national research council industrial research assistance program characteristics of firms that grow...

TRANSCRIPT

National Research CouncilIndustrial Research Assistance Program

Characteristics of Firms that Grow fromSmall to Medium Size

Presented by Denise GuillemetteFPTT Conference – 17 June 2004

2

Collaborative Project with Statistics Canada

• Collaboration between the Science, Innovation and Electronic Information Division (SIEID), Statistics Canada and NRC-IRAP (Frances Anderson and Michael Bordt, Stat Can Project Managers)

• Objective: to increase the knowledge about the internal and external environmental factors surrounding the growth of firms in that very important phase of moving from small to medium size

3

Methodology • Literature review• Interviews (25) with firms, some of which have

made the transition• Production of statistical tables from existing

datasets:• The Longitudinal Employment Analysis

Program (LEAP)/Small Area File (SAF) – represent 1.1 million of firms in 1995

• The Survey of Innovation 1999• The Research and Development in Canadian

Industry (RDCI)• The Advanced Technologies in Canadian

Manufacturing Survey 1998

4

Definition of High Growth Firms

High Growth Firms (also called Gazelles) are firms that doubled the number of employees in five years and at the end of the five years have at least 20 employees

5

Definitions of Non-High Growth Firms

• Growers are firms that increased the number of employees by at least 20% and less than 100%

• Stable firms are firms that remained within 20% range of their employment from the start of the reference period

• Decliners are firms that decreased their employment by more than 20% form the start of the reference period

• Deaths are firm did not exist at the end of the five years.

6

Methodology (cont’d)

• Comparison between the high growth firms (referred to as gazelles) and the non-high growth categorized as growers, stable firms, decliners and deaths by size category

• Size categories• Small 1-99:

• 1-19, 20-49, 50-99• Medium 100-499• Large 500+

• Investigate differences between two size categories: 20-49 and 50-99

• Period for the study is from 1995 to 2000 (with some exceptions)

7

Theory of Stages of Growth• Firms are not all growth oriented: Growth orientation of a

firm at the time of its formation maybe one of the most critical factors which will affect the growth path of the venture

• “Life Style” stage : deliberate choice of the business manager/owner or it could be the limited nature of the enterprise’s market. Firms are set up to support a certain life style

• “Foundation” (family businesses): set up to generate enough income for those involved

• “Capped Growth” stage: firms that have disengaged from the growth process after successfully expanding from the start-up phase

• Entrepreneurial growth-oriented firms: aim is to increasing value, i.e. to realise a return on investment for stakeholders

8

Growth Distribution of Firms Between 1995-2000 (LEAP/SAF)

Ref: Statistics Canada LEAP/SAF

% Growth Distribution of Firms Between 1995-2000

1.4

10.6

50.0

26.0

6.35.5

0

10

20

30

40

50

60

MicroGazelles

Gazelles Growers Stable Declined Died

9

Where were the Job in 1995?

• Only 4% of employment were in the firms that will will experience high growth (include 1% in the micro-high growth firms)

• 34% of employment were in firms that will experience growth (17% of growers + 17% stable firms)

• The majority, 62%, of employment were in firms that will either decline or died (40% decliners + 22% died)

10

Who Pay More?

• In 1995, firms with 500+ employees exhibit the largest average pay compare to any other size category

• In 2000, the high growth firms with 100-499 employees (medium-sized) exhibit the highest average pay compare to any other size category and growth distribution (surpassing the large firms by 16.5%)

• In general, between 1995 and 2000, the change in average pay is highest for firms that experienced high growth except for the large firms – being the lowest

11

Hypothesis # 1: There will be more smaller high grow firms than large high grow firms

12

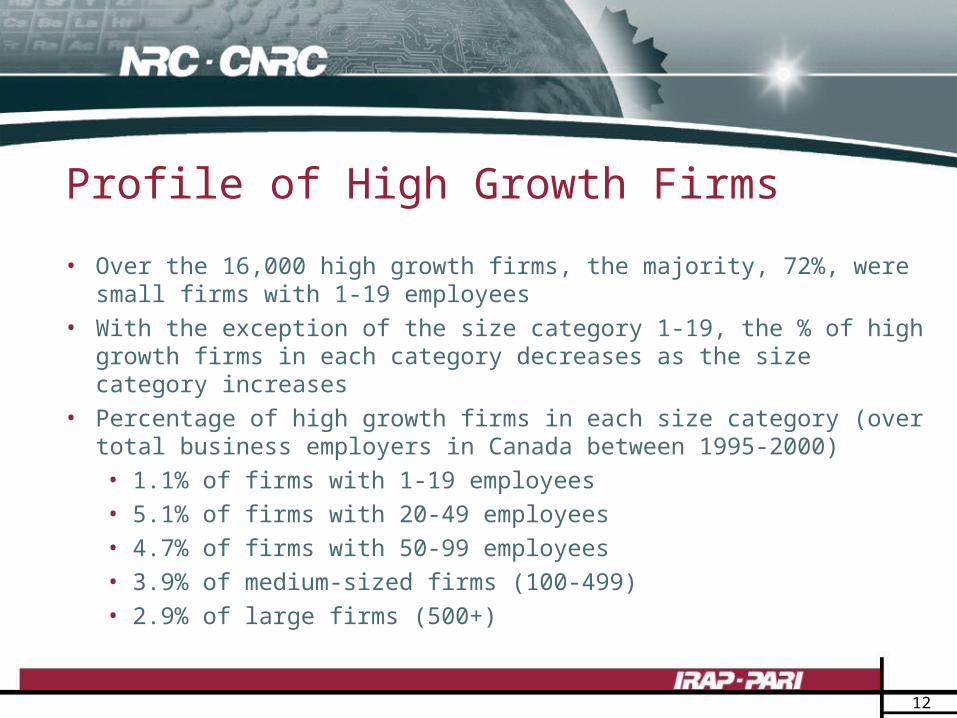

Profile of High Growth Firms

• Over the 16,000 high growth firms, the majority, 72%, were small firms with 1-19 employees

• With the exception of the size category 1-19, the % of high growth firms in each category decreases as the size category increases

• Percentage of high growth firms in each size category (over total business employers in Canada between 1995-2000)• 1.1% of firms with 1-19 employees• 5.1% of firms with 20-49 employees• 4.7% of firms with 50-99 employees• 3.9% of medium-sized firms (100-499) • 2.9% of large firms (500+)

13

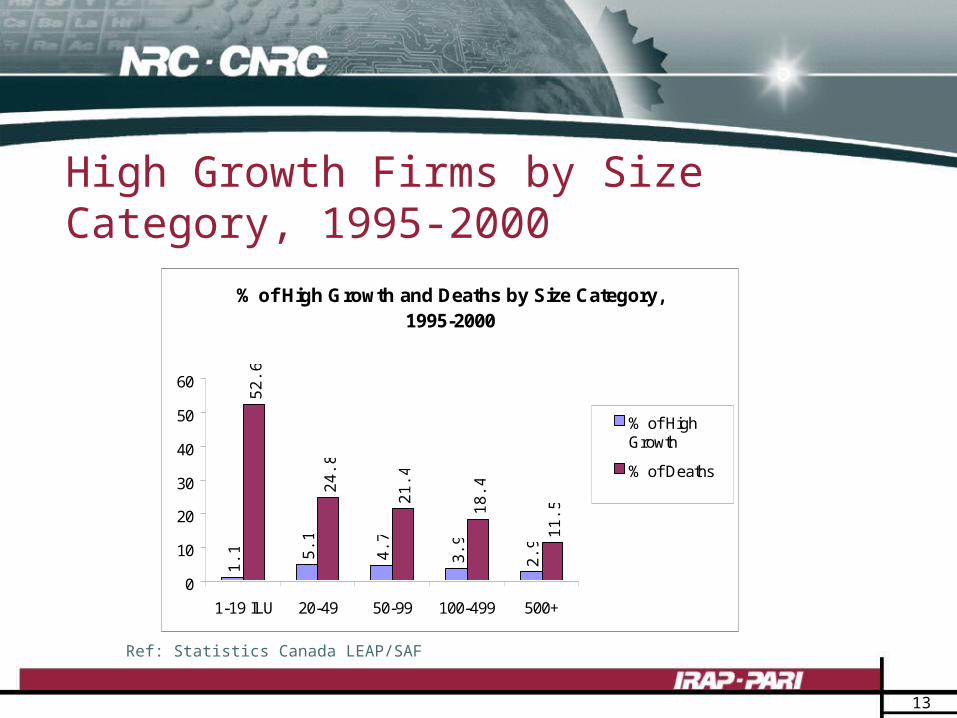

High Growth Firms by Size Category, 1995-2000

Ref: Statistics Canada LEAP/SAF

% of High Growth and Deaths by Size Category, 1995-2000

1.1 5.

1

4.7

3.9

2.9

52.6

24.8

21.4

18.4

11.5

0

10

20

30

40

50

60

1-19 ILU 20-49 50-99 100-499 500+

% of HighGrowth

% of Deaths

14

Hypothesis # 2: High growth small firms will be concentrated in certain industries

15

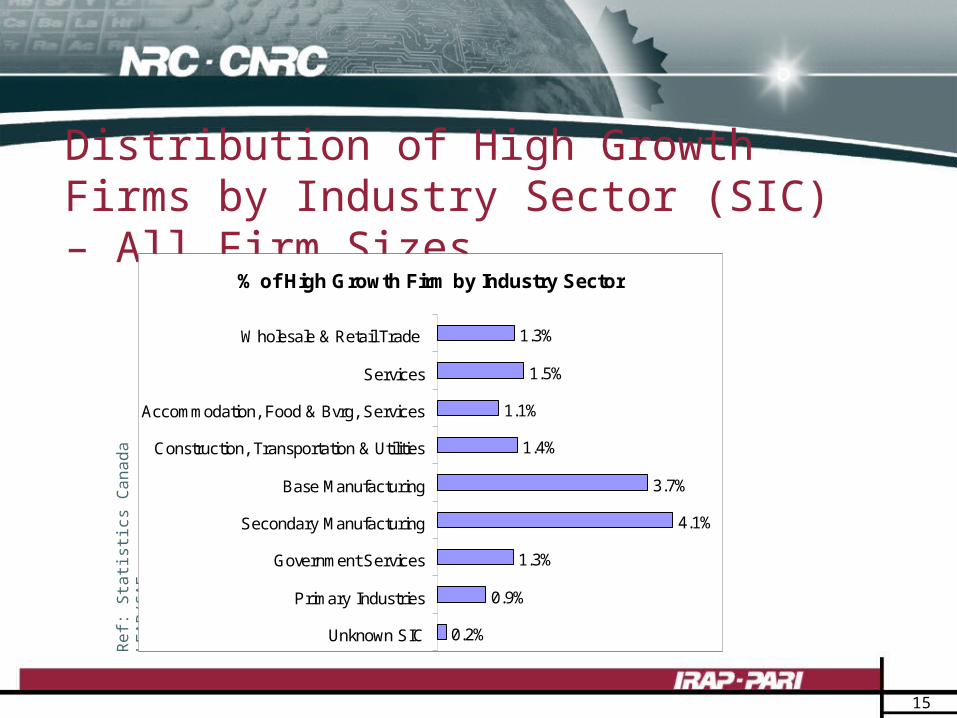

Distribution of High Growth Firms by Industry Sector (SIC) – All Firm Sizes

Ref:

Sta

tist

ics

Can

ad

a

LE

AP

/SA

F

% of High Growth Firm by Industry Sector

1.3%

1.5%

1.1%

1.4%

3.7%

4.1%

1.3%

0.9%

0.2%

Wholesale & Retail Trade

Services

Accommodation, Food & Bvrg, Services

Construction, Transportation & Utilities

Base Manufacturing

Secondary Manufacturing

Government Services

Primary Industries

Unknown SIC

16

Secondary and Base Manufacturing

Secondary Manufacturing• Fabricated Metal Products (Except Machinery and

Transportation Equip) 30, Machinery (except Electrical Machinery) 31, Transportation Equip. 32, Electrical and Electronic Products 33, Non-Metallic Mineral Products 35, Refined Petreleum and Coal Products 36, Chemical and Chemicalo Products 37, Other Manufacturing 39

Base Manufacturing• Food 10, Beverage 11, Tobacco Products 12, Rubber Products

15, Plastic Products 16, Leather and Allied Products 17, Primary Textile 18, Textile Products 19, Clothing 24, Wood 25, Furniture and Fixture 26, Paper and Allied products 27, Printing, Publishing and Allied Products 28, Primary Metal 29

17

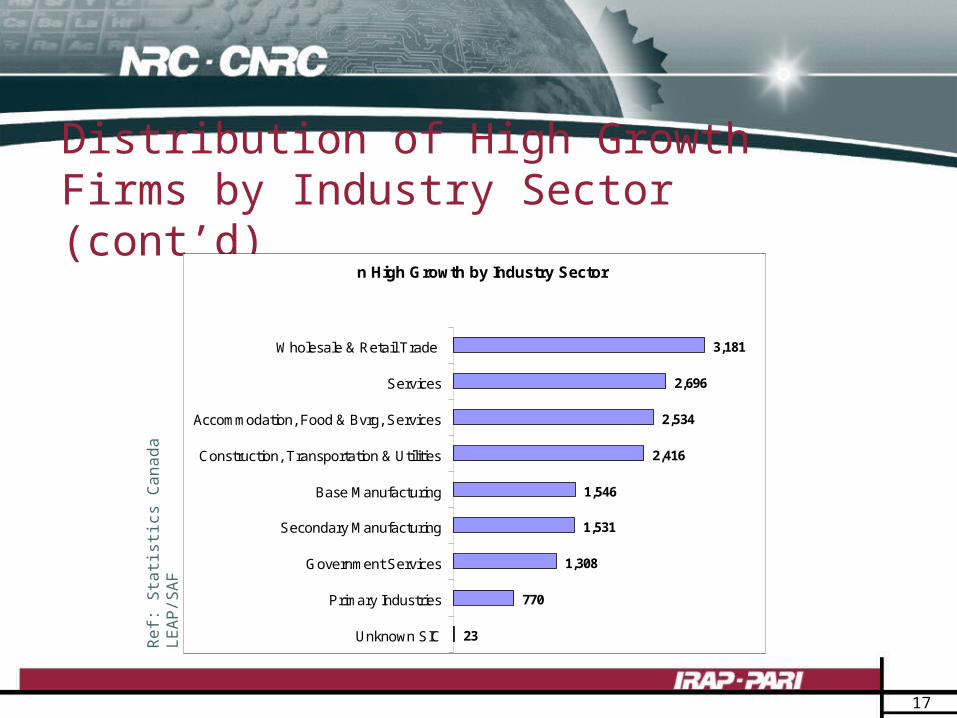

Distribution of High Growth Firms by Industry Sector (cont’d)

n High Growth by Industry Sector

3,181

2,696

2,534

2,416

1,546

1,531

1,308

770

23

Wholesale & Retail Trade

Services

Accommodation, Food & Bvrg, Services

Construction, Transportation & Utilities

Base Manufacturing

Secondary Manufacturing

Government Services

Primary Industries

Unknown SIC

Ref:

Sta

tist

ics

Can

ad

a

LE

AP

/SA

F

18

Distribution of High Growth Firms by Industry Sector (cont’d)

Ref: Statistics Canada LEAP/SAF

6.9

5.9

5.3

5.2

5.1

5.0

5.0

4.5

4.2

4.0

Plastic Products Industry

Electrical Electronic Products

Primary Metal Industries

Transportation Equipment Industries

Furniture Fixture Industries

Wood Industries

Paper Allied Products Industries

Machinery Industry

Fabricated Metal Products

Primary Textile Industry

19

Hypothesis # 3: High growth small firms will be concentrated in certain geographical locations

20

Communities with High Growth Firms• Top 5 communities in terms of number of high growth firms

are:• Toronto – 2781• Montréal – 2029• Vancouver – 1027• Calgary – 823• Edmonton – 668

• Top 5 communities in terms of “%” of high growth firms are:• Yellowknife (NW) – 3.4%• Wood Buffalo (AB) – 3.2%• Saint-Georges (QC) – 2.9%• Grande Prairies (AB) - 2.6%• Chatham (ON) – 2.6%

21

Conclusion

• Based on the LEAP/SAF database, there is no evidence that large communities influence high growth

• Rank in percentage of major communities in Canada:• Vancouver 86• Edmonton 34• Saskatoon 53• Winnipeg 58• Hamilton 60• Quebec 29• Moncton 50• St-John’s 46

22

Hypothesis # 4: Small firms that have developed R&D resources, competencies and capabilities will be more likely to exhibit high growth

23

Average Amount Spent on R&D Activities Per Small R&D Performers in 1995 (in $000)

$497$394

$237

$327

$650

$436

$807

$999

$0

$200

$400

$600

$800

$1,000

$1,200

High growth Growth Stable Declining

20-49 employees

50-99 employees

Source: Statistics Canada, Research and Development in Canadian Industry

24

% Change in Revenues of Small R&D Performers from 1995 to 2000 (constant value $)

7%

17%

43%

197%

-3%

18%

75%

36%

-50%

0%

50%

100%

150%

200%

250%

High growth Growth Stable Declining

20-49 employees

50-99 employees

Source: Statistics Canada, Research and Development in Canadian Industry

25

Hypothesis # 5: Small firms that have developed innovation resources, competencies and capabilities will be more likely to exhibit high growth

26

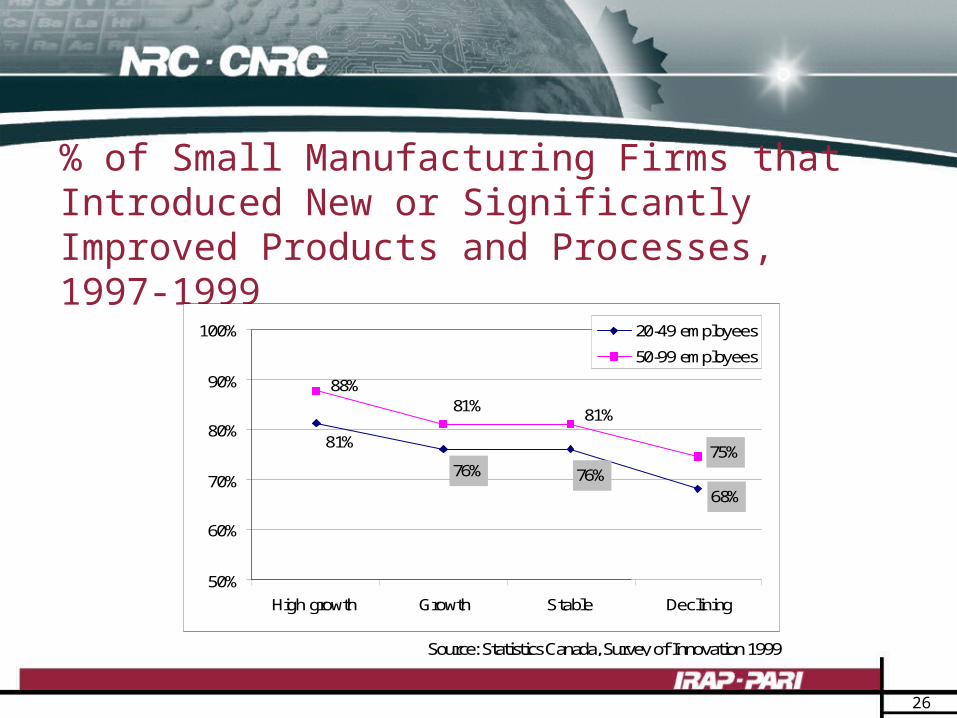

% of Small Manufacturing Firms that Introduced New or Significantly Improved Products and Processes, 1997-1999

68%76%76%

81%75%

81%81%

88%

50%

60%

70%

80%

90%

100%

High growth Growth Stable Declining

20-49 employees

50-99 employees

Source: Statistics Canada, Survey of Innovation 1999

27

ConclusionIn very general terms, based on the Survey of Innovation

1999, high growth firms with 20-49 employees are significantly different from other types of firms in the same size category.

The High Growth firms are:• Are more innovative• Apply more for patents• Use more confidentiality agreements• Use more R&D Tax Credit programs• Are more involved in innovation collaborations

28

Exceptions for Firms with 20-49 Employees

• There is no significant difference between high growth and growers in terms of:• Involvement in R&D activities• Use of at least one government program

• There is no significant difference between high growth and declining firms in terms of:• Introducing a world first innovation

29

Conclusion (cont’d)In very general terms, based on the indicators developed for

the Innovation Survey 1999, there is not much difference between high growth firms with 50-99 employees and non-high growth firms

• Exceptions: Significant differences exist between:• High growth and decliners in terms of “ innovators”• High growth and non-high growth in terms of

“introducing world first innovation”• High growth and stable and decliner firms in terms of

“patent applications”• High growth and decliners in terms of “use of

confidentiality agreements”

30

Thanks

Questions