notification no. 30/2012-st dated 20 th june 2012 as amended by notification no. 45/2012-st dated 7...

TRANSCRIPT

Notification no. 30/2012-ST dated 20th June 2012 as amended by notification no. 45/2012-ST dated 7th August 2012

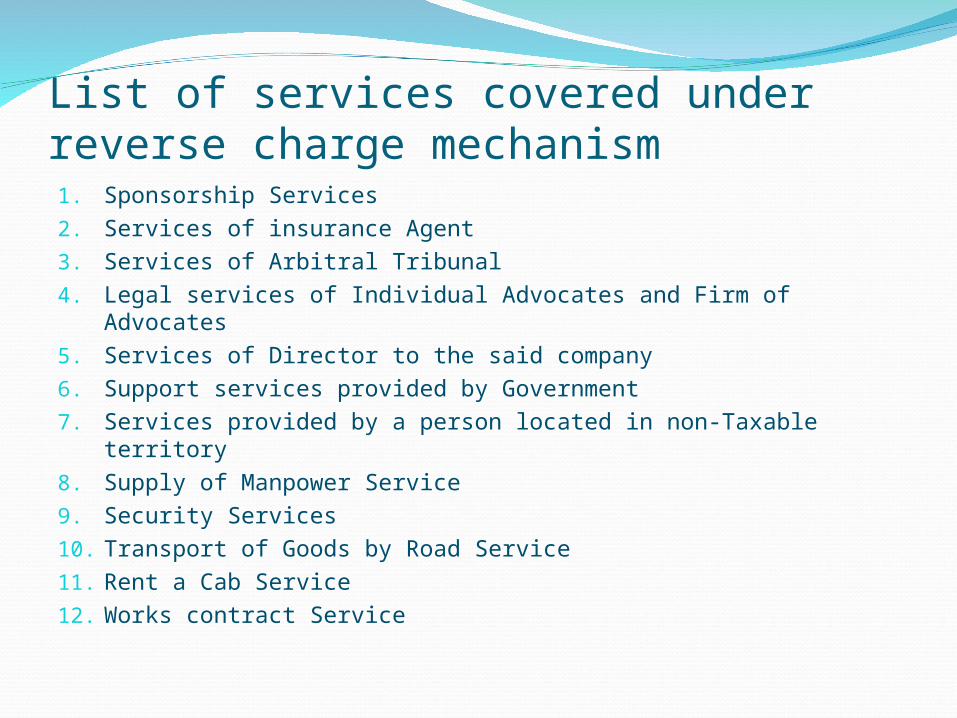

List of services covered under reverse charge mechanism1. Sponsorship Services2. Services of insurance Agent3. Services of Arbitral Tribunal4. Legal services of Individual Advocates and Firm of Advocates5. Services of Director to the said company6. Support services provided by Government7. Services provided by a person located in non-Taxable territory8. Supply of Manpower Service9. Security Services10. Transport of Goods by Road Service11. Rent a Cab Service12. Works contract Service

1. Sponsorship Services

Conditions

Service Provider – Any Person Service Receiver – Body Corporate or Partnership Firm

located in Taxable territory

Amount of Service Tax payable by:

Service provider – NIL Service Receiver – 100%

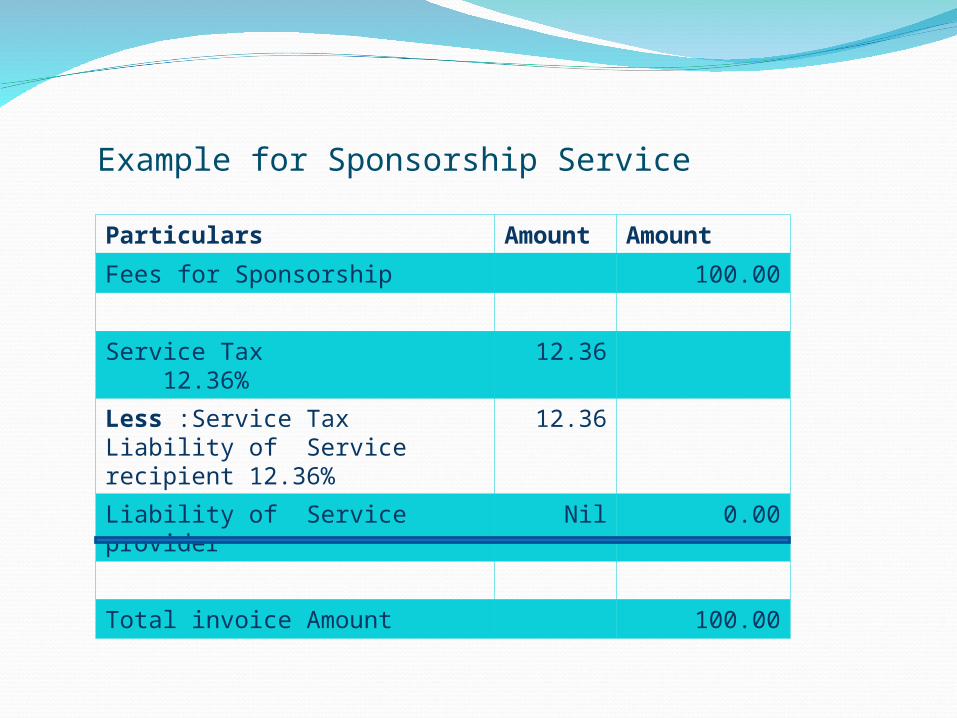

Example for Sponsorship Service

Particulars Amount Amount

Fees for Sponsorship 100.00

Service Tax 12.36% 12.36

Less :Service Tax Liability of Service recipient 12.36%

12.36

Liability of Service provider Nil 0.00

Total invoice Amount 100.00

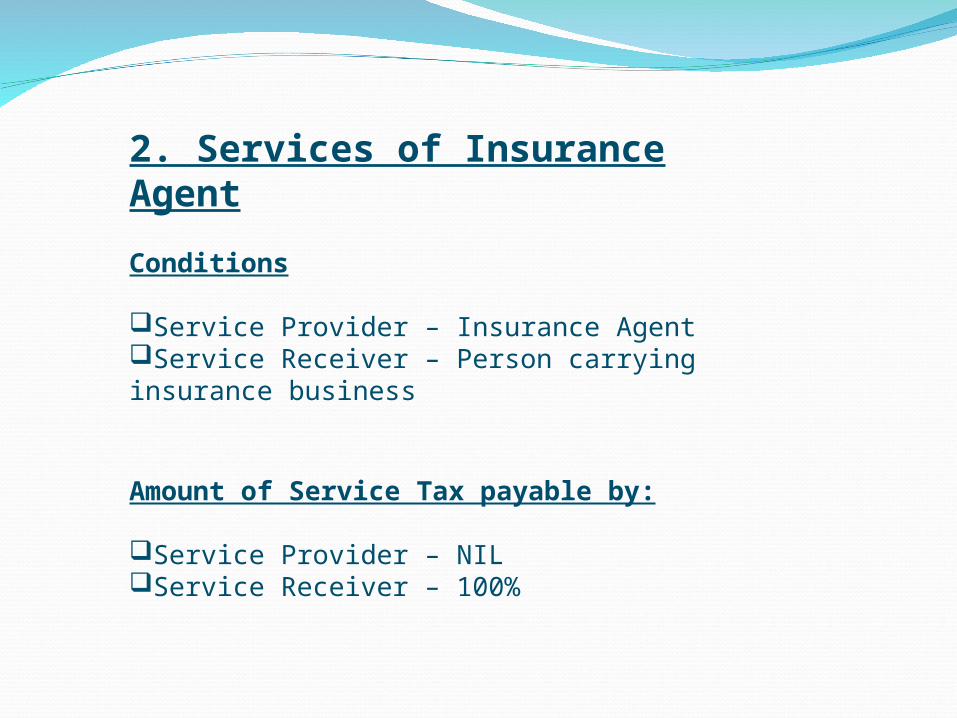

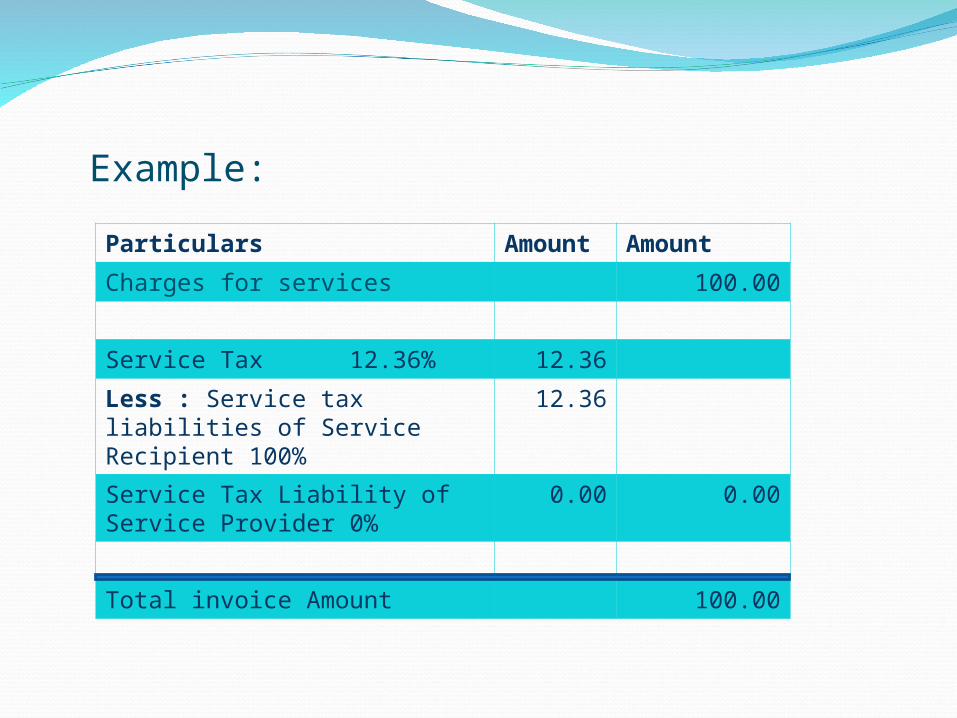

2. Services of Insurance Agent

Conditions

Service Provider – Insurance AgentService Receiver – Person carrying insurance business

Amount of Service Tax payable by:

Service Provider – NILService Receiver – 100%

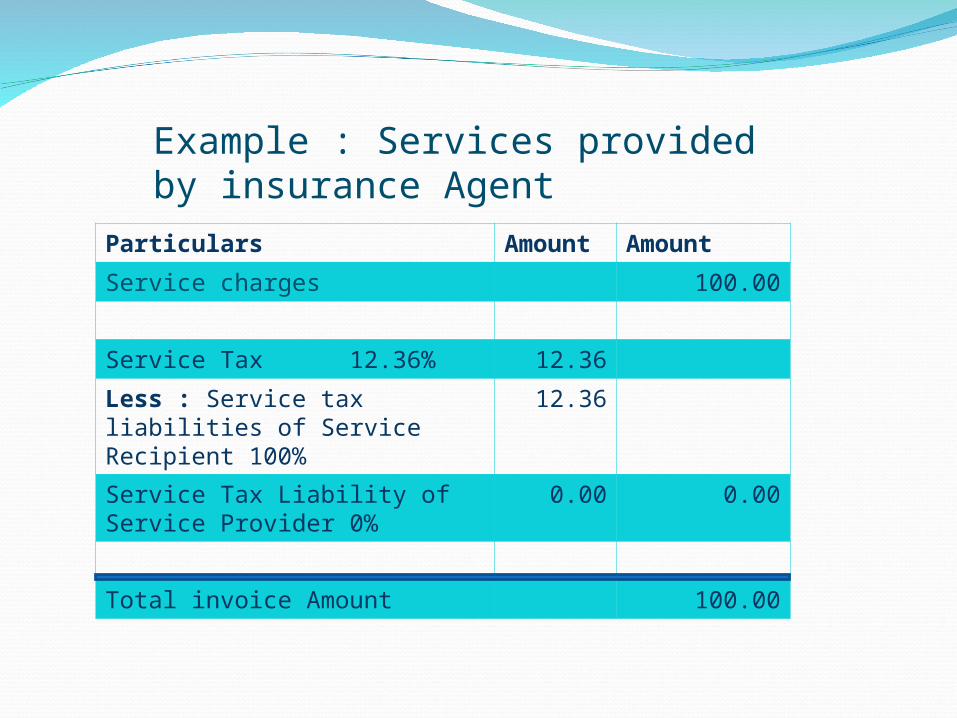

Example : Services provided by insurance Agent

Particulars Amount Amount

Service charges 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

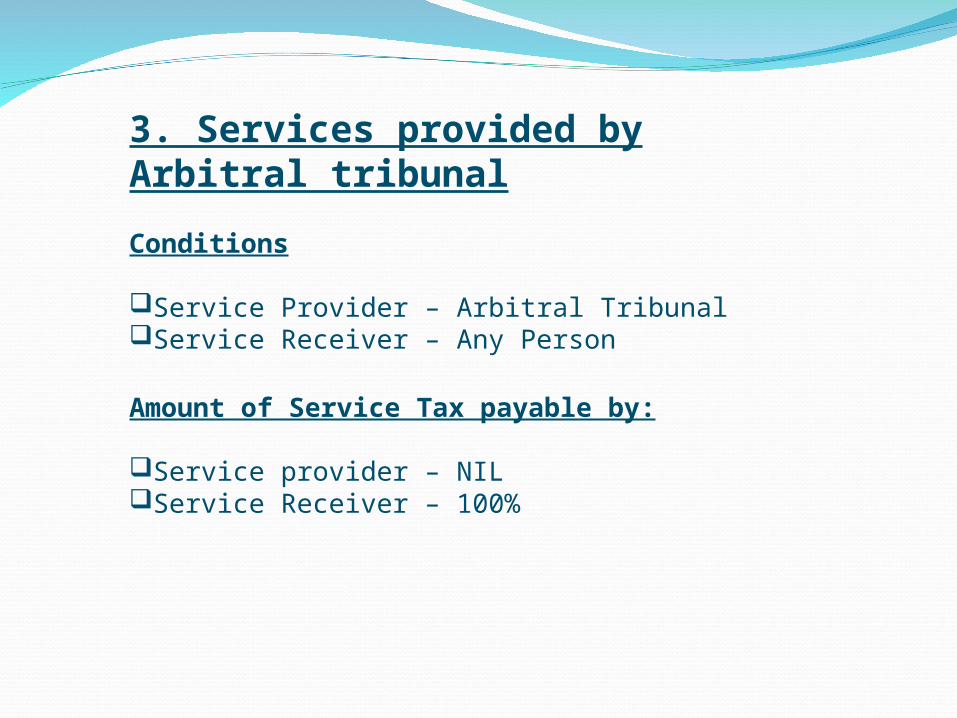

3. Services provided by Arbitral tribunal

Conditions

Service Provider – Arbitral TribunalService Receiver – Any Person

Amount of Service Tax payable by:

Service provider – NILService Receiver – 100%

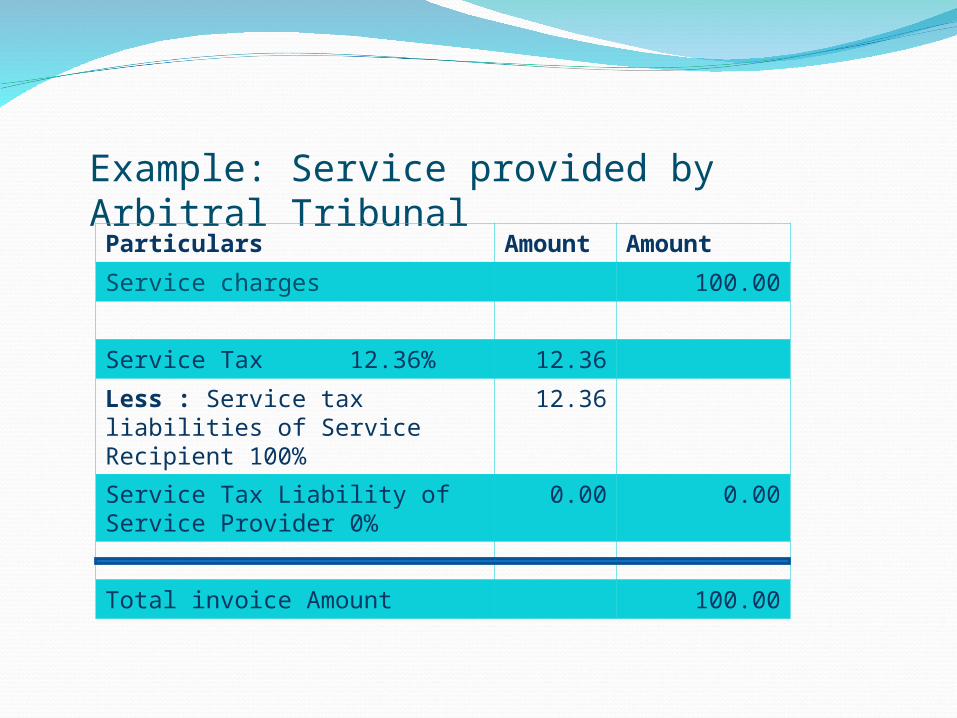

Example: Service provided by Arbitral Tribunal

Particulars Amount Amount

Service charges 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

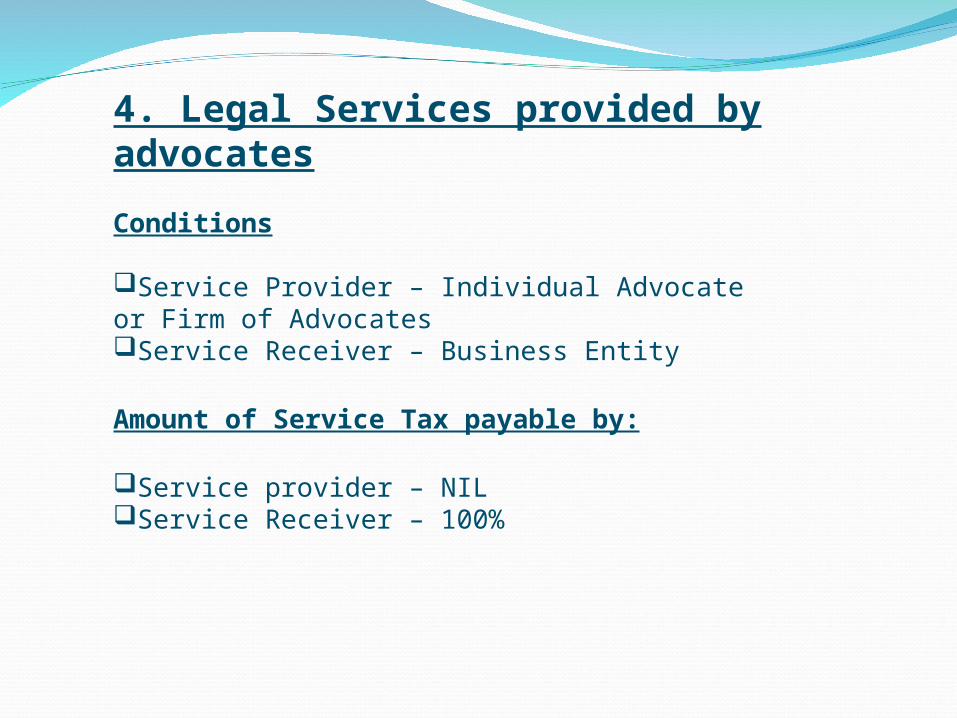

4. Legal Services provided by advocates

Conditions

Service Provider – Individual Advocate or Firm of AdvocatesService Receiver – Business Entity

Amount of Service Tax payable by:

Service provider – NILService Receiver – 100%

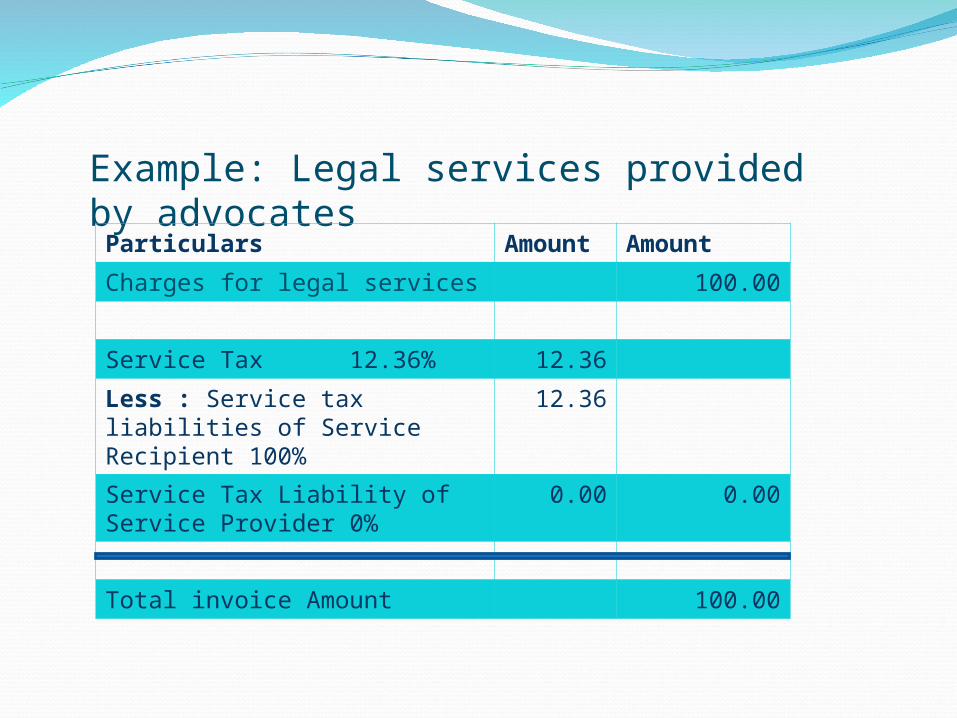

Example: Legal services provided by advocates

Particulars Amount Amount

Charges for legal services 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

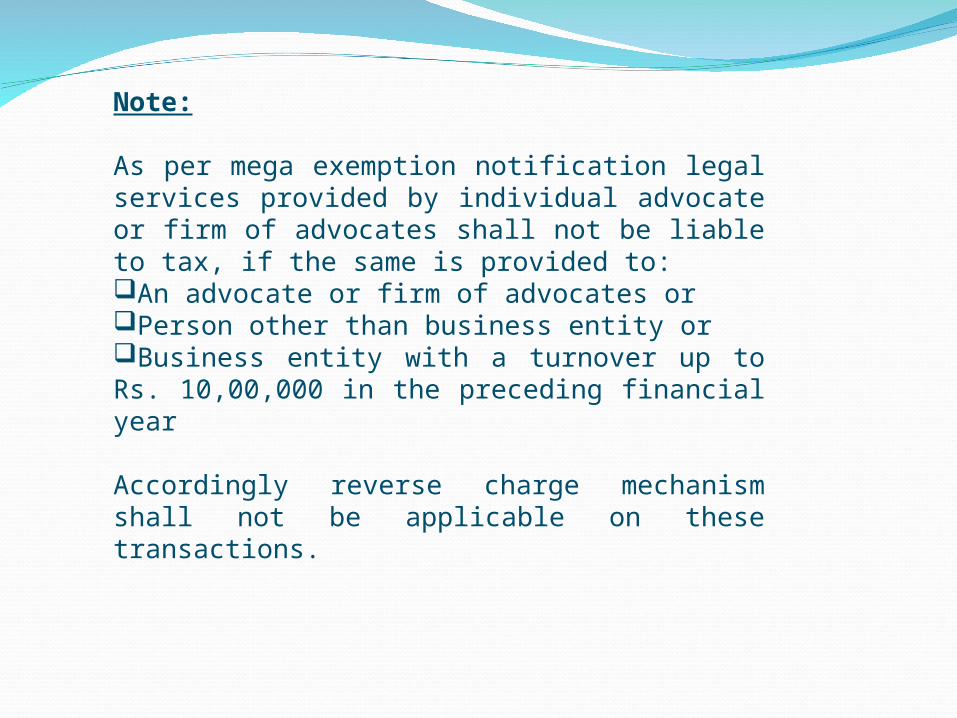

Note:

As per mega exemption notification legal services provided by individual advocate or firm of advocates shall not be liable to tax, if the same is provided to:An advocate or firm of advocates orPerson other than business entity orBusiness entity with a turnover up to Rs. 10,00,000 in the preceding financial year

Accordingly reverse charge mechanism shall not be applicable on these transactions.

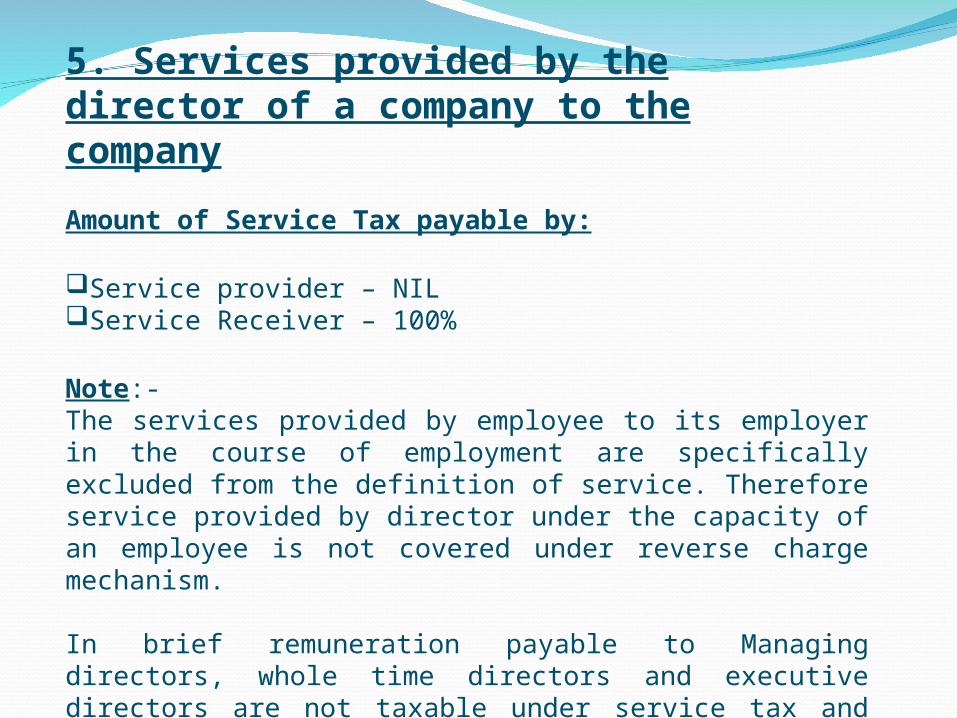

5. Services provided by the director of a company to the company

Amount of Service Tax payable by:

Service provider – NILService Receiver – 100%

Note:-The services provided by employee to its employer in the course of employment are specifically excluded from the definition of service. Therefore service provided by director under the capacity of an employee is not covered under reverse charge mechanism.

In brief remuneration payable to Managing directors, whole time directors and executive directors are not taxable under service tax and the services provided by part-time/ Expert/ Independent/ Nominee directors are liable to service tax and reverse charge mechanism is applicable on the same.

Example:

Particulars Amount Amount

Charges for services 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

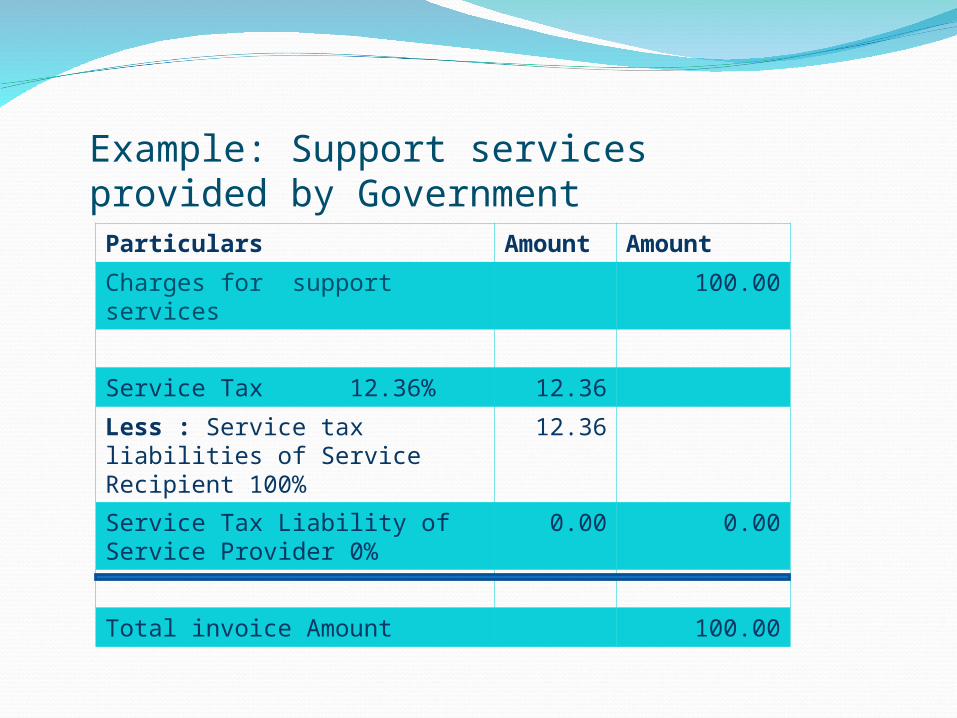

6. Support Services provided by Government

Conditions

Service Provider – Government or Local AuthorityService Receiver – Business Entity

Nature of Service – Support Services, Excluding:

1.Renting of Immovable property services,

2.services by the Department of Posts by way of speed post, express parcel post, life insurance and agency services

3.services in relation to an aircraft or a vessel

4.transport of goods or passengers.

Definition of Support Services:

“support services" means infrastructural, operational, administrative, logistic, marketing or any other support of any kind comprising functions that entities carry out in ordinary course of operations and shall include advertisement and promotion, construction or works contract, renting of immovable property, security, testing and analysis.

Amount of Service Tax payable by:

Service Provider – NilService Receiver – 100%

Example: Support services provided by Government

Particulars Amount Amount

Charges for support services 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

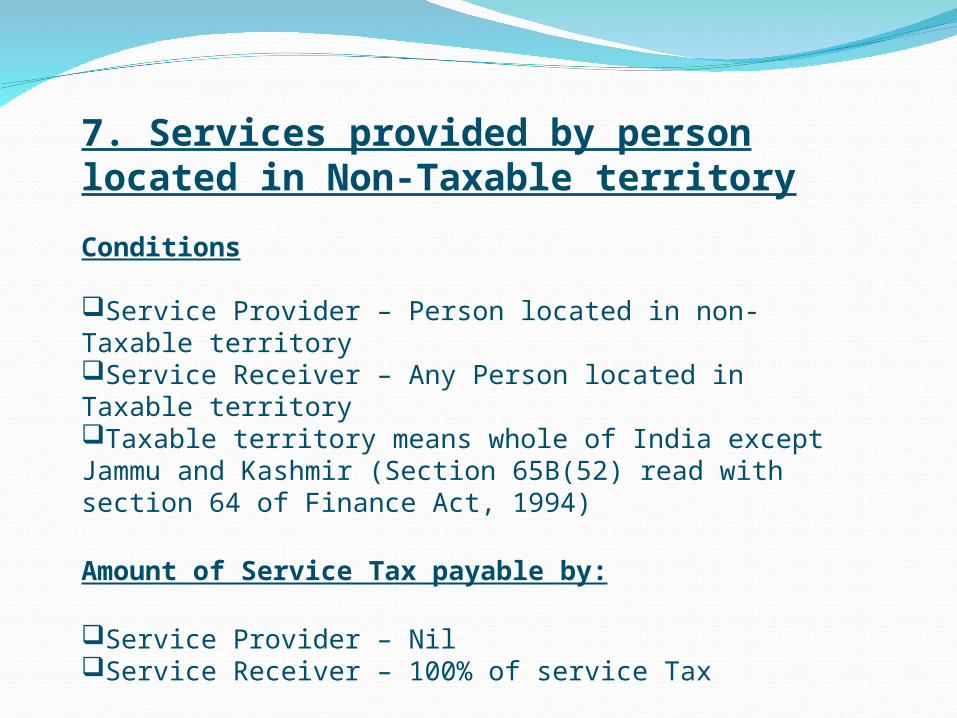

7. Services provided by person located in Non-Taxable territory

Conditions

Service Provider – Person located in non-Taxable territoryService Receiver – Any Person located in Taxable territoryTaxable territory means whole of India except Jammu and Kashmir (Section 65B(52) read with section 64 of Finance Act, 1994)

Amount of Service Tax payable by:

Service Provider – NilService Receiver – 100% of service Tax

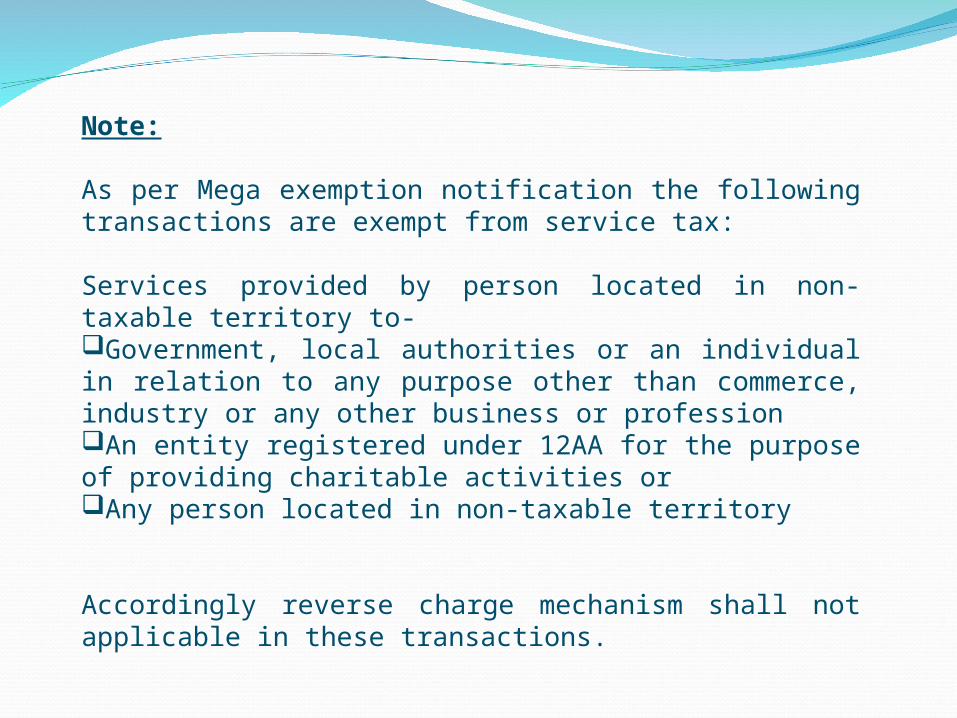

Note:

As per Mega exemption notification the following transactions are exempt from service tax:

Services provided by person located in non-taxable territory to-Government, local authorities or an individual in relation to any purpose other than commerce, industry or any other business or professionAn entity registered under 12AA for the purpose of providing charitable activities orAny person located in non-taxable territory

Accordingly reverse charge mechanism shall not applicable in these transactions.

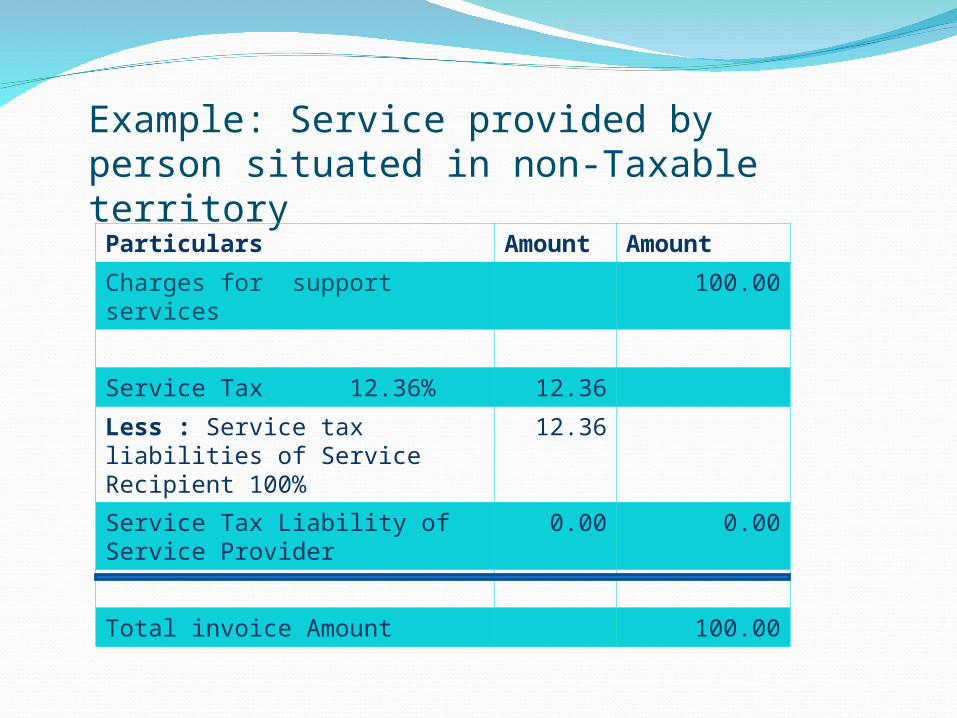

Example: Service provided by person situated in non-Taxable territory

Particulars Amount Amount

Charges for support services 100.00

Service Tax 12.36% 12.36

Less : Service tax liabilities of Service Recipient 100%

12.36

Service Tax Liability of Service Provider

0.00 0.00

Total invoice Amount 100.00

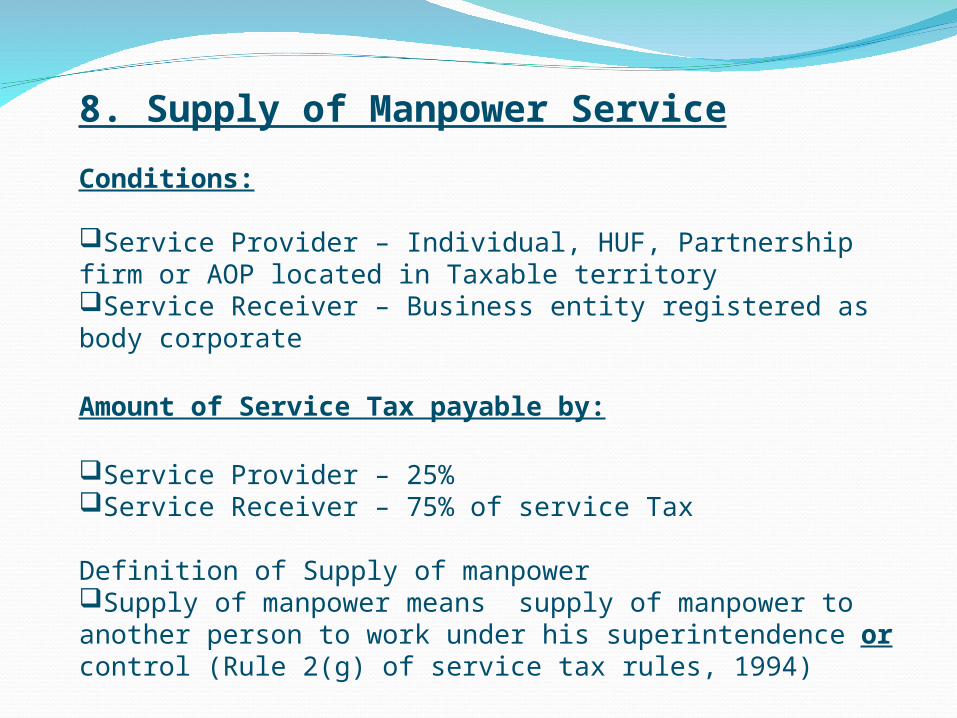

8. Supply of Manpower Service

Conditions:

Service Provider – Individual, HUF, Partnership firm or AOP located in Taxable territoryService Receiver – Business entity registered as body corporate

Amount of Service Tax payable by:

Service Provider – 25%Service Receiver – 75% of service Tax

Definition of Supply of manpowerSupply of manpower means supply of manpower to another person to work under his superintendence or control (Rule 2(g) of service tax rules, 1994)

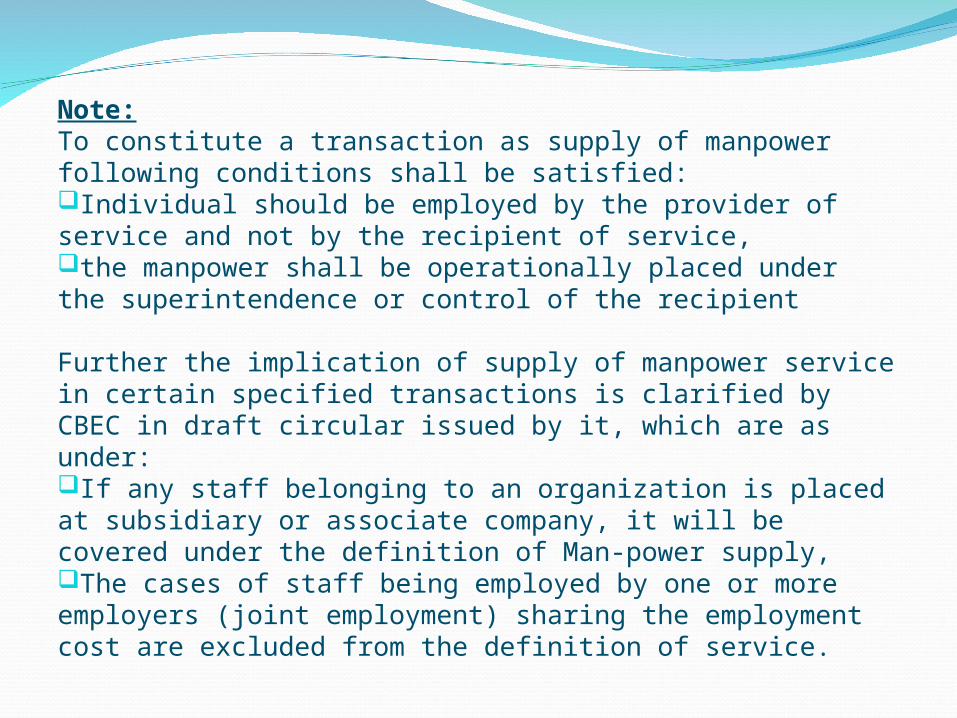

Note:To constitute a transaction as supply of manpower following conditions shall be satisfied:Individual should be employed by the provider of service and not by the recipient of service,the manpower shall be operationally placed under the superintendence or control of the recipient

Further the implication of supply of manpower service in certain specified transactions is clarified by CBEC in draft circular issued by it, which are as under:If any staff belonging to an organization is placed at subsidiary or associate company, it will be covered under the definition of Man-power supply,The cases of staff being employed by one or more employers (joint employment) sharing the employment cost are excluded from the definition of service.

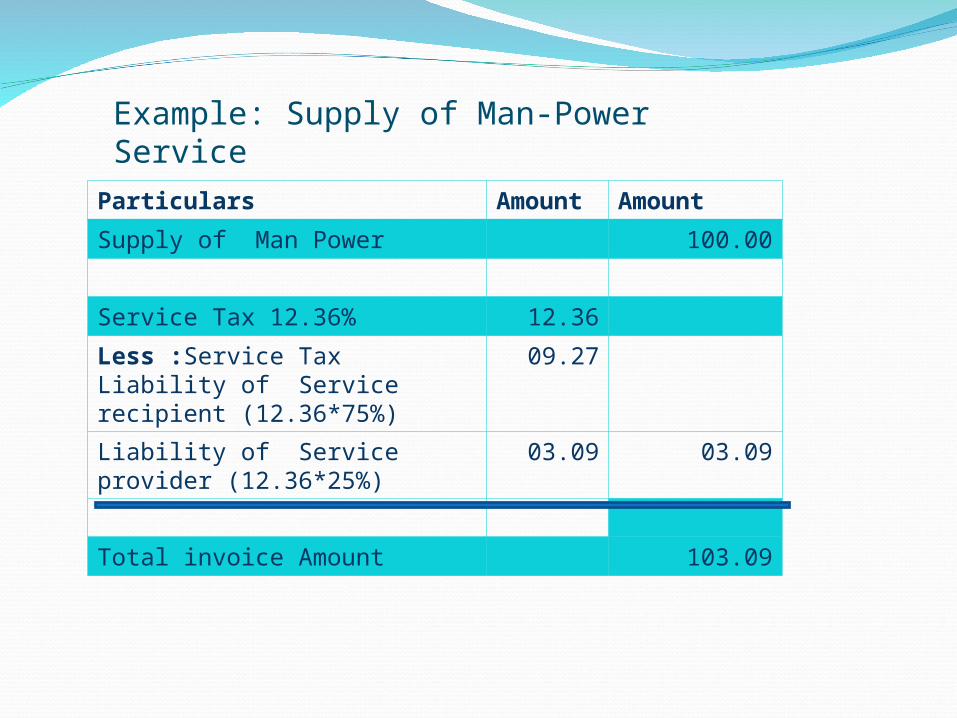

Example: Supply of Man-Power Service

Particulars Amount Amount

Supply of Man Power 100.00

Service Tax 12.36% 12.36

Less :Service Tax Liability of Service recipient (12.36*75%)

09.27

Liability of Service provider (12.36*25%)

03.09 03.09

Total invoice Amount 103.09

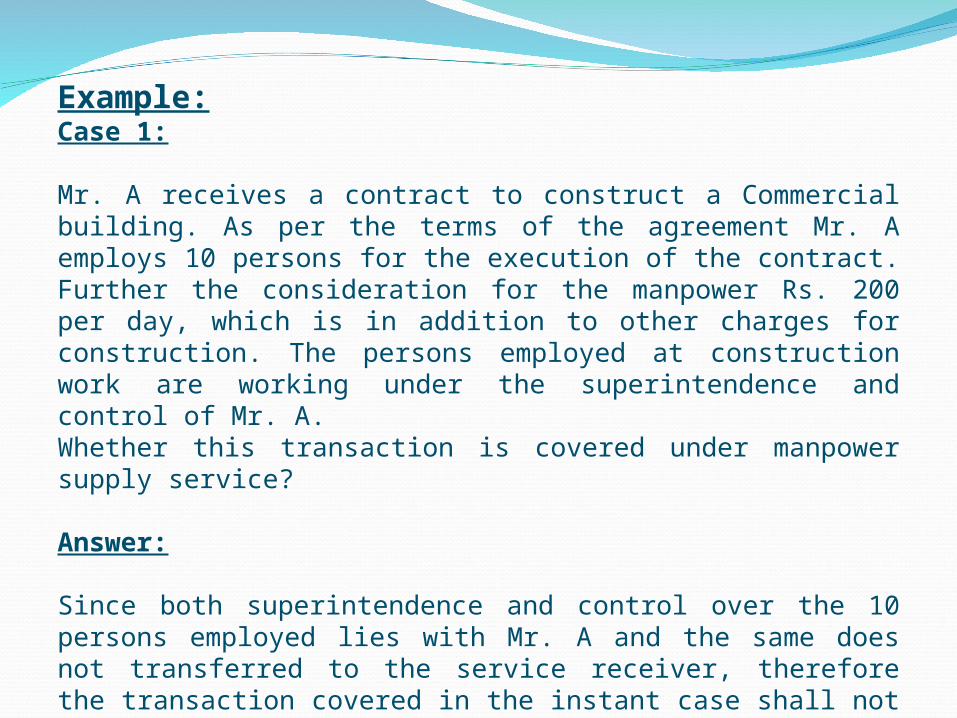

Example:Case 1:

Mr. A receives a contract to construct a Commercial building. As per the terms of the agreement Mr. A employs 10 persons for the execution of the contract. Further the consideration for the manpower Rs. 200 per day, which is in addition to other charges for construction. The persons employed at construction work are working under the superintendence and control of Mr. A. Whether this transaction is covered under manpower supply service?

Answer:

Since both superintendence and control over the 10 persons employed lies with Mr. A and the same does not transferred to the service receiver, therefore the transaction covered in the instant case shall not amount to supply of manpower. Accordingly reverse charge mechanism shall not applicable on the same.

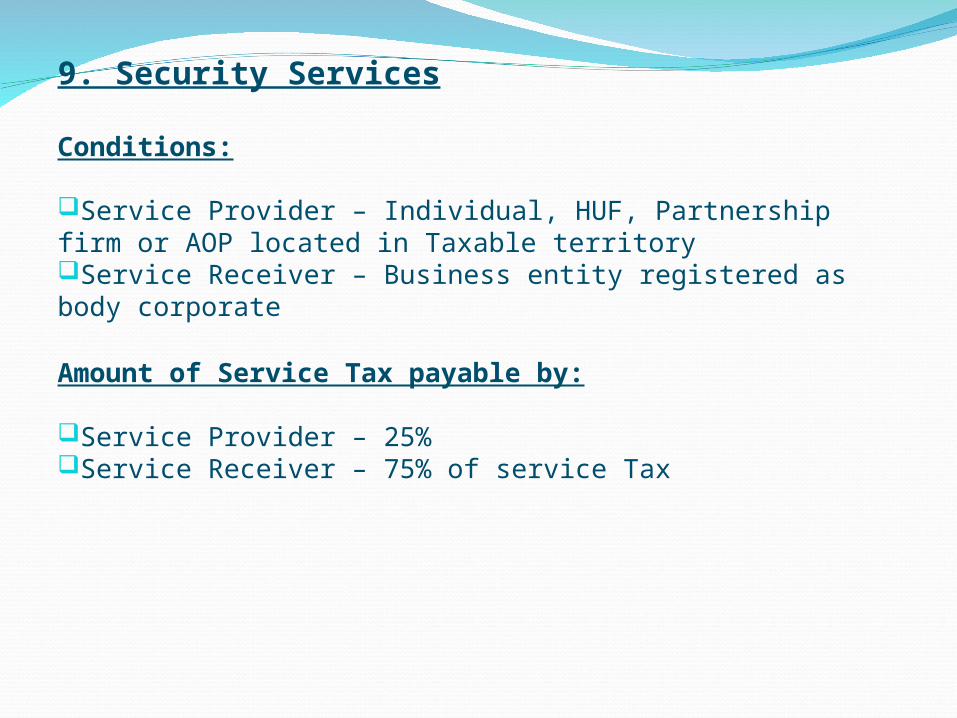

9. Security Services

Conditions:

Service Provider – Individual, HUF, Partnership firm or AOP located in Taxable territoryService Receiver – Business entity registered as body corporate

Amount of Service Tax payable by:

Service Provider – 25%Service Receiver – 75% of service Tax

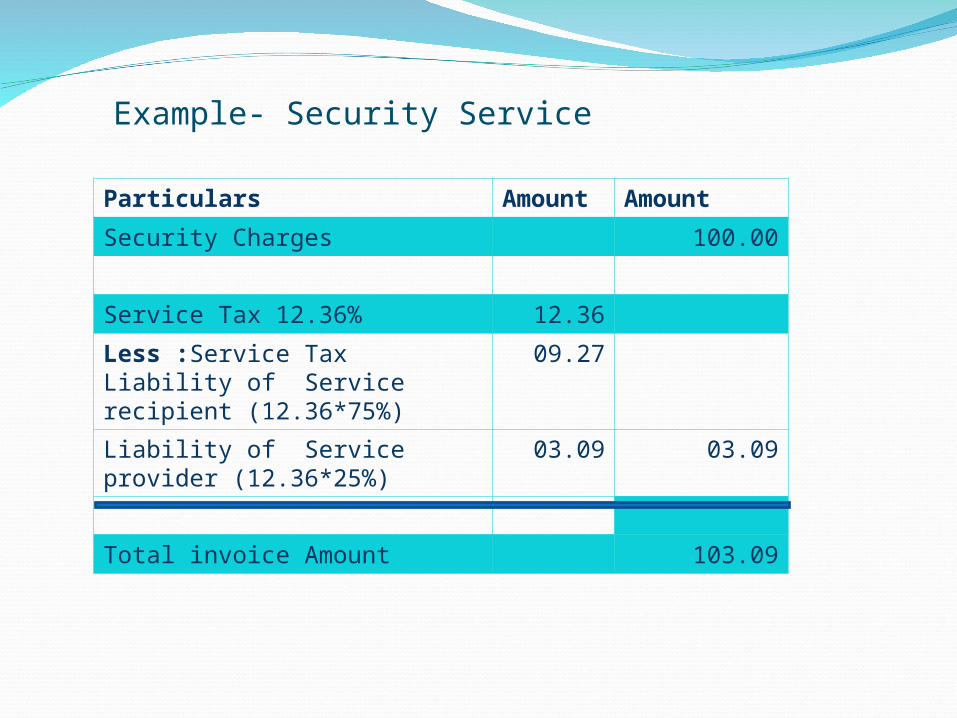

Example- Security Service

Particulars Amount Amount

Security Charges 100.00

Service Tax 12.36% 12.36

Less :Service Tax Liability of Service recipient (12.36*75%)

09.27

Liability of Service provider (12.36*25%)

03.09 03.09

Total invoice Amount 103.09

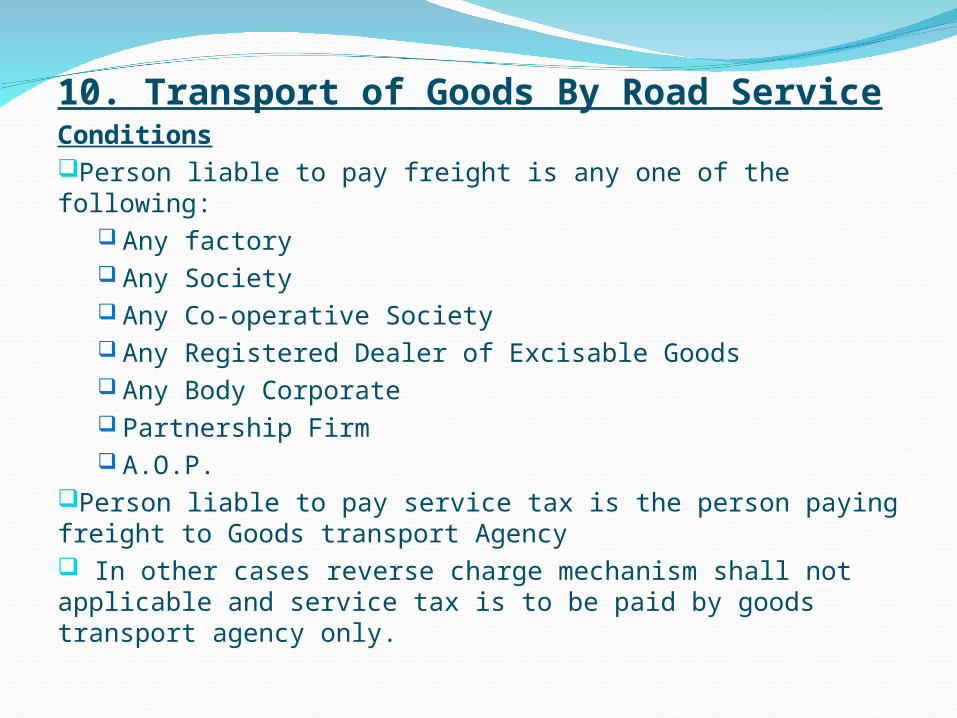

10. Transport of Goods By Road ServiceConditionsPerson liable to pay freight is any one of the following:

Any factory Any Society Any Co-operative Society Any Registered Dealer of Excisable Goods Any Body Corporate Partnership Firm A.O.P.

Person liable to pay service tax is the person paying freight to Goods transport Agency In other cases reverse charge mechanism shall not applicable and service tax is to be paid by goods transport agency only.

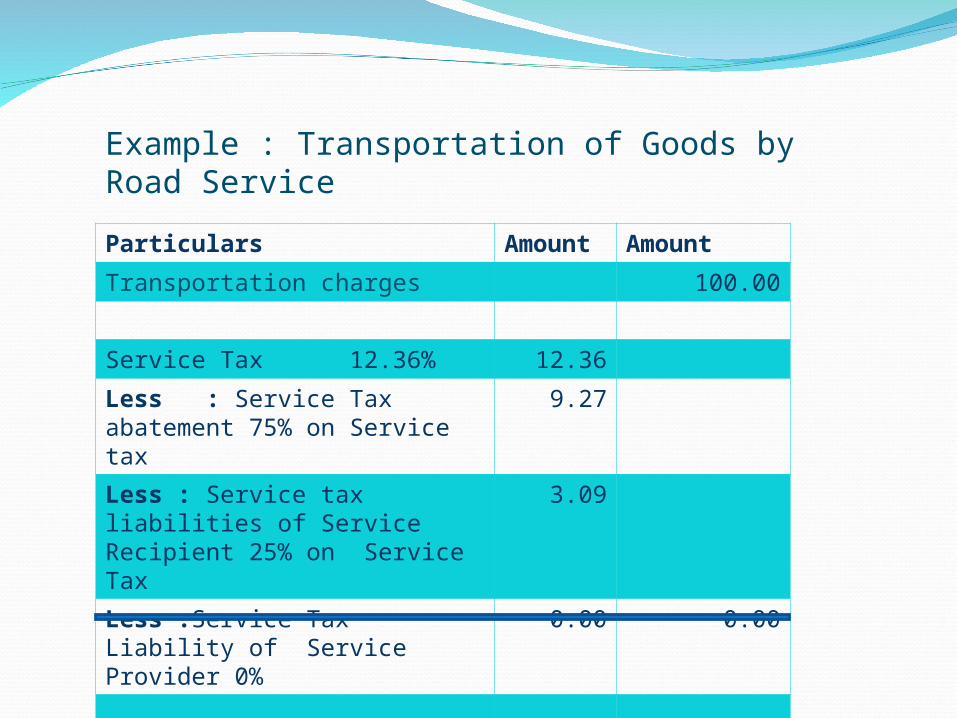

Example : Transportation of Goods by Road Service

Particulars Amount Amount

Transportation charges 100.00

Service Tax 12.36% 12.36

Less : Service Tax abatement 75% on Service tax

9.27

Less : Service tax liabilities of Service Recipient 25% on Service Tax

3.09

Less :Service Tax Liability of Service Provider 0%

0.00 0.00

Total invoice Amount 100.00

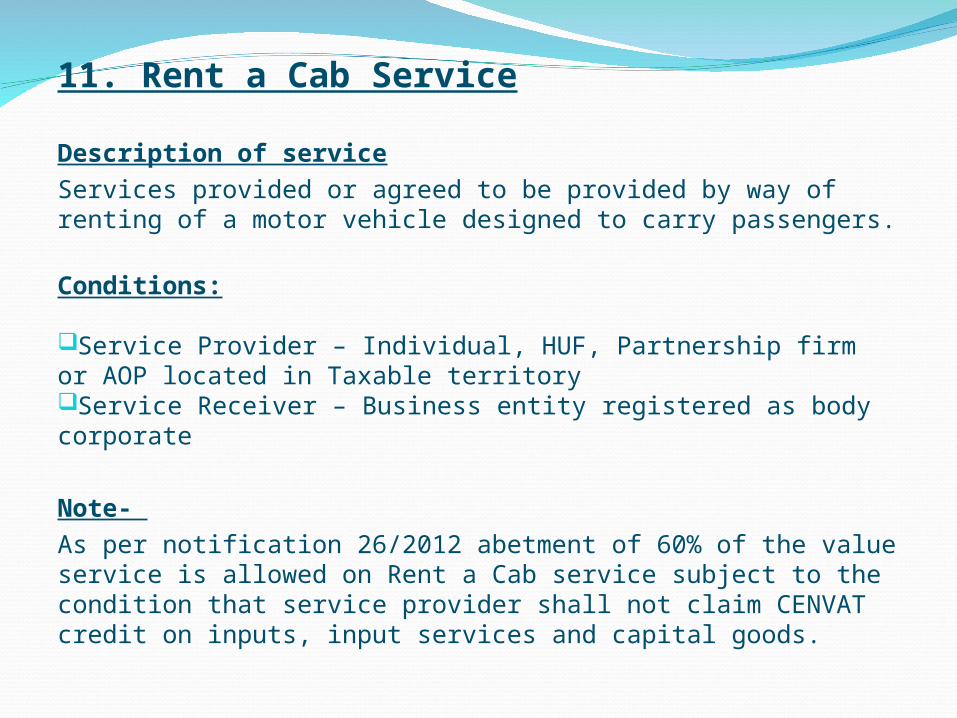

11. Rent a Cab Service

Description of serviceServices provided or agreed to be provided by way of renting of a motor vehicle designed to carry passengers.

Conditions:

Service Provider – Individual, HUF, Partnership firm or AOP located in Taxable territoryService Receiver – Business entity registered as body corporate

Note- As per notification 26/2012 abetment of 60% of the value service is allowed on Rent a Cab service subject to the condition that service provider shall not claim CENVAT credit on inputs, input services and capital goods.

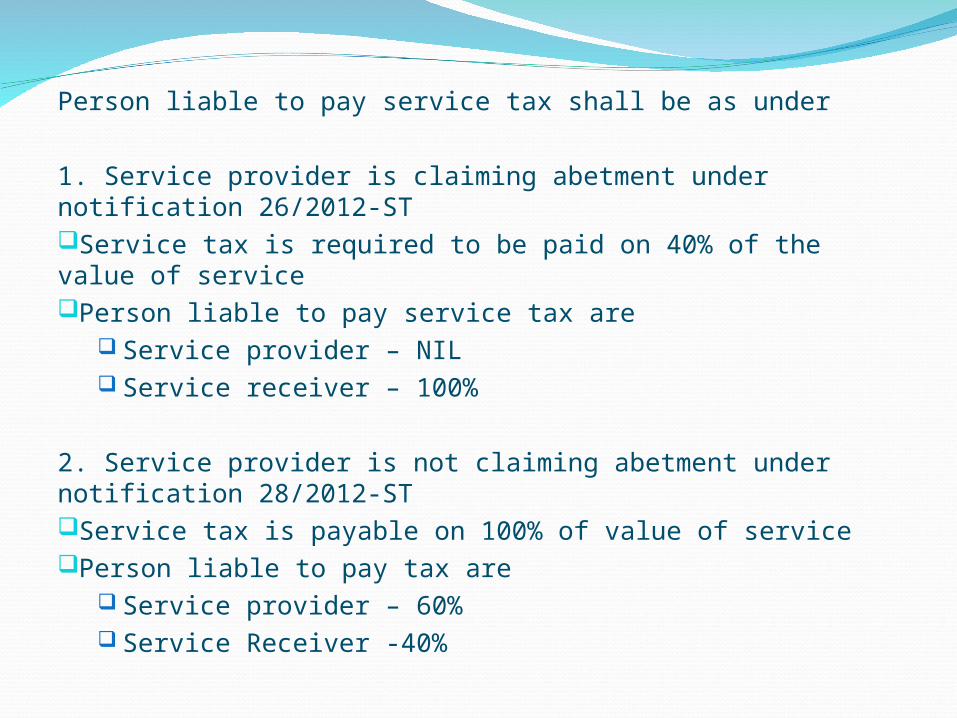

Person liable to pay service tax shall be as under

1. Service provider is claiming abetment under notification 26/2012-STService tax is required to be paid on 40% of the value of servicePerson liable to pay service tax are

Service provider – NIL Service receiver – 100%

2. Service provider is not claiming abetment under notification 28/2012-STService tax is payable on 100% of value of servicePerson liable to pay tax are

Service provider – 60% Service Receiver -40%

Particulars Amount Amount

Rent Charges 100.00

Service Tax 12.36% 12.36

Less : Service Tax Abatement 7.42 0.00

Less :Service Tax Liability of Service recipient 4.94%

4.94

Less : Liability of Service provider 0.00 0.00

Total invoice Amount 100.00

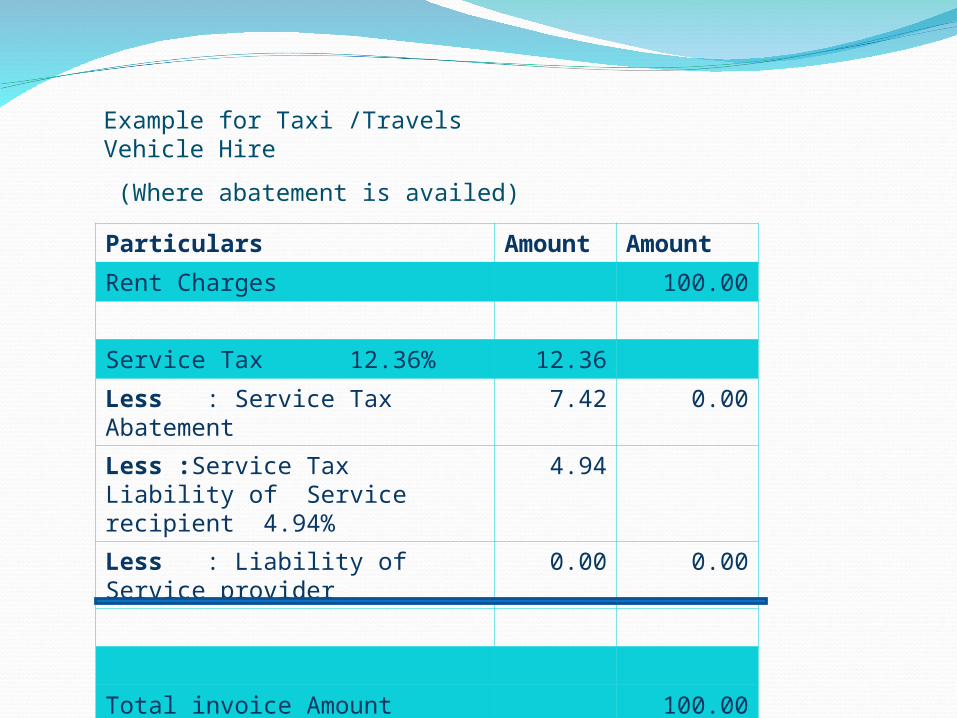

Example for Taxi /Travels Vehicle Hire

(Where abatement is availed)

Particulars Amount Amount

Rent Charges 100.00

Service Tax 12.36% 12.36

Less :Service Tax Liability of Service recipient (12.36*40%)

4.94

Liability of Service provider (12.36*60%)

7.42 7.42

Total invoice Amount 107.42

Example for Taxi /Travels Vehicle Hire

(Where abatement is not availed)

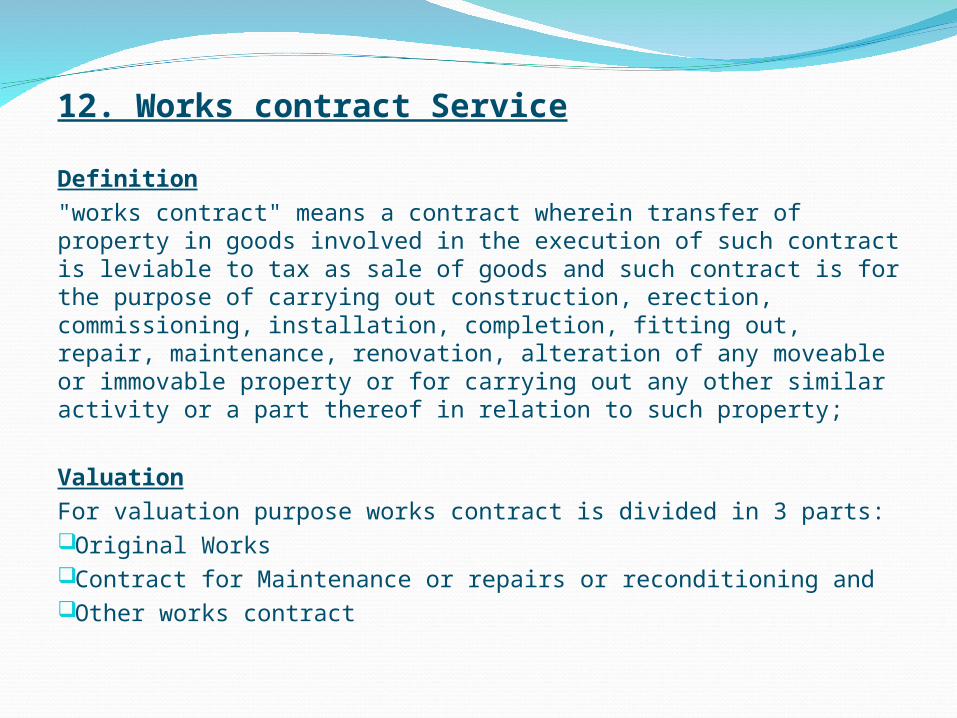

12. Works contract Service

Definition"works contract" means a contract wherein transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods and such contract is for the purpose of carrying out construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, alteration of any moveable or immovable property or for carrying out any other similar activity or a part thereof in relation to such property;

ValuationFor valuation purpose works contract is divided in 3 parts:Original WorksContract for Maintenance or repairs or reconditioning andOther works contract

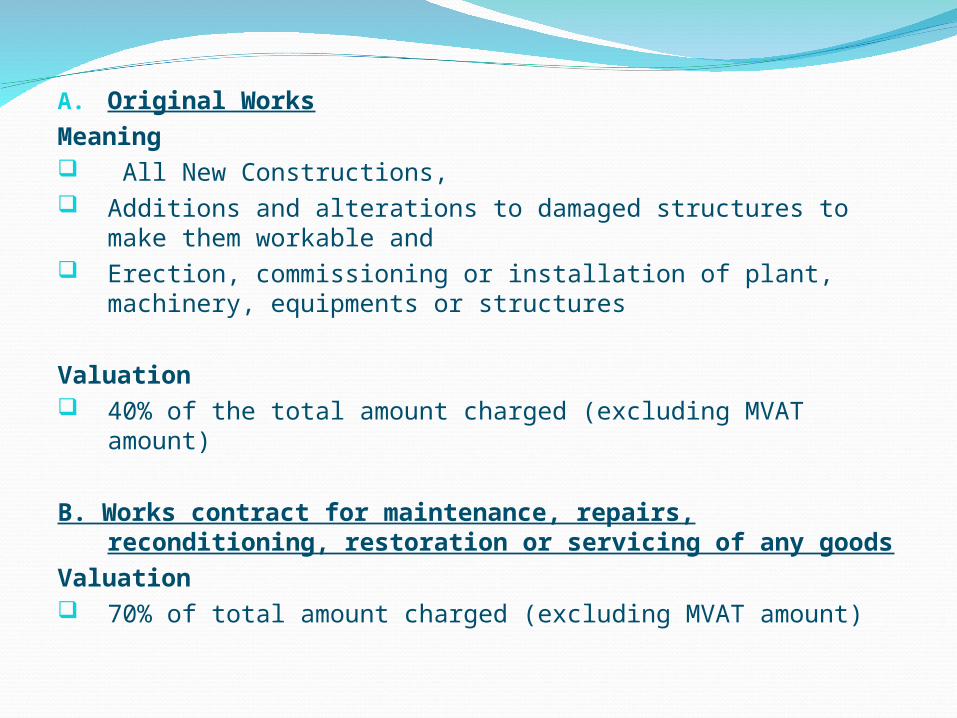

A. Original WorksMeaning All New Constructions, Additions and alterations to damaged structures to make them workable

and Erection, commissioning or installation of plant, machinery, equipments

or structures

Valuation 40% of the total amount charged (excluding MVAT amount)

B. Works contract for maintenance, repairs, reconditioning, restoration or servicing of any goods

Valuation 70% of total amount charged (excluding MVAT amount)

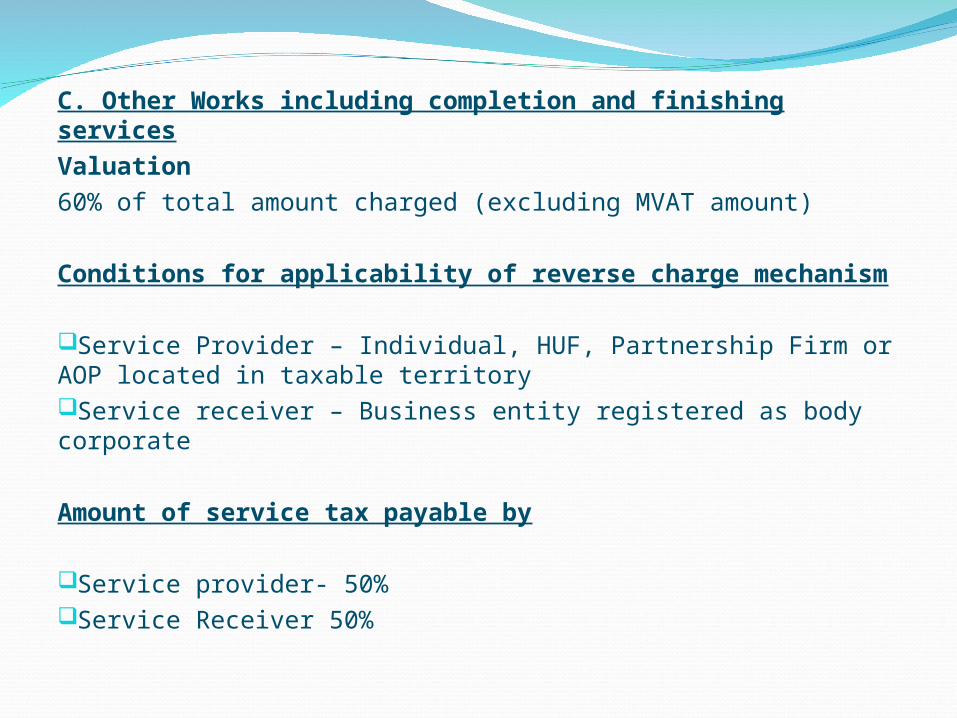

C. Other Works including completion and finishing servicesValuation60% of total amount charged (excluding MVAT amount)

Conditions for applicability of reverse charge mechanism

Service Provider – Individual, HUF, Partnership Firm or AOP located in taxable territoryService receiver – Business entity registered as body corporate

Amount of service tax payable by

Service provider- 50%Service Receiver 50%

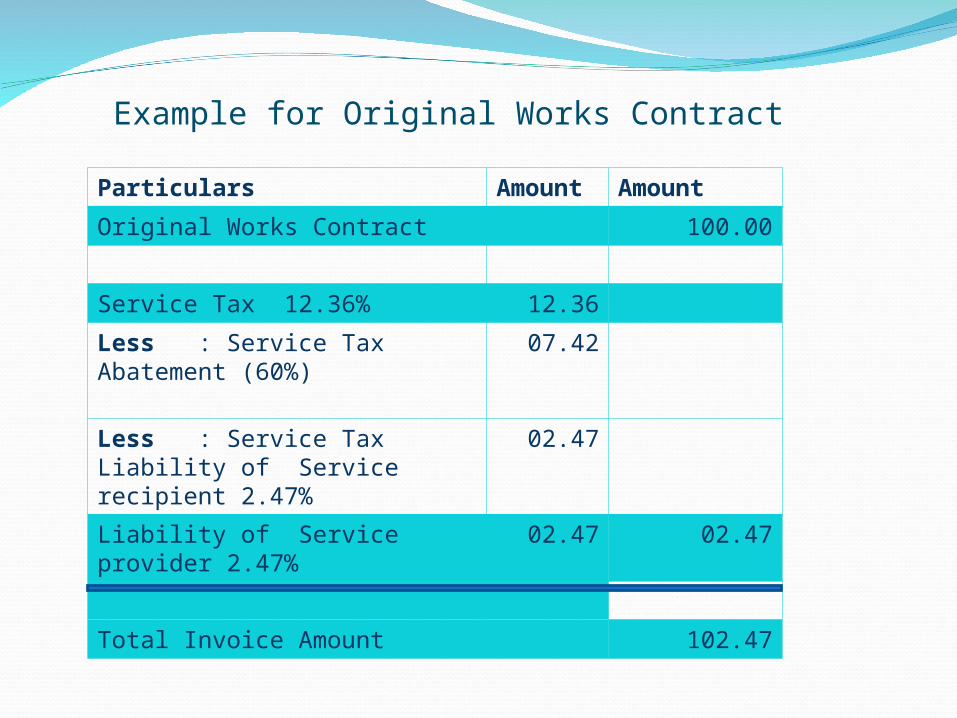

Example for Original Works Contract

Particulars Amount Amount

Original Works Contract 100.00

Service Tax 12.36% 12.36

Less : Service Tax Abatement (60%) 07.42

Less : Service Tax Liability of Service recipient 2.47%

02.47

Liability of Service provider 2.47% 02.47 02.47

Total Invoice Amount 102.47

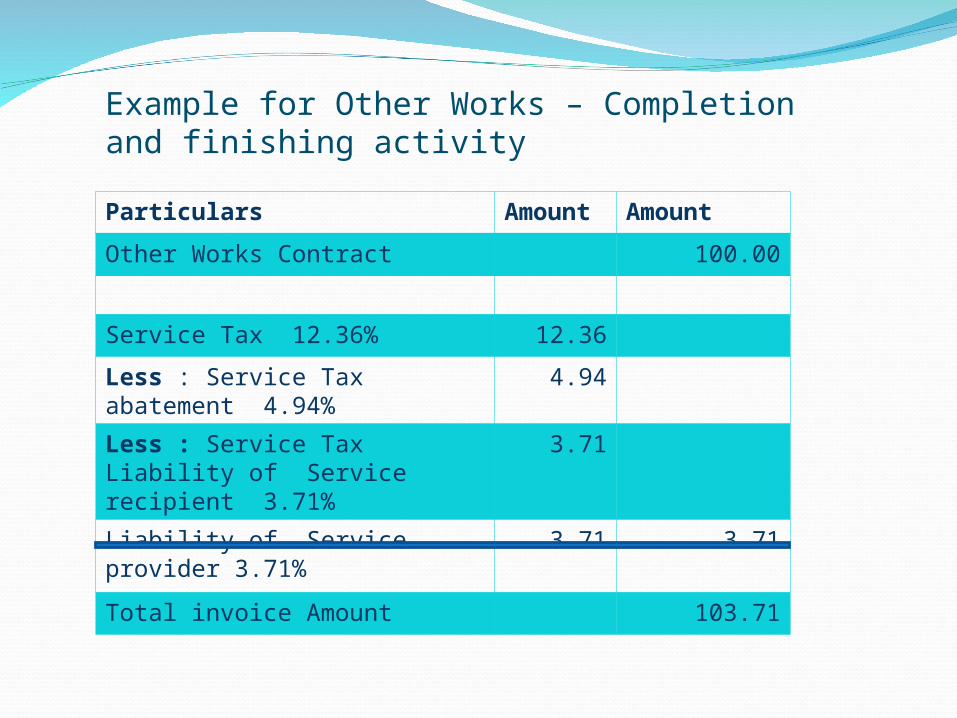

Example for Other Works – Completion and finishing activity

Particulars Amount Amount

Other Works Contract 100.00

Service Tax 12.36% 12.36

Less : Service Tax abatement 4.94% 4.94

Less : Service Tax Liability of Service recipient 3.71%

3.71

Liability of Service provider 3.71% 3.71 3.71

Total invoice Amount 103.71

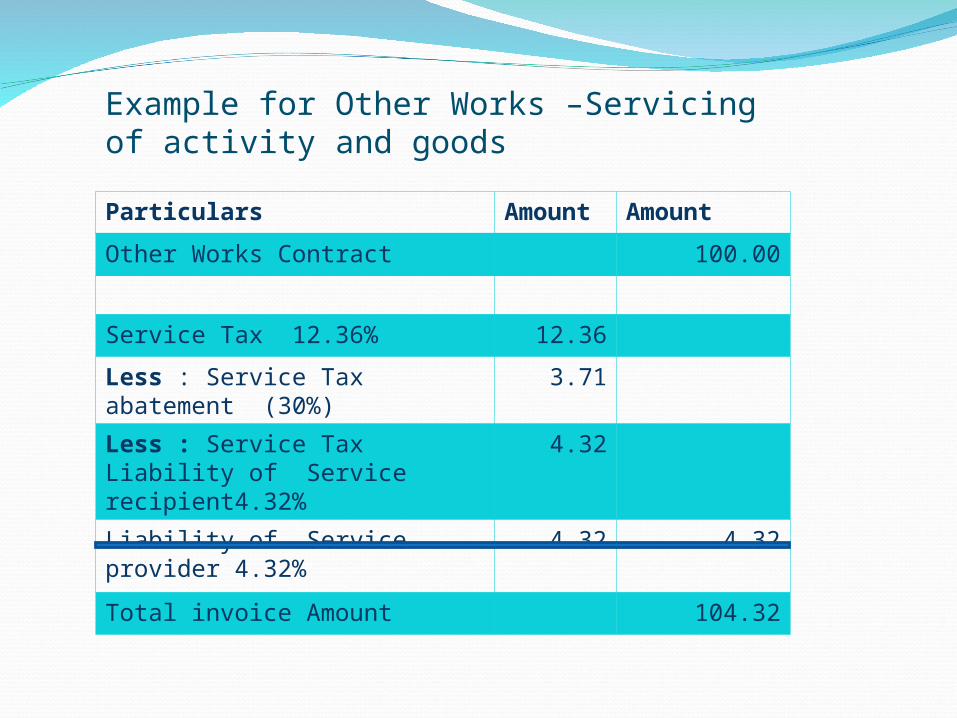

Example for Other Works –Servicing of activity and goods

Particulars Amount Amount

Other Works Contract 100.00

Service Tax 12.36% 12.36

Less : Service Tax abatement (30%) 3.71

Less : Service Tax Liability of Service recipient4.32%

4.32

Liability of Service provider 4.32% 4.32 4.32

Total invoice Amount 104.32

Point of Taxation in case of Reverse charge Mechanism

The point of taxation in case of Reverse charge mechanism shall be governed by Rule 7 of Point of Taxation Rules, 2011.

As per Rule 7 of POT rules the point of taxation in case of reverse charge mechanism shall be the date on which payment is made by the service receiver to the service provider. Therefore liability to pay service charge is the month in which payment to service provider is made.

However if payment to the service provider is not made within six months from the date of invoice than point of taxation shall be determined as per general rules of Point of Taxation rules, 2011.