nextpharma - jefferies 1340 5 nextpharm… · nextpharma today is a business ... quality control...

TRANSCRIPT

1

Andy Kelley - COO

NextPharma

Jefferies 2014 Global Healthcare Conference19th – 20th November

2

Agenda

• Market Overview

• Introduction to NextPharma

• Services, Operational set-up and Markets supplied

• Key Success Factors, Customers and Products

• Strategic Outlook

• Q&A Session

2

3

I. MARKET OVERVIEW

3

4

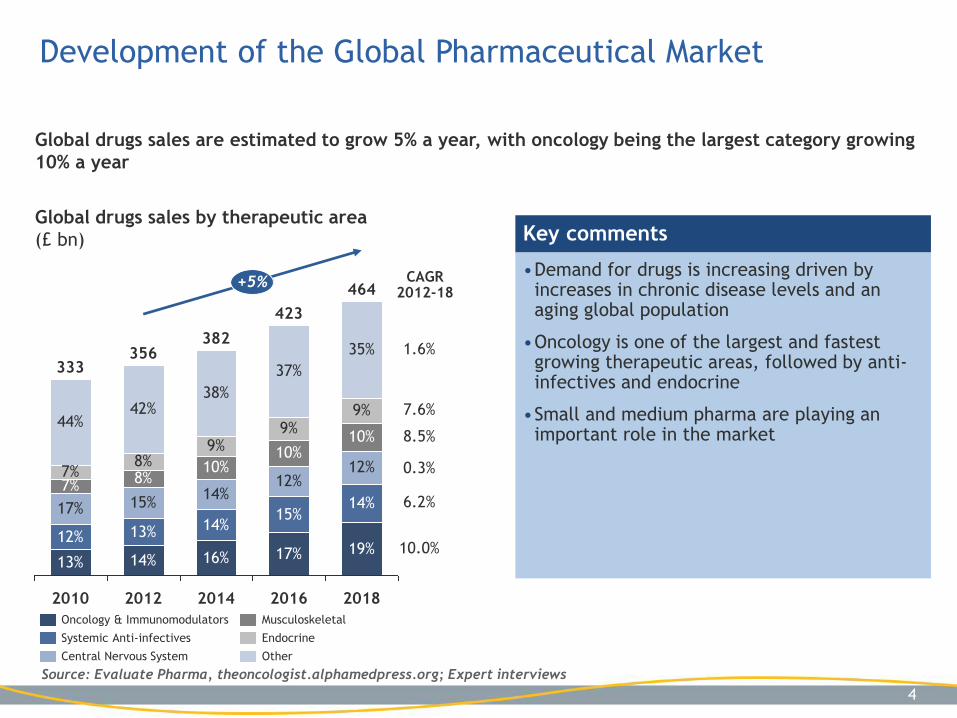

Development of the Global Pharmaceutical Market

4

Global drugs sales are estimated to grow 5% a year, with oncology being the largest category growing

10% a year

14%

19%

2016

423

37%

9%

10%

12%

15%

17%

2014

382

38%

+5%

2018

35%

9%

10%

12%

464

9%

10%

14%

14%

16%

2012

356

42%

8%8%

15%

13%

14%

2010

333

44%

7%7%

17%

12%

13%

Other

Endocrine

Musculoskeletal

Central Nervous System

Systemic Anti-infectives

Oncology & Immunomodulators

7.6%

8.5%

0.3%

6.2%

10.0%

1.6%

CAGR2012-18

Key comments

•Demand for drugs is increasing driven by increases in chronic disease levels and an aging global population

•Oncology is one of the largest and fastest growing therapeutic areas, followed by anti-infectives and endocrine

•Small and medium pharma are playing an important role in the market

Global drugs sales by therapeutic area

(£ bn)

Source: Evaluate Pharma, theoncologist.alphamedpress.org; Expert interviews

5

Development of the Global CMO market

5

Global CMO market is estimated to grow 7% a year across all geographies, and solid dose form

constitutes 62% of the market

5 5 5 5 6 6 6 7 7

3 3 4 4 4 4 5 554

44

45

55

66

+7%

+6%

17

18

16

17

15

16

14

15

13

14

12

13

11

13

10

12

2009

11

USEuropeROW

CAGR14-1709-14

62% 62% 62% 61%

33% 33% 33% 33%

100%

2011

5%100%

2012

100%

2013

5%5%

2018

6%

100%

Semisolids Liquids Solids

6%

8%

6%

7%

7%6%

Global CMO market by regions

(US$ bn)

Breakdown by dosage forms

(% of total market value)

Source: Frost & Sullivan, BCC Research

6

II. INTRODUCTION TO NEXTPHARMA

6

7

NextPharma ‘snapshot’

Double digit growth €143m turnover

Over 150 customers

including 7 out of the top 10

pharmaceutical companies

6 centres of excellence

1,000+ employees

• Capability to produce 4 billion tablets

• 500m finished packs produced

Approximately 100 customer &

authority audits each year

More than 10,000 batch releases

25%+ of employees work

in quality & regulatory roles

Smart

every

time

7

88

With over 150 customers across 6 continents

8

Send, UK• Head Office

Limay, France• Liquids

• Suppositories

Bielefeld, Germany• Modified Release/Pellets

• Analytical Services

Göttingen, Germany• Solids

• Clinical Trials Services

Berlin, Germany• Penicillins

Waltrop, Germany• Hormonal solids & semi-solids

• Semi-solids

Göttingen, Germany• Cephalosporin

Our 6 Centres of Excellence

9

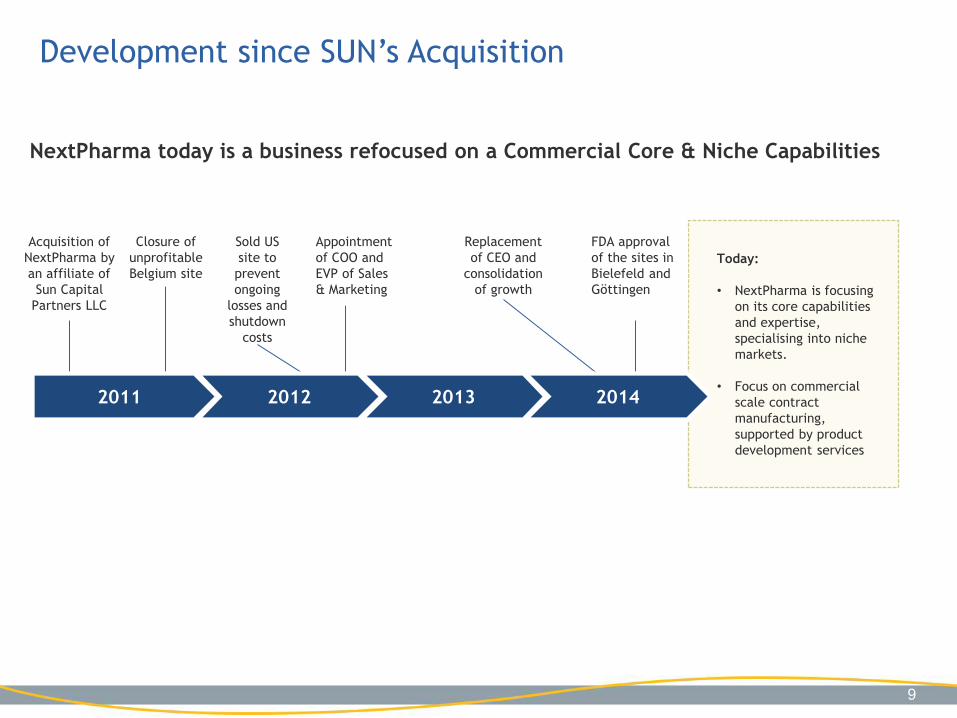

NextPharma today is a business refocused on a Commercial Core & Niche Capabilities

Today:

• NextPharma is focusing

on its core capabilities

and expertise,

specialising into niche

markets.

• Focus on commercial

scale contract

manufacturing,

supported by product

development services

Acquisition of

NextPharma by

an affiliate of

Sun Capital

Partners LLC

Appointment

of COO and

EVP of Sales

& Marketing

Closure of

unprofitable

Belgium site

Sold US

site to

prevent

ongoing

losses and

shutdown

costs

FDA approval

of the sites in

Bielefeld and

Göttingen

Replacement

of CEO and

consolidation

of growth

2011 2012 2013 2014

Development since SUN’s Acquisition

9

10

III. SERVICES, OPERATIONAL SET-UP AND MARKETS SUPPLIED

10

11

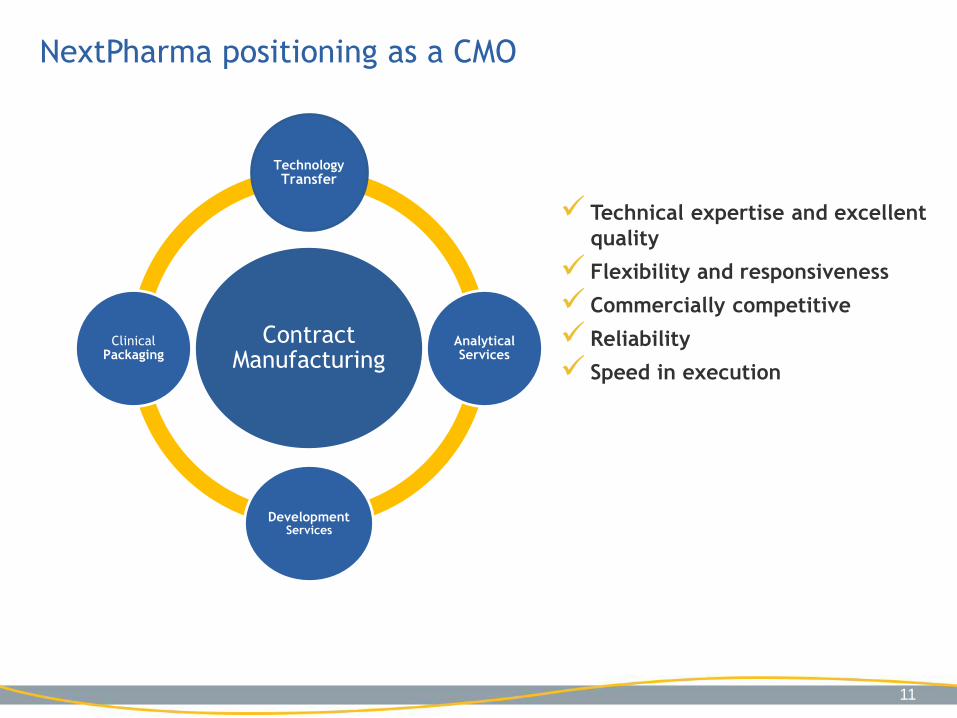

NextPharma positioning as a CMO

Contract Manufacturing

Technology Transfer

AnalyticalServices

DevelopmentServices

Clinical Packaging

Technical expertise and excellent

quality

Flexibility and responsiveness

Commercially competitive

Reliability

Speed in execution

11

12

NextPharma: What do we do in simple terms?

NextPharma provides contract manufacturing services to pharmaceutical companies serving global

markets

NextPharma manufactures, amongst others:

Oral contraceptive for 10+ pharmaceutical companies across Europe

Antibiotics (penicillins and cephalosporins) to treat infections

Controlled drugs (narcotics)

Painkillers (tablets, gels, sprays)

Testosterone gels

Vitamin supplements (pellets)

12

13

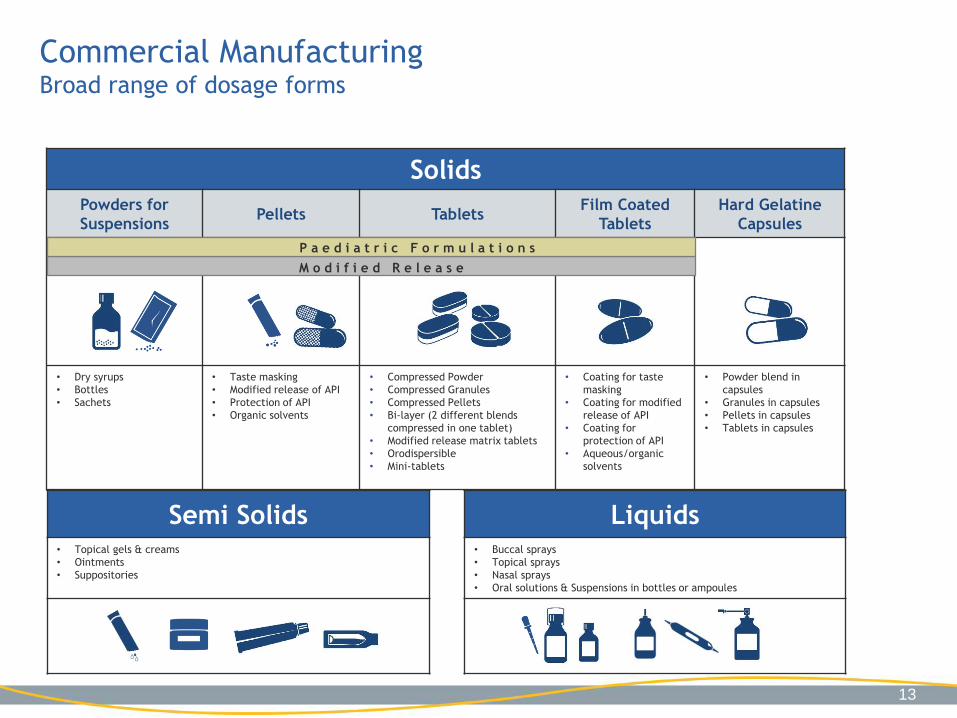

SolidsPowders for

SuspensionsPellets Tablets

Film Coated

Tablets

Hard Gelatine

Capsules

• Dry syrups

• Bottles

• Sachets

• Taste masking

• Modified release of API

• Protection of API

• Organic solvents

• Compressed Powder

• Compressed Granules

• Compressed Pellets

• Bi-layer (2 different blends

compressed in one tablet)

• Modified release matrix tablets

• Orodispersible

• Mini-tablets

• Coating for taste

masking

• Coating for modified

release of API

• Coating for

protection of API

• Aqueous/organic

solvents

• Powder blend in

capsules

• Granules in capsules

• Pellets in capsules

• Tablets in capsules

P a e d i a t r i c F o r m u l a t i o n s

M o d i f i e d R e l e a s e

Liquids• Buccal sprays

• Topical sprays

• Nasal sprays

• Oral solutions & Suspensions in bottles or ampoules

Semi Solids• Topical gels & creams

• Ointments

• Suppositories

13

Commercial ManufacturingBroad range of dosage forms

14

NextPharma’s services: Pharmaceutical development

Pharmaceuticaldevelopment

• Formulation and

process development

• Analytical method

development

• Stability testing

14

NextPharma develops and provides the process for transferring

the product formulation to industrial scale manufacturing

Pharmaceutical development services support contract

manufacturing services and include:

• formulation development

• analytical and microbiological testing, manufacturing of clinical batches

as well as clinical trial labelling and

• stability testing

• tech transfer / scale-up

15

NextPharma’s services: Clinical supply

15

Clinical Manufacturing, Packaging & Labelling

• Blinding/Encapsulation capabilities for all major dosage forms

• Primary and secondary packaging of solids, semi-solids, liquids

Storage & Distribution

Regulatory Support

Clinicalsupply

• Clinical batch

manufacture

• Phase I – IV

clinical trials supply

16

NextPharma’s services: Commercial Manufacturing

16

NextPharma’s manufacturing centres of excellence provide

customers with reliable product supply in facilities that include

European, US FDA and ANVISA approvals.

Sourcing and testing of materials

Bulk manufacture

Primary packaging

Secondary packaging

Quality Control and market release

Shipment to customer

• Validation batches

• Technology transfer

• Launch and supply

CommercialManufacturing

17

Markets we supply

Berlin

Bielefeld

Göttingen

Limay

Waltrop

Europe USA ROW

17

NextPharma Group FDA success update:

• Waltrop: successful routine re-inspection January 2014

• Bielefeld: first FDA audit for US market successfully completed August 2014

• Göttingen: first FDA audit for US market successfully completed September 2014

18

IV. KEY SUCCESS FACTORS, CUSTOMERS AND PRODUCTS

18

19

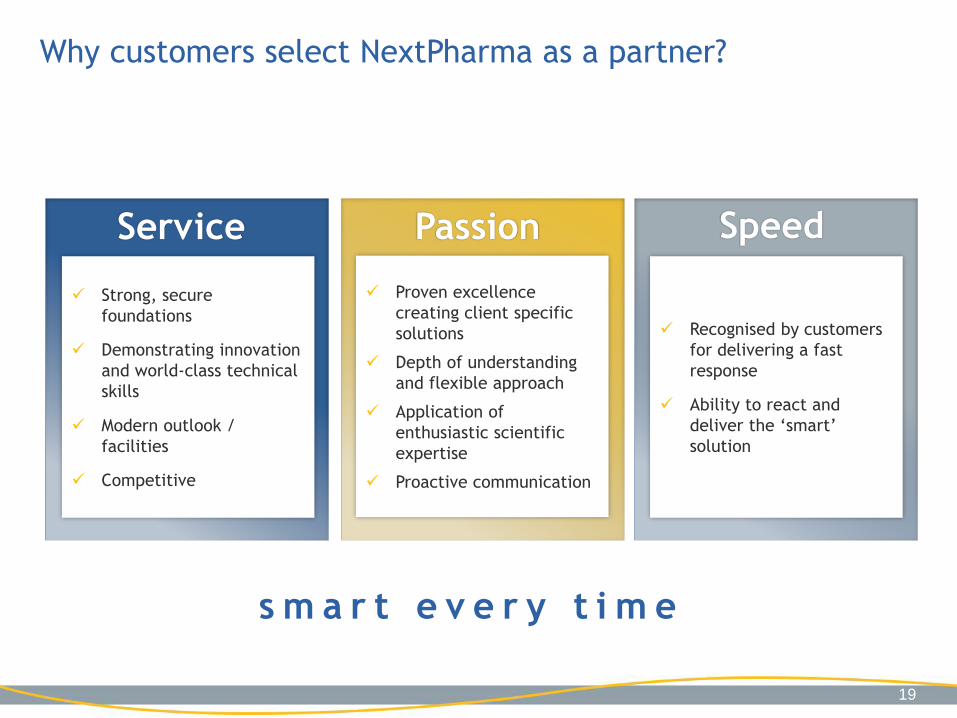

Why customers select NextPharma as a partner?

Service

Strong, secure

foundations

Demonstrating innovation

and world-class technical

skills

Modern outlook /

facilities

Competitive

Speed

Recognised by customers

for delivering a fast

response

Ability to react and

deliver the ‘smart’

solution

Passion

Proven excellence

creating client specific

solutions

Depth of understanding

and flexible approach

Application of

enthusiastic scientific

expertise

Proactive communication

s m a r t e v e r y t i m e

19

20

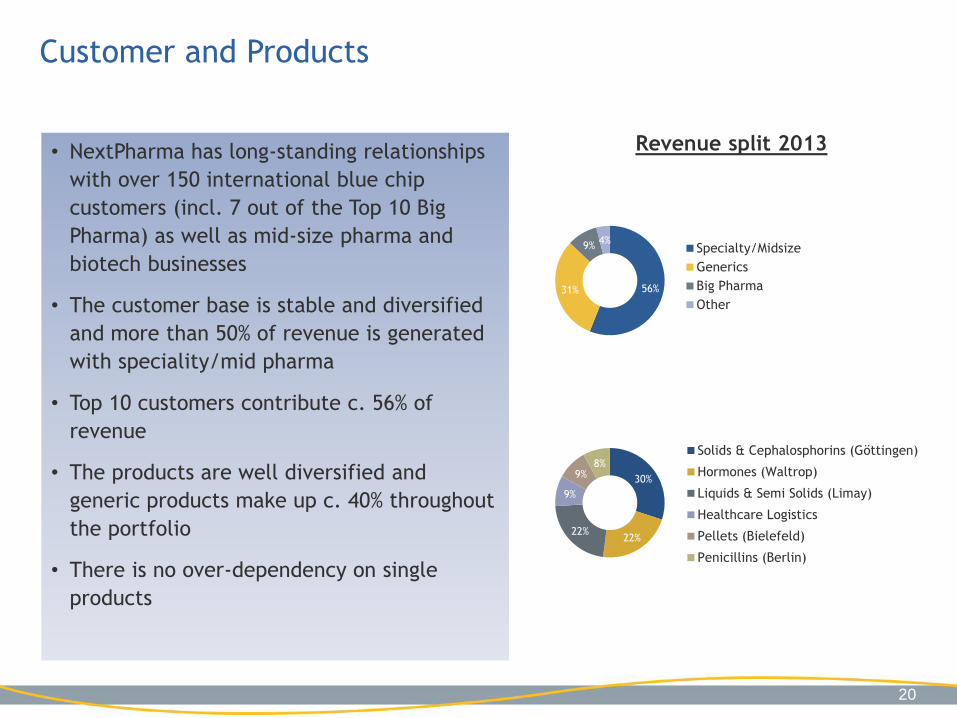

Customer and Products

Revenue split 2013

56%31%

9%4%

Specialty/Midsize

Generics

Big Pharma

Other

30%

22%22%

9%

9%8%

Solids & Cephalosphorins (Göttingen)

Hormones (Waltrop)

Liquids & Semi Solids (Limay)

Healthcare Logistics

Pellets (Bielefeld)

Penicillins (Berlin)

• NextPharma has long-standing relationships

with over 150 international blue chip

customers (incl. 7 out of the Top 10 Big

Pharma) as well as mid-size pharma and

biotech businesses

• The customer base is stable and diversified

and more than 50% of revenue is generated

with speciality/mid pharma

• Top 10 customers contribute c. 56% of

revenue

• The products are well diversified and

generic products make up c. 40% throughout

the portfolio

• There is no over-dependency on single

products

20

21

V. STRATEGIC OUTLOOK

21

22

Strategic Outlook (1/2)

Focus on core expertise

• Further focus on its core expertise in Contract Manufacturing Services, including specialised product

types/technologies (e.g. hormones, antibiotics, pelleting)

Focus on key strategic customers with long-term supply agreements

• Growth is expected to be in line with market average over the period, with growth from existing key

strategic customers. Revenue assumptions from new business wins for CMS are based on known projects

within the sales pipeline.

Strategic or customer-funded capital investment

• Focus on strategic or customer-funded capital investment to support growth and secure future business

22

23

Strategic Outlook (2/2)

FDA approvals to further penetrate the US market

• It is a strategic objective to upgrade the quality level in most of our sites to comply with FDA

regulations, in order to penetrate the US market (the largest Pharma market in the world) and to access

US customers bringing products to Europe.

Cost savings

• Drive cost savings through implementation of the on-going reorganisation programme

Improvement of efficiency and profitability

• Generate efficiency savings and improve profitability through rationalisation of low margin

customers/products/SKUs

23

24

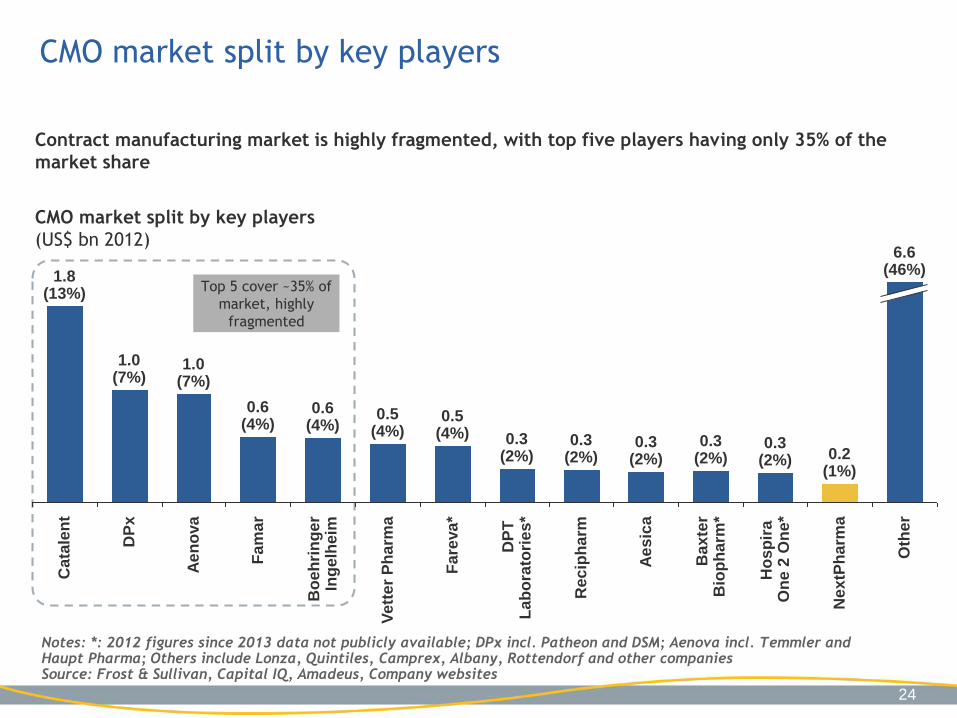

CMO market split by key players

24

Contract manufacturing market is highly fragmented, with top five players having only 35% of the

market share

CMO market split by key players

(US$ bn 2012)

Notes: *: 2012 figures since 2013 data not publicly available; DPx incl. Patheon and DSM; Aenova incl. Temmler and Haupt Pharma; Others include Lonza, Quintiles, Camprex, Albany, Rottendorf and other companiesSource: Frost & Sullivan, Capital IQ, Amadeus, Company websites

0.2(1%)

Nex

tPh

arm

a

6.6(46%)

Oth

er

Ho

sp

ira

O

ne

2 O

ne

*

0.3(2%)

Bax

ter

Bio

ph

arm

*

0.3(2%)

Ae

sic

a

0.3(2%)

Rec

iph

arm

0.3(2%)

DP

T

La

bo

rato

rie

s*

0.3(2%)

Fa

reva

*

0.5(4%)

Ve

tte

r P

ha

rma

0.5(4%)

Bo

eh

rin

ge

rIn

ge

lhe

im

0.6(4%)

Fa

ma

r

0.6(4%)

Ae

no

va

1.0(7%)

DP

x

1.0(7%)

Cata

len

t

1.8(13%)

Top 5 cover ~35% of

market, highly

fragmented

25

The CMO market is experiencing rapid consolidation

25

CMOs are following different M&A strategies. This leads to a significant M&A activity which results

in increasing acquisition multiples.

Key Transaction themes

1. Scale and market Share – selected transactions include:

Acquisition of Meda’s New Jersey facilities to add additional cold storage and a larger analytical laboratory

(Sep 14)

Acquisition of Temmler to establish the groups position as a European market leader and add new dosage form

capabilities/service segments e.g., clinical trial materials, distribution logistics and licensing (Oct 12)

2. New capabilities and service segments – selected transactions include:

Acquisition of Aesica provides horizontal integration in oral delivery and vertical integration in drug

formulation and finished dose manufacturing (Sep 14)

Acquisition of Corvette Group strengthen capabilities in lyophilisation, specifically handling hormones in both

vials and ampoules (Aug 14)

Acquisition of Contract Packaging Resources to enhance its global packaging services (Sep 14) and Haupt

Pharma in line with adding capability to manufacture steriles and other complex products, such as hormones,

antibiotics and cytostatics (Oct 13)

3. Increased focus – selected transactions include:

Divestment of clinical trial supply and packaging services to Bellwyck (Sep 12)

Divestment of commercial pharmaceutical packaging operations to Frazier Healthcare, creating PCI (Jun 12)

26

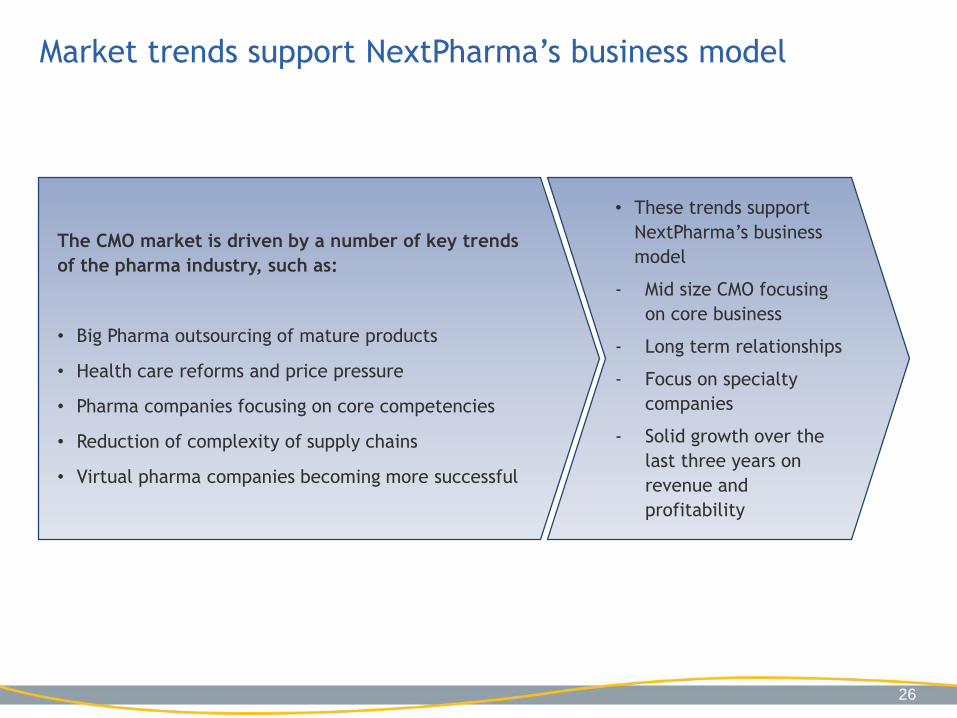

Market trends support NextPharma’s business model

The CMO market is driven by a number of key trends

of the pharma industry, such as:

• Big Pharma outsourcing of mature products

• Health care reforms and price pressure

• Pharma companies focusing on core competencies

• Reduction of complexity of supply chains

• Virtual pharma companies becoming more successful

• These trends support

NextPharma’s business

model

- Mid size CMO focusing

on core business

- Long term relationships

- Focus on specialty

companies

- Solid growth over the

last three years on

revenue and

profitability

26

27

Q&AName of the Presenter

27