newbase 636 special 29 june 2015

TRANSCRIPT

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 1

NewBase 29 June 2015 - Issue No. 636 Senior Editor Eng. Khaled Al Awadi

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

Egypt solidifies links to China with membership in Silk Road Economic Belt trade union

http://www.albawaba.com/business

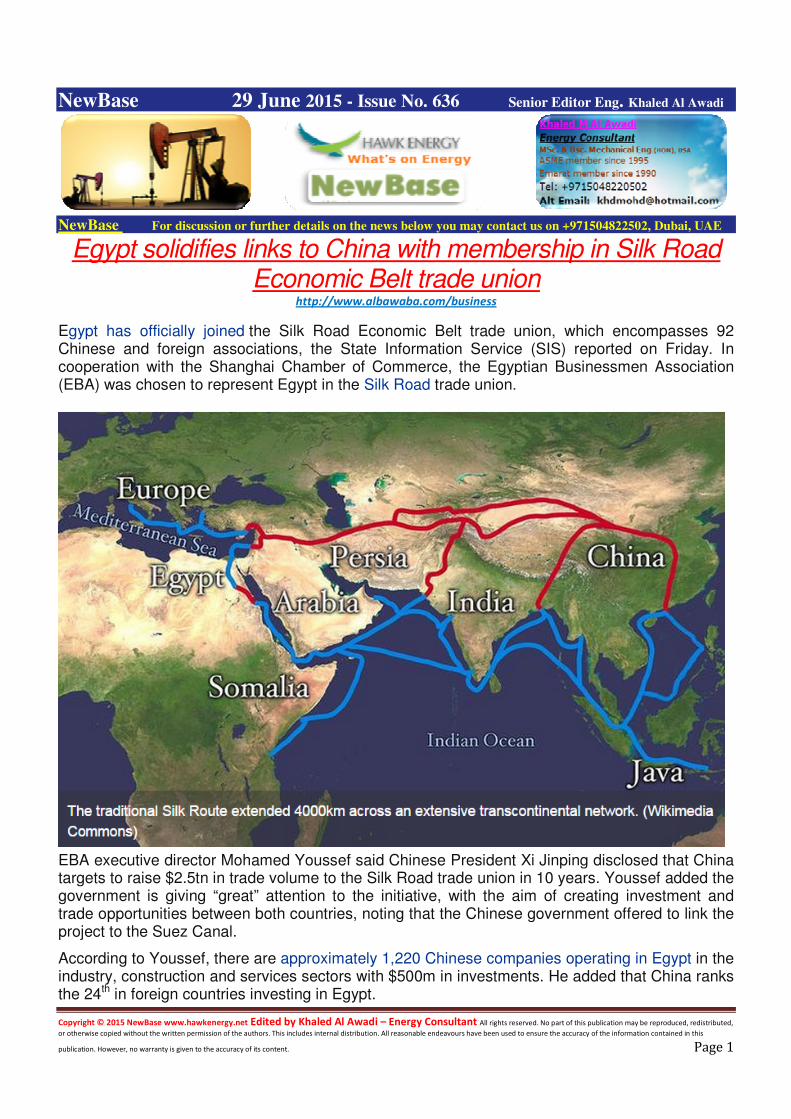

Egypt has officially joined the Silk Road Economic Belt trade union, which encompasses 92 Chinese and foreign associations, the State Information Service (SIS) reported on Friday. In cooperation with the Shanghai Chamber of Commerce, the Egyptian Businessmen Association (EBA) was chosen to represent Egypt in the Silk Road trade union.

EBA executive director Mohamed Youssef said Chinese President Xi Jinping disclosed that China targets to raise $2.5tn in trade volume to the Silk Road trade union in 10 years. Youssef added the government is giving “great” attention to the initiative, with the aim of creating investment and trade opportunities between both countries, noting that the Chinese government offered to link the project to the Suez Canal.

According to Youssef, there are approximately 1,220 Chinese companies operating in Egypt in the industry, construction and services sectors with $500m in investments. He added that China ranks the 24th in foreign countries investing in Egypt.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 2

The Silk Road Economic Belt is one of three initiatives adopted by the Chinese president. The initiative was proposed in September 2013 with the aim of linking three continents; Asia, Africa and Europe. The belt was said to reopen the links between China and Europe though the Middle East, Central Asian, South China Sea, the Malacca Strait and the Indian Ocean, to East and South Africa.

President Abdel Fattah Al-Sisi visited China in December 2014, where he signed with his Chinese counterpart a comprehensive strategic partnership agreement. This included three cooperation agreements in the fields of economy and technical cooperation.

The two parties signed a Memorandum of Understanding (MoU) to establish a joint laboratory for renewable energy, between Egypt’s Ministry of Scientific Research and China’s Ministry of Science and Technology. The third agreement was a cooperation agreement between China National Space Administration (CNSA) and the National Authority for Remote Sensing and Space Sciences (NARSS).

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 3

China’s “One Belt – One Road” Mega-Project Will Boost Eurasian Natural Gas Opportunities

Ariel Cohen, Ph.D., is Director, Center for Energy

The efforts of China to ensure its economic development and preeminence include the creation of the “New Silk Road” - the enormous system of infrastructure mega-projects to stretch from the Pacific to the Atlantic. If completed, it will be the largest infrastructure undertaking ever built. Natural gas features prominently in the plan.

This was the focus of a two-day conference in Beijing, where I chaired the Eurasia energy panel, and I walked away in awe. The conference was organized by the Chinese Academy of Social Sciences and Institute for the Analysis of Global Security in Washington – an energy and security think tank.

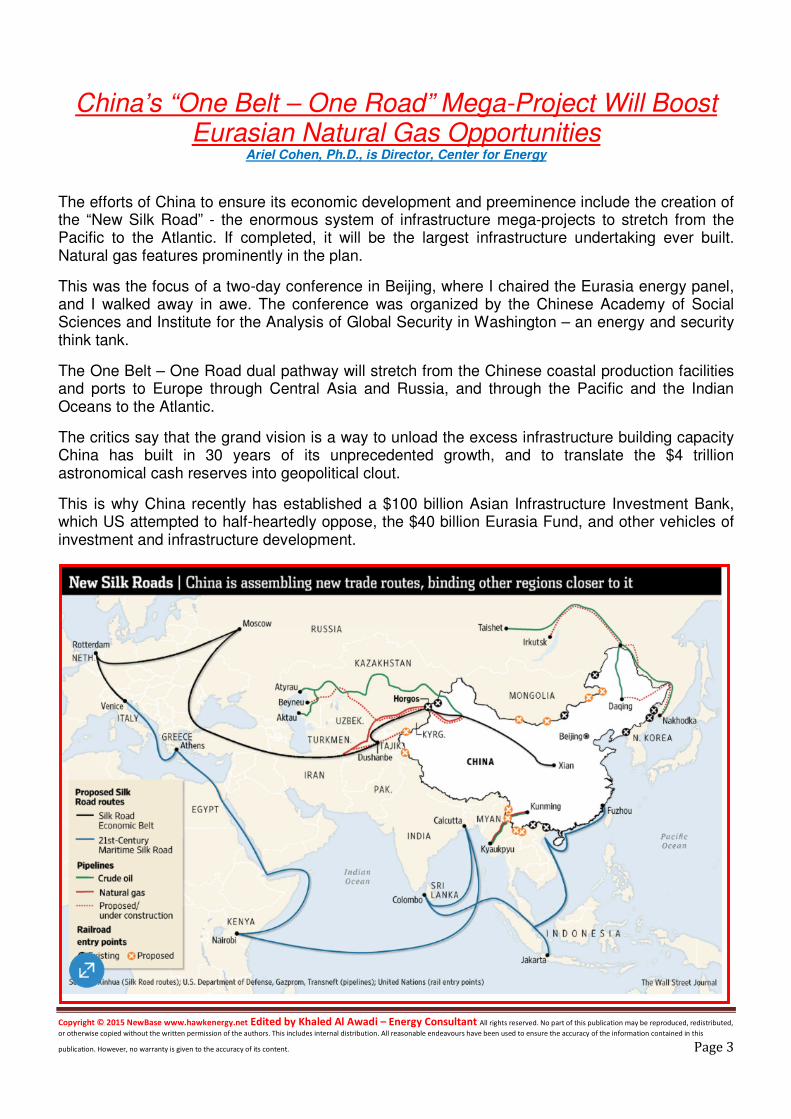

The One Belt – One Road dual pathway will stretch from the Chinese coastal production facilities and ports to Europe through Central Asia and Russia, and through the Pacific and the Indian Oceans to the Atlantic.

The critics say that the grand vision is a way to unload the excess infrastructure building capacity China has built in 30 years of its unprecedented growth, and to translate the $4 trillion astronomical cash reserves into geopolitical clout.

This is why China recently has established a $100 billion Asian Infrastructure Investment Bank, which US attempted to half-heartedly oppose, the $40 billion Eurasia Fund, and other vehicles of investment and infrastructure development.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 4

This is a project bigger than trans-continental railroads of the nineteenth century in North America in Russia. It is bigger than the Suez and Panama Canals combined. If China persist upon its Eurasian Silk Road beyond President Xi’s two terms in office, its creation will boost the economy of the transit regions significantly by providing millions of jobs and improving security in “failed” or “failing” states in Central and South Asia: Myanmar, Bangladesh, Pakistan, Afghanistan, Tajikistan, and Kyrgyzstan, to mention a few.

The One Belt-One Road will stretch on land: through Mongolia, Kazakhstan and Russia, to Western Europe. There are southern branches to Burma (Myanmar), Pakistan and Iran. A look at the map discloses that China “hugs” India by building the Karakorum highway to the Pakistani port of Gwadar on the Arabian Sea. This makes the leadership in New Delhi nervous, taking into account that in 1962 the two Asian giants have fought a fierce but short war in Tibet, with India losing territory.

“One Belt-One Road” features natural gas projects prominently. First, it’s backbone: the longest pipeline on earth, the Central Asia – China pipeline of 8,000 km, which goes from Turkmenistan via Uzbekistan and Azerbaijan, to China. Currently, it supplies 55 billion cubic meters of gas a year to the energy-starved and polluted Chinese cities. CNPC executives, who built this feat of engineering, pat themselves on the back. Deservedly so.

The two Russian pipelines: Power of Siberia in the East and Altay in the West, are capable of brining up to 80 bcm of gas a year to China, when fully built. The challenge is the price, the terrain, and reserves for the Altay pipeline – currently those are not confirmed.

However, Chinese appetites do not stop there. Turkmenistan and Iran have the fourth and the second largest reserves on the planet respectively. A much-discussed Turkmenistan-Afghanistan-Pakistan-India (TAPI) pipeline, and the Iran-Pakistan-India (IPI) pipeline are both on the table. Beijing would like to extend a pipeline from either one of them – to China. However, the Balochi Sunni Moslem rebels who fight both the Shia Islamic Republic of Iran and the Sunni, but mostly secular regime in Islamabad, threaten IPI, while the Taliban in Afghanistan may derail TAPI. The very tough mountainous terrain and syphoning of gas by the local tribes are additional problems the pipelines will face. The security challenge for the Chinese and local operators are going to be huge.

However, if the pipelines are delayed, one can envisage the LNG tankers on the maritime Silk Road is going to bring LNG to China from Australia, East and West Africa, and the Gulf.

Speaking of energy security of the region, the implementation of this mega-project will also allow energy resources to flow to new consumers in the developing regions. Moreover, creation of unified energy systems will make the participating countries interdependent in terms of energy consumption, which will serve as a “safety net” for regional security.

Having the rules of engagement equitable and transparent will go a long way to attract stake-holders and capital to the infrastructure projects, including ports, oil and gas fields and pipelines, LNG and other port facilities, petrochemical processing, and IT.

If it does it right, China can strengthen its own security, interdependence and cooperation with the world by allowing Western, including North American and global firms, to participate in this historic

undertaking.

-Ariel Cohen, Ph.D., is Director, Center for Energy, Natural Resources and Geopolitics at the Institute for the Analysis of Global Security (www.iags.org) and a Senior Fellow at the Global Energy Center and the Dinu Patriciu Eurasia Center at The Atlantic Council.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 5

Iran said to boost condensate stockpiles after refinery delay Bloomberg + NewBas

Iran’s delay in starting the Gulf Star refinery means it’s being forced to boost stockpiles of condensate, a light oil found in natural gas deposits, said four people with knowledge of the situation. The 360,000 barrel-a-day refinery won’t start this year as planned, leaving excess condensate supply from the South Pars gas deposit, said the people, asking not to be identified because the information is private. State-run National Iranian Oil Co’s press office didn’t respond to two calls seeking comment on Thursday, a weekend day in Iran.

Iran’s stockpiles are growing as international sanctions are curbing exports of crude oil. The Gulf Star refinery, meant to process the condensate from South Pars, may not start until the second half of next year, two of the people said. “The Gulf Star refinery is the most important refining project in Iran,” Siamak Adibi, a London-based analyst at Facts Global Energy, said by telephone on Thursday. “Iran wants to eventually cut condensate exports to zero by using the fuel to make gasoline and becoming self-sufficient.” Iran now imports gasoline to meet domestic demand. Iran is producing about 500,000 bpd of South Pars condensate, the people said. That’s up from the 350,000 barrels produced on average daily last year, FGE’s Adibi said. Iran is storing the fuel on tankers in the Gulf and in onshore tanks in Dalian, China, the people said. Iran’s exports of crude and condensate fell to 1.4mn bpd on average last year due to sanctions, the US Energy Information Administration said on its website on Wednesday. Sales averaged about 2.6mn bpd in 2011, before the US and European Union imposed the restrictions, the EIA said. .

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 6

U.S. refinery capacity reaches 18 million barrels per day Source: U.S. Energy Information Administration, 2015 Refinery Capacity Report

Increased refinery runs—based on increases in both capacity and utilization—have helped accommodate increases in U.S. crude oil production. The United States' capacity to refine crude oil into petroleum products—measured as operable atmospheric crude distillation unit (CDU) capacity—increased by 0.2% in 2014, reaching 18.0 million barrels per calendar day (b/d), according to EIA's recently released annual Refinery Capacity Report.

The refinery capacity reported for the beginning of 2015 includes expansions that were operable on January 1, but not necessarily operating. Because these units were not operating as of January 1, capacity for those projects is listed as idle. Dakota Prairie Refining recently completed construction of one of the few new refineries built in the United States over the past 30 years. This relatively simple refinery, which is located in western North Dakota, has CDU capacity of 19,000 b/d and will refine locally produced crude oil to make diesel fuel. Earlier this year, Kinder Morgan added a 42,000 b/d condensate splitter to its Galena Park, Texas crude oil terminal that is also included in the capacity estimate for the start of 2015. A second unit, with similar capacity, is expected to start operating this summer, but it is not included in the January 1, 2015 capacity estimate. U.S. refinery capacity and utilization have increased to accommodate increasing domestic crude oil production, which rose to an average 8.7 million b/d in 2014, 3.2 million barrels higher than in 2010. Gross inputs to refineries averaged a record 16.1 million b/d in 2014 compared with 15.1 million b/d in 2010. Nearly 75% of the 1.0 million b/d increase in refinery gross inputs is the result of a 4 percentage point increase in refinery utilization compared with 2010 (from 86% to 90%). The rest of the increase is attributable to capacity expansions. Over the same period, crude imports decreased by 1.9 million b/d, and crude exports increased by 0.3 million b/d.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 7

The report also includes information on expansions planned for the remainder of 2015. Capacity is expected to expand by an additional 119,000 barrels per stream day later in 2015. Delek US plans to increase CDU capacity by 10,000 b/d at its Tyler, Texas refinery, and Marathon reported that it plans to add 35,000 b/d of condensate splitter capacity at its Catlettsburg, Kentucky refinery by the end of the year. Further investment in refinery expansion projects will depend on expectations of relative crude oil prices and the relative economic advantage of the U.S. refining fleet compared with refineries in the rest of the world.

EIA's Refinery Capacity Report measures refinery capacity in barrels per stream day and barrels per calendar day. Barrels per stream day reflects the maximum number of barrels of input that a distillation facility can process within a 24-hour period when running at full capacity under optimal crude oil and product slate conditions with no allowance for downtime. Barrels per calendar day is a measure of the amount of input that a distillation unit can process in a 24-hour period under usual operating conditions and maintenance downtime. Stream day capacity is typically about 6% higher than calendar day capacity.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 8

Argentina and China lead shale development outside North America in first-half 2015

U.S. EIA and Advanced Resources International, Inc., World Shale Gas and Shale Oil Resource Assessment

As recently as last year, only four countries in the world were producing commercial volumes of either natural gas from shale formations (shale gas) or crude oil from tight formations (tight oil): the United States and Canada, and more recently, Argentina and China. Beyond these four countries, other countries have started exploring hydrocarbons from shale and other tight resources, but they are still short of reaching commercial production.

The 2013 World Shale Gas and Shale Oil Resource Assessment, produced by EIA and Advanced Resources International (ARI), noted large shale deposits in China and Argentina. Exploration and drilling is already underway in these countries. For the last two years, China has drilled more than 200 wells, and Argentina has drilled more than 275 wells. Each country has the potential to significantly increase production of shale gas and tight oil.

In Argentina, many international companies hold leases and have drilled wells in shale formations. Much of the initial activity has targeted shale oil and natural gas in the Neuquen Basin's Vaca Muerta shale formation, located in west-central Argentina.

National energy company Yacimientos Petroliferos Fiscales (YPF), the largest shale operator in the country, reported production in April 2015 of 22,900 barrels per day (b/d) of oil and 67 million cubic feet per day (MMcf/d) of natural gas from three joint ventures in Vaca Muerta: one with Chevron at the Loma Campana field, a second one with Dow Chemical at the El Orejano field, and a third joint venture with Petronas at La Amarga Chica field.

In addition, China's national oil company Sinopec and Russia's national oil company Gazprom have recently signed a memorandum of understanding with YPF to jointly develop shale from the same basin.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 9

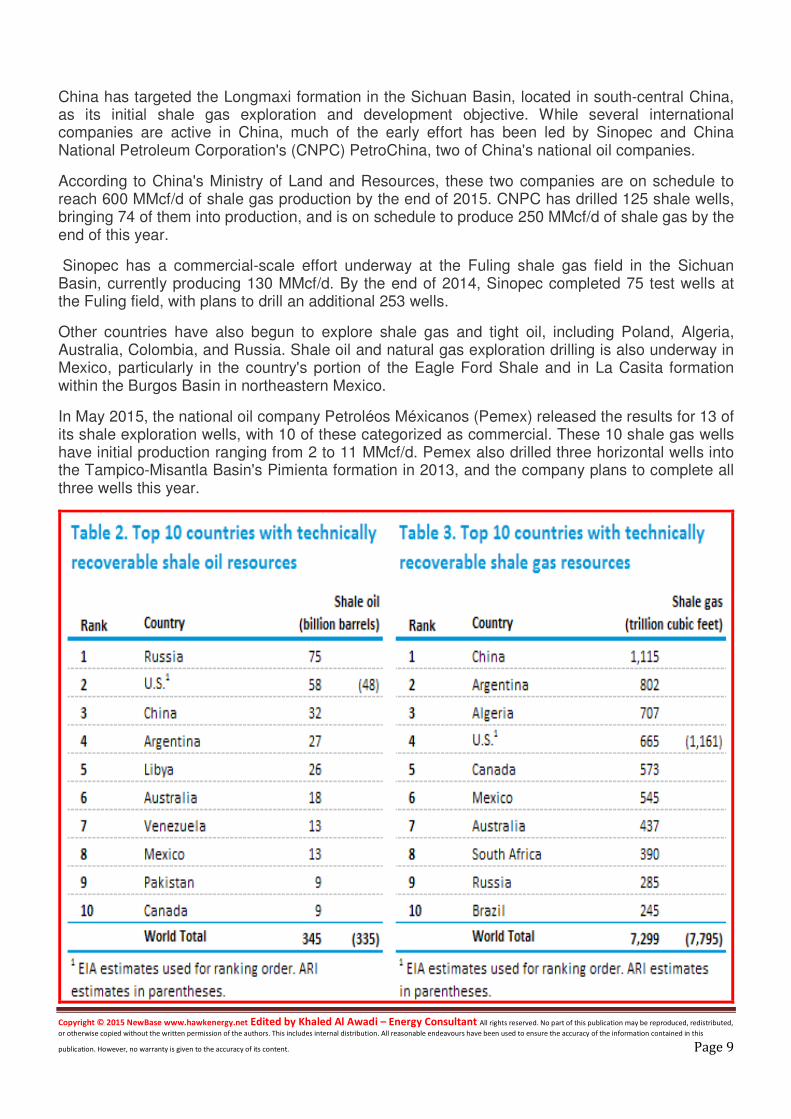

China has targeted the Longmaxi formation in the Sichuan Basin, located in south-central China, as its initial shale gas exploration and development objective. While several international companies are active in China, much of the early effort has been led by Sinopec and China National Petroleum Corporation's (CNPC) PetroChina, two of China's national oil companies.

According to China's Ministry of Land and Resources, these two companies are on schedule to reach 600 MMcf/d of shale gas production by the end of 2015. CNPC has drilled 125 shale wells, bringing 74 of them into production, and is on schedule to produce 250 MMcf/d of shale gas by the end of this year.

Sinopec has a commercial-scale effort underway at the Fuling shale gas field in the Sichuan Basin, currently producing 130 MMcf/d. By the end of 2014, Sinopec completed 75 test wells at the Fuling field, with plans to drill an additional 253 wells.

Other countries have also begun to explore shale gas and tight oil, including Poland, Algeria, Australia, Colombia, and Russia. Shale oil and natural gas exploration drilling is also underway in Mexico, particularly in the country's portion of the Eagle Ford Shale and in La Casita formation within the Burgos Basin in northeastern Mexico.

In May 2015, the national oil company Petroléos Méxicanos (Pemex) released the results for 13 of its shale exploration wells, with 10 of these categorized as commercial. These 10 shale gas wells have initial production ranging from 2 to 11 MMcf/d. Pemex also drilled three horizontal wells into the Tampico-Misantla Basin's Pimienta formation in 2013, and the company plans to complete all three wells this year.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 10

First sign of a US drilling recovery emerges in rigs Bloomberg + NewBase

There’s good news and bad news for the energy industry in Baker Hughes Inc rig counts. An unprecedented retreat from America’s oil fields dragged on for a 29th straight week, with the number of rigs targeting crude slumping to the lowest since 2010. That was more than offset by a rebound in gas exploration, which spurred the first increase in total US drilling in more than 6 months.

Five new gas rigs were enough to boost the total rig count by two, ending a record streak of declines that began in early December as America’s oil explorers sidelined more than half their drilling equipment. The crude they were pumping out of US shale formations helped create

a global glut that drove prices down 49% in the second half of 2014. “This is the first sign that we may see a drilling recovery in the second half of the year,” James Williams, president of energy consultancy WTRG Economics, said by phone from London, Arkansas. “Drilling contractors like Halliburton, Baker Hughes and Cameron should be celebrating because it didn’t get any worse this week. These days, that’s worthy of a small celebration.” Rigs drilling for oil fell by three this week to 628, the least since August 6, 2010, as those targeting natural gas jumped to 228, Baker Hughes said on its website Friday. The total count, which includes three miscellaneous rigs, gained to 859. US oil and gas explorer WPX Energy Inc said on Thursday that it plans to raise its rig count by two this year and resume well completions in the Williston Basin, home of North Dakota’s Bakken shale. Even with the collapse in oil drilling, the US pumped 9.61mn bpd of crude in the week ended June 5, the highest in weekly Energy Information Administration data since 1983. The agency forecast that production from tight-rock formations such as the Bakken and Texas’s Eagle Ford shale will shrink 1.3% to 5.58mn bpd this month. America’s gas production is rising for the 10th straight year, driven by gains from the Marcellus shale in the eastern US Inventories have rebounded faster than the five-year average since the stockpiling season began in April, wiping out a deficit that had persisted November 2013. Natural gas futures for July delivery fell 7.7 cents on Friday to settle at $2.773 per million British thermal units on the New York Mercantile Exchange. US benchmark West Texas Intermediate oil for August delivery fell 7 cents to settle at $59.63 on the Nymex. While futures have climbed 12% this year, they’re down 44% from a year ago. This year’s rise in oil prices, coupled with a decline in drilling and completion costs, may spur enough of a rebound in new oil production to stave off a drop in US crude supply, Bloomberg Intelligence analysts Vincent Piazza and Syarifa Galeb said in a report Wednesday. “Shorter-cycle, just-in-time inventory helps to steady production,” they said. “Output may remain resilient in the near-term.”

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 11

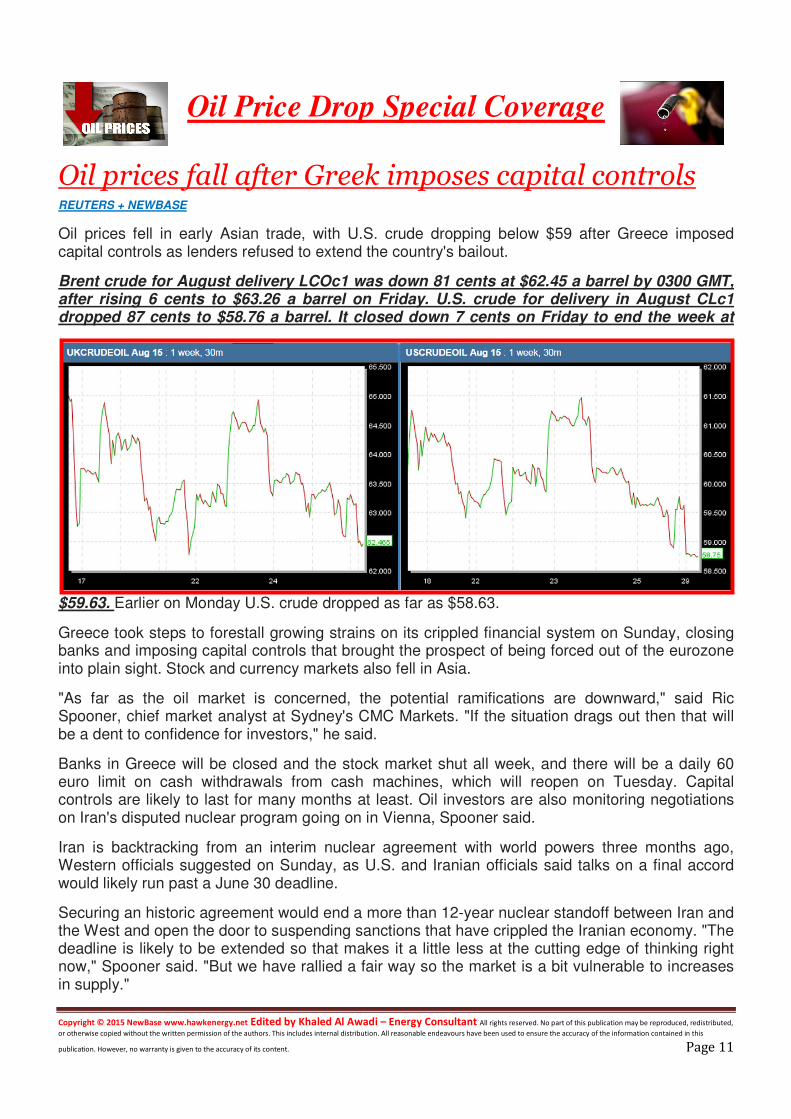

Oil Price Drop Special Coverage

Oil prices fall after Greek imposes capital controls REUTERS + NEWBASE

Oil prices fell in early Asian trade, with U.S. crude dropping below $59 after Greece imposed capital controls as lenders refused to extend the country's bailout.

Brent crude for August delivery LCOc1 was down 81 cents at $62.45 a barrel by 0300 GMT, after rising 6 cents to $63.26 a barrel on Friday. U.S. crude for delivery in August CLc1 dropped 87 cents to $58.76 a barrel. It closed down 7 cents on Friday to end the week at

$59.63. Earlier on Monday U.S. crude dropped as far as $58.63.

Greece took steps to forestall growing strains on its crippled financial system on Sunday, closing banks and imposing capital controls that brought the prospect of being forced out of the eurozone into plain sight. Stock and currency markets also fell in Asia.

"As far as the oil market is concerned, the potential ramifications are downward," said Ric Spooner, chief market analyst at Sydney's CMC Markets. "If the situation drags out then that will be a dent to confidence for investors," he said.

Banks in Greece will be closed and the stock market shut all week, and there will be a daily 60 euro limit on cash withdrawals from cash machines, which will reopen on Tuesday. Capital controls are likely to last for many months at least. Oil investors are also monitoring negotiations on Iran's disputed nuclear program going on in Vienna, Spooner said.

Iran is backtracking from an interim nuclear agreement with world powers three months ago, Western officials suggested on Sunday, as U.S. and Iranian officials said talks on a final accord would likely run past a June 30 deadline.

Securing an historic agreement would end a more than 12-year nuclear standoff between Iran and the West and open the door to suspending sanctions that have crippled the Iranian economy. "The deadline is likely to be extended so that makes it a little less at the cutting edge of thinking right now," Spooner said. "But we have rallied a fair way so the market is a bit vulnerable to increases in supply."

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 12

Oil prices influence stock market through the private sector Saudi Gazette

Movement in oil prices influences the stock market through the private sector. In the short term a rise or fall in oil prices has an immediate effect on business confidence. As oil prices remain high (or low) beyond the short-term, business leaders begin to form opinions on future investment decisions, Jadwa Investment said in its report on “Oil Prices and the Saudi Stock Exchange”.

Over the medium term these investment decisions are implemented and ultimately have an impact on private sector growth. The higher or lower anticipated growth of listed companies translates into a better or worse performance on the TASI. Looking over the same periods in which oil prices declined, as mentioned above (1981-1986, 1992-1994 and 1997-1999), there is a more varied adjustment to private sector GFCF. It seems that, whereas government GFCF usually adjusts to lower or higher oil prices within one to two

years, private investment decisions are more lagged. Since private sector GFCF adjustment to oil prices is varied, the impact of the private sector transmission on the stock market will be less immediate. During the slump in oil prices between 1981-1986, private sector GFCF declined in each of the years, except 1983, and recovered, with a 1.9 percent increase, year-on-year, only in 1988. As oil prices dropped in each of the years between 1991 and 1994, GCFC declined in only 1994. During the price decline of 1997 and 1998, no cuts in GFCF were made. There is one exception where an immediate drop in oil prices has had an instant impact on GFCF. This was seen in 2009, but due to the global nature of the events unfolding then and the major fluctuations in oil prices during that year the reason for a immediate cut in GFCF is apparent. Looking at data on net-income of listed companies and oil prices, the relationship is not so apparent, although this is based on a shorter span of data going back to 2005. From 2006 to 2008 we saw a year-on-year rise in Brent prices, but average net-income per company dropped in each of the three years. In 2009 the fallout from the global financial crisis affected oil prices and profitability, both of which were down, year-on-year. In 2010 and 2011 oil prices increased, year-on-year, and so did average profitability. In 2012, oil prices were virtually flat, year-on-year, but profits were down slightly. Since 2012, we have seen a year-on-year decline in oil prices but rises in average profitability of listed companies. Although there seems to be no clear relationship between oil prices and net-income of listed companies, the analysis is somewhat hampered by the number of companies being added to the Tadawul since 2006. There have some large IPOs during this period but also a number of smaller companies have also been included, especially so from sectors such as insurance and media, which has partially distorted average net-income over the period in question.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 13

Movements in the price of oil will influence investment by both the public and private sector, which will in turn affect the stock market. However, in order determine a more precise nature of relationship between the oil price and the TASI we mapped the correlation of sector share prices with Brent crude oil prices using daily data over the past eight years. The correlation of the TASI to oil prices over this period is equal to 0.355, which is not very strong given the dependence of the economy on oil, in general. There has been a clear divergence between the TASI and oil prices for much of the recent past, with correlation following a progressively downward trend. In the two years between March 2007 to March 2009 correlation was at 0.811, but decreased to equal 0.355 in the eight years between March 2007 to March 2015. Correlation between oil prices and the TASI was the highest during March 2007 to March 2009 and March 2009 to March 2011, but lower in the two years from March 2011 and March 2013. In fact, the period between March 2013 to March 2015 shows negative correlation, although it becomes increasingly positive from September 2014, as oil prices begin to fall rapidly.

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 14

NewBase For discussion or further details on the news below you may contact us on +971504822502, Dubai, UAE

Your partner in Energy Services

NewBase energy news is produced daily (Sunday to Thursday) and

sponsored by Hawk Energy Service – Dubai, UAE.

For additional free subscription emails please contact Hawk Energy

Khaled Malallah Al Awadi, Energy Consultant MS & BS Mechanical Engineering (HON), USA Emarat member since 1990 ASME member since 1995 Hawk Energy member 2010

Mobile: +97150-4822502 [email protected] [email protected]

Khaled Al Awadi is a UAE National with a total of 25 years of experience in the Oil & Gas sector. Currently working as Technical Affairs Specialist for Emirates General Petroleum Corp. “Emarat“ with external voluntary Energy consultation for the GCC area via Hawk Energy Service as a UAE operations base , Most of the experience were spent as the Gas Operations Manager in Emarat , responsible for Emarat Gas Pipeline Network Facility & gas compressor stations . Through the years, he has developed great experiences in the designing & constructing of gas pipelines, gas metering &

regulating stations and in the engineering of supply routes. Many years were spent drafting, & compiling gas transportation, operation & maintenance agreements along with many MOUs for the local authorities. He has become a reference for many of the Oil & Gas Conferences held in the UAE and Energy program broadcasted internationally, via GCC leading satellite Channels.

NewBase : For discussion or further details on the news above you may contact us on +971504822502 , Dubai , UAE

NewBase 28 June 2015 K. Al Awadi

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 15

Copyright © 2015 NewBase www.hawkenergy.net Edited by Khaled Al Awadi – Energy Consultant All rights reserved. No part of this publication may be reproduced, redistributed,

or otherwise copied without the written permission of the authors. This includes internal distribution. All reasonable endeavours have been used to ensure the accuracy of the information contained in this

publication. However, no warranty is given to the accuracy of its content. Page 16