new guidance for cpas offering personal financial...

TRANSCRIPT

New Guidance for CPAs Offering

Personal Financial Planning

Presented by:

Christine Romsdahl, CPA/PFS

Agenda

• Personal Financial Planning (PFP) Landscape

• Statement on Standards in PFP Services (the Statement, SSPFPS)– Applicability: Covered Services and

Persons

– Responsibilities in the Delivery of PFP Services: select, key provisions

• Q&A

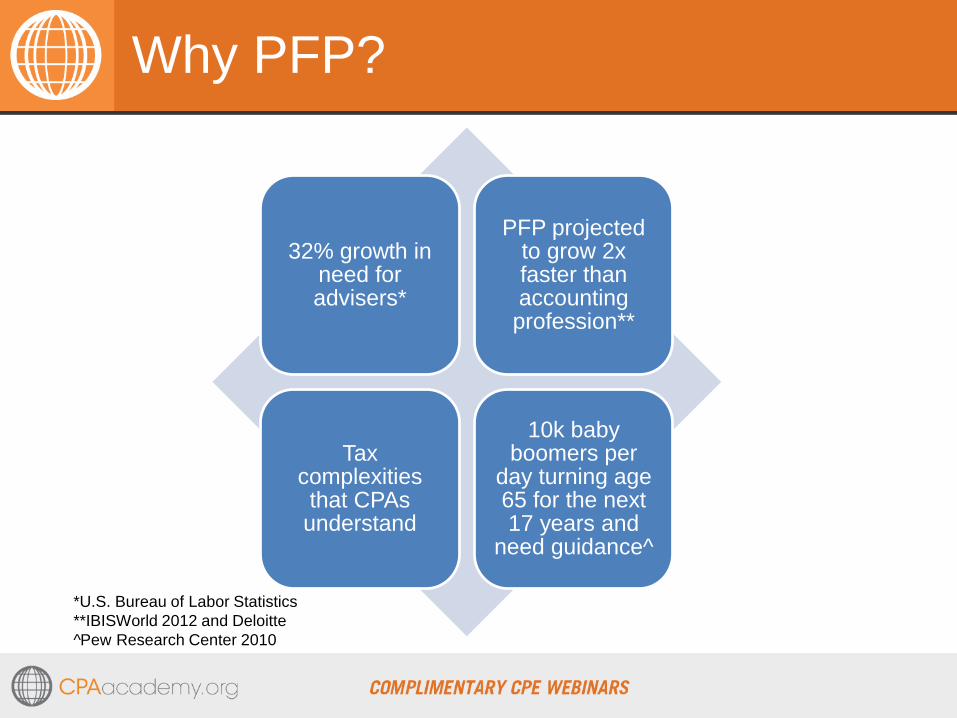

Why PFP?

32% growth in need for advisers*

PFP projected to grow 2x faster than accounting profession**

Tax complexities that CPAs

understand

10k baby boomers per

day turning age 65 for the next 17 years and

need guidance^

*U.S. Bureau of Labor Statistics

**IBISWorld 2012 and Deloitte

^Pew Research Center 2010

How You Can Leverage SSPFPS in Your Practice

• Better define the parameters of your professional responsibilities in PFP

• Use as a framework for effective delivery of PFP services

• Protect your clients’ best interests

• Ensure you have met your professional responsibilities

• Formalize and grow your PFP practice

Formalize and Grow Your PFP Practice

• The Statement provides a roadmap to help you practice competently and confidently.

• The Statement on Standards in PFP Services provides an opportunity to formalize ad hoc PFP related services that add to or increase revenue streams.

• Market yourself as someone who adheres to these personal financial planning standards and Code of Professional Conduct; and that they are integral to your practice.

Are You Subject to the Statement?

PFP Requires a Process … Paragraph 3

• PFP is the process of identifying personal goals and

resources, designing financial strategies and making

personalized recommendations (whether written or oral) that,

when implemented, [are designed to] assist the client in

achieving these goals. This process may include

implementation of recommendations, monitoring or updating

of the engagement.

Cash flow planning

Risk management and

insurance planning

Retirement planning

Investment planning

Estate, gift and wealth

transfer planning

Elder planning

Charitable planning

Education planning

Tax planning

Do you make personalized

recommendations in one

or more of the following

activities?

YES

NO

YES

YES

YES

NO

NO

NO

Do you represent to the public or clients

that you provide PFP services?

Do you engage in activities that would

require registration as an investment

adviser under federal or state law?

Do you sell a product as a result of the

PFP engagement?

The AICPA Statement on Standards in

Personal Financial Planning Services

does not apply. However, the AICPA

Code of Professional Conduct applies.

The AICPA Statement on

Standards in Personal

Financial Planning

Services applies.

When does the Statement apply?

Frequently Asked Questions

• During an interview for income tax preparation, my client asks me about health and elder planning for her elderly parents. I review various alternatives available to the client, including Medicaid and private care facilities, and based upon the information, I suggest a particular strategy. I further recommend that the client discuss the suggested strategy with an attorney and seek implementation by the attorney of a final plan.

Is this activity covered by the Statement?

Frequently Asked Questions

• In addition to providing personal financial planning for clients, I also provide tax planning and compliance work for a number of tax-only clients. During these tax planning engagements, I often run present value computations to determine the impact of various alternatives (for example, depreciation methods, timing of tax deductions between years).

Is this work subject to the Statement?

Frequently Asked Questions

• I perform retirement planning services and refer clients

to insurance brokers who compensate me, sometimes in

cash and other times in noncash compensation.

Am I deemed to be selling a product for purposes of the

Statement?

• I perform estate planning services and send clients to

several attorneys that compensate me for referrals,

sometimes in cash and other times in noncash

compensation.

Am I deemed to be selling a product for purposes of the

Statement?

Requirements of the Statement

The Statement on Standards in PFP Services:

Does …

… establish a process to

maintain an ethical and competent

PFP services practice.

Does not …

… instruct a member on

how to undertake a

personal financial plan.

Key Elements:

• Self Assessment - Ability to Perform the Duties

• Compliance

• Documentation of the PFP engagement

• Communication with the client

• Disclosures

• Use of professional judgment

Responsibilities of Members in PFP Engagements

• Before undertaking a PFP engagement, assess your ability to perform the services in context of the AICPA Code of Professional Conduct:

– Competency (Rule 201)

– Objectivity (Rule 102)

– Integrity

– Disclosure of conflicts of interest

– Privacy and confidentiality

Responsibilities of Members in PFP Engagements

• 19. The member should possess a level of knowledge of personal financial planning principles and theory and a level of skill in the application of such principles that will enable him or her to:

– identify client goals and objectives;

– gather and analyze relevant information;

– consider and apply appropriate planning approaches and methods; and

– use professional judgment in developing financial recommendations

Responsibilities of Members in PFP Engagements

• 20. The member should evaluate whether any conflicts of interest exist with regard to the engagement as follows: – If the member determines conflicts of interest exist, the

member should determine whether the engagement can be performed objectively.

– If the member determines the engagement can be performed objectively, the member should disclose all known conflicts of interest and obtain consent as required under Interpretation No. 102-2, “Conflicts of Interest,” under Rule 102, Integrity and Objectivity (AICPA, Professional Standards, ET sec. 102 par. .03).

– If the member determines that the engagement cannot be performed objectively, the engagement should be terminated.

Responsibilities of Members in PFP Engagements

• 21. The member should comply with applicable federal, state, and other laws and regulations.

The member should comply with professional standards applicable to the PFP engagement unless superseded by laws or regulations.

When there is a conflict between the statement and laws or regulations, the laws or regulations will prevail unless less stringent than the statement.

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

– Timing of the engagement

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

– Timing of the engagement

– Scope limitations and other constraints

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

– Timing of the engagement

– Scope limitations and other constraints

– Conflicts of interest

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

– Timing of the engagement

– Scope limitations and other constraints

– Conflicts of interest

– Responsibility, or lack thereof, for helping the client implement

planning decisions

Planning the Engagement

• 24. The member should document and communicate to the client the scope

and nature of services to be provided and disclose the member’s agreed

upon compensation for such services. This communication should be

documented in the file and include descriptions of the following when

applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service

providers

– Timing of the engagement

– Scope limitations and other constraints

– Conflicts of interest

– Responsibility, or lack thereof, for helping the client implement

planning decisions

– Responsibility, or lack thereof, for monitoring the client’s progress in

achieving goals

Planning the Engagement

• 24. The member should document and communicate to the client the scope and nature of services to be provided and disclose the member’s agreed upon compensation for such services. This communication should be documented in the file and include descriptions of the following when applicable to the engagement:

– Engagement objectives

– Scope of services to be provided

– Roles and responsibilities of the member, client, and other service providers

– Timing of the engagement

– Scope limitations and other constraints

– Conflicts of interest

– Responsibility, or lack thereof, for helping the client implementplanning decisions

– Responsibility, or lack thereof, for monitoring the client’s progress in achieving goals

– Responsibility, or lack thereof, for updating the plan and proposing new action

Frequently Asked Questions

• Is there a specific format or specific language that must be used to meet the requirements of documenting and communicating to the client as set forth by the statement?

• I perform ongoing review of my clients’ financial situations, which is covered by one original engagement letter or other service agreement, such as an investment advisory agreement.

Under the statement, would a new engagement letter or service agreement (or modification thereof) be necessary?

Planning the Engagement

• 25. The member should evaluate the appropriateness of the original engagement as the engagement proceeds and document and communicate needed changes to the client.

• 26. If the member is aware of a service needed to complete the engagement and does not, or will not, provide that service, the member should limit the scope of the engagement accordingly and recommend that the client engage another service provider for that service in writing.

Responsibilities of Members in PFP Engagements

• 22. Prior to beginning the

engagement, and throughout the

engagement as circumstances

dictate, the member should

disclose in writing all

compensation the member and

the member’s firm or affiliates will

receive for services rendered or

products sold.

• 22. Continued:

The disclosure should include

…

Responsibilities of Members in PFP Engagements

Responsibilities of Members in PFP Engagements

• 22. Continued:

The disclosure should include

…

– the method of compensation,

including the impact of indirect

compensation;

Responsibilities of Members in PFP Engagements

• 22. Continued:

The disclosure should include

…

– the method of compensation,

including the impact of indirect

compensation;

– the amount of compensation;

Responsibilities of Members in PFP Engagements

• 22. Continued:

The disclosure should include …

– the method of compensation,

including the impact of indirect

compensation;

– the amount of compensation;

– the time period over which

compensation will be received; and

Responsibilities of Members in PFP Engagements

• 22. Continued:

The disclosure should include …

– the method of compensation, including the impact of indirect compensation;

– the amount of compensation;

– the time period over which compensation will be received; and

– the compensation, including noncash benefits, received by the member for referrals to other providers.

Frequently Asked Questions

• What compensation disclosure is required to begin the engagement if it is not possible to determine or reasonably estimate the amount of compensation to be earned?

• Hourly compensation disclosures: Paragraph 22 of the statement requires that compensation disclosures are made prior to beginning the engagement. How should this be disclosed if the specific dollar amount cannot be determined for engagements charged on an hourly fee basis?

Frequently Asked Questions

• Investment compensation disclosures:Paragraph 22 of the statement requires that compensation disclosures are made prior to beginning the engagement. How should this be disclosed if the specific dollar amount cannot be determined?

• Insurance compensation disclosure: Paragraph 22 of the statement requires that compensation disclosures are made prior to beginning the engagement. How should this be disclosed if the specific dollar amount of compensation cannot be determined on the sale of insurance products?

Frequently Asked Questions

• Am I required to make additional, separate or duplicate disclosures to the client in an engagement letter if the disclosures have been made in another client communication (e.g., investment advisory agreement or other client contract)?

Responsibilities of Members in PFP Engagements

• 23. If compensation

alternatives are offered, the

member should disclose the

differences in these alternatives

in writing.

Obtaining & Analyzing Information

• 28. The member should use professional judgment when obtaining and analyzing relevant information necessary to develop recommendations based on the stated engagement objectives.

• 29. If the member is unable to collect sufficient relevant information to establish a reasonable basis for recommendations, the engagement scope may be restricted to those matters for which sufficient information is available. This scope limitation should be communicated to the client in writing, including that this limitation should be taken into account in the assessment of conclusions and recommendations developed.

Obtaining & Analyzing Information

• 30. If sufficient information does not exist to proceed as agreed, the member should terminate or modify the engagement through mutual agreement with the client. This engagement modification or termination should be communicated in writing.

• 31. When analyzing information obtained while performing the engagement, the member should– evaluate the reasonableness of estimates and

assumptions that are significant to the plan;

– use assumptions that are appropriate and consistent with each other; and

– consider the interrelationship of various PFP activities

Developing & Communicating Recommendations

• 32. The member should establish a reasonable basis for PFP recommendations.

• 33. The member should develop recommendations derived from analyses of relevant information, client goals, and the client’s overall financial circumstances. Even when an engagement addresses a limited number of personal financial goals, the member should consider the client’s overall known financial circumstances.

• 34. The nature and extent of analyses and other procedures performed when establishing a basis for recommendations are affected by the scope and objectives of the engagement and should be documented.

Developing & Communicating Recommendations

• 35. The member should communicate to the client the assumptions and estimates that are significant to the recommendations. This should be documented and include the following:

– A summary of the client’s goals

– Significant assumptions

– Estimates

– Recommendations

– A description of limitations on the work performed

– The recommendations in the engagement should contain qualifications to the recommendations if the effects of certain planning areas on the client’s overall financial picture were not considered

Implementation Engagements

• 37. The member should communicate in writing the level of responsibility, if any, for the following:

– Selecting and acquiring products

– Selecting service providers

– Establishing selection criteria

– Coordinating or reviewing the delivery of services or products by other service providers

Implementation Engagements

• 39. A member who is engaged to participate in recommending products should …

– gather information that establishes a reasonable basis for determining whether a product meets the selection criteria.

– communicate this evaluation in writing, along with product recommendations.

– disclose in writing any compensation received for recommending products.

Working With Other Service Providers

• 45. When referring another service provider to a client, the member should …

– consider the professional qualifications of another service provider before referring the client to that service provider;

– disclose, in writing, any compensation received for making such referrals; and

– communicate, in writing, the extent to which the member will or will not evaluate the work performed by the service provider.

Questions???