october 2016 geneva, switzerland · october 2016 geneva, switzerland siem reap, cambodia overview...

TRANSCRIPT

LFA Finance TrainingPUDR GuidelinesKey Finance sections

October 2016Geneva, SwitzerlandSiem Reap, Cambodia

Overview of the presentation - Agenda

1

Introduction & Overview

Progress Update and Disbursement Request –Finance Sections

Questions & Answers /Conclusion

Implementer Financial Reporting is key for our activity

2

A minimum set of reliable financial information regarding the implementation of grants is important for the Global Fund to:

• Demonstrate the efficiency of investments

• Enhance transparency and accurate reporting on the use of funds to stakeholders

• Link financial information to programmatic performance

• Enhance the ability to make informed decisions

• Track absorption and the associated bottlenecks

• Analyze the financial risks across the portfolio

Financial Reporting in 5 main reports

3

STANDARD QUARTERLY REPORTING Cash Balance Report – now on semi-annual basis Quarterly Expenditures Report – now on semi-annual

basis

STANDARD ANNUAL REPORTING Progress Update/Disbursement Request (Including Annual

Financial Report) External Audit Report Tax Report

4

MAYMAY JUNJUN JULJUL AUGAUG SEPSEP OCTOCT NOVNOV DECDECJANJAN FEBFEB MARMAR APRAPR

High Impact

Core

Cash Bal.

PU/DR*

Audit

Audit

Cash Bal.

Semi-annual Exp.

Cash Bal.

Tax

Tax

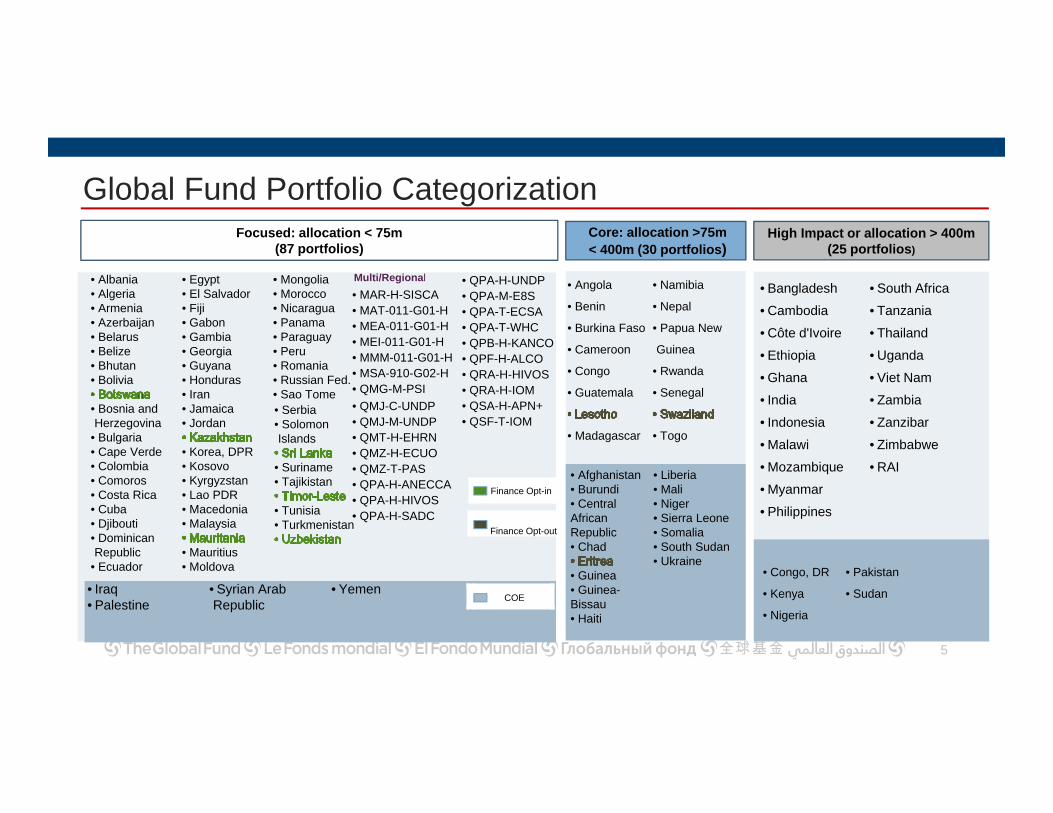

Financial Reporting Timelines based on country classification

Cash Balance Reporting

Semi-annual expenditure Reporting (included in PU/DR also)

PU / DR

Audit

TaxTax

PU/DR* Indicative for grants with a reporting cycle of January to December. Other cycles report PUDR based on the relevant cycle.

Cash Bal.

Cash Bal.

Cash Bal.

Cash Bal.

Cash Bal.

AuditPU/DR*

PU/DR*

Focused

High Impact or allocation > 400m (25 portfolios)

Focused: allocation < 75m (87 portfolios)

Core: allocation >75m < 400m (30 portfolios)

5

Global Fund Portfolio Categorization

• Serbia• Solomon Islands

• Suriname• Tajikistan

• Tunisia• Turkmenistan

• Angola

• Benin

• Burkina Faso

• Cameroon

• Congo

• Guatemala

• Madagascar

• Namibia

• Nepal

• Papua New

Guinea

• Rwanda

• Senegal

• Togo

• Bangladesh

• Cambodia

• Côte d'Ivoire

• Ethiopia

• Ghana

• India

• Indonesia

• Malawi

• Mozambique

• Myanmar

• Philippines

• South Africa

• Tanzania

• Thailand

• Uganda

• Viet Nam

• Zambia

• Zanzibar

• Zimbabwe

• RAI

• Albania• Algeria• Armenia• Azerbaijan• Belarus• Belize• Bhutan• Bolivia

• Bosnia and Herzegovina

• Bulgaria• Cape Verde• Colombia• Comoros• Costa Rica• Cuba• Djibouti• Dominican Republic

• Ecuador

• Egypt• El Salvador• Fiji• Gabon• Gambia• Georgia• Guyana• Honduras• Iran• Jamaica• Jordan

• Korea, DPR• Kosovo• Kyrgyzstan• Lao PDR• Macedonia• Malaysia

• Mauritius• Moldova

• Mongolia• Morocco• Nicaragua• Panama• Paraguay• Peru• Romania• Russian Fed.• Sao Tome

• QMJ-C-UNDP• QMJ-M-UNDP• QMT-H-EHRN• QMZ-H-ECUO• QMZ-T-PAS• QPA-H-ANECCA• QPA-H-HIVOS• QPA-H-SADC

Multi/Regional

• Iraq• Palestine

• Syrian Arab Republic

• Yemen• Congo, DR

• Kenya

• Nigeria

• Pakistan

• Sudan

• Afghanistan• Burundi• Central African Republic• Chad

• Guinea• Guinea-Bissau• Haiti

• Liberia• Mali• Niger• Sierra Leone• Somalia• South Sudan• Ukraine

COE

• MAR-H-SISCA• MAT-011-G01-H• MEA-011-G01-H• MEI-011-G01-H• MMM-011-G01-H• MSA-910-G02-H• QMG-M-PSI

Finance Opt-out

Finance Opt-in

• QPA-H-UNDP• QPA-M-E8S• QPA-T-ECSA• QPA-T-WHC• QPB-H-KANCO• QPF-H-ALCO• QRA-H-HIVOS• QRA-H-IOM• QSA-H-APN+• QSF-T-IOM

Overview of the presentation - Agenda

6

Introduction & Overview

Progress Update and Disbursement Request –Finance Sections

Questions and Answers / Conclusion

Disclaimer

7

This presentation and training do not replace PU/DR guidelines. All stakeholders should familiarize themselves with the guidelines.

The presentation is to:

• Answer some specific LFA questions

• Complement available materials

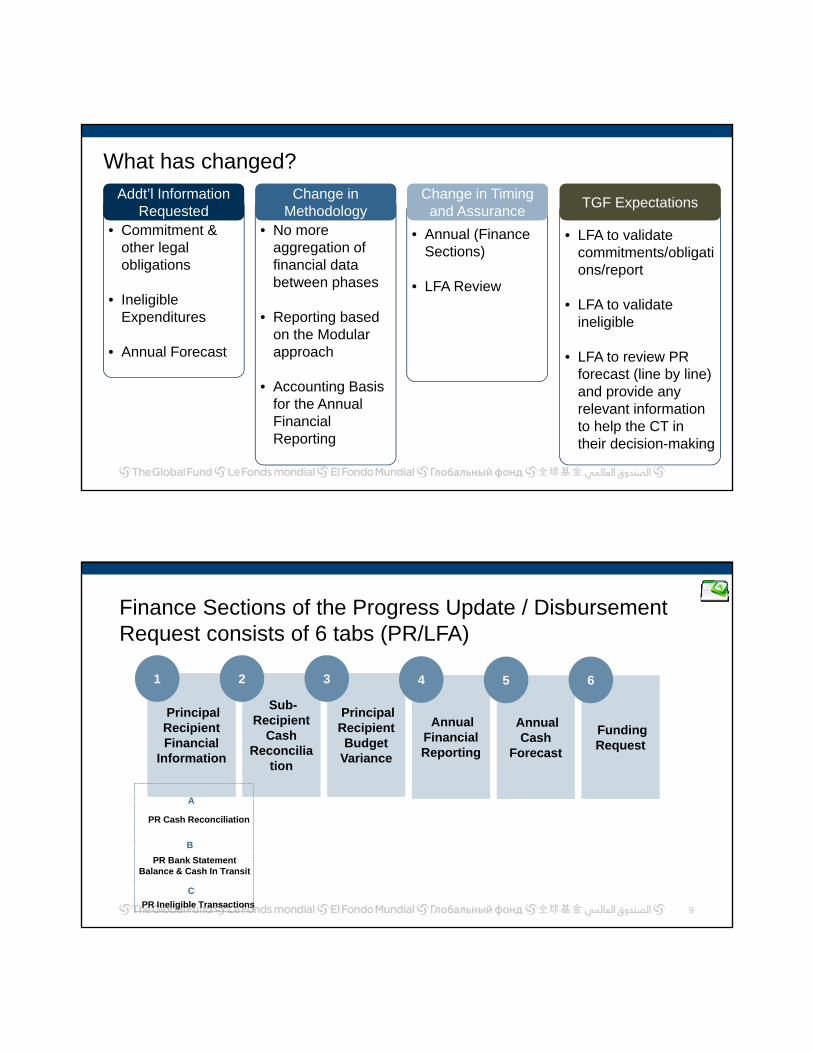

What has changed?

8

• Commitment & other legal obligations

• Ineligible Expenditures

• Annual Forecast

Addt’l Information Requested

Addt’l Information Requested

• No more aggregation of financial data between phases

• Reporting based on the Modular approach

• Accounting Basis for the Annual Financial Reporting

Change in Methodology

Change in Methodology

• Annual (Finance Sections)

• LFA Review

Change in Timing and Assurance

Change in Timing and Assurance

• LFA to validate commitments/obligations/report

• LFA to validate ineligible

• LFA to review PR forecast (line by line) and provide any relevant information to help the CT in their decision-making

TGF ExpectationsTGF Expectations

Finance Sections of the Progress Update / Disbursement Request consists of 6 tabs (PR/LFA)

9

Principal Recipient Financial

Information

Principal Recipient Financial

Information

1

Sub-Recipient

Cash Reconcilia

tion

Sub-Recipient

Cash Reconcilia

tion

2

Principal Recipient Budget

Variance

Principal Recipient Budget

Variance

3

Annual Financial Reporting

Annual Financial Reporting

4

Annual Cash

Forecast

Annual Cash

Forecast

5

Funding RequestFunding Request

6

PR Bank Statement Balance & Cash In Transit

B

PR Ineligible Transactions

C

PR Cash Reconciliation

A

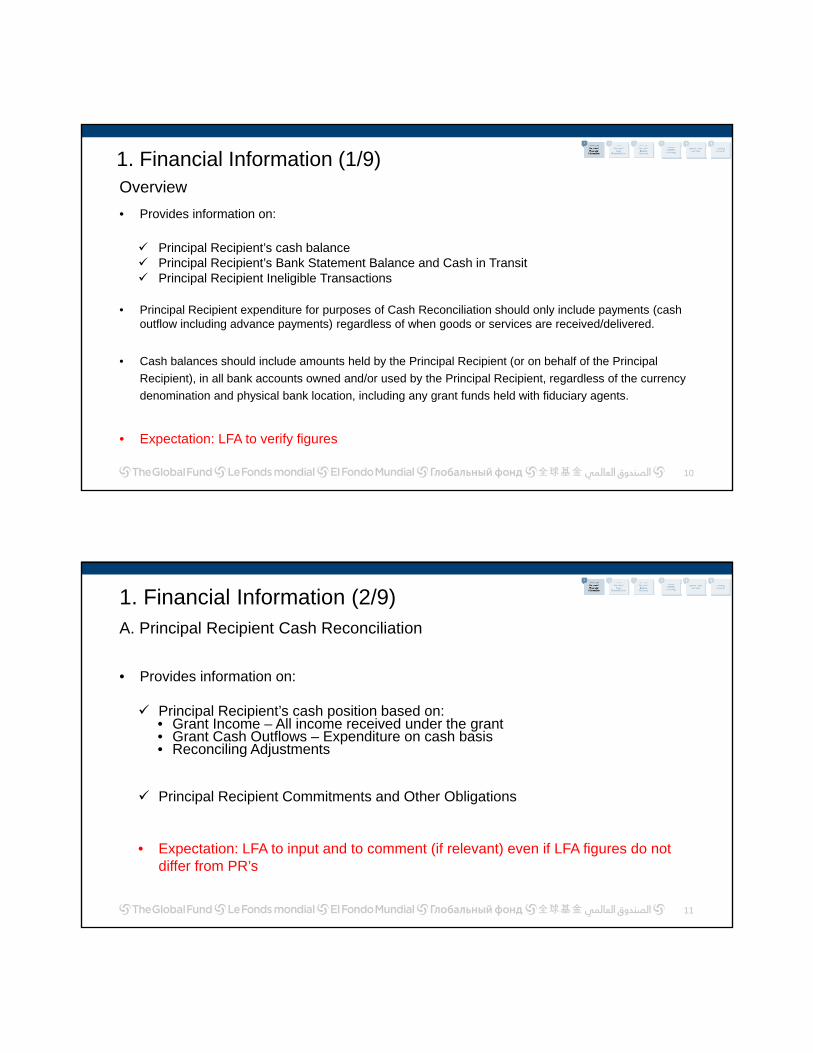

Overview

• Provides information on:

Principal Recipient’s cash balance Principal Recipient’s Bank Statement Balance and Cash in Transit Principal Recipient Ineligible Transactions

• Principal Recipient expenditure for purposes of Cash Reconciliation should only include payments (cash outflow including advance payments) regardless of when goods or services are received/delivered.

• Cash balances should include amounts held by the Principal Recipient (or on behalf of the Principal

Recipient), in all bank accounts owned and/or used by the Principal Recipient, regardless of the currency

denomination and physical bank location, including any grant funds held with fiduciary agents.

• Expectation: LFA to verify figures

10

1. Financial Information (1/9)

1. Financial Information (2/9)

• Provides information on:

Principal Recipient’s cash position based on:• Grant Income – All income received under the grant• Grant Cash Outflows – Expenditure on cash basis• Reconciling Adjustments

Principal Recipient Commitments and Other Obligations

• Expectation: LFA to input and to comment (if relevant) even if LFA figures do not differ from PR’s

11

A. Principal Recipient Cash Reconciliation

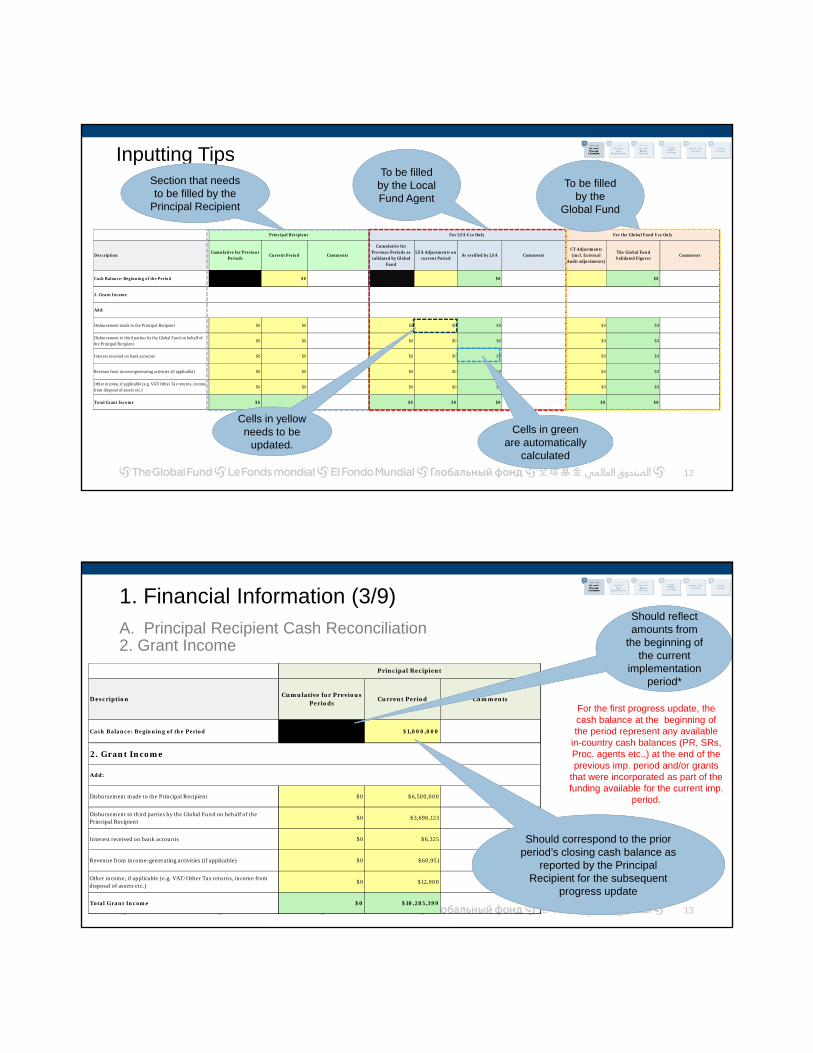

Inputting Tips

12

DescriptionCumulative for Previous

PeriodsCurrent Period Comments

Cumulative for Previous Periods as validated by Global

Fund

LFA Adjustments on current Period

As verified by LFA CommentsCT Adjustments (incl. External

Audit adjustments)

The Global Fund Validated Figures

Comments

Cash Balance: Beginning of the Period $0 $0 $0 $0

2. Grant Income

Add:

Disbursement made to the Principal Recipient $0 $0 $0 $0 $0 $0 $0

Disbursement to third parties by the Global Fund on behalf of the Principal Recipient

$0 $0 $0 $0 $0 $0 $0

Interest received on bank accounts $0 $0 $0 $0 $0 $0 $0

Revenue from income-generating activities (if applicable) $0 $0 $0 $0 $0 $0 $0

Other income, if applicable (e.g. VAT/Other Tax returns, income from disposal of assets etc.)

$0 $0 $0 $0 $0 $0 $0

Total Grant Income $0 $0 $0 $0 $0 $0 $0

Principal Recipient For LFA Use Only For the Global Fund Use Only

Section that needs to be filled by the

Principal Recipient

To be filled by the Local Fund Agent

To be filled by the

Global Fund

Cells in yellow needs to be

updated.

Cells in green are automatically

calculated

1. Financial Information (3/9)

13

A. Principal Recipient Cash Reconciliation2. Grant Income

DescriptionCumulative for Previous

PeriodsCurrent Period Comments

Cash Balance: Beginning of the Period $0 $1,000,000

2. Grant Income

Add:

Disbursement made to the Principal Recipient $0 $6,500,000

Disbursement to third parties by the Global Fund on behalf of the Principal Recipient

$0 $3,698,123

Interest received on bank accounts $0 $6,325

Revenue from income-generating activities (if applicable) $0 $68,951

Other income, if applicable (e.g. VAT/Other Tax returns, income from disposal of assets etc.)

$0 $12,000

Total Grant Income $0 $10,285,399

Principal Recipient

Should reflect Should reflect amounts from

the beginning of the current

implementation period*

Should correspond to the prior period’s closing cash balance as

reported by the Principal Recipient for the subsequent

progress update

For the first progress update, the cash balance at the beginning of the period represent any available

in-country cash balances (PR, SRs, Proc. agents etc..) at the end of the previous imp. period and/or grants

that were incorporated as part of the funding available for the current imp.

period.

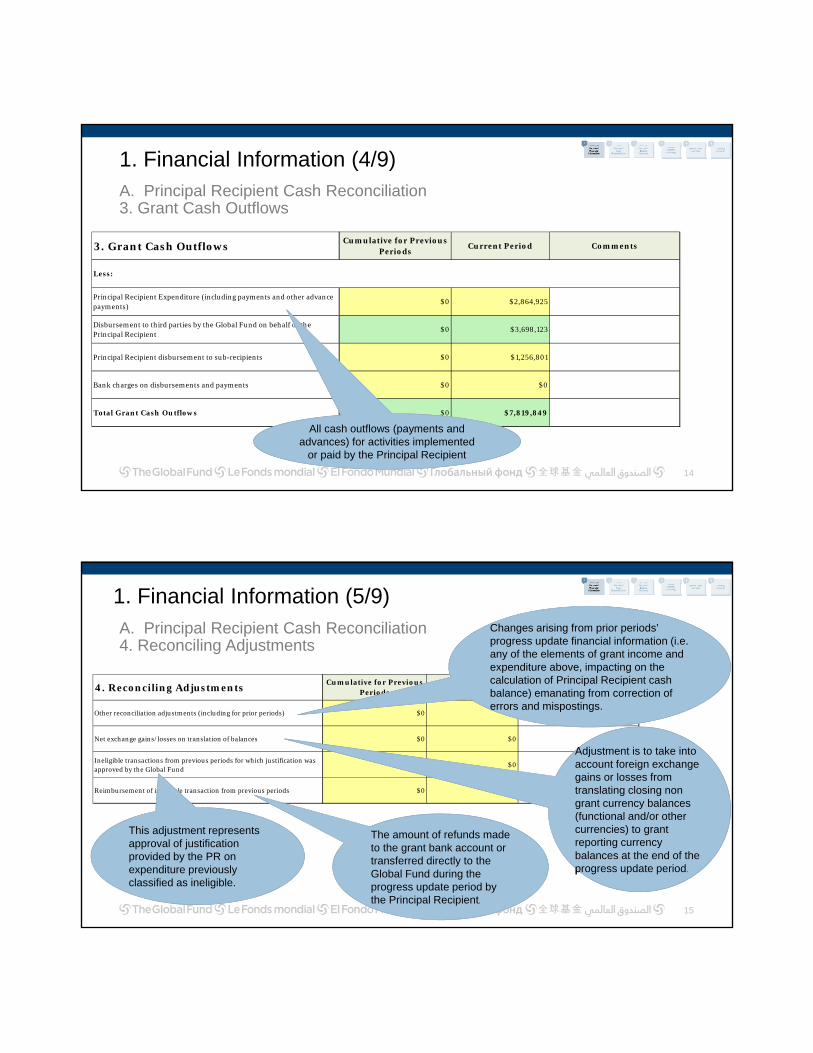

1. Financial Information (4/9)

14

A. Principal Recipient Cash Reconciliation3. Grant Cash Outflows

3. Grant Cash OutflowsCumulative for Previous

PeriodsCurrent Period Comments

Less:

Principal Recipient Expenditure (including payments and other advance payments)

$0 $2,864,925

Disbursement to third parties by the Global Fund on behalf of the Principal Recipient

$0 $3,698,123

Principal Recipient disbursement to sub-recipients $0 $1,256,801

Bank charges on disbursements and payments $0 $0

Total Grant Cash Outflows $0 $7,819,849

All cash outflows (payments and advances) for activities implemented

or paid by the Principal Recipient

1. Financial Information (5/9)

15

A. Principal Recipient Cash Reconciliation4. Reconciling Adjustments

4. Reconciling AdjustmentsCumulative for Previous

PeriodsCurrent Period Comments

Other reconciliation adjustments (including for prior periods) $0 $0

Net exchange gains/losses on translation of balances $0 $0

Ineligible transactions from previous periods for which justification was approved by the Global Fund

$0 $0

Reimbursement of ineligible transaction from previous periods $0 $0

Changes

errors and mispostings.

Changes arising from prior periods’ progress update financial information (i.e. any of the elements of grant income and expenditure above, impacting on the calculation of Principal Recipient cash balance) emanating from correction of errors and mispostings.

Adjustment is to take into

progress update period

Adjustment is to take into account foreign exchange gains or losses from translating closing non grant currency balances (functional and/or other currencies) to grant reporting currency balances at the end of the progress update period.

This adjustment represents approval of justification provided by the PR on expenditure previously classified as ineligible.

The amount of refunds made to the grant bank account or transferred directly to the Global Fund during the progress update period by the Principal Recipient.

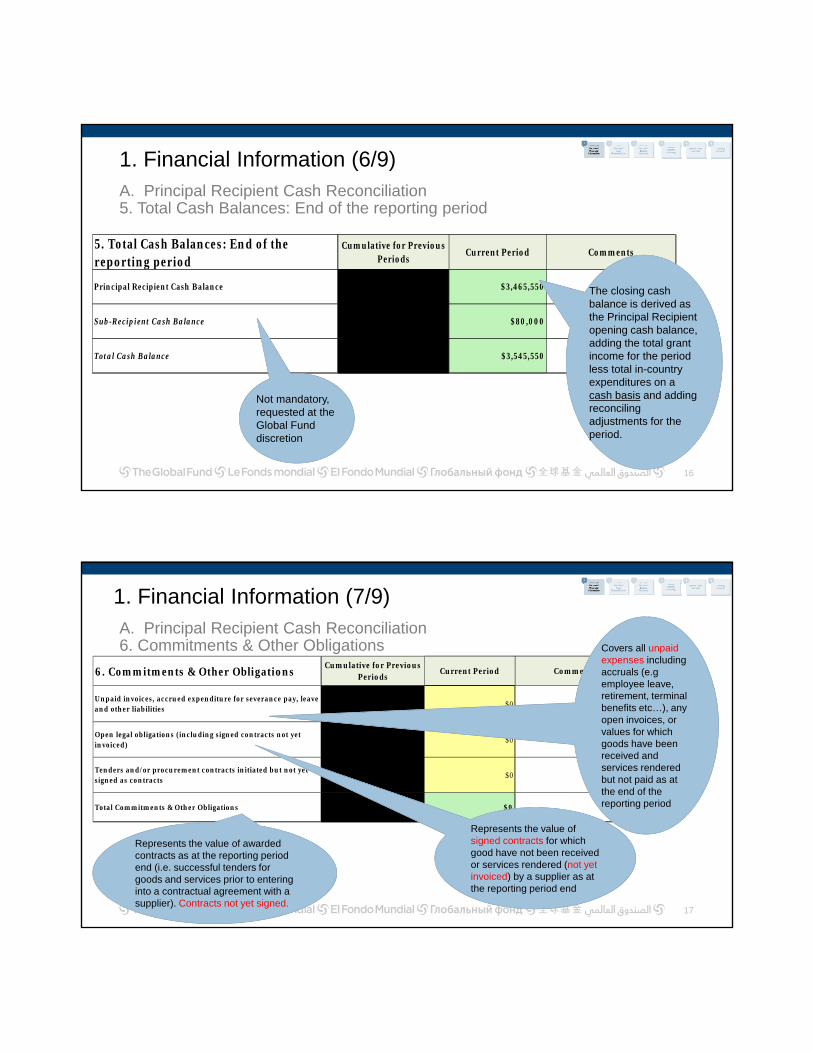

1. Financial Information (6/9)

16

A. Principal Recipient Cash Reconciliation5. Total Cash Balances: End of the reporting period

5. Total Cash Balances: End of the reporting period

Cumulative for Previous Periods

Current Period Comments

Principal Recipient Cash Balance $0 $3,465,550

Sub-Recipient Cash Balance $0 $80,000

Total Cash Balance $0 $3,545,550

The closing cash

period

The closing cash balance is derived as the Principal Recipient opening cash balance, adding the total grant income for the period less total in-country expenditures on a cash basis and adding reconciling adjustments for the period.

Not mandatory, requested at the Global Fund discretion

1. Financial Information (7/9)

17

A. Principal Recipient Cash Reconciliation6. Commitments & Other Obligations

6. Commitments & Other ObligationsCumulative for Previous

PeriodsCurrent Period Comments

Unpaid invoices, accrued expenditure for severance pay, leave and other liabilities

$0 $0

Open legal obligations (including signed contracts not yet invoiced)

$0 $0

Tenders and/or procurement contracts initiated but not yet signed as contracts

$0 $0

Total Commitments & Other Obligations $0 $0

Covers all unpaid expenses including accruals (e.g employee leave, retirement, terminal benefits etc…), any open invoices, or values for which goods have been received and services rendered but not paid as at the end of the reporting period

Represents the value of signed contracts for which good have not been received or services rendered (not yet invoiced) by a supplier as at the reporting period end

Represents the value of awarded contracts as at the reporting period end (i.e. successful tenders for goods and services prior to entering into a contractual agreement with a supplier). Contracts not yet signed.

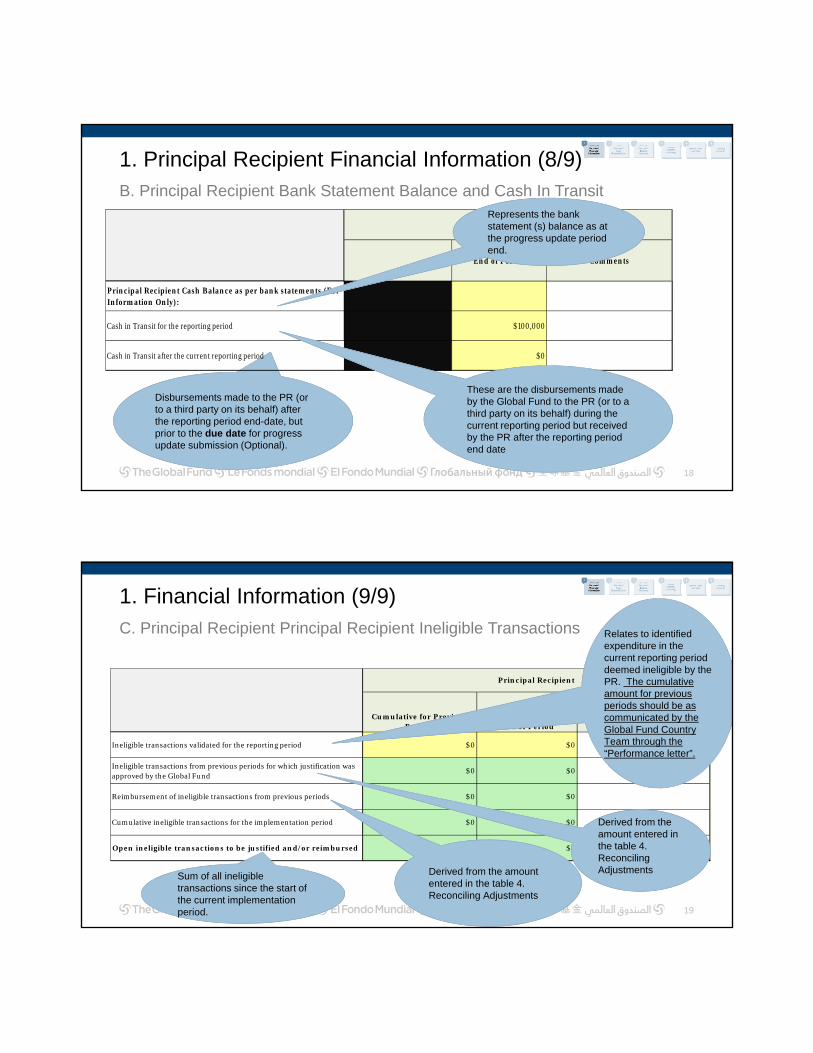

1. Principal Recipient Financial Information (8/9)

18

B. Principal Recipient Bank Statement Balance and Cash In Transit

Disbursements made to the PR (or to a third party on its behalf) after the reporting period end-date, but prior to the due date for progress update submission (Optional).

End of Period Comments

Principal Recipient Cash Balance as per bank statements (For Information Only):

Cash in Transit for the reporting period $100,000

Cash in Transit after the current reporting period $0

Principal RecipientRepresents the bank statement (s) balance as at the progress update period end.

These are the disbursements made by the Global Fund to the PR (or to a third party on its behalf) during the current reporting period but received by the PR after the reporting period end date

1. Financial Information (9/9)

19

C. Principal Recipient Principal Recipient Ineligible Transactions

Cumulative for Previous Periods End of Period Comments

Ineligible transactions validated for the reporting period $0 $0

Ineligible transactions from previous periods for which justification was approved by the Global Fund

$0 $0

Reimbursement of ineligible transactions from previous periods $0 $0

Cumulative ineligible transactions for the implementation period $0 $0

Open ineligible transactions to be justified and/or reimbursed $0 $0

Principal Recipient

Relates to identified expenditure in the current reporting period deemed ineligible by the PR. The cumulative amount for previous periods should be as communicated by the Global Fund Country Team through the “Performance letter”.

Derived from the Derived from the amount entered in the table 4. Reconciling AdjustmentsDerived from the amount

entered in the table 4. Reconciling Adjustments

Sum

period.

Sum of all ineligible transactions since the start of the current implementation period.

Financial Information Questions for Discussion

Refer to handout – each table is to answer one question from the Financial Information Questions (except the last one)

3 min

Nominate one person to present your table’s answers

2 min

Discussion of Final Question 5 min

14

Overview

• The Sub-Recipient cash reconciliation statement provides the reconciliation of funds provided to Sub-Recipients at a given progress update period end date

• Sub-Recipient open advances are defined as disbursements made to Sub-Recipients and other Sub-Recipient income less Sub-Recipient expenditures validated and recorded by the Principal Recipient in its records as fully liquidated amounts (i.e. recognized officially as Sub-Recipient expenditure by the Principal Recipient in its own records)

• Not mandatory but need to be provided at the request of the Global Fund.

If requested, the LFA should agree the scope of this work with the CT. A repetition of PR written data is not a review.

21

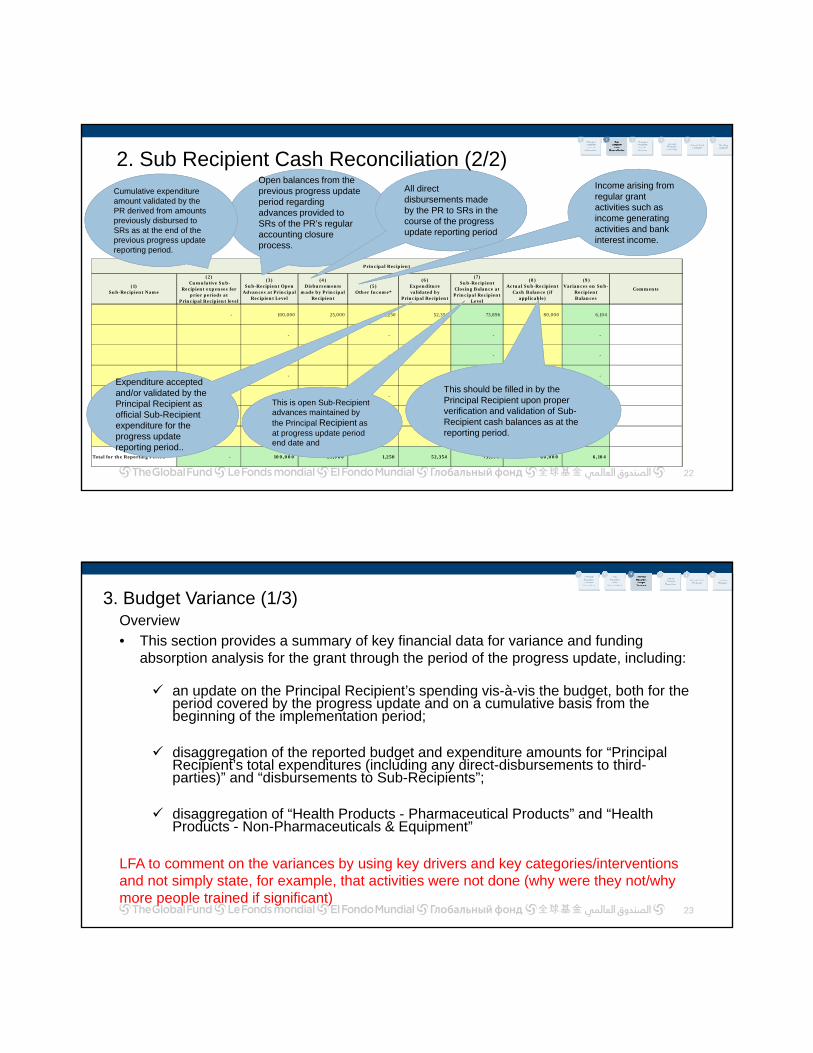

2. Sub Recipient Cash Reconciliation (1/2)

22

(1) Sub-Recipient Name

(2) Cumulative Sub-

Recipient expenses for prior periods at

Principal Recipient level

(3) Sub-Recipient Open

Advances at Principal Recipient Level

(4) Disbursements

made by Principal Recipient

(5) Other Income*

(6) Expenditure validated by

Principal Recipient

(7) Sub-Recipient

Closing Balance at Principal Recipient

Level

(8) Actual Sub-Recipient

Cash Balance (if applicable)

(9)Variances on Sub-

Recipient Balances

Comments

- 100,000 25,000 1,250 52,354 73,896 80,000 6,104

- - - -

- - - -

- - - - -

- - - -

- - - -

- - - -

Total for the Reporting Period - 100,000 25,000 1,250 52,354 73,896 80,000 6,104

Principal Recipient

Expenditure accepted

reporting

Expenditure accepted and/or validated by the Principal Recipient as official Sub-Recipient expenditure for the progress update reporting period..

Open balances from the Open balances from the previous progress update period regarding advances provided to SRs of the PR’s regular accounting closure process.

Cumulative expenditure amount validated by the PR derived from amounts previously disbursed to SRs as at the end of the previous progress update reporting period.

All direct disbursements made by the PR to SRs in the course of the progress update reporting period

Income arising from regular grant activities such as income generating activities and bank interest income.

This is open Sub-Recipient advances maintained by the Principal Recipient as at progress update period end date and

This should be filled in by the Principal Recipient upon proper verification and validation of Sub-Recipient cash balances as at the reporting period.

2. Sub Recipient Cash Reconciliation (2/2)

Overview

• This section provides a summary of key financial data for variance and funding absorption analysis for the grant through the period of the progress update, including:

an update on the Principal Recipient’s spending vis-à-vis the budget, both for the period covered by the progress update and on a cumulative basis from the beginning of the implementation period;

disaggregation of the reported budget and expenditure amounts for “Principal Recipient’s total expenditures (including any direct-disbursements to third-parties)” and “disbursements to Sub-Recipients”;

disaggregation of “Health Products - Pharmaceutical Products” and “Health Products - Non-Pharmaceuticals & Equipment”

LFA to comment on the variances by using key drivers and key categories/interventions and not simply state, for example, that activities were not done (why were they not/why more people trained if significant)

23

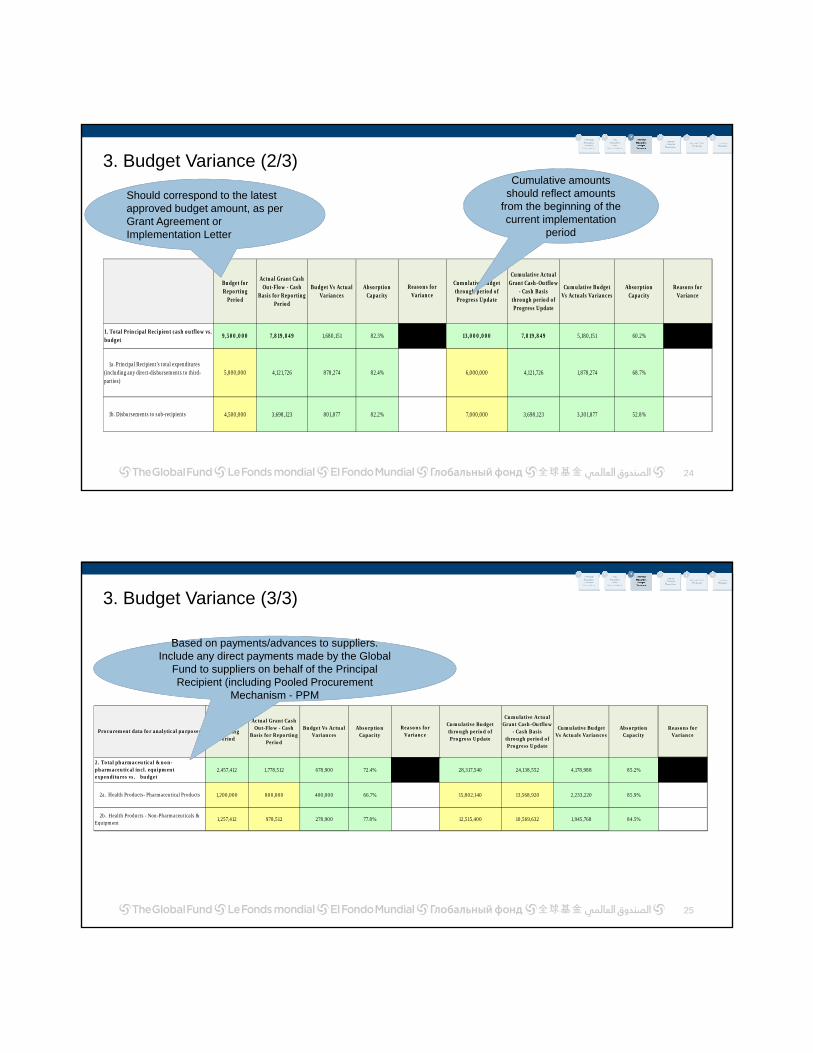

3. Budget Variance (1/3)

24

Budget for Reporting

Period

Actual Grant Cash Out-Flow - Cash

Basis for Reporting Period

Budget Vs Actual Variances

Absorption Capacity

Cumulative Budget through period of Progress Update

Cumulative Actual Grant Cash-Outflow

- Cash Basis through period of Progress Update

Cumulative Budget Vs Actuals Variances

Absorption Capacity

Reasons for Variance

9,500,000 7,819,849 1,680,151 82.3% 13,000,000 7,819,849 5,180,151 60.2%

5,000,000 4,121,726 878,274 82.4% 6,000,000 4,121,726 1,878,274 68.7%

4,500,000 3,698,123 801,877 82.2% 7,000,000 3,698,123 3,301,877 52.8%

1a. Principal Recipient's total expenditures (including any direct-disbursements to third-parties)

1b. Disbursements to sub-recipients

1. Total Principal Recipient cash outflow vs. budget

Reasons for Variance

Should correspond to the latest approved budget amount, as per Grant Agreement or Implementation Letter

Cumulative amounts Cumulative amounts should reflect amounts

from the beginning of the current implementation

period

3. Budget Variance (2/3)

25

Budget for Reporting

Period

Actual Grant Cash Out-Flow - Cash

Basis for Reporting Period

Budget Vs Actual Variances

Absorption Capacity

Cumulative Budget through period of Progress Update

Cumulative Actual Grant Cash-Outflow

- Cash Basis through period of Progress Update

Cumulative Budget Vs Actuals Variances

Absorption Capacity

Reasons for Variance

2,457,412 1,778,512 678,900 72.4% 28,317,540 24,138,552 4,178,988 85.2%

1,200,000 800,000 400,000 66.7% 15,802,140 13,568,920 2,233,220 85.9%

1,257,412 978,512 278,900 77.8% 12,515,400 10,569,632 1,945,768 84.5%

Reasons for Variance

2a. Health Products- Pharmaceutical Products

2b. Health Products - Non-Pharmaceuticals & Equipment

Procurement data for analytical purposes

2. Total pharmaceutical & non-pharmaceutical incl. equipment expenditures vs. budget

Based on payments/advances to suppliers.

PPM

Based on payments/advances to suppliers. Include any direct payments made by the Global

Fund to suppliers on behalf of the Principal Recipient (including Pooled Procurement

Mechanism - PPM

3. Budget Variance (3/3)

Budget Variance Questions for Discussion

Refer to handout – each table is to answer one question from the Budget Variance question set

3 min

Nominate one person to present your table’s answers

2 min

14

Overview

• The report covers in-country expenditures and variance analysis against the approved activity plan and funding for Principal Recipient and Sub-Recipients, reported for the current grant cycle year and cumulatively from the beginning of the implementation period.

• The financial information reported should include the approved budgets, expenditures and variance analysis by (a) cost grouping (b) modules and interventions; and (c) implementers (Principal Recipients and Sub-Recipients).

27

4. Annual Financial Report (1/8)

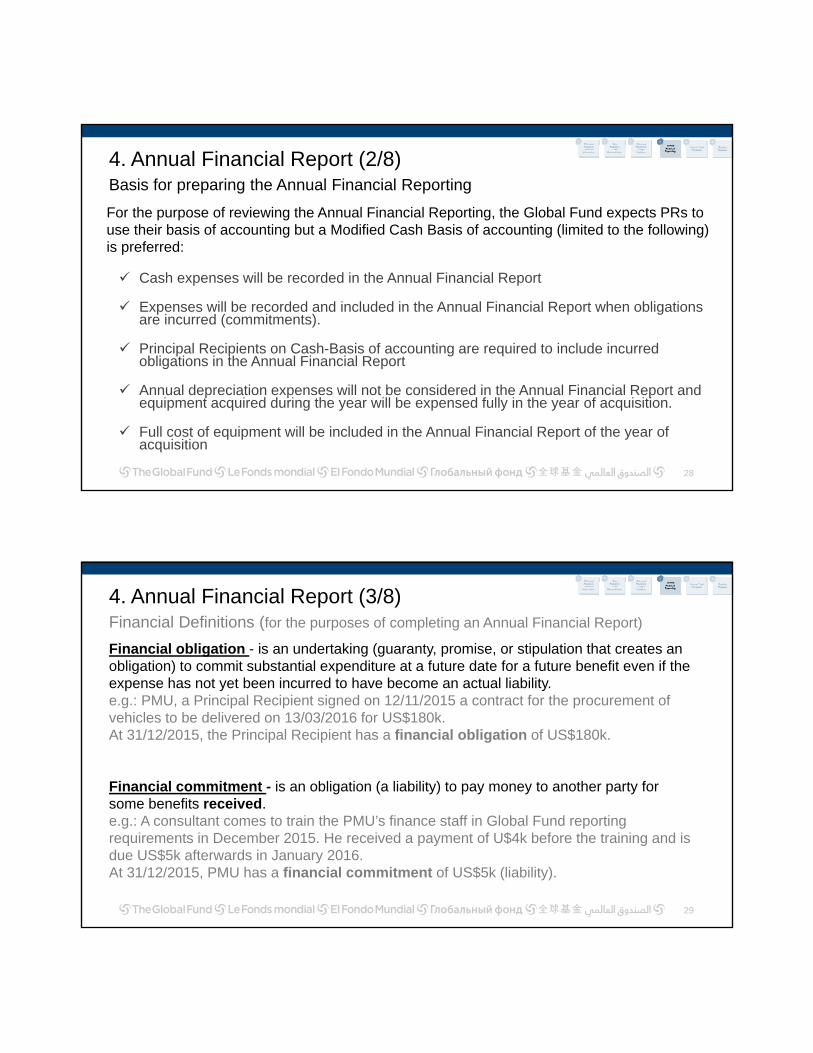

Basis for preparing the Annual Financial Reporting

For the purpose of reviewing the Annual Financial Reporting, the Global Fund expects PRs to use their basis of accounting but a Modified Cash Basis of accounting (limited to the following) is preferred:

Cash expenses will be recorded in the Annual Financial Report

Expenses will be recorded and included in the Annual Financial Report when obligations are incurred (commitments).

Principal Recipients on Cash-Basis of accounting are required to include incurred obligations in the Annual Financial Report

Annual depreciation expenses will not be considered in the Annual Financial Report and equipment acquired during the year will be expensed fully in the year of acquisition.

Full cost of equipment will be included in the Annual Financial Report of the year of acquisition

28

4. Annual Financial Report (2/8)

Financial Definitions (for the purposes of completing an Annual Financial Report)

Financial obligation - is an undertaking (guaranty, promise, or stipulation that creates an obligation) to commit substantial expenditure at a future date for a future benefit even if the expense has not yet been incurred to have become an actual liability.e.g.: PMU, a Principal Recipient signed on 12/11/2015 a contract for the procurement of vehicles to be delivered on 13/03/2016 for US$180k.At 31/12/2015, the Principal Recipient has a financial obligation of US$180k.

Financial commitment - is an obligation (a liability) to pay money to another party for some benefits received.e.g.: A consultant comes to train the PMU’s finance staff in Global Fund reporting requirements in December 2015. He received a payment of U$4k before the training and is due US$5k afterwards in January 2016.At 31/12/2015, PMU has a financial commitment of US$5k (liability).

29

4. Annual Financial Report (3/8)

Financial Definitions (for the purposes on completing an Annual Financial Report)

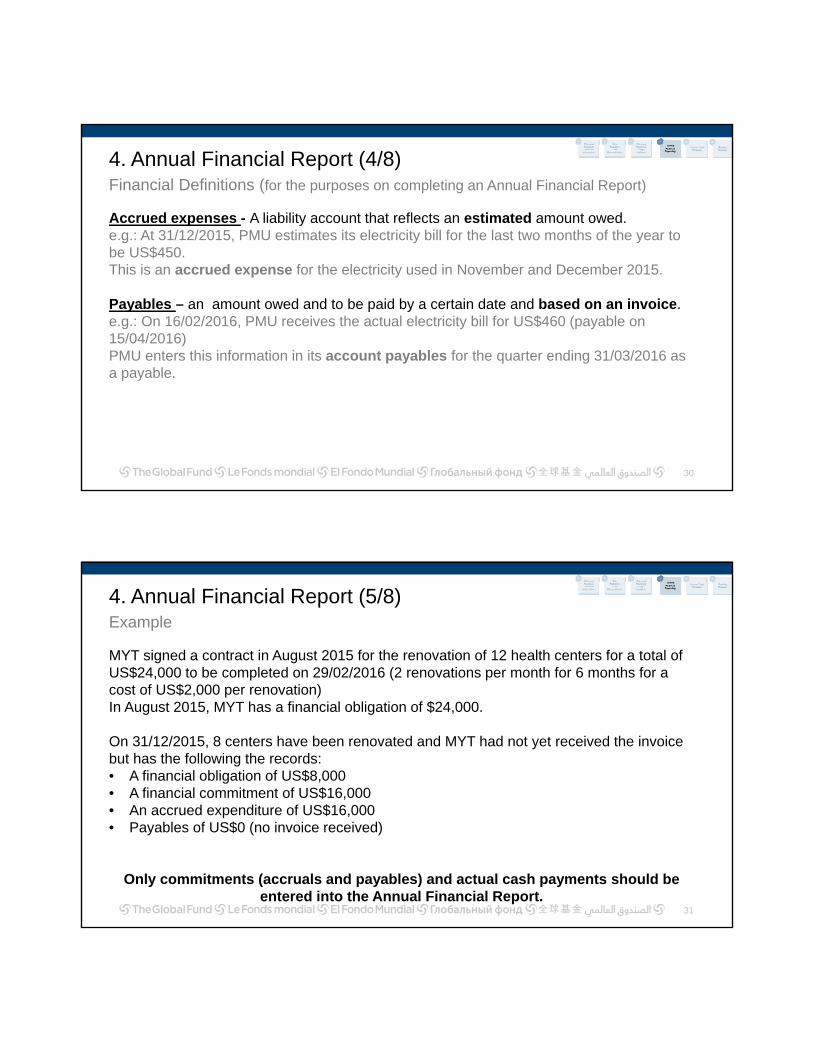

Accrued expenses - A liability account that reflects an estimated amount owed.e.g.: At 31/12/2015, PMU estimates its electricity bill for the last two months of the year to be US$450. This is an accrued expense for the electricity used in November and December 2015.

Payables – an amount owed and to be paid by a certain date and based on an invoice.e.g.: On 16/02/2016, PMU receives the actual electricity bill for US$460 (payable on 15/04/2016) PMU enters this information in its account payables for the quarter ending 31/03/2016 as a payable.

30

4. Annual Financial Report (4/8)

Example

MYT signed a contract in August 2015 for the renovation of 12 health centers for a total of US$24,000 to be completed on 29/02/2016 (2 renovations per month for 6 months for a cost of US$2,000 per renovation)In August 2015, MYT has a financial obligation of $24,000.

On 31/12/2015, 8 centers have been renovated and MYT had not yet received the invoice but has the following the records:• A financial obligation of US$8,000• A financial commitment of US$16,000• An accrued expenditure of US$16,000• Payables of US$0 (no invoice received)

Only commitments (accruals and payables) and actual cash payments should be entered into the Annual Financial Report.

31

4. Annual Financial Report (5/8)

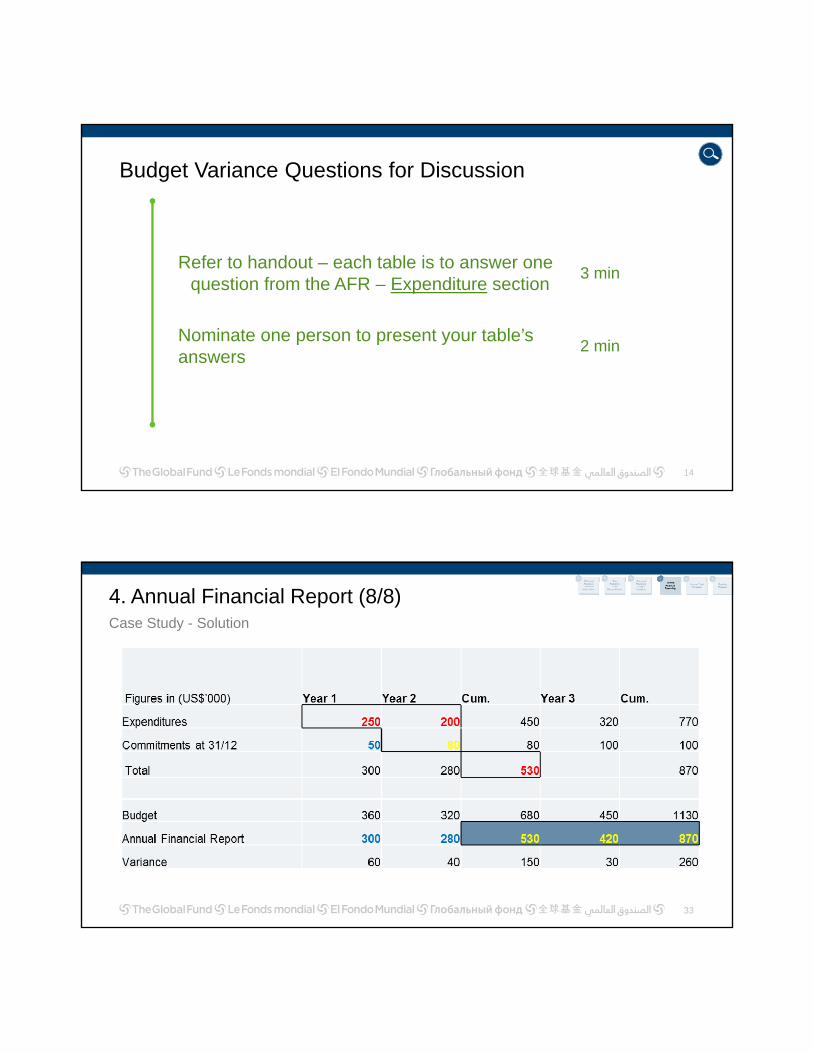

Budget Variance Questions for Discussion

Refer to handout – each table is to answer one question from the AFR – Expenditure section

3 min

Nominate one person to present your table’s answers

2 min

14

Case Study - Solution

33

4. Annual Financial Report (8/8)

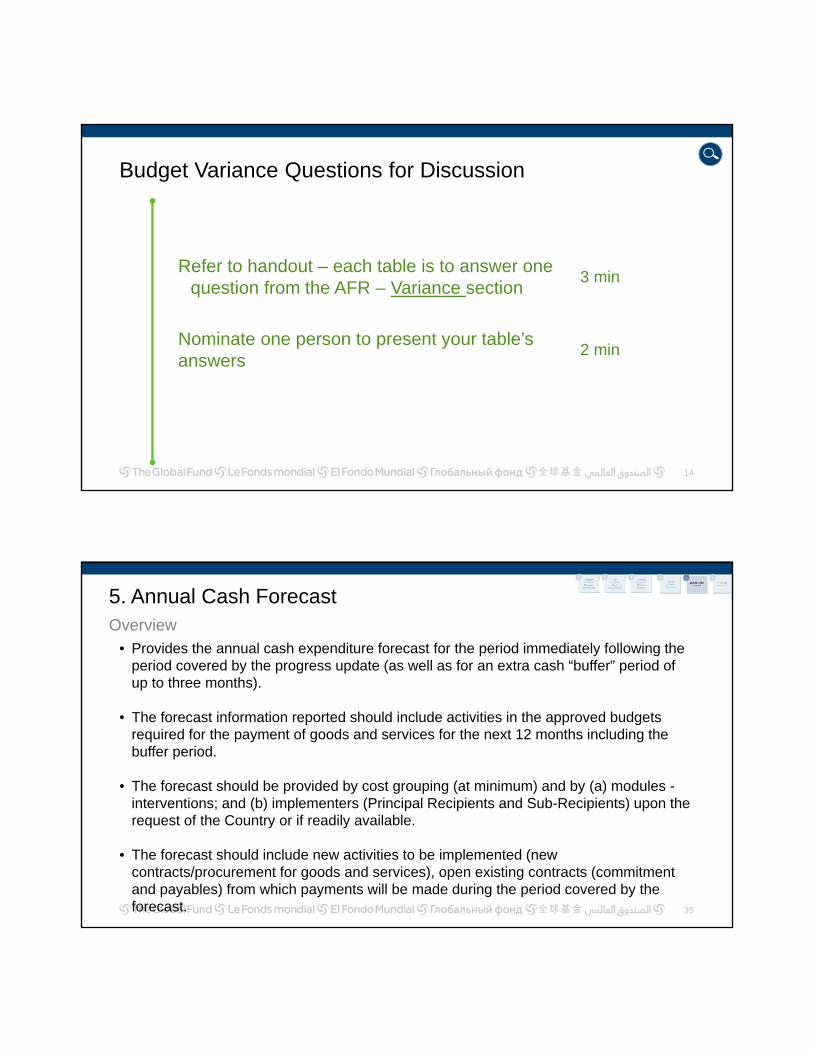

Budget Variance Questions for Discussion

Refer to handout – each table is to answer one question from the AFR – Variance section

3 min

Nominate one person to present your table’s answers

2 min

14

Overview

• Provides the annual cash expenditure forecast for the period immediately following the period covered by the progress update (as well as for an extra cash “buffer” period of up to three months).

• The forecast information reported should include activities in the approved budgets required for the payment of goods and services for the next 12 months including the buffer period.

• The forecast should be provided by cost grouping (at minimum) and by (a) modules -interventions; and (b) implementers (Principal Recipients and Sub-Recipients) upon the request of the Country or if readily available.

• The forecast should include new activities to be implemented (new contracts/procurement for goods and services), open existing contracts (commitment and payables) from which payments will be made during the period covered by the forecast. 35

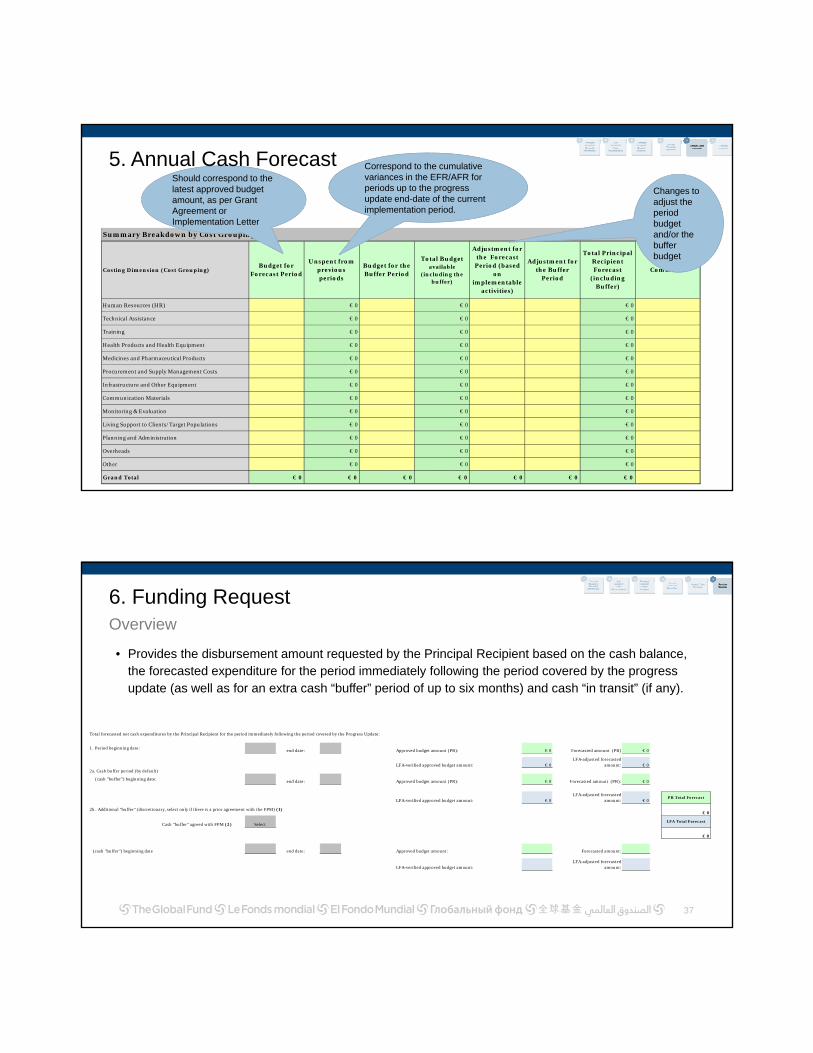

5. Annual Cash Forecast

36

Summary Breakdown by Cost Grouping

Costing Dimension (Cost Grouping)Budget for

Forecast Period

Unspent from previous periods

Budget for the Buffer Period

Total Budget available

(including the buffer)

Adjustment for the Forecast

Period (based on

implementable activities)

Adjustment for the Buffer

Period

Total Principal Recipient Forecast

(including Buffer)

Comments

Human Resources (HR) € 0 € 0 € 0

Technical Assistance € 0 € 0 € 0

Training € 0 € 0 € 0

Health Products and Health Equipment € 0 € 0 € 0

Medicines and Pharmaceutical Products € 0 € 0 € 0

Procurement and Supply Management Costs € 0 € 0 € 0

Infrastructure and Other Equipment € 0 € 0 € 0

Communication Materials € 0 € 0 € 0

Monitoring & Evaluation € 0 € 0 € 0

Living Support to Clients/Target Populations € 0 € 0 € 0

Planning and Administration € 0 € 0 € 0

Overheads € 0 € 0 € 0

Other € 0 € 0 € 0

Grand Total € 0 € 0 € 0 € 0 € 0 € 0 € 0

implementation period.

Correspond to the cumulative variances in the EFR/AFR for periods up to the progress update end-date of the current implementation period.

Should correspond to the

Implementation Letter

Should correspond to the latest approved budget amount, as per Grant Agreement or Implementation Letter

Changes to adjust the period budget and/or the buffer budget

5. Annual Cash Forecast

Overview

• Provides the disbursement amount requested by the Principal Recipient based on the cash balance, the forecasted expenditure for the period immediately following the period covered by the progress update (as well as for an extra cash “buffer” period of up to six months) and cash “in transit” (if any).

37

6. Funding Request

Total forecasted net cash expenditures by the Principal Recipient for the period immediately following the period covered by the Progress Update:

1. Period beginning date: end date: Approved budget amount (PR): € 0 Forecasted amount (PR) € 0

LFA-verified approved budget amount: € 0LFA-adjusted forecasted

amount: € 02a. Cash buffer period (by default)

(cash "buffer") beginning date: end date: Approved budget amount (PR): € 0 Forecasted amount (PR): € 0

LFA-verified approved budget amount: € 0LFA-adjusted forecasted

amount: € 0PR Total Forecast

2b. Additional "buffer" (discretionary, select only if there is a prior agreement with the FPM) (1)€ 0

Select LFA Total Forecast

€ 0

(cash "buffer") beginning date end date: Approved budget amount: Forecasted amount:

LFA-verified approved budget amount:LFA-adjusted forecasted

amount:

Cash "buffer" agreed with FPM (2)

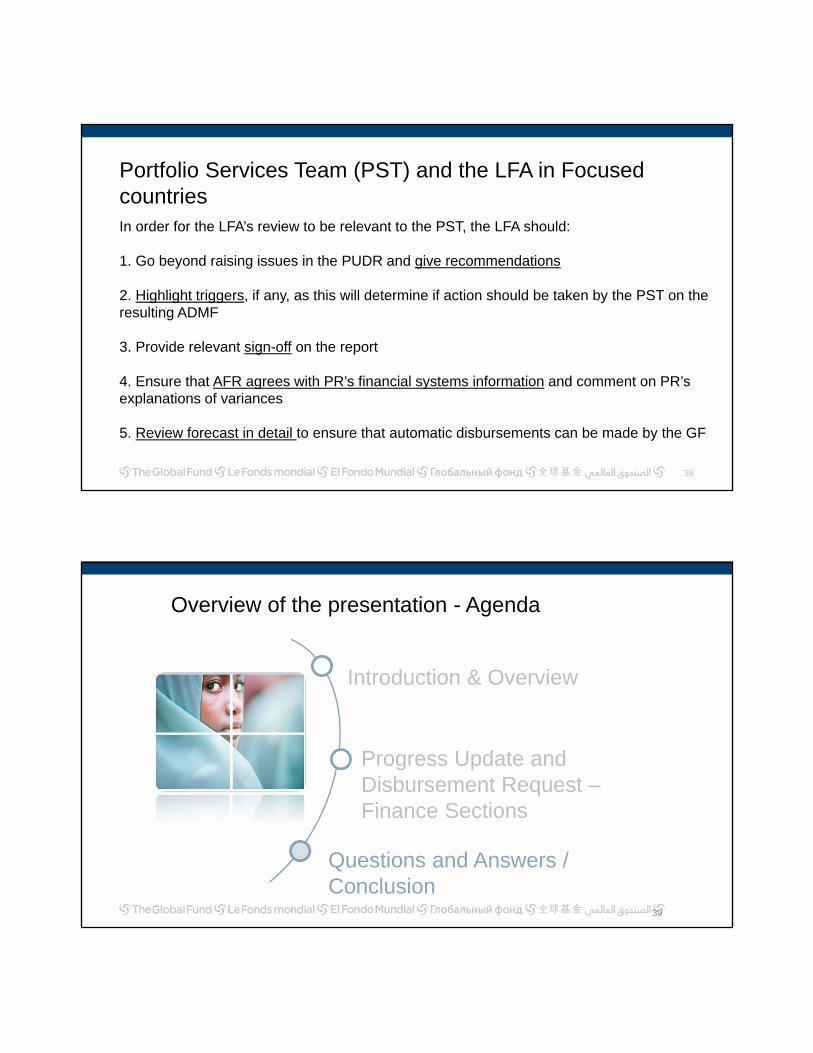

Portfolio Services Team (PST) and the LFA in FocusedcountriesIn order for the LFA’s review to be relevant to the PST, the LFA should:

1. Go beyond raising issues in the PUDR and give recommendations

2. Highlight triggers, if any, as this will determine if action should be taken by the PST on the resulting ADMF

3. Provide relevant sign-off on the report

4. Ensure that AFR agrees with PR’s financial systems information and comment on PR’s explanations of variances

5. Review forecast in detail to ensure that automatic disbursements can be made by the GF

38

Overview of the presentation - Agenda

39

Introduction & Overview

Progress Update and Disbursement Request –Finance Sections

Questions and Answers / Conclusion

Questions and Answers

40

Conclusions1. Relevant detailed comments should be included in the LFA’s sections

2. Some unadjusted figures require comments (unusual/material unadjusted figures)

3. LFA is expected to comment on PR’s explanations of variances but can add to explanations if relevant and when PR’s comment is incomplete

4. The LFA should obtain a line-by-line forecast from the PR and comment on unusual/material lines/activities

5. Information on PPM disbursements are given to the CT for the PRs, LFAs should be proactive and ensure that they are included in the mailing list (from the CT to the PRS) / applicable to all other information

6. The CTs use the detailed forecast in obtaining an annual funding decision so should be provided by both the PR and the LFA

7. Seek to obtain scope of work when SRs are to be visited during spot checks

41

Thank You

42