nba 600: session 8 e-commerce amazon.com 13 february 2003 daniel huttenlocher

TRANSCRIPT

NBA 600: Session 8E-Commerce Amazon.com

13 February 2003

Daniel Huttenlocher

2

Today’s Class

Retail electronic commerce– Look at Amazon.com

• Where they are today• How they got there• What future holds – shopping platform

– Amazon’s focus on user experience (UE)– Leave eBay to communities, not a retailer

Some electronic commerce statistics– Multi channel shoppers

Revisiting some failed businesses– FreshDirect

3

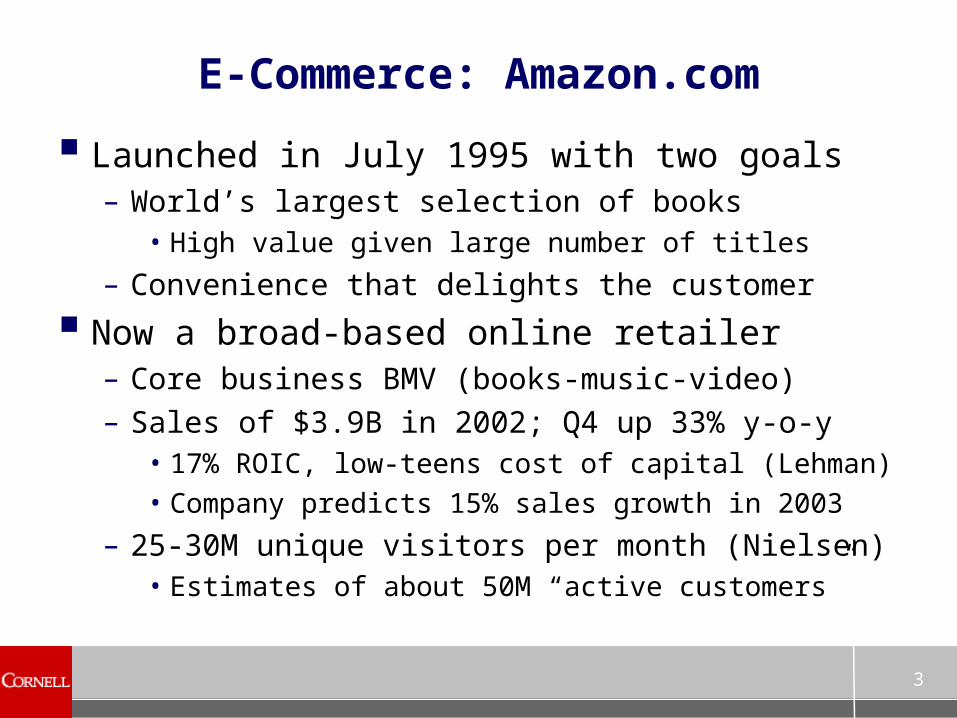

E-Commerce: Amazon.com

Launched in July 1995 with two goals– World’s largest selection of books

• High value given large number of titles

– Convenience that delights the customer

Now a broad-based online retailer– Core business BMV (books-music-video)– Sales of $3.9B in 2002; Q4 up 33% y-o-y

• 17% ROIC, low-teens cost of capital (Lehman)• Company predicts 15% sales growth in 2003

– 25-30M unique visitors per month (Nielsen)• Estimates of about 50M “active customers”

4

What Amazon.com Provides

Online storefront – user experience– For own stores as well as partners and

Marketplace merchants• Marketplace is “mall” of independent merchants

23% of sales in Q1 2002 (Jupiter Media Metrix)

– Extensive focus on delightful user experience• Driven many innovations, adopted others

Payment processing Fulfillment

– Via own warehouses and partnerships with distributors

– Close ties with shippers (UPS, Fedex)

5

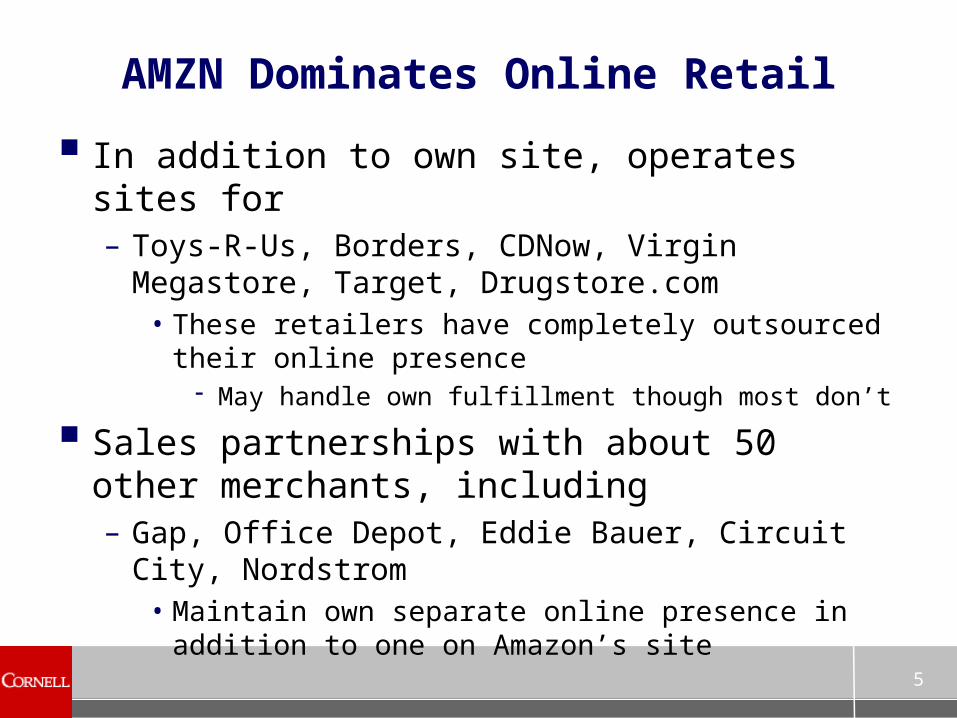

AMZN Dominates Online Retail

In addition to own site, operates sites for– Toys-R-Us, Borders, CDNow, Virgin Megastore,

Target, Drugstore.com• These retailers have completely outsourced their

online presence May handle own fulfillment though most don’t

Sales partnerships with about 50 other merchants, including– Gap, Office Depot, Eddie Bauer, Circuit City,

Nordstrom• Maintain own separate online presence in

addition to one on Amazon’s site

6

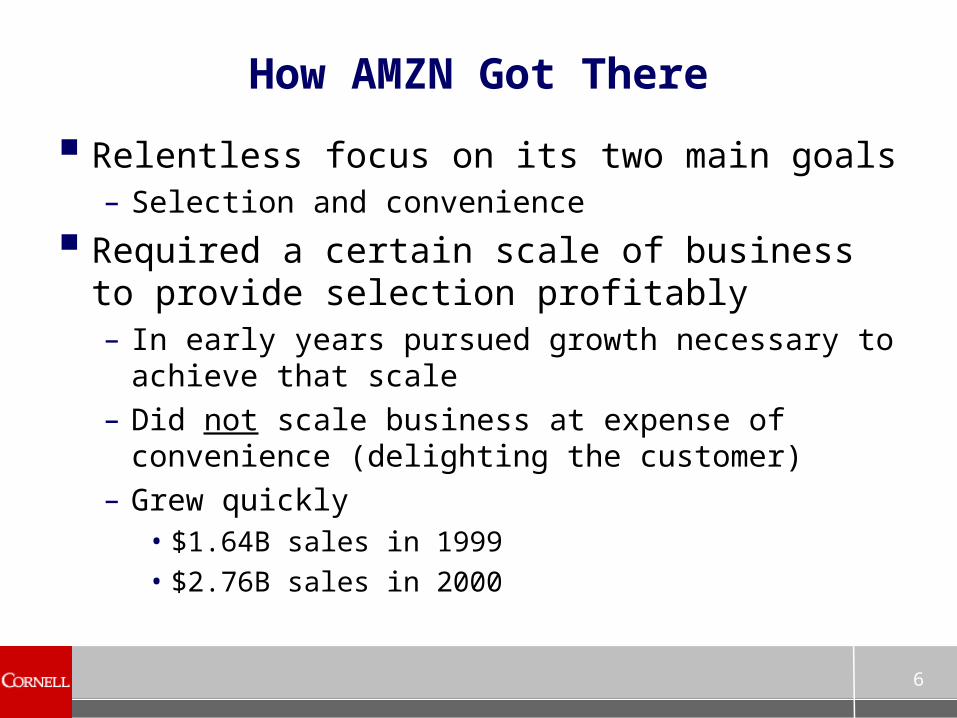

How AMZN Got There

Relentless focus on its two main goals– Selection and convenience

Required a certain scale of business to provide selection profitably– In early years pursued growth necessary to

achieve that scale– Did not scale business at expense of

convenience (delighting the customer)– Grew quickly

• $1.64B sales in 1999• $2.76B sales in 2000

7

What Others Missed

Many saw Amazon’s focus on growth as the goal– It was not; selection and convenience were– Many pursued growth at any cost

Buy.com focus on “lowest prices on earth” – At cost of horrible customer service

• Hard to recover from bad reputation– Focus on price without operational means to

deliver it profitably

Pets.com sales at below cost of goods– Low value goods with high shipping costs

• Amazon did invest in it though

8

AMZN Did Lose Billions

Scaling while providing a delightful user experience was expensive– But losses due to acquisitions, capital

investments and operational inefficiencies• Rather than cost of goods• All could, in principle, be controlled over time

Amazon did not engage in destructive focus on price– Price leader relative to other channels, not

other Internet sites• Strategy seems to have paid off, Buy.com has

(est.) 10% of Amazon’s revenue

9

Building Expensive Infrastructure

Amazon’s initial model was to outsource fulfillment– Largely to Ingram a large book distributor

Found hard to delight customers– Shipping delays were not under their control

• Flexibility to ship in pieces, etc.• Potential logistical advantages of operating high

volume business

In 1999 opened own distribution centers– Rapidly drove down fulfillment costs (% sales)

• 17% Q1‘99, 14% Q1‘01, 12% Q1‘02, 10.6% Q4‘02

10

Capital Markets Forced a Change

Profitability rather than growth as best strategy to achieve goals– Q4 2000 Bezos “March to profitability”

Lehman report questioned whether cash necessary to survive the year, Q1 2001– Potential problem for supplier credit relations

• Critical for operational costs

– March became a dash• More open about what was profitable and by

what measures

Pursued strategies market allowed

11

AMZN Marketplace

Also in late 2000 started showing goods from independent vendors along side own merchandise– Amazon’s merchandise description and pricing

with links to other, generally used, versions

Now also support sales of items not sold by Amazon itself– Brings Amazon and eBay closer in terms of

independent merchants and merchandise• Different models – auction versus fixed pricing• eBay experimenting with fixed price

– Different consumer populations?

12

A Page from WalMart Playbook

In late 2001 Amazon started focusing more on price – has driven growth– Free shipping on orders over certain size

• Many studies show shipping costs are biggest impediment to shopping online

– Discounts on certain product categories• E.g., books over $30

Had achieved scale and operational efficiencies to enable price leadership– Did not make price primary strategy until able

• Quickly dropping fulfillment costs; gross sales

13

Affording Free Shipping

Amazon estimates free shipping will cost it $100M in 2003– Currently available on orders over $25

Longer shipping times for free delivery– Flexibility to lower cost

• Consolidate into one shipment, get vendor to drop-ship, etc.

Dropping TV advertising, relying on print, Internet, word of mouth– Savings of $50M

Resulting sales increase

14

Not Damaging Reputation

Peoples’ expectations for quality of interactions with Amazon are high– Ease of use, selection, rapid delivery

Does slower free shipping disappoint– Expectation of same service even though told

it won’t be– Ease of switching shipping options

Focus on cost makes it important to better control inventory, avoid over stocking– Amazon seems to be working bugs out of new

approach, WSJ 1/9/03 anecdotal evidence

15

Commonalities: AMZN, FDX, DELL

Exploit three ways that the Internet can deliver more value to customers– Better information, service and selection

Focus on information as value-added component of product or service– Use as differentiator from other channels– As grow, use as differentiator within channel

Avoid competing on price until scale or efficiency allow it – Start with premium product and move down– May need price against established channels

16

Where Online Commerce is Going

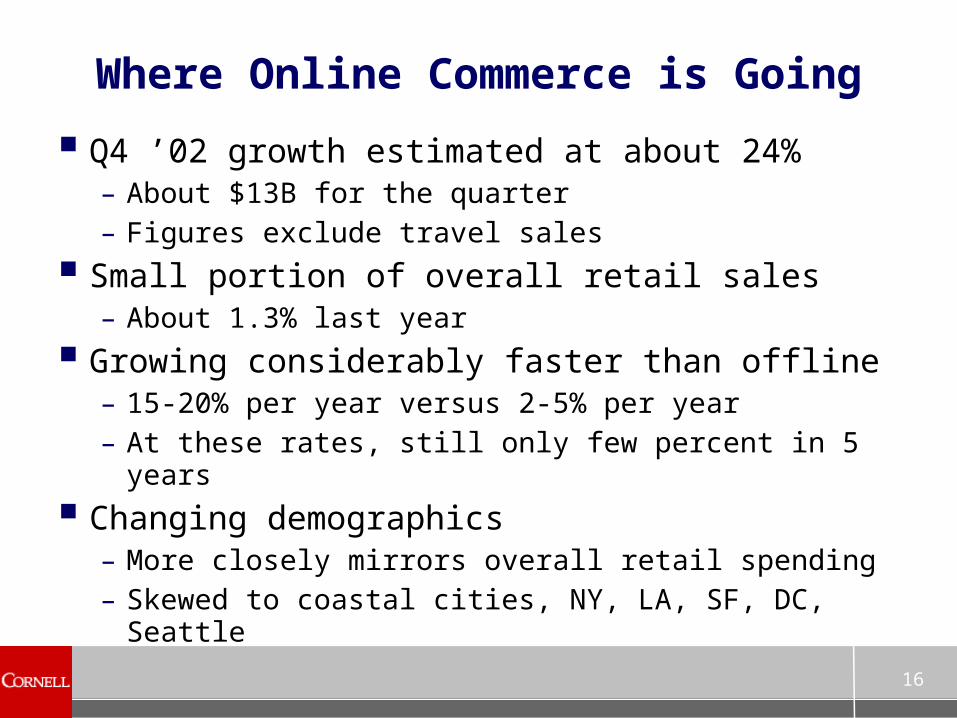

Q4 ’02 growth estimated at about 24%– About $13B for the quarter– Figures exclude travel sales

Small portion of overall retail sales– About 1.3% last year

Growing considerably faster than offline– 15-20% per year versus 2-5% per year– At these rates, still only few percent in 5 years

Changing demographics– More closely mirrors overall retail spending– Skewed to coastal cities, NY, LA, SF, DC, Seattle

17

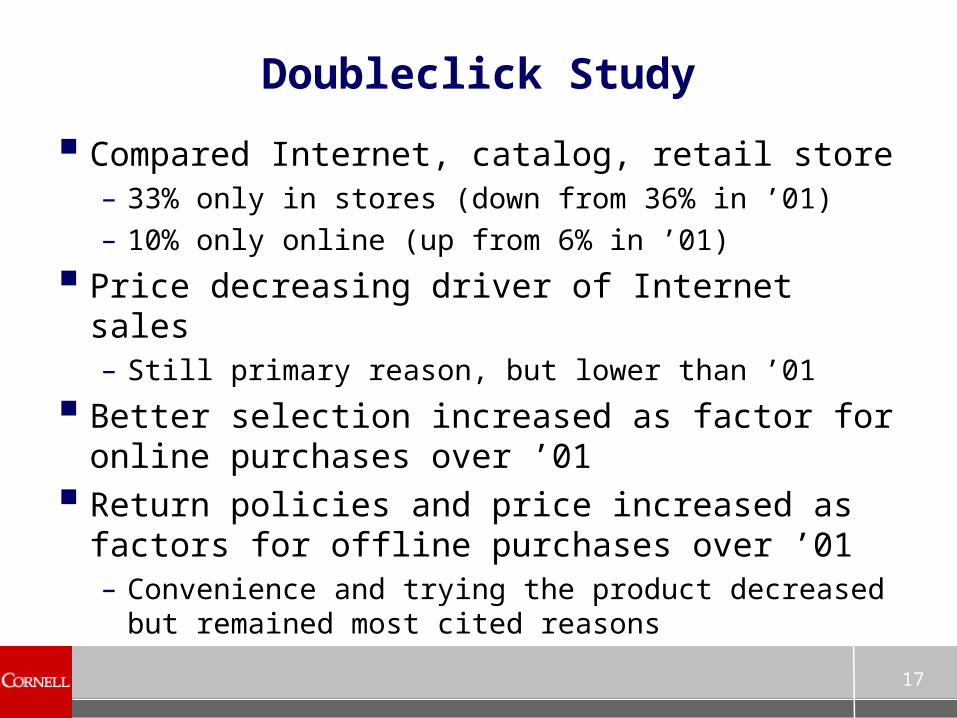

Doubleclick Study

Compared Internet, catalog, retail store– 33% only in stores (down from 36% in ’01)– 10% only online (up from 6% in ’01)

Price decreasing driver of Internet sales– Still primary reason, but lower than ’01

Better selection increased as factor for online purchases over ’01

Return policies and price increased as factors for offline purchases over ’01– Convenience and trying the product decreased

but remained most cited reasons

18

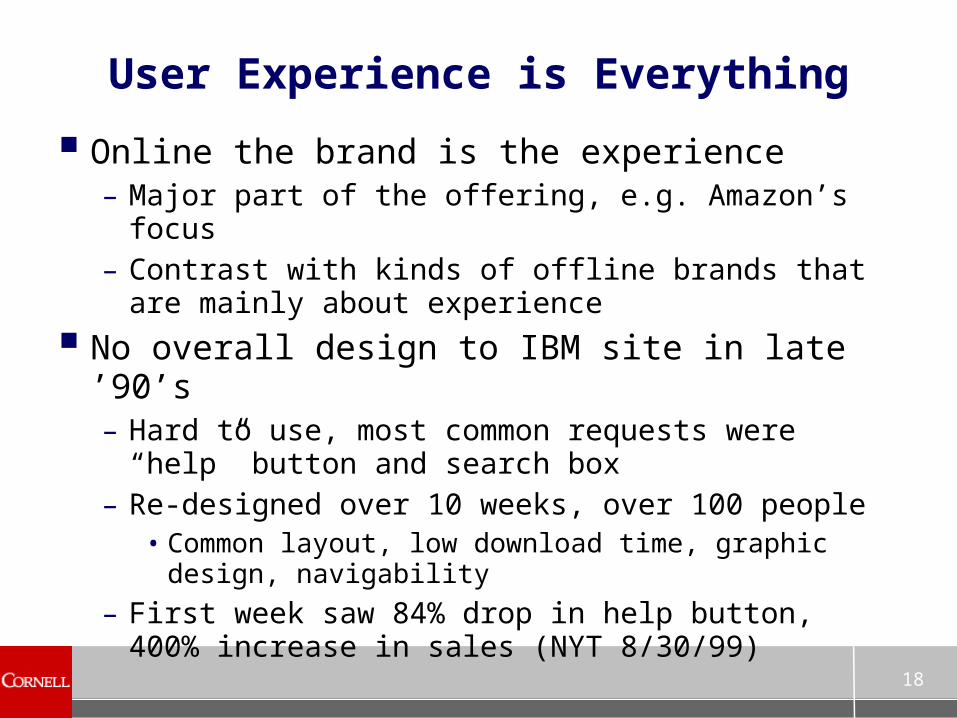

User Experience is Everything

Online the brand is the experience– Major part of the offering, e.g. Amazon’s focus– Contrast with kinds of offline brands that are

mainly about experience

No overall design to IBM site in late ’90’s– Hard to use, most common requests were

“help” button and search box– Re-designed over 10 weeks, over 100 people

• Common layout, low download time, graphic design, navigability

– First week saw 84% drop in help button, 400% increase in sales (NYT 8/30/99)

19

AMZN Focus on Customer

Company attracts people with customer focus – not just in customer facing roles– Including software developers

Continuous testing in their usability lab– Entire experience, not just Web interaction– Tradeoff of new features versus clutter

Metrics to evaluate each change– Careful evaluation of how changes drive sales

Leading the customer carefully– E.g., with one-click addressing fears by making

clear it was easy to cancel

20

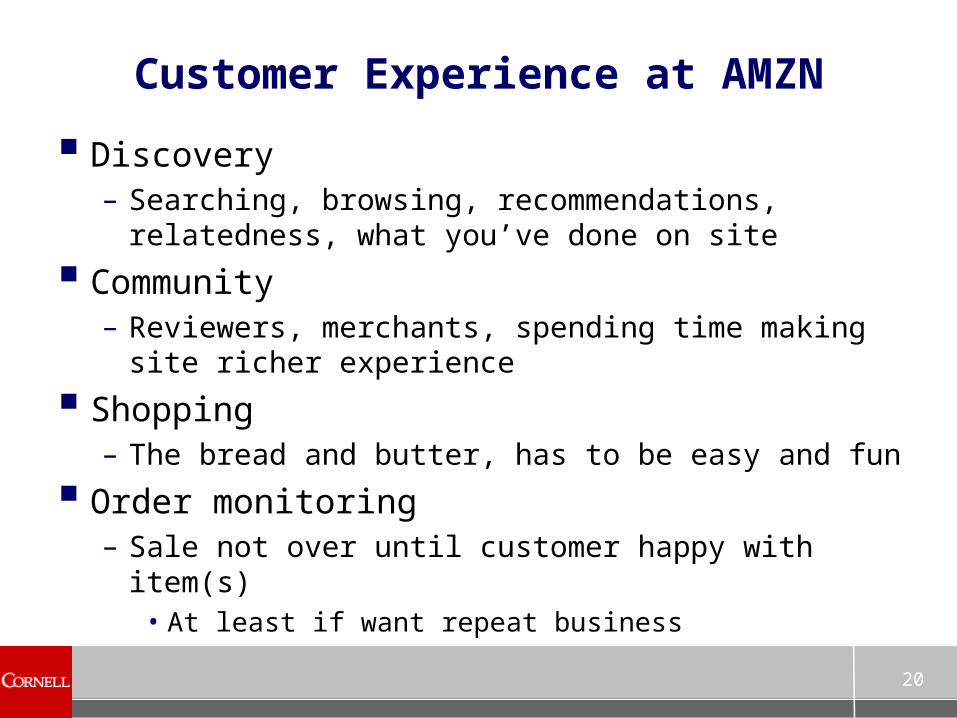

Customer Experience at AMZN

Discovery– Searching, browsing, recommendations,

relatedness, what you’ve done on site

Community– Reviewers, merchants, spending time making

site richer experience

Shopping– The bread and butter, has to be easy and fun

Order monitoring– Sale not over until customer happy with item(s)

• At least if want repeat business

21

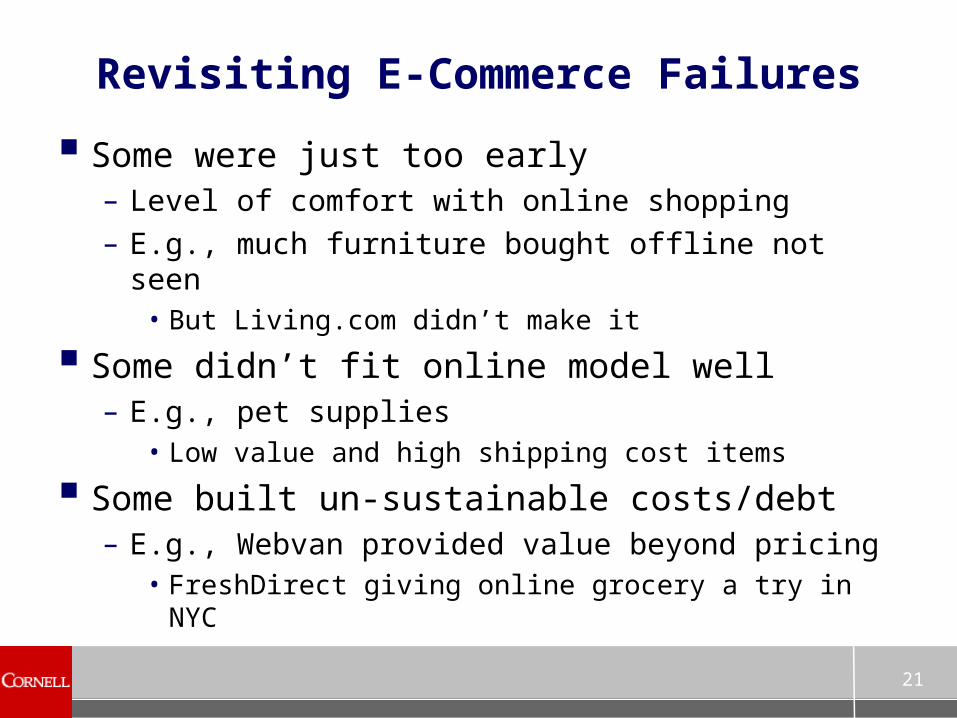

Revisiting E-Commerce Failures

Some were just too early– Level of comfort with online shopping– E.g., much furniture bought offline not seen

• But Living.com didn’t make it

Some didn’t fit online model well– E.g., pet supplies

• Low value and high shipping cost items

Some built un-sustainable costs/debt– E.g., Webvan provided value beyond pricing

• FreshDirect giving online grocery a try in NYC

22

FreshDirect Online Grocer

Focus is on the food– Modeled on Dell: provide great choice and use

Internet to deliver it• With new manufacturing process

Better quality and selection of fresh foods– Prices 10-30% lower than Manhattan stores– Fixed $3.95 delivery fee, minimum $40 order

• Deliver only at night and on weekends

Direct from warehouse to customer– Many items prepared in the warehouse

Raised $120M; goal $225M/yr sales by ’04

23

Summary

Importance of user experience on brand– Requires commitment across the company– Requires common site design, navigation

• But content needs to be accurate, so best under control of individual business group/team

Selection and convenience are big drivers of online commerce– Price secondary focus for successful firms– Perhaps getting less important for consumers

Online community plays role too