = diag(Vart−1(y1t), . . . ,Vart−1(yNt))

where the Vart−1(yit), i = 1, . . . , N are modeled as univariate

GARCH processes.

Eduardo Rossi c© - Econometria finanziaria 2010 87

The Dynamic Conditional Correlation GARCH Model

The standardized returns are:

ηt = D−1/2t yt

Et−1(ηtη′

t) = D−1/2t HtD

−1/2t = Rt = {ρij,t}

we can use the conditional variance of ηt to describe the conditional

correlation of yt.

The conditional correlation estimator is

ρij,t =qij,t√qii,tqjj,t

.

Where qij,t are assumed to follow a GARCH(1,1) model

qij,t = ρij + α(ηi,t−1ηj,t−1 − ρij) + β(qij,t−1 − ρij) (6)

The term ρij is not the unconditional correlation between ηit and ηjt;

the unconditional correlation between ηit and ηjt has no closed form.

Eduardo Rossi c© - Econometria finanziaria 2010 88

The Dynamic Conditional Correlation GARCH Model

Engle (2002) assumes that ρij ≃ qij . However, Aielli (2006) and

Engle et al. (2008) suggest to modify the standard DCC in order to

correct the asymptotic bias which is due to the fact that 1T

∑t ǫtǫ

′

t

does not converge to Q. It is known though that the impact of this is

very small (see Engle and Sheppard (2001)).

Eduardo Rossi c© - Econometria finanziaria 2010 89

The Dynamic Conditional Correlation GARCH Model

The conditional covariance matrix is positive definite, Qt, as long as

it is a weighted average of definite matrices and semidefinite matrices.

To ensure p.-d-ness of Qt we must impose α+ β < 1 In matrix from:

Qt = Q(1− α− β) + α(ηt−1η′

t−1) + β(Qt−1) (7)

where Q is the unconditional covariance matrix of ηt.

Eduardo Rossi c© - Econometria finanziaria 2010 90

The DCC - Correlation targeting

DCC model has correlation targeting, when α+ β < 1

E[Qt] = R

E[Qt] = E[Qt−1]

E[ηtη′

t] = E[Qt]

E[Qt] = Q(1− α− β) + αE[ηt−1η′

t−1] + βE[Qt−1]

E[Qt] = R(1− α− β) + αE[Qt] + βE[Qt]

Eduardo Rossi c© - Econometria finanziaria 2010 91

The DCC - Correlation targeting

Clearly more complex positive definite multivariate GARCH models

could be used for the correlation parameterization as long as the

unconditional moments are set to the sample correlation matrix.

For example, the MARCH family of Ding and Engle (2001) can be

expressed in first order form as:

Qt = Q⊙ (ιι′ −A−B) +A⊙ ǫt−1ǫ′

t−1 +B⊙Qt−1 (8)

where ⊙ denotes the Hadamard product ({A⊙B}ij = aijbij).

Eduardo Rossi c© - Econometria finanziaria 2010 92

The DCC - Correlation targeting

The Generalized-DCC model specification:

Dt = diag{ωi}+ diag{κi} ⊙ yt−1y′

t−1 + diag{λi} ⊙Dt−1

Qt = S⊙ (ιι′ −A−B) +A⊙ ǫt−1ǫ′

t−1 +B⊙Qt−1

Rt = diag{Qt}−1/2Qt diag{Qt}−1/2.

A and B are symmetric matrices.

The assumption of normality gives rise to a likelihood function.

Without this assumption, the estimator will still have the QML

interpretation. The second equation simply expresses the assumption

that each of the assets follows a univariate GARCH process.

Eduardo Rossi c© - Econometria finanziaria 2010 93

The DCC - Correlation targeting

A real square matrix A, is positive definite if and only if

B = A∗−1AA∗−1 is positive definite, with A∗ = diag{A}.In order to ensure that Ht is positive definite we must have that

D−1/2t HtD

−1/2 is positive definite.

Eduardo Rossi c© - Econometria finanziaria 2010 94

The DCC - Correlation targeting

Ht is positive definite ∀t ∈ T , if the following restrictions on the

univariate GARCH parameters are satisfied for all series

i ∈ [1, . . . , N ] :

1. ωi > 0

2. κi and λi such that Dii,t > 0 with probability 1

3. D2ii,0 > 0

4. The roots of 1− κiZ − λiZ are outside the unit circle.

Eduardo Rossi c© - Econometria finanziaria 2010 95

The DCC - Correlation targeting

and the parameters in the DCC satisfy:

1. α ≥ 0

2. β ≥ 0

3. α+ β ≤ 1

4. The minimum eigenvalue of Q0 > δ > 0 (where Q0 must be

positive definite)

Eduardo Rossi c© - Econometria finanziaria 2010 96

The DCC - Correlation targeting

The log-likelihood function can be written as:

logLT = −1

2

T∑

t=1

(N log(2π) + log |Ht|+ r′tH−1t rt)

= −1

2

T∑

t=1

(N log(2π) + log |D1/2t RtD

1/2t |+ r′tD

−1/2t R−1

t D−1/2t rt)

= −1

2

T∑

t=1

(N log(2π) + log |Dt|+ log |Rt|+ ǫ′tR−1t ǫt)

Eduardo Rossi c© - Econometria finanziaria 2010 97

The DCC - Correlation targeting

Adding and subtracting r′tD−1/2t D

−1/2t rt = ǫ′tǫt

logLT = −1

2

T∑

t=1

(N log(2π) + log |Dt|+ r′tD−1/2t D

−1/2t rt

−ǫ′tǫt + log |Rt|+ ǫ′tR−1t ǫt)

= −1

2

T∑

t=1

(N log(2π) + log |Dt|+ r′tD−1t rt)

−1

2

T∑

t=1

(ǫ′tR−1t ǫt − ǫ′tǫt + log |Rt|)

Eduardo Rossi c© - Econometria finanziaria 2010 98

The DCC - Correlation targeting

Volatility component:

LV (θ) ≡ logLV,T (θ) = −1

2

T∑

t=1

(N log(2π) + log |Dt|+ r′tD−1t rt)

Correlation component:

LC(θ,φ) ≡ logLC,T (θ,φ) = −1

2

T∑

t=1

(ǫ′tR−1t ǫt − ǫ′tǫt + log |Rt|)

θ denotes the parameters in Dt and φ the parameters in Rt.

Eduardo Rossi c© - Econometria finanziaria 2010 99

The DCC - Correlation targeting

L(θ,φ) = LV (θ) + LC(θ,φ)

LV (θ) = −1

2

T∑

t=1

N∑

i=1

(log(2π) + log(hi,t) +

r2i,thi,t

).

The likelihood is apparently the sum of individual GARCH

likelihoods, which will be jointly maximized by separately

maximizing each term.

Eduardo Rossi c© - Econometria finanziaria 2010 100

The DCC - Correlation targeting

Two-step procedure:

1.

θ = argmax{LV (θ)}

2.

maxφ

{LC(θ,φ)}.

Under regularity conditions, consistency of the first step will ensure

consistency of the second step. The maximum of the second step will

a function of the first step parameter estimates. If the first step is

consistent then the second step will be too as long as the function is

continuous in a neighborhood of the true parameters.

Eduardo Rossi c© - Econometria finanziaria 2010 101

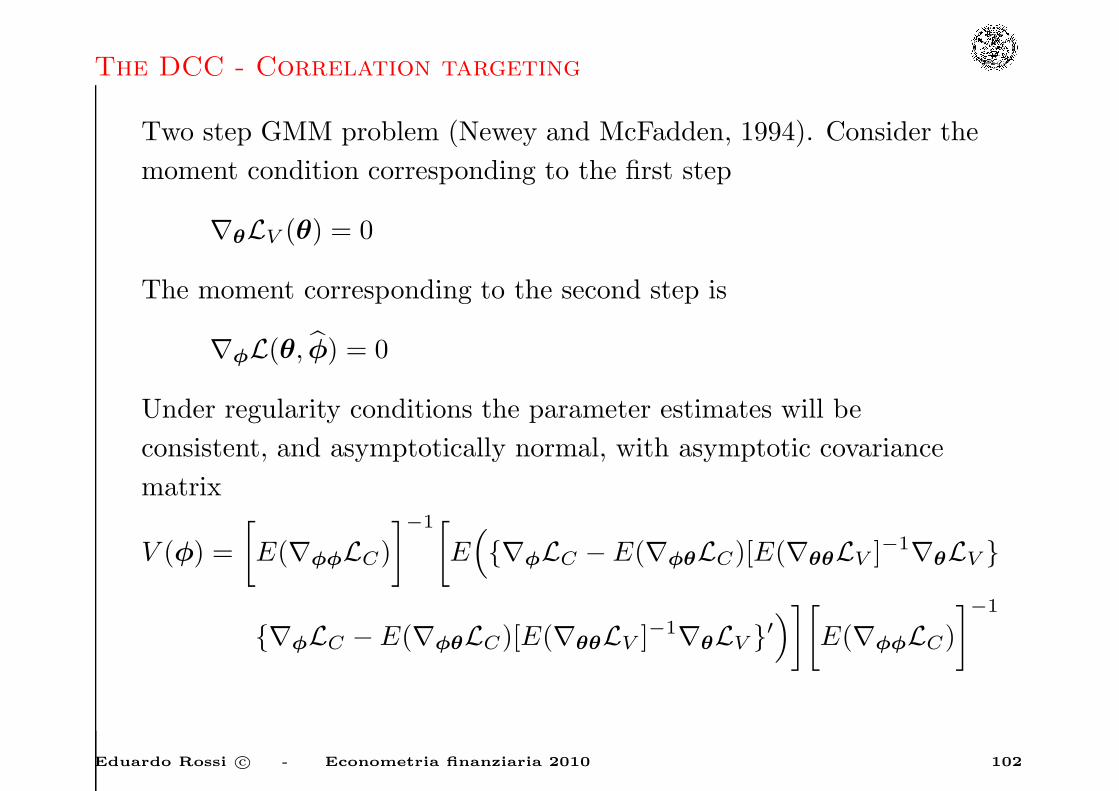

The DCC - Correlation targeting

Two step GMM problem (Newey and McFadden, 1994). Consider the

moment condition corresponding to the first step

∇θLV (θ) = 0

The moment corresponding to the second step is

∇φL(θ, φ) = 0

Under regularity conditions the parameter estimates will be

consistent, and asymptotically normal, with asymptotic covariance

matrix

V (φ) =

[E(∇φφLC)

]−1[

E({∇φLC − E(∇φθLC)[E(∇θθLV ]

−1∇θLV }

{∇φLC − E(∇φθLC)[E(∇θθLV ]−1∇θLV }′

)][E(∇φφLC)

]−1

Eduardo Rossi c© - Econometria finanziaria 2010 102