nada market review: shifting luxury vehicle … perspective/2014...nada market review: shifting...

TRANSCRIPT

April 2014

NADA Market Review:

Shifting Luxury Vehicle Preferences

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 2

© 2014 NADA Used Car Guide

TABLE OF CONTENTS

Introduction ................................................................................................................................. 2

Emerging Trends in Market Share for Luxury Cars & Utility Vehicles ........................................ 2

Value Retention for Luxury Vehicles Revisited ........................................................................... 3

Changes in Used Supply .............................................................................................................. 4

Impact of Supply Growth on Used Prices .................................................................................... 5

Thoughts on the Future ............................................................................................................... 7

At NADA Used Car Guide ............................................................................................................. 8

NADA Market Review: Shifting Luxury Vehicle Preferences

Introduction

Since the Great Recession ended in 2009, the auto industry gradually

recovered as consumer appetite for big purchases returned after

spending fell due to poor economic conditions. With the U.S.

economic recovery in its fifth year, it is interesting to see how much

the luxury automobile market has changed over time, especially with

the increased importance of perceived value. Buyers are becoming

more mindful of how they spend their money, opting for practical

purchases of expensive items rather than frivolous and excessive buys.

This change in mindset was evident in the NADA Spring 2013 Car

Shopper Preference Survey, which revealed quality/dependability as

the most important element in a new vehicle purchase decision. By

looking at the market share of each segment, we can identify

emerging developments in luxury demand and provided insight on

expectations for the future.

Emerging Trends in Market Share for Luxury Cars & Utility Vehicles

Between 2009 and 2013, total light vehicle sales in the United States increased by over

49%; when excluding mainstream vehicle deliveries, we see that luxury sales increased

by over 62%. The growth in luxury consumption translates into a 1.03-percentage point

improvement in market share, which climbed to 12.8% of the total market in 2013.

With the U.S. economic

recovery in its fifth year, it is

interesting to see how much

the luxury automobile market

has changed over time,

especially with increased

importance of perceived

value.

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 3

© 2014 NADA Used Car Guide

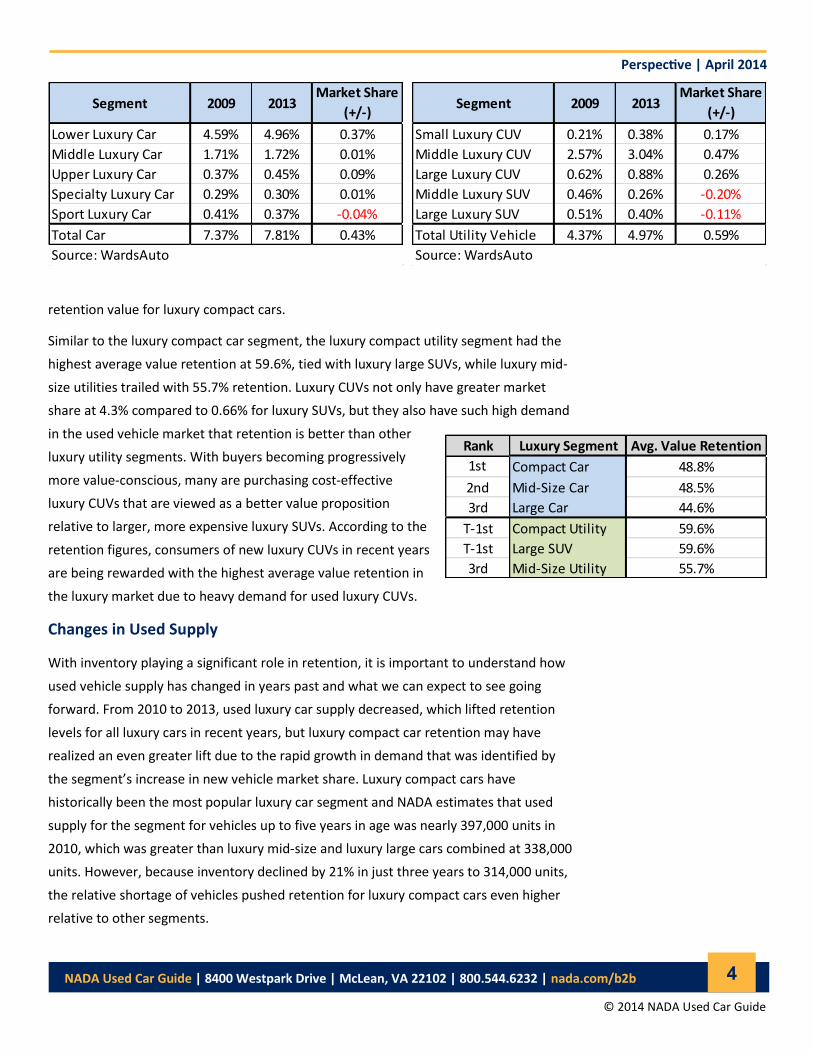

Examining each luxury segment individually shows

that both cars and trucks claimed greater share, but

in different ways. Luxury car share went up by 0.43-

percentage points, primarily due to 0.37-percentage

point growth in the lower luxury car segment while

all others had relatively unchanged market share. As

competition among automakers intensifies in the

entry-level luxury marketplace, the data suggests that

the growth was almost exclusively due to new buyers

entering the market as opposed to a cannibalization

of upper luxury sales taking place.

An examination of market share among luxury utility

vehicles tells a different story: a definitive shift in

consumer preferences has occurred with SUV

demand falling in favor of CUVs. While total luxury

utility vehicle share was up 0.59-percentage points,

middle and large luxury SUVs were down a combined

0.31-percentage points. On the other hand, luxury

CUVs were up 0.9-percentage points, which means

the disparity in market share growth between luxury

CUVs and SUVs was 1.21-percentage points after only

a few years. Thus, a distinct trend in the luxury

segment has been forming with buyers shifting away

from SUV purchases toward more practical CUVs, in addition to the expansion of the

lower luxury car segment.

Value Retention for Luxury Vehicles Revisited

In the February and March 2014 releases of NADA Perspective, which covered value

retention for three-year-old cars and trucks, respectively, we analyzed each segment

individually and discussed how they compare to one another. The average model in the

luxury compact car segment retained 48.8% of its value, besting both the luxury mid-

size and luxury large car segments, which achieved respective averages of 48.5% and

44.6%. Therefore, not only do new luxury compact cars cost less to purchase than their

mid-size and large counterparts, but they also exhibit superior value retention. The

popularity of new lower luxury cars can be seen in the segment’s 4.96% market share

compared to 2.85% for all other luxury car segments combined. Demand also remains

high relative to supply on the used side of the market as is exhibited in the high

4.6% 4.9% 5.1% 4.8% 5.0%

1.7%1.7% 1.5%

1.5%1.7%

0.4%0.5% 0.5%

0.5%0.5%0.3%

0.3% 0.3%0.3%

0.3%0.4%0.3% 0.3%

0.3%0.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2009 2010 2011 2012 2013

Mar

ket

Shar

e

Period

Luxury Car Market Share by Segment

Lower Luxury Car Middle Luxury Car Upper Luxury Car Specialty Luxury Car Sport Luxury Car

Source: WardsAuto

0.2% 0.2% 0.2% 0.3% 0.4%

2.6%2.9% 3.0%

3.1% 3.0%

0.6%

0.8% 0.7%

0.8% 0.9%0.5%

0.5%0.3%

0.3%0.3%

0.5%

0.5%0.5%

0.4%0.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2009 2010 2011 2012 2013

Mar

ket S

hare

Period

Luxury Utility Vehicle Market Share by Segment

Small Luxury CUV Middle Luxury CUV Large Luxury CUV Middle Luxury SUV Large Luxury SUV

Source: WardsAuto

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 4

© 2014 NADA Used Car Guide

retention value for luxury compact cars.

Similar to the luxury compact car segment, the luxury compact utility segment had the

highest average value retention at 59.6%, tied with luxury large SUVs, while luxury mid-

size utilities trailed with 55.7% retention. Luxury CUVs not only have greater market

share at 4.3% compared to 0.66% for luxury SUVs, but they also have such high demand

in the used vehicle market that retention is better than other

luxury utility segments. With buyers becoming progressively

more value-conscious, many are purchasing cost-effective

luxury CUVs that are viewed as a better value proposition

relative to larger, more expensive luxury SUVs. According to the

retention figures, consumers of new luxury CUVs in recent years

are being rewarded with the highest average value retention in

the luxury market due to heavy demand for used luxury CUVs.

Changes in Used Supply

With inventory playing a significant role in retention, it is important to understand how

used vehicle supply has changed in years past and what we can expect to see going

forward. From 2010 to 2013, used luxury car supply decreased, which lifted retention

levels for all luxury cars in recent years, but luxury compact car retention may have

realized an even greater lift due to the rapid growth in demand that was identified by

the segment’s increase in new vehicle market share. Luxury compact cars have

historically been the most popular luxury car segment and NADA estimates that used

supply for the segment for vehicles up to five years in age was nearly 397,000 units in

2010, which was greater than luxury mid-size and luxury large cars combined at 338,000

units. However, because inventory declined by 21% in just three years to 314,000 units,

the relative shortage of vehicles pushed retention for luxury compact cars even higher

relative to other segments.

Segment 2009 2013Market Share

(+/-)

Lower Luxury Car 4.59% 4.96% 0.37%

Middle Luxury Car 1.71% 1.72% 0.01%

Upper Luxury Car 0.37% 0.45% 0.09%

Specialty Luxury Car 0.29% 0.30% 0.01%

Sport Luxury Car 0.41% 0.37% -0.04%

Total Car 7.37% 7.81% 0.43%

Source: WardsAuto

Segment 2009 2013Market Share

(+/-)

Small Luxury CUV 0.21% 0.38% 0.17%

Middle Luxury CUV 2.57% 3.04% 0.47%

Large Luxury CUV 0.62% 0.88% 0.26%

Middle Luxury SUV 0.46% 0.26% -0.20%

Large Luxury SUV 0.51% 0.40% -0.11%

Total Utility Vehicle 4.37% 4.97% 0.59%

Source: WardsAuto

Rank Luxury Segment Avg. Value Retention

1st Compact Car 48.8%

2nd Mid-Size Car 48.5%

3rd Large Car 44.6%

T-1st Compact Utility 59.6%

T-1st Large SUV 59.6%

3rd Mid-Size Utility 55.7%

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 5

© 2014 NADA Used Car Guide

Interestingly, used luxury compact utility supply

increased between 2010 and 2013 while inventory

has mostly fallen for luxury mid-size utilities and

luxury large SUVs. This was unlike the result found

with luxury compact cars versus luxury mid-size and

luxury large cars. Supply for luxury compact utilities

was only 7,101 units as recently as 2006, but grew to

nearly 70,000 by 2013 while inventory declined by

26% for all other luxury utilities combined between

2008 and 2012, as the trend in demand for luxury

CUVs has largely been opposite that of luxury SUVs

over the past several years. Inventory for used luxury

compact utilities up to five years in age grew in the

last few years just as demand increased in the new

retail market, captured by the segment’s expanded

market share. Thus, the value retention of three-year-

old luxury compact utilities may have been slightly

depressed compared to other luxury utilities.

Impact of Supply Growth on Used Prices

For many expensive products across various

industries, the growth in demand for new goods

inevitably leads to the existence of a used

marketplace (cellular phones, sporting equipment,

etc.). However, the demand in the used market generally does not lag much – if at all –

behind the new retail side, which means that even if new product sales climb, until

those items reach the used market, the shortage in used supply will inflate prices of

secondhand goods. The concept of supply and demand helps explain how retention

values have been affected thus far in the luxury segments, and by forecasting changes in

future used supply, we can anticipate shifts in prices and present our expectations going

forward.

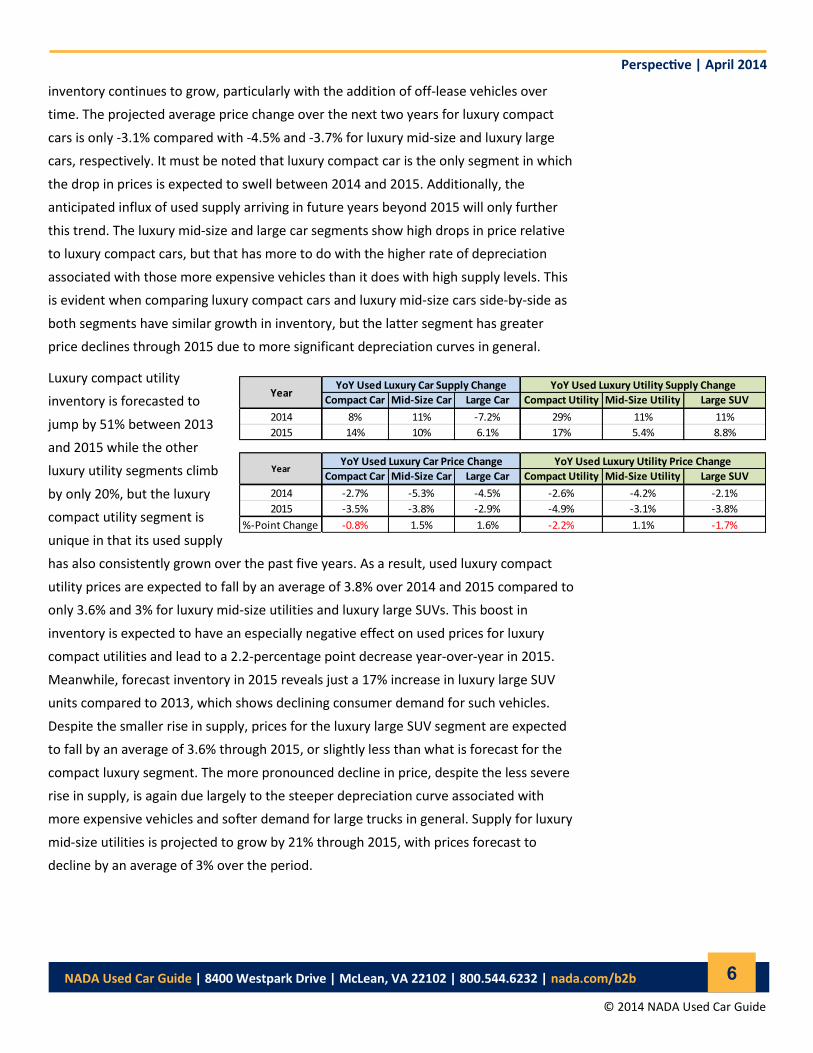

NADA’s used luxury car supply estimates for 2014 and 2015 show that much of the

growth is concentrated in two segments: compact and mid-size cars. Between 2013 and

2015, used inventory is expected to rise by 23% and 21% for luxury compact and luxury

mid-size cars, respectively, while falling by 2% for luxury large cars. This translates over

to the used market in that prices for units up to eight years in age are expected to drop

further for luxury compact cars compared to the other luxury car segments as used

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015

Use

d V

eh

icle

Su

pp

ly (T

ho

usa

nd

s)

Period

NADA Used Luxury Car Supply EstimatesUnits up to five years in age

Luxury Large Car Luxury Mid-Size Car Luxury Compact Car

Source: NADA Used Car Guide

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015

Use

d V

eh

icle

Su

pp

ly (T

ho

usa

nd

s)

Period

NADA Used Luxury Utility Vehicle Supply EstimatesUnits up to five years in age

Luxury Compact Utility Luxury Large SUV Luxury Mid-Size Utility

Source: NADA Used Car Guide

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 6

© 2014 NADA Used Car Guide

inventory continues to grow, particularly with the addition of off-lease vehicles over

time. The projected average price change over the next two years for luxury compact

cars is only -3.1% compared with -4.5% and -3.7% for luxury mid-size and luxury large

cars, respectively. It must be noted that luxury compact car is the only segment in which

the drop in prices is expected to swell between 2014 and 2015. Additionally, the

anticipated influx of used supply arriving in future years beyond 2015 will only further

this trend. The luxury mid-size and large car segments show high drops in price relative

to luxury compact cars, but that has more to do with the higher rate of depreciation

associated with those more expensive vehicles than it does with high supply levels. This

is evident when comparing luxury compact cars and luxury mid-size cars side-by-side as

both segments have similar growth in inventory, but the latter segment has greater

price declines through 2015 due to more significant depreciation curves in general.

Luxury compact utility

inventory is forecasted to

jump by 51% between 2013

and 2015 while the other

luxury utility segments climb

by only 20%, but the luxury

compact utility segment is

unique in that its used supply

has also consistently grown over the past five years. As a result, used luxury compact

utility prices are expected to fall by an average of 3.8% over 2014 and 2015 compared to

only 3.6% and 3% for luxury mid-size utilities and luxury large SUVs. This boost in

inventory is expected to have an especially negative effect on used prices for luxury

compact utilities and lead to a 2.2-percentage point decrease year-over-year in 2015.

Meanwhile, forecast inventory in 2015 reveals just a 17% increase in luxury large SUV

units compared to 2013, which shows declining consumer demand for such vehicles.

Despite the smaller rise in supply, prices for the luxury large SUV segment are expected

to fall by an average of 3.6% through 2015, or slightly less than what is forecast for the

compact luxury segment. The more pronounced decline in price, despite the less severe

rise in supply, is again due largely to the steeper depreciation curve associated with

more expensive vehicles and softer demand for large trucks in general. Supply for luxury

mid-size utilities is projected to grow by 21% through 2015, with prices forecast to

decline by an average of 3% over the period.

Compact Car Mid-Size Car Large Car Compact Utility Mid-Size Utility Large SUV

2014 8% 11% -7.2% 29% 11% 11%

2015 14% 10% 6.1% 17% 5.4% 8.8%

Compact Car Mid-Size Car Large Car Compact Utility Mid-Size Utility Large SUV

2014 -2.7% -5.3% -4.5% -2.6% -4.2% -2.1%

2015 -3.5% -3.8% -2.9% -4.9% -3.1% -3.8%

%-Point Change -0.8% 1.5% 1.6% -2.2% 1.1% -1.7%

YoY Used Luxury Car Price Change YoY Used Luxury Utility Price ChangeYear

YearYoY Used Luxury Car Supply Change YoY Used Luxury Utility Supply Change

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 7

© 2014 NADA Used Car Guide

Thoughts on the Future

Just as every action has an equal and opposite reaction, the shifting preferences of

luxury buyers toward more practical, value-oriented compact cars and utilities has

caused a boost in new vehicle sales that will inevitably result in rising used supply and

softer used prices. With the high volume of new sales units in these segments during

2012 and 2013 returning in 2015 and 2016 for three-year off-lease vehicles, it will not be

a surprise to see declining used prices continuing beyond 2015 for both luxury compact

cars and luxury compact utilities. Over the years, luxury compact cars and utilities have

progressively shown to be great values for the money, but with the rising popularity of

these products continuing into the future, the laws of supply and demand will

unavoidably impact value retention and used prices.

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 8

© 2014 NADA Used Car Guide

AT NADA USED CAR GUIDE

Financial Industry, Accounting, Legal, OEM Captive Steve Stafford 800.248.6232 x7275 [email protected]

Director, Sales and Customer Service Dan Ruddy 800.248.6232 x4707 [email protected]

Credit Unions, Fleet, Lease, Rental Industry, Government Doug Ott 800.248.6232 x4710 [email protected]

Automotive OEMs Stu Zalud 800.248.6232 x4636 [email protected]

Automotive Dealers, Auctions, Insurance Jim Dodd 800.248.6232 x7115 [email protected]

PR Manager Allyson Toolan 800.248.6232 x7165 [email protected]

Business Development Manager James Gibson 800.248.6232 x7136 [email protected]

What’s New

Available on iPhone, iPad and Android devices, the recently enhanced NADA MarketValues is

the fastest, easiest and most cost-efficient way to make smart vehicle decisions on the go. This

native app allows you to get your NADA values anywhere, anytime without an Internet

connection. Subscriptions start at $50 per month and when you download NADA

MarketValues from Google Play or the Apple Store for $1.99, you’ll receive a FREE 30-day trial!

On the Road

Jonathan Banks and Steve Stafford are attending the Auto Finance Risk Summit 2014 from May 5 – 6 in Newport Beach, California.

On Tuesday, May 6 at 11:15 a.m., Banks is participating on a panel titled “Collateral Values: How Much Will Valuations Drop?” The

panel will focus on the state of collateral values today, a possible timeline for a steeper decline and metrics for better portfolio

management.

Doug Ott is attending the Georgia Association of Tax Officials Conference on May 12—15 in Athens, Georgia. Stop by our booth to

see him. Larry Dixon is attending and speaking on a panel at the 18th Annual Non-Prime Auto Financing Conference on May 28—30

in Forth Worth Texas. Held by the National Automotive Finance Association, the event provides an excellent forum for education and

networking for those within the non-prime auto finance sector.

About NADA Used Car Guide

Since 1933, NADA Used Car Guide has earned its reputation as the leading provider of

vehicle valuation products, services and information to businesses throughout the United

States and worldwide. NADA’s editorial team collects and analyzes over one million

combined automotive and truck wholesale and retail transactions per month. Its

guidebooks, auction data, analysis and data solutions offer automotive/truck, finance,

insurance and government professionals the timely information and reliable solutions

they need to make better business decisions. Visit nada.com/b2b to learn more.

Perspective | April 2014

NADA Used Car Guide | 8400 Westpark Drive | McLean, VA 22102 | 800.544.6232 | nada.com/b2b 9

© 2014 NADA Used Car Guide

NADA CONSULTING SERVICES

NADA’s market intelligence team leverages a database of nearly 200 million automotive transactions and more than

100 economic and automotive market-related series to describe the factors driving current trends to help industry

stakeholders make more informed decisions. Analyzing data at both wholesale and retail levels, the team continuously

provides content that is both useful and usable to the automotive industry, financial institutions, businesses and

consumers.

Complemented by NADA’s analytics team, which maintains and advances NADA’s internal forecasting models and

develops customized forecasting solutions for automotive clients, the market intelligence team is responsible for

publishing white papers, special reports and the Used Car & Truck Blog. Throughout every piece of content, the team

strives to go beyond what is happening in the automotive industry to confidently answer why it is happening and how it

will impact the market in the future.

Senior Director, Vehicle Analysis & Analytics Jonathan Banks 800.248.6232 x4709 [email protected]

Senior Manager, Market Intelligence Larry Dixon 800.248.6232 x4713 [email protected]

Automotive Analyst David Paris 800.248.6232 x7044 [email protected]

Automotive Analyst Joseph Choi 800.248.6232 x4706 [email protected]

ADDITIONAL RESOURCES

Connect with NADA

White Papers NADA’s white papers and special reports aim to inform industry stakeholders on current and expected used vehicle price movement to better maximize today’s opportunities and manage tomorrow’s risk.

Used Car & Truck Blog Written and managed by the Market Intelligence team, the Used Car & Truck Blog analyzes market data, lends insight into industry trends and highlights relevant events.

NADA Perspective

Leveraging data from various industry

sources and NADA’s analysts, NADA

Perspective takes a deep dive into a

range of industry trends to determine

why they are happening and what to

expect in the future.

Guidelines Updated monthly with a robust data set from various industry sources and NADA’s own proprietary analytical tool, Guidelines provides the insight needed to make decisions in today’s market.

Read our Blog

nada.com/usedcar

Follow Us on Twitter

@NADAUsedCarGde

Find Us on Facebook

Facebook.com/NADAUsedCarGuide

Watch Us on YouTube

Youtube.com/NADAUsedCarGuide

Disclaimer: NADA Used Car Guide makes no representations about future performance or results based on the data and the contents available in this report (“Guidelines”). Guidelines is provided for informational purposes only and is provided AS IS without warranty or guarantee of any kind. By accessing Guidel ines via email or the NADA website, you agree not to reprint, reproduce, or distribute Guidelines without the express written permission of NADA Used Car Guide.