national academy of social insurance (nasi) - …...the national academy of social insurance (the...

TRANSCRIPT

Benefits, Costs, and Coverage

October 2018

Washington, DC

Workers’ Compensation:

The National Academy of Social Insurance (the Academy) is a non-profit, non-partisan organization made up of the nation’s leadingexperts on social insurance. Social insurance encompasses broad-basedsystems that help workers pool risks to avoid loss of income due toretirement, death, disability, or unemployment, and to ensure access tohealth care. The mission of the Academy is to advance solutions tochallenges facing the nation by increasing public understanding of howsocial insurance contributes to economic security. The Academy convenes steering committees and study panels that are charged withconducting research, issuing findings, and, in some cases, making recommendations based on their analyses. Members of these groups areselected for their recognized expertise in a particular area of social insurance, and with due consideration for the balance of disciplines andperspectives appropriate to the project.

This research report presents data on trends in workers’ compensationbenefits, costs, and coverage as of 2016. The report was prepared withthe guidance of the Study Panel on Workers’ Compensation Data and,in accordance with procedures of the Academy, has been reviewed forcompleteness, accuracy, clarity, and objectivity by a committee selectedby the Board of Directors. The purpose of the report is to present thedata and describe trends over time, but not to make policy recommendations.

The Social Security Administration provides partial funding to supportthe collection, processing, and validation of data for this report. Thedata are also used in tables for its Annual Statistical Supplement to theSocial Security Bulletin. The Centers for Medicare & Medicaid Servicesprovide funding to produce selected tables for this report that are alsoused in its own estimates. The project also receives financial supportfrom the Office of Workers’ Compensation Programs in the U.S.Department of Labor and in-kind support from the National Councilon Compensation Insurance and the National Association of InsuranceCommissioners.

© 2018 National Academy of Social InsuranceISBN: 1-884902-63-4

Board of Directors

William M. Rodgers III, Chair

Renée M. Landers, Vice Chair

Jason J. Fichtner, Treasurer

Martha E. Ford, Secretary

G. Lawrence Atkins

Robert A. Berenson

Ngina S. Chiteji

Harry J. Conaway

Cecilia A. Conrad

Indivar Dutta-Gupta

Howard Fluhr

Alexander W. Hertel-Fernandez

Douglas J. Holtz-Eakin

Kilolo Kijakazi

Shaun C. O’Brien

Earl R. Pomeroy

Maya D. Rockeymoore

Rebecca M. Vallas

Founding Chair

Robert M. Ball

Chief Executive Officer

William J. Arnone

1200 New Hampshire Ave., NW

Suite 830

Washington, DC 20036

Telephone (202) 452-8097

Facsimile (202) 452-8111

Web: www.nasi.org Twitter: @socialinsurance

Workers’ Compensation:

Benefits, Costs, and Coverage(2016 data)

by

Christopher F. McLaren, Marjorie L. Baldwin, and Leslie I. Boden

with advice from the

Study Panel on Workers’ Compensation Data

Washington, DC

October 2018

Workers’ Compensation: Benefits, Costs, and Coverage • i

Workers’ compensation provides funding for medicalcare, rehabilitation, and cash benefits for workerswho are injured on the job or who contract work-related illnesses. The program also pays benefits tofamilies of workers who die of work-related injuriesor illnesses. Unlike most other U.S. social insuranceprograms, workers’ compensation programs are regulated by the states, with no federal financing.The programs were established by state statute orwithin state constitutions beginning in 1911, beforemost federal social insurance programs were enacted.The federal government provides workers’ compen-sation insurance for federal employees and forworkers in some high-risk industries, but no federallaws set standards for workers’ compensation programs or require comprehensive reporting ofworkers’ compensation data.

The lack of federal standards or reporting require-ments for state workers’ compensation programsmakes it difficult to provide national estimates basedon uniform definitions of amounts of benefits paid,costs to employers, and numbers of workers covered.In order to produce national summary statistics onthe program, it is necessary to compile data fromvarious sources.

Until 1995, the U.S. Social Security Administration(SSA) produced the only comprehensive nationaldata on workers’ compensation benefits, costs, andcoverage, with annual estimates dating back to 1946.SSA discontinued the series in 1995 and theNational Academy of Social Insurance (theAcademy) assumed the task of reporting nationaldata on workers’ compensation in 1997. TheAcademy published its first report that year and hasproduced the report annually ever since.

This is the Academy’s 21st annual report on workers’compensation benefits, costs, and coverage. Thisreport presents new data on state and federal work-ers’ compensation programs for 2016 and updatedestimates for 2012-2015. The revised estimates inthis report replace estimates in the Academy’s priorreports.

The Academy and its expert advisors are continuallyseeking ways to improve the report and to adapt estimation methods to track new developments inworkers’ compensation programs. Detailed

descriptions of the methods used to produce the estimates in this report are available online atwww.nasi.org/research/workers-compensation.

Despite the Academy’s continued efforts to improvethe quality of its estimates, there are limitations tothe data which we acknowledge in the report. It isimportant to note, for example, that our estimates ofworkers’ compensation costs borne by employersmay not capture the full economic and human costsof work-related injuries, illnesses, and fatalities.These costs – borne by workers, families, and communities – are significant but are beyond thescope of this report. Additionally, the report does notevaluate whether workers’ compensation programsare meeting key objectives, such as: preventing work-related injuries and illnesses; compensating injuredworkers adequately and equitably; rehabilitatinginjured workers and returning them to work at anaffordable cost.

The audience for the Academy’s annual report onworkers’ compensation includes actuaries, insurers,journalists, business and labor leaders, employee ben-efit specialists, federal and state policymakers, andresearchers working in universities, government, andprivate consulting firms. The data from some tablesare published by the National Safety Council (NSC)(in Injury Facts), by the Employee Benefit ResearchInstitute (in Employee Benefit News, Fundamentals ofEmployee Benefit Programs) and by the SSA (in theAnnual Statistical Supplement to the Social SecurityBulletin).

The Academy’s estimates inform state and federalpolicymakers in numerous ways. The federal Centersfor Medicare & Medicaid Services (CMS), for exam-ple, uses the data in estimates and projections ofhealth care spending in the United States. TheNational Institute for Occupational Safety andHealth (NIOSH) uses the data to track the costs ofworkplace injuries in the United States. TheInternational Association of Industrial AccidentBoards and Commissions (IAIABC), the organiza-tion of state and provincial agencies that administerworkers’ compensation in the United States andCanada, uses the information to track and comparethe performance of workers’ compensation programsin the United States with similar systems in Canada.

Preface

AcknowledgementsThe Academy expresses its deep appreciation to staffmembers in the 50 states and District of Columbiaworkers’ compensation offices who provide data ontheir jurisdictions each year. While there are toomany individuals to name here, we are grateful forthe time they spend responding to our survey andanswering clarification questions as needed. Withoutsupport from these individuals, constructing thisannual data series would be impossible. TheAcademy also acknowledges support from the U.S.Social Security Administration (SSA), Centers forMedicare & Medicaid Services (CMS), and theOffice of Workers’ Compensation Programs of theU.S. Department of Labor (DOL).

The authors gratefully acknowledge the time andexpertise contributed by members of the Academy’sStudy Panel on Workers’ Compensation Data. All

members of the Panel are listed on page iii, but weespecially acknowledge the contributions of: TerryBogyo, John F. Burton Jr., Jeff Eddinger, DougHolmes, Mike Manley, Nicole Nestoriak, and FrankNeuhauser. We also thank Elliot Schreur (Academy),Griffin Murphy, the Academy’s workers’ compensa-tion summer intern, and Amy Zhou, for theirresearch assistance. Finally, we appreciate commentsfrom Michael Duff (University of Wyoming),Michael Dworsky (RAND Corporation), and ScottSyzmendera who reviewed a final draft for theBoard.

Marjorie Baldwin Chair, Study Panel on Workers’ Compensation Data

ii NATIONAL ACADEMY OF SOCIAL INSURANCE

Workers’ Compensation: Benefits, Costs, and Coverage • iii

Marjorie Baldwin, ChairProfessor, W. P. Carey School of Business, Department of Economics,Arizona State University

Christine BakerPrincipal and Consultant,Strategic Access Partners

Leslie BodenProfessor, School of PublicHealth, Boston University

Terry BogyoIndependent Workers’Compensation Researcher,Canada

Aaron BrandenburgAssistant Director, DataCoordination and StatisticalAnalysis, National Association ofInsurance Commissioners

John F. Burton, Jr.Professor Emeritus, School ofManagement & Labor Relations,Rutgers University, and School ofIndustrial and Labor Relations,Cornell University

Aaron CatlinDeputy Director, NationalHealth Statistics Group, Officeof the Actuary, Centers forMedicare & Medicaid Services

Charles DavoliLouisiana Workers’ AdvocateLabor Representative of theGovernor’s Workers’Compensation Advisory Council

Jeff EddingerSenior Divisional ExecutiveRegulatory Services, NationalCouncil on CompensationInsurance

Douglas J. HolmesPresident, UWC StrategicServices on Unemploymentand Workers’ Compensation

Jennifer Wolf HorejshExecutive Director, InternationalAssociation of IndustrialAccident Boards andCommissions

Kate KimpanVice President, Workers’Compensation Programs, Dade Moeller & Associates

Mike ManleyIndependent Workers’Compensation Researcher,Panama

Nicole NestoriakResearch Economist, Bureau of Labor Statistics, U.S.Department of Labor

Frank NeuhauserExecutive Director, Center forthe Study of Social Insurance,University of California, Berkeley

Seth A. SeaburyAssociate Professor ofOphthalmology; Director, Keck-SchaefferInitiative for Population Health,University of Southern California

Hilery SimpsonAssistant Commissioner, Office of Safety, Health, andWorking Conditions, U.S. Bureau of Labor Statistics

Emily A. SpielerProfessor of Law, NortheasternUniversity School of Law

Robert Steggert Retired, Marriott International, Inc.

Gary SteinbergRetired, Deputy Director, Officeof Workers’ CompensationPrograms, U.S. Department ofLabor

Alex SwedlowPresident, California Workers’Compensation Institute

Ramona TanabeExecutive Vice President,Workers Compensation Research Institute

Benjamin WashingtonEconomist, National HealthStatistics Group, Office of theActuary, Centers for Medicare& Medicaid Services

Study Panel on Workers’ Compensation Data

iv NATIONAL ACADEMY OF SOCIAL INSURANCE

Workers’ Compensation: Benefits, Costs, and Coverage • v

Table of ContentsPreface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Study Panel on Workers’ Compensation Data. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

National Trends (Table 1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

State Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Background on Workers’ Compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

History of Workers’ Compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Workers’ Compensation Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Sources of Workers’ Compensation Insurance. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Estimates for 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Covered Employment and Wages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Methods for Estimating Covered Employment and Wages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

National Estimates of Covered Employment and Wages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

State Estimates of Covered Employment and Wages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Workers’ Compensation Benefits Paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Data Sources and Methods for Estimating Benefits Paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

National Estimates of Benefits Paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

State Estimates of Benefits Paid in 2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

State Trends in Benefits Paid. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Benefits Per $100 of Covered Payroll . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Cash Benefits by Type of Claim . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Employer Costs for Workers’ Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Data Sources for Estimating Employer Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

National Estimates of Employer Costs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

State Estimates of Employer Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Benefits Paid Relative to Employer Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Estimates of Employer Costs from Other Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Direct and Indirect Costs to Workers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Incidence of Workplace Injuries and Workers’ Compensation Claims. . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Incidence of Work-Related Injuries. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Incidence of Workers’ Compensation Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Addendum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Other Disability Benefit Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Benefits Incurred vs. Benefits Paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Appendix A: Coverage Estimates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Appendix B: Federal Programs. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Federal Programs Included in the Academy’s Estimates. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Federal Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Longshore and Harbor Workers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Coal Miners with Black Lung Disease. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

Federal Programs Not Included in the Academy’s Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Energy Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Workers Exposed to Radiation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

Veterans of Military Service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

Railroad Employees and Merchant Mariners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Appendix C: Workers’ Compensation under State Laws. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

References. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

TablesTable 1: Overview of Workers’ Compensation Benefits, Costs, and Coverage, 2012-2016 . . . . . . . .2

Table 2: Workers’ Compensation Covered Jobs and Covered Payroll, 1996-2016 . . . . . . . . . . . . . .11

Table 3: Workers’ Compensation Covered Jobs by State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . .12

Table 4: Workers’ Compensation Covered Payroll by State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . .14

Table 5 Workers’ Compensation Benefits Paid by Type of Insurer, 1996-2016 . . . . . . . . . . . . . . . . .18

Table 6: Workers’ Compensation Employer-Paid Benefits UnderDeductible Provisions, 1996-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Table 7: Percentage Distribution of Workers’ Compensation Benefit Payments by Type of Coverage: With and Without Deductibles, 1996-2016 . . . . . . . . . . . . . . . . . . . . .21

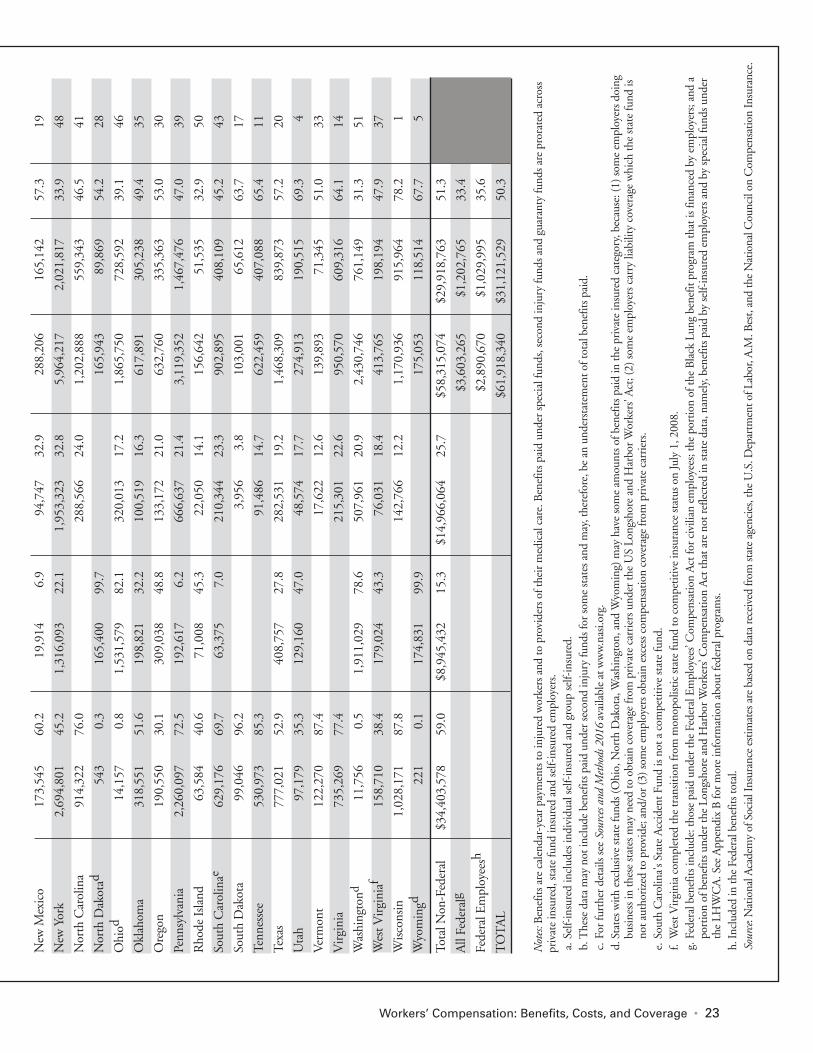

Table 8: Workers’ Compensation Benefits Paid by Type of Insurer and State, 2016 . . . . . . . . . . . . .22

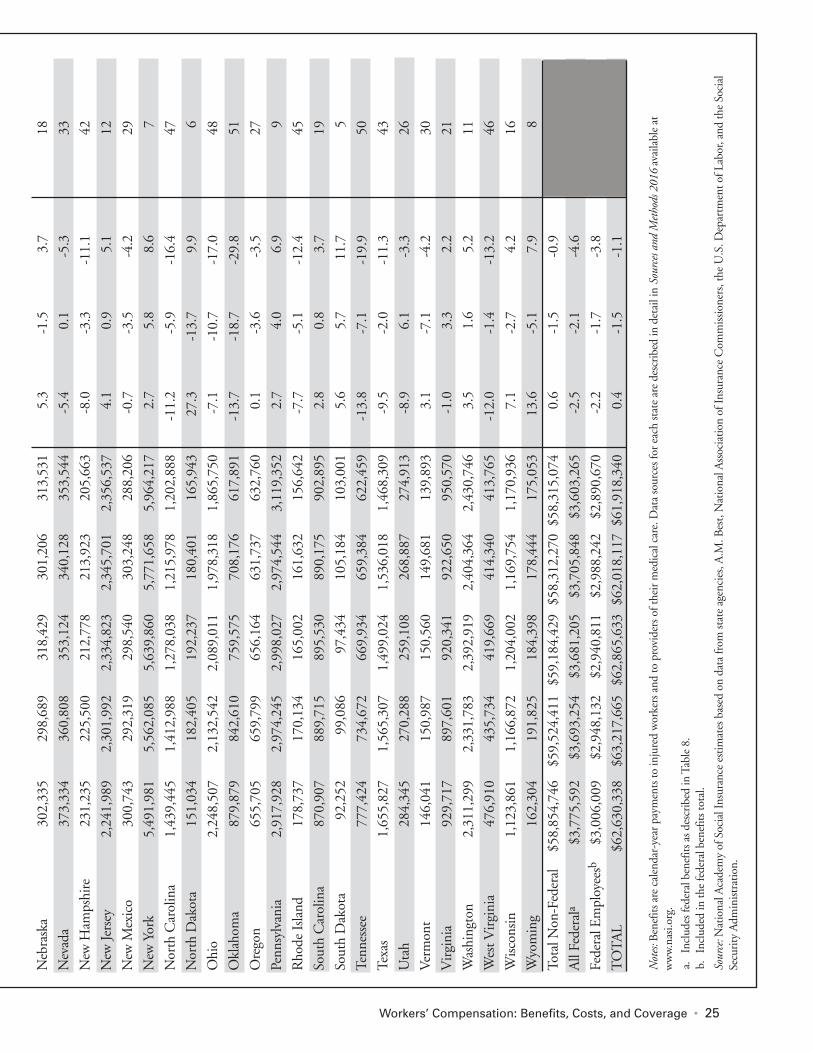

Table 9: Workers’ Compensation Total Benefits Paid and Five-Year Percent Change by State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24

Table 10: Workers’ Compensation Medical Benefits Paid and Five-Year Percent Change by State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28

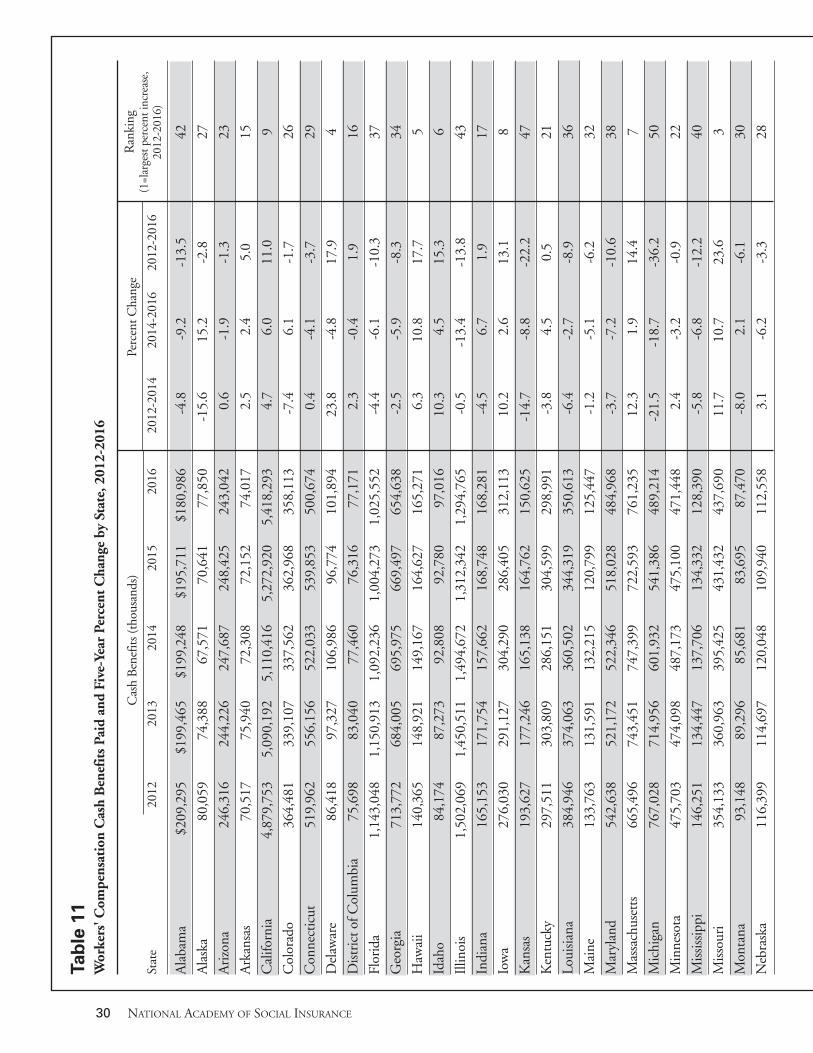

Table 11: Workers’ Compensation Cash Benefits Paid and Five-Year Percent Changeby State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30

Table 12: Workers’ Compensation Total Benefits Paid Per $100 of Covered Payrollby State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .32

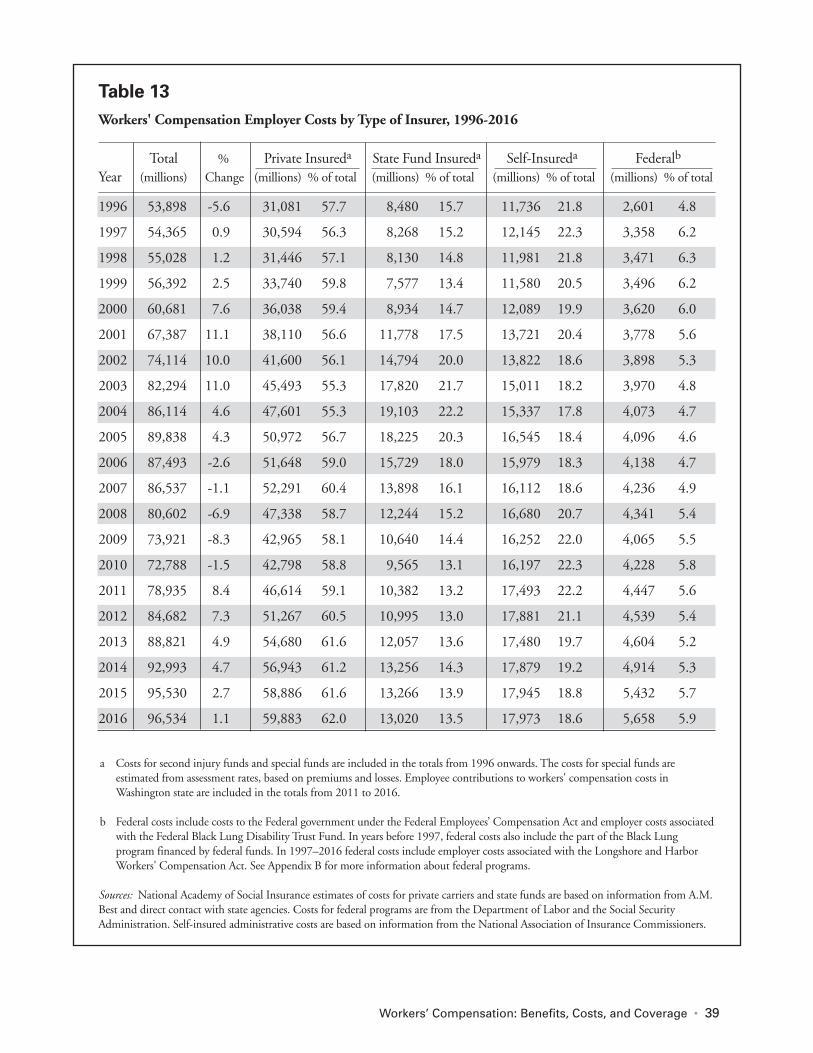

Table 13: Workers’ Compensation Employer Costs by Type of Insurer, 1996-2016 . . . . . . . . . . . . . . .39

Table 14: Employer Costs for Workers’ Compensation Per $100 of Covered Payroll by State, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .42

Table 15: Workers’ Compensation Benefit/Cost Ratios, 1996-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . .44

Table 16: Fatal Occupational Injuries and Fatal Injury Rates: All and Wage & Salary Workers, 1996-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .47

Table 17: Non-Fatal Occupational Injuries and Illnesses Among Private Industry Employers, 1996-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .49

Table 18: Number of Workers’ Compensation Claims Per 100,000 Insured Workers: Private Carriers in 38 Jurisdictions, 1996-2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .51

Table 19: Dual Eligible Individuals: Social Security Disability Insurance (SSDI) Beneficiaries with Workers’ Compensation (WC) or Public Disability Benefits (PDB), 2016 . . . . . . . . . . .55

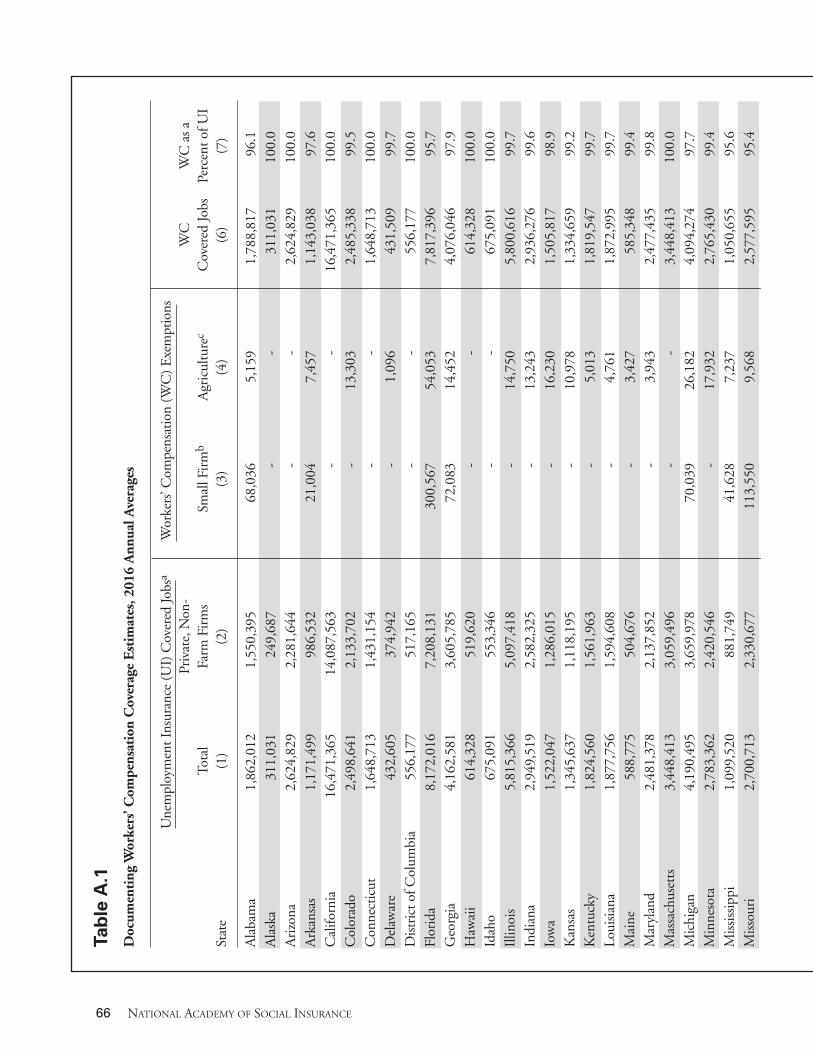

Table A.1: Documenting Workers’ Compensation Coverage Estimates, 2016 Annual Averages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .66

Table A.2: Workers’ Compensation Coverage as a Percent of the Employed Workforce, 2006-2016 National Averages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .68

vi NATIONAL ACADEMY OF SOCIAL INSURANCE

Workers’ Compensation: Benefits, Costs, and Coverage • vii

Table B.1: Federal Employees’ Compensation Act, Benefits and Costs, 2012-2016 . . . . . . . . . . . . . . .69

Table B.2: Longshore and Harbor Workers’ Compensation Act (LHWCA), Benefits, Costs, and Death Claims, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .71

Table B.3: Black Lung Benefits Act, Benefits and Costs, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . .72

Table B.4: Benefits and Costs of the Energy Employees Occupational Illness Compensation Program Act: Parts B and E, 2012-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .73

Table B.5: Radiation Exposure Compensation Act, Benefits Paid as of June, 2018 . . . . . . . . . . . . . . .74

Table B.6: Federal Veterans’ Compensation Program: Fiscal Year 2016 . . . . . . . . . . . . . . . . . . . . . . . .74

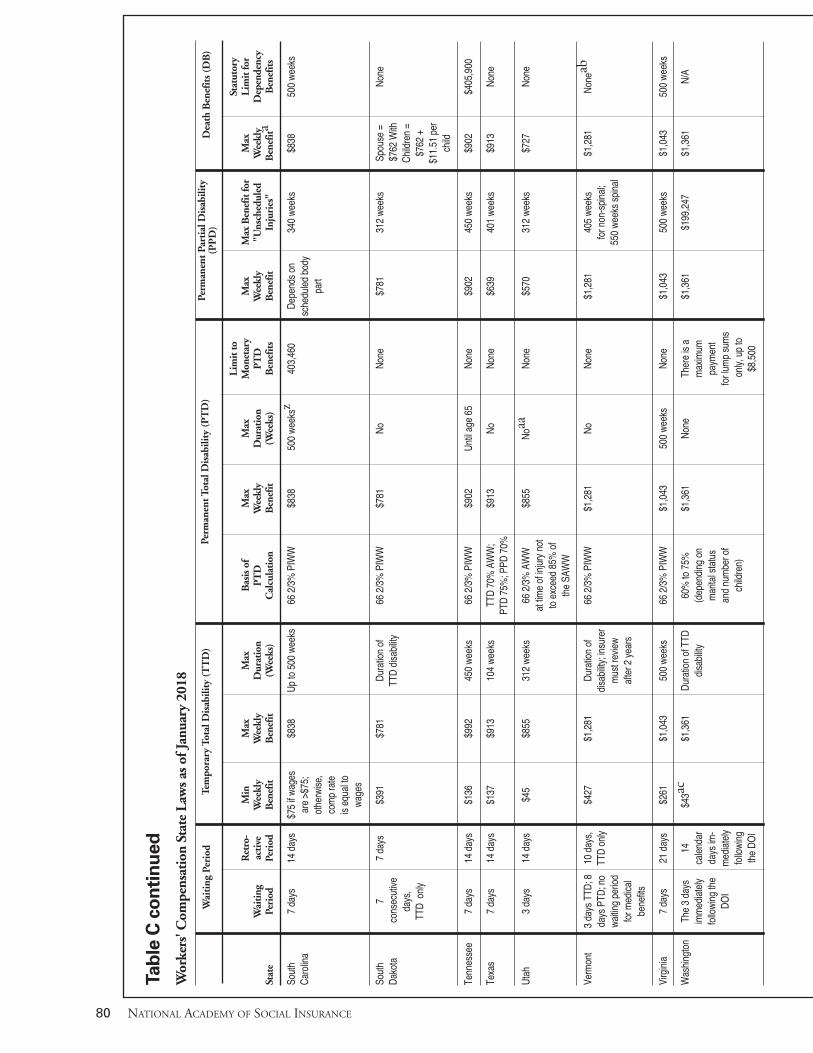

Table C: Workers’ Compensation State Laws as of January 2018 . . . . . . . . . . . . . . . . . . . . . . . . . . . .76

FiguresFigure 1: Workers’ Compensation Benefits and Costs Per $100 of Covered Payroll, 1980–2016 . . . . .3

Figure 2: Workers’ Compensation Medical and Cash Benefits Per $100 of Covered Payroll, 1980–2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Figure 3: Percentage Share of Medical and Cash Benefits, 1980–2016 . . . . . . . . . . . . . . . . . . . . . . . .35

Figure 4a: Types of Disabilities in Workers’ Compensation Cases with Cash Benefits, 1996-2014, Percentage of Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37

Figure 4b: Types of Disabilities in Workers’ Compensation Cases with Cash Benefits, 1996-2014, Percentage of Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .37

Figure 5: Private Industry Occupational Injuries and Illnesses: Incidence Rates, 1980-2016 . . . . . . .50

Figure 6: Proportion of Worker SSDI Beneficiaries with Connection to Workers’ Compensation or Public Disability Benefits, 2006-2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .56

Additional Appendices On-lineAdditional appendices are published in Sources, Methods, and State Summaries: A Companion toWorkers’ Compensation: Benefits, Costs, and Coverage available on the Academy’s website atwww.nasi.org. These appendices provide more information on:

� Data sources for each state

� Methods used to estimate workers’ compensation benefits and costs by type of coverage,

including:

• Deductibles

• Self-insured benefit payments and administrative costs

• Medical benefits

� Updated version of Table 9.B1 of the Annual Statistical Supplement to the Social

Security Bulletin

� 2012 to 2016 trends in benefits paid by second injury funds, special funds, and guaranty funds

� State summary tables that report key metrics from 2012 to 2016

viii NATIONAL ACADEMY OF SOCIAL INSURANCE

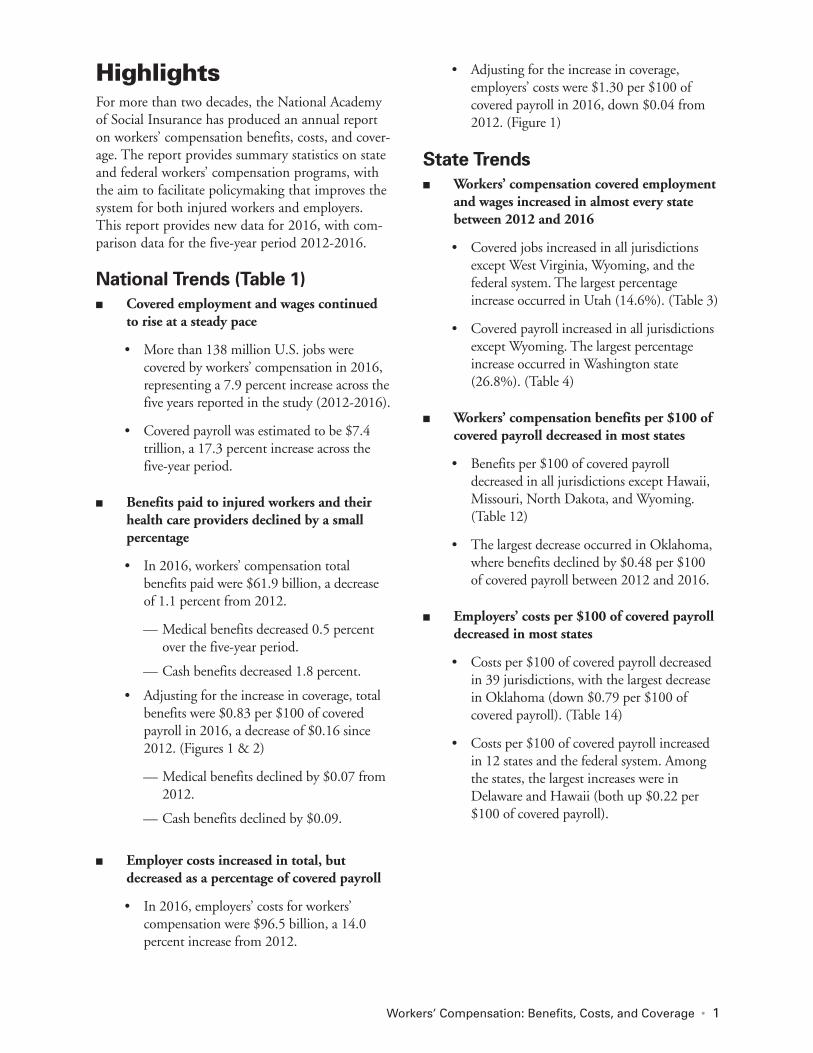

Highlights For more than two decades, the National Academyof Social Insurance has produced an annual reporton workers’ compensation benefits, costs, and cover-age. The report provides summary statistics on stateand federal workers’ compensation programs, withthe aim to facilitate policymaking that improves thesystem for both injured workers and employers.This report provides new data for 2016, with com-parison data for the five-year period 2012-2016.

National Trends (Table 1)� Covered employment and wages continued

to rise at a steady pace

• More than 138 million U.S. jobs were covered by workers’ compensation in 2016,representing a 7.9 percent increase across thefive years reported in the study (2012-2016).

• Covered payroll was estimated to be $7.4trillion, a 17.3 percent increase across thefive-year period.

� Benefits paid to injured workers and theirhealth care providers declined by a small percentage

• In 2016, workers’ compensation total benefits paid were $61.9 billion, a decreaseof 1.1 percent from 2012.

— Medical benefits decreased 0.5 percentover the five-year period.

— Cash benefits decreased 1.8 percent.

• Adjusting for the increase in coverage, totalbenefits were $0.83 per $100 of coveredpayroll in 2016, a decrease of $0.16 since2012. (Figures 1 & 2)

— Medical benefits declined by $0.07 from2012.

— Cash benefits declined by $0.09.

� Employer costs increased in total, butdecreased as a percentage of covered payroll

• In 2016, employers’ costs for workers’ compensation were $96.5 billion, a 14.0percent increase from 2012.

• Adjusting for the increase in coverage,employers’ costs were $1.30 per $100 of covered payroll in 2016, down $0.04 from2012. (Figure 1)

State Trends � Workers’ compensation covered employment

and wages increased in almost every statebetween 2012 and 2016

• Covered jobs increased in all jurisdictionsexcept West Virginia, Wyoming, and thefederal system. The largest percentageincrease occurred in Utah (14.6%). (Table 3)

• Covered payroll increased in all jurisdictionsexcept Wyoming. The largest percentageincrease occurred in Washington state(26.8%). (Table 4)

� Workers’ compensation benefits per $100 ofcovered payroll decreased in most states

• Benefits per $100 of covered payrolldecreased in all jurisdictions except Hawaii,Missouri, North Dakota, and Wyoming.(Table 12)

• The largest decrease occurred in Oklahoma,where benefits declined by $0.48 per $100of covered payroll between 2012 and 2016.

� Employers’ costs per $100 of covered payrolldecreased in most states

• Costs per $100 of covered payroll decreasedin 39 jurisdictions, with the largest decreasein Oklahoma (down $0.79 per $100 of covered payroll). (Table 14)

• Costs per $100 of covered payroll increasedin 12 states and the federal system. Amongthe states, the largest increases were inDelaware and Hawaii (both up $0.22 per$100 of covered payroll).

Workers’ Compensation: Benefits, Costs, and Coverage • 1

Background on Workers’ Compensation This section of the report, covering backgroundmaterial that is repeated annually, describes the his-tory of workers’ compensation insurance in theUnited States; the current structure of state workers’compensation programs; types of benefits paid; andhow workers’ compensation is financed. Reportingof detailed program data for 2016 begins on page 16and a glossary of terms used in this report is foundon page 57.1

History of Workers’ CompensationWorkers’ compensation was the first social insuranceprogram adopted in most developed countries. Thefirst modern workers’ compensation laws, based onthe principle of employer liability for workplaceinjuries, were adopted in Germany in 1884 underChancellor Otto von Bismarck (Clayton, 2004). In1897, England passed a similar law, holding employ-ers liable so long as the worker could prove that theyhad been injured on the job.

The first workers’ compensation law in the UnitedStates was enacted in 1908 to cover certain federal

2 NATIONAL ACADEMY OF SOCIAL INSURANCE

Table 1Overview of Workers' Compensation Benefits, Costs, and Coverage, 2012-2016

Percent Change

Aggregate Benefits, Coverage, and Costs 2016 2012-2014 2014-2016 2012-2016

Covered Jobs (in thousands) 138,251 3.7 4.0 7.9

Covered Payroll (in billions) $7,422 8.0 8.7 17.3

Workers' Compensation Benefits Paid (in billions) 61.9 0.4 -1.5 -1.1

Medical Benefits 31.1 2.2 -2.6 -0.5

Cash Benefits 30.8 -1.5 -0.3 -1.8

Employer Costs for Workers' Compensation (in billions) 96.5 9.8 3.8 14.0

Benefits and Costs per $100 of Dollar Change

Covered Payroll 2016 2012-2014 2014-2016 2012-2016

Workers' Compensation Benefits Paid $0.83 -$0.07 -$0.09 -$0.16

Medical Benefits 0.42 -0.02 -0.05 -0.07

Cash Benefits 0.41 -0.05 -0.04 -0.09

Employer Costs for Workers' Compensation 1.30 0.02 -0.06 -0.04

Notes: Benefits are calendar-year payments to injured workers (cash benefits) and to providers of their medical care (medicalbenefits). Costs for employers who purchase workers' compensation insurance include calendar-year insurance premiums paidplus benefits paid by the employer to meet the annual deductible, if any. Costs for self-insuring employers are calendar-yearbenefits paid plus the administrative costs associated with providing those benefits.

Source: National Academy of Social Insurance estimates.

1 This report tracks benefits, costs, and coverage in the 50 states plus the District of Columbia. For brevity, we refer to the District ofColumbia as a state.

civilian workers. The first state laws that survivedconstitutional challenges were enacted in 1911.2

Most states adopted workers’ compensation laws in arelatively short period between 1910 and 1920. Ofthe contiguous 48 states, the last to pass a workers’compensation law was Mississippi in 1948.

Before workers’ compensation laws were enacted,injured workers’ primary legal remedy for a work-related injury was to file a tort suit claimingnegligence on the part of their employer.3 Employerscould use three common law defenses to avoid liability: assumption of risk (showing the injuryresulted from the risks of employment of which the

Figure 1Workers’ Compensation Benefits and Costs Per $100 of Covered Payroll, 1980-2016

Notes: Benefits are calendar-year payments to injured workers and to providers of their medical care. Costs for employers who purchase workers' compensation insurance include calendar-year insurance premiums paid plus benefits paid by the employer to meet the annual deductible, if any. Costs forself-insuring employers are calendar-year benefits paid plus the administrative costs associated with providing those benefits.

Source: National Academy of Social Insurance estimates.

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

1.861.76

1.671.58

1.94

1.50

1.64

1.49

1.79

2.04

2.18 2.16 2.172.132.05

1.83

1.621.51

1.421.36 1.35

1.46

1.61

1.74 1.74 1.72

1.581.48

1.351.30

1.251.30 1.34 1.37 1.36

0.96 0.971.04 1.05 1.09

1.171.23

1.291.34

1.461.57

1.65 1.65

1.531.47

1.351.26

1.17 1.13 1.121.06 1.10 1.13 1.16 1.13 1.09

0.99 0.96 0.991.03 1.00 1.01 0.99 0.97

0.92

1.33

0.86

1.30

0.83

Workers’ Compensation: Benefits, Costs, and Coverage • 3

Employer Costs

Benefits

2 In 1910 New York became the first state to adopt a workmen’s compensation [as the program was then known] statute of general ap-plication, which was compulsory for certain especially hazardous jobs and optional for others…“[I]n 1911, in Ives v. South BuffaloRailway Co…the Court of Appeals of New York held the New York act unconstitutional on the grounds of deprivation of propertywithout due process of law,” (Wilborn et al., 2017). In 1911, nine states, including Kansas, New Jersey and Wisconsin, enacted elective laws in order to avoid the Ives type of decision, and Washington adopted a compulsory statute, which was upheld by theWashington Supreme Court (Somers and Somers, 1954). Kansas and Washington had the first enactment date (March 14, 1911),but those laws were not effective until after May 3, 1911, the same date when the Wisconsin law was enacted and took effect(Krohm, 2011).

3 Some injured workers received voluntary compensation from their employers or medical benefits paid through personal accident insurance, but many workers received no compensation at all (Fishback and Kantor, 1996).

worker should have been aware);4 the fellow servantrule (showing the injury was caused by a fellowworker’s negligence); or contributory negligence(showing the worker’s own negligence contributed tothe injury, regardless of any fault of the employer).Given the available defenses, it was not surprisingthat employers often prevailed in court. Employerswere, however, at risk for substantial and unpredictable losses if a worker’s lawsuit was successful. Litigation also created friction betweenemployers and workers so that both sides becameincreasingly dissatisfied with the status quo, settingthe stage for reform.

Initial reforms came in the form of employer liabilityacts, which eliminated some of the employer’s common law defenses. Nonetheless, employees stillhad the burden of proving negligence on the part ofthe employer, which remained a significant obstacleto recovery of damages (Burton and Mitchell,2003).5 Ultimately, both employers and employeesfavored workers’ compensation legislation to ensurethat workers who sustained occupational injuries or contracted occupational diseases received predictableand timely compensation. As a quid pro quo, workers’ compensation became the “exclusive remedy” for occupational injuries and diseases, andan employer’s liability was limited to the statutory

4 NATIONAL ACADEMY OF SOCIAL INSURANCE

4 A more complete definition is provided by Willborn, et al. (2017): “The assumption of risk doctrine…barred recovery for the ordi-nary risks of employment; as well as the extraordinary risks of employment, if the worker knew of them or might reasonably havebeen expected to know of them.”

5 As a result, the employers’ liability approach was abandoned in all jurisdictions and industries except the railroads, where it still exists.

Figure 2Workers’ Compensation Medical and Cash Benefits Per $100 of Covered Payroll, 1980-2016

Source: National Academy of Social Insurance estimates.

0.68 0.680.70 0.71

0.73

0.780.80

0.820.84

0.89

0.94

0.990.96

0.87 0.89

0.81

0.76

0.69

0.650.64

0.59 0.60 0.61 0.61 0.60

0.28 0.29

0.340.36

0.39

0.43

0.470.50

0.57

0.62

0.660.69

0.58

0.54

0.500.48 0.48 0.48 0.47

0.500.52

0.550.53

0.51

0.58

0.520.50 0.50

0.530.51 0.50 0.50 0.48

0.45

0.34

0.66

0.47 0.460.49 0.50 0.49

0.51 0.49 0.49

0.47

0.43

0.43

0.41

0.42

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

Cash Benefits

Medical Benefits

benefits specified in a state workers’ compensationact.6

The adoption of state workers’ compensation programs has been called a significant event in thenation’s economic, legal, and political history.Passage of the laws required prodigious efforts on thepart of business and labor leaders in each state toreach agreements on the specifics of the laws.Essentially, business and labor reached a grand compromise: Injured workers gave up the right tosue their employers in return for guaranteed benefits.Employers agreed to pay compensation for coveredinjuries on a no-fault basis in return for statutorylimits on coverage.

Today, each of the 50 states, the District ofColumbia, and the U.S. territories has its own workers’ compensation program. Separate U.S. government programs cover federal civilian employ-ees, long shore and harbor workers, and specifichigh-risk workers (e.g., coal miners with black lungdisease, energy employees exposed to certain materi-

als such as beryllium, workers exposed to radiation,and veterans of military service). State workers’ com-pensation programs vary in terms of who is allowedto provide insurance, which injuries or illnesses arecompensable, and the level of benefits provided.However, there is consistency across states in centralfeatures of the programs:

n With the exception of Texas, workers’ compen-sation insurance coverage is mandatory for pri-vate-sector employers in all states, with limitedexemptions for small employers and for workersin specific classifications, such as agricultural ordomestic employees.7 Oklahoma implementeda law in 2014 that allowed employers to opt-out of a traditional workers’ compensation planby adopting an alternative benefit plan. ThisOpt-Out Act was in place in 2015, but theSupreme Court of the State of Oklahoma ruledthat it was unconstitutional in September2016.8

n Workers’ compensation pays 100 percent ofinjury-related medical costs for injured workersand cash benefits for lost work time. Lost-timecompensation may be subject to a waitingperiod (typically three to seven days) that maybe paid retroactively if the disability involveshospitalization or a lengthy duration of workabsence. Wage-replacement rates vary by statebut, on average, replace about two-thirds of aworker’s pre-injury gross wage up to state-specified limits. Lost-time compensation is tax-exempt and typically restricted by minimumsand maximums established by state law.

Workers’ Compensation: Benefits, Costs, and Coverage • 5

Workers’ compensation is the “exclusive remedy” for occupationalinjuries and diseases. An employer’sliability is limited to the statutory benefits specified by the workers’

compensation act in their jurisdiction.

6 Under the exclusive remedy concept, the worker accepts workers’ compensation as payment in full and gives up the right to sue.There are limited exceptions to the exclusive remedy concept in some states, such as when there is an intentional injury of the em-ployee or when an employer violates a safety regulation. A suit is also possible if the employer is uninsured.

7 In addition, many states allow specific classes of employers to voluntarily purchase workers’ compensation coverage or to opt-out ofstatutory coverage, e.g., independent contractors, corporate officers, and local governments. Wyoming statute §27-14-108 exemptsemployers from purchasing workers’ compensation insurance if their employees are not engaged in extra-hazardous employment.However, the Statute’s classification of extra-hazardous employment is so extensive that almost every occupation is covered.

8 Oklahoma passed sweeping workers’ compensation statutory amendments in 2013 when Senate Bill 1062 was signed into law. Thebill, which became effective January 1, 2014, allowed employers to provide insurance for injured workers under alternative benefitsystems while maintaining their immunity from tort litigation by injured employees. Under the Oklahoma Employee Injury BenefitAct (OEIBA also known as the “Opt-Out Act”) a “qualified employer” could opt-out of the state workers’ compensation system if itprovided the State Insurance Commissioner with a written private benefit plan that offered comparable coverage consistent with thestate constitution and showed proof that the employer was financially capable of paying the required compensation.

The Opt-Out Act was reviewed in Vasquez v. Dillard’s by the Oklahoma Workers’ Compensation Commission (OK WCC), whichfound that the Act was unconstitutional. The ruling was appealed to the Oklahoma State Supreme Court, which confirmed theCommission’s finding that the Opt-Out Act was unconstitutional (Vasquez v. Dillard's, Inc. 381 P. 3d 768, 2016). The StateSupreme Court, in its decision, wrote: “The core provision of the Opt Out Act, 85A O.S. Supp.2015 203, creates impermissible,unequal, disparate treatment of a select group of injured workers. Therefore, we hold that the Oklahoma Employee Benefit InjuryAct, 85A O.S. 2014 201-213, is an unconstitutional special law under the Oklahoma Constitution.”

n Workers’ compensation is financed exclusivelyby employers except in three states where work-ers pay part of the cost of workers’ compensa-tion benefits and services through direct payrolldeductions or charges.9 Employers purchaseworkers’ compensation insurance from privateinsurers or from a state workers’ compensationinsurance fund, and many large employers self-insure.10

Workers’ Compensation Benefits There are three basic types of workers’ compensationclaims through which injured workers or their med-ical providers may collect benefits: (1) medical-only;(2) temporary disability; and (3) permanent disabili-ty. The type of claim is determined by the severity ofinjury and whether or not the claim involves aninjury-related work absence.

Medical-only claims. Most workers’ compensationclaims do not involve lost work time in excess of thewaiting period for cash benefits, so only medicalbenefits (and not cash benefits) are paid for theseclaims. “Medical-only” claims are the most commontype of workers’ compensation claim, but they repre-sent only a small share of overall payments.

Temporary disability claims. When a work-relatedinjury or illness temporarily prevents a worker fromreturning to their pre-injury job or to another jobfor the same employer, temporary total disability(TTD) benefits are paid in addition to medical ben-efits. Benefits replace approximately two-thirds ofthe worker’s gross, pre-injury weekly earnings fromthe time-of-injury employer up to state-specifiedlimits. If the worker had concurrent employment at

the time of injury – an additional job (or jobs) withanother employer – earnings from a second or otherjob may or may not be covered by temporary disabil-ity benefits.

Compensation for temporary disability is subject tomaximum and minimum benefit levels that varyfrom state to state. As of January 2017, the maxi-mum weekly TTD benefit ranged from a high of$1,688 in Iowa to a low of $478 in Mississippi. Theminimum weekly benefit ranged from a high of$583 in North Dakota to a low of $20 in Arkansas,Florida, and Wisconsin.11

Most workers who receive TTD benefits fully recover and return to work, at which time benefitsend. In many cases, however, employers makeaccommodations allowing injured workers to returnto transitional work before they are physically able toresume all of their former job duties. In these cases,workers may be assigned to restricted duties or short-er hours at lower wages. When injured workersreturn to work at less than their pre-injury wage,they may be eligible for temporary partial disability(TPD) benefits in some states.

Permanent disability claims. Some injured workersexperience work-related injuries or illnesses thatresult in permanent impairments. These workersmay be eligible for either permanent partial or permanent total disability benefits, after they reachmaximum medical improvement (the point at whichfurther medical intervention is no longer expected toimprove functional capacity or provide further healing).12 Permanent total disability (PTD) benefitsare paid to workers who are considered legallyunable to work at all because of a work-related

6 NATIONAL ACADEMY OF SOCIAL INSURANCE

9 In Washington, workers pay part of workers’ compensation premium costs through payroll deductions (See page 36 and footnote toTable 14). Oregon assesses employers and employees for the Workers Benefit Fund, which pays monthly cost-of-living increases forcertain beneficiaries and provides funding for return to work policies that provide incentives to improve employment for injuredworkers. Between 2014 and 2016, the Oregon Workers Benefit Fund Assessment was 3.3 cents per hour worked – employers paid1.65 cents per hour and workers paid 1.65 cents per hour. New Mexico applies a per capita assessment based on employment on thelast day of the quarter. Since 2004, the quarterly workers’ compensation fee is $4.30 per covered worker, which is split between em-ployers and employees. The employers’ share is $2.30 per covered worker and the employees’ share is $2.00. The majority of the totalfee ($4.00 – $2.00 from employers and $2.00 from employees) is used primarily to fund the operation of the New Mexico Workers’Compensation Administration. The additional $0.30 per covered worker paid by employers is used to fund the Workers’ Compensa-tion Uninsured Employers Fund.

10 Some economists argue that workers pay a substantial portion of program costs indirectly in the form of lower wages (Leigh, et al.2000; Gruber and Krueger, 1991).

11 Colorado, Iowa, Maine, Michigan, Montana, Nevada, Oklahoma, and Rhode Island do not have a specified minimum weekly TTDbenefit. Details on benefit and coverage provisions of state laws are summarized in Appendix C.

12 In most claims where workers ultimately receive permanent disability benefits, there is initially a period in which the workers receivetemporary disability benefits, as described in the preceding paragraphs.

injury or illness.13 Permanent partial disability(PPD) benefits are paid to workers whose injuriesresult in permanent impairments, even though theyare able to work in some capacity.

States differ in their methods for determiningwhether a worker is entitled to permanent partialdisability benefits, the extent of permanent disability,and the amount of benefits to be paid (Barth andNiss, 1999; Burton, 2008). There are three opera-tional approaches to determining eligibility for PPDbenefits: The impairment approach pays benefits ifthe worker has a permanent medical loss. The loss ofearning capacity approach pays benefits if the impair-ment causes a permanent loss of earning capacity.The wage loss approach pays benefits only if theworker has actual wage losses. In the first case, theamount of permanent disability benefits is deter-mined by some measure of physical loss to the body;in the second case by an estimate of reduced earningcapacity. In the third case, if the worker has the abili-ty to work in some capacity and actually works, heor she will not receive PPD benefits if no wage loss isincurred.14 Most states impose limits on either themaximum duration or maximum amount of perma-nent disability benefits.15

Fatalities. Workers’ compensation programs also paydeath benefits when a work-related illness or injuryis fatal. The benefits typically include an amount forfuneral and burial expenses, and cash benefits for theworker’s family or dependents. For workers who diewithout dependents, benefits are designed to coverfuneral and burial expenses.

Sources of Workers’ Compensation Insurance Non-federal employers pay for workers’ compensa-tion by purchasing insurance from a privateinsurance carrier, a state workers’ compensationinsurance plan (called a state fund), or by self-

insuring. Federal workers’ compensation insurancecovers federal civilian employees and some private-sector workers employed either in high-risk jobs orjobs related to national defense (see Federal Programson page 8). Many states also have special workers’compensation funds to cover exceptional circum-stances, such as a second work-related injury.

Private insurance. Workers’ compensation policiesprovided by private insurers operate much like automobile or homeowners’ insurance. Employerspurchase insurance for a premium, which variesaccording to expected risk. There are two types ofpolicies: (1) a policy that requires the insurer to payall workers’ compensation benefits; and (2) a policywith a deductible that requires the employer to reimburse the insurer for benefits paid up to thespecified deductible amount. In return for acceptinga policy with a deductible, the employer pays a lowerpremium. Deductibles may be written into an insurance policy on a per-injury basis, an aggregate-benefit basis, or a combination of both. Most statespermit deductible policies in workers’ compensationinsurance, but state regulations vary regardingspecifics (e.g. the maximum deductible allowed andthe minimum premium volume eligible for adeductible policy).

State funds. State workers’ compensation funds areestablished by an act of a state legislature and may bedesignated as exclusive or competitive. An exclusivestate fund is, by statute, the sole provider of workers’compensation insurance in a state (although somestates with an exclusive state fund allow largeemployers to self-insure). A competitive state fundcompetes with private insurers. For this report, wedefine an insurer as a competitive state fund if: (1)the insurer sells workers’ compensation policies toprivate-sector employers in the voluntary insurancemarket; and (2) the insurer is exempt from federaltaxes.16 In 2016, four states had exclusive state funds

Workers’ Compensation: Benefits, Costs, and Coverage • 7

13 Most states allow permanently and totally disabling conditions to be compensated for life if the condition leads to an inability to work. The requirements for a lifetime PTD benefit vary across jurisdictions, but many have a provision such that if an injuredworker has a permanent disability rating over a specified threshold (for instance, more than 70 percent disabled), then the workerwould qualify.

14 A few states do not pay permanent disability benefits if the injured worker returns to work at a wage that is at least 80 percent oftheir pre-injury wage.

15 Many PPD cases are settled with compromise and release agreements (see glossary for complete definition).

16 All competitive state funds are exempt from federal taxes and six funds are also exempt from paying state premium taxes (Hawaii,Idaho, Louisiana, New Mexico, Texas, and Utah).

and, according to our criteria, 17 states had competi-tive state funds.17,18 In addition, South Carolinahad a nonexclusive state fund that provided workers’compensation insurance for state and local govern-ment employees but did not write policies for privateemployers. West Virginia discontinued its state fundin 2009. However, the state was still paying benefitsin 2016 on some claims involving injuries thatoccurred before 2009.

Self-insurance. Many large employers choose to self-insure for workers’ compensation.19 Where self-insurance is permitted, employers must apply forpermission to self-insure from the regulatory authority, and demonstrate that they have sufficientfinancial resources to cover their expected workers’compensation losses.20 Some states permit groups ofemployers in the same industry or trade associationto self-insure through group self-insurance.

Federal programs. The federal government coversworkers’ compensation benefits for federal civilianemployees under the Federal EmployeesCompensation Act (FECA). Federal programs alsocover some private-sector workers, including coalminers with black lung disease, employees of overseas contractors with the U.S. government,

energy employees exposed to certain hazardous materials, workers engaged in manufacturing atomicbombs, and veterans injured while on active duty inthe armed forces. The federal government also provides oversight for workers covered under theLongshore and Harbor Workers’ Compensation Act(LHWCA), but employers are still required to purchase private insurance or self-insure. (Moredetails about these federal programs are provided inAppendix B.)

Guaranty funds. State guaranty funds ensure benefitpayments to injured workers in cases where a privateinsurance carrier or self-insured employer becomesinsolvent and does not have sufficient assets ear-marked to pay outstanding benefits. The benefitpayments and administrative costs of guaranty fundsfor private insurers are typically funded throughassessments on workers’ compensation insurers,while the costs of guaranty funds for self-insuredemployers are funded through assessments on self-insuring employers.

Second injury funds. Second injury funds reim-burse employers or insurance carriers in cases wherean employee with a pre-existing condition related toa work-related injury experiences another work-related injury or illness. The second injury fund paysany costs associated with the prior condition toreduce the cost burden on the current employer. Thefunds encourage employers to hire injured workerswho want to return to work with residual impair-ments. The current employer is responsible only forworkers’ compensation benefits associated with thesecond injury or illness. Second injury funds arefinanced through assessments on employers, and, ina small number of jurisdictions, with general fundmonies.21

17 In 2016, North Dakota, Ohio, Washington, and Wyoming had exclusive state funds. Competitive state funds operated in California,Colorado, Hawaii, Idaho, Kentucky, Louisiana, Maryland, Missouri, Montana, New Mexico, New York, Oklahoma, Oregon, Penn-sylvania, Rhode Island, Texas, and Utah.

18 Of the 17 competitive state funds, 12 operated as the “insurer of last resort,” by selling policies to high-risk employers or any otheremployers that were unable to self-insure or purchase insurance from a private carrier.

19 Employers are allowed to self-insure in all states except for North Dakota and Wyoming, which both require all employers to obtainworkers’ compensation insurance from their exclusive state funds.

20 Nearly all self-insured firms are required to post some type of financial security (e.g. surety bonds) so that workers’ compensationbenefits are paid even if the employer experiences financial distress.

21 See Sources and Methods 2016 on the Academy’s website for further details on special funds, second injury funds, and guarantyfunds.

8 NATIONAL ACADEMY OF SOCIAL INSURANCE

Employers pay for workers’ compensation by purchasing

insurance from a private insurancecarrier, or a state workers’

compensation insurance plan (called a state fund), or some large

employers may self-insure.

Workers’ Compensation: Benefits, Costs, and Coverage • 9

Estimates for 2016The workers’ compensation system involves numerous stakeholder groups: employers, workers,insurers, attorneys, medical providers and state governments. The estimates presented in this reportreflect the aggregate experience of only two groups:workers who rely on compensation for workplaceinjuries, and employers (including the federal government) who pay the bills. The estimates represent benefits and costs paid in each of the lastfive calendar years.

Estimates of benefits for 2016 include paymentsmade in 2016 for injuries and illnesses that occurredin 2016 and in prior years. If an employer purchasesworkers’ compensation insurance from a privateinsurer or state fund, estimates of costs for 2016include premiums that incorporate projected futureliabilities for injuries and illnesses that occur in 2016.If an employer is self-insured, the cost estimatesinclude only those payments made in 2016, eventhough the employer is liable for future costs.

The Academy’s measures are designed to provide thebest available estimates of workers’ compensationbenefits, costs, and coverage, in a given year and overtime. The estimates are not designed to assess the performance of the insurance industry or insurancemarkets. Other organizations analyze insurancetrends.22 The estimates are also not designed to measure the performance of the workers’ compensa-tion system with respect to: the prevention ofoccupational injuries and illnesses; the adequacy,equity, and affordability of compensation; or theimpact of vocational rehabilitation and job accommodations in returning injured workers towork.

Finally, it is not appropriate to use the estimates tocompare the performance of workers’ compensationsystems in different states. Benefits and costs varyacross states not only because their workers’ compensation systems differ, but also because statesdiffer in the relative risk of their industry/occupational mix. A meaningful comparison of

benefits or costs across states must control for variation in system features (including waiting peri-ods, compensation rates, limits on insurable earningsand medical fees), the mix of industries and occupations covered (the proportions of employersin different insurance classifications in each state),and worker outcomes (such as claim acceptance rate,return-to-work rate), which is beyond the scope ofthis report.

Covered Employmentand Wages Methods for Estimating CoveredEmployment and Wages There is no national system for counting the numberof jobs covered by workers’ compensation, so thenumber of covered jobs and wages must be estimat-ed. The Academy’s methodology (for all states exceptTexas) is designed to count the number of jobswhich are legally required to be covered by workers’compensation under state laws.23

The Academy’s measures are designed to provide the best

available estimates of workers’ compensation benefits, costs, andcoverage at the state and national

levels. The estimates provide data ontrends over time, both nationally

and within states However, it is notappropriate to use the estimates to

compare the performance of workers’ compensation systems

across different states.

22 The National Council on Compensation Insurance and state rating bureaus, for example, assess insurance developments in the statesand advise regulators and insurers on proposed insurance rates.

23 Workers’ compensation covered employment is measured in terms of ‘covered jobs’ as opposed to ‘covered workers.’ Refer to Appen-dix A, Employed Workforce Coverage Estimates.

10 NATIONAL ACADEMY OF SOCIAL INSURANCE

We use the number of jobs and amount of wagescovered by unemployment insurance (UI) in eachstate as the starting point for our estimates.24 Then,we estimate the number of jobs that are not requiredto be covered by workers’ compensation according toeach state’s statute regarding exemptions for smallfirms and/or agricultural employers. We subtract thenumber of exempted jobs from the UI base to deter-mine the number of UI covered jobs that are coveredby workers’ compensation. We then calculate theproportion of UI-covered jobs that are covered byworkers’ compensation in each state, and apply thisproportion to the state’s UI-covered payroll to obtaintotal workers’ compensation covered payroll. InTexas, where coverage is optional for employers, weapply the proportion of jobs in firms that opt-in toworkers’ compensation to the UI base.

The Academy’s methodology may undercount theactual number of jobs (and wages) covered becausesome employers that are not required to carry workers’ compensation do so anyway. For example,self-employed persons are not typically required tocarry unemployment or workers’ compensationinsurance, but, in some states, self-employed personsmay voluntarily elect to be covered. In states withexemptions for small firms, some small firms mayvoluntarily purchase workers’ compensation insurance.

On the other hand, our methodology may overesti-mate the number of jobs (and wages) coveredbecause some employers are not in compliance withtheir state’s workers’ compensation or unemploy-ment insurance laws. Every state has a program todetect and penalize employers who fail to report orcover jobs under state labor statutes, but no definitive national study has documented the extentof noncompliance. (For more details on theAcademy’s methods for estimating coverage refer toAppendix A.)

National Estimates of CoveredEmployment and Wages In 2016, workers’ compensation covered an estimat-ed 138.3 million U.S. jobs, a 1.8 percent increasefrom the previous year (Table 2). Covered payrollwas $7.4 trillion, an increase of 3.1 percent from2015. Covered employment and wages haveincreased steadily since 2011, but the rate of increasedeclined in 2016.

Between 2012 and 2016, covered non-federalemployment increased by an estimated 10.2 millionjobs, or 8.1 percent (Table 3). Covered non-federalwages increased by $1.1 trillion or 17.7 percent(Table 4). Overall, in 2016, workers’ compensationcoverage extended to an estimated 97.4 percent of allnon-federal jobs covered by unemployment insur-ance (Table A.1),25 and 86.5 percent of all jobs inthe U.S. (Table A.2).

In contrast to the trend in the non-federal sector,coverage in the federal workers’ compensation pro-gram declined by 27,000 jobs between 2012 and2016 (Table 3). Federal covered employment fell by2.3 percent between 2012 and 2014, but increasedby 1.3 percent between 2014 and 2016, for an over-all reduction of 1.0 percent over the time period.With respect to covered payroll, there was virtuallyno change in the federal system between 2012 and2014 (0.0%) but covered wages increased by 5.8 percent between 2014 and 2016 (Table 4).

24 Unemployment Insurance (UI) programs, under the U.S. Department of Labor, provide cash benefits to workers who become un-employed (through no fault of their own) and meet specific eligibility requirements.

25 According to unpublished estimates provided by the BLS, 3 percent of civilian (non-federal) workers represented by the BLS Na-tional Compensation Survey (NCS) were employed in establishments reporting zero annual workers’ compensation costs in March2017 (DOL, 2018). Civilian workers are those employed in private industry or state and local governments. Excluded from privateindustry are the self-employed and farm and private household workers. Federal government workers are excluded from the publicsector. The private industry series and the state and local government series provide data for the two sectors separately. The Acad-emy’s estimate of legally required workers’ compensation coverage is 97.5 percent of all UI covered jobs in 2016, which is virtuallyidentical to the workers’ compensation coverage shown by the NCS.

Workers’ compensation covered employment and payroll increased in2016, but the rate of increase wasslower than in the previous year.

Workers’ Compensation: Benefits, Costs, and Coverage • 11

Table 2Workers' Compensation Covered Jobs and Covered Payroll, 1996-2016

Covered Jobs Covered Payroll Year (thousands) Percent Change (billions) Percent Change

1996 114,773 1.7 3,337 6.9

1997 118,145 2.9 3,591 7.6

1998 121,485 2.8 3,885 8.2

1999 124,349 2.4 4,151 6.8

2000 127,141 2.2 4,495 8.3

2001 126,972 -0.1 4,604 2.4

2002 125,603 -1.1 4,615 0.2

2003 124,685 -0.7 4,717 2.2

2004 125,878 1.0 4,953 5.0

2005 128,158 1.8 5,213 5.3

2006 130,339 1.7 5,544 6.3

2007 131,734 1.1 5,857 5.6

2008 130,643 -0.8 5,954 1.7

2009 124,856 -4.4 5,675 -4.7

2010 124,638 -0.2 5,834 2.8

2011 125,876 1.0 6,058 3.8

2012 128,141 1.8 6,326 4.4

2013 130,368 1.7 6,501 2.8

2014 132,902 1.9 6,831 5.1

2015 135,850 2.2 7,198 5.4

2016 138,251 1.8 7,422 3.1

Source: National Academy of Social Insurance estimates. See Appendix A for more details.

12 NATIONAL ACADEMY OF SOCIAL INSURANCE

Table 3

Wor

kers' C

ompe

nsation Cov

ered

Job

s by

State, 2

012-20

16

Num

ber of

Jobs

(in

thou

sand

s)Pe

rcen

t Cha

nge

Ran

king

Stat

e20

1220

1320

1420

1520

1620

12-2

014

2014

-201

620

12-2

016

Alaba

ma

1,69

81,

717

1,73

71,

765

1,78

92.

33.

05.

329

Alask

a31

131

331

531

731

11.

4-1

.30.

049

Arizo

na2,

374

2,43

12,

485

2,55

52,

625

4.7

5.6

10.6

12

Ark

ansa

s1,

098

1,09

81,

109

1,12

91,

143

1.0

3.0

4.1

39

Califo

rnia

14,6

7415

,139

15,5

6716

,051

16,4

716.

15.

812

.26

Col

orad

o2,

200

2,27

12,

353

2,42

82,

485

6.9

5.6

13.0

4

Con

nect

icut

1,61

11,

623

1,63

61,

645

1,64

91.

60.

82.

446

Delaw

are

398

407

417

427

432

4.7

3.5

8.3

16

District o

f Col

umbi

a50

651

953

254

555

65.

14.

59.

813

Flor

ida

6,86

67,

045

7,27

87,

561

7,81

76.

07.

413

.92

Geo

rgia

3,65

93,

737

3,84

93,

968

4,07

65.

25.

911

.49

Haw

aii

569

583

593

605

614

4.3

3.6

8.0

19

Idah

o60

261

863

465

267

55.

36.

512

.17

Illin

ois

5,53

75,

590

5,66

95,

754

5,80

12.

42.

34.

836

Indi

ana

2,76

22,

799

2,84

22,

892

2,93

62.

93.

36.

322

Iow

a1,

443

1,46

41,

483

1,49

71,

506

2.8

1.5

4.4

37

Kan

sas

1,28

51,

303

1,32

21,

332

1,33

52.

91.

03.

940

Ken

tuck

y1,

718

1,73

81,

765

1,79

41,

820

2.7

3.1

5.9

23

Loui

sian

a1,

833

1,85

81,

889

1,89

61,

873

3.1

-0.9

2.2

47

Mai

ne56

556

957

357

858

51.

42.

13.

542

Mar

ylan

d2,

363

2,38

42,

406

2,44

32,

477

1.8

3.0

4.8

33

Mas

sach

uset

ts3,

190

3,24

43,

315

3,38

23,

448

3.9

4.0

8.1

17

Michi

gan

3,78

83,

873

3,94

44,

016

4,09

44.

13.

88.

118

Min

neso

ta2,

597

2,64

32,

682

2,72

72,

765

3.3

3.1

6.5

21

Mississip

pi1,

008

1,01

81,

027

1,04

11,

051

1.9

2.3

4.2

38

(1=l

arge

st p

erce

nt in

crea

se,

2012

-201

6)

Workers’ Compensation: Benefits, Costs, and Coverage • 13

Miss

ouri

2,43

62,

467

2,49

62,

541

2,57

82.

43.

35.

824

Mon

tana

414

421

424

432

438

2.4

3.3

5.8

25

Neb

rask

a89

290

591

893

194

02.

92.

45.

428

Nev

ada

1,11

21,

140

1,18

21,

224

1,26

26.

46.

713

.53

New

Ham

pshi

re60

561

161

962

964

02.

33.

35.

726

New

Jersey

3,72

53,

769

3,79

33,

841

3,90

51.

82.

94.

834

New

Mex

ico

730

738

746

755

756

2.3

1.2

3.5

41

New

Yor

k8,

428

8,54

98,

710

8,87

89,

015

3.3

3.5

7.0

20

Nor

th C

arol

ina

3,74

43,

814

3,89

94,

002

4,09

74.

15.

19.

414

Nor

th D

akot

a39

941

443

242

440

48.

3-6

.51.

348

Ohi

o4,

967

5,03

35,

108

5,18

25,

242

2.8

2.6

5.5

27

Okl

ahom

a1,

406

1,43

51,

461

1,47

21,

454

3.9

-0.5

3.4

43

Ore

gon

1,61

21,

651

1,69

91,

760

1,81

35.

36.

712

.45

Penn

sylv

ania

5,45

85,

482

5,52

95,

576

5,62

11.

31.

73.

044

Rho

de Is

land

441

445

452

459

462

2.6

2.1

4.8

35

Sout

h C

arol

ina

1,71

71,

755

1,80

41,

858

1,90

35.

15.

510

.811

Sout

h D

akot

a38

538

939

540

040

42.

72.

25.

031

Tenn

esse

e2,

507

2,55

02,

607

2,67

72,

742

4.0

5.2

9.4

15

Texa

s8,

477

8,67

88,

903

9,23

89,

472

5.0

6.4

11.7

8

Uta

h1,

177

1,21

61,

253

1,30

11,

348

6.5

7.6

14.6

1

Ver

mon

t29

029

229

529

829

81.

81.

02.

945

Virgi

nia

3,37

53,

400

3,41

63,

490

3,54

21.

23.

74.

932

Was

hing

ton

2,82

22,

889

2,97

23,

049

3,14

15.

35.

711

.310

Wes

t Virgi

nia

674

668

665

661

649

-1.3

-2.4

-3.7

51

Wisco

nsin

2,60

12,

628

2,66

62,

701

2,73

32.

52.

55.

130

Wyo

min

g27

127

227

727

526

42.

3-4

.6-2

.450

Tota

l Non

-Fed

eral

125,

321

127,

597

130,

146

133,

057

135,

458

3.8

4.1

8.1

Fede

ral E

mpl

oyee

s2,

820

2,77

12,

756

2,79

32,

793

-2.3

1.3

-1.0

TO

TAL

128,

141

130,

368

132,

902

135,

850

138,

251

3.7

4.0

7.9

Sour

ce:N

atio

nal A

cade

my

of S

ocia

l Ins

uran

ce estim

ates

. See

App

endi

x A fo

r m

ore de

tails

.

14 NATIONAL ACADEMY OF SOCIAL INSURANCE

Table 4

Wor

kers' C

ompe

nsation Cov

ered

Pay

roll by

State, 2

012-20

16

Cov

ered

Pay

roll

(in m

illio

ns)

Perc

ent C

hang

eRan

king

Stat

e20

1220

1320

1420

1520

1620

12-2

014

2014

-201

620

12-2

016

Alaba

ma

$69,

543

$70,

928

$73,

424

$76,

375

$78,

405

5.6

6.8

12.7

37Alask

a15

,367

15,8

2216

,499

17,0

0816

,316

7.4

-1.1

6.2

49Arizo

na10

6,98

611

0,45

511

5,30

012

1,11

712

6,02

57.

89.

317

.819

Ark

ansa

s41

,475

42,2

9743

,869

45,6

9347

,036

5.8

7.2

13.4

33C

alifo

rnia

831,

610

861,

194

914,

844

986,

111

1,03

3,04

810

.012

.924

.24

Col

orad

o11

0,07

311

4,42

612

2,94

213

0,42

113

4,65

311

.79.

522

.38

Con

nect

icut

99,9

3510

1,06

410

4,44

110

7,65

210

8,46

94.

53.

98.

546

Delaw

are

20,5

5321

,108

22,1

0422

,963

23,1

177.

54.

612

.538

District o

f Col

umbi

a38

,542

39,7

5641

,850

44,2

4545

,668

8.6

9.1

18.5

16Fl

orid

a29

3,32

730

4,27

332

2,82

234

6,21

536

4,25

910

.112

.824

.25

Geo

rgia

167,

072

172,

639

183,

067

194,

315

204,

327

9.6

11.6

22.3

9H

awai

i23

,760

24,7

5325

,911

27,4

5528

,671

9.1

10.7

20.7

11Id

aho

21,4

6322

,475

23,7

6825

,003

26,4

2110

.711

.223

.16

Illin

ois

287,

520

292,

573

305,

179

320,

627

325,

926

6.1

6.8

13.4

34In

dian

a11

3,01

711

5,79

812

0,02

412

6,04

413

0,02

06.

28.

315

.029

Iow

a57

,861

59,8

7362

,775

65,6

9167

,335

8.5

7.3

16.4

24K

ansa

s52

,268

53,6

0755

,958

57,9

0758

,383

7.1

4.3

11.7

41K

entu

cky

68,6

9270

,161

73,2

6277

,074

79,5

316.

78.

615

.827

Loui

sian

a78

,716

81,1

7184

,992

86,3

8884

,735

8.0

-0.3

7.6

48M

aine

21,4

2621

,976

22,7

8323

,734

24,4

896.

37.

514

.331

Mar

ylan

d12

2,14

812

3,58

612

7,74

113

3,95

313

7,95

24.

68.

012

.935

Mas

sach

uset

ts19

3,73

320

0,04

421

1,96

722

5,05

423

2,04

09.

49.

519

.814

Michi

gan

175,

830

181,

351

190,

005

199,

827

207,

375

8.1

9.1

17.9

18M

inne

sota

127,

560

132,

003

137,

888

145,

477

149,

647

8.1

8.5

17.3

21M

ississip

pi35

,511

36,4

9137

,457

38,4

8539

,380

5.5

5.1

10.9

43

(1=l

arge

st p

erce

nt in

crea

se,

2012

-201

6)

Workers’ Compensation: Benefits, Costs, and Coverage • 15

Misso

uri

102,

953

105,

206

109,

409

114,

664

117,

818

6.3

7.7

14.4

30M

onta

na15

,008

15,4

9216

,159

16,9

6917

,472

7.7

8.1

16.4

23N

ebra

ska

34,6

8735

,821

37,4

5039

,527

40,6

138.

08.

417