nestle india - company update-jun-15-edel - myirisbreport.myiris.com/es1/nesindia_20150602.pdf ·...

TRANSCRIPT

Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset. Edelweiss Securities Limited

Nestle India’s (Nestle) flagship brand Maggi has landed in a soup. It has come under the scanner of many state regulators for excessive lead and MSG content. As per our channel checks, post the brouhaha, Maggi sales have nosedived. Further, while Kerala has banned its sale, Delhi is mulling action due to negative test reports (samples contained lead). The prepared dishes segment (of which Maggi Noodles forms bulk) contributes ~30% to Nestle’s revenue. We cut CY15E and CY16E EPS 18.2% and 19.5% YoY, respectively, and expect the stock to de‐rate, further aggravated by an anticipated deficient monsoon. Hence, we downgrade to ‘REDUCE’.

Maggi volumes, margins to tumble on content rumble The prepared dishes segment has been the fastest growing segment for Nestle over

the past few years. We expect Maggi’s volumes to come under pressure in coming

quarters. As per news channels, the Future Group has stopped Maggi sales in its stores.

In a bid to revive the brand, the company will have to invest heavily to communicate

that its products are safe (similar to what Cadbury did in 2003). Legal costs/promotions

will also inch up, which will take a toll on margin.

Damage control drive to divert premiumisation focus Nestle’s effort towards driving premiumisation and improving the overall growth

trajectory may take a hit because of change in focus to damage control and revive the

Maggi brand. Also, during this phase, the brand may lose market share to rivals (ITC’s

Yippee noodles), adding further fuel to fire.

Outlook and valuations: Challenging; downgrade to ‘REDUCE’ Nestle’s volumes will come under pressure due to the negative brand perception on

Maggi. Moreover, apart from the brand, the issue could impact the company’s other

offerings as well. With the stock at 45.8x CY16 P/E, we downgrade

recommendation/rating to ‘REDUCE/SU’ from ‘HOLD/SP’ with a revised target price of

INR5,641.

COMPANY UPDATE

NESTLE INDIA Maggi muddle: Noodles land in content soup

EDELWEISS 4D RATINGS

Absolute Rating REDUCE

Rating Relative to Sector Underperformer

Risk Rating Relative to Sector Low

Sector Relative to Market Underweight

MARKET DATA (R: NEST.BO, B: NEST IN)

CMP : INR 6,803

Target Price : INR 5,641

52‐week range (INR) : 7,505 / 4,755

Share in issue (mn) : 96.4

M cap (INR bn/USD mn) : 656 / 10,271

Avg. Daily Vol.BSE/NSE(‘000) : 29.5 SHARE HOLDING PATTERN (%)

Current Q3FY15 Q2FY15

Promoters *

62.8 62.8 62.8

MF's, FI's & BK’s 4.5 4.7 4.8

FII's 12.5 13.8 14.3

Others 20.2 18.7 18.1

* Promoters pledged shares (% of share in issue)

: NIL

PRICE PERFORMANCE (%)

Stock Nifty

EW Consumer goods Index

1 month 1.5 3.1 4.2

3 months (5.0) (5.3) (2.6)

12 months 34.5 16.6 17.6

Abneesh Roy +91 22 6620 3141

Pooja Lath +91 22 6620 3075

Tanmay Sharma +91 22 4040 7586

India Equity Research| Consumer Goods

June 2, 2015

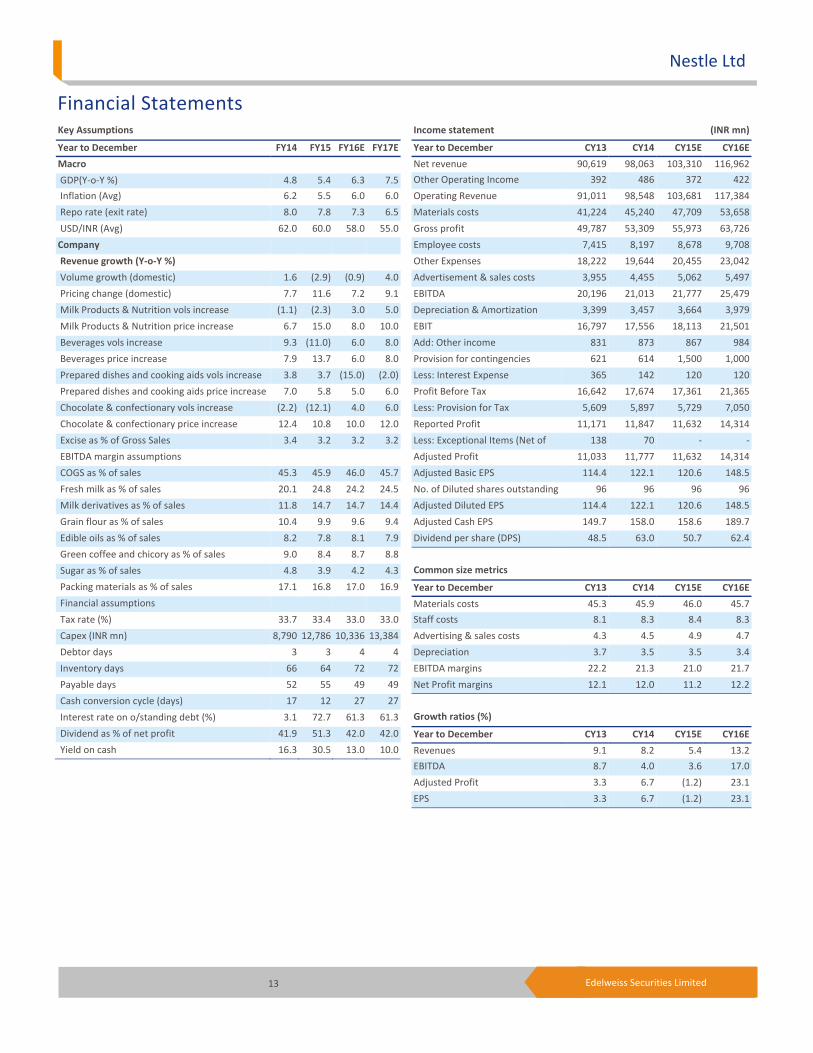

Financials

Year to December CY13 CY14 CY15E CY16E

Revenues (INR mn) 90,619 98,063 103,310 116,962

Rev. growth (%) 9.1 8.2 5.4 13.2

EBITDA (INR mn) 20,196 21,013 21,777 25,479

Adjusted Profit (INR mn) 11,033 11,777 11,632 14,314

No. of Shares outstanding (mn) 96 96 96 96

Adjusted Diluted EPS (INR) 114.4 122.1 120.6 148.5

EPS growth (%) 3.3 6.7 (1.2) 23.1

Diluted P/E (x) 59.5 55.7 56.4 45.8

EV/EBITDA (x) 32.4 30.8 29.5 25.0

ROAE (%) 53.0 45.2 37.1 37.7

Consumer Goods

2 Edelweiss Securities Limited

Uttar Pradesh started the fire

The brouhaha began in Uttar Pradesh when the state’s Food Safety and Drug Administration

(FDA) found higher‐than‐permissible lead and monosodium glutamate (MSG) content in

some packets of Maggi. Following the report, the food regulator asked Nestle to recall

~200000 packets of Maggi, which it believed were not safe for consumption.

Endemic becoming epidemic….

The problem was compounded further as other state government’s too started probing into

the issue and ordered sample testing. Consequently, FSSAI has collected samples from most

states of India which will be tested on all parameters. Moreover, the news has gone viral on

social media and television, denting the brand value to a great extent.

Table 1: Action taken by different state government till now

Source: Edelweiss research

Nestle take

Nestle has released a press statement in which it has denied the news about its product

containing lead or MSG more than the prescribed limit. To validate its statement, the

company has sent its samples for testing to an independent accredited laboratory.

Nestle’s comments on the issue:

“The company does not agree with the order and is filing the requisite representation with

the authorities. People can be confident that Maggi Noodle products are safe to eat.”

“We have in place strict food safety and quality controls at our Maggi factories, including

through quality check at each stage of our raw material sourcing and manufacturing

process.”

“We have submitted samples of Maggi Noodles from almost 600 product batches to an

external laboratory for independent analysis and we tested samples from almost 1000

batches at our accredited laboratory. These samples represent around 125mn packets.”

“All the results of these internal and external tests show that lead levels are well within the

limits specified by food regulations and that Maggi noodles are safe to eat. “

State Action taken

Uttar Pradesh Filed a criminal case against Nestle India after Maggi samples contained excess lead content

Uttarakhand and UP Served notice to Bollywood actors Amitabh Bachchan, Madhuri Dixit and Priety Zinda as they

have featured in Maggi ads

Delhi Possible ban in Delhi as Maggi samples were found to be unsafe for consumption

Kerala Has issued orders to ban sale of Maggi instant noodles in the Kerala state outlets

Bihar Filed FIR against those actors who have promoted Maggi

Karnataka Has sent Maggi samples for testing in an independent lab

Harayana Has sent Maggi samples for testing

Maharashtra Has sent Maggi samples for testing

West Bengal Awaiting results of the samples sent for testing (convened a high‐level meeting)

Goa FDA found no ingredient above the harmful levels

Tamil Nadu Ordered lab test of Maggi

Himachal Pradesh Ordered lab test of Maggi

Andhra Pradesh and Telengana Collected 22 random samples from different batches of Maggi and sent for lab testing

Nestle Ltd

3 Edelweiss Securities Limited

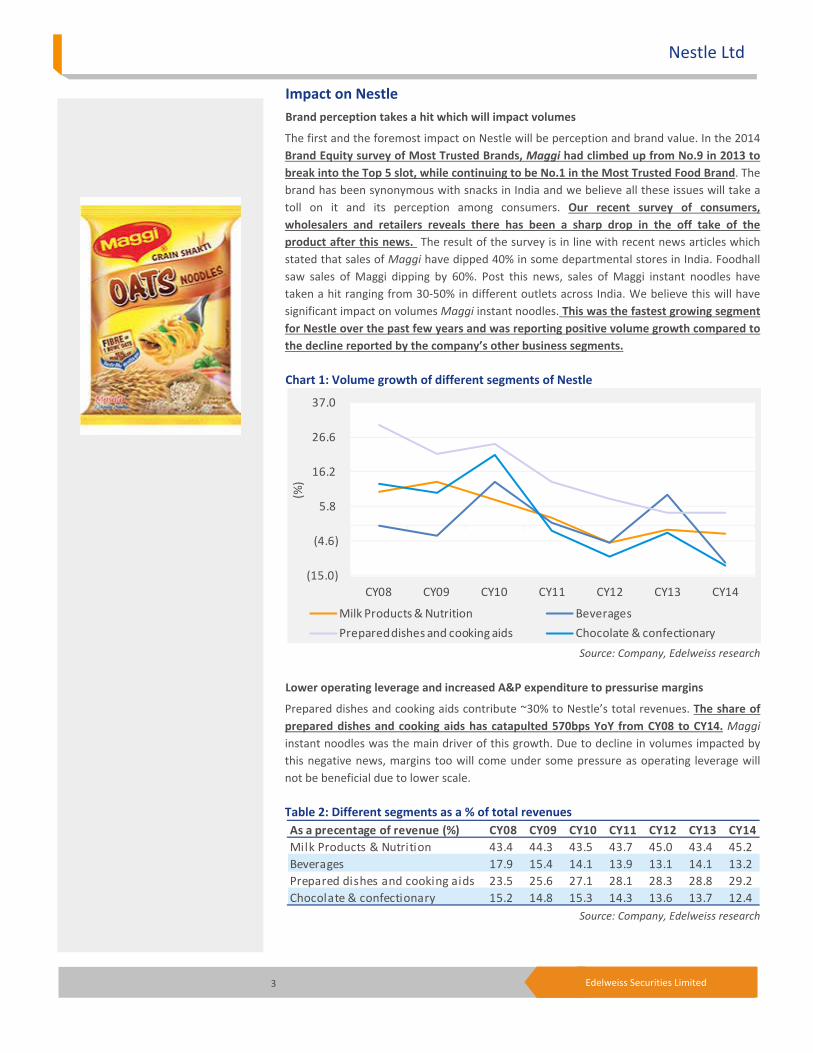

Impact on Nestle

Brand perception takes a hit which will impact volumes

The first and the foremost impact on Nestle will be perception and brand value. In the 2014

Brand Equity survey of Most Trusted Brands, Maggi had climbed up from No.9 in 2013 to

break into the Top 5 slot, while continuing to be No.1 in the Most Trusted Food Brand. The

brand has been synonymous with snacks in India and we believe all these issues will take a

toll on it and its perception among consumers. Our recent survey of consumers,

wholesalers and retailers reveals there has been a sharp drop in the off take of the

product after this news. The result of the survey is in line with recent news articles which

stated that sales of Maggi have dipped 40% in some departmental stores in India. Foodhall

saw sales of Maggi dipping by 60%. Post this news, sales of Maggi instant noodles have

taken a hit ranging from 30‐50% in different outlets across India. We believe this will have

significant impact on volumes Maggi instant noodles. This was the fastest growing segment

for Nestle over the past few years and was reporting positive volume growth compared to

the decline reported by the company’s other business segments.

Chart 1: Volume growth of different segments of Nestle

Source: Company, Edelweiss research

Lower operating leverage and increased A&P expenditure to pressurise margins

Prepared dishes and cooking aids contribute ~30% to Nestle’s total revenues. The share of

prepared dishes and cooking aids has catapulted 570bps YoY from CY08 to CY14. Maggi

instant noodles was the main driver of this growth. Due to decline in volumes impacted by

this negative news, margins too will come under some pressure as operating leverage will

not be beneficial due to lower scale.

Table 2: Different segments as a % of total revenues

Source: Company, Edelweiss research

(15.0)

(4.6)

5.8

16.2

26.6

37.0

CY08 CY09 CY10 CY11 CY12 CY13 CY14

(%)

Milk Products & Nutrition Beverages

Prepared dishes and cooking aids Chocolate & confectionary

As a precentage of revenue (%) CY08 CY09 CY10 CY11 CY12 CY13 CY14

Milk Products & Nutrition 43.4 44.3 43.5 43.7 45.0 43.4 45.2

Beverages 17.9 15.4 14.1 13.9 13.1 14.1 13.2

Prepared dishes and cooking aids 23.5 25.6 27.1 28.1 28.3 28.8 29.2

Chocolate & confectionary 15.2 14.8 15.3 14.3 13.6 13.7 12.4

Consumer Goods

4 Edelweiss Securities Limited

Over the past few years, the company has invested substantially in the brand, not only for

brand building, but also to expand distribution. The company drove penetration of Maggi in

small and semi urban towns with the communication that was relevant for consumers

therein. To win back the lost goodwill (even if the company comes out clean after the

sample testing), Nestle will have to invest behind the brand by way of advertisements and

promotions again to reiterate the fact the Maggi is safe for consumption. Hence, we

believe that A&P will increase as percentage of sales, which will further impact margins.

Apart from this, the company will see an increase in legal and other expenditure as well,

which may arise due to the litigation filed against the company.

Monsoon also not favouring

The Indian Meteorological Department (IMD), in its second stage forecast of South West

monsoon (June to September), has downgraded its April forecast of 93% Long Period

Average (LPA), which is ‘below normal’, to 88%, which is ‘deficient’. Deficient monsoon will

added fuel to fire as it will lead to an increase in the raw material prices like milk, wheat, rice

etc which will further impact the gross margins of the company. Not only Nestle, but other

food companies, HUL, GSK Consumer, ITC etc., will also bear the brunt.

Table 3: 2015 monsoon expected to be similar to 2014 geographically…

Source: IMD, Edelweiss research

Management bandwidth to get diverted to damage control

Nestle had been a laggard in the past years as it shifted focus on increasing profitability,

which was impacting volume growth. Also, the pace of new launches had dried up. But since

the time Mr. Etienne Benet, the new MD, took over, there has been a marked shift in

Nestle’s strategy. The company is focusing on premiumisation, SKU rationalisation and is

focused on driving growth via a leaner and premium product portfolio. New product

launches gathered pace with the likes of Maggi Oats Noodles, 'NAN LO‐LAC' as the first ever

low lactose formula, Nestlé Kit Kat Senses Milk, Nestlé Kit Kat Senses Dark and Nestlé Extra

Smooth etc. Apart from this, management was also investing behind the brand to drive

volumes. But this news will certainly have a temporary impact on the focus on the

management which will now shift to damage control of one of its most important brand.

This may impact new launches and innovation as well as they may be postponed.

Could potentially impact other brands as well

The recent probe may raise concerns on Nestle’s other brands as well. Apart from the issue

of Maggi, another issue has also come up from Tamil Nadu where a consumer found worms

in Nan Pro 3 Milk powder. This can lead to testing of the company’s other brands as well,

which raises the specter of its other products coming under the scanner. Also, sales of other

products that come under the Maggi mother brand like Maggi Tomato Ketchup, Maggi

healthy soups, Maggi masala e magic too may come under pressure. This will lead to some

market share loss to competitors.

Regions2015 Jun‐Sep (IMD forecast)

(% of long period average

2014 Jun‐Sep (Actual),

(% of long period average)

Country as a whole 88 88

Northwest India 85 79

Central India 90 90

South Peninsula 92 93

North East India 90 88

Nestle Ltd

5 Edelweiss Securities Limited

Table 4: Nestle’s market share strong in different categories

Source: Company, Edelweiss research

How does it affect other food players….

We believe in the short term there is a possibility of market share gain for companies

selling instant noodles, resulting from consumers shifting from Nestle’s Maggi to other

instant noodles brands. ITC is expected to be a key beneficiary from this shift with its

brand Yippee Noodles, which has gained market share from Nestle and also has a strong

distribution network. Other companies selling instant noodles are HUL (Knorr), Top Ramen

noodles from Nissin, among others.

However, over the medium to long term, the Nestle issue will heighten the scrutiny of

other food companies as well, which may bring up new issues. Also, we believe that if

more such issues crop up, overall packed food sales will be impacted. Consumers may cut

down consumption of packaged foods for health reasons, which will impact food

companies apart from Nestle like HUL, ITC, GSK Consumer, Agro Tech Foods, Marico,

Britannia, Dabur etc.

Other brands impacted in the past

Cadbury: Sales of Cadbury were impacted in 2003 when a customer found worms in Cadbury's Dairy Milk in Maharashtra. To build back the lost goodwill, the company had to

invest significantly in the brand. It also improved its packaging facility to ensure hygienic

conditions. It also roped in Bollywoood actor Amitabh Bachchan for the brand and started

advertising strongly.

Cola: Sales of soft drinks were stopped in schools and government offices after tests on 11

products made by Pepsi and CocaCola showed high pesticide levels, up to 24x the

recommended limit. To counter this, cola companies had to invest in the brands and

communicate to customers that the soft drinks were safe for human consumption. They

advertised in news papers and televisions highlighting that they make one of the safest

beverages in the world.

Similar issues came up with McDonald’s, Subway etc., where the companies had to file

litigations and also communicate to customers that their products were safe for

consumption. Taking cue from these cases, we believe Nestle will also have to increase

A&P spends to communicate the safety of its products.

Category Market share (%) Market positionNoodles 80.2 First

Infant Milk Nutrition 41 Second

Infant Milk Cereals 96 First

Tea cream 49.9 First

Instant Coffee 51.8 First

Wafers and whites 68.5 First

Overall chocolate 18.8 Second

Ketchup 26.9 First

Pasta 65.7 First

Consumer Goods

6 Edelweiss Securities Limited

Outlook and valuations: Challenging; downgrade to ’REDUCE’

Nestle’s performance had improved consistently over the past 4 quarters and the company

was on track for course correction. The benign raw material environment helped the

company register multi‐year high gross margins and it is well placed to gain from the

impending urban recovery because of its product portfolio which is well suited to urban

centric consumers. However, the Maggi issue and the widespread counter measures taken

by state governments have raised concerns over the growth path. The Maggi brand has

taken a hit as sales are down 40‐50% post the news. Moreover, Kerala has banned sales of

Maggi and lead was found in samples tested in Delhi, which has raised the specter of a

possible ban there as well.

The prepared dish segment contributes ~30% to the company’s overall revenues and hence

in the light of the recent news we downgrade the stock to ‘REDUCE’ from ‘HOLD’ and rate it

sector ‘Sector Underperformer’. We cut out revenue estimates for CY15 and CY16 by 6.5%

and 8.8% YoY, respectively. Also, there will be margin pressure because of the lower

operating leverage and increased A&P spends to support the brand. We cut EPS for CY15E

and CY16E 18.2% YoY and 19.5% YoY, respectively to arrive at EPS of INR120.6 and INR148.5

for CY15E and CY16E, respectively. We cut our target multiple to 38x CY16E to arrive at a

target price of INR5,641.

Chart 2: 1 year forward PE

Source: Edelweiss research

2,000

3,200

4,400

5,600

6,800

8,000

Jun‐10

Dec‐10

Jun‐11

Dec‐11

Jun‐12

Dec‐12

Jun‐13

Dec‐13

Jun‐14

Dec‐14

Jun‐15

(INR)

55x

30x

35x

45x

40x

50x

30x

35x

45x

40x

50x

Nestle Ltd

7 Edelweiss Securities Limited

Table 5: Segmental performance

Table 6: Segmental performance

Table 7: Overall volume growth

Source: Company, Edelweiss research

Q1CY13 Q2CY13 Q3CY13 Q4CY13 Q1CY14 Q2CY14 Q3CY14 Q4CY14 Q1CY15

Exports growth(%) 50.9 46.9 73.9 20.9 (4.4) 4.1 (3.9) 17.9 19.2

Net domestic sales growth (%) 7.7 9.2 8.0 3.7 3.4 9.7 9.9 11.3 7.6

Net sales growth (%) 9.8 11.4 11.0 4.6 2.9 9.3 8.9 11.7 8.4

Gross margin (%) 55.0 55.0 55.2 53.6 53.9 52.7 54.1 55.7 57.8

EBITDA margin(%) 23.9 22.4 21.4 21.1 21.3 20.6 21.3 22.1 24.2

Tax Rate 35.1 33.0 33.5 33.2 34.6 32.4 32.6 33.8 34.2

Other Expenses 23.5 24.2 25.7 24.4 24.8 23.5 24.7 25.0 24.9

COGS (% of Sales) 45.0 45.0 44.8 46.4 46.1 47.3 45.9 44.3 42.2

CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11 CY12 CY13 CY14

Milk Products & Nutrition

Volume growth (% YoY) 7.4 2.7 2.9 5.4 10.1 13.1 7.6 2.5 (5.1) (1.1) (2.3)

Price growth (% YoY) 1.6 6.1 6.3 16.3 11.7 5.4 11.6 17.8 21.4 6.7 15.0

Beverages

Volume growth (% YoY) (4.0) (1.6) (9.2) 7.9 0.0 (3.1) 13.2 0.9 (5.0) 9.3 (11.0)

Price growth (% YoY) 0.8 12.1 14.4 10.6 10.9 3.6 (1.2) 17.8 10.6 7.9 13.7

Prepared dishes and cooking aids

Volume growth (% YoY) 3.8 8.5 20.0 24.8 30.1 21.7 24.4 13.2 8.0 3.8 3.7

Price growth (% YoY) (1.0) 9.9 (0.7) 4.6 3.5 4.3 3.9 10.3 4.4 7.0 5.8

Chocolate & confectionary

Volume growth (% YoY) 9.9 11.3 15.8 17.6 12.4 9.7 21.2 (1.5) (9.4) (2.2) (72.5)

Price growth (% YoY) (6.3) (0.3) 2.3 6.1 6.3 3.5 4.3 14.4 17.3 12.4 253.8

Period Volume growth (% YoY)

CY14 (0.6)

CY13 1.9

CY12 0.8

CY11 6.8

CY10 17.0

CY09 14.9

CY08 16.9

CY07 13.8

CY06 8.3

CY05 4.9

CY04 5.1

CY03 10.2

Consumer Goods

8 Edelweiss Securities Limited

Nestle India 2014 Annual report | Key takeaways

Nestle India: Nutrition, Health and Wellness

Financials

Net sales jumped 8.2% YoY to INR98bn.

Overall volumes declined 0.6% YoY in CY14.

Net domestic sales grew 8.6% YoY primarily due to better realisations.

Export sales, at INR6,442mn, rose 2.9% YoY impacted by coffee exports to Russia.

Export of culinary products saw some uptick in major markets and the company

expects this to continue.

Exports of instant tea slowed down, in Europe as well as in the Far East. Instant coffee

exports also dropped due to lower imports by the affiliate in Russia.

Total dividend paid during CY14 was INR63.0 per share compared to INR48.5 per share

in CY13.

Prepared Dishes and Cooking Aids

In 2014 Brand Equity survey of Most Trusted Brands, Maggi climbed up from No.9 in

2013 to break into the Top 5, while continuing to be the No.1 Most Trusted Food Brand.

Nestle maintained its leadership and improved volumes.

During CY14, the company launched Maggi Oats Noodles with the goodness of grains

(Grain Shakti) to enter the breakfast segment with an enjoyable and healthy offering

for the family.

Nestle drove penetration of Maggi in small, semi urban towns with communication

that was relevant for those consumers, while in the sauces category the company

recruited new consumers to drive growth with Maggi Pichkoo.

While volumes jumped 3.7% YoY, sales stood at INR29bn (up 9.7% YoY).

Milk Products and Nutrition

Nestlé works with over 100,000 milk farmers.

The company launched Nestlé Masala Buttermilk which has the goodness of Ayurveda

and the company is working with Nestlé R&D and application groups to develop more

products.

Nestle is putting lot of resources behind the campaign 'Superbaby‐When breastfed it

shows'. It is important to encourage advocacy around the cause and make

breastfeeding a part of community knowledge and practice. Resultantly, Nestle

develops products that provide mothers with balanced nutrition when she is pregnant

or feeding her child.

Nestle launched 'NAN LO‐LAC' as the first ever low lactose formula in India for

nutritional management of diarrhea.

The company also test launched Nestlé Buttermilk and Nestlé Lassi in Delhi to assess

the market in the liquid refreshment section.

Volumes declined 2.29% YoY while sales stood at INR45.7bn (up 12.4% YoY).

Nestle Ltd

9 Edelweiss Securities Limited

Chocolate and Confectionery

Nestle is the leader in the lighter eating segment with wafer‐based products such as

Kitkat and Munch and in whites with Milkybar which has the goodness of milk.

Nestle India has stopped using artificial colours in the chocolate and confectionery

portfolio since 2012.

The growth of the industry decelerated while commodity and packaging prices

increased.

The company with focus on premiumising introduced 'Slow Churned Chocolate' for the

first time in India under Nestlé Kit kat Senses Milk, Nestlé Maggi Dark and Nestlé Extra

Smooth.

Nestlé Polo, the iconic 'Mint with the Hole', was re‐launched with menthol crystals and

attractive new packaging.

Nestlé Milkybar, which continues to be the leader in 'whites', was renovated and

relaunched with an innovative concept of 'play eat & learn' to create more value.

Volumes declined 12% YoY while sales stood at INR12.5mn (down 2.58% YoY).

Coffee and Beverages

Brand Equity's Most Trusted Brands survey for 2014 ranked Nescafe in the top 5 Hot

Beverage brands and the 100 Most Trusted Brands of the country.

The good communication strategy led to volume and value growth and market share

gains in Nescafe.

Performance of Nestea was satisfactory in CY14.

Volumes declined 10.9% YoY while sales stood at INR13.4bn (grew 1.19% YoY).

Nestle Professional

CY14 was a challenging year for this business.

Beverages vending solutions category was adversely impacted by surge in milk prices at

the start of CY14, but focus on cost control and execution of an enhanced strategy

enabled it to end the year stronger.

Nestle remains committed to consolidate and build further on its strengths in the out‐

of‐home industry.

Distribution and supply chain

The focus in CY14 was to improve availability in a sustained manner in secondary and

tertiary towns.

Nestle has invested in improving sales automation systems to enhance productivity of

its sales force.

The company has implemented a system to streamline milk collection to directly pay

farmers who supply milk to the Moga factory.

Chairman’s and MD’s messages: Key highlights

Indian economy faces 2 main concerns—food security and nutrition.

Consumer Goods

10 Edelweiss Securities Limited

Food processing and technology can reduce or completely eliminate the wastage of

agricultural produce in India, which is estimated to be over INR500bn every year.

Nestle's vision is to become a leader of Nutrition, Health and Wellness in India.

To achieve this, the company will need bold changes, swift adaptation and tough

decisions, especially for evolving a product portfolio that is more focused on premium

and value‐up ranges.

Using state‐of‐the‐art facility, the company has reduced water consumption per tonne

of production by 72% in the past 15 years.

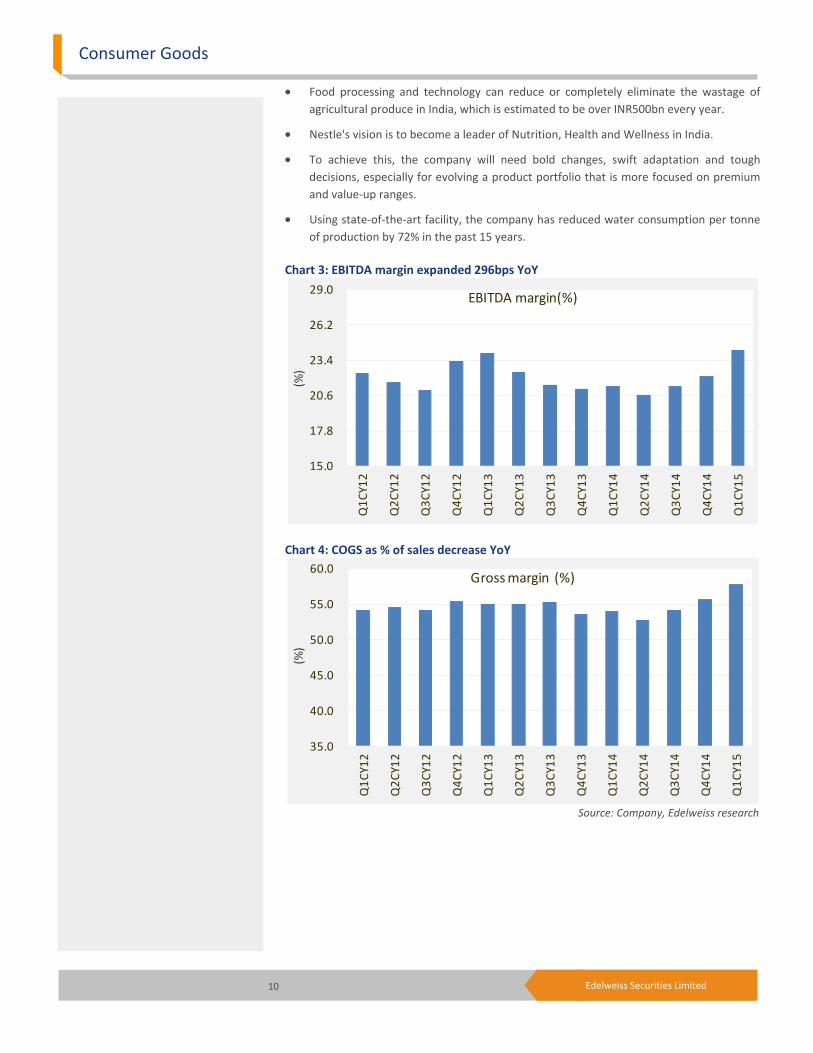

Chart 3: EBITDA margin expanded 296bps YoY

Chart 4: COGS as % of sales decrease YoY

Source: Company, Edelweiss research

15.0

17.8

20.6

23.4

26.2

29.0

Q1CY12

Q2CY12

Q3CY12

Q4CY12

Q1CY13

Q2CY13

Q3CY13

Q4CY13

Q1CY14

Q2CY14

Q3CY14

Q4CY14

Q1CY15

(%)

EBITDA margin(%)

35.0

40.0

45.0

50.0

55.0

60.0

Q1CY12

Q2CY12

Q3CY12

Q4CY12

Q1CY13

Q2CY13

Q3CY13

Q4CY13

Q1CY14

Q2CY14

Q3CY14

Q4CY14

Q1CY15

(%)

Gross margin (%)

Nestle Ltd

11 Edelweiss Securities Limited

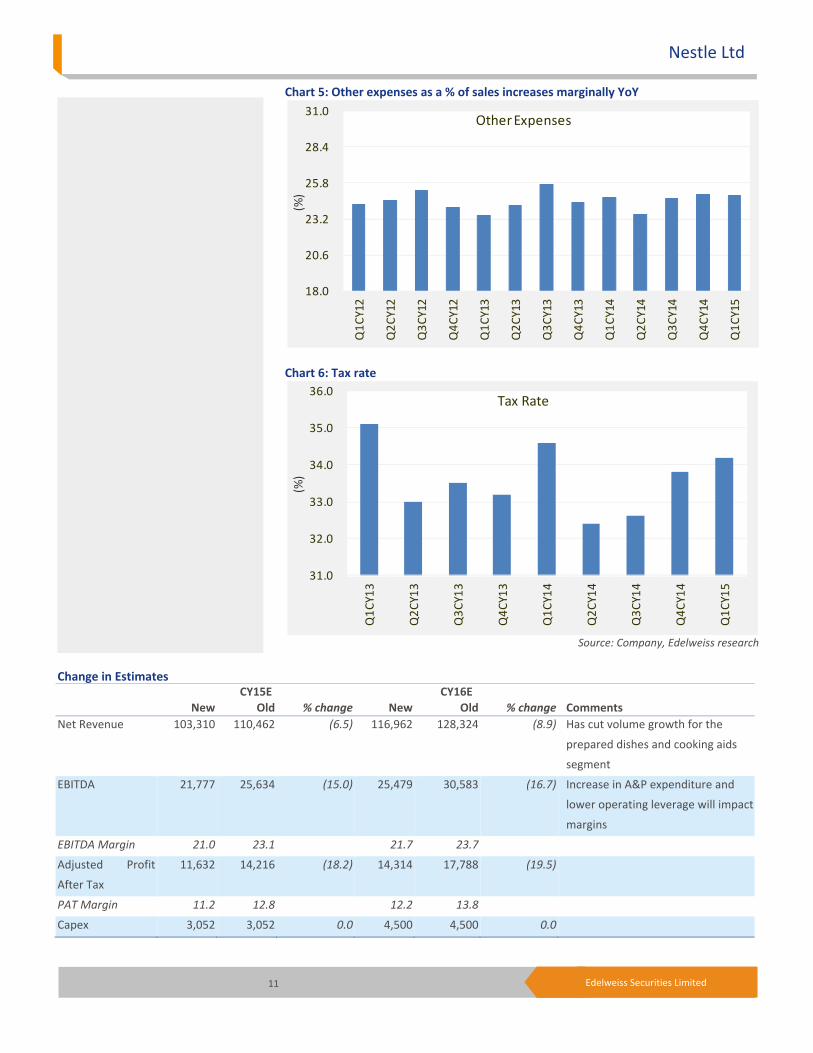

Chart 5: Other expenses as a % of sales increases marginally YoY

Chart 6: Tax rate

Source: Company, Edelweiss research

18.0

20.6

23.2

25.8

28.4

31.0

Q1CY12

Q2CY12

Q3CY12

Q4CY12

Q1CY13

Q2CY13

Q3CY13

Q4CY13

Q1CY14

Q2CY14

Q3CY14

Q4CY14

Q1CY15

(%)

Other Expenses

31.0

32.0

33.0

34.0

35.0

36.0

Q1CY13

Q2CY13

Q3CY13

Q4CY13

Q1CY14

Q2CY14

Q3CY14

Q4CY14

Q1CY15

(%)

Tax Rate

Change in Estimates CY15E CY16E

New Old % change New Old % change Comments

Net Revenue 103,310 110,462 (6.5) 116,962 128,324 (8.9) Has cut volume growth for the

prepared dishes and cooking aids

segment

EBITDA 21,777 25,634 (15.0) 25,479 30,583 (16.7) Increase in A&P expenditure and

lower operating leverage will impact

margins

EBITDA Margin 21.0 23.1 21.7 23.7

Adjusted Profit

After Tax

11,632 14,216 (18.2) 14,314 17,788 (19.5)

PAT Margin 11.2 12.8 12.2 13.8

Capex 3,052 3,052 0.0 4,500 4,500 0.0

Consumer Goods

12 Edelweiss Securities Limited

Company Description

Nestle, a 62.8% subsidiary of its parent Nestlé S.A. of Switzerland, is India’s third largest

FMCG company after HUL and ITC. The company set up its first factory at Moga, Punjab, to

develop milk production. Over the years, Nestlé has set up seven factories across the

country, and is now involved in manufacturing and marketing a range of quality products. It

has well‐established brands, including Maggi, Nescafe, Lactogen, KitKat, and Milkmaid.

Nestlé enjoys leadership position in its core categories like baby foods, instant noodles, and

instant coffee. It enjoys a distinct advantage over competitors in the F&B space on account

of its strong focus on developing products around the nutrition, health, and wellness

platform, and a culture of renovation and innovation in its offerings, backed by strong

parent support.

Investment Theme

Nestle India (Nestle) is the best play on Indian processed food industry, which is on a high

growth trajectory with multiple growth drivers in place, including low penetration levels,

rising income levels, urbanisation, and changing lifestyle. Nestlé with established brands

across food categories is expected to be a major beneficiary of this growth. Nestle is

increasingly focusing to expand into tier II and tier III cities by introducing stock‐keeping

units (SKUs) below INR 10. Also, company has effectively leveraged its recent

innovations/renovation positioned on health and wellness platform to gain incremental

sales. Nestle’s high pricing power on account of strong brand equity shall aid in fighting

margin pressure despite inflationary concern. Low volume growth in the past couple of

quarters is a cause of concern.

Key Risks

Sharp increase in input costs

Sharp rise in the prices of its key inputs such as milk, wheat flour, edible oils, and sugar

could impact margins adversely.

Competition from new entrants

GSK Consumer, ITC and HUL entered the noodles category in select markets and this could

increase the ad spend for Nestlé. Nestlé also faces competition from dairy cooperatives like

Amul and Mother Dairy, which have low focus on maintaining profit margins. Increase in

competition could also limit Nestlé’s ability to pass on input price hikes to consumers.

Failure of new product launches

Nestlé has launched premium variants in various categories such as chocolates, noodles,

ketchup, and dairy products, which could hit margins, in case they do not click in the

market.

13 Edelweiss Securities Limited

Nestle Ltd

Financial Statements

Income statement (INR mn)

Year to December CY13 CY14 CY15E CY16E

Net revenue 90,619 98,063 103,310 116,962

Other Operating Income 392 486 372 422

Operating Revenue 91,011 98,548 103,681 117,384

Materials costs 41,224 45,240 47,709 53,658

Gross profit 49,787 53,309 55,973 63,726

Employee costs 7,415 8,197 8,678 9,708

Other Expenses 18,222 19,644 20,455 23,042

Advertisement & sales costs 3,955 4,455 5,062 5,497

EBITDA 20,196 21,013 21,777 25,479

Depreciation & Amortization 3,399 3,457 3,664 3,979

EBIT 16,797 17,556 18,113 21,501

Add: Other income 831 873 867 984

Provision for contingencies 621 614 1,500 1,000

Less: Interest Expense 365 142 120 120

Profit Before Tax 16,642 17,674 17,361 21,365

Less: Provision for Tax 5,609 5,897 5,729 7,050

Reported Profit 11,171 11,847 11,632 14,314

Less: Exceptional Items (Net of 138 70 ‐ ‐

Adjusted Profit 11,033 11,777 11,632 14,314

Adjusted Basic EPS 114.4 122.1 120.6 148.5

No. of Diluted shares outstanding 96 96 96 96

Adjusted Diluted EPS 114.4 122.1 120.6 148.5

Adjusted Cash EPS 149.7 158.0 158.6 189.7

Dividend per share (DPS) 48.5 63.0 50.7 62.4

Common size metrics

Year to December CY13 CY14 CY15E CY16E

Materials costs 45.3 45.9 46.0 45.7

Staff costs 8.1 8.3 8.4 8.3

Advertising & sales costs 4.3 4.5 4.9 4.7

Depreciation 3.7 3.5 3.5 3.4

EBITDA margins 22.2 21.3 21.0 21.7

Net Profit margins 12.1 12.0 11.2 12.2

Growth ratios (%)

Year to December CY13 CY14 CY15E CY16E

Revenues 9.1 8.2 5.4 13.2

EBITDA 8.7 4.0 3.6 17.0

Adjusted Profit 3.3 6.7 (1.2) 23.1

EPS 3.3 6.7 (1.2) 23.1

Key Assumptions

Year to December FY14 FY15 FY16E FY17E

Macro

GDP(Y‐o‐Y %) 4.8 5.4 6.3 7.5

Inflation (Avg) 6.2 5.5 6.0 6.0

Repo rate (exit rate) 8.0 7.8 7.3 6.5

USD/INR (Avg) 62.0 60.0 58.0 55.0

Company

Revenue growth (Y‐o‐Y %)

Volume growth (domestic) 1.6 (2.9) (0.9) 4.0

Pricing change (domestic) 7.7 11.6 7.2 9.1

Milk Products & Nutrition vols increase (1.1) (2.3) 3.0 5.0

Milk Products & Nutrition price increase 6.7 15.0 8.0 10.0

Beverages vols increase 9.3 (11.0) 6.0 8.0

Beverages price increase 7.9 13.7 6.0 8.0

Prepared dishes and cooking aids vols increase 3.8 3.7 (15.0) (2.0)

Prepared dishes and cooking aids price increase 7.0 5.8 5.0 6.0

Chocolate & confectionary vols increase (2.2) (12.1) 4.0 6.0

Chocolate & confectionary price increase 12.4 10.8 10.0 12.0

Excise as % of Gross Sales 3.4 3.2 3.2 3.2

EBITDA margin assumptions

COGS as % of sales 45.3 45.9 46.0 45.7

Fresh milk as % of sales 20.1 24.8 24.2 24.5

Milk derivatives as % of sales 11.8 14.7 14.7 14.4

Grain flour as % of sales 10.4 9.9 9.6 9.4

Edible oils as % of sales 8.2 7.8 8.1 7.9

Green coffee and chicory as % of sales 9.0 8.4 8.7 8.8

Sugar as % of sales 4.8 3.9 4.2 4.3

Packing materials as % of sales 17.1 16.8 17.0 16.9

Financial assumptions

Tax rate (%) 33.7 33.4 33.0 33.0

Capex (INR mn) 8,790 12,786 10,336 13,384

Debtor days 3 3 4 4

Inventory days 66 64 72 72

Payable days 52 55 49 49

Cash conversion cycle (days) 17 12 27 27

Interest rate on o/standing debt (%) 3.1 72.7 61.3 61.3

Dividend as % of net profit 41.9 51.3 42.0 42.0

Yield on cash 16.3 30.5 13.0 10.0

14 Edelweiss Securities Limited

Consumer Goods

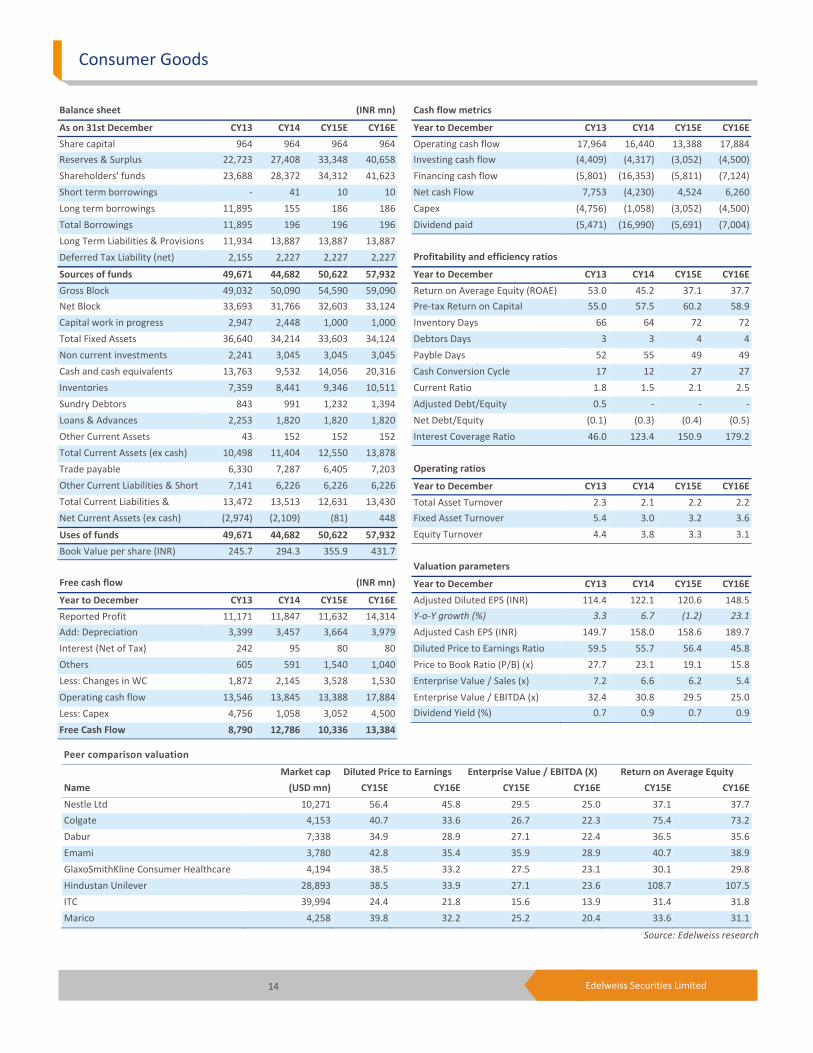

Peer comparison valuation

Market cap Diluted Price to Earnings Enterprise Value / EBITDA (X) Return on Average Equity

Name (USD mn) CY15E CY16E CY15E CY16E CY15E CY16E

Nestle Ltd 10,271 56.4 45.8 29.5 25.0 37.1 37.7

Colgate 4,153 40.7 33.6 26.7 22.3 75.4 73.2

Dabur 7,338 34.9 28.9 27.1 22.4 36.5 35.6

Emami 3,780 42.8 35.4 35.9 28.9 40.7 38.9

GlaxoSmithKline Consumer Healthcare 4,194 38.5 33.2 27.5 23.1 30.1 29.8

Hindustan Unilever 28,893 38.5 33.9 27.1 23.6 108.7 107.5

ITC 39,994 24.4 21.8 15.6 13.9 31.4 31.8

Marico 4,258 39.8 32.2 25.2 20.4 33.6 31.1

Source: Edelweiss research

Cash flow metrics

Year to December CY13 CY14 CY15E CY16E

Operating cash flow 17,964 16,440 13,388 17,884

Investing cash flow (4,409) (4,317) (3,052) (4,500)

Financing cash flow (5,801) (16,353) (5,811) (7,124)

Net cash Flow 7,753 (4,230) 4,524 6,260

Capex (4,756) (1,058) (3,052) (4,500)

Dividend paid (5,471) (16,990) (5,691) (7,004)

Profitability and efficiency ratios

Year to December CY13 CY14 CY15E CY16E

Return on Average Equity (ROAE) 53.0 45.2 37.1 37.7

Pre‐tax Return on Capital 55.0 57.5 60.2 58.9

Inventory Days 66 64 72 72

Debtors Days 3 3 4 4

Payble Days 52 55 49 49

Cash Conversion Cycle 17 12 27 27

Current Ratio 1.8 1.5 2.1 2.5

Adjusted Debt/Equity 0.5 ‐ ‐ ‐

Net Debt/Equity (0.1) (0.3) (0.4) (0.5)

Interest Coverage Ratio 46.0 123.4 150.9 179.2

Operating ratios

Year to December CY13 CY14 CY15E CY16E

Total Asset Turnover 2.3 2.1 2.2 2.2

Fixed Asset Turnover 5.4 3.0 3.2 3.6

Equity Turnover 4.4 3.8 3.3 3.1

Valuation parameters

Year to December CY13 CY14 CY15E CY16E

Adjusted Diluted EPS (INR) 114.4 122.1 120.6 148.5

Y‐o‐Y growth (%) 3.3 6.7 (1.2) 23.1

Adjusted Cash EPS (INR) 149.7 158.0 158.6 189.7

Diluted Price to Earnings Ratio 59.5 55.7 56.4 45.8

Price to Book Ratio (P/B) (x) 27.7 23.1 19.1 15.8

Enterprise Value / Sales (x) 7.2 6.6 6.2 5.4

Enterprise Value / EBITDA (x) 32.4 30.8 29.5 25.0

Dividend Yield (%) 0.7 0.9 0.7 0.9

Balance sheet (INR mn)

As on 31st December CY13 CY14 CY15E CY16E

Share capital 964 964 964 964

Reserves & Surplus 22,723 27,408 33,348 40,658

Shareholders' funds 23,688 28,372 34,312 41,623

Short term borrowings ‐ 41 10 10

Long term borrowings 11,895 155 186 186

Total Borrowings 11,895 196 196 196

Long Term Liabilities & Provisions 11,934 13,887 13,887 13,887

Deferred Tax Liability (net) 2,155 2,227 2,227 2,227

Sources of funds 49,671 44,682 50,622 57,932

Gross Block 49,032 50,090 54,590 59,090

Net Block 33,693 31,766 32,603 33,124

Capital work in progress 2,947 2,448 1,000 1,000

Total Fixed Assets 36,640 34,214 33,603 34,124

Non current investments 2,241 3,045 3,045 3,045

Cash and cash equivalents 13,763 9,532 14,056 20,316

Inventories 7,359 8,441 9,346 10,511

Sundry Debtors 843 991 1,232 1,394

Loans & Advances 2,253 1,820 1,820 1,820

Other Current Assets 43 152 152 152

Total Current Assets (ex cash) 10,498 11,404 12,550 13,878

Trade payable 6,330 7,287 6,405 7,203

Other Current Liabilities & Short 7,141 6,226 6,226 6,226

Total Current Liabilities & 13,472 13,513 12,631 13,430

Net Current Assets (ex cash) (2,974) (2,109) (81) 448

Uses of funds 49,671 44,682 50,622 57,932

Book Value per share (INR) 245.7 294.3 355.9 431.7

Free cash flow (INR mn)

Year to December CY13 CY14 CY15E CY16E

Reported Profit 11,171 11,847 11,632 14,314

Add: Depreciation 3,399 3,457 3,664 3,979

Interest (Net of Tax) 242 95 80 80

Others 605 591 1,540 1,040

Less: Changes in WC 1,872 2,145 3,528 1,530

Operating cash flow 13,546 13,845 13,388 17,884

Less: Capex 4,756 1,058 3,052 4,500

Free Cash Flow 8,790 12,786 10,336 13,384

15 Edelweiss Securities Limited

Nestle Ltd

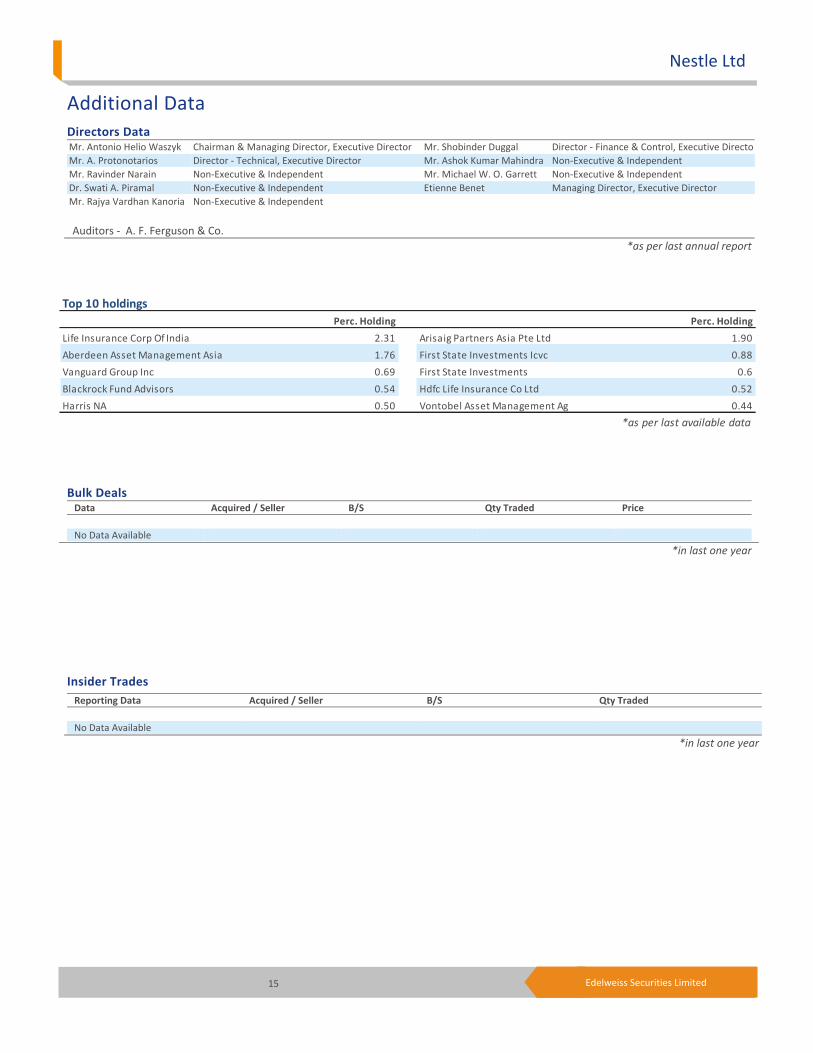

Top 10 holdings

Perc. Holding Perc. Holding

Life Insurance Corp Of India 2.31 Arisaig Partners Asia Pte Ltd 1.90

Aberdeen Asset Management Asia 1.76 First State Investments Icvc 0.88

Vanguard Group Inc 0.69 First State Investments 0.6

Blackrock Fund Advisors 0.54 Hdfc Life Insurance Co Ltd 0.52

Harris NA 0.50 Vontobel Asset Management Ag 0.44

*as per last available data

Insider Trades Reporting Data Acquired / Seller B/S Qty Traded

No Data Available

*in last one year

Bulk Deals Data Acquired / Seller B/S Qty Traded Price

No Data Available

*in last one year

Additional Data

Directors Data Mr. Antonio Helio Waszyk Chairman & Managing Director, Executive Director Mr. Shobinder Duggal Director ‐ Finance & Control, Executive Director

Mr. A. Protonotarios Director ‐ Technical, Executive Director Mr. Ashok Kumar Mahindra Non‐Executive & Independent

Mr. Ravinder Narain Non‐Executive & Independent Mr. Michael W. O. Garrett Non‐Executive & Independent

Dr. Swati A. Piramal Non‐Executive & Independent Etienne Benet Managing Director, Executive Director

Mr. Rajya Vardhan Kanoria Non‐Executive & Independent

Auditors ‐ A. F. Ferguson & Co.

*as per last annual report

16 Edelweiss Securities Limited

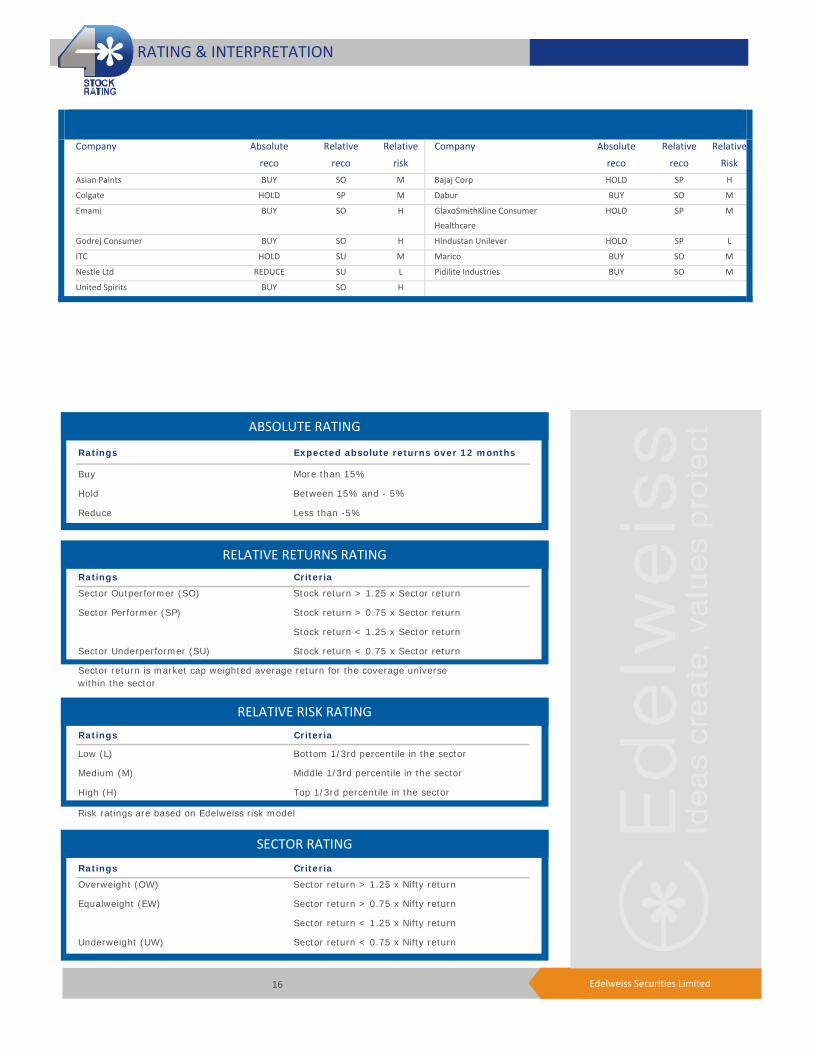

Company Absolute

reco Relative

reco Relative

risk

Company Absolute

reco

Relative

reco

Relative

Risk

Asian Paints BUY SO M Bajaj Corp HOLD SP H

Colgate HOLD SP M Dabur BUY SO M

Emami BUY SO H GlaxoSmithKline Consumer

Healthcare

HOLD SP M

Godrej Consumer BUY SO H Hindustan Unilever HOLD SP L

ITC HOLD SU M Marico BUY SO M

Nestle Ltd REDUCE SU L Pidilite Industries BUY SO M

United Spirits BUY SO H

RATING & INTERPRETATION

ABSOLUTE RATING

Ratings Expected absolute returns over 12 months

Buy More than 15%

Hold Between 15% and - 5%

Reduce Less than -5%

RELATIVE RETURNS RATING

Ratings Criteria

Sector Outperformer (SO) Stock return > 1.25 x Sector return

Sector Performer (SP) Stock return > 0.75 x Sector return

Stock return < 1.25 x Sector return

Sector Underperformer (SU) Stock return < 0.75 x Sector return

Sector return is market cap weighted average return for the coverage universe within the sector

RELATIVE RISK RATING

Ratings Criteria

Low (L) Bottom 1/3rd percentile in the sector

Medium (M) Middle 1/3rd percentile in the sector

High (H) Top 1/3rd percentile in the sector

Risk ratings are based on Edelweiss risk model

SECTOR RATING

Ratings Criteria

Overweight (OW) Sector return > 1.25 x Nifty return

Equalweight (EW) Sector return > 0.75 x Nifty return

Sector return < 1.25 x Nifty return

Underweight (UW) Sector return < 0.75 x Nifty return

17 Edelweiss Securities Limited

Nestle Ltd

Edelweiss Securities Limited, Edelweiss House, off C.S.T. Road, Kalina, Mumbai – 400 098.

Board: (91‐22) 4009 4400, Email: [email protected]

Nirav Sheth

Head Research

Coverage group(s) of stocks by primary analyst(s): Consumer Goods

Asian Paints, Bajaj Corp, Colgate, Dabur, Godrej Consumer , Emami, Hindustan Unilever, ITC, Marico, Nestle Ltd, Pidilite Industries, GlaxoSmithKline Consumer Healthcare, United Spirits

Distribution of Ratings / Market Cap

Edelweiss Research Coverage Universe

Rating Distribution* 155 45 8 208* stocks under review

Market Cap (INR) 151 54 3

Date Company Title Price (INR) Recos

Recent Research

28‐May‐15 Consumer Goods

Staples growth likely bottomed out; Result Review

27‐May‐15 United Spirits

Gross margins cheer, but write offs spoil the party; Result Update

3,501 Buy

22‐May‐15 ITC Volumes skid again; Result Update

329 Hold

> 50bn Between 10bn and 50 bn < 10bn

Buy Hold Reduce Total

Rating Interpretation

Buy appreciate more than 15% over a 12‐month period

Hold appreciate up to 15% over a 12‐month period

Reduce depreciate more than 5% over a 12‐month period

Rating Expected to

One year price chart

3,936

4,927

5,918

6,909

7,900

8,891

Jun‐14

Jul‐14

Aug‐14

Sep‐14

Oct‐14

Nov‐14

Dec‐14

Jan‐15

Feb‐15

Mar‐15

Apr‐15

May‐15

Jun‐15

(INR)

Nestle Ltd

18 Edelweiss Securities Limited

Consumer Goods

DISCLAIMER

This report has been prepared by Edelweiss Securities Limited (“Edelweiss”) and distributed as per Regulation 22(1) of SEBI (Research Analysts) Regulations 2014 having SEBI Registration No.INH200000121 in the capacity of a Research Analyst. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is from publicly available data or other sources believed to be reliable. This report is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors. This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Edelweiss and affiliates/ group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by law, and persons in whose possession this report comes, should observe, any such restrictions. The information given in this report is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. Edelweiss reserves the right to make modifications and alterations to this statement as may be required from time to time. Edelweiss or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Edelweiss is committed to providing independent and transparent recommendation to its clients. Neither Edelweiss nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including loss of revenue or lost profits that may arise from or in connection with the use of the information. Past performance is not necessarily a guide to future performance. The disclosures of interest statements incorporated in this report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The information provided in these reports remains, unless otherwise stated, the copyright of Edelweiss. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of Edelweiss and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

Edelweiss shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the Edelweiss to present the data. In no event shall the Edelweiss be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the Edelweiss through this report.

Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

Additional Disclaimers

Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

19 Edelweiss Securities Limited

Nestle Ltd

Access the entire repository of Edelweiss Research on www.edelresearch.com

In reliance on the exemption from registration provided by Rule 15a‐6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker‐dealer, Edelweiss Financial Services Inc. ("EFSI"). Transactions in securities discussed in this research report should be effected through Edelweiss Financial Services Inc. Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA"). In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report or any of its contents. This research report must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person. Disclaimer for Canadian Persons

This research report is a product of Edelweiss Securities Limited ("ESL"), which is the employer of the research analysts who have prepared the research report. The research analysts preparing the research report are resident outside the Canada and are not associated persons of any Canadian registered adviser and/or dealer and, therefore, the analysts are not subject to supervision by a Canadian registered adviser and/or dealer, and are not required to satisfy the regulatory licensing requirements of the Ontario Securities Commission, other Canadian provincial securities regulators, the Investment Industry Regulatory Organization of Canada and are not required to otherwise comply with Canadian rules or regulations regarding, among other things, the research analysts' business or relationship with a subject company or trading of securities by a research analyst. This report is intended for distribution by ESL only to "Permitted Clients" (as defined in National Instrument 31‐103 ("NI 31‐103")) who are resident in the Province of Ontario, Canada (an "Ontario Permitted Client"). If the recipient of this report is not an Ontario Permitted Client, as specified above, then the recipient should not act upon this report and should return the report to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any Canadian person. ESL is relying on an exemption from the adviser and/or dealer registration requirements under NI 31‐103 available to certain international advisers and/or dealers. Please be advised that (i) ESL is not registered in the Province of Ontario to trade in securities nor is it registered in the Province of Ontario to provide advice with respect to securities; (ii) ESL's head office or principal place of business is located in India; (iii) all or substantially all of ESL's assets may be situated outside of Canada; (iv) there may be difficulty enforcing legal rights against ESL because of the above; and (v) the name and address of the ESL's agent for service of process in the Province of Ontario is: Bamac Services Inc., 181 Bay Street, Suite 2100, Toronto, Ontario M5J 2T3 Canada.

Disclosures under the provisions of SEBI (Research Analysts) Regulations 2014 (Regulations)

Edelweiss Securities Limited (“ESL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository services and related activities. The business of ESL and its associates are organized around five broad business groups – Credit including Housing and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance. There were no instances of non‐compliance by ESL on any matter related to the capital markets, resulting in significant and material disciplinary action during the last three years except that ESL had submitted an offer of settlement with Securities and Exchange commission, USA (SEC) and the same has been accepted by SEC without admitting or denying the findings in relation to their charges of non registration as a broker dealer.

Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved